insigniam quarterly spring 2015 - pathways to growth

TRANSCRIPT

VO L U M E 3 , I S S U E 1 | S P R I N G 2 015

SPECIAL FORCES Arcadis U.S. CEO and turnaround expert John Jastrem on transforming disaster into success.

COFFEE WITH AN ACCENTThe CEO of The Coffee Bean & Tea Leaf on expanding your enterprise overseas.

AN INSIDE PERSPECTIVE ON DRIVING GROWTH AMID THE DISRUPTION OF THE GLOBAL HEALTHCARE MARKET

™

FORWARD FACINGCardinal Health

Medical Segment CEO Donald Casey Jr. is

leading his company into the future.THE HEART

OF THE MATTER

The corporate culture acts like DNA, it holds the instructions and protocols that can drive dramatic

growth. When organic growth is hard to achieve and growth strategies wither and die, look to the corporate

culture. Transformational leadership sees to it that the corporate culture contains the elements that continually support a stream of dramatic growth.

— NATHAN O. ROSENBERG FOUNDING PARTNER, INSIGNIAM

LETTER

INSIGNIAM QUARTERLY 1

NFINDING THE FACTORS THAT FUEL GROWTHNo one disputes the science behind Mother Nature’s growth process. For plant life to flourish, the necessity of sunlight, water, and nutrients can’t be argued.

So why would we go about enterprise growth with any less certainty? After all, we have conducted thorough research to unearth the factors that lead companies to not just survive, but thrive. These prerequisites to growth can then be incorporated at every level.

Take corporate culture, for instance. Some may think that culture is too intangible to be molded. Yet our research, described in this issue, outlines nine specific facets of corporate culture and how they must be oriented for abundant growth. This, in turn, provides a clear road map for executives.

The same can be said for leadership. When executives fight inhibitory factors such as corporate myopia, and embrace risk and creative processes, growth through innovation is around the corner.

A quick glance at Fortune 500 companies reveals some truly exemplary case studies in growth, such as that of Cardinal Health, which ranks No. 22 on the esteemed list. Our in-depth interview with our cover subject, Donald Casey Jr., the CEO of the company’s medical segment, reveals how Cardinal Health has positioned itself for expansion during a time of unprecedented change in the healthcare industry. In many ways, Casey’s approach has taken into consideration the 10 disruptive forces in healthcare we identify in this issue, and Cardinal Health is now excelling into the future.

Even when an organization is riddled with apathy, suffering from dwindling profits, and facing a seemingly inevitable demise — we’ve found a fertile breeding ground for opportunity. We visit with turnaround expert and Arcadis U.S. CEO John Jastrem, who outlines what to do when it seems like the enterprise is out of options.

The truth is that, given the right tools and information, any company can take decisive action that will lead to expansion. And in that vein, I present our spring 2015 issue, which considers the many sides of corporate growth from multiple perspectives. Dramatic growth only appears to be just out of reach, and here at Insigniam, we eagerly look forward to partnering with you in the journey to achieve new corporate goals.

SPRING 2015

Shideh Sedgh BinaFounding Partner, Insigniam

SPRING 20152 INSIGNIAM QUARTERLY

46 10 DISRUPTIVE FORCES IN HEALTHCARE Insigniam Extensive research has unearthed the factors most affecting healthcare and the related steps companies can take to succeed.

48 GROWTH THROUGH ADVERSITY Stacey ClosserTurnaround expert and Arcadis U.S. CEO John Jastrem explains how you can transform disaster into untold success.

52 GROWTH WITH AN ACCENTJoe GuintoFrom cheeseburgers to lattes, The Coffee Bean & Tea Leaf CEO John Dawson understands how to transform domestic brands into global enterprises.

58 ORGANIC GROWTHRob CalderinAn in-depth look at the pathways to achieving organic growth, a top priority of C-suite executives in 2015.

FEATURES

THE HEART OF THE MATTER Chris WarrenAs the CEO of Cardinal Health’s Medical Segment, Donald Casey Jr. has positioned the company for dramatic growth through an innovative approach to the changing healthcare market.

COVER STORY38

TABLE OF CONTENTS

SPRING 2015 INSIGNIAM QUARTERLY 3

EDITOR-IN-CHIEF Shideh Sedgh Bina

EXECUTIVE EDITOR Nathan O. Rosenberg

CHIEF FINANCIAL OFFICER Ralph Gotto

DIRECTOR OF WORLDWIDE Karen Turner

CLIENT SERVICES [email protected]

DIRECTOR OF SPECIAL PROJECTS Alexes Fath

GENERAL MANAGER Jas Robertson

PRESIDENT Paul Buckley

EDITORIAL DIRECTOR Amy Robinson

MANAGING EDITOR Brian Keagy

CREATIVE DIRECTOR Kyle Phelps

ASSISTANT ART DIRECTOR Emily Slack

PRODUCTION MANAGER Pedro Armstrong

IMAGING SPECIALIST John Gay

ACCOUNT DIRECTOR Cory Davies

EDITORIAL QUERIES

750 N. Saint Paul Street

Suite 2100

Dallas, Texas 75201

www.dcustom.com

214.523.0300

For advertising information, contact Jas Robertson at

214.937.9811 or [email protected]

Insigniam Quarterly is published by D Custom, 750 Saint Paul Street, Ste. 2100, Dallas, Texas 75201. Copyright 2015 by Insigniam. All rights reserved. Letters to the editors may be sent to Insigniam Quarterly c/o D Custom, 750 Saint Paul Street, Ste. 2100, Dallas, Texas 75201. No part of this publication may be reproduced in any form or by any means without prior written permission of the publisher and Insigniam. Printed in the U.S.A. Magazine patents pending. For subscriptions, please visit www.insigniamquarterly.com.

QUART E R LY

VOLUME 3, ISSUE 1 | SPRING 2015

“We talk about it a ton. What are we doing to help our customers with their biggest challenges every day?”

— DONALD CASEY JR., CEO, CARDINAL HEALTH MEDICAL SEGMENT

THE TICKERInnovating your way to growth.

TOP LINEIndustries and markets experiencing explosive growth.

BLOOD, SWEAT & TEARSImplementing a global shared services department to produce international growth at The Hershey Company.

THE BOARDROOM Is your company using an outdated model for board of director involvement?

IQ BOOSTBuilding a passion for growth.

040810

14

64

18

24

28

32

DEPARTMENTS

On the cover:Cardinal Health Medical Segment CEO Donald Casey Jr.

VO L U M E 3 , I S S U E 1 | S P R I N G 2 015

SPECIAL FORCES Arcadis U.S. CEO and turnaround expert John Jastrem on transforming disaster into success.

COFFEE WITH AN ACCENTThe CEO of The Coffee Bean & Tea Leaf on expanding your enterprise overseas.

AN INSIDE PERSPECTIVE ON DRIVING GROWTH ADMID THE DISRUPTION OF THE GLOBAL HEALTHCARE MARKET

™

FORWARD FACINGCardinal Health

Medical Segment CEO Donald Casey Jr. is

leading his company into the future.THE HEART

OF THE MATTER

Insigniam and its publisher, D Custom, distribute this editorial magazine to share the opinions and insights of companies and their leaders on impactful global business issues. Insigniam Quarterly’s inclusion of a company or individual does not indicate that they are a client of Insigniam. Remuneration is not provided for editorial coverage. Individuals appearing in Insigniam Quarterly have done so with direct consent, or provided consent by a designated authorized agent in addition to being disclosed on the magazine’s audience and purpose.

MINI-FEATURES

™

LEADERSHIP FOR EXPLOSIVE GROWTHHow executives can build on enterprise strengths to create a process that leads to innovative growth.

UNLEASH CULTURE TO FUEL GROWTH Aligning the nine facets of corporate culture to prime any organization for success.

GROWTH FACTORS: TOP 10 EMERGING MARKETS An analysis of the major factors fueling the growth rates in these top emerging markets.

INVENTING GROWTHMove past traditional means of acquiring growth by developing an organization geared toward innovation.

THE TICKER

NO TOYING AROUND: LEGO’S ALL-STAR COMEBACK

esearch shows that children are spending less and time playing with LEGO bricks every year. Thankfully, LEGO corporate leaders are well aware of this trend — and that’s exactly why creativity is flourishing at the company, sales are booming, and the business surpassed rival Mattel to become the largest toy manufacturer in the world by revenue and profit in 2014. A firm believer in experimentation, LEGO has given its executives a simple mission: to routinely reinvent the business from the bottom up. Through the introduction of films, video games, apps, and augmented-reality experiences, senior leaders have quickly embraced that mandate.

It bears remembering that disruption didn’t always come naturally to the company. Thirteen years ago, LEGO was on the verge of stagnation, culminating in a disastrous 2002 holiday

season when 40 percent of its retail stock went unsold. So the company decided to slash costs and get back to basics. It doubled down on its core competency: mastering the mechanics of play. Conducting groundbreaking research on how children play, LEGO quickly gained insights few companies possessed. It parlayed these insights, along with its flair for design and cutting-edge R&D, into a rapid-fire barrage of new ventures and quickly staged an all-star comeback.

Recently hailed by Fast Company as “the Apple of toys,” the organization no longer sees itself as being in the business of playthings. Rather, recognizing that children no longer make meaningful distinctions between physical and digital interactions, it has repositioned itself as being in the business of “play experiences.” Poised to unleash an onslaught of groundbreaking new ventures from free motion-tracking games you can play with a wave of your hand to massive internet-ready apps, it just goes to show… even when the basic building blocks of a business seem to be crumbling, clever recombination is all it often takes to piece them back together.

