inside the minds of participants report 2015€¦ · inside the minds of plan participants 3 the...

TRANSCRIPT

NOVEMBER 2015

INSIDE THE MINDS OF PLAN PARTICIPANTSWHO’S READY, WHO’S WILLING, WHO’S ABLE... WHO’S NOT

IN THIS PAPER: RETIREMENT CONFIDENCE is noticeably correlated to higher levels of financial literacy and investment capability. But most plan participants feel confused and unprepared. Automatic enrollment into target-date funds helps, but different investor “personas” need more targeted communications and engagement methods to increase investment knowledge and gain better retirement outcomes.

Investment Products Offered • Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed

There is no guarantee that any forecasts or opinions in this material will be realized. Information should not be construed as investment advice.

ABOUT AB’S DEFINED CONTRIBUTION RESEARCHThe Defined Contribution (DC) team at AB has conducted annual surveys of employees since 2005 and biennial surveys of plan sponsors since 2006. These snapshots help us understand the attitudes and behaviors of workers toward retirement saving, the changing state of DC plans, and the concerns, perspectives and strategies of plan sponsors.

We want to share this research with plan sponsors. We believe it will help them understand how to lead participants to better savings outcomes and more comfortable, confident retirements. We conducted our 11th annual web-based plan-participant survey in May and June 2015. It was based on a national sample of 1,009 employees who were eligible for their companies’ retirement plans, were at least 18 years old and worked for firms that offered DC plans.

“Target date” in a fund’s name refers to the approximate year when a plan participant expects to retire and begin withdrawing from his or her account. Target-date funds gradually adjust their asset allocation, lowering risk as a participant nears retirement. Investments in target-date funds are not guaranteed against loss of principal at any time, and account values can be more or less than the original amount invested—including at the time of the fund’s target date. Also, investing in target-date funds does not guarantee sufficient income in retirement.

How we explained an additional target-date fund feature of a guaranteed stream of income in retirement:

“The income payments would be based on a percentage of your highest account balance in the years leading up to your retirement. This type of fund would be offered to you at a very competitive price. This type of enhanced target-date fund would offer you: an income stream that will last as long as you live; the potential to increase the size of your income stream with gains in your investments; income protection in down markets—they won’t reduce the size of your guaranteed payments; the flexibility to take part or all of your money out of your account at any time without incurring withdrawal fees.”

INSIDE THE MINDS OF PLAN PARTICIPANTS 1

There are many likely reasons that US workers lack investment competence: “I’m too busy.” “I’ll think about it tomorrow.” “Investing is complicated.” It’s not easy to keep up, let alone get ahead. So, most of us simply avoid learning even the basics of practical investing for retirement.

That knowledge deficit helped drive the creation of target-date funds. It contributed to the rise of automatic enrollment and the Department of Labor’s (DOL) approval of diversified, all-in-one solutions as qualified default investment alternatives (QDIAs).

But is automatic enrollment into a QDIA the end to the story? No.

Results from our latest survey of American workers offer compelling insights about their love/hate relationship with retirement saving. They also reveal what plan sponsors and investment providers can do to strengthen that relationship and make workers more confident in it. Everyone wants the same thing: to help Americans achieve better retirement outcomes.

RETIREMENT CONFIDENCE: CHRONICALLY LOWWorkers haven’t had much confidence recently, except in our 2013 results. And that survey was conducted toward the end of a very strong year for US stocks. In 2014, fears of slower global growth tempered market returns, and they’ve done the same to confidence, which fell back to 25% in 2015.

Workers’ top concerns remain the same: They don’t think they’ll have enough money to live as they do now. Social Security may not help as much as it did in the past, and people are afraid of depending on others. The main reason for whatever level of confidence our respon-dents have? At least they’ve saved some money. But one-fourth of them plan to delay retirement, and nearly a third say they’ll continue to work part time once they do retire. Curiously, nearly one-fourth say they’ll get a pension, even though more companies are terminating or freezing their defined benefit (DB) plans.

That result raises another big issue: a lot of the investment and retire-ment-planning knowledge workers believe they have is mistaken.

ARE DC PLANS WORKING FOR WORKERS?

Knowledge is power. Knowledge breeds confidence. Knowledge clarifies planning. But knowledge is largely missing from the retirement-savings mindset of many American workers.

FEW WORKERS SEE A COMFORTABLE RETIREMENT AS A REALITY“How confident are you that you’ll have a comfortable retirement?”

05 06 07 08 09 10Year

11 12 13 14 15

27% 25%

41%

29%

18%

24%26% 25%

32%

27% 25%

% of employees who are confident/very confidentSource: AB Research, 2015

“WHAT ARE THE KEY REASONS FOR YOUR LEVEL OF RETIREMENT CONFIDENCE?”

I’ll get a pensionfrom my employer

I plan on delaying my retirement

I’ll work part-time

I’ve saved some money but need to save more 42%

32%

24%

23%

Source: AB Research, 2015

2

DC plans started as a supplemental benefit, offering freedom of choice. Now, they’re the primary retirement vehicle for most workers. But many workers don’t understand enough to handle what has become the freedom to fail.

