inox leisure 28-sep-2015 - sharekhan leisure.pdfeps (rs) 2.2 8.0 11.4 14.8 per (x) 100.3 27.3 19.2...

TRANSCRIPT

September 28, 2015Visit us at www.sharekhan.com

INOX Leisure Reco: Buy

Poised to script a blockbuster CMP: Rs219

Company details

Price target: Rs307

Market cap: Rs2,112 cr

52-week high/low: Rs270/145

NSE volume: 2.4 lakh(No of shares)

BSE code: 532706

NSE code: INOXLEISUR

Sharekhan code: INOXLEISUR

Free float: 5.0 cr(No of shares)

Price performance

(%) 1m 3m 6m 12m

Absolute 2.1 23.8 35.7 22.0

Relative 1.5 32.1 46.2 24.4to Sensex

Price chart

Shareholding pattern

Key points

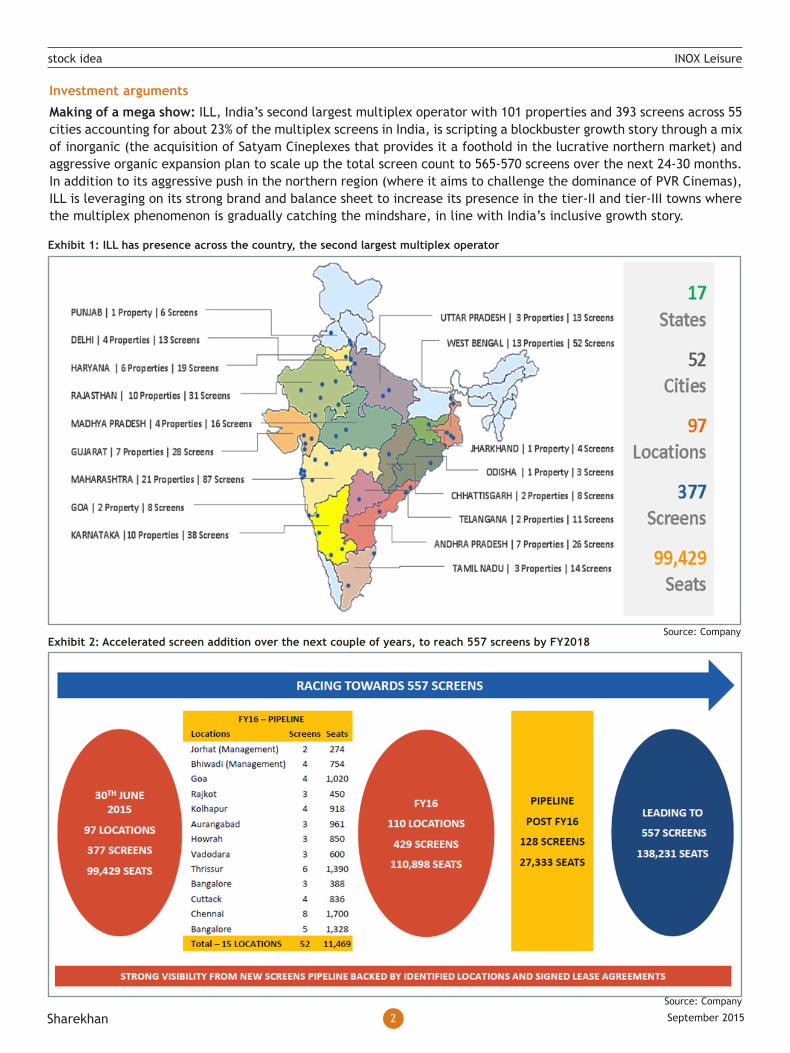

Making of a mega show: INOX Leisure Ltd (ILL), India’s second largest multiplexoperator with 101 properties and 393 screens across 55 cities accounting for about23% of the multiplex screens in India, is scripting a blockbuster growth story througha mix of inorganic (acquisition of Satyam Cineplexes that provides it a foothold inthe lucrative northern market) and aggressive organic expansion plan to scale upthe total screen count to 565-570 screens over the next 24-30 months. In additionto its aggressive push in the northern region (where it aims to challenge thedominance of PVR Cinemas), ILL is leveraging on its strong brand and balance sheetto increase its presence in tier-II and tier-III towns where the multiplex phenomenonis gradually catching the mindshare, in line with India’s inclusive growth story.

Top-class casting and script in place: The ILL mega show is supported by an improvingcontent quality in the Indian mainstream and regional cinema with its movies regularlyhitting the Rs100-crore or Rs200-crore box-office collection mark. The acceptance ofHollywood movies has also provided another source of quality saleable content formultiplexes not just in metros but across cities in the country. The economic conditionsare also turning favourable to support a robust uptick in urban discretionary spending,given the sharp moderation in inflation and a steady job market. The urban leisureconsumption would also get a boost from the expected 25-30% hike in salaries of thecentral and state government employees with the implementation of the SeventhPay Commission’s recommendation.

Recommend Buy with price target of Rs307: ILL’s revenues and net income areexpected to grow at a CAGR of 19% and 35.5% respectively over FY2016-18 led bystrong box-office revenues (at a 19% CAGR), higher F&B revenues (at a 23% CAGR)and advertising revenues (at a 20% CAGR) over FY2016-18. Further, a healthy balancesheet with a 0.3 debt/equity ratio and treasury shares of 4.3 crore shares providestrength to drive the inorganic growth activities in the coming years. At the currentmarket price of Rs219, the stock trades at EV/EBITDA of 11x, 9x and 7.4x FY2016E,FY2017E and FY2018E earnings respectively. We believe ILL with its strong brand andextended reach is well poised to leverage the opportunity in India’s under-penetratedmultiplex sector. We initiate coverage on ILL with a price target of Rs307, based on9x FY2018E EV/EBITDA.

