institute of actuaries of india actuarial advice and resultant liabilities of an appointed actuary...

TRANSCRIPT

Institute of Actuaries of India

Actuarial advice and resultant liabilities of an Appointed Actuary

India Fellowship Seminar-December 2014

Serving the Cause of Public InterestIndian Actuarial Profession

Sipika TandonSupriyo ChakiAdarsh Kishor AgarwalA V Karthikeyan

Under the guidance ofMr. Saket Singhal

www.actuariesindia.org2

Agenda

Introduction

Appointed Actuaries in India

Actuarial advice and risks associated with it

Stakeholders – expectations & governing regulations

Challenges and liabilities of Appointed Actuaries

Impact of Legislation and Regulation

Mitigation Plan and insurance protection

Prof

essi

onal

ism

, Eth

ics

and

Cond

uct

www.actuariesindia.org3

Actuarial advice – expert or a mere adviser? Actuaries can act as expert in a specific area or a mere professional adviser Expert may fail to follow instructions and unable to explain the deviation May be liable in negligence for making a mistake in arriving at conclusion

Appointed Actuary – working as IRDA’s eye

To inform Authority of own opinion whether insurer has contravened any act At the same time needs to contribute to business growth – potential conflict of interest

Independence of Opinion

Responsibilities towards various stakeholders – their expectations and liabilities associated with Appointed Actuary’s advice

Actuaries as professionals

Appointed Actuary – a mandatory requirement in Indian insurance industry

Introduction

www.actuariesindia.org4

Appointed Actuaries in IndiaPerforming a multifaceted role in life and general insurance

Central to financial soundness of the company – to ensure that business is conducted in sound financial lines and monitor unfair actions

Central to the financial soundness of the general insurance company – to ensure that business is conducted in sound financial lines having regard to Policyholders’ Reasonable Expectations

To perform an annual actuarial investigations into the financial condition of GI business Certify the adequacy of the claim reserves Ensure appropriateness of premium rates and policy conditions Advise the Board on capital requirements To carry out economic capital calculation To report in writing to the Board on the results and implications of any valuation carried out for

statutory purposes

To carry out actuarial investigations to assess financial soundness of the insurer – FCR requirement Carrying out valuation of liabilities Ensure appropriateness of premium rates and policy conditions Advise the Board on capital requirements Advise and report on allocation of surplus To report in writing to the Board on the results and implications of any valuation carried out for

statutory purposes

www.actuariesindia.org5

Actuarial AdviceResponsibilities of Appointed Actuary in General Insurance

Managing actuarial function – Business As Usual (BAU) Reserve calculation and estimation of reserving uncertainty Pricing and product design Asset – liability management and solvency calculation Insurance contract wording, investment and reinsurance

Internal Management Reporting Rendering actuarial advice to management of insurer Participation in Board Meetings Drawing management attention to any potential violation of rule/regulation

Regulatory Submission Certification of IBNR and other reserves Prepare and submit Financial Condition Report Economic Capital related submission Handling associated queries from IRDA

Other Professional Responsibilities Participation in industry bodies and various actuarial committees Contribution to the development of actuarial profession in India

