innovation inside 2015 (eng)

DESCRIPTION

The state of innovation in organizations in 2015 (2nd Study).TRANSCRIPT

The State of Innovation in Organizations 2015 (2nd Study)

Innovation insideOrganizations are innovating, but much work needs to be done for them to fully reap the rewards.

2 INSITUM

The State of Innovation in Organizations 2015 (2nd Study)

Innovation insideOrganizations are innovating, but much work needs to be done for them to fully reap the rewards.

4 INSITUM

> Why did we undertake this project?

Introduction The Americas as a whole have experienced rapid growth, but this growth has been uneven. There are many countries that remain unstable and isolated. As a result, some of the largest economies are now in close proximity to a variety of newcomers in emerging markets.

When we analyze the state of innovation in the Americas, we find a situation that is not too surprising — large companies with ample resources are better able to take advantage of innovation’s potential, while the majority of other companies are much more timid when experimenting with innovation initiatives. Despite that, in the last year we have seen important advances towards the adoption of innovation as a strategic tool. We believe there is much to be done for organizations to realize the value that innovation can provide in improving competitiveness, productivity and growth in the region.

This is the second year we have explored the state of innovation in organizations through a comprehensive qualitative and quantitative study. As a complement to last year, this year INSITUM has partnered

with some of the region’s top business schools and invited a greater number of companies to participate and share their experiences. We are thankful for the interest, participation and knowledge contributed by the following business schools:

EGADE Business School (Mexico)

Insper (Brazil)

PAD Escuela de Dirección, Universidad de Piura (Peru)

IE Instituto de Empresa (Spain)

We are convinced that by co-creating this type of research initiative among large corporations, academia, governmental institutions and entrepreneurs, we can make this region one of the most innovative and competitive in the world. This report provides some directional insights that we hope will be interesting and useful for your organization.

Luis Arnal, INSITUM CEO

The State of Innovation in Organizations 2015 (2nd Study) 5

6 INSITUM

Innovation has become an indispensable necessity for companies in it for the long term. The importance of innovation has been discussed for years and many companies have made great strides in this direction. But for the most part, innovation efforts exist in isolation and have been mostly informal. They often lack strategy, expertise, financial support, sufficient time and the support from senior management required to yield concrete results. Part of the problem lies in the absence of information that exists about the topic — from the ambiguous definition of the word “innovation” (which is used just as often to describe a technological initiative as a brainstorming session) to the lack of emphasis on innovating that exists in many organizations (where there is often no person or group responsible for innovation).

This year, INSITUM was recognized by Fast Company as one of the most innovative businesses, due in large part to our status as industry leaders who help the world’s largest companies perform user-centered innovation. We believe that it is our responsibility to spread the knowledge that our survey participants have generously shared — many of them top leaders in innovation, as well. Our primary intention is to inspire a greater number of leaders to foster innovation in a more efficient, effective and relevant manner.

> About this report

The State of Innovation in Organizations 2015 (2nd Study) 7

1How is innovation implemented? What models, processes and strategies do organizations use to implement it?

2What kinds of projects, resources and investments do organizations consider to be most beneficial for innovation?

3What are the catalysts and barriers for innovation within organizations?

4

What level of expertise and skill is required for organizations and their people to implement innovation initiatives?

5

What practices work well and what must be done for organizations to reap all of the benefits of innovation?

What is the state of innovation in organizations?This report explores the following five themes:

8 INSITUM

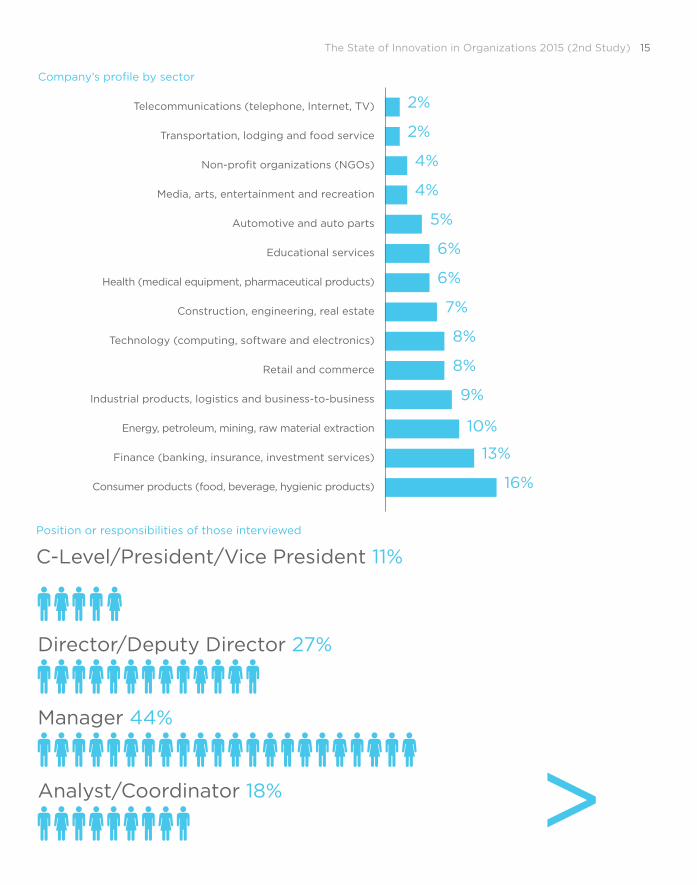

Who participated in this project?This year, we had higher participation than last year. Our partnerships with business schools in various countries helped us obtain a greater and more diverse reach, both geographically and in terms of participant profiles.

As expected, there was significant participation from consumer goods companies (food, beverages, hygienic products, etc.), finances (banking, insurance and investment services) and industrial products/business-to-business/raw materials, which are representative of the largest sectors across the participant countries.

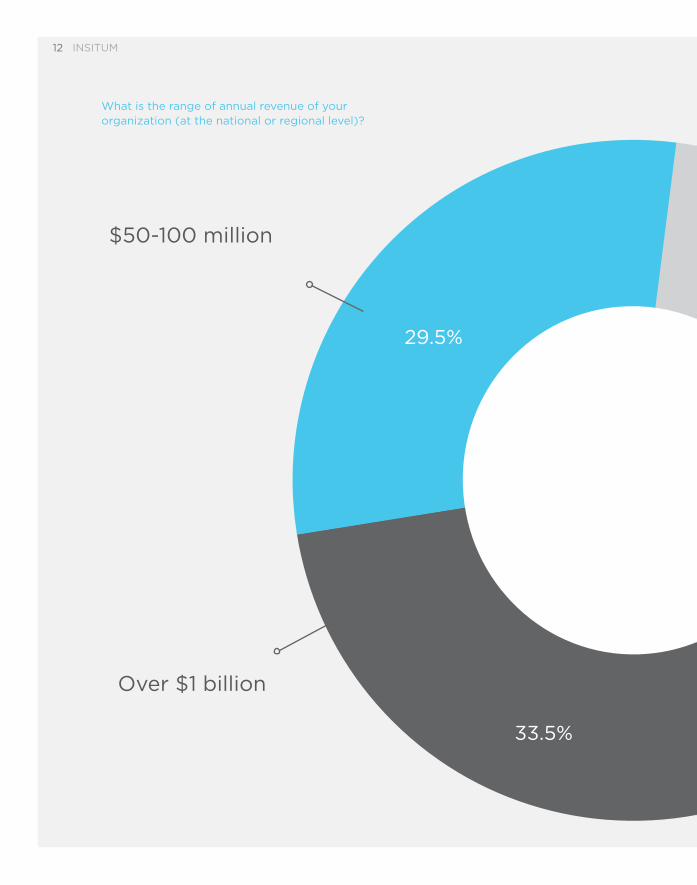

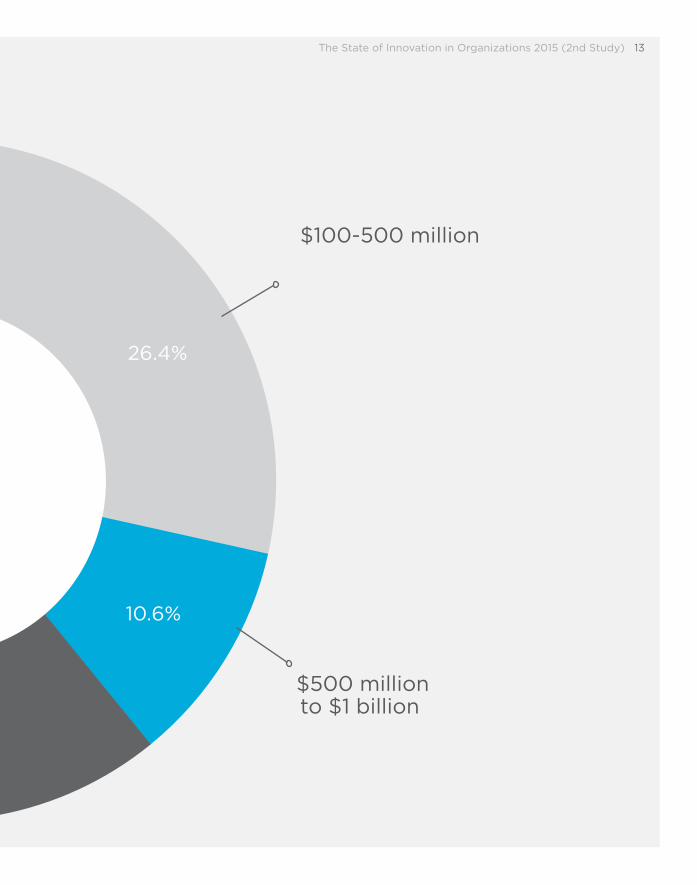

For the purposes of this analysis, we focused on including only companies with annual revenues of more than $50 million, dividing the companies into four categories:

$50 to $100 million

$100 to $500 million

$500 to $1 billion

Over $1 billion (All financial information contained in this document is represented in U.S. dollars.)

> AAM > Abbvie > Abicalçados > Anheuser-Busch InBev

> ABIT > Accenture > Acres Finance > Aeromexico > AIG > AkzoNobel > Alexion > Alicorp > Allstate > Alpina > Alsea > America Movil > American Express > Amgen > Arcelor Mittal > Argos > Asisomos > Atento > Avianca > Avon > AXA > Banamex Citibank > Banco Compartamos

> Banco de Crédito del Peru

> Banco Galicia > Banco Inter- americano de Desarrollo (BID)

> Bancolombia > Banorte Ixe > Barcel > Baxter > Bayer > BBVA > BBVA Bancomer > Bimbo > Boehringer Ingelheim

> Bombardier > Bosch > Boyden > Bradesco > Brasil Kirin > Brastemp > BRF S.A. > Buenaventura > Caixa Economica Federal

> Cámara de Comercio de Bogotá

> Campbell’s > Cargo Logistics > Carlyle > Carso > Carvajal > CBC > Celgene > Celima > Cemex > Central Media > Cerveceria Cuauhtemoc Moctezuma

> Cielo > Cigna > Cinemex > Cinepolis > Claro > Climatempo > Clorox > CocaCola > Coelho de Fonseca

> Colgate Palmolive > Compañía Universal Textil

> Compartamos Banco

> Consultoría Gouvêa de Souza

> Coppel > Corona

In total, we received responses from the following companies and more. (We include only those whose representatives shared that information.)