Key risk: (1) ILL has accelerated its expansion plan over the next two to threeyears and any delay in the execution of the plan is a risk; and (2) any pause in theinflow of quality movie content will affect the earnings of the company.

Valuation

Particulars FY2015* FY2016E FY2017E FY2018ETotal revenues (Rs cr) 1,016.8 1,374.3 1,665.2 1,947.3EBITDA margin (%) 12.1 14.7 15.1 15.4Net profit (Rs cr) 20.0 73.7 104.5 135.4EPS (Rs) 2.2 8.0 11.4 14.8PER (x) 100.3 27.3 19.2 14.8P/BV (x) 3.0 2.7 2.4 2.0EV/EBITDA (x) 18.7 11.3 9.0 7.4RoE (%) 3.0 9.8 12.2 13.7RoCE (%) 6.9 13.3 15.7 17.6*FY2015 includes consolidation of Satyam Cineplexes, which will affect the overall profitability Source: Company and Sharekhan Research

2 September 2015Sharekhan

stock idea INOX Leisure

Investment arguments

Making of a mega show: ILL, India’s second largest multiplex operator with 101 properties and 393 screens across 55cities accounting for about 23% of the multiplex screens in India, is scripting a blockbuster growth story through a mixof inorganic (the acquisition of Satyam Cineplexes that provides it a foothold in the lucrative northern market) andaggressive organic expansion plan to scale up the total screen count to 565-570 screens over the next 24-30 months.In addition to its aggressive push in the northern region (where it aims to challenge the dominance of PVR Cinemas),ILL is leveraging on its strong brand and balance sheet to increase its presence in the tier-II and tier-III towns wherethe multiplex phenomenon is gradually catching the mindshare, in line with India’s inclusive growth story.

Source: Company

Exhibit 1: ILL has presence across the country, the second largest multiplex operator

Exhibit 2: Accelerated screen addition over the next couple of years, to reach 557 screens by FY2018

Source: Company

3 September 2015Sharekhan

stock idea INOX Leisure

Top-class casting and script in place: ILL’s mega show is supported by an improving content quality in the Indianmainstream and regional cinema with movies regularly hitting the Rs100-crore or Rs200-crore box-office collectionmark. The acceptance of Hollywood movies has also provided another source of quality saleable content for multiplexesnot just in metros but across cities in the country.

Growing acceptance of quality content across markets

• From one movie in 2008, “Ghajini”, which crossed the Rs100-crore mark in 18 days, there were nine moviesin 2014 that made it to +Rs100-crore club.

• It took “Bajrangi Bhaijaan” just three days to reach the Rs100-crore mark as compared with the 18 daystaken by “Ghajini” in 2008.

• Even regional movies like “Baahubali” (a Telugu movie dubbed in Hindi) crossed the Rs100-crore mark in2015.

• Hollywood movie “Furious 7” garnered Rs104 crore in the domestic box office while other Hollywood movieslike “Avatar” (2009; Rs145 crore), “2012” (2009; Rs94 crore) and “Life of Pi” (2012; Rs80 crore) were alsowidely accepted in the domestic box office.

• A higher number of screen releases from 1,600 screen releases of “Dabaang” in 2010 to more than 4,500screen releases for “Bajrangi Bhaijaan” in 2015 also helped the latter to reach the Rs100-crore mark in justthree days, the fastest in Indian film history.

Source: Industry reports

Exhibit 3: Retail attractiveness of tier-II and tier-III cities

Source: Industry reports

Exhibit 4: Retail attractiveness of tier-I cities

Multiplex phenomenon is gradually catching the mindshare and wallet share of tier-II and tier-III towns

Exhibit 5: Screen additions by major multiplex chains in 2014

Cinema Number of Number ofproperties screens Locations

Inox Leisure 9 31 Udupi, Jalgaon, Bhilwara, Vizag, Faridabad, Gurgaon, Noida, Delhi, Kolkata

PVR Cinemas 5 22 Hubli, Ahmedabad, Mangalore, Bhopal, Jalandhar

Cinepolis 3 26 Vijayawada, Vadodara, Thane

Carnival Cinemas 1 3 Delhi

K Sera Sera Miniplex 3 6 Abohar, Nawanshahr, Hoshiarpur

Mukta Arts 4 11 Sangli, Aurangabad, Bhopal, Hyderabad

Priya Entertainment 1 3 Haldia

Total 26 102Source: Industry reports

4 September 2015Sharekhan

stock idea INOX Leisure

Exhibit 6: Rs100-crore break-up year-wise

Year No. of movies Highest (cr)