11,755

$80 MILLION

$4.6 BILLION

LEGO’s 2013 revenue, which has more than doubled since 2009,

when it was $2.1 billion

Amount of money spent each year on R&D in 2013, up from $52 million in 2009.

Number of LEGO employees in 2013, an increase from 7,286 just four years prior.

SPRING 2015 INSIGNIAM QUARTERLY 5

Studies of the world’s most successful firms show that the fastest way to unlock your organization’s creativity and growth potential is through simply providing employees with f lexible platforms for brainstorming, sharing, and executing new ideas. An increasing number of business leaders, from Wells Fargo to Unilever, are embracing these collaborative brainstorming principles. Nearly a fifth of all enterprises now use cloud computing and websites to innovate — just one of many tools for capturing worker suggestions. But what’s even more eye-opening is how market leaders are using these tools to drive continuing growth and success.

For example: At big data leader EMC, business units pose pressing strategic problems to employees to solve via innovation contests. Workers can suggest solutions, source feedback, and vote for winning ideas online, which are transformed into real-world prototypes. Strikingly, though, many of the firm’s best new innovations are happening when employees independently team up to bring failing ideas to life. At personal finance-software developer Intuit, leaders go one step further. Employees can propose ideas, secure staffing and resources, and actually go to market with pilot programs, sans management approval — and dozens of revenue-generating features and products have resulted. Even government

THE POWER OF THE PLATFORM

agencies such as NASA and the Federal Trade Commission are now using crowdsourcing portals like Challenge.gov and offering cash prizes to the public for creating new, business-ready solutions. So the next time you want to spark ongoing growth and success? It frequently pays to get a second — or even 200th — opinion, just as the world’s most celebrated business leaders do.

INNOVATE FASTERWhen it comes to innovation, less is often more. According to a recent book Make Change Work for You: 10 Ways to Future-Proof Yourself, Fearlessly Innovate, and Succeed Despite Uncertainty, evolutions and slight shifts in thinking can be every bit as powerful as revolutions and game-changing breakthroughs. Here are five ways you can rapidly drive innovation in your enterprise without huge investments:

Constantly experiment with new products and strategies, iterating and improving, based on the results you get from the market.

Always look for ways to reposition your products toward new customers. Ask yourself: Who else might want our solutions? What new problems can we solve?

Build an environment that encourages colleagues to bring new ideas to light, and look for insight from unusual places — customers can be your best source.

Share information freely through departments. When teams are aligned, you can more easily bring about innovations.

Play a portfolio of strategic bets and innovative new ventures: These efforts can help you continually learn, grow, and stay ahead of the pack.

SPRING 20156 INSIGNIAM QUARTERLY

THE TICKER

INNOVATION FOR BREAKFASTWhy not start the day with a fresh, piping hot cup of oatmeal — served straight from your Keurig coffeemaker? Thanks to food manufacturer General Mills and the magic of open innovation, the choice is yours. With sales of cold cereals (representing about 22 percent of the firm’s U.S.-based business) down as much as 10.7 percent from 2003 to 2013, the company recently faced a difficult choice: Adapt or decline. With an increase in customers’ demand for grab-and-go convenience, the rising popularity of fast-food retailers’ $3 drive-through oatmeal cups, and the decrease in the amount of time most have to sit around the breakfast table, the company realized it had an

opportunity: It could use booming sales of single-serve coffeemakers as a way to reach today’s time-strapped customer. After internal brainstorming sessions, innovation teams created an early sketch of potential solutions. They then presented prospective ideas to their network of suppliers, and external vendors quickly came up with flavoring recipes, packaging, and prototypes. Following successful concept testing — General Mills setup a lemonade stand-style display in Minneapolis malls — its Nature Valley Bistro Cups quickly served up rapid success. As soon as the cups were launched on Amazon, they sold out; and they’re now carried in over 6,000 retail stores.

The next time you feel like the boss is looking over your shoulder at work, consider this: She could be sharing your desk instead. In fact, at industry-leading software developer Menlo Innovations, which has a roster of all-star clients such as AAA and Domino’s, teamwork is the most important driver of business growth. Two workers share every computer in the office, and partners and projects shift weekly, which makes for an unusual fit as senior executives and junior interns must often learn to cowork. But this switching system (borrowed from the airline industry) is no laughing matter. It not only helps facilitate creativity and innovation, it also helps open employees’ eyes to new perspectives. Through direct, hands-on mentorship and learning, workers are exposed to new influences, ingrain vital leadership skills, and facilitate ongoing knowledge transfer. Just how successful is Menlo’s buddy system? Ask the thousands of executives from firms ranging from Thomson Reuters to Toyota who now visit the business to learn from its strategies.

AT MENLO, EVERYONE STANDS TOGETHER

Menlo’s “switching system” is borrowed

from the airline industry.

6,000NUMBER OF RETAIL

STORES CARRYING THE NATURE VALLEY BISTRO

CUPS

22%OF GENERAL MILL’S

BUSINESS IS IN COLD CEREALS

Here’s how three leading organizations used the power of changing perspective and iterative growth strategies to quickly solve problems and create powerful results.

SIMPLE SHIFTS; HUGE WINDFALLS

AD

TARGETWhen retailer Target wanted to

increase revenues, it didn’t open more giant strip-mall outlets. It introduced pint-size CityTarget stores in highly trafficked urban areas selling locally branded merchandise and household goods (e.g. paper towels) in smaller packages. The concept’s been so successful that the chain has doubled the number of these stores in one year.

UNITED AIRLINESWith an average of 5,200 flights to 369

destinations a day, United Airlines is often faced with unforeseen weather delays and cancellations. During events such as these, it once took three to five minutes to rebook each inconvenienced passenger, even with a team of hundreds of agents. At a customer’s suggestion, United introduced an automated rebooking system that tracks flight progress — and in the wake of delays, the system can now reroute customers in just three seconds with no human interaction required.

MASTER LOCKThreatened by a flood of low-priced

foreign competitors, the padlock maker sought out niche markets for new products where it could exercise its brand-name advantage — continually repositioning these products until they reached max performance. For instance, a steering-wheel lock that initially failed when targeted at mainstream auto owners proved hugely successful when rebranded as a security device for trailers and towing vehicles.

PDMA2015PDMA2015ANNUAL CONFERENCENovember 7-11, 2015Disneyland HotelAnaheim, California

8 INSIGNIAM QUARTERLY SPRING 2015

TOP LINE

BY THE NUMBERSCOMPILED BY GEOFF WILLIAMS

$18 BILLIONThe amount of profits Apple earned in the first fiscal quarter of 2015, one of the highest in corporate history.

6,000%Uber’s growth in the

last five years. By mid-2014, the company was

valued at $18 billion.

750%Airbnb’s growth in the last five years. It’s now worth

$10 billion. Much of the reason for Apple’s growth in that quarter was due to this country. Revenue in China grew 70 percent.

ROBOTICS$15 billion in 2010

and expected to be $67 billion by 2025.

FITNESS$24 billion in 2015 and

expected to grow 23 percent in the next 10 years.

3-D PRINTING$3.8 billion in 2014 and projected to be

$16.2 billion by 2018.

ONLINE RETAIL SALES$263 billion in 2013 and expected to be $414 billion by 2018.

CHINA

INDUSTRIES EXPERIENCING EXPLOSIVE GROWTH

INSIGNIAM QUARTERLY 9SPRING 2015

36.1%Indian budget airline IndiGo’s current market share. Since its first flight took off in 2006, the innovative carrier has become the fastest-growing and largest airline company in India.

Ulta Beauty, based in Bolingbrook, Illinois, has tripled

its store count to 765 since 2007. In the third quarter of 2014, the

cosmetics company saw:

7.2 PERCENT AND 7.5 PERCENTProjections for India’s growth, this year and next. Next year, it’s expected that India will be the world’s fastest-

growing large economy.

THE GROWTH AND DEVELOPMENT OF PEOPLE IS THE HIGHEST CALLING OF LEADERSHIP.— HARVEY S. FIRESTONE, FOUNDER OF FIRESTONE TIRE AND RUBBER COMPANY

JET

GR

OU

P

IND

IGO

SPIC

EJET

AIR

IND

IA

GO

AIR

A 30 PERCENT INCREASE IN PROFIT.

A 21 PERCENT INCREASE IN REVENUE.

A 59 PERCENT INCREASE IN STOCK PRICES.(OVER 2014)

COMPANY GROWTH PROFILE

*ACCORDING TO THE WASHINGTON POST.

Founded by Milton S. Hershey in 1894, The Hershey Company has one of those enviable brands that people flock to — literally. Tourists from around the world descend on the small Pennsylvania town the company has called home since

1905 (the company started in Lancaster, Pennsylvania, in 1894) to visit Hershey’s Chocolate World to learn how chocolate is made and enjoy the (non-chocolate-fueled) rush to be had on the roller coasters and other rides at Hersheypark.

While few companies can brag that their consumers travel great distances to interact with their brand, six years ago Hershey executives were pondering how more of the company’s candy could return the favor, especially overseas. Indeed, while Hershey products — which include over 80

brands, such as Hershey’s Milk Chocolate Bars, Hershey’s Kisses, Reese’s Peanut Butter Cups, Jolly Rancher, Ice Breakers mints, and Brookside dark chocolates — were already sold in 50 countries around the globe, the majority

THE INSIDE OUT GAME

SPRING 2015

BLOOD, SWEAT & TEARS

To help the Hershey Company seize its global potential, Jeff Kemmerer first had to address unease and tap the talents of employees at the 121-year-old brand.BY GEOFF WILLIAMS

10 INSIGNIAM QUARTERLY

SPRING 2015

of its customers were in North America. The company’s executives understood that sustainable

growth required an aggressive push into dozens of new global markets. While a big component of success in reaching large numbers of consumers in places like China and India required understanding and adapting their products and marketing messages to suit local tastes, Hershey’s C-suite also understood that in order to flourish they would have to recalibrate some of their own internal infrastructure and operations.

