insights from the ‘best on the...

TRANSCRIPT

Six Morningstar analysts were named among the “Best on the Street” as part of The Wall Street Journal’s 2012 survey. Theses exceptional stock-pickers were chosen based on their performance — FactSet Research Systems collected and calculated scores based on the estimated total return from their buy, sell, and hold recommendations.

These Morningstar analysts were chosen within their respective industries from an eligible field of more than 2,000 professionals at nearly 200 firms (click on their names to see Premium reports on all of the companies that they cover): 3Basili Alukos (Airlines) 3 Matthew Coffina (Food & Drug) 3 Avi Feinberg (Oil Equipment, Services & Distribution) 3 Joung Park (Mining & Metals) 3 David Whiston (Specialty Retailers & Services) 3 Drew Woodbury (Insurance: Life)

We’re proud to offer this special report, which includes insights on top-rated stocks, exclusively to Morningstar Premium members.

Top Picks (listed by analyst)

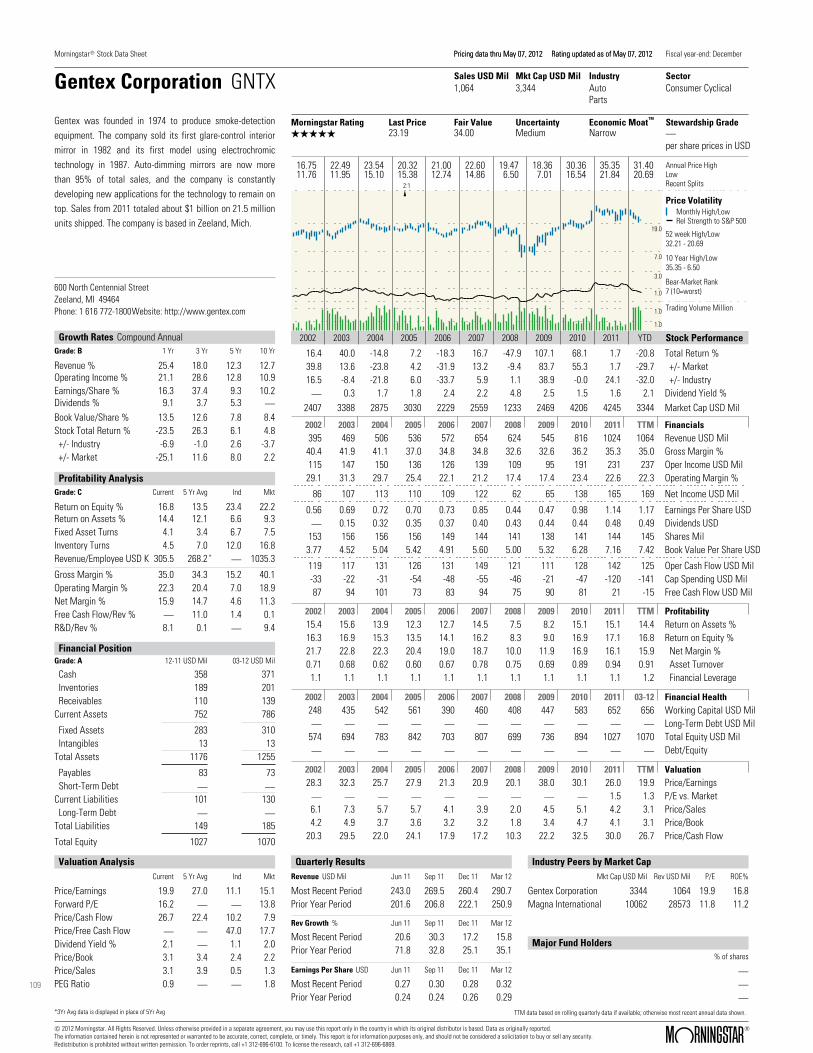

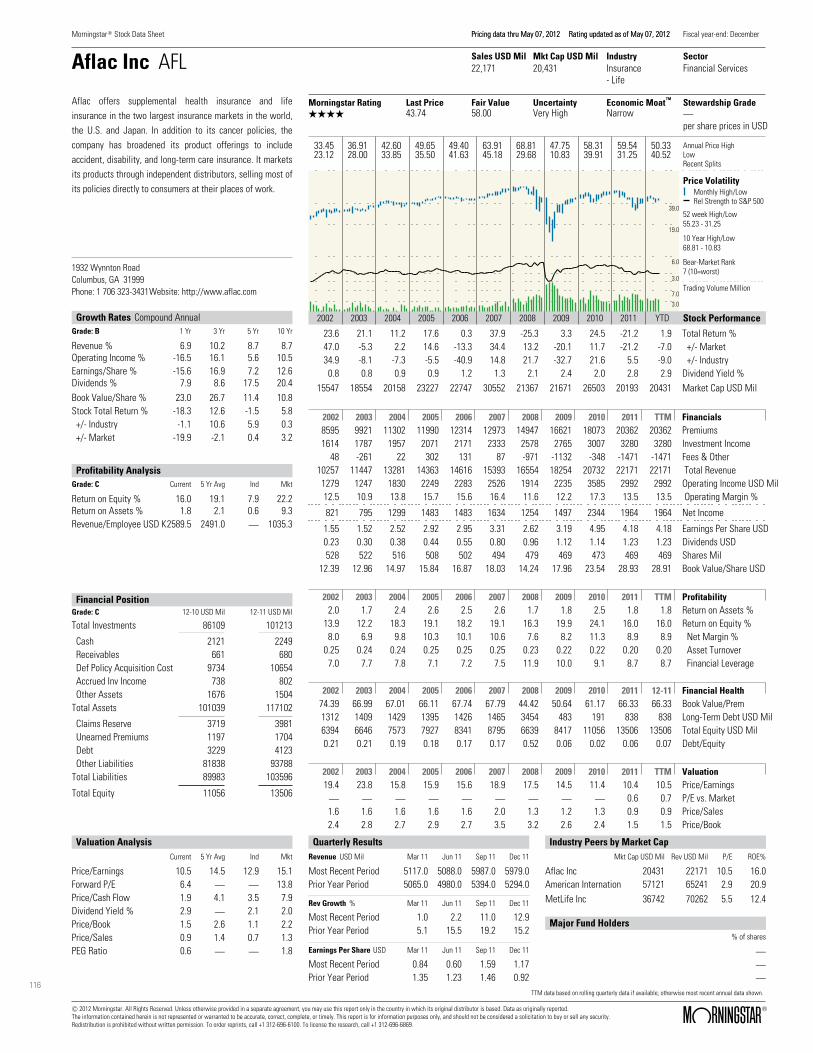

Basili Alukos Joung Park Southwest Airlines Co (LUV) 2 Yamana Gold Inc (AUY) 51 Eldorado Gold Corp (EGO) 59Matthew CoffinaWellPoint Inc (WLP) 11 David WhistonExpress Scripts (ESRX) 21 General Motors Co (GM) 69 Ford Motor Co (F) 86Avi Feinberg Gentex Corp (GNTX) 101DCP Midstream Partners LP (DPM) 33 TC Pipelines LP (TCP) 42 Drew Woodbury Aflac Inc (AFL) 111 Allstate Corp (ALL) 123

Compliments of Morningstar

Insights From the ‘Best on the Street’

2

?

Southwest Airlines Co LUV [NYSE] | QQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry8.26 USD 12.00 USD 6.00 USD 21.00 USD Very High None . Airlines BBB-

Currency amounts expressed with "$"are in U.S. dollars (USD) unlessotherwise denoted.

We expect Southwest will generate nearly $500 million insynergies from its AirTran acquisition.

by Basili Alukos, CPA, CFAStock AnalystAnalysts covering this company do notown its stock.

Pricing data through May 07, 2012.Rating updated as ofMay 07, 2012.

08 09 10 11 12

5.0

6.0

7.0

8.0

9.0

14.0

Stock Price

Thesis May 04, 2012 Despite being the lone stalwart in an industry with poorstructural characteristics, we believe Southwest Airlinesis transforming into a legacy carrier.� The U.S. domestic airline industry has seen a plethora ofnew startups over the past 41 years. While deregulationwas the primary catalyst, we believe the absence of anysignificant barriers to entry allowed swift entrance for anystartup, including Southwest. Southwest entered theairline industry predicated on stimulating leisurepassenger demand by offering cheap fares. By flying onetype of aircraft on direct point-to-point routes, Southwestis able to minimize both flight delays and inventory.Furthermore, Southwest minimizes costs by flying intosecond-tier airports such as Chicago Midway, which havelower landing fees. As a result, Southwest’s low-coststructure has allowed it to deliver operating profits for 39consecutive years, making it the envy of an airline industrythat has seen more than 180 bankruptcies since 1978.� Despite its low-cost focus, Southwest’s success hedgingits fuel costs (its largest expense) overshadows any of itsother cost-containment measures, in our opinion.Management has historically used hedging conservativelyto minimize jet fuel prices. However, Southwest’s currenthedges are not a significant cost advantage today.Moreover, the company will also face salary pressuresfrom its unionized workforce (roughly 82% of allemployees) as more contracts become amendable. Sincewe expect expenses to rise, Southwest must increase itsrevenue by possibly raising fares. However, leisuretravelers are sensitive to price increases, and we suspecta tepid return to flying as these passengers cope with therecovering economy.�� In this regard, we think the AirTran acquisition makessense. Southwest will gain access to 37 new markets(including both small and large-scale airports), but we