2008 1 114.0

2009 1 202.5

2010 2 138.9

2011 5 148.9

2012 9 198.8

2013 8 284.3

2014 9 340.8

2015 4 320.3

Source: Industry reports

A strong content pipeline

Exhibit 7: Upcoming Bollywood movies in 2015

Release date Film name Star cast2-Oct-15 Singh is Bling Akshay Kumar, Kareena Kapoor Khan, Amy Jackson9-Oct-15 Jazbaa Aishwarya Rai Bachchan, Irrfan Khan22-Oct-15 Shaandaar Shahid Kapoor, Alia Bhatt12-Nov-15 Prem Ratan Dhan Payo Salman Khan, Sonam Kapoor, Neil Nitin Mukesh27-Nov-15 Tamasha Ranbir Kapoor, Deepika Padukone4-Dec-15 Wazir Amitabh Bachchan, Farhan Akhtar18-Dec-15 Dilwale Shah Rukh Khan, Kajol, Varun Dhawan, Kriti Sanon18-Dec-15 Bajirao Mastani Ranveer Singh, Priyanka Chopra, Deepika Padukone

Source: Industry reports

Exhibit 8: Upcoming Bollywood movies in 2016

Release date Film name Star cast22-Jan-16 Airlift Akshay Kumar5-Feb-16 Rocky Handsome John Abraham12-Feb-16 Fitoor Katrina Kaif, Aditya Roy Kapur4-Mar-16 Jai GangaaJal Priyanka Chopra18-Mar-16 Kapoor & Sons Sidharth Malhotra, Alia Bhatt15-Apr-16 Fan Shah Rukh Khan29-Apr-16 Baaghi Tiger Shroff, Shraddha Kapoor13-May-16 Azhar Emraan Hashmi3-Jun-16 Jagga Jassos Ranbir Kapoor, Katrina Kaif and Govinda3-Jun-16 Housefull 3 Akshay Kumar, Abhishek Bachchan, Riteish Deshmukh12-Aug-16 Mohenjo Daro Hrithik Roshan12-Aug-16 Rustom Akshay Kumar12-Aug-16 Baadshaho Ajay Devgan

Source: Industry reports

Exhibit 10: Upcoming Hollywood movies in 2015

Release date Film name25-Sep-15 The Intern2-Oct-15 The Martian2-Oct-15 Legend9-Oct-15 Pan16-Oct-15 Crimson Peak16-Oct-15 Bridge of Spies23-Oct-15 The Last Witch Hunter6-Nov-15 Spectre20-Nov-15 The Hunger Games: Mockingjay - Part 225-Nov-15 The Good Dinosaur18-Dec-15 Star Wars: The Force Awakens

Source: Industry reports

Exhibit 9: Bollywood movies released in Q2FY2015

Release date Film name Star cast3-Jul-15 Guddu Rangeela Arshad Warsi, Amit Sadh10-Jul-15 Baahubali Prabhas, Rana Daggubati, Tamannaah17-Jul-15 Bajrangi Bhaijaan Salman Khan, Kareena Kapoor Khan31-Jul-15 Drishyam Ajay Devgn, Tabu, Shriya Saran7-Aug-15 Bangistan Riteish Deshmukh, Pulkit Samrat14-Aug-15 Brothers Akshay Kumar, Sidharth Malhotra21-Aug-15 All Is Well Abhishek Bachchan, Asin21-Aug-15 Manjhi The Mountain Man Nawazuddin Siddiqui, Radhika Apte28-Aug-15 Phantom Saif Ali Khan, Katrina Kaif28-Aug-15 Baankey Ki Crazy Baraat Sanjay Mishra, Rajpal Yadav4-Sep-15 Welcome Back John Abraham, Shruti Haasan11-Sep-15 Hero Sooraj Pancholi, Athiya Shetty18-Sep-15 Katti Batti Imran Khan, Kangna Ranaut

Source: Industry reports

5 September 2015Sharekhan

stock idea INOX Leisure

Overall consumption capacity set to improve, led by lower inflation and Seventh Pay Commission hike:

The economic conditions are also turning favourable to support a robust uptick in urban discretionary spending, giventhe sharp moderation in inflation and steady job market. The urban leisure consumption would also get a boost fromthe expected 25-30% hike in the salaries of the central and state government employees with the implementation ofthe Seventh Pay Commission’s recommendation.

Seventh Pay Commission hike will help improve the wallet of Indian government employees

• The Seventh Pay Commission was set up by the government to revise the remuneration of about 2.5 crorecentral and state government employees.

• The pay/allowances could rise by 25-30% following the implementation of the Seventh Pay Commission’srecommendation.

• The increase in bonus payments and pay/allowances would cumulatively imply spending of Rs2,60,000crore, which is to the tune of 1.5-1.7% of the gross domestic product in FY2017.

Source: Industry reports

Exhibit 11: Around 2.5 crore people from central and state government will benefit from the implementation of the recommendationof the Seventh Pay Commission which will lead to an inflow of around Rs2,600 billion by FY2017 and drive the discretionary spending.

Exhibit 12: The India consumption story

Source: Industry reports

*Middle class segment expected togrow much faster and form around 59%of the total consumption

India is well placed to have higherdisposal income growth as comparedwith other emerging markets

Exhibit 13: India’s personal disposable income (PDI) growthcomparison with other emerging markets