Case in point: In order to serve its existing international customers, Hershey already had an international division with multiple off ices and manufacturing plants located around the globe, in places like Canada, Brazil, China, and Mexico. But that meant there was also a lot of redundancy and wasted resources involved with each country handling its own payroll, IT, shipping, and transportation. That sort of inefficiency could easily take an oversized bite out of the growth and profits it hoped to secure by attracting new customers around the world. The answer to this dilemma: the creation of a global shared services (GSS) department to uniformly handle these important responsibilities everywhere Hershey operated. In other words, GSS was a way for global Hershey operations to speak the same language internally so that the company could be more effective at pursuing the polyglot, often-complex international markets essential for growth.

UP FOR A CHALLENGEAlmost by definition, the establishment and smooth

functioning of GSS at Hershey would be simultaneously a complex task and, if done right, one that relatively few people at the company would even notice. That is, taking disparate and essential functions and processes occurring in far-flung corners of the world and making them uniform is a job that would only get someone noticed if it didn’t work.

To take on that formidable responsibility, Hershey’s then-CEO David J. West, who has since left to head up Del Monte, turned to 23-year company veteran Jeff Kemmerer. It was a logical choice. During his tenure at Hershey, Kemmerer had established a reputation and a track record as someone who was eager to take on tough projects. “Every time they’ve

EVERYTHING’S BEEN OUT OF MY COMFORT ZONE, AND SO EVERY TIME I BECOME COMFORTABLE, THEY’VE SAID, ‘OK, NOW WE’D LIKE YOU TO DO THIS.’

—Jeff Kemmerer, vice president of global shared services at The Hershey Company

come to me and asked me to take on a new challenge, I’ve always said, ‘yes,’ and each experience has been better than the previous one,” says Kemmerer. “Everything’s been out

of my comfort zone, and so every time I become comfortable, they’ve said, ‘OK, now we’d like you to do this.’”

Kemmerer had already shown an ability to lead and manage major change that involved unifying myriad processes. As director of Hershey’s Enterprise Solutions Center, a group charged with continuous improvement of integrated business processes, Kemmerer saved the company $20 million by instituting best practices and improving business and accounting processes. Additionally, Kemmerer spent two years as the director of Hershey’s sales f inance organization and then three-plus years as vice president of finance for Hershey Canada, Inc.

NOT JUST ABOUT THE NUMBERSWith his accounting and finance background, Kemmerer

clearly had a knack for understanding the numbers and metrics he needed to focus on to make GSS a success. But what was harder to predict — and every bit as important — was the human part of the equation. Would the employees Kemmerer needed to create a shared services organization be willing to embrace a fundamentally new course? “Jeff had the foresight to understand that while processes, systems, and structures are obviously important in most significant organizational changes, it is unquestionably

$7.4 billion in 2014

$5.3 billion in 2009

HERSHEY’S TOTAL REVENUE

INSIGNIAM QUARTERLY 11

BUILDING THE FUTUREKemmerer didn’t need to worry. As a result of his openness,

he didn’t have to contend with negative fallout from the announcement. But he also believes that transparency allowed him to build both trust and genuine enthusiasm for what GSS meant for Hershey.

“Jeff ’s commitment to building trust, being authentic and transparent, and taking risks demonstrates the kind of leadership required to be successful in an enterprise-wide change initiative,” comments Bonnie Wingate, partner at Insigniam. “The rewards can be significant, as they were with Hershey’s growth outside North America.”

Kemmerer knew that GSS was moving beyond its challenging transition period into one where a new culture

could be built when he started f ielding employee questions that had nothing to do with the safety of their jobs. “They were asking, ‘Can I play music?’ ‘Can I eat lunch at my desk?’ Every

SPRING 2015

BLOOD, SWEAT & TEARS

the people involved in and effected by the change that ultimately determine whether it will succeed or fail,” says Jon Kleinman, Insigniam partner.

Kemmerer began working on GSS as the vice president of the division in August of 2009. And although he took his time learning all about the existing processes and strategizing what changes would be necessary, he also knew from the beginning it would entail a substantial culture shift and a restructuring that would inevitably include job cuts. So, too, did the staffers he managed. “Whenever I’d introduce the shared service concept, many employees would say, ‘Just tell us who has a job and who doesn’t,’” he recalls. Kemmerer’s initial response to those questions was an indication of the sort of transparency and openness he now sees was essential to the successful establishment of GSS. “I don’t know. I need your help to figure that out,” he told anyone who asked about job security.

Which is not to say that a commitment to transparency didn’t mean that there weren’t bumps and lessons to learn along the way. During an initial two-day working session with the 140 employees who first populated GSS, Kemmerer learned that his employees fell into one of three categories: those who understood and cheered the wisdom of GSS, those who were ambivalent, and those who were steadfastly against the change GSS represented. “They were never going to buy in. You can’t worry much about them,” Kemmerer says now, though he admits that he wasn’t as forceful as he should have been with the dissidents. “I should have been more aggressive at identifying the blockers faster, the ones who don’t have the potential to grow.”

What he did do, though, was focus his attention on those who were uncertain about GSS and what it meant to them individually. Kemmerer regularly had lunch with 15 to 20 of those employees as a way to demonstrate that he genuinely wanted to hear their concerns and ideas. It didn’t start well. “I got a lot of blank stares,” he says about the first lunch meeting. But by being consistent about soliciting their input, a rapport, trust, and enthusiasm began to build. “They were asking me, ‘What about this?’ ‘Have you considered that?’” he recalls.

The cohesion Kemmerer was steadfastly building paid dividends when he let his lunchmates know that he would need to eliminate 30 to 40 positions. After hearing his explanation, his employees asked if they could share the news with their coworkers. Committed to transparency, Kemmerer said, “yes,” though he quickly had second thoughts. “I was sick to my stomach,” he says. “I thought, ‘What have I done?’”

Tourists from around the world flock to Hershey, Pennsylvania, to visit Hershey’s Chocolate World and Hersheypark.

12 INSIGNIAM QUARTERLY

SPRING 2015

conversation was about the work environment instead of whether a position would be eliminated,” he says.

What Kemmerer told employees not only answered their specific questions, but also helped lay the groundwork for the sort of culture he knew would be essential for GSS to flourish. As long as what they did at their desks didn’t negatively impact others, he had no problem with it. It was a way of reinforcing the idea that employees feel independent and empowered. “Every employee of shared service is a leader,” he says. “You don’t want employees waiting to be told what to do. We wanted an empowered environment.”

Six years after the launch of GSS, not all questions about the division’s role have been sorted out. There’s an ongoing and healthy debate about what work GSS should handle and what individual departments at Hershey should take on. And Kemmerer has been careful to tie the growth of GSS to that of the departments they serve.

Yet what is not in question is how GSS has helped fuel Hershey’s international growth. Hershey has seen its sales grow from $5.3 billion in 2009 to $7.4 billion last year,

and the company has now set $10 billion as its target. The most rapid growth has come from outside the United States, with Hershey now selling its products in 70 countries.

Nor is there any question in Kemmerer’s mind about what makes this kind of growth possible: people. “Employees are your most important asset, and you have to act that way even when you make difficult decisions, like letting a person go,” he says. “You first care about the person and focus on them being successful.”

In his own way, Kemmerer has helped expand Hershey’s reach around the world. And who knows, it might even mean a few new languages will soon be heard at Hershey’s Chocolate World and Hersheypark.

INSIGNIAM QUARTERLY 13

SPRING 201514 INSIGNIAM QUARTERLY

With implementation of the Sarbanes-Oxley controls now in place at most publicly held companies, many boards of directors are shifting attention to issues that are more likely to grow revenues and profits. A McKinsey survey (“The View From the Boardroom”) supports this shift in concluding that one-third of the company directors surveyed want to spend significantly less time on audit and compensation issues.

Many directors have expressed a desire to become more involved with their company’s strategic growth planning. The McKinsey study found that 75 percent of the directors surveyed want to spend at least a quarter of their board time dealing with the company’s business strategy, its risks, and maximizing growth opportunities.

Though just one survey, these conclusions support what many of us see in the boardroom every day: The pendulum of topics commanding directors’ attention is swinging from oversight and compliance back to where it should be focused on the company’s growth plans. Boards do their jobs best when challenging the CEO to grow revenue, asking questions, and vetting the strategic plan. That’s how directors increase shareholder value.