believe the crown jewel is Atlanta Hartsfield. This is theworld’s busiest airport by passenger traffic and servesaround 90 million passengers annually. With strongerfinancial backing, we expect Southwest will expand theAirTran footprint and believe Southwest can garner asubstantial portion of its stated $400 million in revenuesynergies from the acquisition. In fact, we believe thetotal run rate could achieve $500 million, due toSouthwest’s lower offerings in this and other big marketsAirTran serves.� Even so, any merger comes with integration risks, but webelieve the AirTran purchase may signal the end to theSouthwest to which most passengers are accustomed toflying. For one, Southwest is acquiring a�different�type ofaircraft--the Boeing�717--which we think ends theadvantage Southwest had by flying a single-aircraft fleet.In addition, Southwest is now expanding its presence inthe large airports New York (LaGuardia) and Boston(Logan). This should improve growth prospects, but thesemore-congested airports will slow Southwest’s aircraftturnover.�� Moreover, Southwest is acquiring larger aircraft with theidea it will commence service to Hawaii in 2012, and itappears international flying is next on the radar. Whileinternational flights are more profitable, we suspect thenew Southwest will more closely resemble a legacycarrier than its traditional operating model, and we thinkits future returns will suffer as a result. Valuation, Growth and Profitability Our fair value estimate for Southwest is $12 pershare.�We expect that Southwest will delivermid-single-digit growth in 2012 due to modestly higherticket prices, as the reduction in industry capacity shouldbolster yields.�We suspect Southwest’s decision toabstain from charging the first and second checked bagfees should enable the company to fly fuller planes. In thelonger term, however, we suspect increased competitionwill cause growth to slow, although we project thatSouthwest should generate roughly $500 million in

3

Southwest Airlines Co LUV [NYSE] | QQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry8.26 USD 12.00 USD 6.00 USD 21.00 USD Very High None . Airlines BBB-

Close Competitors Currency(Mil) Market Cap TTM Sales Oper Income Net Income

Southwest Airlines Co

JetBlue Airways Corporation

USD

USD

6,341 16,546 601 271

1,377 4,695 366 113

Morningstar data as of May 07, 2012.

revenue synergies over the long run. All told, thistranslates into 5% revenue growth for the combinedcompany over the next five years, which is down from theaverage 10% increase delivered historically.�� Both the stronger growth and better airplane utilizationshould bolster profitability because of the high amount ofoperating leverage innate in an airline. As such, we expectSouthwest to deliver 6% average annual�operatingmargins during our forecast period. Although impressivefor an airline, our operating margin expectations arebelow the company’s long-term 9% yearly average. Weexpect Southwest will pare expansion plans to cope withthe current economic environment and predict capitalspending will average 5% per year over our forecastperiod, which is well below historical averages. Risk Integrating AirTran will pose the biggest hurdle forSouthwest, as the company must, among other things,combine the two workforces and�earn its single operatingcertificate in relatively short order. Merger aside,�risingfuel costs most threaten Southwest’s success, in ouropinion. Despite its successful hedges, fuel costs areextremely volatile and represent roughly 30% of the firm’stotal operating costs. Labor costs also represent asignificant risk to Southwest’s profitability because unionrepresentation covers�nearly 75% of the combined-entity’sworkers. Losing its investment-grade credit rating couldalso be detrimental for Southwest, as a lower rating willcause Southwest to post more cash collateral and could

impair its future hedging abilities. Bulls Say

Preying on weaker competitors, Southwest has usedthe downturn to expand service offerings toMinneapolis-St. Paul, New York LaGuardia, and BostonLogan airports. If successful, these new markets willprovide ample growth opportunities going forward. Southwest and AirTran have very little route overlap,and the combined entity gains access to 37 newmarkets, which will provide instant growth potentialand reduces any cannibalization traditionally associatedwith an airline merger. In attempt to increase growth, Southwest is introducingthe Boeing 737-800 into its fleet beginning in 2012.These planes are more fuel efficient--we estimateSouthwest can replace three 737-300 flights with two737-800s--and these planes enable Southwest to flylong-haul routes including to and from Hawaii.

Bears Say

Airlines for America estimates that the tax percentageon airfare has tripled to roughly 20% of the price of aticket today, up from 7% in 1972. We don’t expect theamount of taxation to decrease going forward,especially as the government contemplates ways to payfor increased security measures, so Southwest and theindustry likely will receive a smaller share of futureticket proceeds. Southwest is solely a domestic carrier and has roughly40% of its capacity concentrated in the Western U.S.,leaving it more susceptible to a U.S. geographicslowdown than many of its competitors. Southwest has encountered regulatory problems overthe past two years in regard to maintenance procedureson some of its older aircraft. Southwest could face finesor customers may select another airline if these

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

4

Southwest Airlines Co LUV [NYSE] | QQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry8.26 USD 12.00 USD 6.00 USD 21.00 USD Very High None . Airlines BBB-

problems persist, both of which could hurt growth andprofitability.

Financial Overview Financial Health: Southwest is in decent financial shape.The company holds $3.8 billion in cash and short-terminvestments, in addition to an $800 million undrawnrevolver. The firm should be able to meet its principalcommitments over the next five years, although higherfuel prices could pose a problem. Company Overview Profile: Texas-based Southwest Airlines is the largestcarrier in the United States as measured by the number oforiginating passengers boarded. Combined with its recentacquisition of AirTran, Southwest operates a fleet ofnearly 700 aircraft comprising an all Boeing fleet. Theairline specializes in short-haul routes using apoint-to-point network and offers frequent flights toaround 110 markets cities. The combined firm employsalmost 46,000 workers and generates�approximately $17billion in annual revenue on a consolidated basis. Management: We think Southwest has historically done adecent job allocating shareholder capital in light ofoperating in the horrendous airline industry. Until fuelprices soared during most of the last decade, Southwestexploited its low-cost advantage to produce ROICs inexcess of its cost of capital. However, the company’saging workforce and elevated fuel prices�eroded�its moat,and we expect the poor fundamentals of the airlineindustry will dictate Southwest’s returns rather than poorcapital-allocation decisions.�� Southwest is run by CEO Gary Kelly, who began workingfor the carrier in 1986 as the firm’s controller beforeearning his current title in 2004. Kelly has done an

admirable job managing the airline through the 2008recession. Along with CFO Laura Wright, also a firmveteran, we believe that the management team has whatit takes to lead the Southwest-AirTran integration�andready the company to expand its international operations.

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

5

Southwest Airlines Co LUV [NYSE] | QQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry8.26 USD 12.00 USD 6.00 USD 21.00 USD Very High None . Airlines BBB-

Analyst Notes

Apr. 20, 2012 US Airways’ Labor Agreement Further Suggests it is Readying a Bid for Bankrupt AMR

US Airways issued a news release on April 20, saying thecompany reached agreements for collective bargainingagreements that would govern the American Airlinesemployees represented by the Transport Workers Union,Association of Professional Flight Attendants, and AlliedPilots Association. The release states that theseagreements are contingent upon a merger between USAirways and AMR, although there is no agreement at thistime.� �During its fourth-quarter earnings call, US Airwaysannounced that it retained financial advisors to exploreoptions for AMR. At the time, we concluded that USAirways would bid on AMR, and these agreements suggestUS Airways is far along in the process of launching a bid.�� �

As we said in late January, US Airways deserves credit forrightsizing its business and emerging as a strongercompetitor today. However, we believe US Airways needsto bulk up its network to compete in the industry, especiallyas closest competitor Southwest is readying forinternational flying by 2014. � �We expect to hear more from US Airways when it reportsnext week, but we wouldn’t be surprised if the companylaunches a bid within the next two quarters, especially ifAMR plans to exit bankruptcy by the end of this year.��

Apr. 19, 2012 Southwest Reports First-Quarter Earnings

Southwest Airlines reported first-quarter earnings onThursday that were mostly consistent with our projections,and we are maintaining our fair value estimate. Pro formarevenue increased 6% from the year-ago period, drivenentirely by higher ticket prices. Despite the growth, profitswere pressured by a 17% increase in fuel costs. As a result,operating margins contracted 170 basis points to 0.6%.However, Southwest’s meager profit was due to $170million benefit mostly related to fuel hedges. Without theeffect of hedges, the firm would have reported an $18million loss. � �We believe Southwest will remain in a state of flux until itcompletes its AirTran integration in 2014. Until then, thecompany will operate as two separate airlines, whereAirTran will maintain its business class and baggage fee,while Southwest sustains its no checked baggage fees.