FINANCIAL LITERACY: TOO MANY UNKNOWN KNOWNS

In past surveys, our survey results delineated two basic types of DC plan participants: those who actively invest and save, and those “accidental” participants who only invest because they’re in a DC plan. The typical split was 60/40 in favor of accidental. Over the last few years, the balance moved much closer to even, which puzzled us. So this year, we wanted to find out if knowledge had generally increased. We added eight simple questions about investing, and many of our respondents didn’t fare too well.

You can take the quiz yourself. On this page, we show the questions and the percentages of respondents who answered correctly (in boxes). The correct answers are on the inside back cover.

1. Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

a. More than $102

b. Exactly $102

c. Less than $102

d. Don’t know

e. Prefer not to answer

Two of the answers are obviously wrong, but allowable—“don’t know” and “prefer not to answer.” Only 14% chose these. For the most part, our employed workers did well, with the best scores turned in by the older age brackets (55–64 and 65–75 scored 79% and 89%, respectively).

2. Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, would you be able to buy more than, exactly the same as, or less than today with the money in this account?

a. Buy more than

b. Exactly the same as

c. Less than today with the money in this account

d. Don’t know

e. Prefer not to answer

Already, the number of correct responses is declining—a lot. But once again, “older is wiser” seems to be holding true, as more than 75% of those in the two older age brackets got the right answer.

3. If interest rates rise, what will typically happen to bond prices?

a. They will rise

b. They will fall

c. They will stay the same

d. There is no relationship between bond prices and interest rates

e. Don’t know

f. Prefer not to answer

Only respondents in the oldest age bracket did well here—65% got it right. Interestingly, the youngest (those 18–24) did better than those aged 25–34 (26% vs. 19%). Unfortunately, one-third of our respondents chose “Don’t know.”

4. Do you think that the following statement is true or false? “Buying a single company stock usually provides a safer return than a stock mutual fund.”

a. True

b. False

c. Don’t know

d. Prefer not to answer

The percentage of correct responses is certainly better than it was for the previous question, but the number of those answering “Don’t know” has now climbed to 36%, and 60% of 18–24-year-olds chose this answer.

5. Which of the following statements describes the main function of the stock market?

a. It helps to predict stock earnings

b. It results in an increase in the price of stocks

c. It brings people who want to buy stocks together with those who want to sell stocks

d. None of the above

e. Don’t know

f. Prefer not to answer

More than half of respondents got this one right—mainly the two oldest age categories. The two youngest age groups (18–24 and 25–34) not only had the lowest percentage of correct answers; they also had more inaccurate answers, as opposed to other groups, who had more “don’t know” responses. Later in this research, we’ll explore

73%

CORRECT

51%

CORRECT64%

CORRECT

34%

CORRECT

54%

CORRECT

INSIDE THE MINDS OF PLAN PARTICIPANTS 3

the tendency of younger workers to be more likely to “know” inaccu-rate information—and how it bolsters a false, eager confidence.

6. Considering a long time period (for example 10 or 20 years), which asset normally gives the highest return?

a. Savings accounts

b. Bonds

c. Stocks

d. Don’t know

e. Prefer not to answer

The “older and wiser” trend continued here. Of those aged 65–75, 72% got the correct answer. And the trend of “young, eager but inaccurate” also continued. That’s a pity, because America’s looming retirement problem can’t be fixed by waiting for everyone to grow wiser just by growing older. Plan sponsors, investment providers and government agencies need to harness the eagerness of younger generations while they’re young.

7. Normally, which asset displays the highest fluctuations over time?

a. Savings accounts

b. Bonds

c. Stocks

d. Don’t know

e. Prefer not to answer

The majority of every age group answered this one correctly. However, roughly one-fourth of the two younger age brackets chose inaccurate answers. (Again, choosing “don’t know” or “prefer not to answer” isn’t inaccurate; it just isn’t right.) The issue when so many younger workers choose wrong answers: misinformation is a more difficult obstacle to investment and retirement education than no information at all.

8. When an investor spreads his money among different assets, does the risk of losing money:

a. Increase

b. Decrease

c. Stay the same

d. Don’t know

e. Prefer not to answer

Just over half our respondents answered this correctly, even though it’s based on a bedrock principle of sound, long-term investing. It’s a concept that has been pounded home in DC educational materials for decades. Clearly, there’s a disconnect between providing retirement-saving education and getting participants to use it—or understand it if they do use it.

Among our respondents, only 12% are “Whiz Kids,” who got all eight questions right. Another 28% qualify as well-versed, getting 6 or 7 correct answers. In the middle of the pack, roughly one-third answered 3 to 5 questions correctly, while one-fourth remain “In the Dark,” with two or fewer correct answers.

Financial literacy is more than just academic. In many cases, our survey results show that more financial literacy goes hand in hand with higher engagement, higher contribution rates and higher confidence. We’ll refer to these levels of financial literacy when we explore new ways to categorize and understand employees, in order to help them build better retirement outcomes.

TOO MANY WORKERS DON’T UNDERSTAND THE BASICSPercent of Respondents

86–73–50–2Number of Correct Answers

35%

26%28%

12%

Source: AB Research, 2015

48%

CORRECT

67%

CORRECT

55%

CORRECT

4

Workers need a better understanding of how to save wisely and steadily for retirement. Automatic enrollment has increased participation levels in recent years, but engagement levels still have quite a way to go.