The attention of boards of directors is swinging away from oversight back to where it should be, focusing on company growth. BY JOHN REHFELD

THE COMPANY DIRECTOR’S ROLE IN COMPANY GROWTH

THE BOARDROOM

SPRING 2015 INSIGNIAM QUARTERLY 15

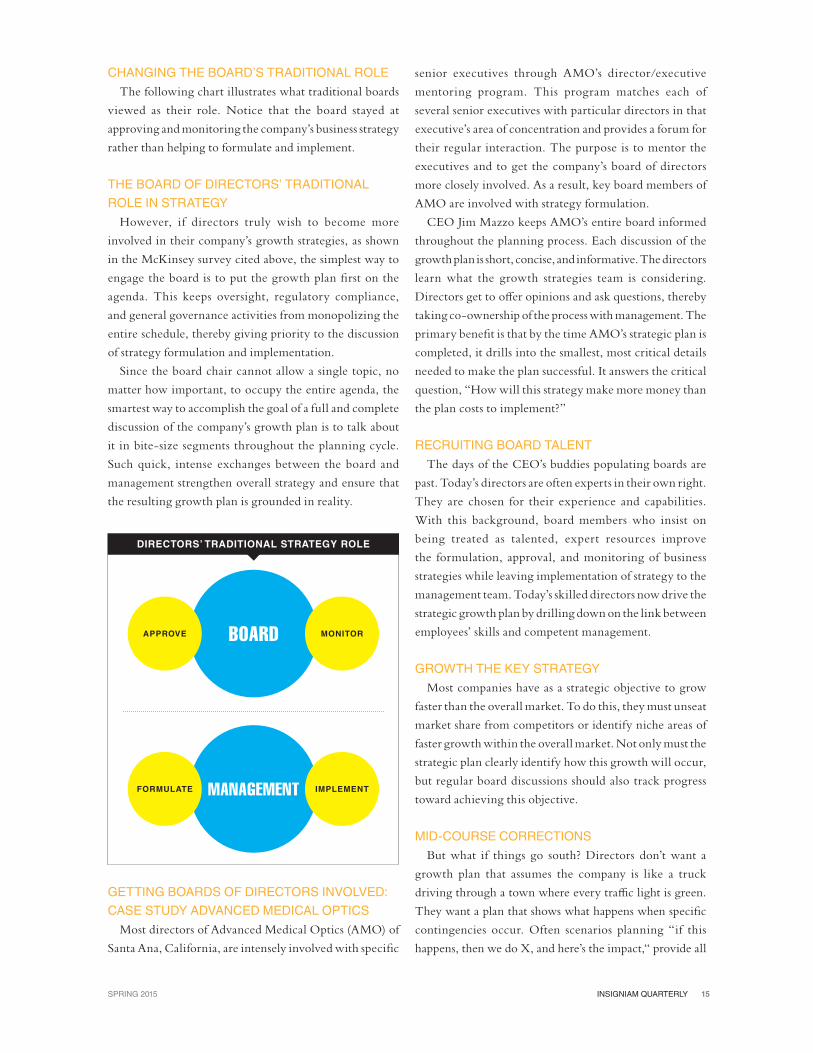

CHANGING THE BOARD’S TRADITIONAL ROLEThe following chart illustrates what traditional boards

viewed as their role. Notice that the board stayed at approving and monitoring the company’s business strategy rather than helping to formulate and implement.

THE BOARD OF DIRECTORS’ TRADITIONAL ROLE IN STRATEGY

However, if directors truly wish to become more involved in their company’s growth strategies, as shown in the McKinsey survey cited above, the simplest way to engage the board is to put the growth plan first on the agenda. This keeps oversight, regulatory compliance, and general governance activities from monopolizing the entire schedule, thereby giving priority to the discussion of strategy formulation and implementation.

Since the board chair cannot allow a single topic, no matter how important, to occupy the entire agenda, the smartest way to accomplish the goal of a full and complete discussion of the company’s growth plan is to talk about it in bite-size segments throughout the planning cycle. Such quick, intense exchanges between the board and management strengthen overall strategy and ensure that the resulting growth plan is grounded in reality.

GETTING BOARDS OF DIRECTORS INVOLVED: CASE STUDY ADVANCED MEDICAL OPTICS

Most directors of Advanced Medical Optics (AMO) of Santa Ana, California, are intensely involved with specific

senior executives through AMO’s director/executive mentoring program. This program matches each of several senior executives with particular directors in that executive’s area of concentration and provides a forum for their regular interaction. The purpose is to mentor the executives and to get the company’s board of directors more closely involved. As a result, key board members of AMO are involved with strategy formulation.

CEO Jim Mazzo keeps AMO’s entire board informed throughout the planning process. Each discussion of the growth plan is short, concise, and informative. The directors learn what the growth strategies team is considering. Directors get to offer opinions and ask questions, thereby taking co-ownership of the process with management. The primary benefit is that by the time AMO’s strategic plan is completed, it drills into the smallest, most critical details needed to make the plan successful. It answers the critical question, “How will this strategy make more money than the plan costs to implement?”

RECRUITING BOARD TALENTThe days of the CEO’s buddies populating boards are

past. Today’s directors are often experts in their own right. They are chosen for their experience and capabilities. With this background, board members who insist on being treated as talented, expert resources improve the formulation, approval, and monitoring of business strategies while leaving implementation of strategy to the management team. Today’s skilled directors now drive the strategic growth plan by drilling down on the link between employees’ skills and competent management.

GROWTH THE KEY STRATEGYMost companies have as a strategic objective to grow

faster than the overall market. To do this, they must unseat market share from competitors or identify niche areas of faster growth within the overall market. Not only must the strategic plan clearly identify how this growth will occur, but regular board discussions should also track progress toward achieving this objective.

MID-COURSE CORRECTIONSBut what if things go south? Directors don’t want a

growth plan that assumes the company is like a truck driving through a town where every traffic light is green. They want a plan that shows what happens when specific contingencies occur. Often scenarios planning “if this happens, then we do X, and here’s the impact,“ provide all

BOARDAPPROVE MONITOR

MANAGEMENTFORMULATE IMPLEMENT

DIRECTORS’ TRADITIONAL STRATEGY ROLE

SPRING 201516 INSIGNIAM QUARTERLY

the insight necessary. Certainly, directors need the business and industry background to know what critical questions to ask and how to accurately interpret the responses. Such questions frequently facilitate healthy board discussion. They often take the following forms:

6 What are the potential upside and downside of specific contingencies?

6 What is the probability of each? 6 What events must happen for the upside or downside

contingency to occur? 6 Can the board of directors control any of the

contingencies? 6 What are some alternatives and options for dealing

with contingencies, assuming the best case and worst case scenarios?

HARNESSING BOARD TALENTS: CASE STUDY PRIMAL SOLUTIONS

Getting the board involved in formulating, approving, and monitoring the company’s strategy engages directors’ often ignored capabilities. A good example is the management of VoIP software producer, Primal Solutions. Management quickly realized that the board not only wanted to participate in strategy formulation, but that its members also had more experience in formulating business strategy than did many management teams of companies considerably larger than Primal Solutions with its $10 million in sales.

Primal Solutions’ CEO asked the lead director and one advisory council member to work with the management team to formulate the company’s business strategy. Together, they filled specific experience gaps. As directors, their intent was to guide, help avoid pitfalls, and empower the CEO throughout the process. Their role was to stay in the background and support the discussions rather than to dominate them.

Five members of the management team, a member of the board of directors and an outside facilitator shaped Primal’s business strategies and the plan to achieve them over one two-day meeting and three subsequent one-day meetings. The board member’s presence added to the sense of urgency and seriousness that the project demanded.

The resulting strategic plan reorganized the company into two different business units. The plan also recommended some strategic personnel changes needed to implement the plan. These changes would not likely have occurred as quickly had the strategic plan not been treated as a blueprint to be followed by management and monitored by the board.

Primal Solutions’ approach succeeded because they

followed these important rules:

6 Schedule significant time — several full days in this case — to hold meaningful conversations.

6 Create an atmosphere that makes the strategic planning team feel like it’s okay to challenge and question assumptions, and it’s okay not to know the answer, because we’re all working toward a common goal: to increase shareholder value.

6 Review the broad competitive landscape and alternative market scenarios.

6 Hold subsequent meetings to review and approve each stage of the strategic growth plan.

6 Devise a scheme to measure specific metrics used to track plan implementation and performance.

6 Reserve significant parts of each board meeting to devote to the company’s growth strategy.

6 Benchmark and monitor the company’s market position compared to that of its competitors.

6 Identify and track the two or three capabilities that are critical to achieving success.

TAPPING THE BOARD OF DIRECTORS’ SPECIAL TALENTS

Two simple questions that are very important to formulating the company’s strategic plan can help identify possible shortfalls in the board’s capabilities:1 What essential areas of expertise, technical know-

how, and experience does the growth plan require?2 What inventory of this expertise, technical know-

how, and experience does each board member bring to the table?

Getting the answers to these questions may require a competency assessment either by the board itself or by the strategic planning team. Along with board members who have technical qualifications, directors recruited to help formulate the strategic growth plan must be evaluated regarding their attitudes, values, time constraints, abilities to work cooperatively, and desire to contribute to the team’s success.

USING AN ADVISORY BOARD: CASE STUDY SONIC FOUNDRY

What if the board doesn’t have the necessary qualifications to help with the strategic growth plan? It is difficult to quickly change the composition of the statutory board. However, a company can swiftly create and enable an advisory board with relevant experience and industry contacts.

THE BOARDROOM

SPRING 2015 INSIGNIAM QUARTERLY 17

A good example of this is Sonic Foundry (SoFo), a company that created a real-time multimedia presentation recorder and web communications system. SoFo’s growth strategy requires them to cross the chasm by moving sales from customers who are strictly early adopters to customers who are in the mainstream market. Since SoFo is a small company, the business strategies team consisted solely of the CEO and the head of sales and marketing. Owing to the company’s prior business and rapid evolution, the statutory board lacked the distance learning and distribution experience needed to help management create the strategic plan. Even worse, SoFo’s small window of opportunity to stay competitive didn’t allow time to recruit statutory board members who had the right backgrounds. Instead, they quickly formed an advisory board. The full 10-person advisory board meets twice a year. However, the smaller, specialized committees such as the growth strategies committee meet considerably more often.