Further, we expect Southwest will face the higher fuel priceenvironment with minimal hedge exposure, and believe thecompany will struggle to increase ticket prices further givenits large base of leisure travelers, who are more sensitiveto ticket prices. � �Despite these�headwinds, we think Southwest’s futurelooks better beyond 2014. The company announced itselected Amadeus, a reservations technology company, toprovide international capability to its domestic-only ticketsystems. This will become more important once therepealed Wright Amendment expires in 2014, which willallow Southwest to operate direct flights from Love Field(Dallas) to international markets. Coupled with the deliveryof larger 737-800 aircraft, we expect the company willbenefit immensely from international markets, and willlikely steal share from rivals.��

Jan. 19, 2012 Southwest Reports 4Q Earnings

Southwest Airlines reported fourth-quarter earnings on Thursday that were mostly consistent with our projections.��

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

6

Southwest Airlines Co LUV [NYSE] | QQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry8.26 USD 12.00 USD 6.00 USD 21.00 USD Very High None . Airlines BBB-

Analyst Notes (continued)

�Pro forma revenue increased 9% from the year-ago period,driven by a 9% increase in ticket prices and 2% greatervolume. Southwest did a commendable job of controllingmanageable expenses, as its costs per available seat mile,excluding integration items and fuel, budged only 0.5%higher versus the prior year. However, Southwest paid 34%more per gallon for fuel, which caused fuel expenses tosurge 30% higher than last year. As a result, operatingmargins contracted 240 basis points to 3.6%. �

�The AirTran integration is progressing well. Southwestnoted it is already producing more than $200 million in netannualized pre-tax synergies. We believe Southwest willexceed its $400 million synergy goal because the companynow has access to Atlanta-Hartsfield, the world’s busiestairport by annual number of passengers. Still, therealization of these savings depends on a successfulintegration.��

Nov. 29, 2011 As We Expected, AMR Succumbs to Bankruptcy

AMR Corporation , the parent of American Airlines,announced Tuesday that it is voluntarily filing for Chapter11 reorganization. On Oct. 21, we published our belief thatAMR would succumb to bankruptcy and that its commonequity would be worthless. We lowered our credit rating onAMR to CC on Monday, as we thought financial distresswas imminent. We are maintaining our current $0 fair valueestimate, but will lower our credit rating to D as a result ofthe filing.� �We believe that a bankruptcy filing, while difficult, is thecorrect move for AMR to cleanse its debt-laden balancesheet and bloated cost structure.�As of the third quarter,AMR held about $12 billion in debt and $7 billion in pensionliabilities compared with $4.3 billion in unrestricted cash($4.1 billion as of the bankruptcy filing date). We hadexpected the company’s cash balance to dwindle to $1.2billion at the end of 2012, which we opined was insufficientto operate an airline and repay 2013 debt commitments.� �We calculate that the pretax labor cost differentialbetween AMR and other legacy carriers over the past fewyears was $1.2 billion-$1.5 billion, nearly double AMR’sestimate of $800 million. Further, we calculate the cost ofoperating an antiquated fleet of aircraft cost AMR about

$115 million annually in additional costs for repair andmaintenance alone, versus the legacy carriers. This numberdoesn’t include the additional cost burn due to operatingfuel-inefficient aircraft or the opportunity cost of flyingapproximately one hour per day fewer�over AMR’s entirefleet.�Collectively, we believe these cost disadvantagescaused AMR to file for bankruptcy, and we believe thecosts were sufficiently burdensome that even if thecompany had signed a new labor deal with its pilots, itwould not have averted bankruptcy.� �There has been speculation of an AMR-US Airways mergerafter AMR’s bankruptcy. We believe this merger wouldmake sense, as US Airways employs a lower-cost structureand would be profitable on the domestic front, while AMR,given its strong international presence, would operate theinternational routes. However, we acknowledge thatcomplications exist, specifically pilot integration, that couldderail a merger.� �Even if a merger doesn’t occur, we expect that the AMRbankruptcy will benefit the industry. We think AMR wasextremely aggressive on pricing as it struggled to survive;now that the company will emerge with a leaner coststructure, we expect ticket prices will trend higher over the

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

7

Southwest Airlines Co LUV [NYSE] | QQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry8.26 USD 12.00 USD 6.00 USD 21.00 USD Very High None . Airlines BBB-

Analyst Notes (continued)

long term.�

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

Disclaimers & DisclosuresNo Morningstar employees are officers or directors of this company. Morningstar Inc. does not own more than 1% of the shares of this company. Analystscovering this company do not own its stock. The information contained herein is not represented or warranted to be accurate, correct, complete, or timely.This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.

8

Morningstar Stock Data Sheet Pricing data thru May 07, 2012 Rating updated as of May 07, 2012Pricing data thru May 07, 2012 Rating updated as of May 07, 2012 Fiscal year-end: December

Southwest Airlines Co LUV Sales USD Mil Mkt Cap USD Mil Industry Sector16,546 6,341 Airlines

Industrials

TMMorningstar Rating Last Price Fair Value Uncertainty Economic Moat Stewardship GradeQQQQ 8.26 12.00 Very High None .

per share prices in USD

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD

1.0

3.0

6.0

14.0

4.0

8.0

22.0011.11

19.6911.72

17.0612.88

16.9513.05

18.2014.61

16.9612.12

16.777.05

11.784.95

14.3210.42

13.597.15

10.057.76

Annual Price HighLowRecent Splits

Price VolatilityMonthly High/LowRel Strength to S&P 500

52 week High/Low12.44 - 7.15

10 Year High/Low22.00 - 4.95

Bear-Market Rank5 (10=worst)

Trading Volume Million

Stock Performance

Texas-based Southwest Airlines is the largest carrier in theUnited States as measured by the number of originatingpassengers boarded. Combined with its recent acquisition ofAirTran, Southwest operates a fleet of nearly 700 aircraftcomprising an all Boeing fleet. The airline specializes inshort-haul routes using a point-to-point network and offersfrequent flights to around 110 markets cities. The combinedfirm employs almost 46,000 workers andgenerates�approximately $17 billion in annual revenue on aconsolidated basis.

P.O. Box 36611 Dallas, TX 75235-1611Phone: 1 214 792-4000Website: http://www.southwest.com

Growth Rates Compound AnnualGrade: B 1 Yr 3 Yr 5 Yr 10 Yr

Revenue % 29.4 12.4 11.5 10.9Operating Income % -29.9 15.6 -5.8 0.9Earnings/Share % -62.3 -1.4 -17.7 -9.6Dividends % 0.0 0.0 0.0 0.0Book Value/Share % 6.7 10.0 1.8 5.5Stock Total Return % -31.6 4.8 -10.8 -7.5+/- Industry -23.3 -13.7 -4.6 -8.7+/- Market -33.2 -9.9 -8.9 -10.1

Profitability AnalysisGrade: D Current 5 Yr Avg Ind Mkt

Return on Equity % 4.0 5.0 14.2 22.2Return on Assets % 1.5 2.0 1.8 9.3Fixed Asset Turns 1.5 1.1 1.7 7.5Inventory Turns 19.0 20.1 30.7 16.8Revenue/Employee USD K 357.9 329.9 . 1035.3

Gross Margin % 56.8 58.3 52.6 40.1Operating Margin % 3.6 5.4 6.4 18.9Net Margin % 1.6 2.8 2.0 11.3Free Cash Flow/Rev % 3.7 . 3.7 0.1R&D/Rev % . . . 9.4

*

*3Yr Avg data is displayed in place of 5Yr Avg

Financial PositionGrade: C 12-11 USD Mil 03-12 USD Mil

Cash 829 1558Inventories 401 432Receivables 299 367

Current Assets 4345 5120

Fixed Assets 12127 12095Intangibles 970 1117

Total Assets 18068 18826

Payables 1057 1208Short-Term Debt 644 259

Current Liabilities 4533 5047Long-Term Debt 3107 3048

Total Liabilities 11191 11729

Total Equity 6877 7097

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TTM FinancialsRevenue USD Mil5522 5937 6530 7584 9086 9861 11023 10350 12104 15658 16546Gross Margin %51.1 52.9 52.5 52.6 49.5 46.2 59.8 63.6 63.9 57.9 56.8Oper Income USD Mil417 483 554 820 934 791 449 262 988 693 601Operating Margin %7.6 8.1 8.5 10.8 10.3 8.0 4.1 2.5 8.2 4.4 3.6

Net Income USD Mil241 442 313 548 499 645 178 99 459 178 271

Earnings Per Share USD0.30 0.54 0.38 0.67 0.61 0.84 0.24 0.13 0.61 0.23 0.35Dividends USD0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.02Shares Mil803 819 824 818 818 768 742 741 747 775 781Book Value Per Share USD5.69 6.40 7.09 8.42 8.14 9.46 6.70 7.34 8.34 8.83 9.24

Oper Cash Flow USD Mil520 1336 1157 2229 1406 2845 -1521 985 1561 1385 1645Cap Spending USD Mil-603 -1238 -1775 -1210 -1399 -1331 -923 -585 -493 -968 -1038Free Cash Flow USD Mil-83 98 -618 1019 7 1514 -2444 400 1068 417 607

Valuation AnalysisCurrent 5 Yr Avg Ind Mkt

Price/Earnings 23.8 39.3 14.8 15.1Forward P/E 8.2 . . 13.8Price/Cash Flow 3.9 . 4.6 7.9Price/Free Cash Flow 10.6 . 13.7 17.7Dividend Yield % 0.2 . 0.3 2.0Price/Book 0.9 1.3 2.3 2.2Price/Sales 0.4 0.7 0.4 1.3PEG Ratio 0.4 . . 1.8