Source: Industry reports

*

6 September 2015Sharekhan

stock idea INOX Leisure

ILL financials

Revenues (FY2015)*

Box-office collectionrevenues F&B revenues

Advertisementrevenues Exhibition Cost Cost of F&B Others

1. Gross box-officecollection (GBOC) is66.2% of totalrevenues

2. Entertainment taxas % of GBOC is18.0%

3. Net box-officecollection is 62%(includingdistributers’ share)

1. F&B revenues are18.8% of totalrevenues

2. No. of patronsspending on F&Bwas 3.5 croreFY2015

3. Spend per head isRs55

1.Advertisementrevenues are 8.0%of total revenues

2.As of FY2015 totalno. of screens is372

3.Advertisementrevenue per screenis Rs2.3 million

1. Exhibition cost as %of GBOC is 37%

2. Distributor’s shareas % of exhibitioncost is 97%

3. Distributor’s shareas % of GBOC is35.9%

1. Cost of F&B as % ofF&B revenues is23%

2. Cost per head isRs55

3. F&B margin is 77%

1.Rent expenses is17% as % of totalrevenues and 25%as % of totalexpenses

2. Employee cost is 6%as % of totalrevenues and 11%as % total expenses

3.Others expenses is23% as % of totalrevenues and 36%as % of totalexpenses

Expenses (FY2015)*

Total revenue is Rs1,016.8 crore Total cost Rs644.7 crore

OPM 12.1%

Financial positives

* FY2015 includes consolidation of Satyam Cineplexes, which will affect the overall profitability

Exhibit 14: Revenues to grow by 24% CAGR over FY2015-18

Key segmental revenues FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E CAGRFY15-18E

Gross box-office collection 188 254 313 559 597 673 928 1,124 1,306 24.7

Food and beverages 42 54 71 142 162 191 282 351 424 30.4

Advertising revenues 13 14 18 32 50 81 105 126 151 23.0

Total revenues 253.6 337.3 418.7 765.3 868.8 1,016.8 1,374.3 1,665.2 1,947.3 24.2

Source: Company and Sharekhan Research

Exhibit 15: Gross box-office revenue trend

Source: Company and Sharekhan Research

Food and beverages to grow at a CAGR of 30.4% overFY2015-2018

Factors to drive growth

• We expect the food and beverage (F&B) business to growat a 30.4% CAGR over FY2015-18, led by the company’s

Gross box-office collection to deliver 24.7% CAGR overFY2015-18

Factors to drive growth

• We expect strong screen addition over the next 24-30months, with the screen count reaching 577 screens by2018 (management targets). We estimate the companywould have 528 screens by FY2018 versus the currentscreen count of 393 screens. Footfalls are expected toincrease at a 21% compounded annual growth rate (CAGR)over FY2015-18 to reach 7.2 crore footfalls by FY2018.

• We have built a 3.9% CAGR in ATP, reaching Rs184 byFY2018, led by an increasing contribution of theHollywood movies (accounting for around 15% of thetotal revenues) coupled with a higher number of 3Dmovie releases, which command a 15-20% premiumover the regular movies.

Source: Company and Sharekhan Research

7 September 2015Sharekhan

stock idea INOX Leisure

increasing thrust on stepping up growth in the segment.The management has taken initiatives like changing themenu based on a movie, keeping in mind the taste budsof guests; serving a larger menu spread; and providingon-seat delivery. The spending per head (SPH) hasincreased to Rs55 in FY2015 from Rs41 in FY2011.

• The company also provides a choice of international,Indian and city-centric special cuisines. In order to drivegrowth in the F&B business and to speed up thetransaction time to serve more guests, ILL has investedin technology in concession counters (REFUEL). Guestsstanding in long queues can place their orders with INOXrepresentatives who carry the menu on their tablets.These tablets are used as Queue Busters for taking ordersfrom guests standing in long queues. This initiative speedsup the transaction time, thereby serving more guests.

Exhibit 16: Food and beverage revenue trend

Source: Company and Sharekhan Research

Advertising revenues to grow at a CAGR of 23% overFY2015-18

Factors to drive growth

• As per a FICCI-KPMG report on the Indian media andentertainment industry in 2015, cinema advertising is aRs490-crore market, projected to reach Rs1,382 crore by2019. ILL’s advertisement revenue per screen has improvedfrom Rs0.8 million in FY2011 to Rs2.3 million in FY2015.

• The company is taking several steps to improve itsadvertising revenues including focusing on high-valueand long-term deals, innovative transaction structures,expansion of the breadth and depth of marketingteams, and optimisation of the advertisement rates.

• An increased screen presence gives multiplexes higherbargaining power with advertisers and drives higheradvertisement and other operating revenues perscreen. With the screen count reaching close to 530screens by FY2018, we expect further acceleration inthe advertising growth and estimate that ILL’sadvertising revenue per screen will increase to Rs2.9million by FY2018 from Rs2.3 million in FY2015.

Exhibit 17: Advertising revenue trend

Source: Company and Sharekhan Research

Exhibit 18: OPM to improve by 340BPS over FY2015-18E

Exhibit 19: Return ratios set to improve

Exhibit 20: Comfortable debt/equity ratio augurs well for growthacceleration

Source: Company and Sharekhan Research

Source: Company and Sharekhan Research

Source: Company and Sharekhan Research

8 September 2015Sharekhan

stock idea INOX Leisure

Exhibit 23: Total footfalls for INOX (in mn)

Source: Company and Sharekhan Research

Exhibit 24: Spend per head for INOX

Source: Company and Sharekhan Research

(in

Rs)

Exhibit 22: Average ticket price for INOX

Source: Company and Sharekhan Research

(in

Rs)

Exhibit 21: Number of screens added during the year

Source: Company and Sharekhan Research

(no.

of

scre

en)

(in

mn)