UNCERTAINTY PRINCIPLE: COMBATING MISINFORMATION, HESITANCY AND CONFUSION

What helps boost retirement confidence? The most frequently cited reason for confidence (42%) is having money already tucked away in savings. Workers realize they need to save more, and nearly three-fourths of our respondents say they save money outside their workplace retirement plan. More than half of them say they’ll use those savings for emergencies.

The second and third most-cited goals for these non-retirement plan savings (respondents could select up to three of 13 possible answers) are to provide income in retirement, and to live comfortably and enjoy life. Income is a decidedly future-oriented goal; the other has a more current or “whenever” orientation.

But what about primary savings goals for the money inside their DC plan? Whether or not participants have any outside savings, 71% say the main purpose of their DC plan savings is to provide income in retirement. That’s good, but the next most frequently cited reason is to live comfortably and enjoy life (34%). That’s not good: if the intention is to use an account “whenever,” it can mean hefty early-withdrawal penalties.

LIFETIME INCOME: THE PERENNIAL WISH-LIST FAVORITEWhen asked what features and benefits they most want from a DC plan, workers overwhelmingly call for a steady income stream in retirement (69%). That response was far more frequent than even protection of principal (44%), the second choice on their “most wanted” list.

This brings up an issue that many plan sponsors, consultants and advisors are wrestling with now: Should companies embed a lifetime income benefit into their DC plans? To reach enough participants, such an option would more than likely have to be a plan’s QDIA used in conjunction with automatic enrollment.

WHAT DO PARTICIPANTS WANT IN THEIR DC PLANS?

Steady income streamin retirement

Protection of principal

Investing in a well-diversified mix of investments

Withdrawing moneywith no fees or penalties

Upside potential

Transferring money amongoptions at any time

Downside protectionof income stream

Having professionals adjust funds more conservatively

over time

Funds from recognizedbrand names

69%

44%

42%

38%

36%

23%

22%

19%

14%

Source: AB Research, 2015

TOP SAVINGS GOALS FOR ASSETS INSIDE DC PLANS

Provide income in retirement

Live comfortably/enjoy life

Have moneyfor an emergency

Be debt free

Pay bills

Pay for healthcare/medications

71%

34%

20%

16%

15%

12%

Source: AB Research, 2015

INSIDE THE MINDS OF PLAN PARTICIPANTS 5

1 AB, Inside the Minds of Plan Sponsors, 2015.2 Callan Investments Institute, 2015 Defined Contribution Trends. Survey included 144 plan sponsors from large DC plans, 85% of which had $100 million or more in assets.

The true benefit of automatic features shows

up in the details.

AUTOMATIC ENROLLMENT STILL IN EARLY STAGESHowever, automatic enrollment has yet to become a decisive force in plan participation. While 55% of plan sponsors say their plans offer automatic enrollment,1 only 24% of participants say they were automatically enrolled by their employer. The other 76% say they “actively filled out the necessary forms and enrolled myself.”

The trend in automatic enrollment keeps increasing, with over 60% of large DC plans now using it, up from roughly 35% in 2006.2 Primarily, plan sponsors use automatic enrollment for new hires, and our participant survey reflects that: The percentage of younger workers who are automatically enrolled is higher—30% versus 24% for the entire survey population—and we believe this will continue to increase over time.

ENGAGEMENT AND CAPABILITY ARE NOT THE SAME THINGRegardless of the high percentage of workers actively engaged in their enrollment, plan sponsors should focus on the extensive value of automatic features in combination with a QDIA. When we questioned participants on their investing capabilities, the need for more hands-on help became clear.

Most of our respondents (80%) say they selected how much they contribute to their current DC plan. Some 40% choose their invest-ment options without consulting anyone. Another 34% consult with or rely solely on a financial advisor for this decision. Most participants diversify—investing either in several options that sometimes include an asset-allocation fund, or just in an asset-allocation fund (such as a target-date, lifecycle or lifestyle funds).

So far, that’s pretty good. But on closer inspection, participants reveal declining confidence in their capabilities. Less than half say they want to select their own mix of individual funds or are comfortable deciding how much to invest in each fund. Even fewer have the time to keep an eye on those investments and make

changes as they get closer to retirement. And doubts grow about whether their investments will generate an income stream that will last throughout retirement.

It’s in the details that we can see the true benefit of automatic enrollment and automatic escalation. However, those very benefits—and the inertia they leverage—may be contributing to a decline in engagement. And that engagement deficit appears to play a role in a lack of confidence and retirement readiness.

COMFORT LEVELS REVEAL DECLINING CONFIDENCE IN INVESTING CAPABILITIES

Have the desire to select own mix of

individual funds

Comfortable deciding how much to invest

in each fund

Have the time to keep an eye on investments and make changes as I

get closer to retirement

Confident my investments will generate an income stream that will last for

my entire life

DisagreeMixedAgree

13%41%46%

11%41%47%

14%43%43%

11%51%38%

Answers were on a scale of 1–10 with 8–10=agree; 4–7=mixed; 1–3=disagreeSource: AB Research, 2015

6

Target-date solutions hold roughly $1 trillion in assets—about 20% of the DC market—and they’re growing fast.3 But do participants understand them any better than they grasp investing in general?