www.actuariesindia.org

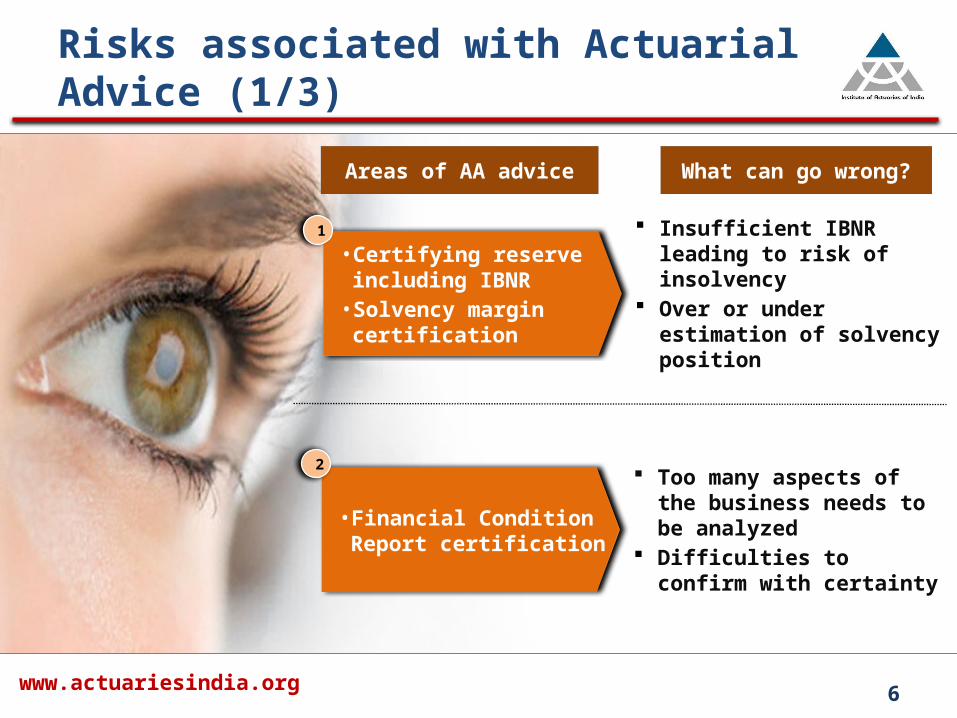

Risks associated with Actuarial Advice (1/3)

• Certifying reserve including IBNR• Solvency margin certification

1

Insufficient IBNR leading to risk of insolvency

Over or under estimation of solvency position

Areas of AA advice What can go wrong?

• Financial Condition Report certification

2

Too many aspects of the business needs to be analyzed

Difficulties to confirm with certainty

6

www.actuariesindia.org

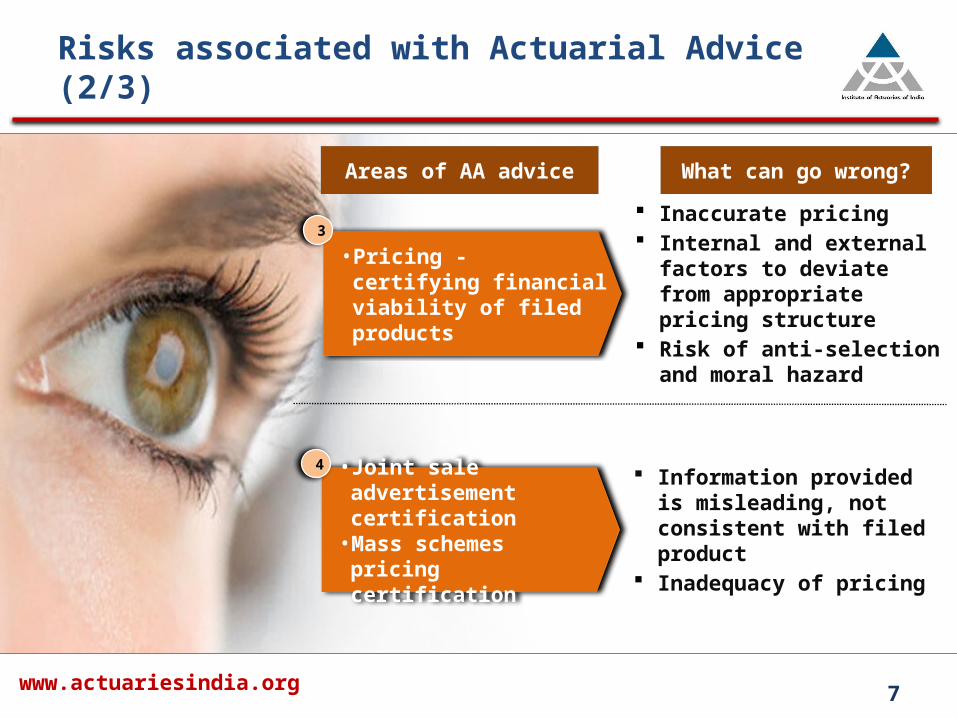

Risks associated with Actuarial Advice (2/3)