The State of Innovation in Organizations 2015 (2nd Study) 9

> Corporación ATSA

> Corporación M > Cosco > CPS > Credit Suisse > Daimler > Danone > Danper Trujillo > Data Business > Davivienda > Derco > Desigual > Diageo > Dwyer > EcoPetrol > Edegel > Edelnor > EduCorp > Electrolux > Elementia > Elica > Endeavor > Endress+Hauser > Enel > ER|Ronald > Estrella Roja > FabTech > Falabella > Farmacias del Ahorro

> FedEx > FEMSA > Fermet > Financiera Trinitas > Fisacero > Flextronics > Ford > Frisa > Fuerzas Armadas > Gdf Suez Energía > General Motors > Gentera > Goldcorp > Goodyear > Governo do Estado de São Paulo

> Graña y Montero > Granja Rinconada

del Sur > Grünenthal > Grupo Aje > Grupo Mexico > Grupo Nutresa > Grupo Posadas > Grupo Salinas > GSK > H&M > Heineken > Henkel > Herdez Del Fuerte > Honeywell > HSBC > IAE > IBM > ICA > IGT > Imocom > IMSS > Indra > Industrias Gutierrez

> Industrias Nettalco

> Infra > Intec > Intelbras > Interbank > Iron Wall > IT Consulting > Itaú Unibanco > ITESM > ITISA > JBS > Kimberly-Clark > Knight Piesold Consulting

> KPMG > Lala > Lamosa > Latam Airlines > Laureate > Leonisa > LG > Liberty Seguros > Liverpool > Lojao do bras > L’Oreal > LP&LP

> M.G Trading > Mabe > Magazine Luiza > Mapfre > Marcan > Mattel > McDonald’s > McKinsey > Mead Johnson Nutrition

> Medios Educativos

> Mercedes-Benz do Brasil

> Merck > Mexichem > Michelin > Midea Carrier > Millicom (Tigo) > Minera Almax > Ministerio de la producción

> Black Creek MIRA > Molinos Río de la Plata

> Mondeléz > Monsanto > Movistar > MSD > Multimedical Supplies

> Nacobre > Nadro > Natura > Negocios inmobiliarios Boston

> Nestlé > Nextel > NIC México > Nitron > Novartis > O Boticario > Odebrecht > Oficina de Normalización Previsional

> OMB > Omron > Oracle

> Otis > Oxxo > Panasonic > Pão de Açúcar > Partisan e Visagio > PepsiCo > Perfect Choice > Petróleos Mexicanos

> Pineda Covalin > PM Roca > Pontificia Universidad Católica del Peru

> Ponto Frio > Porto Seguro > Pozuelo > Previdencia > Procter & Gamble > Publicis > Ragasa > Rimac Seguros > Roche > SAB Miller > Sabritas/Quaker > Samsung > Sancela > Sanofi > Saraiva > SCA > Scotiabank > Secretaría de la Función Pública

> Seguros Bolívar > Seguros Pacífico > SERVIMEC > Shell > Sigma Alimentos > Sinérgica > SKF > Sodexo > Soriana > Sorteo TEC > Spencer Stuart > Steigen > Sura > TDM > Teamfoods > Technip > Tec-Quest

> Telefónica > Telefonica Vivo > Televisa > Ternium > Terpel > Teva Pharmaceutical

> Tigo > Total Facility Solutions

> Totvs > Tranbit > Tyco International > UANL > UCB > Unilever > Universidad EAFIT

> UPC > Vale > Vonhaucke > Wal-Mart > Walgreens > Whirlpool > World Duty Free Group

> Yobel > Zenú

10 INSITUM

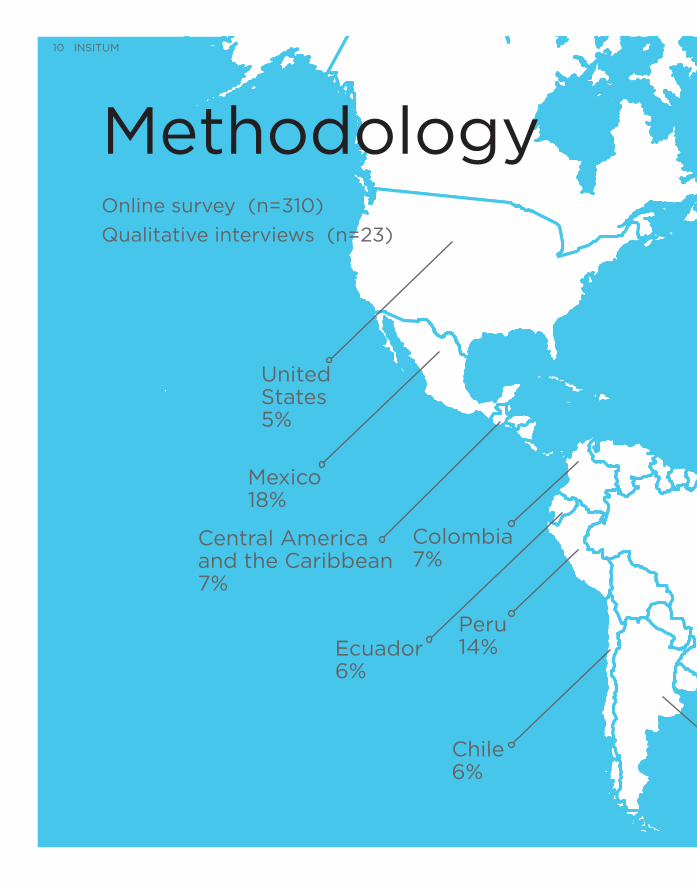

MethodologyOnline survey (n=310)

Qualitative interviews (n=23)

United States 5%

Mexico18%

Central America and the Caribbean 7%

Colombia7%

Ecuador6%

Peru14%

Chile6%

The State of Innovation in Organizations 2015 (2nd Study) 11

Brazil10%

Argentina6%

Spain5%

Other16%

12 INSITUM

What is the range of annual revenue of your organization (at the national or regional level)?

$50-100 million

Over $1 billion

29.5%

33.5%

The State of Innovation in Organizations 2015 (2nd Study) 13

$500 million to $1 billion

$100-500 million

10.6%

26.4%

14 INSITUM

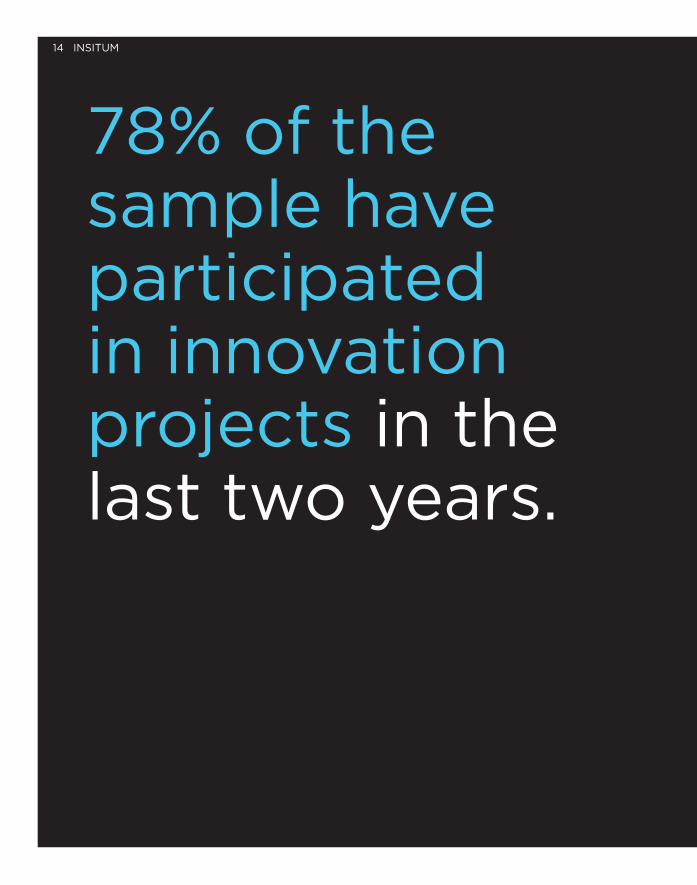

78% of the sample have participated in innovation projects in the last two years.

The State of Innovation in Organizations 2015 (2nd Study) 15

Telecommunications (telephone, Internet, TV)

Transportation, lodging and food service

Non-profit organizations (NGOs)

Media, arts, entertainment and recreation

Automotive and auto parts

Educational services

Health (medical equipment, pharmaceutical products)

Construction, engineering, real estate

Technology (computing, software and electronics)

Retail and commerce

Industrial products, logistics and business-to-business

Energy, petroleum, mining, raw material extraction

Finance (banking, insurance, investment services)

Consumer products (food, beverage, hygienic products)

2%

2%

4%

4%

5%

6%

6%

7%

8%

8%

9%

10%

13%

16%

Manager 44%

Analyst/Coordinator 18%

Director/Deputy Director 27%

C-Level/President/Vice President 11%

Company’s profile by sector

Position or responsibilities of those interviewed

16 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 17

What innovation initiatives have you carried out?

In everyday language, the term “innovation” is often used as a synonym for developing a noteworthy new product. However, innovation does not apply exclusively to products, but can be much more. It has been successfully applied as a powerful process to devise much more than products.

When we asked which types of innovation companies have invested in, we learned that our participants are very aware that there are different ways to apply innovation to their organizations.

18 INSITUM

How are organizations applying innovation?Responses to the question “What kinds of innovation has your business invested in the last 12 months?” revealed that process innovation (53%) is the most popular type of innovation. This, we believe, is because process redesign, or identifying new ways of doing things, generally requires less material investment, is performed internally and brings the most immediate benefits of any type of innovation. In the last year, this type of innovation saw the greatest increase (+8%).

In second place, we see that product innovation (47%) continues to be one of the principal types of innovation in which businesses invest. In many cases, increasing the supply of new products is the most concrete and attainable for businesses looking to grow or conquer new markets.In third place, we have innovation in services (41%), which also saw a

substantial increase in the last year (+7%). This indicates a growing awareness that services are an integral part of a business’s offering and that there are many opportunities to focus on to improve the customer experience.

In fourth place, 41% of businesses have invested in the redesign of their business models. This type of innovation also indicates a constant effort to adapt to the needs of the market and to offer (and reap) more value — perhaps motivated by competition.

It is notable that there are two types of innovation that suffered significant declines in 2014: innovation within human resources (-7%) and innovation in production (-7%). It seems that these two strategies have proved more difficult for businesses to adopt. As one vice president of human resources told us, “You don’t realize how hard it is to change processes that have existed for years and worked well”.

The State of Innovation in Organizations 2015 (2nd Study) 19

60

50

40

30

20

10

0

20% 20%

5%

Pro

ce

sse

s

Pro

du

cts

Se

rvic

es

Bu

sin

ess

mo

de

l

Ch

an

ne

ls

Hu

man

reso

urc

es

Bra

nd

ing

Pro

du

cti

on

No

ne

/ % change from 2014

53%47%

41% 41%

28%25%

What types of innovation has your organization worked on (at the national or regional level) in the last 12 months?

8%

1%

7%

2%

4%

2%

7% 7%

“We are orienting [the business] toward our clients and the most immediate way to see an effect is by changing our way of doing things ... it takes fewer resources to change a process than a product.” — Director of Experience, Banking

20 INSITUM

The type of innovation varies according to company size.When we compare the size of a company with the way it innovates, it is evident that very large companies (over $1 billion in revenue) are the ones that execute a wider range of innovation initiatives, taking first place in almost every category with the exception of innovation in production systems, where large organizations (between $500 million and $1 billion in revenue) dominate.

Across these types of innovation, there is important overlap between very large and large organizations (for example in human resources, processes and branding), which suggests that these organizations’ priorities and approach to managing innovation are highly similar.

However, medium-sized companies (between $100 and $500 million) and small companies (less than $100 million) are the lowest ranked in nearly all categories, indicating that the priorities for innovation lie above all in processes (56% and 42%, respectively) and products (45% and 40%, respectively).

What kinds of innovation has your organization worked on (at the national or regional level) in the last 12 months?

59%

32%

31%

29%

26%

26%

54%

52%

56%

42%

53%

47%

45%

40%

Business model

Human

resources Processes Products

18%

15%

$50 million to $100 million

$100 million to $500 million

$500 million to $1 billion

Over $1 billion

The State of Innovation in Organizations 2015 (2nd Study) 21

“Innovation used to be focused on products and brands, but after four years, we’re beginning to enter other areas of the business that notice this and ask for our help to resolve issues that have nothing to do with the product. For example, in quality or channels.” — VP of Products, Holding Company

As we might expect, the smallest businesses are focused on growing through new products and on increasing efficiency through process innovation, as other kinds of innovation may require greater expertise or more resources than they currently have.

37%

19%

24%

49%

39%

37%

23%

30%

29%

26%

19%

21%

29%

23%

Channels Services Branding Production

14% 12%

22 INSITUM

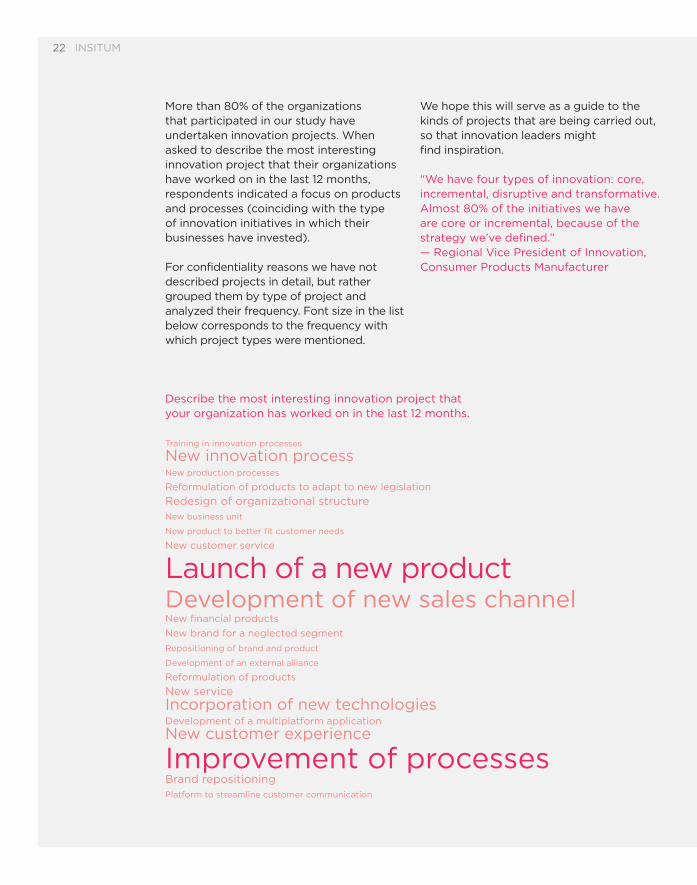

More than 80% of the organizations that participated in our study have undertaken innovation projects. When asked to describe the most interesting innovation project that their organizations have worked on in the last 12 months, respondents indicated a focus on products and processes (coinciding with the type of innovation initiatives in which their businesses have invested).