Total Return %-24.7 16.2 1.0 1.0 -6.7 -20.3 -29.2 32.8 13.7 -33.9 -3.5+/- Market-1.3 -10.2 -8.0 -2.0 -20.3 -23.8 9.3 9.4 0.9 -33.9 -12.4+/- Industry-3.8 -15.4 -3.0 -25.1 -26.7 -9.0 14.4 7.5 -15.0 -8.6 -20.1

Dividend Yield %0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.1 0.2 0.2Market Cap USD Mil10796 12741 12692 13024 12131 8955 6376 8490 9702 6664 6341

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TTM ProfitabilityReturn on Assets %2.7 4.7 3.0 4.3 3.6 4.3 1.1 0.7 3.1 1.1 1.5Return on Equity %5.7 9.3 5.9 9.0 7.6 9.6 3.0 1.9 7.8 2.7 4.0

Net Margin %4.4 7.4 4.8 7.2 5.5 6.5 1.6 1.0 3.8 1.1 1.6Asset Turnover0.62 0.63 0.62 0.59 0.66 0.65 0.71 0.72 0.81 0.93 0.94Financial Leverage2.0 2.0 2.0 2.1 2.1 2.4 2.9 2.6 2.5 2.6 2.6

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 03-12 Financial HealthWorking Capital USD Mil798 590 30 -228 -286 -395 87 682 974 -188 73Long-Term Debt USD Mil1553 1332 1700 1394 1567 2050 3498 3325 2875 3107 3048Total Equity USD Mil4422 5052 5524 6675 6449 6941 4953 5466 6237 6877 7097Debt/Equity0.35 0.26 0.31 0.21 0.24 0.30 0.71 0.61 0.46 0.45 0.43

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TTM ValuationPrice/Earnings46.3 29.9 42.9 24.5 25.1 14.5 36.0 87.7 21.3 37.2 23.8P/E vs. Market. . . . . . . . . 2.1 1.6Price/Sales2.0 2.2 2.0 1.8 1.4 0.9 0.6 0.8 0.8 0.4 0.4Price/Book2.4 2.5 2.3 2.0 1.9 1.3 1.3 1.6 1.6 1.0 0.9Price/Cash Flow21.5 9.9 11.6 6.0 9.1 3.3 . 8.6 6.2 4.8 3.9

Quarterly ResultsRevenue

Rev Growth

Earnings Per Share

USD Mil Jun 11 Sep 11 Dec 11 Mar 12

% Jun 11 Sep 11 Dec 11 Mar 12

USD Jun 11 Sep 11 Dec 11 Mar 12

Most Recent Period 4136.0 4311.0 4108.0 3991.0Prior Year Period 3168.0 3192.0 3114.0 3103.0

Most Recent Period 30.6 35.1 31.9 28.6Prior Year Period 21.1 19.7 14.8 18.0

Most Recent Period 0.21 -0.18 0.20 0.13Prior Year Period 0.15 0.27 0.17 0.01

Industry Peers by Market Cap

Major Fund Holders

Mkt Cap USD Mil Rev USD Mil P/E ROE%

% of shares

Southwest Airlines C 6341 16546 23.8 4.0JetBlue Airways Corp 1377 4695 15.6 6.5

.

.

.

TTM data based on rolling quarterly data if available; otherwise most recent annual data shown.

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported. The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security. Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869. ß

®

9

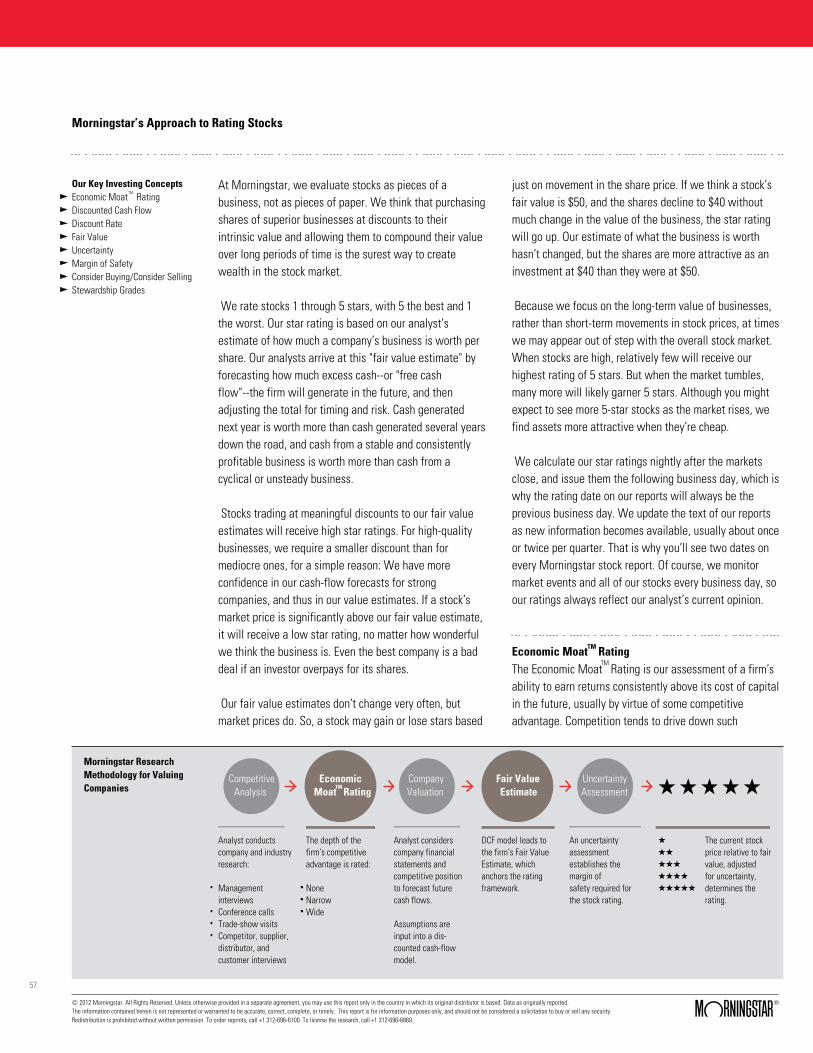

Morningstar’s Approach to Rating Stocks

Our Key Investing ConceptsEconomic Moat Rating��Discounted Cash Flow��Discount Rate��Fair Value��Uncertainty��Margin of Safety��Consider Buying/Consider Selling��Stewardship Grades��

TMAt Morningstar, we evaluate stocks as pieces of abusiness, not as pieces of paper. We think that purchasingshares of superior businesses at discounts to theirintrinsic value and allowing them to compound their valueover long periods of time is the surest way to createwealth in the stock market. We rate stocks 1 through 5 stars, with 5 the best and 1the worst. Our star rating is based on our analyst’sestimate of how much a company’s business is worth pershare. Our analysts arrive at this "fair value estimate" byforecasting how much excess cash--or "free cashflow"--the firm will generate in the future, and thenadjusting the total for timing and risk. Cash generatednext year is worth more than cash generated several yearsdown the road, and cash from a stable and consistentlyprofitable business is worth more than cash from acyclical or unsteady business. Stocks trading at meaningful discounts to our fair valueestimates will receive high star ratings. For high-qualitybusinesses, we require a smaller discount than formediocre ones, for a simple reason: We have moreconfidence in our cash-flow forecasts for strongcompanies, and thus in our value estimates. If a stock’smarket price is significantly above our fair value estimate,it will receive a low star rating, no matter how wonderfulwe think the business is. Even the best company is a baddeal if an investor overpays for its shares. Our fair value estimates don’t change very often, butmarket prices do. So, a stock may gain or lose stars based

just on movement in the share price. If we think a stock’sfair value is $50, and the shares decline to $40 withoutmuch change in the value of the business, the star ratingwill go up. Our estimate of what the business is worthhasn’t changed, but the shares are more attractive as aninvestment at $40 than they were at $50. Because we focus on the long-term value of businesses,rather than short-term movements in stock prices, at timeswe may appear out of step with the overall stock market.When stocks are high, relatively few will receive ourhighest rating of 5 stars. But when the market tumbles,many more will likely garner 5 stars. Although you mightexpect to see more 5-star stocks as the market rises, wefind assets more attractive when they’re cheap. We calculate our star ratings nightly after the marketsclose, and issue them the following business day, which iswhy the rating date on our reports will always be theprevious business day. We update the text of our reportsas new information becomes available, usually about onceor twice per quarter. That is why you’ll see two dates onevery Morningstar stock report. Of course, we monitormarket events and all of our stocks every business day, soour ratings always reflect our analyst’s current opinion. Economic Moat Rating The Economic Moat Rating is our assessment of a firm’sability to earn returns consistently above its cost of capitalin the future, usually by virtue of some competitiveadvantage. Competition tends to drive down such

TM

TM

Morningstar ResearchMethodology for ValuingCompanies QQQQQCompetitive Economic Company Fair Value Uncertainty

Analysis Moat Rating Valuation Estimate AssessmentTM

Analyst conducts The depth of the Analyst considers DCF model leads to An uncertaintycompany and industry firm’s competitive company financial the firm’s Fair Value assessmentresearch: advantage is rated: statements and Estimate, which establishes the� � competitive position anchors the rating margin ofManagement None to forecast future framework. safety required forinterviews Narrow cash flows. the stock rating.Conference calls Wide �Trade-show visits Assumptions areCompetitor, supplier, input into a dis-distributor, and counted cash-flowcustomer interviews model.