Operating metric charts

Exhibit 25: Strong brand partnerships

Source: Company

9 September 2015Sharekhan

stock idea INOX Leisure

Exhibit 31: Geographical mix of seats for PVR Cinemas and ILL in Q1FY16

Exhibit 32: Trend in debt/equity in PVR Cinemas and ILL

Exhibit 27: Screen addition trend PVR Cinemas vs ILL

Source: Company and Sharekhan Research

(no.

of

scre

en a

dded

)

Exhibit 29: Trends in SPH in PVR Cinemas and ILL

(in

Rs)

Exhibit 28: Trends in ATP in PVR Cinemas and ILL

(in

Rs)

Exhibit 30: Advertising revenues per screen (Rs mn)

(in

mn)

PVR Cinemas vs ILL

Exhibit 26: Metric comparison at the end of Q1FY2016

Operating metrics PVR Cinemas ILLCities 106 52Screens 474 377Seats 111,278 99,429Occupancy 38% 33%Admits (mn) 19.0 14.5ATP (INR) 183 165SPH (INR) 74 59SPH/ATP 40% 36%Ad revenues/screen (Rs cr) 0.36 0.05Gross revenues (Rs cr) 486 349EBIDTA (Rs cr) 113 66EBIDTA margin 23.1% 18.8%PAT (Rs) 61.7 25.26PAT margin 12.7% 7.24%EBIDTA/seat (Rs) 10,110 6,594EBIDTA/footfall (Rs) 59.2 45.2

Source: Company & Sharekhan Research

Source: Company and Sharekhan Research

Source: Company and Sharekhan Research

Source: Company and Sharekhan Research

Source: Company and Sharekhan Research

Source: Company and Sharekhan Research

10 September 2015Sharekhan

stock idea INOX Leisure

Valuation

Recommend Buy with a price target of Rs307: ILL’s revenues and net income are expected to grow at a CAGR of 19%and 35.5% respectively over FY2016-18 led by strong box-office revenues (at a 19% CAGR), higher F&B revenues (ata 23% CAGR) and advertising revenues (at a 20% CAGR) over FY2016-18. Further, a healthy balance sheet with a 0.3debt/equity ratio and treasury shares of 4.3 crore shares provide strength to drive inorganic growth activities in thecoming years. At the current market price of Rs219, the stock trades at enterprise value (EV)/earnings beforeinterest, tax, depreciation and amortisation (EBITDA) of 11x, 9x and 7.4x FY2016E, FY2017E and FY2018E earningsrespectively. We believe ILL with its strong brand and extended reach is well placed to leverage the opportunity inIndia’s under-penetrated multiplex sector. We initiate coverage on ILL with a price target of Rs307, based on 9xFY2018E EV/EBITDA.

50 x

40 x

30 x

20 x

10 x

Exhibit 34: PER band

13 x

10 x

7 x

5 x

3 x

Exhibit 35: EV/EBITDA band

Exhibit 33: Peer comparison

Domestic P/E (x) P/BV (x) EV/EBITDA (x) RoE (%)

Peer FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E

INOX 27.3 19.2 14.8 2.7 2.4 2.0 11.3 9.0 7.4 9.8 12.2 13.7

PVR 30.2 23.1 18.4 5.5 4.7 3.8 13.1 11.0 9.3 20.3 20.4 20.1

Source: Bloomberg and Sharekhan Research

International P/E (x) P/BV (x) EV/EBITDA (x) RoE (%)

Peer CY15E CY16E CY17E CY15E CY16E CY17E CY15E CY16E CY17E CY15E CY16E CY17E

Regal Entertainment Group 16.5 15.2 13.4 NM NM NM 8.1 7.7 6.9 NM NM NM

Major Cineplex Group PCL 22.3 19.3 16.8 4.3 4.1 3.9 12.0 10.7 9.9 20.3 22.4 23.8

Cineworld Group PLC 19.8 18.0 16.3 2.7 2.5 2.2 11.5 10.6 9.7 13.8 14.2 14.7

Source: Bloomberg

Source: Bloomberg Source: Bloomberg

11 September 2015Sharekhan

stock idea INOX Leisure

Profit & Loss account (consolidated) Rs cr

Particulars FY14 FY15 FY16E FY17E FY18E

Total operating income 868.8 1,016.8 1,374.3 1,665.2 1,947.3

% Growth 13.5 17.0 35.2 21.2 16.9

Total expenses 523.4 644.7 830.8 994.6 1,160.0

% Growth 14.4 23.2 28.9 19.7 16.6

Operating profit 121.9 122.8 202.0 251.3 300.3

% Growth 24.4 0.7 64.6 24.4 19.5

Other income 9.0 8.3 9.5 9.5 9.5

Interest 27.6 38.6 29.6 23.0 19.8

Depreciation 50.7 75.8 83.6 94.6 104.5

Expectional item 0.4 0.6 - - -

Profit before tax 52.2 16.0 98.3 143.2 185.5

% Growth 77.7 (69.3) 514.5 45.6 29.6

Tax 15.3 (4.1) 24.6 38.7 50.1

Net profit 36.9 20.0 73.7 104.5 135.4

% Growth 100.2 (45.7) 267.8 41.7 29.6

FinancialsCash flow statement (consolidated) Rs cr

Particulars FY14 FY15 FY16E FY17E FY18E

PAT 36.9 20.0 73.7 104.5 135.4

Depreciation 50.7 75.8 83.6 94.6 104.5

Change in WC 1.8 (54.7) (16.5) (57.3) (68.2)

Operating CF 89.4 41.2 140.9 141.9 171.8Capex (90.3) (274.5) (128.8) (115.0) (124.2)