For confidentiality reasons we have not described projects in detail, but rather grouped them by type of project and analyzed their frequency. Font size in the list below corresponds to the frequency with which project types were mentioned.

We hope this will serve as a guide to the kinds of projects that are being carried out, so that innovation leaders might find inspiration.

“We have four types of innovation: core, incremental, disruptive and transformative. Almost 80% of the initiatives we have are core or incremental, because of the strategy we’ve defined.” — Regional Vice President of Innovation, Consumer Products Manufacturer

Describe the most interesting innovation project that your organization has worked on in the last 12 months.

Training in innovation processes

New innovation processNew production processes

Reformulation of products to adapt to new legislation

Redesign of organizational structureNew business unit

New product to better fit customer needs

New customer service

Launch of a new productDevelopment of new sales channelNew financial products

New brand for a neglected segment

Repositioning of brand and product

Development of an external alliance

Reformulation of products

New serviceIncorporation of new technologiesDevelopment of a multiplatform application

New customer experience

Improvement of processesBrand repositioningPlatform to streamline customer communication

The State of Innovation in Organizations 2015 (2nd Study) 23

The most interesting innovation projects remain those that are focused on products and processes.

24 INSITUM

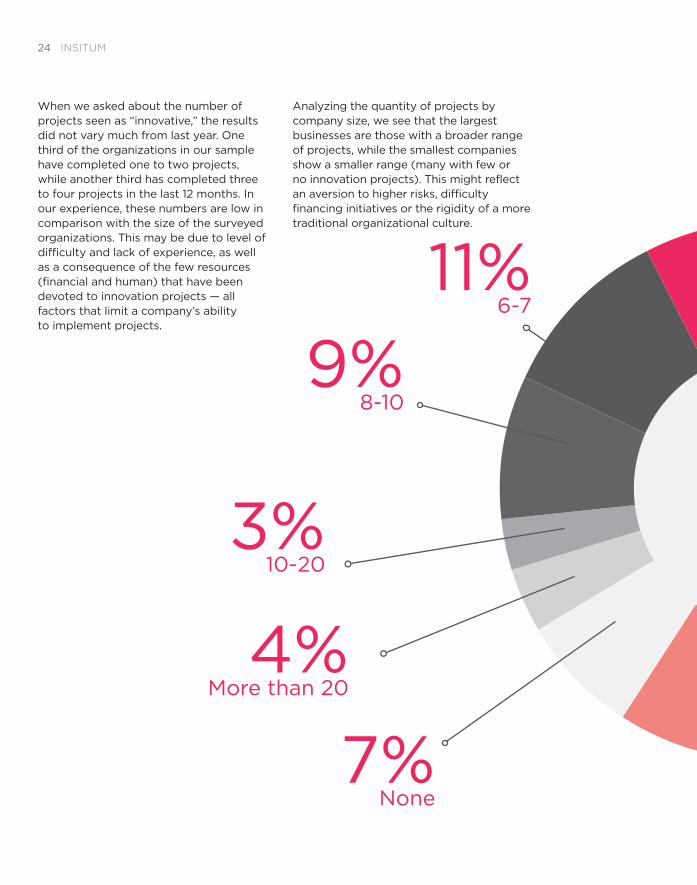

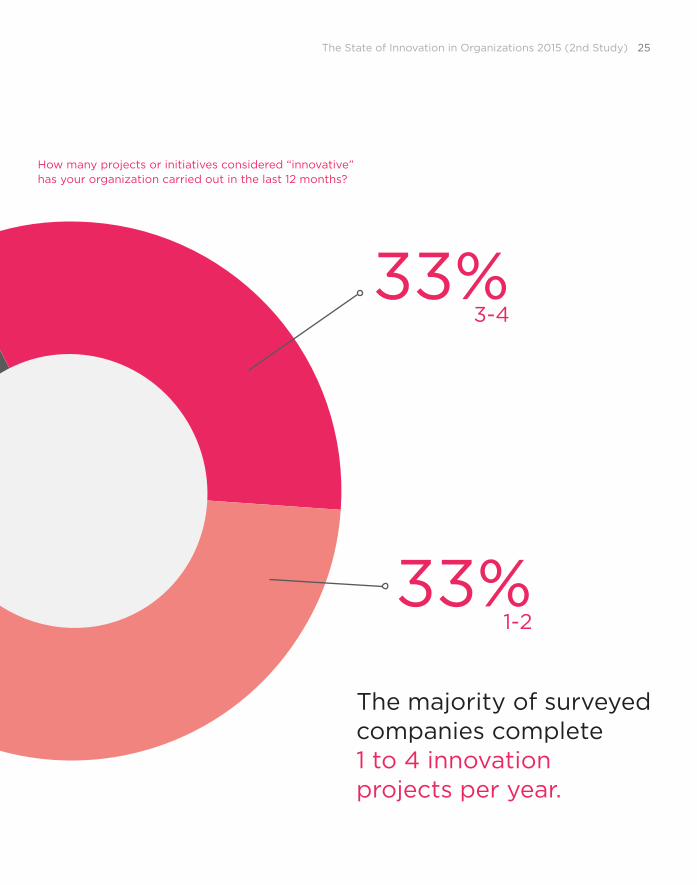

When we asked about the number of projects seen as “innovative,” the results did not vary much from last year. One third of the organizations in our sample have completed one to two projects, while another third has completed three to four projects in the last 12 months. In our experience, these numbers are low in comparison with the size of the surveyed organizations. This may be due to level of difficulty and lack of experience, as well as a consequence of the few resources (financial and human) that have been devoted to innovation projects — all factors that limit a company’s ability to implement projects.

Analyzing the quantity of projects by company size, we see that the largest businesses are those with a broader range of projects, while the smallest companies show a smaller range (many with few or no innovation projects). This might reflect an aversion to higher risks, difficulty financing initiatives or the rigidity of a more traditional organizational culture.

11% 6-7

9% 8-10

3% 10-20

4% More than 20

7% None

The State of Innovation in Organizations 2015 (2nd Study) 25

How many projects or initiatives considered “innovative” has your organization carried out in the last 12 months?

33% 1-2

33% 3-4

The majority of surveyed companies complete 1 to 4 innovation projects per year.

26 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 27

How is innovation implemented? Is there a strategy, tool or process to facilitate it?

There are various ways innovation can operate in a company. In our experience, there is no single ideal model that can be applied to all organizations. Rather, the best strategy depends on many variables including culture, scale of operations, diversification, sector, the types of innovation prioritized, innovation strategy and many more.

Some companies implement innovation centrally, while others do so in a network model, diffusely. For some, innovation is “top-down” from the CEO’s office, while for others it is a “bottom-up” effort with the participation of employees.

28 INSITUM

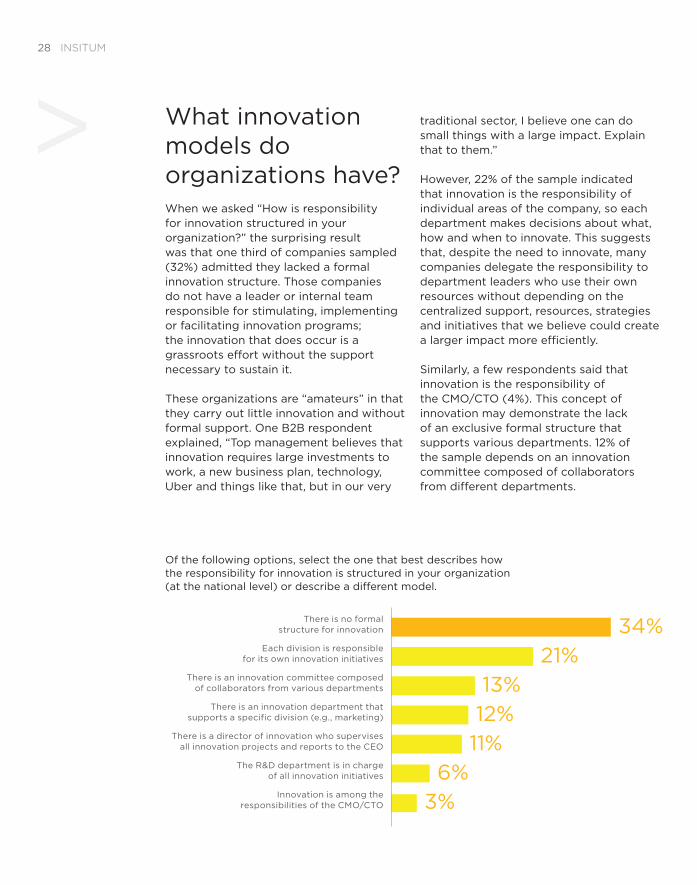

What innovation models do organizations have?When we asked “How is responsibility for innovation structured in your organization?” the surprising result was that one third of companies sampled (32%) admitted they lacked a formal innovation structure. Those companies do not have a leader or internal team responsible for stimulating, implementing or facilitating innovation programs; the innovation that does occur is a grassroots effort without the support necessary to sustain it.

These organizations are “amateurs” in that they carry out little innovation and without formal support. One B2B respondent explained, “Top management believes that innovation requires large investments to work, a new business plan, technology, Uber and things like that, but in our very

traditional sector, I believe one can do small things with a large impact. Explain that to them.”

However, 22% of the sample indicated that innovation is the responsibility of individual areas of the company, so each department makes decisions about what, how and when to innovate. This suggests that, despite the need to innovate, many companies delegate the responsibility to department leaders who use their own resources without depending on the centralized support, resources, strategies and initiatives that we believe could create a larger impact more efficiently.

Similarly, a few respondents said that innovation is the responsibility of the CMO/CTO (4%). This concept of innovation may demonstrate the lack of an exclusive formal structure that supports various departments. 12% of the sample depends on an innovation committee composed of collaborators from different departments.

Of the following options, select the one that best describes how the responsibility for innovation is structured in your organization (at the national level) or describe a different model.

There is no formal structure for innovation

Each division is responsible for its own innovation initiatives

There is an innovation committee composed of collaborators from various departments

There is an innovation department that supports a specific division (e.g., marketing)

There is a director of innovation who supervises all innovation projects and reports to the CEO

The R&D department is in charge of all innovation initiatives

Innovation is among the responsibilities of the CMO/CTO

34%

21%

13%

12%

11%

6%

3%

The State of Innovation in Organizations 2015 (2nd Study) 29

This indicates more innovation experience. These organizations have opted for an interdisciplinary strategy for executing innovative projects, though it remains a responsibility of the committee members.

Only 11% of surveyed organizations utilize a formal, centralized innovation department that provides support to various divisions. This is a more professionalized innovation model, unfortunately found only in a small percentage of organizations, but with a visible upward trend. As one interviewee (a CEO in the financial services sector) said, “We know that if we don’t innovate, our business is going to disappear. We are committed to creating an innovation department this year and we are in search of a team, but there are few people out there with the experience that this position requires.”Another interesting finding is that “R&D” appears to be understood as being synonymous with innovation. Yet in reality, we found that only 5% of surveyed

companies had an R&D department that leads all innovation initiatives. This seems to indicate that innovation is not the exclusive province of the R&D department, but instead occurs in all areas of the company, and that the department has little power to initiate company-wide innovation initiatives.

34%

There are still many companies in which innovation occurs without a formal or centralized structure.

30 INSITUM

A more formal and established processOne of the biggest differences we noted from the previous year emerged when we asked about the characteristics of organizations’ innovation processes. From the question, “How would you evaluate the process that your organization uses to innovate?” we can observe certain continuities from the previous year that indicate that the processes are not rigid, but rather adaptable to the needs of each project. Like the previous year, the most frequent responses were: “The process is adapted depending on each situation or need” (40%) and “Each department innovates using its own process” (31%).