SoFo’s use of committee members from the advisory board expanded the growth strategy team’s depth and experience. SoFo’s strategic planning process resulted in a number of key decisions being made, such as unbundling the products to make them easier to use and moving the purchase decision from their customers’ IT departments to the end users. SoFo also raised prices and began charging for features that they had once just given away. Profit margins rose.

Today, SoFo has a formalized strategic planning process that holds three one-day meetings annually and involves the management team and the advisory board. The management team reports back to the advisory board on lessons learned and actions taken. Like Primal Solutions’ board, SoFo’s advisory board members participating in formulating the company’s growth strategies are not interested in dominating the discussions. Rather, their mission is to add expertise to planning deliberations and to empowering the CEO.

MANAGING THE BOARD’S AGENDABoard meetings are busy affairs. Adding one more thing

to an already crowded agenda can be disruptive. If that additional thing is something so critical to the company’s future value as business growth strategies, then the board must create a new paradigm to manage its agenda.

Boards that want more involvement in formulating company growth strategies create a strategic review committee. This committee draws out the board’s expertise, but doesn’t take huge chunks of board time, since

the committee meets off-line, often with key members of the management team. The strategic review committee saves the board time by communicating and prompting board discussion on strategic direction, identifying and monitoring business drivers, keeping an eye on and responding to major strategic issues, and understanding the company’s competitive position all of which are among the board’s responsibilities in providing strategic oversight.

PROVIDING DIRECTORS THE INFORMATION THEY NEED

Engaged directors often first want to understand the market. They need independent information showing market size and market share for both the company and for competitors. They want to see sales trends in the market place and to identify where new customers are entering the market while the old standbys may be exiting from it. Savvy directors make the connection between those market segments and niches that are expanding and those that are contracting. They link that information with key points in the strategic growth plan and then reach their conclusions.

CONCLUSIONWith some advance attention to likely concerns and

questions, members of boards of directors gain greater confidence that the planning team has looked into all the areas that hold potential opportunity or threat for the company. Such oversight often requires individual members of the board and outside advisors with specific expertise to become involved in the strategic planning process. The board of directors empowers the CEO to lead the company’s planning process and provides a sometimes necessary assist to create the final plan. With this higher level of involvement, the board of directors has all the information it needs to thoroughly discuss the growth plan and to approve its implementation.

Look for boards of the future to become increasingly involved, not only in approving and monitoring their company’s business strategies, but also in offering concrete advice to the management team in strategic formulation and implementation. Because directors are more qualified now than ever before, expect them to use their vast experience to help grow revenues and profits.

Reprinted with permission from the Graziadio Business Review.

proprietary process for creativity and execution. To create a system that leads to better innovation and more successful marketing, executives must first know how to overcome factors inherent in organizations that all too often limit the business’ ability to grow.

1 CORPORATE GRAVITYKodak knew film, and it did film very well. It

created the industry for personal cameras. But the company did not anticipate when or how quickly the market — the very market it generated and led — would move to digital. The reason: Kodak was caught in its own corporate gravity; it was stuck in an orbit around a core product.

Too many companies find themselves in similar situations. They develop a core product or service, one that produces a growing income stream that supports much of the company. Understandably, then, companies organize themselves around that core, setting up rules, structures, and systems

Peter Drucker boldly declared that “business has only two functions — marketing and innovation. Marketing and innovation produce results,” Drucker wrote in his seminal 1954 tome, The Practice of Management. “All the rest are costs.”

The world of business has changed a lot in the 61 years since Drucker published those words. But he is still right. Executives who boost innovation or improve effective marketing — and especially those who succeed in doing both — are the leaders who will help their companies achieve explosive growth.

But that kind of growth also requires that leaders build on the inherent strengths of the enterprise to create a

SPRING 201518 INSIGNIAM QUARTERLY

BY NATHAN O. ROSENBERG AND SHIDEH SEDGH BINA

LEADING FOR EXPLOSIVE GROWTH

SPRING 2015 INSIGNIAM QUARTERLY 19

to protect it and keep the income stream flowing. But once the business model is organized around that

core product or service, management may begin to perceive change — specifically, change that could launch them into new markets or create new business models that eat into the core business model — as threats. Stray too far from the core, the thinking goes, and you might end up cannibalizing or even destroying the source of the enterprise’s success.

In practical terms, corporate gravity might occur when a chief financial officer sets hurdle rates for investments that are too high for most innovations to clear. To be sure, high hurdle rates will protect the core product. And while it is easy to calculate the value of an improvement to the core product or service, the CFO may get conservative when calculating returns on a new way of doing business. That often unrecognized prejudice will weigh down innovations so that they never get off the ground and find their true value in the marketplace.

Arbitrary decision-making has the same impact. Insigniam recently worked with one company that wanted

to accelerate new product launches. It had been debuting one new product every two years and wanted to dramatically change that by unveiling one new product per quarter. That required a substantial amount of product testing. But after a few months the testing ground to a halt. Why? Because the company president ignored the test results and made the call on which new products would make it to market. As a result, the employees saw no reason to champion new ideas, because there were no guidelines for knowing whether their ideas had a chance of ever being produced.

Even when guidelines are in place, corporate gravity can weigh down the creative process. For example, we consulted with a pharmaceutical company recently that experienced a drop in market share for one of its major products to No. 2 from the No. 1 position, and other products were beginning to falter. We discovered that the CEO had recently established a regulatory review panel. The team’s primary task was to make sure the company never again ran afoul of regulators. That task may have been a worthy one. But to achieve it, the review panel swung to a “no risk is

SPRING 201520 INSIGNIAM QUARTERLY

the best risk” policy and simply killed most new marketing initiatives that came before it. While not intentional, it had the effect of stopping any new creativity and the potential innovation that could follow.

2 CORPORATE MYOPIAWhen a company is unable to recognize future

value, it has developed corporate myopia. This short-sightedness may spring from judging value in a time period that is too immediate or from the inability to see value through the customer’s eyes. It is a dangerous condition. When companies can only see what’s in their immediate future and that which only relates to their current mix of products or services, they fail to envision revolutionary new ideas on the marketing or innovation side. That leaves room for competitors to step in.

A consumer goods company lost a rapidly growing category that currently generates about $500 million in annual sales due to corporate myopia. The company had the technology for what would eventually be sold as the Swiffer Sweeper. But they could not see the value in a product because they were focused too narrowly on the way that houses had been cleaned in the previous decade. Once the company passed on the Swiffer concept, a competitor bought it, redefined household cleaning, and created a new product franchise.

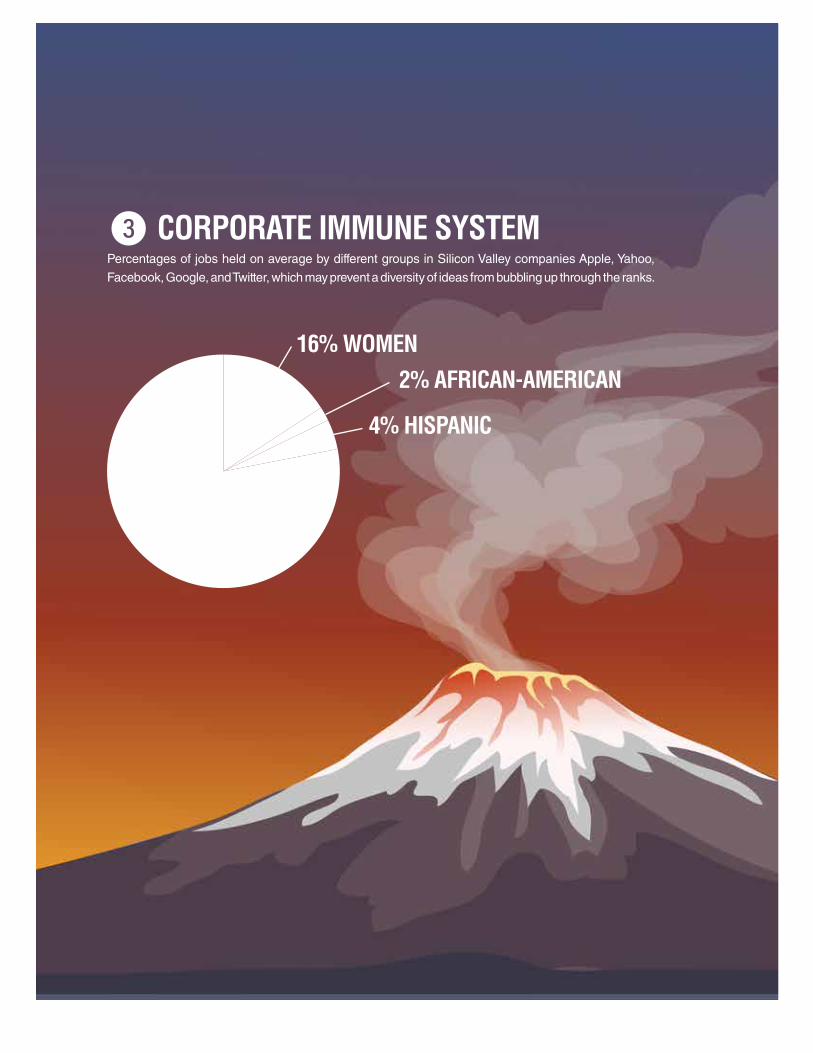

3 CORPORATE IMMUNE SYSTEM

The human immune system works hard to kill off foreign bodies, the things that might hurt us.

Organizations do that, too, working to kill off dangers of all kinds. That is sometimes good. But occasionally the corporate immune system simply attacks anything unfamiliar, even ideas that could breath new life into the organization.