WHAT’S IN A NAME? MISINFORMATION PLAGUES TARGET-DATE FUNDS, TOO

3 Cerulli Associates, Retirement Markets 2014: Sizing Opportunities in Private and Public Retirement Plans.

Workers’ understanding of target-date solutions is on the decline. In fact, fewer participants are certain whether or not they even invest in a target-date solution than they were last year. The decline may be tied to an increase in automatic enrollment. If so, that lack of engagement or understanding would be an undesired side effect of a healthy retirement-savings aid.

Target-date fund users most frequently say these funds keep them appropriately invested to and through retirement (34%). They also like that the funds are easy to understand (30%) and that a professional money manager invests the assets according to the participant’s retirement time frame (27%). Respondents who don’t invest in target-date funds often say they don’t know enough about them (42%). But another 35% say their employer doesn’t offer target-date funds, and 28% say target-date funds take away the control they want.

While many nonusers say they don’t know enough, target-date fund users often know even less. And both groups apparently understand less now than respondents in our 2014 survey.

SORRY, WRONG ANSWERWe posed five questions to respondents who knew whether or not they invested in target-date funds. In all but one response, target-date fund users are now giving wrong answers more fre-quently than in our 2014 survey—and more frequently than the 2015 nonusers. The only question that got a better result for target-date fund users versus nonusers was that target-date funds become more conservative as you get closer to retirement (73% of users versus 54% of nonusers). But fewer target-date users got the right answer than last year: 73% this year versus 80% in 2014.

WHERE’S THE CONFUSION? IN THE MATERIALS? IN THE DATE?Among respondents who believe target-date funds are guaranteed, 38% say the year listed in the fund name tells them their accounts are guaranteed to be sufficiently funded in that year. Nearly as many (34%) think the materials they received about the funds say they’re guaranteed. And more than one-fourth tell us that the representative who presented to their company told them the funds were guaranteed.

Despite what participants know or don’t know about target-date funds, when they were asked how they’d feel if their employer automatically invested their contributions into a target-date fund,

MORE PARTICIPANTS DON’T KNOW IF THEY’RE IN TARGET-DATE FUNDS OR NOT

l Invested in target-date funds

l Not invested in target-date funds

l Don’t know

20152014

47%

32%21% 23% 32%

45%

Source: AB Research, 2014, 2015

MISPERCEPTIONS RISING AMONG TARGET-DATE USERS% of respondents answering incorrectly (who know whether or not they use target-date funds)

l Guarantee you’ll meet your income needs in retirement

l Account balance guaranteed to never go down

l Invested 100% in cash at retirement

l FDIC insured

20152014TDF Users TDF Users TDF Nonusers

22%

36%34%29% 28%26%

18%16%12% 12% 11%10%

Source: AB Research 2014, 2015

INSIDE THE MINDS OF PLAN PARTICIPANTS 7

90% say yes to automatic enrollment in a guaranteed-

income target-date fund.

an overwhelming 87% reacted favorably. More than half (53%) said they’d like it or, at least wouldn’t object; another 34% said they would keep some money in the fund and move some into other investments.

GUARANTEED INCOME TARGET-DATE FUNDS APPEAL BROADLY AMONG WORKERSBut what boosts the interest and engagement of all employees in our survey? It’s the potential to invest in a target-date fund with a guaranteed stream of income for life.

First, we asked how appealing respondents would find such a fund. While 84% of current target-date fund users found it appealing or extremely appealing, even 65% of nonusers agreed on that point. And of those participants who didn’t know whether they were in a target-date fund or not, just over half found such a fund to be appealing or extremely appealing. Interestingly, 62% of nonpar-ticipants say they’d be interested in such a guaranteed-income target-date fund and that it would enhance their desire to participate in the DC plan.

Beyond the appeal, we asked our respondents how likely they would be to invest in such a fund. Over half (54%) of current plan participants say they’d be likely or very likely to invest in a guaranteed-income target-date fund. Surprisingly, more than three-fourths of nonparticipants (78%) agree. They also feel it would enhance their desire to join their company’s retirement plan.

But to generate successful participation levels in this type of option within a DC plan, plan sponsors would need to make it the plan’s QDIA, used in conjunction with automatic enrollment. So, we asked our respondents what they would do if their employer automatically enrolled them in a target-date fund with a guaranteed income stream in retirement. The results are overwhelmingly positive.

Nearly 90% of all employees would keep some or all of their contri-butions in a target-date fund that guaranteed an income stream for life. That feature has topped their wish list of retirement plan features every one of the past seven years that we’ve asked this question.

HOW WOULD YOU FEEL IF YOUR EMPLOYER AUTOMATICALLY INVESTED YOUR CONTRIBUTIONS INTO A TARGET-DATE FUND WITH A GUARANTEED INCOME FEATURE?% of plan participants and nonparticipants

l I would opt out l I’d keep some money in/move some to other investments

l I wouldn’t object l I would like it

Plan Participants NonparticipantsTDF Users TDF Nonusers Don’t Know

48%

18%24% 27%

28%

29%

32%

39%

20%

36%

35% 24%

4%

18% 9% 9%

Source: AB Research, 2015

WHY DO YOU THINK TARGET-DATE FUNDS ARE GUARANTEED?% of respondents who believe target-date funds are guaranteed:

l Materials say the funds are guaranteed

l Year listed in fund name means it’s guaranteed to be suciently funded in that year