• Pricing - certifying financial viability of filed products

3 Inaccurate pricing Internal and external factors to

deviate from appropriate pricing structure

Risk of anti-selection and moral hazard

Areas of AA advice What can go wrong?

• Joint sale advertisement certification•Mass schemes pricing

certification

4

Information provided is misleading, not consistent with filed product

Inadequacy of pricing

7

www.actuariesindia.org

Risks associated with Actuarial Advice (3/3)

• Economic Capital certification

5 Use of wrong methodology or model

Inappropriate assumptions Data issues – unavailability and

less granular

Areas of AA advice What can go wrong?

• Asset Liability certification

6 Failing to consider factors having significant relevance to business

Not including relevant shock scenarios

8

www.actuariesindia.org9

Spectrum of Stakeholders

Appointed Actuary’s Advice

Board of Directors

Shareholders

Employees

Credit rating agencies

Brokers

IRDA

Government of India

Existing policyholders

Prospective policyholders

Institute of Actuaries

of India

General Insurance Council

Fellow Actuaries

Reinsurers

Corporate Agents

www.actuariesindia.org10

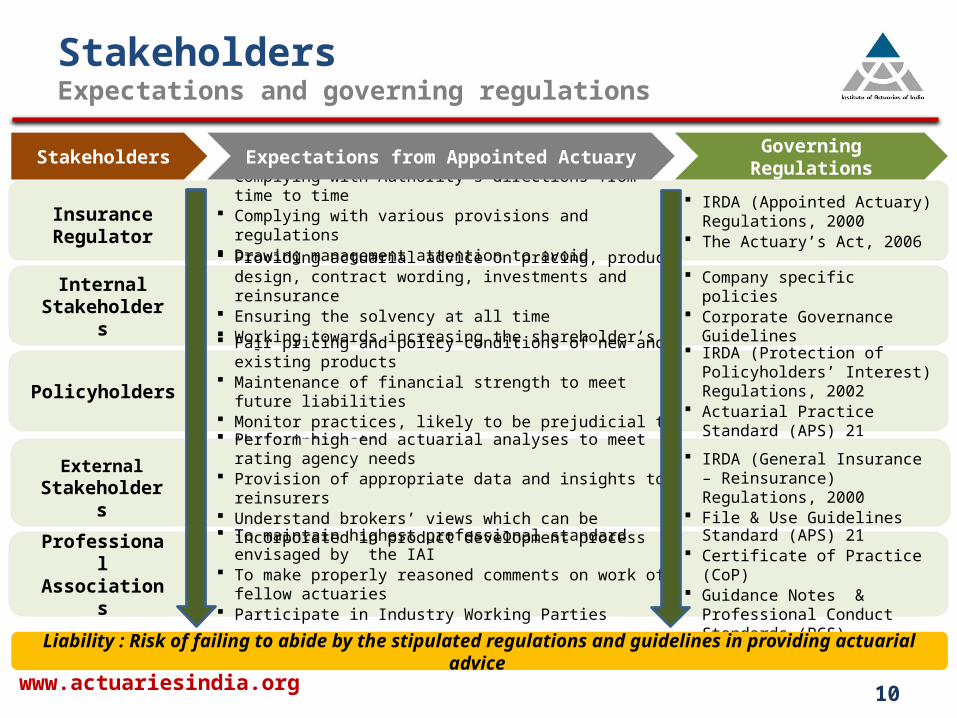

StakeholdersExpectations and governing regulations

Stakeholders Governing Regulations

Insurance Regulator

Complying with Authority’s directions from time to time Complying with various provisions and regulations Drawing management attention to avoid contravention of Act