One of our interviewees (a director of marketing in the entertainment sector) added: “Innovation is constant work, but it isn’t so structured — it isn’t as though there were an innovation department or policy. Instead, it falls on individuals, each of whom seizes opportunities in his or her area”.

Similarly, the tendency to use a variety of methods and processes depending on the department or challenge continues. This need for adaptation is clear in the affirmation of one of the telecom managers we surveyed: “We still need processes that can be adapted to different kinds of teams and challenges … no single process is applicable everywhere”.

How would you evaluate the process that your organization/division uses to innovate? (mark all that apply)

There is no process for innovation (I do not know of one)

It is a rigorous process that does not allow for adjustments

There is a process on paper, but it is ineffective for this type of organization

It is a fun and invigorating process

There is an improvised and informal process

It is a traditional “stage gate”

It is a process in which we co-create with our clients from ideation to execution

It is an open and collaborative process that fosters alliances

It is a process centered on the user (consumer/customer insights)

It is a flexible, creative and collaborative process

Each group innovates using its own process

The process is adapted to every situation or need

19%8%

10%11%

18%12%

23%14%

30%17%

21%17%

17%

22%

27%24%

30%28%

33%31%

41%40%

2014 2015

The State of Innovation in Organizations 2015 (2nd Study) 31

Compared to 2014, we see significant differences in having dedicated resources to formalize and implement innovation processes. It is worth noting that the response “There is an improvised and informal process” (17%) has declined significantly in relation to the previous year (30%). Similarly, the option “There is no process for innovation” falls in last place this year at 8%, compared to 19% the previous year. These two data points lead us to believe that organizations are more aware of the need for a planned innovation process. Informality and improvisation have given way to other options that demonstrate a certain maturity in organizations, although this might also include increased bureaucracy.

As one director of professional services indicates, “Until recently, we left much up to improvisation … now we have at least a plan to work from”.

This year, the questionnaire included two new possible responses to this question: “It is an open and collaborative process that fosters alliances with third parties” (22%) and “It is a process in which we co-create with our clients from ideation to execution (17%). With both options, we aimed to better understand the willingness of organizations to foster open innovation, whether with partner companies or with their own clients. Indeed, there appears to be relevance, as these option placed well (fifth and sixth respectively).

In the last year, more companies have implemented innovation processes and they are more rigorous and formal.

32 INSITUM

How many companies have a well-defined and well-communicated organizational innovation strategy?Innovation can be the primary tool to ensure the growth of a company, but this is only possible when innovation efforts are aligned with a strategy. In many cases, companies carry out isolated innovation projects without comprehensive strategies behind them, making initiatives difficult to implement.

The businesses with the most impactful innovation initiatives are those in which efforts stem from a strategy. In 2014, 60% of companies responded that they did have an innovation strategy, while this year the number rose to 63.5%.

“Innovation and strategy have to be in constant conversation — they’re part of the same whole.” — VP of Innovation, Industrial Conglomerate.

“Last year, we hired [a consultant] who helped us to develop our innovation strategy over two years, defining areas, leaders, processes and objectives.” — VP, Labor Union.

We consider this to be only a modest increase and believe that vast opportunities remain for more businesses to focus their efforts on innovation based on a clear strategy.

Nonetheless, simply having an innovation strategy is not enough — it must be well defined and clearly communicated. This year, we requested more details about innovation strategies. It is noteworthy that relatively few companies have a well-defined innovation strategy (31%), while a similar percentage have an innovation strategy that is not sufficiently well defined to be applied correctly (28%). As one CEO of a beverage manufacturer indicated: “Innovation is part of our strategy and we know there are many opportunities throughout the business — we have the latest technology but are unsure of where to start … products, brands, distribution, manufacturing. When you see opportunities everywhere, you get confused and want to do everything at once!”.

Has your organization developed an organizational innovation strategy?

28%Yes, but it is not well defined

4.5%Yes, but I am unfamiliar with it

6.8%Not sure

29.7%No

31%Yes, it is well defined

The State of Innovation in Organizations 2015 (2nd Study) 33

This demonstrates the work required for organizations to define an innovation strategy and apply it correctly throughout. Approximately one-third (29.7%) lack an organizational innovation strategy. We believe this is due to two factors: 1) organizational innovation is not part of the routine business processes or models organizations have implemented (as through a strategic marketing plan or a portfolio review); and 2) there are sectors where innovation is not prioritized, as the sectors least likely to implement an innovation strategy are: construction, engineering, and real estate; energy/petroleum/mining/extraction and raw material management; finance (banking, insurance and investment services); industrial products, logistics, and business-to-business; and retail/commerce.

As one commerce director of operations said, “For an industrial products company like ours, innovation is very focused on [investing in] technology and nothing else … we have not thought enough about a specific strategy that would identify three innovation priorities for the year”.

“What does ‘innovation strategy’ refer to? Here we have strategic planning exercises, but we do not have one focused on innovation initiatives.” — CMO, Beverage Manufacturer.

All of this underscores the importance of every organization investing time and resources in defining an innovation strategy that incorporates different areas of the business and that aligns with its corporate strategy — even for less visible sectors where the focus is on operation, efficiency and cost, but where customer needs remain unmet or require differentiation.

“Good [innovation] strategies promote the alignment of different groups within the organization, define objectives and priorities, and help to focus those efforts.” — Gary P. Pisano, Harvard Business Review, June 2015

Do you have a well-defined and well-communicated organizational innovation strategy?

Yes 2015 63.5%2014 60% No 2015 29.7%

2014 35.5%

Highest-ranking sectors: > Consumer products (food, beverage, hygienic products, etc.)

> Telecommunications (telephone, Internet, TV, etc.)

> Technology (computing, software, electronics, etc.)

> Media, arts, entertainment and recreation

Lowest-ranking sectors: > Construction, engineering, and real estate > Energy/petroleum/mining/extraction and raw material management

> Finance (banking, insurance and investment services)

> Industrial products, logistics, business-to-business

> Retail and commerce

2015 6.8%

Not sure2014 4.5%

The State of Innovation in Organizations 2015 (2nd Study) 35

A growing number of companies have an organizational innovation strategy, though in many cases it is not communicated effectively.

36 INSITUM

What kinds of organizations have a department whose primary responsibility is innovation? Innovation is such a fundamental responsibility in today’s organizations that it requires at least one person whose primary responsibility is innovation.

This is what distinguishes expert organizations from the “amateurs”; the experts are those that truly devote people, time and resources to making innovation work — and they yield results. In our sample, we found that the largest organizations (more than $1 billion) and the consumer products sector (food, beverage, hygienic products) are those with the largest number of people whose primary responsibility is innovation. In contrast, the more amateur organizations tend to be the smallest (less than $100 million) and those in the construction, engineering and real estate sectors, with a very limited number of people exclusively dedicated to innovation.

Does your organization (at the national level) have a department, group or individual whose primary responsibility is innovation?

These sectors represent organizations that indicated having a department dedicated primarily to innovation:

68% 32%

59% 41%

55% 45%

34% 66%

75%Consumer products (food, beverage, hygienic products)

58%Automotive and auto parts

50%Finance (banking, insurance and investment services)

And these were cited least often:

35%Energy/petroleum/mining/extraction and raw material management

21%Construction, engineering and real estate

The State of Innovation in Organizations 2015 (2nd Study) 37

The largest organizations have the most resources to develop their own innovation departments, although this appears to be emerging only in certain sectors, such as consumer products, automotive/auto parts and banking/finance.

38 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 39

Who is behind innovation in organizations?

All innovation starts with people.Innovation leaders in organizations require certain skills to implement processes and inspire the rest of the organization to innovate. The objective of this section is to explore their most important roles and to understand which skills enable them to do this work. This information may be useful for shaping recruitment tools or personnel evaluation.

40 INSITUM

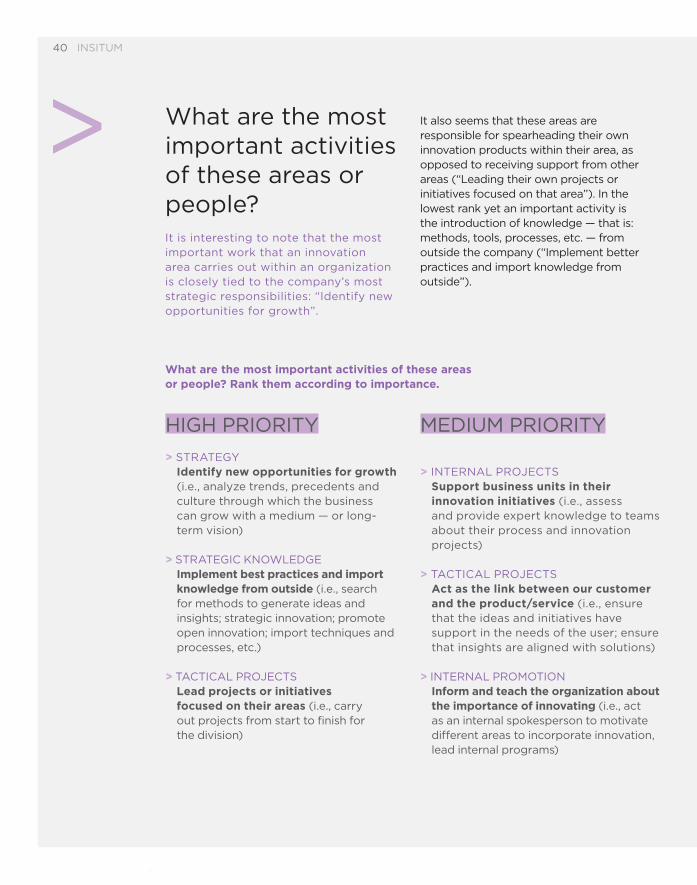

What are the most important activities of these areas or people? It is interesting to note that the most important work that an innovation area carries out within an organization is closely tied to the company’s most strategic responsibilities: “Identify new opportunities for growth”.

It also seems that these areas are responsible for spearheading their own innovation products within their area, as opposed to receiving support from other areas (“Leading their own projects or initiatives focused on that area”). In the lowest rank yet an important activity is the introduction of knowledge — that is: methods, tools, processes, etc. — from outside the company (“Implement better practices and import knowledge from outside”).

What are the most important activities of these areas or people? Rank them according to importance.

HIGH PRIORITY MEDIUM PRIORITY

> STRATEGY Identify new opportunities for growth

(i.e., analyze trends, precedents and culture through which the business can grow with a medium — or long- term vision)

> STRATEGIC KNOWLEDGE Implement best practices and import

knowledge from outside (i.e., search for methods to generate ideas and insights; strategic innovation; promote open innovation; import techniques and processes, etc.)

> TACTICAL PROJECTS Lead projects or initiatives

focused on their areas (i.e., carry out projects from start to finish for the division)

> INTERNAL PROJECTS Support business units in their

innovation initiatives (i.e., assess and provide expert knowledge to teams about their process and innovation projects)

> TACTICAL PROJECTS Act as the link between our customer

and the product/service (i.e., ensure that the ideas and initiatives have support in the needs of the user; ensure that insights are aligned with solutions)

> INTERNAL PROMOTION Inform and teach the organization about

the importance of innovating (i.e., act as an internal spokesperson to motivate different areas to incorporate innovation, lead internal programs)

The State of Innovation in Organizations 2015 (2nd Study) 41

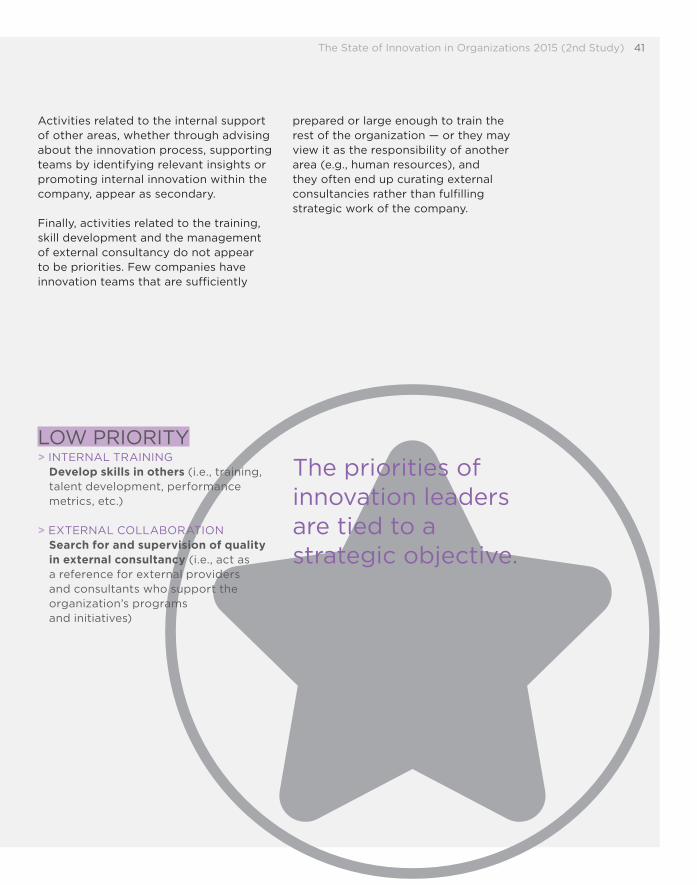

Activities related to the internal support of other areas, whether through advising about the innovation process, supporting teams by identifying relevant insights or promoting internal innovation within the company, appear as secondary. Finally, activities related to the training, skill development and the management of external consultancy do not appear to be priorities. Few companies have innovation teams that are sufficiently

prepared or large enough to train the rest of the organization — or they may view it as the responsibility of another area (e.g., human resources), and they often end up curating external consultancies rather than fulfilling strategic work of the company.