Take the diversity issues now facing many Silicon Valley firms for example. The workforces at the top tech companies are mostly comprised of white or Asian men. In 2014, Google, for instance, employed more than 46,000 people, but just 2 percent were African-American. Inside Google’s tech division, more than 80 percent of workers were male and 60 percent of them were white. Apple, Yahoo, Facebook, and Twitter have all recently reported similar numbers.

The problem, many think, is not outright racial or gender bias on behalf of the top tech firms. In fact, the point is not gender or race; it is diversity of experience that will lead to new and better ideas. In this case, the thinking is that Silicon Valley executives and managers simply tend to recruit workers who come from the same backgrounds as themselves and have the same perspectives and styles that the executives and managers themselves exhibit. Leaders in all kinds of companies suffer from that same kind of indirect bias when they hire people who resemble themselves in one way or another.

That is what a corporate immune system does: It simply tries to replicate the sources of its prior success and all too often views anything new as a potential threat to future success. That’s a force that can greatly inhibit innovation and growth.

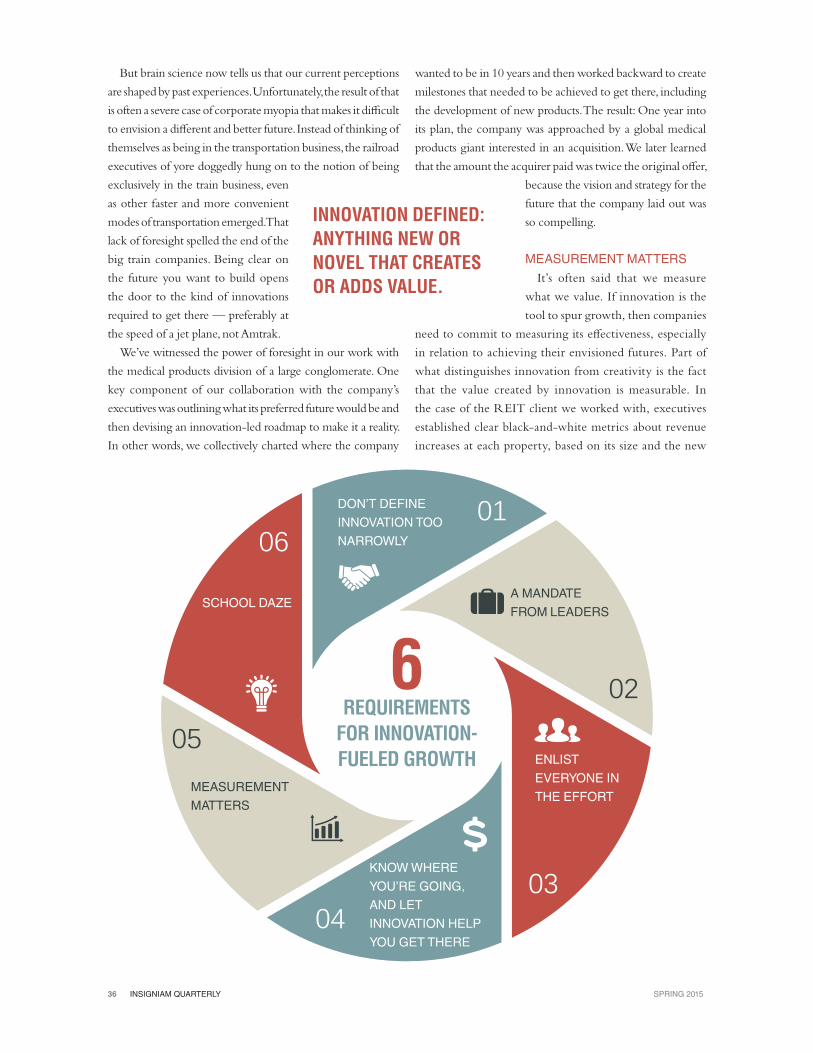

INSPIRE CREATIVITY AND GROWTHLeaders who want to avoid the inherent problems with the

corporate immune system, corporate myopia, and corporate gravity will want to create a process that identifies factors that inspire creativity and growth and identifies ones that inhibit creativity and growth. That method can take any number of forms, but whatever the shape, it must do three things: embrace risk, create a process for creativity, and measure the creation of value in ways other than traditional profit and loss statements.

Embrace RiskWayne Delker, the just-retired chief innovation officer

at Clorox, has long managed a massive portfolio of R&D projects, many of which are product redesigns. That could involve anything from putting grooves in Kingsford charcoal briquettes to reduce the weight of the bag and make the charcoal to burn hotter to inventing a product like the ToiletWand. “We have to simultaneously innovate across those different product lines to keep the brands healthy,” Delker said recently.

WHEN COMPANIES CAN ONLY SEE WHAT’S IN THEIR IMMEDIATE FUTURE AND THAT WHICH ONLY RELATES TO THEIR CURRENT MIX OF PRODUCTS OR SERVICES, THEY FAIL TO ENVISION REVOLUTIONARY NEW IDEAS ON THE MARKETING OR INNOVATION SIDE. THAT LEAVES ROOM FOR COMPETITORS TO STEP IN.

SPRING 2015 INSIGNIAM QUARTERLY 21

Clorox executives do not always know that a new product will connect with consumers. After all, before the ToiletWand, with its disposable sponges preloaded with Clorox Toilet Bowl Cleaner, hit the market, consumers had spent decades using wire-and-bristle-capped toilet brushes. Who could say, then, that the wand would be something millions would embrace?

That uncertainty and the risks associated with it did not stop Clorox, because the company trusts what Buckminster Fuller called the “profound knowledge” of its leaders, and it has a proprietary process to bring new technologies and ideas to the market while managing Clorox’s exposure to risk.

The most common mistake in regard to profound knowledge is that it presents itself as gut instinct about the industry in which you work. And all business leaders have been traditionally trained to ensure that facts triumph over gut. Leaders who are in the marketplace stand in the stream of their industry every day, with information and data flowing by them constantly. Sometimes all the data, facts, and projections one would like to be working with prove too fluid to capture. But these leaders of growth know what is out there when they have been standing in that stream long enough. The judgments made based on knowledge and wisdom gained from sustained engagement in the marketplace (even if the leaders cannot fully articulate the basis of the judgments) often turn out to be better grounds for a business decision on a new product or marketing approach than a BASES score.

Create a Process for CreativityCultivating creativity is bigger than a suggestion box.

Companies have to invest in an infrastructure that fosters innovation and gives creative ideas an outlet. Employees have to know how to take an idea and turn it into a prototype and how to move that prototype to a new product or marketing campaign.

One example that worked for one of Insigniam’s clients:

Create an office of project management and pair it with an office of project acceleration. Combined, the two are able to push a larger number of ideas through the corporate pipeline. The new innovation office created and published a proprietary innovation process that anyone and everyone in the enterprise can use.

However the infrastructure is set up, execution is key. And execution requires a culture that is focused on accountability. That does not mean “blame, shame, and credit.” Instead, accountability is a system of measuring outcomes. Just like in accounting where your balance sheet must add up correctly, there also has to be a balance in performance accountability. Think of it like this: Producing the intended result is a product of action; accountability is acknowledging the actual result and the actions taken or not taken.

Create a New ScoreboardBalance sheets and income statements are important. But

those agreed-on financial tools do not measure or show valuable developments in innovation and marketing. And, as anyone reading this article will know, the first rule of management is that you tend to get what you measure. Therefore, leaders of growth will have a metric and a scoreboard that measures, captures and displays the value generated by innovation and marketing. What is tracked and displayed on this new scoreboard is critical.

Do you value lead times? Quality control? Brand recognition? Then put those on the scoreboard. Wayne Delker invented a metric to measure ROI for R&D and reported the number at executive team meetings, just as the CFO reported earnings.

Peter Drucker first told us 61 years ago, the two and only two functions of a business that generate value are innovation and marketing. Growth leaders provide an environment that supports creativity through culture, processes, and structure, and have ways to account for the value generated by that creativity.

FACTORS PREVENTING CORPORATE LEADERS FROM CREATING A SYSTEM THAT LEADS TO BETTER INNOVATION, MARKETING — AND GROWTH.3

CORPORATE GRAVITY

CORPORATE MYOPIA

MILLION BILLION

1

2

1975

1996

2004

2012

The digital camera is invented by Kodak, which it quickly placed back in the closet. In fact, Kodak invented much of the technology used in digital imaging.

Kodak remakes itself as a digital imaging company, a decade after the first digital camera hit the consumer market.

Kodak files for Chapter 11 bankruptcy, having failed to capitalize on digital imaging due to corporate gravity.

Kodak’s revenues peak at $16 billion, but the company was not adequately prepared for the digital camera’s imminent market penetration.

$500Annual sales of Swiffer Sweeper, a product that a consumer goods company passed on because they were focused too narrowly on the way houses had been cleaned in the previous decade.

U.S. household-care market size.

$4575%

Swiffer Sweeper owner Proctor & Gamble’s hold on the quick-clean market in 2005, just 6 years after launching the cleaning aid.

CORPORATE IMMUNE SYSTEM3Percentages of jobs held on average by different groups in Silicon Valley companies Apple, Yahoo, Facebook, Google, and Twitter, which may prevent a diversity of ideas from bubbling up through the ranks.

2% AFRICAN-AMERICAN16% WOMEN

4% HISPANIC

24 INSIGNIAM QUARTERLY SPRING 2015

Societies, like computers, have operating systems. These systems consist of a set of rules for human behavior and how people act. “The laws, social customs, and economic arrangements that we encounter each day sit atop a layer of instructions, protocols, and suppositions about how the world works,” says business guru Daniel H. Pink in Drive: The Surprising Truth About What Motivates Us.