The current stockprice relative to fairvalue, adjustedfor uncertainty,determines therating.

QQQQQQQQQQQQQQQ

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

10

Morningstar’s Approach to Rating Stocks (continued)

economic profits, but companies that can earn them for anextended time by creating a competitive advantagepossess an Economic Moat. We see these companies assuperior investments. Discounted Cash Flow This is a method for valuing companies that involvesprojecting the amount of cash a business will generate inthe future, subtracting the amount of cash that thecompany will need to reinvest in its business, and usingthe result to calculate the worth of the firm. We use thistechnique to value nearly all of the companies we cover. Discount Rate We use this number to adjust the value of our forecastedcash flows for the risk that they may not materialize. For aprofitable company in a steady line of business, we’ll usea lower discount rate, also known as "cost of capital,"than for a firm in a cyclical business with fiercecompetition, since there’s less risk clouding the firm’sfuture. Fair Value This is the output of our discounted cash-flow valuationmodels, and is our per-share estimate of a company’sintrinsic worth. We adjust our fair values for off-balancesheet liabilities or assets that a firm might have--forexample, we deduct from a company’s fair value if it hasissued a lot of stock options or has an under-fundedpension plan. Our fair value estimate differs from a "targetprice" in two ways. First, it’s an estimate of what thebusiness is worth, whereas a price target typically reflectswhat other investors may pay for the stock. Second, it’s along-term estimate, whereas price targets generally focuson the next two to 12 months. Uncertainty To generate the Morningstar Uncertainty Rating, analystsconsider factors such as sales predictability, operatingleverage, and financial leverage. Analysts then classifytheir ability to bound the fair value estimate for the stockinto one of several uncertainty levels: Low, Medium, High,

Very High, or Extreme. The greater the level of uncertainty,the greater the discount to fair value required before astock can earn 5 stars, and the greater the premium to fairvalue before a stock earns a 1-star rating. Margin of Safety This is the discount to fair value we would require beforerecommending a stock. We think it’s always prudent tobuy stocks for less than they’re worth.The margin of safetyis like an insurance policy that protects investors from badnews or overly optimistic fair value estimates. We requirelarger margins of safety for less predictable stocks, andsmaller margins of safety for more predictable stocks. Consider Buying/Consider Selling The consider buying price is the price at which a stockwould be rated 5 stars, and thus the point at which wewould consider the stock an extremely attractivepurchase. Conversely, consider selling is the price atwhich a stock would have a 1 star rating, at which pointwe’d consider the stock overvalued, with low expectedreturns relative to its risk. Stewardship Grades Our corporate Stewardship Rating represents ourassessment of management’s stewardship of shareholdercapital, with particular emphasis on capital allocationdecisions. Analysts consider companies’ investmentstrategy and valuation, financial leverage, dividend andshare buyback policies, execution, compensation, relatedparty transactions, and accounting practices. Corporategovernance practices are only considered if they’ve had ademonstrated impact on shareholder value. Analystsassign one of three ratings: "Exemplary," "Standard," and"Poor." Analysts judge stewardship from an equity holder’sperspective. Ratings are determined on an absolute basis.Most companies will receive a Standard rating, and this isthe default rating in the absence of evidence thatmanagers have made exceptionally strong or poor capitalallocation decisions.

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

11

?

WellPoint Inc WLP [NYSE] | QQQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry66.60 USD 105.00 USD 73.50 USD 141.75 USD Medium Narrow . Health Care Plans A-

Currency amounts expressed with "$"are in U.S. dollars (USD) unlessotherwise denoted.

WellPoint 1Q Consistent With Our Expectations, butManagement Execution Remains a Weakness

by Matthew Coffina, CFASenior Stock AnalystAnalysts covering this company do notown its stock.

Pricing data through May 07, 2012.Rating updated as ofMay 07, 2012.

08 09 10 11 12

33.0

43.0

53.0

63.0

73.0Stock Price

Analyst Note Apr. 25, 2012 Our full-year estimates for WellPoint appear within reach,following the release of first-quarter results, and we aremaintaining our $105 fair value estimate. We continue toview WellPoint as meaningfully undervalued. Excluding investment gains, WellPoint’s first-quarterearnings per share declined by 1 cent to $2.34. A 10.6%decline in the share count was not enough to make up fora slightly larger decline in operating income. Operatingrevenue increased 3.4%, with more than half of thisgrowth attributable to the CareMore acquisition and therest the result of premium increases. Both the medical cost ratio (medical costs as a percentageof premium revenue) and the operating cost ratio (selling,general, and administrative expense as a percentage ofoperating revenue) deteriorated in the first quarter. Themedical cost ratio was up 120 basis points to 83.3%. Thefirst quarter is a seasonally strong quarter, and our modelincorporates an 85.3% rate for the full year with furtherdeterioration in subsequent years. The operating cost ratiowas worse than we expected, up 10 basis points to14.3%. We are counting on improvements in this metric tohelp offset medical cost pressures. We are discouraged by WellPoint’s membership results.The company shed 3% of local group and national accountmembers since the end of last year. Managementattributed this loss to disciplined pricing and competitivepressure. While trading off membership for margins isusually a good idea for managed-care organizations,WellPoint is experiencing both deteriorating membershipand margins. This is exactly the opposite of what wewould expect, as WellPoint’s scale should give it a costadvantage that enables it to grow membership withoutsacrificing margins. Management execution appears to belacking, particularly relative to peer UnitedHealth.

Thesis Feb. 27, 2012 WellPoint faces several risks, including�heightenedregulatory scrutiny of premium rate increases and thepossibility that health insurance exchanges will increasecompetition and erode the company’s economic moat. Onthe other hand, WellPoint enjoys a meaningful costadvantage from its unmatched combination of regionaland national scale. We believe recent share prices wellbelow our fair value estimate offer investors a reasonablemargin of safety.� Scale is critical in managed care for two reasons: it allowsmanaged-care organizations (MCOs) to spread fixedadministrative costs over more members, and it helpsthem to negotiate the best discounts with health-careproviders. WellPoint is one of the nation’s largest MCOsby medical membership, and the regional concentration ofits 14 Blue Cross and Blue Shield plans gives it aparticularly strong bargaining position with providers.� Health-care spending growth has consistently outpacednominal gross domestic product growth during the last 50years. Because health-care costs increase so rapidly andconsistently, it is essential for MCOs to raise premiums atleast in line with medical costs to prevent margincontraction. WellPoint underestimated its medical costtrends in 2008, leading to significant deterioration in itsmedical cost ratio (medical costs as a percentage ofpremium revenue). However, the company recognized itsproblem earlier than any of its peers and quickly raisedprices, leading to an almost immediate improvement inresults. We think this was a clear demonstration of thecompany’s pricing power and its dedication to rationalpricing.� While short-term fluctuations in medical cost trends arenearly impossible to predict, over the long run we expectmost MCOs to�try to�raise prices in line with average costgrowth. The sector is relatively consolidated, marginshave a much greater effect on the bottom line thanmembership levels, and customer relationships tend to besticky, so it generally isn’t worthwhile for an MCO toundercut its competitors on price.�

12

Morningstar’s Approach to Rating Stocks (continued)

economic profits, but companies that can earn them for anextended time by creating a competitive advantagepossess an Economic Moat. We see these companies assuperior investments. Discounted Cash Flow This is a method for valuing companies that involvesprojecting the amount of cash a business will generate inthe future, subtracting the amount of cash that thecompany will need to reinvest in its business, and usingthe result to calculate the worth of the firm. We use thistechnique to value nearly all of the companies we cover. Discount Rate We use this number to adjust the value of our forecastedcash flows for the risk that they may not materialize. For aprofitable company in a steady line of business, we’ll usea lower discount rate, also known as "cost of capital,"than for a firm in a cyclical business with fiercecompetition, since there’s less risk clouding the firm’sfuture. Fair Value This is the output of our discounted cash-flow valuationmodels, and is our per-share estimate of a company’sintrinsic worth. We adjust our fair values for off-balancesheet liabilities or assets that a firm might have--forexample, we deduct from a company’s fair value if it hasissued a lot of stock options or has an under-fundedpension plan. Our fair value estimate differs from a "targetprice" in two ways. First, it’s an estimate of what thebusiness is worth, whereas a price target typically reflectswhat other investors may pay for the stock. Second, it’s along-term estimate, whereas price targets generally focuson the next two to 12 months. Uncertainty To generate the Morningstar Uncertainty Rating, analystsconsider factors such as sales predictability, operatingleverage, and financial leverage. Analysts then classifytheir ability to bound the fair value estimate for the stockinto one of several uncertainty levels: Low, Medium, High,