Investing CF (124.9) (274.5) (128.8) (115.0) (124.2)Dividends - - - - -

Debt (38.8) (27.0) 25.0 (20.0) -

Equity 64.0 265.2 0.0 0.0 -

Deferred tax liabilities 6.2 (4.7) - - -

Investments (2.6) (3.4) - - -

Financing CF 28.7 230.2 25.0 (20.0) -Net change (6.8) (3.1) 37.1 6.9 47.6Opening cash 23.3 16.6 13.4 50.5 57.4Closing cash 16.6 13.4 50.5 57.4 104.9

Key ratios (consolidated)

Particulars FY14 FY15 FY16E FY17E FY18E

Margin ratio (%)Operating profit margin 14.0 12.1 14.7 15.1 15.4

PBIT margin 9.2 5.4 9.3 10.0 10.5

PBT margin 6.0 1.6 7.2 8.6 9.5

PAT margin 4.3 2.0 5.4 6.3 7.0

Growth ratio (%)Revenues 13.5 17.0 35.2 21.2 16.9

Operating profit 24.4 0.7 64.6 24.4 19.5

Net profit 100.2 (45.7) 267.8 41.7 29.6

Return ratio (%)RoCE 12.4 6.9 13.3 15.7 17.6

RoNW 9.4 3.0 9.8 12.2 13.7

Total debt/equity 0.6 0.3 0.3 0.3 0.2

Turnover ratioAverage collection period (days) 15 17 16 16 16

Average stock velocity (days) 54 59 58 58 58

Average payment period (days) 50 50 50 45 40

Per share (Rs)Earning per share 4.0 2.2 8.0 11.4 14.8

Cash profit 9.5 10.4 17.1 21.7 26.1

Book value 42.6 73.7 81.7 93.1 107.8

Valuation ratios (x)P/E 54.4 100.3 27.3 19.2 14.8

EV/EBITDA 19.1 18.7 11.3 9.0 7.4

EV/Sales 2.7 2.3 1.7 1.4 1.1

Mkt cap/Sales 2.4 2.1 1.5 1.3 1.1

P/ BV 5.1 3.0 2.7 2.4 2.0

Balance sheet (consolidated) Rs cr

Particulars FY14 FY15 FY16E FY17E FY18E

Equity cap 96.1 96.2 96.2 96.2 96.2

Reserves 444.4 612.7 686.4 791.0 926.4

Interest in Inox BenefitTrust, at cost (149.7) (32.7) (32.7) (32.7) (32.7)

Net worth 390.9 676.2 749.9 854.4 989.9

Borrowings 242.2 215.2 240.2 220.2 220.2

Deffered tax liab 29.0 24.3 24.3 24.3 24.3

Capital employed 662.1 915.7 1,014.5 1,099.0 1,234.4

Net block 634.7 668.1 713.3 733.6 753.4

Investments 3.7 7.1 7.1 7.1 7.1

Goodwill on consolidated - 165.2 165.2 165.2 165.2

Other Non current assets 2.3 4.0 4.0 4.0 4.0

Inventories 8.6 7.6 11.8 14.7 17.7

Sundry debtors 33.4 62.3 61.1 74.0 86.5

Cash and bank balance 16.6 13.4 50.5 57.4 104.9

Loans and advances 157.1 192.0 249.6 312.0 374.4

Other current assets 1.8 1.8 1.8 1.8 1.8

Sundry creditors 72.0 89.3 114.9 124.3 128.9

Other current liabilities 98.8 94.9 109.9 116.6 116.8

Provisions 25.2 21.6 24.9 29.8 34.8

NCA 23.7 75.3 128.8 193.0 308.7

Total Assets 662.1 915.7 1,014.4 1,099.0 1,234.4

Source: Company & Sharekhan Research

12 September 2015Sharekhan

stock idea INOX Leisure

Annexure

Company description

Inox Leisure Ltd (ILL) was incorporated as a public limited company on November 9, 1999. ILL is part of the INOXgroup, which is diversified across industrial gases, engineering plastics, refrigerants, chemicals, cryogenic engineering,renewable energy and entertainment sectors. The company is the second largest player in the multiplex space with amultiplex screen market share of 23%. It is behind PVR Cinemas, which has about 463 screens in its portfolio and amultiplex screen market share of about 27.2%.

Since the launch of its multiplex in Goa in CY2004, ILL is the venue for the prestigious International Film Festival ofIndia (IFFI) every year. Since its inception in CY1999, ILL has been active in exploring acquisitions and/or expansionopportunities on a continuous basis, with a view to consolidating its position in the multiplex industry. In CY2007,Calcutta Cinema Pvt Ltd, a multiplex cinema theatre company based in West Bengal, was merged with ILL.

In May CY2013, Fame India, another multiplex cinema theatre company having a nation-wide presence, was mergedwith it. In August 2014, ILL acquired a third multiplex chain, Satyam Cineplexes, thereby strengthening its presenceto become a significant player in the Indian multiplex space and redefine the movie going experience in India.

ILL along with Satyam Cineplexes currently operates 101 multiplexes and 393 screens in 52 cities, making it a trulypan-Indian multiplex chain. ILL will continue its expansion into cities like Jammu, Mangalore and Cuttack amongothers. The management intends to increase the screen count to about 557 screens and the seat count to 138,281seats across the country in FY2018.