LOW PRIORITY> INTERNAL TRAINING Develop skills in others (i.e., training,

talent development, performance metrics, etc.)

> EXTERNAL COLLABORATION Search for and supervision of quality

in external consultancy (i.e., act as a reference for external providers and consultants who support the organization’s programs and initiatives)

The priorities of innovation leaders are tied to a strategic objective.

42 INSITUM

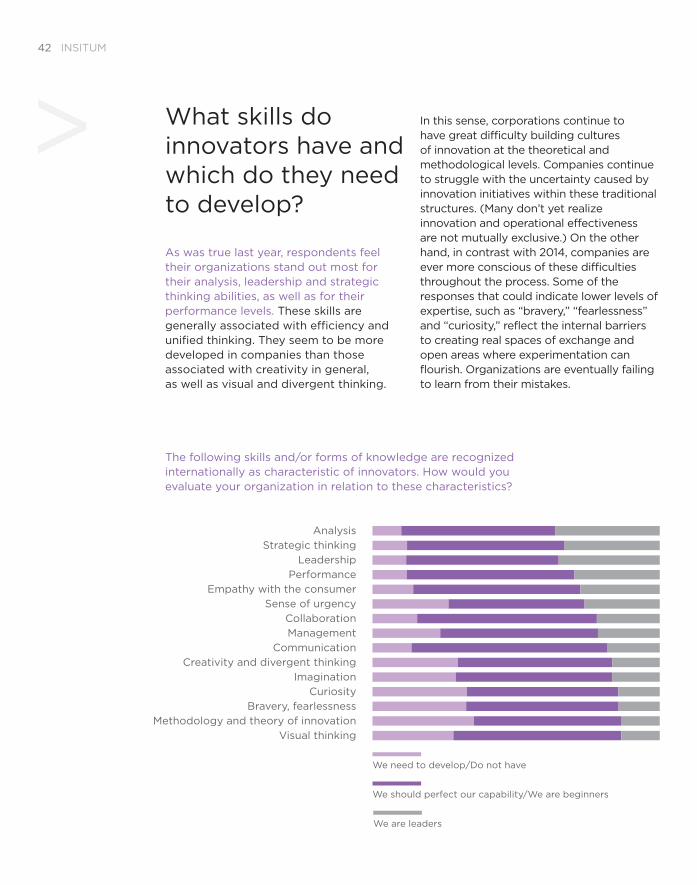

What skills do innovators have and which do they need to develop? As was true last year, respondents feel their organizations stand out most for their analysis, leadership and strategic thinking abilities, as well as for their performance levels. These skills are generally associated with efficiency and unified thinking. They seem to be more developed in companies than those associated with creativity in general, as well as visual and divergent thinking.

In this sense, corporations continue to have great difficulty building cultures of innovation at the theoretical and methodological levels. Companies continue to struggle with the uncertainty caused by innovation initiatives within these traditional structures. (Many don’t yet realize innovation and operational effectiveness are not mutually exclusive.) On the other hand, in contrast with 2014, companies are ever more conscious of these difficulties throughout the process. Some of the responses that could indicate lower levels of expertise, such as “bravery,” “fearlessness” and “curiosity,” reflect the internal barriers to creating real spaces of exchange and open areas where experimentation can flourish. Organizations are eventually failing to learn from their mistakes.

The following skills and/or forms of knowledge are recognized internationally as characteristic of innovators. How would you evaluate your organization in relation to these characteristics?

Analysis

Strategic thinking

Leadership

Performance

Empathy with the consumer

Sense of urgency

Collaboration

Management

Communication

Creativity and divergent thinking

Imagination

Curiosity

Bravery, fearlessness

Methodology and theory of innovation

Visual thinking

We need to develop/Do not have

We should perfect our capability/We are beginners

We are leaders

The State of Innovation in Organizations 2015 (2nd Study) 43

Mexico and Brazil report the most expertise when it comes to methodology and theory of innovation (80% of respondents in those markets), suggesting a greater predisposition towards incorporating these areas into the company than in other countries. They also appear to offer greater teaching of innovation in formal academic programs within business schools. It is also worth noting the recurring responses detailing the lack of methodological skills related to prototyping and rapid development of innovations that arise in organizations. The difficulty of implanting planned solutions and strategies efficiently seems to be an additional impediment to the improvement of organizations’ internal practices.

On the other hand, communication and management seem to be improving with better group-work skills, one of the fundamental skills for implementing innovation in organizations.

Many organizations recognize that they need to further develop their innovation skills to fully realize their potential.

44 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 45

What motivations for and barriers to innovation exist today?The most innovative companies create a culture of innovation throughout the entire organization, one that encourages experimentation, does not fear failure and constantly searches for opportunities to do things better. But what motivates these organizations to be innovative? In this section, we explore the key factors that motivate innovation projects, but also the barriers and difficulties that emerge along the way.

46 INSITUM

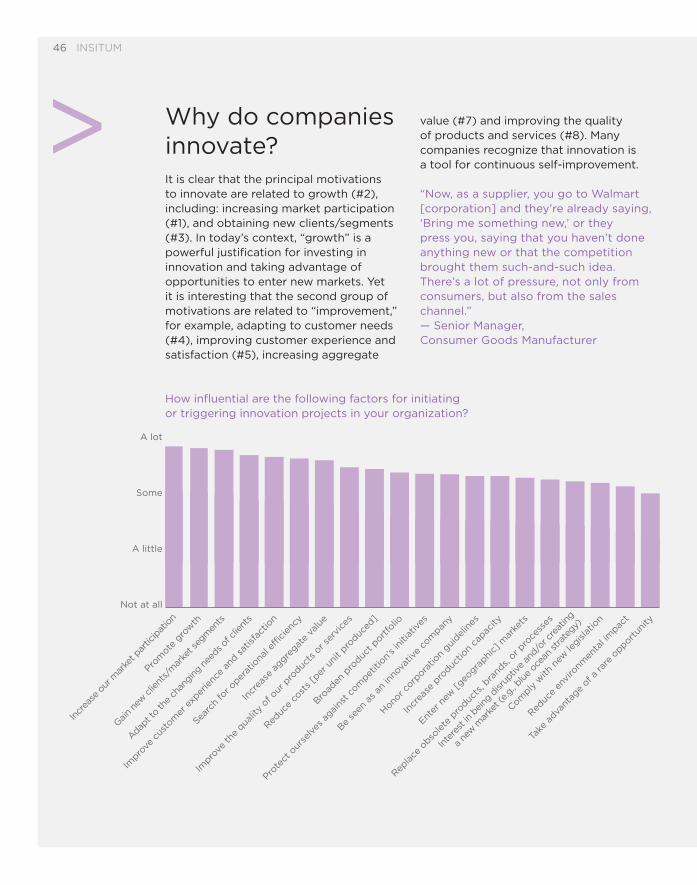

Why do companies innovate?It is clear that the principal motivations to innovate are related to growth (#2), including: increasing market participation (#1), and obtaining new clients/segments (#3). In today’s context, “growth” is a powerful justification for investing in innovation and taking advantage of opportunities to enter new markets. Yet it is interesting that the second group of motivations are related to “improvement,” for example, adapting to customer needs (#4), improving customer experience and satisfaction (#5), increasing aggregate

value (#7) and improving the quality of products and services (#8). Many companies recognize that innovation is a tool for continuous self-improvement.

“Now, as a supplier, you go to Walmart [corporation] and they’re already saying, ‘Bring me something new,’ or they press you, saying that you haven’t done anything new or that the competition brought them such-and-such idea. There’s a lot of pressure, not only from consumers, but also from the sales channel.” — Senior Manager, Consumer Goods Manufacturer

How influential are the following factors for initiating or triggering innovation projects in your organization?

Incr

ease

our

mar

ket p

artic

ipat

ion

Prom

ote g

row

th

Gain

new clie

nts/

mar

ket s

egm

ents

Adapt t

o th

e ch

angin

g nee

ds of c

lient

s

Impro

ve c

usto

mer

exp

erie

nce

and s

atisfa

ctio

n

Searc

h fo

r oper

atio

nal e

fficien

cy

Incr

ease

aggre

gate

valu

e

Impro

ve th

e qua

lity

of our

pro

ducts

or s

ervi

ces

Reduc

e co

sts [p

er u

nit p

roduc

ed]

Broad

en p

roduc

t port

folio

Prote

ct o

urse

lves

agai

nst c

ompet

ition’

s in

itiat

ives

Be se

en a

s an

inno

vativ

e co

mpan

y

Hono

r corp

oratio

n gui

delin

es

Incr

ease

pro

ductio

n ca

pacity

Enter

new

[geo

graphi

c] m

arke

ts

Replace

obso

lete

pro

ducts

, bra

nds,

or pro

cess

es

Inte

rest in

being

disr

uptiv

e an

d/or c

reat

ing

a ne

w m

arke

t (e.g., b

lue oc

ean

stra

tegy)

Comply

with

new

legis

latio

n

Reduc

e en

viro

nmen

tal im

pact

Take

adva

ntag

e of a

rare

opport

unity

A lot

Some

A little

Not at all

The State of Innovation in Organizations 2015 (2nd Study) 47

The third group of motivations is related to “saving,” indicating that companies recognize the value of applying innovation to achieve efficiencies and increase productivity. For example: search for operational efficiency (#6), reduce costs (#9) and increase production capacity (#14). The fourth group of motivations is related to factors extrinsic to the company — legal factors, image or social pressure. For example: be seen as an innovative company (#12), comply with new legislation (#18) and reduce environmental impact (#19).

Nevertheless, there are cases of significant differences depending on company size: the largest companies (more than $1 billion) are more likely to initiate innovation projects to protect themselves against initiatives by competition, enter new (geographic) markets, or to follow guidelines from headquarters. We believe

this is due to competitive pressure and growth pressure that large companies experience.

“We have very ambitious goals for growth (…) on the part of the corporation and the shareholders (…) and Latin America remains underexplored. That’s why we’re able to invest in projects that give us an advantage over the competition that hasn’t yet arrived in Latin America.” — Product Leader, B2B Technology Company

It is worth noting that, for smaller businesses (less than $100 million), extrinsic factors are less important — for example, being seen as an innovative business. Smaller organizations may be under less pressure to manage the image they project outwardly and also less susceptible to the pressure to comply with new legislation.

48 INSITUM

The principal motivations to innovate are tied to growth, but...

The State of Innovation in Organizations 2015 (2nd Study) 49

there are many barriers to overcome.

50 INSITUM

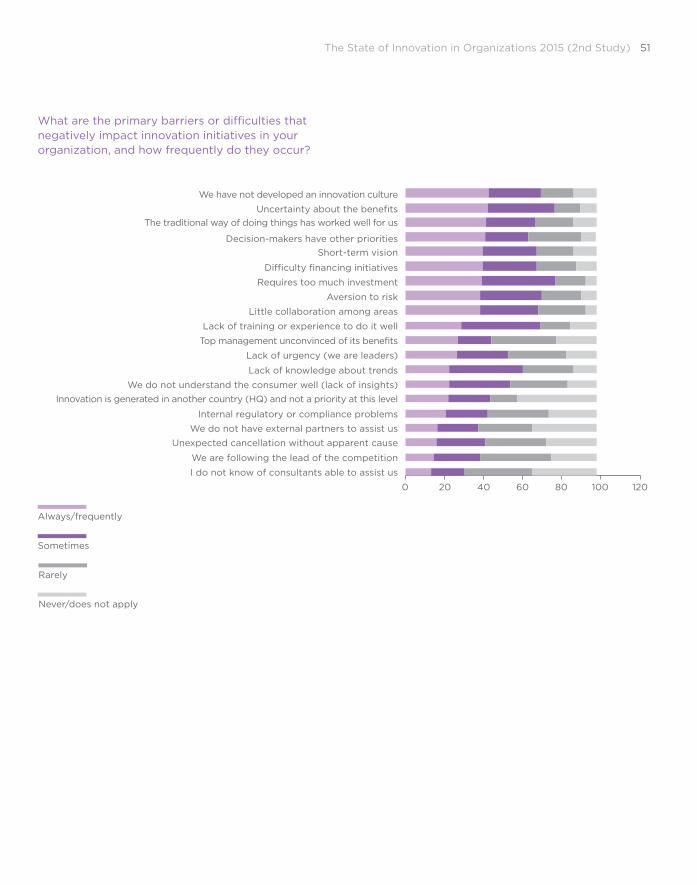

And the barriers to innovation are…As we saw last year, the primary barrier to innovation is that organizations have not yet created a culture of innovation. It is this culture that can break with the status quo through practices that foster development, experimentation and the implementation of innovative solutions. Other challenges stem from this first cultural factor — for example, uncertainty about the benefits of innovation, failure to envision a departure from the traditional way of doing things or simply that leaders have other priorities and see innovation as “nice to have” but not necessary.