Very High, or Extreme. The greater the level of uncertainty,the greater the discount to fair value required before astock can earn 5 stars, and the greater the premium to fairvalue before a stock earns a 1-star rating. Margin of Safety This is the discount to fair value we would require beforerecommending a stock. We think it’s always prudent tobuy stocks for less than they’re worth.The margin of safetyis like an insurance policy that protects investors from badnews or overly optimistic fair value estimates. We requirelarger margins of safety for less predictable stocks, andsmaller margins of safety for more predictable stocks. Consider Buying/Consider Selling The consider buying price is the price at which a stockwould be rated 5 stars, and thus the point at which wewould consider the stock an extremely attractivepurchase. Conversely, consider selling is the price atwhich a stock would have a 1 star rating, at which pointwe’d consider the stock overvalued, with low expectedreturns relative to its risk. Stewardship Grades Our corporate Stewardship Rating represents ourassessment of management’s stewardship of shareholdercapital, with particular emphasis on capital allocationdecisions. Analysts consider companies’ investmentstrategy and valuation, financial leverage, dividend andshare buyback policies, execution, compensation, relatedparty transactions, and accounting practices. Corporategovernance practices are only considered if they’ve had ademonstrated impact on shareholder value. Analystsassign one of three ratings: "Exemplary," "Standard," and"Poor." Analysts judge stewardship from an equity holder’sperspective. Ratings are determined on an absolute basis.Most companies will receive a Standard rating, and this isthe default rating in the absence of evidence thatmanagers have made exceptionally strong or poor capitalallocation decisions.

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

13

WellPoint Inc WLP [NYSE] | QQQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry66.60 USD 105.00 USD 73.50 USD 141.75 USD Medium Narrow . Health Care Plans A-

Close Competitors Currency(Mil) Market Cap TTM Sales Oper Income Net Income

WellPoint Inc

UnitedHealth Group Inc

Aetna Inc

Humana

USD

USD

USD

USD

22,033 61,232 3,841 2,577

57,319 103,712 8,560 5,184

14,931 34,308 2,968 1,911

13,253 37,860 2,128 1,352

Morningstar data as of May 07, 2012. On the other hand, regulators are becoming increasinglyactive in reviewing and preventing premium hikes that aredeemed excessive. While it is generally understood thatunderlying medical costs are the real driver of premiumgrowth, health insurance premiums are a far easier targetfor crusading regulators. If raising premiums becomes toodifficult, MCOs will�need to�find a way to hold downreimbursements to health-care providers, or else suffermargin contraction. On the plus side, WellPoint’s regionalscale still leaves it relatively well positioned to passpricing pressure through to providers.� We are also growing increasingly concerned aboutanother long-term risk: The emergence of health-insuranceexchanges may decentralize health insurance purchasingdecisions. In particular, there are early signs that healthinsurance benefits may be moving from a "defined benefit"model to a "defined contribution" model, similar to theshift that has occurred in retirement benefits. Employersvalue broad provider access at reasonable cost, whichWellPoint is ideally positioned to deliver. If individualsbecome the primary purchasers of insurance, they may bewilling to forgo broad provider access in exchange forlower costs at the providers they use the most. This couldopen the door to increased competition fromlimited-network regional plans and even�verticallyintegrated health�plans offered directly by large hospitalsystems. We will be watching this risk closely in thecoming years. Valuation, Growth and Profitability

We’re raising our fair value estimate for WellPoint to $105from $100 to account for cash earned since our lastupdate.�In our base case, we�project 4.9% compoundannual operating revenue growth during the next fiveyears. We expect the medical cost ratio to deterioratefrom 85.1% in 2011 to 86.5% over the long run. Weexpect selling, general, and administrative costs to declinefrom 14.1% of operating revenue in 2011 to 13.2% by2016. Overall, we expect operating income excludinginterest income to increase around 2% per year during thenext five years. Including share repurchases, we expectadjusted earnings per share to grow at a more robust10.6% per year. Using more optimistic assumptions, wethink operating income could grow 10.7% annually duringthe next five years, in which case our fair value estimatewould be $145 per share. Using more pessimisticassumptions, we think operating income could shrink9.3% annually during the next five years, resulting in a fairvalue estimate of $67 per share. We estimate WellPoint’scost of equity at 10.5%. Risk Regulatory changes could have sudden and unpredictableeffects� on WellPoint’s business. WellPoint’s results couldbe hurt by� regulation that limits the premiums the firm cancharge or mandates� the benefits it must provide, bydecreased funding of the Medicare� or Medicaid programs,or by new government programs that compete� with itsexisting business lines. Managed care is a highly�competitive industry, and battles over market share couldlead to� deteriorating underwriting standards that cut intoWellPoint’s� margins. Bulls Say

WellPoint has one of the largest medical membershipsamong health insurers, giving it significant bargainingpower with health-care providers and leveraging its

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

14

WellPoint Inc WLP [NYSE] | QQQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry66.60 USD 105.00 USD 73.50 USD 141.75 USD Medium Narrow . Health Care Plans A-

largely fixed cost structure. We think the market has overreacted to the threatposed by reform legislation. Some aspects of thelegislation are positive for WellPoint, such as the newfederal insurance subsidies and expansions to theMedicaid program. WellPoint also benefits from itsminimal exposure to Medicare Advantage. As the exclusive licensee of the Blue Cross and/or BlueShield brands in 14 states, WellPoint enjoys thebest-known and most-trusted brand name in thebusiness. This could be a particularly valuablecompetitive advantage in the health-insuranceexchanges. Unlike its peers in other states, WellPoint generallydoesn’t have to compete with nonprofit Blue Cross andBlue Shield plans, which can be a source of irrationalpricing and cyclicality. Because it is less geographically diverse than somepeers, WellPoint may face fewer local regulatoryhurdles as future opportunities for industryconsolidation arise. High regional market share alsoenhances bargaining power with providers.

Bears Say

The PPACA’s commercial medical cost ratio floorsdepressed margins in 2011. There is a risk that thefloors could be raised in the future, creating an ongoingmargin headwind. It is essential for WellPoint to stay ahead of shiftingmedical cost trends. Given WellPoint’s slim margins, asudden acceleration of cost trends can have a drasticeffect on earnings, as occurred in 2008. The PPACA included provisions that will enhanceregulatory oversight of premium increases. WellPointmay find it harder in the future to pass cost increasesthrough to customers. Rising unemployment results in a smaller market foremployer-based insurance, and fewer members can

result in deleveraging of WellPoint’s fixed costs.WellPoint faces an additional revenue headwind asemployers increasingly migrate to fee-based productsrather than risk-based products. As a Blue Cross and Blue Shield licensee, WellPoint hasto keep an unusually large amount of capital in reserve.The company’s $20 billion investment portfolio couldlose value if financial markets decline.

Financial Overview Financial Health: WellPoint’s financial health is solid. Wethink the company can generate normalized free cashflows of at least $2.5 billion annually, and balance sheetleverage is appropriate with a 30% debt/capital ratio. Company Overview Profile: WellPoint is one of the largest U.S. health insurersby medical membership, serving 34 million people. It holdsthe exclusive license to the Blue Cross and/or Blue Shieldnames in 14 states, including California, Georgia, NewYork, and Ohio. WellPoint’s business mix is weightedtoward the commercial market, with a particular focus onsmall-group coverage. Approximately 40% of members arein traditional risk-based products, with the remaining 60%in fee-based products. Management: We give WellPoint a fair stewardshipgrade. We were impressed by the speed with whichmanagement recognized and reacted to acceleratingmedical cost trends in 2008. On the other hand, ahigh-profile actuarial mistake in California in 2010resulted in a long delay in implementing a rate increaseand soured relationships with regulators across thecountry. WellPoint also did not�handle the health-reformdebate as proactively and positively as some peers.�In thelast couple of years, WellPoint has been slow to reduceadministrative costs in light of declining operating

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

15

WellPoint Inc WLP [NYSE] | QQQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry66.60 USD 105.00 USD 73.50 USD 141.75 USD Medium Narrow . Health Care Plans A-

revenue, though more recently management appears tohave gotten a better handle on costs. The long-overdue�ITsystems integration project could provide additionalsavings. We are encouraged by WellPoint’s dedication toreturning capital to shareholders through sharerepurchases, and we believe the repurchases madethrough the past few years’ tumultuous market createdsignificant value for long-term shareholders. WellPointhas been led by CEO Angela Braly since 2007. Braly wastrained as a lawyer and previously served as an executivevice president and general counsel. She spent two yearsas the CEO of Anthem Blue Cross and Blue Shield ofMissouri. Braly was also appointed chair of the board inearly 2010, though we would prefer that the CEO and chairpositions be separated. Braly’s 2010 total compensation of$13 million does not appear unreasonable for the industry,given WellPoint’s size.