l Representative said funds were guaranteed

20152014TDF Users TDF Users TDF Nonusers

19%

47%

38%

34%

13%15%

38%

15%

19%

Source: AB Research 2014, 2015

8

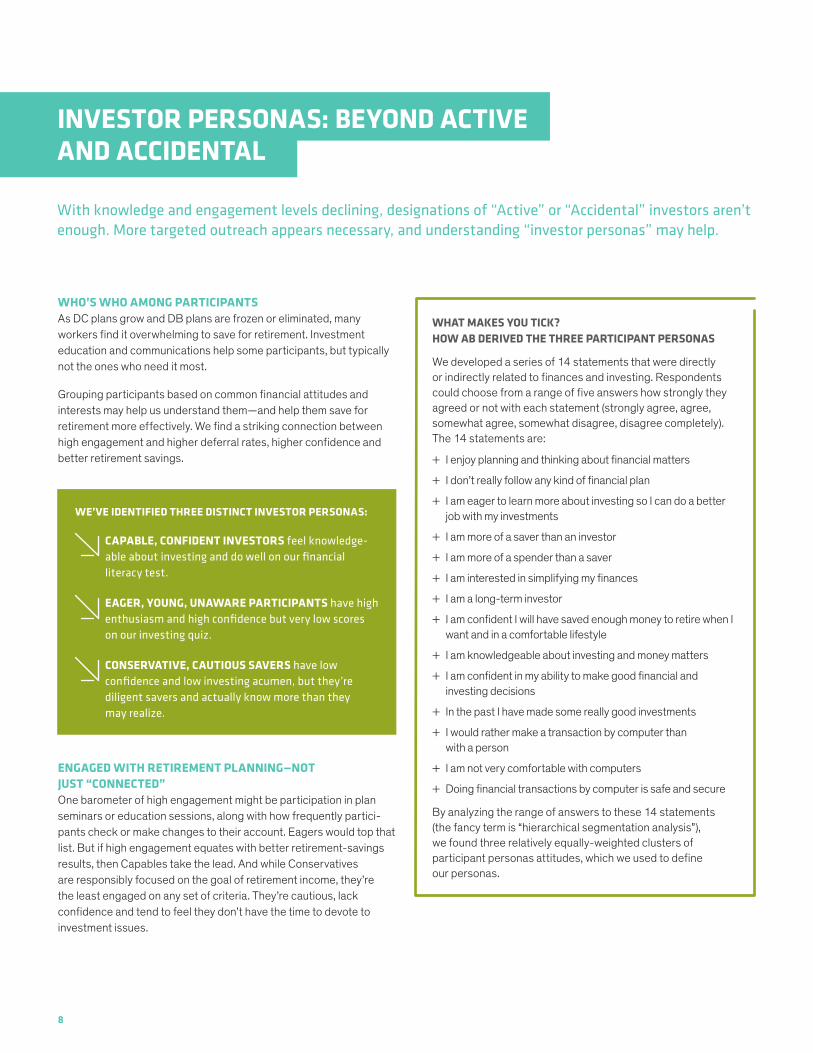

WHO’S WHO AMONG PARTICIPANTSAs DC plans grow and DB plans are frozen or eliminated, many workers find it overwhelming to save for retirement. Investment education and communications help some participants, but typically not the ones who need it most.

Grouping participants based on common financial attitudes and interests may help us understand them—and help them save for retirement more effectively. We find a striking connection between high engagement and higher deferral rates, higher confidence and better retirement savings.

ENGAGED WITH RETIREMENT PLANNING—NOT JUST “CONNECTED”One barometer of high engagement might be participation in plan seminars or education sessions, along with how frequently partici-pants check or make changes to their account. Eagers would top that list. But if high engagement equates with better retirement-savings results, then Capables take the lead. And while Conservatives are responsibly focused on the goal of retirement income, they’re the least engaged on any set of criteria. They’re cautious, lack confidence and tend to feel they don’t have the time to devote to investment issues.

With knowledge and engagement levels declining, designations of “Active” or “Accidental” investors aren’t enough. More targeted outreach appears necessary, and understanding “investor personas” may help.

INVESTOR PERSONAS: BEYOND ACTIVE AND ACCIDENTAL

WE’VE IDENTIFIED THREE DISTINCT INVESTOR PERSONAS:

CAPABLE, CONFIDENT INVESTORS feel knowledge-able about investing and do well on our financial literacy test.

EAGER, YOUNG, UNAWARE PARTICIPANTS have high enthusiasm and high confidence but very low scores on our investing quiz.

CONSERVATIVE, CAUTIOUS SAVERS have low confidence and low investing acumen, but they’re diligent savers and actually know more than they may realize.

WHAT MAKES YOU TICK? HOW AB DERIVED THE THREE PARTICIPANT PERSONAS

We developed a series of 14 statements that were directly or indirectly related to finances and investing. Respondents could choose from a range of five answers how strongly they agreed or not with each statement (strongly agree, agree, somewhat agree, somewhat disagree, disagree completely). The 14 statements are:

+ I enjoy planning and thinking about financial matters

+ I don’t really follow any kind of financial plan

+ I am eager to learn more about investing so I can do a better job with my investments

+ I am more of a saver than an investor

+ I am more of a spender than a saver

+ I am interested in simplifying my finances

+ I am a long-term investor

+ I am confident I will have saved enough money to retire when I want and in a comfortable lifestyle

+ I am knowledgeable about investing and money matters

+ I am confident in my ability to make good financial and investing decisions

+ In the past I have made some really good investments

+ I would rather make a transaction by computer than with a person

+ I am not very comfortable with computers

+ Doing financial transactions by computer is safe and secure

By analyzing the range of answers to these 14 statements (the fancy term is “hierarchical segmentation analysis”), we found three relatively equally-weighted clusters of participant personas attitudes, which we used to define our personas.