“We have been innovating for years, but do you know how many projects have been implemented? (…) Few people are convinced. Since we have 30-year veterans on the board and the business keeps growing, they don’t see a reason to change things or to do something new.” — VP of Innovation, Food Manufacturer

Risk aversion and short-term vision are other common barriers found in many organizations. These are closely linked to corporate culture. Although, as compared to last year (when they ranked second and third in importance, respectively), this year they have declined in importance, ranking fifth and eighth. It seems that organizations are slowly changing and becoming more courageous and visionary in their thinking about innovation.

The State of Innovation in Organizations 2015 (2nd Study) 51

Always/frequently

Sometimes

Rarely

Never/does not apply

0 1206020 8040 100

We have not developed an innovation culture

Uncertainty about the benefits

The traditional way of doing things has worked well for us

Decision-makers have other priorities

Short-term vision

Difficulty financing initiatives

Requires too much investment

Aversion to risk

Little collaboration among areas

Lack of training or experience to do it well

Top management unconvinced of its benefits

Lack of urgency (we are leaders)

Lack of knowledge about trends

We do not understand the consumer well (lack of insights)

Innovation is generated in another country (HQ) and not a priority at this level

Internal regulatory or compliance problems

We do not have external partners to assist us

Unexpected cancellation without apparent cause

We are following the lead of the competition

I do not know of consultants able to assist us

What are the primary barriers or difficulties that negatively impact innovation initiatives in your organization, and how frequently do they occur?

The State of Innovation in Organizations 2015 (2nd Study) 53

How much of a priority is innovation in organizations?Many organizations today include the word “innovation” as part of their mission, vision or corporate culture statement. Others openly claim to be innovative, or position themselves as such to attract clients and talents — but is it really a priority?

54 INSITUM

How much of a priority is innovation in your organization?With this question, we found that reality radically differed from perception. The majority of company respondents consider innovation “fairly important” (44%) or “one of many priorities” (35%), which, in our experience, is generally closer to reality. Comparing this data with the previous year, we see a clear upward trend in innovation’s importance.

“[Innovation] continues to be a priority, with visible results that keep its importance high.” — Senior Manager, Consumer Goods

“This past year, we have worked on recovery and other areas, but as we get through that rough patch, we are investing in innovation again.” — Manager, Pharmaceutical Manufacturer

How much do you think innovation is prioritized in your organization?

It is our main

priority

It is fairly

important

It is one of many

priorities

It is of low

priority

It is not relevant

50

45

40

35

30

25

20

15

10

5

0

The State of Innovation in Organizations 2015 (2nd Study) 55

Innovation continues to become a higher priority for organizations.

56 INSITUM

When asked about their organization’s perceptions and attitudes about innovation, interviewees cited general positivity and important advances in the visibility, importance and execution of innovation, but many also recognize that there is much work to be done and many barriers to overcome in order to reach higher standards.

The general opinion is positive and results have already been achieved, but there is still much to be done.

The State of Innovation in Organizations 2015 (2nd Study) 57

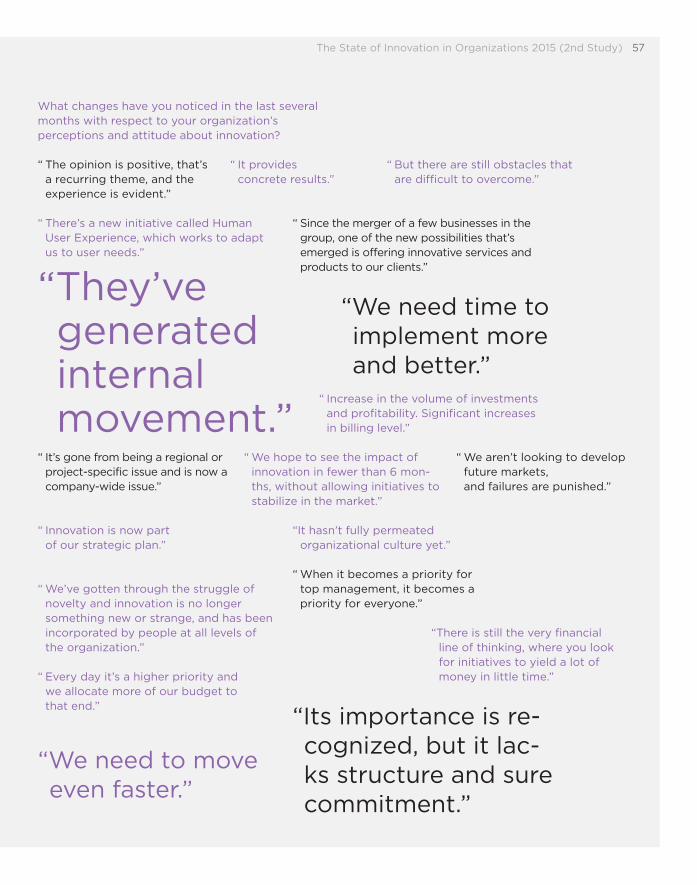

What changes have you noticed in the last several months with respect to your organization’s perceptions and attitude about innovation?

“ The opinion is positive, that’s a recurring theme, and the experience is evident.”

“ We’ve gotten through the struggle of novelty and innovation is no longer something new or strange, and has been incorporated by people at all levels of the organization.”

“ There’s a new initiative called Human User Experience, which works to adapt us to user needs.”

“ It’s gone from being a regional or project-specific issue and is now a company-wide issue.”

“ Every day it’s a higher priority and we allocate more of our budget to that end.”

“ Innovation is now part of our strategic plan.”

“ We hope to see the impact of innovation in fewer than 6 mon-ths, without allowing initiatives to stabilize in the market.”

“It hasn’t fully permeated organizational culture yet.”

“There is still the very financial line of thinking, where you look for initiatives to yield a lot of money in little time.”

“ When it becomes a priority for top management, it becomes a priority for everyone.”

“ Since the merger of a few businesses in the group, one of the new possibilities that’s emerged is offering innovative services and products to our clients.”

“ It provides concrete results.”

“They’ve generated internal movement.”

“ But there are still obstacles that are difficult to overcome.”

“We need time to implement more and better.”

“Its importance is re-cognized, but it lac-ks structure and sure commitment.”

“We need to move even faster.”

“ We aren’t looking to develop future markets, and failures are punished.”

“ Increase in the volume of investments and profitability. Significant increases in billing level.”

58 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 59

What works and does not work in innovation?

That most organizations are still adapting and evolving when it comes to innovation is still new. Some organizations are better prepared than others; there is talent in some and less in others; there are larger and smaller budgets — but the reality is that the conditions are emerging quickly to make innovation a crucial strategic tool.

Although many companies are still “innovation rookies” when it comes to implementing innovation, signs still point to openness, willingness, and optimism. As in the previous year, respondents offered a greater variety of negative responses (what works poorly) than positive (what works well).

60 INSITUM

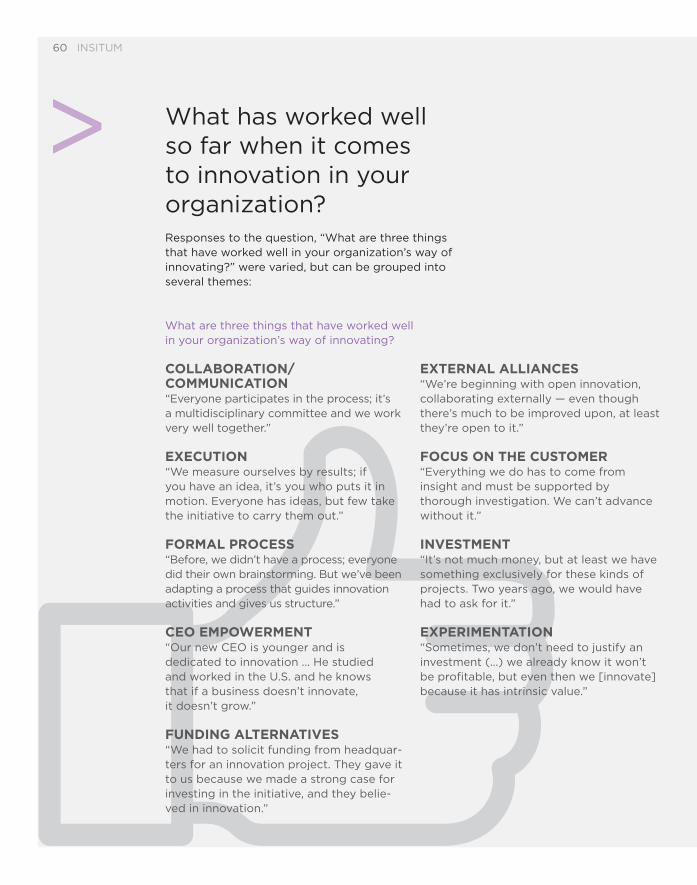

What has worked well so far when it comes to innovation in your organization?Responses to the question, “What are three things that have worked well in your organization’s way of innovating?” were varied, but can be grouped into several themes:

COLLABORATION/COMMUNICATION“Everyone participates in the process; it’s a multidisciplinary committee and we work very well together.”

EXECUTION“We measure ourselves by results; if you have an idea, it’s you who puts it in motion. Everyone has ideas, but few take the initiative to carry them out.”

FORMAL PROCESS“Before, we didn’t have a process; everyone did their own brainstorming. But we’ve been adapting a process that guides innovation activities and gives us structure.”

CEO EMPOWERMENT“Our new CEO is younger and is dedicated to innovation … He studied and worked in the U.S. and he knows that if a business doesn’t innovate, it doesn’t grow.”

FUNDING ALTERNATIVES“We had to solicit funding from headquar-ters for an innovation project. They gave it to us because we made a strong case for investing in the initiative, and they belie-ved in innovation.”

EXTERNAL ALLIANCES“We’re beginning with open innovation, collaborating externally — even though there’s much to be improved upon, at least they’re open to it.”

FOCUS ON THE CUSTOMER“Everything we do has to come from insight and must be supported by thorough investigation. We can’t advance without it.”

INVESTMENT“It’s not much money, but at least we have something exclusively for these kinds of projects. Two years ago, we would have had to ask for it.”

EXPERIMENTATION“Sometimes, we don’t need to justify an investment (…) we already know it won’t be profitable, but even then we [innovate] because it has intrinsic value.”

What are three things that have worked well in your organization’s way of innovating?

The State of Innovation in Organizations 2015 (2nd Study) 61

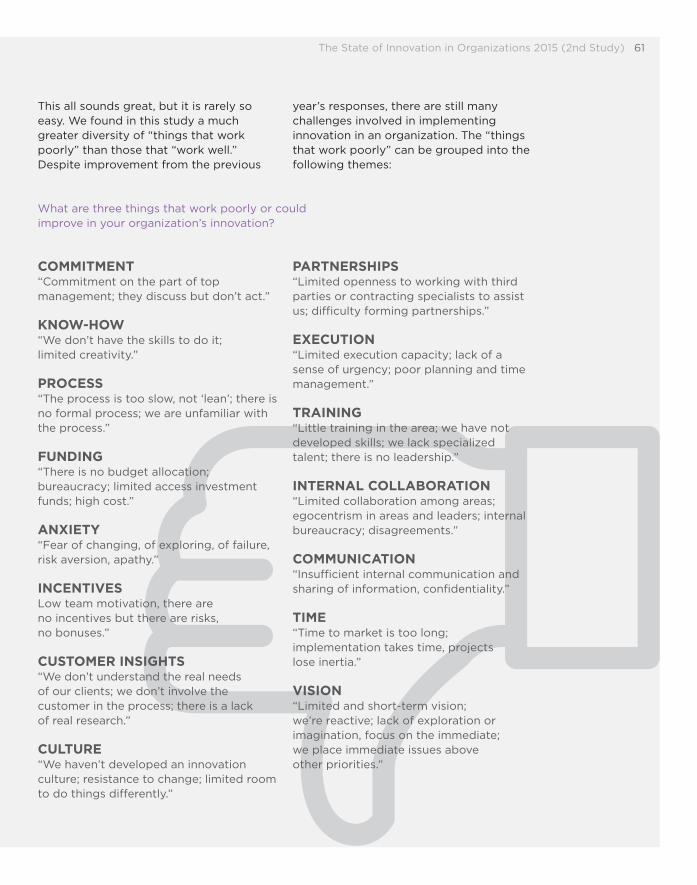

This all sounds great, but it is rarely so easy. We found in this study a much greater diversity of “things that work poorly” than those that “work well.” Despite improvement from the previous

COMMITMENT“Commitment on the part of top management; they discuss but don’t act.”