Key management

Pavan Jain, chairman: Pavan Jain, chairman of the INOX group, is a chemical engineer from IIT, New Delhi andindustrialist with over 38 years of experience.

Vivek Jain, director: Vivek Jain has over 34 years of business experience. He is currently the managing director ofGujarat Fluorochemicals and has grown the company making it the country's largest manufacturer and exporter ofrefrigerant gases.

Deepak Asher, director: A commerce and law graduate, Deepak Asher is also a Fellow Member of the Institute ofChartered Accountants of India and an Associate Member of the Institute of Cost and Works Accountants of India. Hehas more than 25 years of experience in the fields of corporate finance and business strategy. Mr Asher is the presidentof the Multiplex Association of India and a member of the FICCI Entertainment Committee. In 2002, he won theTheatre World Newsmaker of the Year Award for his contribution to the multiplex sector.

Alok Tandon, CEO: As the chief executive officer (CEO) of ILL Mr Tandon is at the helm of ILL's expansion plans andconcentrates on strengthening the INOX brand on a national scale, making it the first choice in the business of cinemaexhibition in India. An engineer by qualification, he has been with ILL since its inception and has more than 25 yearsof varied work experience in companies such as Hoechst, ITC Welcome Group and the Oberoi group.

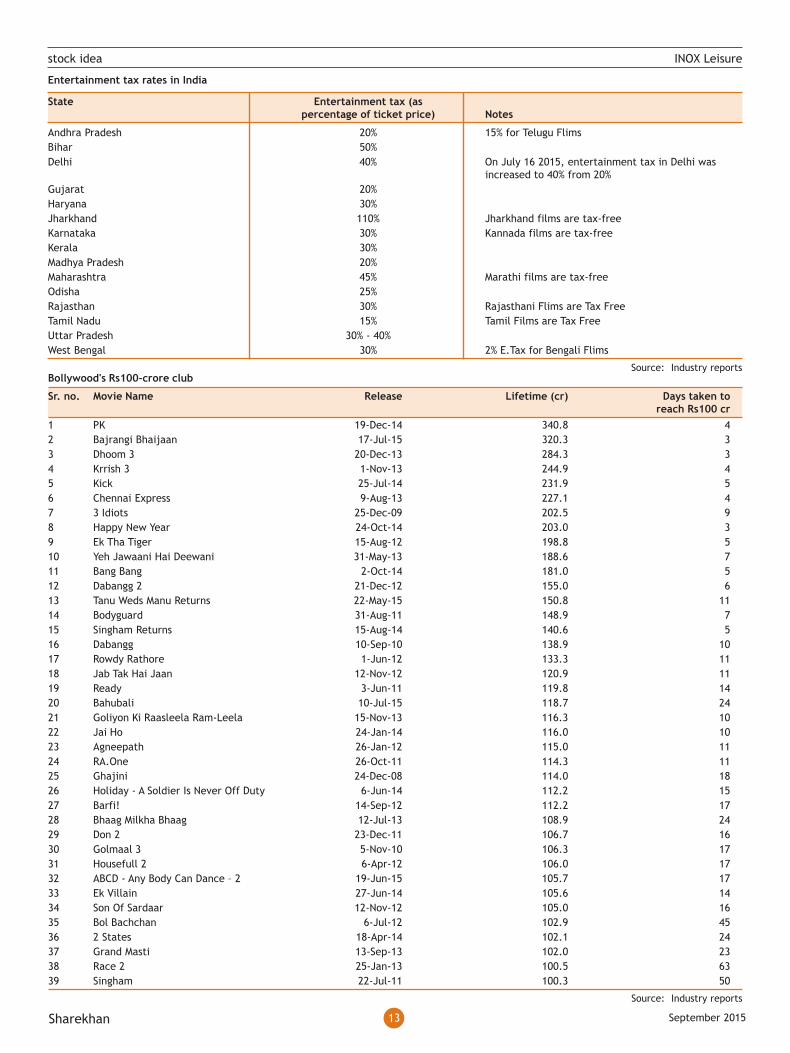

GST could be a big positive for the sector: The indirect tax structure for the entertainment sector is distorted. The overalltax implication is as high as 40-50% in some states, such as Maharashtra, Uttar Pradesh and Bihar. Subsuming of theentertainment tax with the Goods and Services Tax (GST) will help the industry spur growth. While the rate of the GST is notyet clear, the input tax credit will be available for set-off against the output tax liability, which will help reduce costs. TheILL management expects the margin to improve by 150-200 basis points (BPS) after the roll-out of the GST.