INSIDE THE MINDS OF PLAN PARTICIPANTS 9

Higher retirement confidence comes with

improved financial literacy.

THREE INVESTOR PERSONAS CAPABLE EAGER CONSERVATIVE CONFIDENT INVESTOR YOUNG, UNAWARE CAUTIOUS SAVER

Demographics

Median age 50 38 46

Median household income $76,000 $64,000 $60,000

Median deferral rate 8% 6% 6%

Total household DC assets $87,000 $35,000 $51,000

Very confident retirement outlook 38% 31% 12%

Median assets outside DC $47,000 $17,000 $16,000

Graduate degree 24% 11% 17%

Male 64% 48% 37%

Financial literacy: Whiz Kids* 22% 4% 7%

Financial literacy: In the Dark* 15% 40% 24%

Attitudes Toward Retirement (% of each persona group)

Top DC savings goal: retirement income 78% 59% 77%

Check account balance and change investment mix, choices and deferral rate frequently (daily, monthly or quarterly)

19% 33% 14%

Comfortable making asset-allocation decisions 62% 43% 35%

Very experienced/experienced with making investment decisions 37% 28% 9%

Somewhat to very confident of comfortable retirement 85% 63% 58%

Would value a personalized forecast 62% 74% 59%

Likely would pay $1 for personalized forecast 45% 60% 42%

*Whiz Kids answered all 8 financial literacy questions correctly; In the Dark respondents answered 0–2 questions correctly.Source: AB Research, 2015

10

CAPABLE, CONFIDENT INVESTORSAll three categories profess a largely independent outlook (“I’ll do it myself” vs. “Help me do this”) in deciding to be in their DC plan and how much money to save. But Capable investors typically have a collection of responsible attitudes and habits. When asked if they were comfortable selecting investments for their contributions, 70% of Capables said they’d do it themselves; less than half of the other two groups felt that way. Only Capables have a strong majority who feel confident about selecting a strategy that can generate lifetime income once they retire (60% versus roughly 40% for Eagers and Conservatives).

As a group, Capables did the best on our financial literacy quiz: Nearly 60% got six or more correct answers (out of eight). They typically have more household income and DC plan assets than the others, and they have about three times as much savings outside the plan. Perhaps the most notable difference with Capables? On average, the contribution rate of their DC plan is two full percentage points higher than that of the other groups (8% vs. 6%). That, over time, makes a huge difference.

CAPABLES HAVE A CURIOUS RELATIONSHIP WITH TARGET-DATE FUNDSNearly one-third of Capables invest in target-date funds—in line with our overall survey results. But nearly one-fourth of those Capables invest 100% of their assets in target-date funds. That’s far more than the other two groups and much more aligned with the strategic concept of target-date funds. Capables are also more aware of their target-date usage: only 16% said they don’t know whether or not they use one. That’s much lower than the 27% of Eagers and 25% of Conservatives that were unaware.

Capables are also the most independent and savvy group. Those who invest in a target-date fund most frequently state that it keeps them appropriately invested as they save for retirement—and in retirement. Capables who don’t invest in target-date funds cite two big reasons. They like to be in control of their investment strategy, and feel that target-date funds take that control away from them (39%). And they think they can do a better job building their wealth than a target-date fund (40%). Also, if automatically enrolled, this group is far more likely to opt out.

With their better planning, saving and confidence levels, it’s reason-able that these independent investors show a slightly lower interest in target-date funds with a guaranteed lifetime income component.

EAGER, YOUNG, UNAWAREPerhaps the most striking demographic feature of the Eager persona is age: Eagers have a median age of 38, compared with 50 for Capables and 46 for Conservatives. Eagers also reflect a tech-savvy difference from the other two personas: many more of them use smartphones or tablets to get their DC plan information.

And Eagers are just that: eager and engaged. They want to learn more and participate in plan seminars. They also access their accounts more often than the other personas. But that eager connectedness doesn’t translate to accurate understanding. In fact, Eagers had the lowest average scores on the financial literacy quiz—40% of them got zero to two correct answers out of eight.

If plan sponsors and providers approach participants by targeting the strengths and weaknesses of their personas, it may be possible to increase the knowledge of Eager participants and the confidence of the Conservative ones—and ultimately the retirement savings for all personas.

CAPABLE, EAGER, CONSERVATIVE: PROFILES IN CONFIDENCE (OR NOT)

CAPABLE INVESTORS—KNOWLEDGE OF THE FINANCIAL MARKETS WITH DISCIPLINE TO INVEST WISELY

44%

33%

15%

53%

39%

21%

49%

35%

21%

51%

39%

26%

40%

35%

20%

66%

40%

44%

Knowledgeable aboutinvesting and money matters

Confident can make goodfinancial and investing decisions

Made really good investmentsin the past

Enjoy planning and thinkingabout financial matters

Confident they’ll have enoughsaved to retire when they want

Long-term investor

l Capable l Eager l Conservative

Source: AB Research, 2015

INSIDE THE MINDS OF PLAN PARTICIPANTS 11

The good news about Eagers is that time is on their side. Plan sponsors and providers can leverage this eagerness to know more and be more engaged as a path to make Eagers more knowledge-able, better investors and wisely confident.