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

16

WellPoint Inc WLP [NYSE] | QQQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry66.60 USD 105.00 USD 73.50 USD 141.75 USD Medium Narrow . Health Care Plans A-

Analyst Notes

Apr. 25, 2012 WellPoint 1Q Consistent With Our Expectations, but Management Execution Remains a Weakness

Our full-year estimates for WellPoint appear within reach,following the release of first-quarter results, and we aremaintaining our $105 fair value estimate. We continue toview WellPoint as meaningfully undervalued.� �Excluding investment gains, WellPoint’s first-quarterearnings per share declined by 1 cent to $2.34. A 10.6%decline in the share count was not enough to make up for aslightly larger decline in operating income. Operatingrevenue increased 3.4%, with more than half of this growthattributable to the CareMore acquisition and the rest theresult of premium increases. � �Both the medical cost ratio (medical costs as a percentageof premium revenue) and the operating cost ratio (selling,general, and administrative expense as a percentage ofoperating revenue) deteriorated in the first quarter. Themedical cost ratio was up 120 basis points to 83.3%. Thefirst quarter is a seasonally strong quarter, and our modelincorporates an 85.3% rate for the full year with furtherdeterioration in subsequent years. The operating cost ratiowas worse than we expected, up 10 basis points to 14.3%.

We are counting on improvements in this metric to helpoffset medical cost pressures.� �We are discouraged by WellPoint’s membership results.The company shed 3% of local group and national accountmembers since the end of last year. Managementattributed this loss to disciplined pricing and competitivepressure. While trading off membership for margins isusually a good idea for managed-care organizations,WellPoint is experiencing both deteriorating membershipand margins. This is exactly the opposite of what we wouldexpect, as WellPoint’s scale should give it a cost advantagethat enables it to grow membership without sacrificingmargins. Management execution appears to be lacking,particularly relative to peer UnitedHealth.�

Mar. 20, 2012 Supreme Court to Decide on the Constitutionality of the Affordable Care Act

From March 26-28, the U.S. Supreme Court will hear oralarguments on the constitutionality of the Patient Protectionand Affordable Care Act, or PPACA. The most importantprovisions of the health reform law will be implemented in2014, fundamentally transforming the country’s healthinsurance marketplace. Overturning the law throughlegislative means would be almost impossible in the nearterm, as that would likely require a filibuster-proof, 60-voteRepublican majority in the Senate (compared with 47Republican seats currently) and Republican control of thepresidency. The Supreme Court is therefore the last majorhurdle the legislation must pass before it becomesinextricably ingrained in our health-care system. A decision

is expected sometime in the summer.� �The court must decide four key questions. Mostimportantly, does Congress have the constitutionalauthority to require individuals to purchase healthinsurance, or else pay a penalty? This is by far the mostcontroversial provision in the law, as it marks the first timeCongress would compel individuals to purchase acommercial product. Opponents of the individual mandateargue that it amounts to regulating "inactivity" and fallsoutside of Congress’ powers under the Constitution’scommerce clause. Supporters of the provision argue thatnot carrying health insurance is a form of activity because

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

17

WellPoint Inc WLP [NYSE] | QQQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry66.60 USD 105.00 USD 73.50 USD 141.75 USD Medium Narrow . Health Care Plans A-

Analyst Notes (continued)

almost everyone will require health care at some point intheir lives, and without insurance the costs of that care willlikely fall to others.� �The individual mandate is viewed as a central componentof the PPACA, even though penalties for not carryinginsurance are modest (compared with the cost of healthbenefits) and the provision lacks enforcement. In 2014, thepenalty for not carrying insurance is the greater of $95 perindividual or 1% of taxable income. The penalty ramps upto $695 per individual or 2.5% of taxable income by 2016.There are various exemptions and caps to these standards.The penalty will be assessed through income tax returns,but failure to pay does not result in any criminal penalties.The primary enforcement mechanism will be withholdingtax refunds.� �If the individual mandate is ruled unconstitutional, the courtmust then decide what parts of the law, if any, can standwithout the individual mandate. In our view, insurancemarket regulations such as guaranteed issue (forcinginsurers to offer policies to all applicants) and modifiedcommunity rating (only allowing premiums to vary withintight bands based on characteristics such as age and familysize, while forbidding medical underwriting) would almostcertainly have to be eliminated from the law in this case.Otherwise, people would wait until they became ill topurchase insurance, destroying the market for individualinsurance nationwide. It is less clear whether other majorprovisions of the law, including the Medicaid expansionand insurance subsidies, could be allowed to stand withoutthe individual mandate.� �The other two questions are a bit of a sideshow to the mainact of the individual mandate. The court could conclude thatit cannot rule on the individual mandate yet because taxesto enforce it have yet to be collected. This would be adisappointing outcome, as it would prolong the currentstate of uncertainty for years and create a tremendous

mess if the law were later struck down after being fullyimplemented. The last question is whether the PPACA’sMedicaid expansion is overly coercive to the states. Wefind this to be the least compelling argument, as the federalgovernment will assume responsibility for the vast majorityof the incremental cost and states have the ability to optout of the Medicaid program altogether.� �We did not make any changes to our fair value estimatesfor managed-care organizations when the PPACA passedinitially. Modest negatives in the legislation such as limitson underwriting margins, increased regulatory scrutiny ofpremium rates, and Medicare Advantage reimbursementcuts were partly offset by positives like subsidies forindividual insurance and expansions to the Medicaidprogram. Managed-care organizations have also benefitedfrom mild utilization growth and disciplined pricing, whichhas offset any reform-related concerns. As a result, our fairvalue estimates for managed-care organizations havegenerally increased--in some cases significantly--in the twoyears since reform’s passage.� � Regardless of the Supreme Court’s decision, it is unlikelythat we would make any material changes to our fair valueestimates now. However, we think the most favorableoutcome for managed-care organizations at this pointwould be for the law to be upheld. Some aspects of reformare likely to persist even if the PPACA were struck down.For example, state-run insurance exchanges have gainedacceptance as a better way to organize the individual andsmall-group health insurance markets, and would likely bepursued by many states even in the absence of incentivesfrom the federal government. Enhanced state scrutiny ofpremium increases is also probably here to stay.Accountable care organizations have established a footholdas the care delivery systems of the future, and providerconsolidation is likely an irreversible trend. These aspectsof the health reform law are relatively negative for MCOs.� �

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

18

WellPoint Inc WLP [NYSE] | QQQQQTM

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat Stewardship Morningstar Credit Rating Industry66.60 USD 105.00 USD 73.50 USD 141.75 USD Medium Narrow . Health Care Plans A-

Analyst Notes (continued)

On the other hand, if the entire reform law were thrownout, provisions such as the expansion to Medicaid andindividual insurance subsidies are unlikely to be resurrectedin the current political climate, where concern about budgetdeficits has taken precedence over health-care access.These provisions were mostly good for MCOs and provided

an offset to some of the negative aspects described above.With the wheels of reform now set in motion, we thinkMCOs will be better off going forward if the entire law isupheld.�

Jan. 25, 2012 WellPoint 2012 Outlook Ahead of our Expectations, Shares Remain Undervalued

Investors were clearly disappointed by higher medical costsin WellPoint’s fourth quarter and a 2012 outlook that wasbelow Wall Street consensus. Shares plunged 6 percentearly Wednesday, further testing investors’ patience asWellPoint’s stock has consistently underperformed peersdespite being our top industry pick. However, both 2011results and the 2012 outlook were better than theestimates incorporated in our model, as we anticipatedsteadily deteriorating medical cost ratios. We aremaintaining our $100 fair value estimate and continue toview WellPoint as significantly undervalued.� �WellPoint’s 2011 earnings per share of $7.25 comparedwith $7.14 in our model. The 2012 outlook for "at least"$7.60 in earnings compares with our own estimate of$7.46. We were below consensus estimates on bothcounts, which explains why WellPoint can exceed ourexpectations while disappointing the market. Excludinginvestment gains and other unusual items, earningsincreased nearly 4% in 2011 and are projected to grow atleast 8.5% in 2012. We consider this a respectabletrajectory in light of regulatory headwinds.� �Thanks to heightened regulatory scrutiny of premium rates,we expect medical cost pressure to be a recurring themeduring the next five years. WellPoint’s fourth-quartermedical cost ratio (medical costs as a percentage ofpremium revenue) deteriorated 310 basis points to 87.6%.

Once again, management blamed much of the deteriorationon adverse selection in the Medicare Advantage business,particularly in California. The company hopes to correct thiswith plan design changes in 2012. However, this highlightsthe perils of WellPoint’s focus on Medicare expansion, asthis business is arguably outside of the company’s circle ofcompetence.� �For the full year, WellPoint’s consolidated medical costratio deteriorated 190 basis points to 85.1%. This was onlypartly offset by a 100 basis point improvement inadministrative costs as a percentage of operating revenue,as WellPoint’s aggressive cost control efforts resulted in a4.3% decline in administrative expenses. Full-year netincome was down more than 8%, but this was more thanoffset by a lower share count.� �Cash flow remains WellPoint’s greatest strength, with 2011free cash flow around $2.9 billion. With few internal cashneeds, most of this cash flow is available to be returned toshareholders. WellPoint repurchased 11.8% of itsoutstanding shares during 2011 for $3 billion. Sharerepurchases are likely to remain a priority for capitaldeployment as long as WellPoint’s stock remains soundervalued. The board also authorized a 15% increase tothe company’s dividend. However, with a payout ratio ofjust 15%, we continue to see room for significant dividendgrowth.�

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported.The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

ß ®

Disclaimers & DisclosuresNo Morningstar employees are officers or directors of this company. Morningstar Inc. does not own more than 1% of the shares of this company. Analystscovering this company do not own its stock. The information contained herein is not represented or warranted to be accurate, correct, complete, or timely.This report is for information purposes only, and should not be considered a solicitation to buy or sell any security.