Organizations have operating systems, too. Beneath the surface of the hardware (tools and structures) and software (employees and processes) is a complex set of values, arrangements, rules, and suppositions governing how the

organization works. We generally refer to this as corporate culture.

Organizational operating systems or cultures are the invisible forces driving performance. They can either propel or inhibit growth. If the culture aligns and reinforces vision and strategy, you get booming growth like at Apple or Netflix. If it’s myopic and sclerotic, you get an enterprise like RadioShack with a decline that can be traced through a long thread of

self-defeating tactics born from a cultural background that didn’t create the evolution needed to survive.

These cultural systems can be broken down into

nine distinct elements:

• Language and the network of conversations• Customer orientation• What is actually valued• Accountability and responsibility• Traditions, rituals, heroes, legends, and artifacts• Leadership dynamics• Unwritten rules for success

UNLEASH CULTURE TO FUEL GROWTHHow to align the nine facets of corporate culture to drive performance.BY SHIDEH SEDGH BINA AND NATHAN O. ROSENBERG

INSIGNIAM QUARTERLY 25SPRING 2015

• Decision rights and processes• LegacyTogether these elements form the set of instructions,

protocols, and suppositions — the DNA — of the corporate organism. This DNA either primes the organization for growth, or sets it on a course of stagnation, dysfunction, and decline.

LANGUAGE AND THE NETWORK OF CONVERSATIONS

What people say aligns with how they perceive what they’re experiencing. For human beings, perception is not only physical, it’s linguistic — shaped by language. What you listen for when assessing the network of organizational conversations are the elements shaping these interactions.

Listening to what’s being said is often not enough to generate a sense of corporate cultures. You also have to be aware of what’s not being said.

For example, we once interviewed employees at all levels of a high-flying U.S. supercomputer maker in the Midwest. Throughout these interviews, we never once heard an admission that someone made a mistake or wasted the company’s money.

This told us that what was lacking in the corporate culture was a sense of personal responsibility and individual accountability.

When we relayed this to the CEO, he said, “Wow. I never would have gotten that. But the second you say it, you’re absolutely right. This is Midwest nice, and we don’t hold people to account.”

To drive growth, the patterns of conversation must shift from passive expressions such as: “It would be good if...,” “Somebody should…,” and “We need to…,” to active declarations such as “I will…,” “I promise…,” and “Would you…?”

CUSTOMER ORIENTATION How important is the customer? Years ago we had the

opportunity to participate in one of the first known corporate-culture transformations at the Ford Motor Company. We found that some assembly line workers would often strike back at management by sabotaging cars. For example, they’d put a tin can inside a fender so it rattled when the car was driven. They were using customers to animate their hostility toward management. This episode illustrates the consequences of a culture so dysfunctional that both employees and customers became completely alienated from the company and its success.

26 INSIGNIAM QUARTERLY SPRING 2015

When you put employees first, it translates to the customer. After all, in the end, the customer determines your success. Ultimately, only satisfied customers can fuel enterprise growth. And customers are not abstractions.

That’s why some companies actually give the customer a name. For example, during high-level meetings at Amazon.com, CEO Jeff Bezos has an empty chair representing the customer placed at the table. And those at the table had better include the customer in the conversation when decisions are made.

WHAT IS ACTUALLY VALUEDCorporate values are not plaques on walls. They are not

posters. They’re not handbooks passed out to employees. Corporate values are what leadership consistently displays and reinforces through action. What behavior can get you fired? What actions are people rewarded for?

Rewards don’t necessarily mean bonus money. One of the misconceptions we often find among executives is the belief that without bonuses, people won’t pursue high performance. This is incorrect. In Drive, Pink relates what a team of researchers reported to the Bank of Boston in 2005 after completing a study gauging the effects of incentives on performance: “In eight of the nine tasks we examined across the three experiments, higher incentives led to worse performance.”

Clearly, something other than money drives people to achieve. Oftentimes performance of the task — the sense of striving and accomplishment — is its own reward. But this drive is fragile. It needs a hospitable environment to thrive.

A CEO we once worked with regularly composed handwritten notes to employees on his personal stationary to recognize a job well done. People framed these notes and put them up on their walls like they were plaques, because they were so proud to receive a simple handwritten note from their CEO.

But remember: Stated values and beliefs are counterproductive if leadership doesn’t walk the walk. In one organization we worked with, several of the most senior executives regularly violated values and rules explicitly outlined in the employee handbook. That destroys corporate culture. It creates cynicism. It kills growth. You’d be better off having no beliefs than stating a set of beliefs and values that executives habitually violate.

ACCOUNTABILITY AND RESPONSIBILITYTo successfully establish a growth trajectory, enterprise

leaders must strive to create a culture where people aren’t afraid

to bring bad news to leadership. If an employee has a problem delivering something that was promised, that employee should feel comfortable picking up the phone or walking down the hall to alert their superiors in a timely manner.

Agile leaders often respond by offering assistance: “Okay, how can I help you?” or “What resources do you need?” or “Let’s think about how we can solve this problem.” If an employee believes leaders are prepared to support them in a pinch, they’re much more likely to bring up problems before they escalate into crises. Such an environment fosters collaborative problem solving and allows leaders to effectively tap the human resources at their disposal.

TRADITIONS, RITUALS, HEROES, LEGENDS, AND ARTIFACTS

Traditions, rituals, and heroes animate corporate culture. These powerful elements are instilled intentionally. Who do we want to make a hero? What are the stories we want to tell? By introducing potent narratives, we reinforce and give life to corporate values.

At Home Depot, there’s a common-told story involving a customer who needed help installing an attic fan in his home. The associate provided him with the parts, instructions, and tools to do the job. But at the end of the day, the associate realized he forgot to give the customer a critical part for the installation. So he pursued the cashier who transacted the purchase, obtained the customer’s record, and contacted the customer. He then made arrangements to deliver the part to the customer’s house on his way home from work.

What does this story tell new employees? It tells them three things:

• We’re in the do-it-yourself business. Our job is to make do-it-yourselfers successful.

• Customer service is really important.• You take care of the customer.That’s all encapsulated in one story. And you make a

hero of that employee. Skip all of the buzzwords. Stories are more important. At AutoZone, the DIY vehicle-parts retailer renowned for its customer service, meetings start with reading a customer letter about an employee that went the extra mile for the customer. If you’re an organization with a high-performance culture, you instill and sustain these stories.

LEADERSHIP DYNAMICSSuccessful cultures — those primed for growth — make

clear that anyone in the organization can lead. If only senior executives can lead, you’re in big trouble. If the only person who can lead is the CEO, you’re in really big trouble. Highly

INSIGNIAM QUARTERLY 27SPRING 2015

effective organizations have leaders at each and every level. When people step forward to lead, executives from the CEO on down must encourage and incentivize that behavior.

Great leaders encourage other people to lead, even if those people are not effective the first time out. They reinforce and support that behavior. True leaders are not threatened when others take the lead. Organizations saturated with leadership culture propel growth. The high-performing cultures we’ve seen have well-defined leadership governance structures with different leadership bodies across management levels, each with its own charter, accountability, and meeting cadence to instill leadership throughout the enterprise.

UNWRITTEN RULES FOR SUCCESS This element is a tough one. The only way to tease out

unwritten rules for success is by violating them. Therefore, you’re going to get a bruised forehead and a bloody nose walking into walls you simply can’t see. If you examine outcomes, these shadowy rules begin to take shape. What kinds of people succeed in the organization? How do they behave? What are they rewarded for?

But keep in mind: Unwritten rules are rules for succeeding in the company, not for succeeding in the marketplace. And these rules are oftentimes at odds. We witnessed this at a manufacturing company that was fighting market-share erosion due to new, innovative activity from one of their key competitors. They needed to come up with potent, creative marketplace moves quickly. Yet when they called meetings with their top leaders, the unwritten rules said that only those executives that ranked senior vice president and above could sit at the conference table and participate in the conversation. VPs were expected to sit in the chairs around the wall and not participate unless called upon. So much for creativity and agility in the marketplace — the thinking is constrained by one’s title or the location of one’s chair in the meeting room.

DECISION RIGHTS AND PROCESSWho gets to make decisions? Who has the authority to

make changes in a process or shift direction? In many large organizations, nobody knows the answer to these questions. And to the degree that nobody can intelligently answer these questions, you’ve got a problem. If employees want to change something in the company to make a process better, how do they know if they have the right to do so? And if not, who does? Too frequently the answer is, “I don’t know.”

Sometimes leaders refuse to grant people on different levels of the organization with decision-making rights, because they

are afraid people are going to screw up. Sometimes the drive for immediate results leads to decision rights rising to the top—thus reducing risk for the senior levels while shrinking the range of motion of those closest to the market. In an extreme case, we witnessed a $14 billion global company where every contract over $25,000 had to be personally signed by the CEO and any travel expense over $500 had to be approved by an executive committee member. This culture of thrift drove attention and action toward chasing literally every dollar and away from serving customers and executing on critical tactics. Too much management and control indicates bad management. Without the ability to execute on new ideas and innovative changes, employees will give themselves over to a culture of complacency, rather than working hard to continuously improve the way they do business.