CONSERVATIVE, CAUTIOUS SAVERS—NOT SPENDERS, NOT INVESTORSThe single notion of primarily being a saver produced a strikingly contained group of workers that typically don’t see themselves as investors—we refer to them as Conservatives. They feel very unconfident about making financial and investment decisions, having a comfortable retirement, or understanding investing and money matters.

Conservatives did better than Eagers on our finance quiz, but their “no confidence” factor reinforces their doubts about their investing capabilities and perpetuates a disinterest in learning more. It’s notable that nearly two-thirds of Conservatives are female. That may relate to many factors—working single mothers, generally lower pay versus male counterparts or taking time out of the workforce to raise children. All of these factors reinforce their need to be financially

cautious. In other words, they save with as little investment risk as possible.

Conservative savers are less likely to know what types of investments they hold in their DC plan. They do report a much greater tendency to invest cautiously…perhaps too cautiously to build enough savings.

EAGERS ARE MORE CONNECTED THAN ENGAGED% of each persona group

35%

42%

22%

49%

48%

67%

39%

53%

27%

30%

44%

16%

Highly engaged—accessaccount daily to quarterly*

Least engaged—accessaccount annually to never*

Likely to participate in aplan seminar/education

session online or by phone

Use either smartphone or tablet for plan information

l Capable l Eager l Conservative

*Check account balance, change investment mix, change investment choices for new contributions, and change account contribution percentage from salarySource: AB Research, 2015

CONSERVATIVE SAVERS—CAUTIOUS…TO A FAULT?% of each persona group

l Capable l Eager l Conservative

US equity funds*

International/globalequity funds*

More of a saverthan an investor

More of a spenderthan a saver

US bond funds*

International/globalbond funds*

Stable value funds*

Money-market funds*

23%

34%

82%

7%

68%

1%

65%

38%

32%

33%

22%

13%

35%

44%

50%

22%

32%

18%

24%

18%

28%

38%

45%

56%

*In addition to target-date funds, what other types of investments are you invested in within your company’s DC plan?Source: AB Research, 2015

12

AUTOMATIC ENROLLMENT NEEDS AUTOMATIC ESCALATION, TOOAutomatic enrollment currently applies to only one-fourth of participants, but more new hires are being automatically enrolled each year—typically into a target-date fund. That helps many workers begin their journey to retirement readiness, but it can’t correct the behavioral phenomenon of inertia—in this case, as it applies to participants increasing their contributions over time.

That’s why we believe automatic escalation is also necessary. Only 20% of plan sponsors we surveyed currently use both automatic enrollment and escalation. That needs to be improved, because our research shows that the automatic escalation of savings rates may be the most important factor in building longer-lasting retirement savings—other than a guaranteed retirement income stream.4

KNOWLEDGE IS POWERWorkers also need to become more engaged with their retirement- savings efforts. The path to that improvement is clear. Our survey clearly shows that greater financial literacy produces greater engagement, greater responsibility, greater confidence and greater retirement preparedness.

Financial literacy is typically accompanied by:

+ higher household income

+ higher DC plan balances

+ a greater likelihood to be saving for retirement

Financial literacy doesn’t dramatically rise with education or job title, so it’s something that can be achieved generally. Those with higher financial literacy:

+ find diversifying investments attractive

+ more accurately understand target-date funds (and are more likely to invest 100% in them)

+ look for investments with upside potential more than ones with downside protection

+ have higher deferral rates

+ are more concerned about long-term retirement spending concerns such as inflation, outliving savings and using a judicious withdrawal rate for retirement spending needs

America’s retirement readiness is nowhere near what it needs to be. But there are ways to alter that state—both now and in the future.

AUTOMATIC FEATURES FOR NOW,EMPOWERMENT AND KNOWLEDGE FOR TOMORROW

4 AB, “The Future of DC Has Arrived: Improving Retirement Outcomes Now,” 2013.

IMPROVE KNOWLEDGE AND CONFIDENCE WITH TARGETED COMMUNICATIONSEach of our three investor personas has distinct advantages and hurdles. Plan sponsors and providers can leverage those distinctions to increase engagement, which can ultimately lead to greater knowledge and better use of a company’s DC plan.

CAPABLE, CONFIDENT INVESTORS prize their indepen-dence and feel they can do a better investing job.

Their biggest hurdle: they may not truly comprehend the potential pain of taking too much risk.

Suggested action: + Improve their engagement by delivering targeted articles on

the risk/reward hazards of specific investments and investing issues (such as liquidity scarcity and crowded trades).

EAGER, YOUNG, UNAWARE PARTICIPANTS have time and interest on their side.

Their biggest hurdle: they need to make the most of those “assets” to invest well.

Suggested actions: + Explain the startling long-term, cumulative difference that

results from higher contribution rates early on. This may resonate with them.

+ Give them comparative graphics showing the potential growth advantages of long-term investing in equities versus the drag of too much safety (including bonds and money- market funds) in the early decades of retirement saving.