19

Morningstar Stock Data Sheet Pricing data thru May 07, 2012 Rating updated as of May 07, 2012Pricing data thru May 07, 2012 Rating updated as of May 07, 2012 Fiscal year-end: December

WellPoint Inc WLP Sales USD Mil Mkt Cap USD Mil Industry Sector61,232 22,033 Health

Care Plans Healthcare

TMMorningstar Rating Last Price Fair Value Uncertainty Economic Moat Stewardship GradeQQQQQ 66.60 105.00 Medium Narrow .

per share prices in USD

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD

3.0

7.0

19.0

39.0

79.0

3.0 6.0

37.7523.20

41.4526.50

58.8836.10

80.4055.50

80.3765.50

89.9572.90

90.0027.50

60.8929.32

70.0046.52

81.9256.61

74.7363.34

Annual Price HighLowRecent Splits

Price VolatilityMonthly High/LowRel Strength to S&P 500

52 week High/Low81.92 - 56.61

10 Year High/Low90.00 - 23.20

Bear-Market Rank5 (10=worst)

Trading Volume Million

Stock Performance

2:1 2:1

WellPoint is one of the largest U.S. health insurers bymedical membership, serving 34 million people. It holds theexclusive license to the Blue Cross and/or Blue Shield namesin 14 states, including California, Georgia, New York, andOhio. WellPoint’s business mix is weighted toward thecommercial market, with a particular focus on small-groupcoverage. Approximately 40% of members are in traditionalrisk-based products, with the remaining 60% in fee-basedproducts.

120 Monument Circle Indianapolis, IN 46204Phone: 1 317 488-6000Website: http://www.wellpoint.com

Growth Rates Compound AnnualGrade: B 1 Yr 3 Yr 5 Yr 10 Yr

Revenue % 3.3 -0.3 1.3 19.2Operating Income % -9.1 8.2 -5.7 21.1Earnings/Share % 4.5 15.1 8.5 15.9Dividends % . . . .

Book Value/Share % 8.8 17.7 11.6 21.3Stock Total Return % -13.2 12.7 -3.7 7.3+/- Industry -15.8 -9.0 -6.0 -4.0+/- Market -14.8 -2.0 -1.8 4.7

Profitability AnalysisGrade: C Current 5 Yr Avg Ind Mkt

Return on Equity % 10.9 13.8 16.4 22.2Return on Assets % 5.0 6.3 5.8 9.3Fixed Asset Turns 46.4 56.2 46.5 7.5Inventory Turns . . 129.5 16.8Revenue/Employee USD K1624.2 1594.7 . 1035.3

Gross Margin % . . 13.6 40.1Operating Margin % 6.3 8.0 7.0 18.9Net Margin % 4.2 5.2 4.3 11.3Free Cash Flow/Rev % . . 4.7 0.1R&D/Rev % . . . 9.4

*

*3Yr Avg data is displayed in place of 5Yr Avg

Financial PositionGrade: B 12-11 USD Mil 03-12 USD Mil

Cash 2202 2279Inventories . .Receivables 4453 4665

Current Assets . .

Fixed Assets 1418 1455Intangibles 21790 21737

Total Assets 52019 52497

Payables 924 3938Short-Term Debt 1375 1011

Current Liabilities . .Long-Term Debt 8421 8463

Total Liabilities 28731 28968

Total Equity 23288 23528

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TTM FinancialsRevenue USD Mil13282 16771 20815 45136 56953 61134 61251 65028 58802 60711 61232Gross Margin %. . . . . . . . . . .Oper Income USD Mil906 1350 1586 4117 5318 5706 3122 7403 4354 3958 3841Operating Margin %6.8 8.1 7.6 9.1 9.3 9.3 5.1 11.4 7.4 6.5 6.3

Net Income USD Mil549 774 960 2464 3095 3345 2491 4746 2887 2647 2577

Earnings Per Share USD2.26 2.73 3.05 3.94 4.82 5.56 4.76 9.88 6.94 7.25 7.26Dividends USD. . . . . . . . . 1.00 1.04Shares Mil244 284 315 625 642 602 523 480 416 365 355Book Value Per Share USD18.96 21.69 70.10 40.56 39.64 42.42 42.10 55.28 63.04 66.95 71.12

Oper Cash Flow USD Mil991 1143 1303 3257 4044 4345 2535 3039 1417 3374 3483Cap Spending USD Mil-123 -111 -137 -162 -194 -322 -346 -378 -451 -520 -541Free Cash Flow USD Mil. . . . . . . . . . .

Valuation AnalysisCurrent 5 Yr Avg Ind Mkt

Price/Earnings 9.2 9.6 11.3 15.1Forward P/E 7.8 . . 13.8Price/Cash Flow 6.8 10.8 6.7 7.9Price/Free Cash Flow . . 8.6 17.7Dividend Yield % 1.6 . 0.8 2.0Price/Book 0.9 1.2 1.8 2.2Price/Sales 0.4 0.5 0.5 1.3PEG Ratio 0.7 . . 1.8

Total Return %27.1 19.2 55.3 37.5 -1.7 11.5 -52.0 38.4 -2.5 18.3 1.0+/- Market50.5 -7.2 46.3 34.5 -15.3 8.0 -13.5 15.0 -15.3 18.3 -7.9+/- Industry26.0 -29.0 9.1 -6.5 3.7 -11.6 -3.9 2.8 -12.4 -1.3 -7.3

Dividend Yield %. . . . . . . . . 1.5 1.6Market Cap USD Mil8897 10371 16162 49327 48789 47544 21446 26218 21478 23046 22033

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TTM ProfitabilityReturn on Assets %5.9 6.0 3.6 5.4 6.0 6.4 5.0 9.4 5.6 5.2 5.0Return on Equity %14.8 13.6 7.5 11.1 12.5 14.1 11.2 20.5 11.9 11.2 10.9

Net Margin %4.1 4.6 4.6 5.5 5.4 5.5 4.1 7.3 4.9 4.4 4.2Asset Turnover1.43 1.30 0.78 0.99 1.10 1.18 1.22 1.29 1.15 1.19 1.18Financial Leverage2.3 2.2 2.0 2.1 2.1 2.3 2.3 2.1 2.1 2.2 2.2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 03-12 Financial HealthWorking Capital USD Mil3428 4094 7787 11088 -3517 -1356 . . . . .Long-Term Debt USD Mil1659 1663 4277 6325 6493 9024 7834 8338 8148 8421 8463Total Equity USD Mil5362 6000 19459 24993 24576 22990 21432 24863 23813 23288 23528Debt/Equity0.31 0.28 0.22 0.25 0.26 0.39 0.37 0.34 0.34 0.36 0.36

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TTM ValuationPrice/Earnings13.9 13.8 19.1 20.3 16.3 15.8 8.8 5.9 8.2 9.1 9.2P/E vs. Market. . . . . . . . . 0.5 0.6Price/Sales0.6 0.6 0.9 1.0 0.9 0.9 0.4 0.4 0.4 0.4 0.4Price/Book1.7 1.7 0.8 2.0 2.0 2.1 1.0 1.1 0.9 1.0 0.9Price/Cash Flow7.7 9.3 14.1 14.0 12.5 12.2 8.7 9.2 16.7 7.4 6.8

Quarterly ResultsRevenue

Rev Growth

Earnings Per Share

USD Mil Jun 11 Sep 11 Dec 11 Mar 12

% Jun 11 Sep 11 Dec 11 Mar 12

USD Jun 11 Sep 11 Dec 11 Mar 12

Most Recent Period 15100.7 15398.0 15317.7 15415.2Prior Year Period 14457.2 14598.2 14647.9 14894.3

Most Recent Period 4.5 5.5 4.6 3.5Prior Year Period -6.2 -5.4 -23.1 -1.4

Most Recent Period 1.89 1.90 0.96 2.53Prior Year Period 1.71 1.84 1.40 2.44

Industry Peers by Market Cap

Major Fund Holders

Mkt Cap USD Mil Rev USD Mil P/E ROE%

% of shares

WellPoint Inc 22033 61232 9.2 10.9UnitedHealth Group I 57319 103712 11.5 18.7Aetna Inc 14931 34308 8.4 18.6

.

.

.

TTM data based on rolling quarterly data if available; otherwise most recent annual data shown.

© 2012 Morningstar. All Rights Reserved. Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. Data as originally reported. The information contained herein is not represented or warranted to be accurate, correct, complete, or timely. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security. Redistribution is prohibited without written permission. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869. ß

®

20

Morningstar’s Approach to Rating Stocks

Our Key Investing ConceptsEconomic Moat Rating��Discounted Cash Flow��Discount Rate��Fair Value��Uncertainty��Margin of Safety��Consider Buying/Consider Selling��Stewardship Grades��