LEGACY Having a mission statement or credo is important. So is the

informal and formal storytelling that populate an enterprise. This means more than a poster on the wall; it helps everyone throughout the organization align and make decisions. Johnson & Johnson maintains an impressive decades-long commitment to its credo. This four-paragraph statement written in 1943 by then-Chairman Robert Wood Johnson clearly states what is important and the responsibilities of the enterprise, and it outlines the focus of this $65 billion mega-corporation. “We believe our first responsibility is to the doctors, nurses, and patients, to mothers and fathers and all others who use our products and services” and then moving on to employees and communities, and ending with stockholders. By stating and codifying a clear ethos, J&J provides all of its employees with a consistent set of criteria to use as a benchmark for decision-making — the same criteria executives use to guide their decisions — which only serves to empower employees to deliver on stated objectives. The company invests significant money and time into monitoring its adherence to its credo and boasts premier performance among its competitors.

THE CULTURAL MOLECULEWe call each of these facets “elements” because they

come together to create a molecule—the DNA that drives corporate culture. When combined, these elements contain the instructions and protocols that can drive dramatic growth. When these elements lose their power, the organization begins to whither and degenerate. The culture becomes counter to what you want to accomplish and organic growth become harder and harder to achieve.

28 INSIGNIAM QUARTERLY SPRING 2015

SOURCE: INSTITUTIONAL INVESTOR

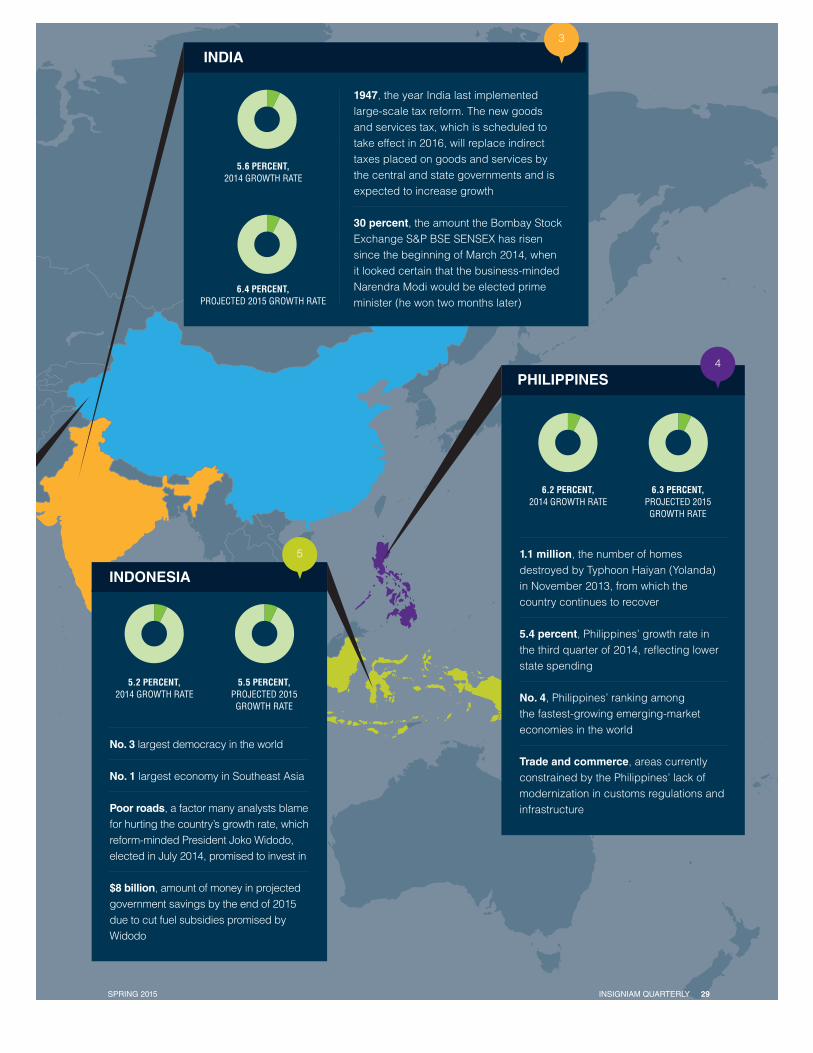

GROWTH FACTORS: The Drivers Behind 2015’s Top 10 Emerging Markets

The growth rates of emerging markets were forecasted to slow to an average of 4.4 percent in 2014, down from 7.5 percent in 2010 according to the International Monetary Fund. But not every country is suffering. Some markets have been

insulated against outside forces, such as dropping commodity prices, through strong internal policies, among other factors. Here, we take an in-depth look at the environments fostering the strong growth of the top 10 emerging markets.

QATAR

$16 billion, cost of Hamad International Airport, opened in 2014, which promises not only global travel, but also 70 retail shops

2022, the year Qatar will host the FIFA World Cup, driving infrastructure improvement projects including road systems, a metro system in Doha, stadiums, and arenas

85 percent of export earnings come from oil and natural gas, making the country vulnerable to unstable prices

1

6.5 PERCENT, 2014 GROWTH RATE

7.7 PERCENT, PROJECTED 2015 GROWTH RATE

7.4 PERCENT,2014 GROWTH RATE

7.1 PERCENT, PROJECTED 2015 GROWTH RATE

10.4 percent, the growth rate of China in 2010, which has since slowed to 7.4 percent in 2014

4 million yuan, the amount paid on the 89.8 million yuan due when Chinese company Chaori Solar defaulted on its bond note in March 2014, raising concerns about how China would balance market liberalization with financial stability

November 2014, the month Shanghai-Hong Kong Stock Connect launched, which opened up the Shanghai Stock Exchange to international trade for the first time and allows mainland investors to buy Hong Kong stocks

CHINA 2

GROSS DOMESTIC PRODUCT GROWTH (IN %) PER THE IMF

Country 2014 2015Qatar 6.5 7.7China 7.4 7.1India 5.6 6.4Philippines 6.2 6.3Indonesia 5.2 5.5Malaysia 5.9 5.2Peru 3.6 5.1Thailand 1.0 4.6Colombia 4.8 4.5United Arab Emirates 4.3 4.5

INSIGNIAM QUARTERLY 29SPRING 2015

1947, the year India last implemented large-scale tax reform. The new goods and services tax, which is scheduled to take effect in 2016, will replace indirect taxes placed on goods and services by the central and state governments and is expected to increase growth

30 percent, the amount the Bombay Stock Exchange S&P BSE SENSEX has risen since the beginning of March 2014, when it looked certain that the business-minded Narendra Modi would be elected prime minister (he won two months later)

5.2 PERCENT, 2014 GROWTH RATE

5.5 PERCENT, PROJECTED 2015 GROWTH RATE

6.2 PERCENT, 2014 GROWTH RATE

6.3 PERCENT, PROJECTED 2015 GROWTH RATE

5.6 PERCENT,2014 GROWTH RATE

6.4 PERCENT, PROJECTED 2015 GROWTH RATE

No. 3 largest democracy in the world

No. 1 largest economy in Southeast Asia

Poor roads, a factor many analysts blame for hurting the country’s growth rate, which reform-minded President Joko Widodo, elected in July 2014, promised to invest in

$8 billion, amount of money in projected government savings by the end of 2015 due to cut fuel subsidies promised by Widodo

3

INDIA

PHILIPPINES

1.1 million, the number of homes destroyed by Typhoon Haiyan (Yolanda) in November 2013, from which the country continues to recover

5.4 percent, Philippines’ growth rate in the third quarter of 2014, reflecting lower state spending

No. 4, Philippines’ ranking among the fastest-growing emerging-market economies in the world

Trade and commerce, areas currently constrained by the Philippines’ lack of modernization in customs regulations and infrastructure

4

5

INDONESIA

MALAYSIA 6

7

PERU

3.6 PERCENT, 2014 GROWTH RATE

5.1 PERCENT, PROJECTED 2015 GROWTH RATE

5.9 PERCENT, 2014 GROWTH RATE

5.2 PERCENT, PROJECTED 2015 GROWTH RATE

4.8 PERCENT,2014 GROWTH RATE

4.5 PERCENT, PROJECTED 2015 GROWTH RATE

COLOMBIA

30 INSIGNIAM QUARTERLY SPRING 2015

40 percent of the world’s supply of palm oil is produced in Malaysia

10 percent of Malaysia’s GDP is account-ed for by palm oil

4.5 percent export tax on crude palm oil was temporarily removed from September 2014 through February 2015 in the hopes of increasing growth

Oil prices are less likely to affect Malaysia due to diversified economy

60 percent of country’s export earnings come from mining

No. 1, the ranking it will achieve as fastest-growing emerging-market economy in Latin America if IMF growth projections come true

3.5 percent was Peru’s lowest interest rate in three years when the central bank cut rates in September 2014

A3, the rating Moody’s Investors Service raised Peru’s credit to in July 2014, matching that of Mexico and trailing only Chile in Latin America

Alonso Segura, the well-regarded economist appointed finance minister in September, who is pushing for major economic reforms

$1 billion, size of bond being pushed by Segura along with tax cuts to finance public sector investments and short-term spending

2X, oil production rate increase in the last 8 years

10 percent of the country’s roads are paved, and the country’s infrastructure badly needs investment

50 years, how long it’s been since the conflict between the Colombian government and the Revolutionary Armed Forces of Colombia began

December 2014, when negotiations began promis-ing a potential end to the conflict, which could lead to increased growth

Emerging market status, the country was upgraded from frontier market by U.S.-based index provider MSCI

Less than 1/3, the fraction of the GDP now accounted for by oil thanks to efforts by the government to diversify the economy

Tourism, the area government has worked to develop through luxury hotels and international airlines Etihad Airways and Emirates

9

10

UNITED ARAB EMIRATES

4.3 PERCENT, 2014 GROWTH RATE

4.5 PERCENT, PROJECTED 2015 GROWTH RATE