+ Make the most of social media to connect with Eagers!

CONSERVATIVE, CAUTIOUS SAVERS need to grasp the potential of high-return investments.

Their biggest hurdle: they need help increasing their comfort level with investing.

Suggested actions: + Help them see that time can be on their side, too.

+ Show them the damaging risk of a savings shortfall from an overly safe approach to investing—they may gain confidence in embracing greater growth potential.

Financial literacy is more than academic. Greater financial knowledge correlates with greater engagement, greater confidence, better retirement plan decisions and better potential retirement outcomes. Correct answers are in bold-face type.

1. Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

a. More than $102

b. Exactly $102

c. Less than $102

d. Don’t know

e. Prefer not to answer

2. Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, would you be able to buy more than, exactly the same as, or less than today with the money in this account?

a. Buy more than

b. Exactly the same as

c. Less than today with the money in this account

d. Don’t know

e. Prefer not to answer

3. If interest rates rise, what will typically happen to bond prices?

a. They will rise

b. They will fall

c. They will stay the same

d. There is no relationship between bond prices and interest rates

e. Don’t know

f. Prefer not to answer

4. Do you think that the following statement is true or false? “Buying a single company stock usually provides a safer return than a stock mutual fund.”

a. True

b. False

c. Don’t know

d. Prefer not to answer

5. Which of the following statements describes the main function of the stock market?

a. It helps to predict stock earnings

b. It results in an increase in the price of stocks

c. It brings people who want to buy stocks together with those who want to sell stocks

d. None of the above

e. Don’t know

f. Prefer not to answer

6. Considering a long time period (for example 10 or 20 years), which asset normally gives the highest return?

a. Savings accounts

b. Bonds

c. Stocks

d. Don’t know

e. Prefer not to answer

7. Normally, which asset displays the highest fluctuations over time?

a. Savings accounts

b. Bonds

c. Stocks

d. Don’t know

e. Prefer not to answer

8. When an investor spreads his money among different assets, does the risk of losing money:

a. Increase

b. Decrease

c. Stay the same

d. Don’t know

e. Prefer not to answer

73%

CORRECT

51%

CORRECT

64%

CORRECT

48%

CORRECT

34%

CORRECT

67%

CORRECT

54%

CORRECT

55%

CORRECT

15-2198DCI–6115–1115

www.abglobal.com

ALLIANCEBERNSTEIN L.P.

1345 Avenue of the Americas New York, NY 10105 (212) 969 1000

ALLIANCEBERNSTEIN LIMITED

50 Berkeley Street, London W1J 8HA United Kingdom +44 20 7470 0100

ALLIANCEBERNSTEIN AUSTRALIA LIMITED

Level 32, Aurora Place, 88 Phillip Street Sydney NSW 2000, Australia +61 2 9255 1299

ALLIANCEBERNSTEIN CANADA, INC.

Brookfield Place, 161 Bay Street, 27th Floor Toronto, Ontario M5J 2S1 (416) 572 2534

ALLIANCEBERNSTEIN JAPAN LTD.

Marunouchi Trust Tower Main 17F 1-8-3, Marunouchi, Chiyoda-ku Tokyo 100-0005, Japan +81 3 5962 9000

ALLIANCEBERNSTEIN INVESTMENTS, INC. TOKYO BRANCH

Marunouchi Trust Tower Main 17F 1-8-3, Marunouchi, Chiyoda-ku Tokyo 100-0005, Japan +81 3 5962 9700

ALLIANCEBERNSTEIN HONG KONG LIMITED 聯博香港有限公司

Suite 3401, 34/F One International Finance Centre 1 Harbour View Street, Central, Hong Kong +852 2918 7888

ALLIANCEBERNSTEIN (SINGAPORE) LTD.

30 Cecil Street, #28-08, Prudential Tower Singapore 049712 +65 6230 4600

SANFORD C. BERNSTEIN & CO., LLC

1345 Avenue of the Americas New York, NY 10105 (212) 969 1000

Note to All Readers: The information contained herein reflects, as of the date hereof, the views of AllianceBernstein L.P. (or its applicable affiliate providing this publication) (“AB”) and sources believed by AB to be reliable. No representation or warranty is made concerning the accuracy of any data compiled herein. In addition, there can be no guarantee that any projection, forecast or opinion in these materials will be realized. Past performance is neither indicative of, nor a guarantee of, future results. The views expressed herein may change at any time subsequent to the date of issue hereof. These materials are provided for informational purposes only and under no circumstances may any information contained herein be construed as investment advice. AB does not provide tax, legal or accounting advice. The information contained herein does not take into account your particular investment objectives, financial situation or needs and you should, in considering this material, discuss your individual circumstances with professionals in those areas before making any decisions. Any information contained herein may not be construed as any sales or marketing materials in respect of, or an offer or solicitation for the purchase or sale of, any financial instrument, product or service sponsored or provided by AllianceBernstein L.P. or any affiliate or agent thereof. References to specific securities are presented solely in the context of industry analysis and are not to be considered recommendations by AB. This is not intended to be legal advice (and should not be relied upon as such) but just a discussion of issues. Plan sponsors should consult with their legal advisors for advice regarding their particular circumstances.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

© 2015 AllianceBernstein L.P.