Internal Stakeholders

Providing actuarial advice on pricing, product design, contract wording, investments and reinsurance

Ensuring the solvency at all time Working towards increasing the shareholder’s value

Company specific policies Corporate Governance Guidelines

Policyholders Fair pricing and policy conditions of new and existing products Maintenance of financial strength to meet future liabilities Monitor practices, likely to be prejudicial to their interests

IRDA (Protection of Policyholders’ Interest) Regulations, 2002

Actuarial Practice Standard (APS) 21

Professional Associations

To maintain highest professional standard envisaged by the IAI To make properly reasoned comments on work of fellow actuaries Participate in Industry Working Parties

Actuarial Practice Standard (APS) 21 Certificate of Practice (CoP) Guidance Notes & Professional

Conduct Standards (PCS)

IRDA (Appointed Actuary) Regulations, 2000

The Actuary’s Act, 2006

External Stakeholders

Perform high end actuarial analyses to meet rating agency needs Provision of appropriate data and insights to reinsurers Understand brokers’ views which can be incorporated in product

development process

IRDA (General Insurance – Reinsurance) Regulations, 2000

File & Use Guidelines

Expectations from Appointed Actuary

Liability : Risk of failing to abide by the stipulated regulations and guidelines in providing actuarial advice

www.actuariesindia.org11

Challenges of Appointed ActuariesToo much to carry, too many forces to balance

Data integrity and unavailability

Unavailability of skilled actuaries to support

Ever changing insurance landscape

Product innovation

New regulatory requirements

Demands of different stakeholders

Understanding the risks being placed upon the Appointed Actuary

www.actuariesindia.org12

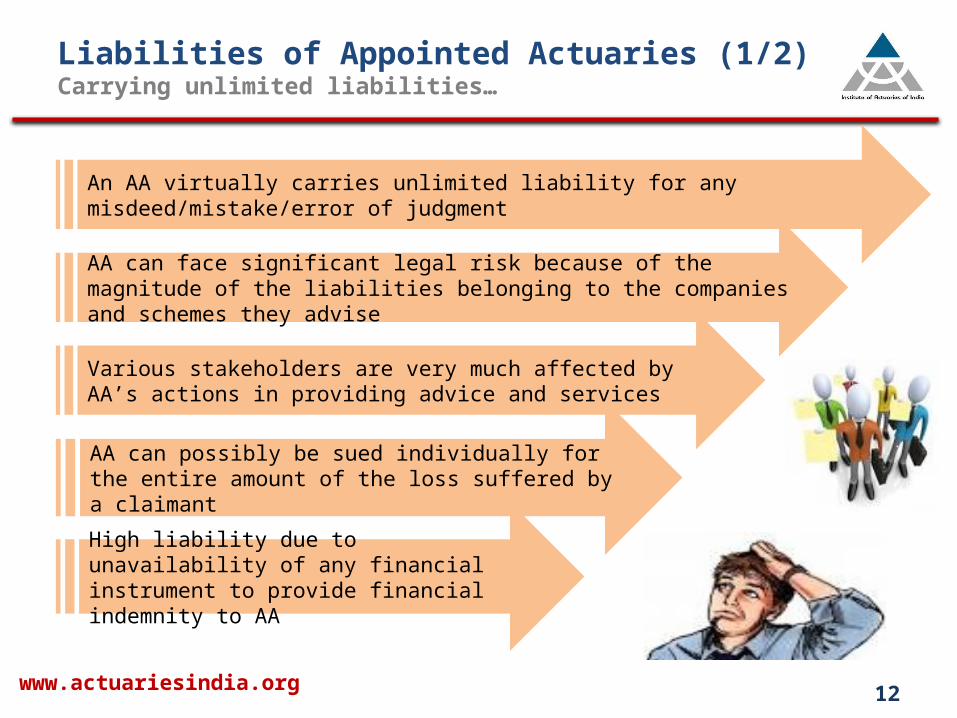

Liabilities of Appointed Actuaries (1/2)Carrying unlimited liabilities…

An AA virtually carries unlimited liability for any misdeed/mistake/error of judgment