KNOW-HOW “We don’t have the skills to do it; limited creativity.”

PROCESS“The process is too slow, not ‘lean’; there is no formal process; we are unfamiliar with the process.”

FUNDING “There is no budget allocation; bureaucracy; limited access investment funds; high cost.”

ANXIETY“Fear of changing, of exploring, of failure, risk aversion, apathy.”

INCENTIVESLow team motivation, there are no incentives but there are risks, no bonuses.”

CUSTOMER INSIGHTS“We don’t understand the real needs of our clients; we don’t involve the customer in the process; there is a lack of real research.”

CULTURE“We haven’t developed an innovation culture; resistance to change; limited room to do things differently.”

PARTNERSHIPS“Limited openness to working with third parties or contracting specialists to assist us; difficulty forming partnerships.”

EXECUTION“Limited execution capacity; lack of a sense of urgency; poor planning and time management.”

TRAINING“Little training in the area; we have not developed skills; we lack specialized talent; there is no leadership.”

INTERNAL COLLABORATION“Limited collaboration among areas; egocentrism in areas and leaders; internal bureaucracy; disagreements.”

COMMUNICATION“Insufficient internal communication and sharing of information, confidentiality.”

TIME“Time to market is too long; implementation takes time, projects lose inertia.”

VISION“Limited and short-term vision; we’re reactive; lack of exploration or imagination, focus on the immediate; we place immediate issues above other priorities.”

What are three things that work poorly or could improve in your organization’s innovation?

year’s responses, there are still many challenges involved in implementing innovation in an organization. The “things that work poorly” can be grouped into the following themes:

62 INSITUM

Of the organizations that did offer training or workshops, the results left much to be desired. Only 70% of those say they recognized any concrete or actionable results, while 30% do not believe that they have obtained a concrete result. In the aggregate, this suggests several conclusions: 1) there is not enough interest overall in professional courses focused on developing innovation skills; 2) some of the current offerings are inadequate and do not focus on providing organizations with concrete results; and 3) good training is sometimes initiated, but not taken far enough. To truly master this type of work, companies could also use more extended support while they are managing actual projects over the course of several cycles. It is therefore necessary to broaden the offerings and increase the quality of training through educational programs at formal academic institutions or through consultancies specializing in innovation training.

Are you receiving training in innovation?In the previous year, one of the primary opportunities we identified for improving innovation capacity in companies was training. This year, we have found that it remains an area in which companies have little interest in investing. In a context in which talent is scarce — especially in the specialized area of innovation — it is indispensable for companies to train personnel in relevant skills. These include creativity, design thinking, innovation processes, innovation metrics, visual thinking and storytelling, among others. It seems from our data that this year, training is on the decline; there are simply a greater number of businesses that have not had training or workshops focused on developing innovation skills in their teams (59.7%). This response from a pharmaceutical business partner captured the phenomenon very well: “[Last year] innovation came into fashion. Every department was requesting training. This year, it seems like they’re applying what they learned last year.”

The State of Innovation in Organizations 2015 (2nd Study) 63

The sectors that indicate they are currently investing the most in training:

> Consumer products (food, beverage, hygienic products)

> Energy/petroleum/mining/extraction/raw material management

> Finance (banking, insurance and investment services)

During the last 12 months, has your organization carried out any training or workshops focused on developing innovation skills in the staff?

YES NO

40.3% vs. 48% in 2014

59.7%vs. 52% in 2014

70% There were concrete and actionable results

30% There were no concrete or actionable results

64 INSITUM

Organizations have an optimistic outlook when it comes to growth.One important factor that is often related to an organization’s openness to innovate is the term “growth.” This year, we hoped to learn more about organizations’ states of mind, so we asked about their experience with growth in the past and their hopes for the future.

In response to the question, “In the last two years, has your organization considered entering a new industry, sector/subsector or product category?” we found that the majority of organizations (39%) had already done so successfully; another portion (32%) had done so, but were still in the process; and a slight minority had not considered entering into a new industry, sector, or product category. Considering the types of businesses that responded, we find this final number disturbingly high and hope that in the coming years, innovation will become one of the most useful tools for helping more companies grow.

In the last two years, has your organization considered entering a new industry, sector/subsector or product category?

No Yes, but it has not

fully taken shape

Yes,successfully

28% 33% 39%

The State of Innovation in Organizations 2015 (2nd Study) 65

Which phrase best describes your organization’s sales growth expectations for coming two years?

41%Aggressive

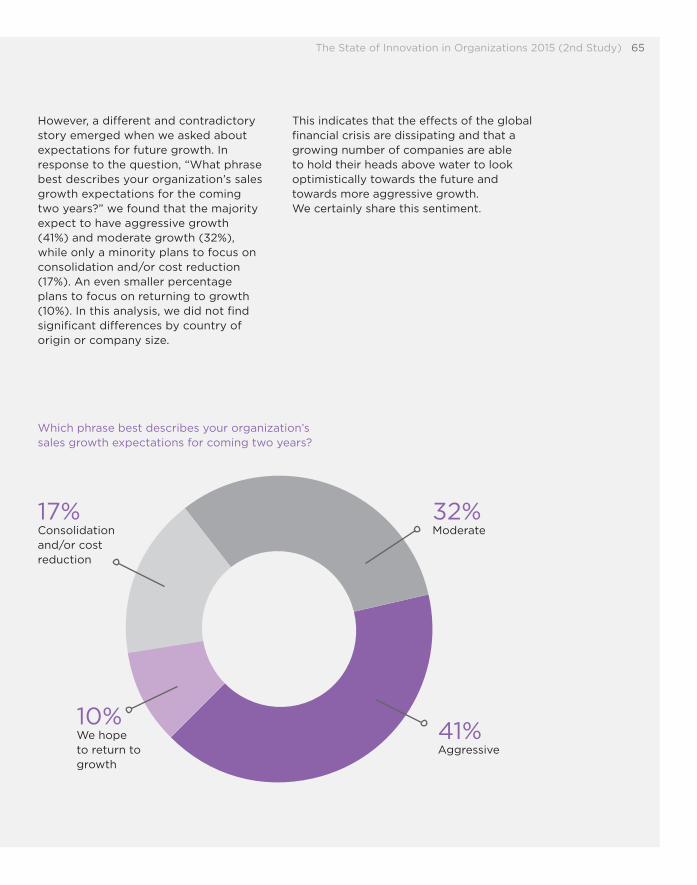

However, a different and contradictory story emerged when we asked about expectations for future growth. In response to the question, “What phrase best describes your organization’s sales growth expectations for the coming two years?” we found that the majority expect to have aggressive growth (41%) and moderate growth (32%), while only a minority plans to focus on consolidation and/or cost reduction (17%). An even smaller percentage plans to focus on returning to growth (10%). In this analysis, we did not find significant differences by country of origin or company size.

This indicates that the effects of the global financial crisis are dissipating and that a growing number of companies are able to hold their heads above water to look optimistically towards the future and towards more aggressive growth. We certainly share this sentiment.

32% Moderate

17% Consolidation and/or cost reduction

10% We hope to return to growth

66 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 67

What is your budgetary allocation for innovation?The difference between organizations that call themselves “innovative” and those that truly are innovative often lies in their financial commitment. Innovation must be a continuous investment that offers results in the long term; it must not be considered casual or sporadic. In this section, we explore the budgetary reality of innovation.

68 INSITUM

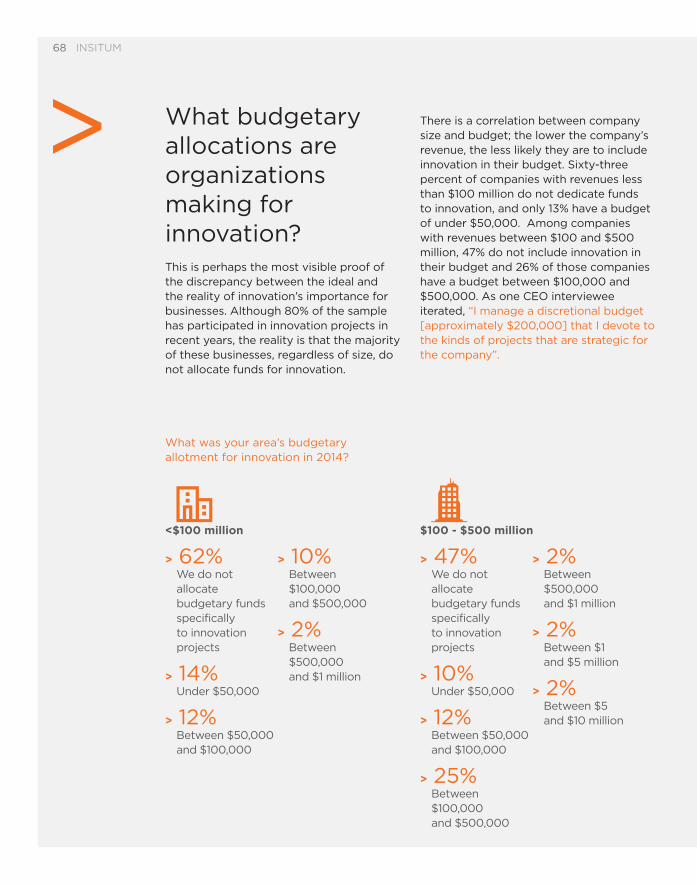

What budgetary allocations are organizations making for innovation?This is perhaps the most visible proof of the discrepancy between the ideal and the reality of innovation’s importance for businesses. Although 80% of the sample has participated in innovation projects in recent years, the reality is that the majority of these businesses, regardless of size, do not allocate funds for innovation.

What was your area’s budgetary allotment for innovation in 2014?

There is a correlation between company size and budget; the lower the company’s revenue, the less likely they are to include innovation in their budget. Sixty-three percent of companies with revenues less than $100 million do not dedicate funds to innovation, and only 13% have a budget of under $50,000. Among companies with revenues between $100 and $500 million, 47% do not include innovation in their budget and 26% of those companies have a budget between $100,000 and $500,000. As one CEO interviewee iterated, “I manage a discretional budget [approximately $200,000] that I devote to the kinds of projects that are strategic for the company”.

<$100 million

> 62%We do not allocate budgetary funds specifically to innovation projects

> 14%Under $50,000

> 12%Between $50,000 and $100,000

> 47%We do not allocate budgetary funds specifically to innovation projects

> 10%Under $50,000

> 12%Between $50,000 and $100,000

> 25%Between $100,000 and $500,000

> 2%Between $500,000 and $1 million

> 2%Between $1 and $5 million

> 2%Between $5 and $10 million

$100 - $500 million

> 10%Between $100,000 and $500,000

> 2%Between $500,000 and $1 million

The State of Innovation in Organizations 2015 (2nd Study) 69

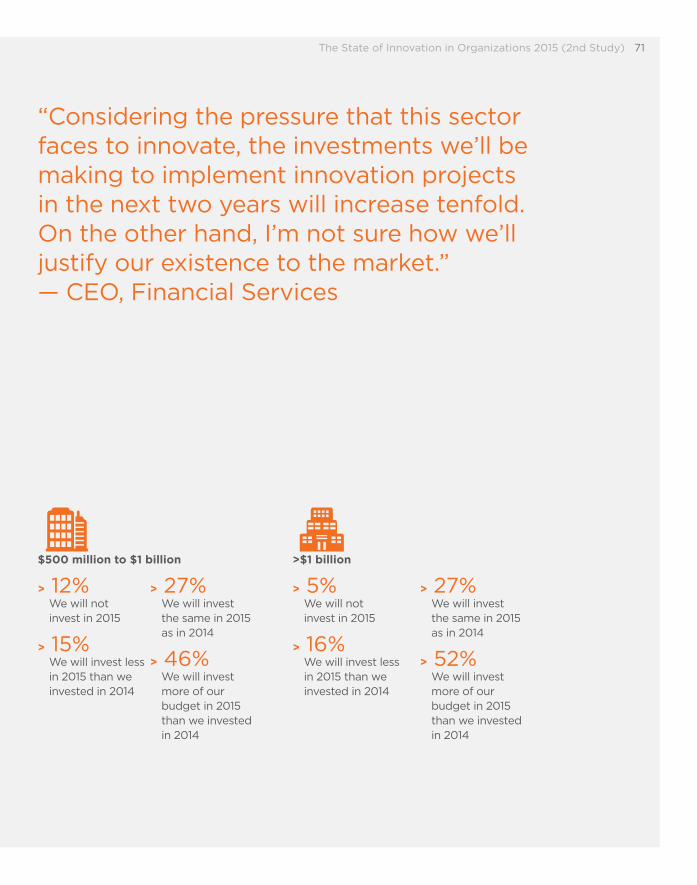

Among larger companies, between $500 and $1 billion, 46% lack a specific budgetary allocation, and 29% allocate between $100,000 and $500,000. “The great challenge to large companies is being able to isolate real innovation projects from those of Horizon 1 [of growth model], those closely connected with the core. It means having capital isolated for projects that involve risk and uncertainty, distinct from resources dedicated to normal development projects.” — Director of Innovation, Consumer Goods Manufacturer.