13 September 2015Sharekhan

stock idea INOX Leisure

Bollywood's Rs100-crore club

Sr. no. Movie Name Release Lifetime (cr) Days taken toreach Rs100 cr

1 PK 19-Dec-14 340.8 42 Bajrangi Bhaijaan 17-Jul-15 320.3 33 Dhoom 3 20-Dec-13 284.3 34 Krrish 3 1-Nov-13 244.9 45 Kick 25-Jul-14 231.9 56 Chennai Express 9-Aug-13 227.1 47 3 Idiots 25-Dec-09 202.5 98 Happy New Year 24-Oct-14 203.0 39 Ek Tha Tiger 15-Aug-12 198.8 510 Yeh Jawaani Hai Deewani 31-May-13 188.6 711 Bang Bang 2-Oct-14 181.0 512 Dabangg 2 21-Dec-12 155.0 613 Tanu Weds Manu Returns 22-May-15 150.8 1114 Bodyguard 31-Aug-11 148.9 715 Singham Returns 15-Aug-14 140.6 516 Dabangg 10-Sep-10 138.9 1017 Rowdy Rathore 1-Jun-12 133.3 1118 Jab Tak Hai Jaan 12-Nov-12 120.9 1119 Ready 3-Jun-11 119.8 1420 Bahubali 10-Jul-15 118.7 2421 Goliyon Ki Raasleela Ram-Leela 15-Nov-13 116.3 1022 Jai Ho 24-Jan-14 116.0 1023 Agneepath 26-Jan-12 115.0 1124 RA.One 26-Oct-11 114.3 1125 Ghajini 24-Dec-08 114.0 1826 Holiday - A Soldier Is Never Off Duty 6-Jun-14 112.2 1527 Barfi! 14-Sep-12 112.2 1728 Bhaag Milkha Bhaag 12-Jul-13 108.9 2429 Don 2 23-Dec-11 106.7 1630 Golmaal 3 5-Nov-10 106.3 1731 Housefull 2 6-Apr-12 106.0 1732 ABCD - Any Body Can Dance – 2 19-Jun-15 105.7 1733 Ek Villain 27-Jun-14 105.6 1434 Son Of Sardaar 12-Nov-12 105.0 1635 Bol Bachchan 6-Jul-12 102.9 4536 2 States 18-Apr-14 102.1 2437 Grand Masti 13-Sep-13 102.0 2338 Race 2 25-Jan-13 100.5 6339 Singham 22-Jul-11 100.3 50

Source: Industry reports

Entertainment tax rates in India

State Entertainment tax (aspercentage of ticket price) Notes

Andhra Pradesh 20% 15% for Telugu FlimsBihar 50%Delhi 40% On July 16 2015, entertainment tax in Delhi was

increased to 40% from 20%Gujarat 20%Haryana 30%Jharkhand 110% Jharkhand films are tax-freeKarnataka 30% Kannada films are tax-freeKerala 30%Madhya Pradesh 20%Maharashtra 45% Marathi films are tax-freeOdisha 25%Rajasthan 30% Rajasthani Flims are Tax FreeTamil Nadu 15% Tamil Films are Tax FreeUttar Pradesh 30% - 40%West Bengal 30% 2% E.Tax for Bengali Flims

Source: Industry reports

14 September 2015Sharekhan

stock idea INOX Leisure

For Private Circulation only

REGISTRATION DETAILS Regd Add: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station,Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Fax: 67481899; E-mail: [email protected]; Website: www.sharekhan.com;CIN: U99999MH1995PLC087498. Sharekhan Ltd.: SEBI Regn. Nos. BSE- INB/INF011073351 ; CD-INE011073351; NSE– INB/INF231073330 ; CD-INE231073330; MCXStock Exchange- INB/INF261073333 ; CD-INE261073330; DP-NSDL-IN-DP-NSDL-233-2003 ; CDSL-IN-DP-CDSL-271-2004 ; PMS-INP000000662 ; Mutual Fund-ARN20669 ; Commodity trading through Sharekhan Commodities Pvt. Ltd.: MCX-10080 ; (MCX/TCM/CORP/0425) ; NCDEX-00132 ; (NCDEX/TCM/CORP/0142) ;NCDEX SPOT-NCDEXSPOT/116/CO/11/20626; For any complaints email at [email protected] ; Disclaimer: Client should read the Risk Disclosure Documentissued by SEBI & relevant exchanges and Do’s & Don’ts by MCX & NCDEX and the T & C on www.sharekhan.com before investing.

DisclaimerThis document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This document may contain confidential and/or privileged material and is not for any type of circulation and anyreview, retransmission, or any other use is strictly prohibited. This document is subject to changes without prior notice. This document does not constitute an offer to sell or solicitation for the purchase or sale of any financial instrument or as an officialconfirmation of any transaction. Though disseminated to all customers who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy and completeness of the said data and hence it should not be relied upon as such.While we would endeavour to update the information herein on a reasonable basis, SHAREKHAN, its subsidiaries and associated companies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the informationcurrent. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investmentdecision. Recipients of this report should also be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The user assumes the entire risk of any use made of this information. Each recipientof this document should make such investigations as he deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult his ownadvisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of SHAREKHAN may have issued otherreports that are inconsistent with and reach different conclusion from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary tolaw, regulation or which would subject SHAREKHAN and affiliates to any registration or licencing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Personsin whose possession this document may come are required to inform themselves of and to observe such restriction. Either SHAREKHAN or its affiliates or its directors or employees/representatives/clients or their relatives may have position(s), make market, actas principal or engage in transactions of purchase or sell of securities, from time to time or may be materially interested in any of the securities or related securities referred to in this report and they may have used the information set forth herein beforepublication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involvedin, or related to, computing or compiling the information have any liability for any damages of any kind. The analyst certifies that all of the views expressed in this document accurately reflect his or her personal views about the subject company or companiesand its or their securities and do not necessarily reflect those of SHAREKHAN. Further, no part of the analyst’s compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document.

Please refer the Risk Disclosure Document issued by SEBI and go through the Rights and Obligations and Do’s and Dont’s issued by Stock Exchanges and Depositories before trading on the Stock Exchanges. Please refer disclaimer for Terms of Use.

Compliance Officer: Ms. Namita Amod Godbole; Tel: 022-6115000; e-mail: [email protected] • Contact: [email protected]