For the largest companies in the survey, those with revenues higher than $1 billion, only 35% do not have a specific allocation for innovation. This underscores that the majority of businesses of any size lack this kind of specific allocation.

$500 million to $1 billion

> 46%We do not allocate budgetary funds specifically to innovation projects

> 17%Under $50,000

> 35%We do not allocate budgetary funds specifically to innovation projects

> 3%Under $50,000

> 13%Between $50,000 and $100,000

> 18%Between $100,000 and $500,000

> 6%Between $500,000 and $1 million

> 13%Between $1 and $5 million

> 4%Between $5 and $10 million

> 8%More than $10 million

>$1 billion

> 29%Between $100,000 and $500,000

> 8%Between $500,000 and $1 million

70 INSITUM

Although current amounts are very small in relation to the revenues of these organizations, it should be noted that expectations for investment among all business types and sizes are highly optimistic. Approximately half of our respondents surveyed agree that in 2015, their organizations’ investment in innovation will be greater than it was in 2014. This is a highly positive sign, as it demonstrates that innovation is providing real value to companies and that this kind of investment has been productive.

“Every year, the number of brands that call for innovation is growing, because they see the results it brings. They’re bringing resources from other large partners, such as television, into these projects, which offers the potential to create a greater impact.” — Senior Manager, Food Manufacturer

How much did your area invest in innovation in 2014?

Unfortunately, there are also companies that, perhaps due to lack of experience or a previous negative experience, will not invest in innovation or will reduce that investment. Although they are a minority, we think they continue to constitute a fairly high percentage (from 20% to 31%), considering the types of organizations we surveyed. We believe that with more experience, more knowledge about innovation and more pressure to innovate, this percentage will shrink.

Still, the expectation for this year is to increase investment in innovation.

> 14%We will not invest in 2015

> 18%We will invest less in 2015 than we invested in 2014

> 15%We will not invest in 2015

> 16%We will invest less in 2015 than we invested in 2014

> 15%We will invest the same in 2015 as in 2014

> 54%We will invest more of our budget in 2015 than we invested in 2014

> 10%We will invest the same in 2015 as in 2014

> 58%We will invest more of our budget in 2015 than we invested in 2014

<$100 million $100-$500 million

The State of Innovation in Organizations 2015 (2nd Study) 71

“Considering the pressure that this sector faces to innovate, the investments we’ll be making to implement innovation projects in the next two years will increase tenfold. On the other hand, I’m not sure how we’ll justify our existence to the market.” — CEO, Financial Services

> 12%We will not invest in 2015

> 15%We will invest less in 2015 than we invested in 2014

> 5%We will not invest in 2015

> 16%We will invest less in 2015 than we invested in 2014

> 27%We will invest the same in 2015 as in 2014

> 52%We will invest more of our budget in 2015 than we invested in 2014

> 27%We will invest the same in 2015 as in 2014

> 46%We will invest more of our budget in 2015 than we invested in 2014

$500 million to $1 billion >$1 billion

72 INSITUM

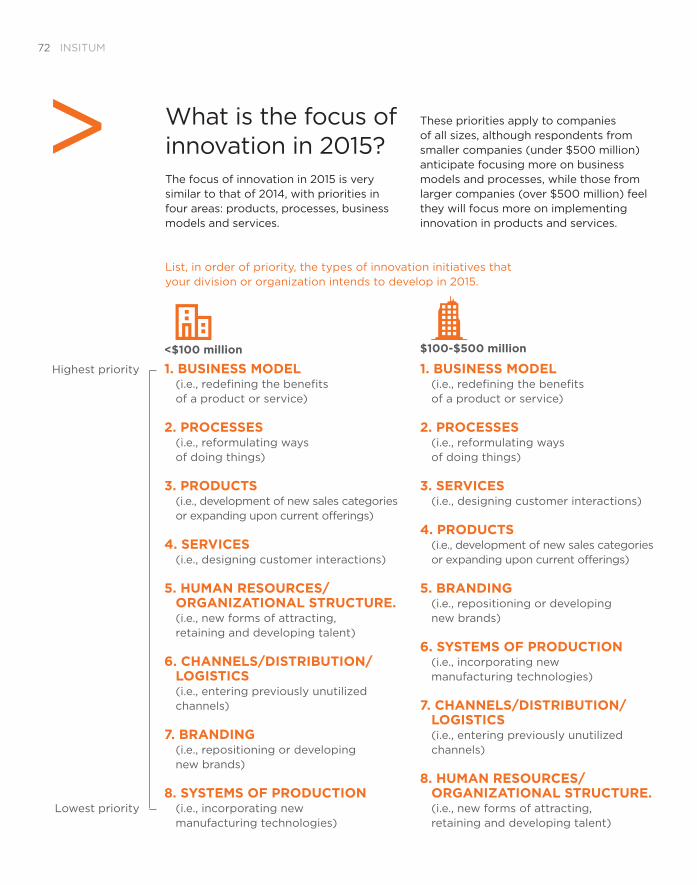

What is the focus of innovation in 2015?The focus of innovation in 2015 is very similar to that of 2014, with priorities in four areas: products, processes, business models and services.

List, in order of priority, the types of innovation initiatives that your division or organization intends to develop in 2015.

These priorities apply to companies of all sizes, although respondents from smaller companies (under $500 million) anticipate focusing more on business models and processes, while those from larger companies (over $500 million) feel they will focus more on implementing innovation in products and services.

1. BUSINESS MODEL (i.e., redefining the benefits of a product or service)

2. PROCESSES (i.e., reformulating ways of doing things)

3. PRODUCTS (i.e., development of new sales categories or expanding upon current offerings)

4. SERVICES (i.e., designing customer interactions)

5. HUMAN RESOURCES/ORGANIZATIONAL STRUCTURE.(i.e., new forms of attracting, retaining and developing talent)

6. CHANNELS/DISTRIBUTION/LOGISTICS (i.e., entering previously unutilized channels)

7. BRANDING (i.e., repositioning or developing new brands)

8. SYSTEMS OF PRODUCTION (i.e., incorporating new manufacturing technologies)

1. BUSINESS MODEL (i.e., redefining the benefits of a product or service)

2. PROCESSES (i.e., reformulating ways of doing things)

3. SERVICES (i.e., designing customer interactions)

4. PRODUCTS (i.e., development of new sales categories or expanding upon current offerings)

5. BRANDING (i.e., repositioning or developing new brands)

6. SYSTEMS OF PRODUCTION (i.e., incorporating new manufacturing technologies)

7. CHANNELS/DISTRIBUTION/LOGISTICS (i.e., entering previously unutilized channels)

8. HUMAN RESOURCES/ORGANIZATIONAL STRUCTURE.(i.e., new forms of attracting, retaining and developing talent)

<$100 million

Highest priority

Lowest priority

$100-$500 million

The State of Innovation in Organizations 2015 (2nd Study) 73

1. PROCESSES (i.e., reformulating ways of doing things)

2. PRODUCTS (i.e., development of new sales categories or expanding upon current offerings)

3. SERVICES (i.e., designing customer interactions)

4. BUSINESS MODEL (i.e., redefining the benefits of a product or service)

5. SYSTEMS OF PRODUCTION (i.e., incorporating new manufacturing technologies)

6. CHANNELS/DISTRIBUTION/LOGISTICS (i.e., entering previously unutilized channels)

7. HUMAN RESOURCES/ORGANIZATIONAL STRUCTURE.(i.e., new forms of attracting, retaining and developing talent)

8. BRANDING (i.e., repositioning or developing new brands)

1. PRODUCTS (i.e., development of new sales categories or expanding upon current offerings)

2. SERVICES (i.e., designing customer interactions)

3. BUSINESS MODEL (i.e., redefining the benefits of a product or service)

4. PROCESSES (i.e., reformulating ways of doing things)

5. CHANNELS/DISTRIBUTION/LOGISTICS (i.e., entering previously unutilized channels)

6. HUMAN RESOURCES/ORGANIZATIONAL STRUCTURE.(i.e., new forms of attracting, retaining and developing talent)

7. SYSTEMS OF PRODUCTION (i.e., incorporating new manufacturing technologies)

8. BRANDING (i.e., repositioning or developing new brands)

The innovation priorities for all types of organizations in 2015 lie in four primary areas: products, processes, business models and services.

$500 million to $1 billion >$1 billion

74 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 75

What needs to be done to improve our capacity for innovation?All organizations we spoke with aspire to improve their capacity for innovation. Some have an optimistic vision, while others are more cautious or guarded — but what they all have in common is that there are many things they can do to improve their innovation capacity. In this section, we share some of these possibilities we hope will serve as a checklist to inspire solutions applicable to your own organization.

76 INSITUM

How can organizations improve their capacity for innovation?We know that organizations have a long way to go in implementing innovation, but, after all, the path is made by walking — and there are always ways to yield an immediate effect. The individuals who participated in our survey shared hundreds of ideas for improving the innovation capacity of organizations. These can be grouped into nine categories:

The State of Innovation in Organizations 2015 (2nd Study) 77

If you could implement one initiative to improve the innovation capacity of your company, which would you choose?

STRATEGY> Have a strategy, a clear and coherent

vision for innovation > Understand which types of initiatives

are important and understand where opportunities lie

“It’s essential to have alignment between the work of upper-level management and the collaborator base… Everyone needs to speak the same language.”

STRUCTURE> Establish a multidisciplinary innovation

committee> Reassign responsibilities and priorities

(e.g., dedicate time to experimentation)“Create a division or position that helps to implement this process, yet one that is independent from operations and is not a marketing or technology division.”

COLLABORATION> Foster teamwork, carry out projects that

encourage collaboration among areas> Involve people of various levels of

seniority in initiatives“An idea and collaboration guidelines should come from the top, or else people won’t act.”

INVOLVE TOP MANAGEMENT’> Involve leaders such that they support

these types of projects; reposition innovation as an investment, not an expense, such that innovation has support from above.

“Everything starts with the CEO’s vision. If those at the top believe in innovation and act accordingly, it can’t work. Companies need to orient themselves towards innovation and this must come from the top.”

INCENTIVES> Provide material or social incentives

for people to take initiative and interest in participating

> Document and recognize errors and lessons learned

AGILITY> Increase the speed of responses and

decisions, reduce bureaucracy and adopt lean processes

> Learn to take more controlled risks in sync with other areas or external collaborators

“Every step we take is slow, because everything needs to be evaluated, supervised and accepted by everyone. A startup doesn’t work like this!”

INVESTMENT> Find new ways to finance projects using

internal or external resources> Increase budgetary allocations or reallocate

from lower-priority areas“We don’t have the budget and I doubt we will in the short term.”

TRAINING> Invest in advanced courses from qualified,

expert providers that do not simply “teach,” but rather “train”

> Devote more resources to training that allows for the introduction of outside ideas

“It’s very difficult to find leaders with the experience that a strategic position requires.”

CULTURE> Change the traditional mentality of

leaders or those with most power in the organization

> Foster experimentation, lean practices, design thinking, “intrapreneurship,” “Startup Weekend” and other practices

“When you’re in your comfort zone, it’s very difficult to step out of it and see which changes to make.”

78 INSITUM

The State of Innovation in Organizations 2015 (2nd Study) 79

Conclusions

80 INSITUM

EXPERTISE IS BEING DEVELOPED, BUT IT IS STILL IN ITS EARLY PHASES AND MUCH REMAINS TO BE DONE.

> In relation to the previous year, we have noted a significant increase in the level of knowledge about the function of innovation, but this is only visible in more mature organizations. There are still many novice organizations with little experience that are reticent to innovate. For these organizations, there is still a great deal of ground to cover.

PROCESSES REMAIN TOO FORMAL TO BE CONDUCIVE TO INNOVATION.