AA can face significant legal risk because of the magnitude of the liabilities belonging to the companies and schemes they advise

Various stakeholders are very much affected by AA’s actions in providing advice and services

AA can possibly be sued individually for the entire amount of the loss suffered by a claimant

High liability due to unavailability of any financial instrument to provide financial indemnity to AA

www.actuariesindia.org13

Disciplinary action by IRDA

Disciplinary Action by IAI

Lawsuits filed by stakeholders against inappropriate advice

Termination from duties by the Employer

Financial penalties

Reputational damage

Liabilities of Appointed Actuaries (2/2)Possible consequences of carrying unlimited liabilities

www.actuariesindia.org14

Impact of Legislation and Regulations

Key Objectives

The various roles performed by Appointed Actuaries in India are regulated and governed by The Actuaries Act, 2006 and the IRDA (Appointed Actuary) Regulations, 2000. The overarching objectives of these are to provide a framework within which the Actuaries need to work and perform contractual obligations.

Surrounding regulations

– Defines professional misconduct– Actions of Authority, Disciplinary

Committee and Council– Appeal procedure and penalties– Quality Review Board

The Actuaries Act, 2006

– Specifies duties and obligations– Elucidate the powers of AA– Cessation of appointment of AA– Mentions about absolute privilege of AA

IRDA Appointed Actuary Regulations, 2000

Actuarial Practice Standards Guidance Notes

Professional Guidance2

1

Professional Conduct Standards Certificate of Practice

www.actuariesindia.org15

Mitigation PlanOperational ways to minimise exposure

4 eye principle to eliminate errors and omissions

Maker-Checker-Reviewer Approach

Sense check on actuarial analyses

Clearly defined Standard Operating Procedure for different activities

Ensure data quality – Garbage in-Garbage Out

Possible Options

Wrong methodology or model is usedInaccurate actuarial calculationMiss out on relevant aspects in actuarial investigations

Follow the basic principles

Data extensive work – validation checks are useful ways to minimise over-reliance on data as it is

Many of the tasks are process oriented and periodic in nature – following updated process documents can reduce the risk of process error

Which risks are mitigated?

www.actuariesindia.org16

Mitigation PlanUse of professional guidance and other inputs

Follow various Guidance Notes issued by the IAI

Interaction with Peer Actuaries - Compare high level KPI with Peer companies

Continuous professional developments and regular trainings

Keep abreast of the various regulatory developments

Keep up-to-date with legal and socio economic changes

Possible Options

Seek professional guidance

Different guidance notes are meant to assist in the provision of actuarial advice and certification in various areas

Important to remain conscious about the legal aspects of professional services and its implications

Inappropriate assumptions are usedFailing to consider factors having significant relevance to businessData issues not effectively dealt with

Which risks are mitigated?

www.actuariesindia.org17

Mitigation PlanSome other areas to lean upon

Get Professional Indemnity insurance

Self awareness of various potential conflicts of interest

Support from appropriate qualified and experienced team members

Monitor developments concerning legal liabilities of actuaries in other countries

Imposing liability caps to limit the liabilities

Possible Options

Be aware of external environment

Understand own risk and use suitable insurance plan to protect unforeseen liabilities

Awareness of various forces around and their dimensions can help to act knowledgeably

Acquire and demonstrate high level of corporate skill

Influenced to deviate from appropriate pricing structureFailure to convince all parties that the actuarial advice has been fair to allUnderestimation of emerging risks and financial liabilities

Which risks are mitigated?

www.actuariesindia.org18

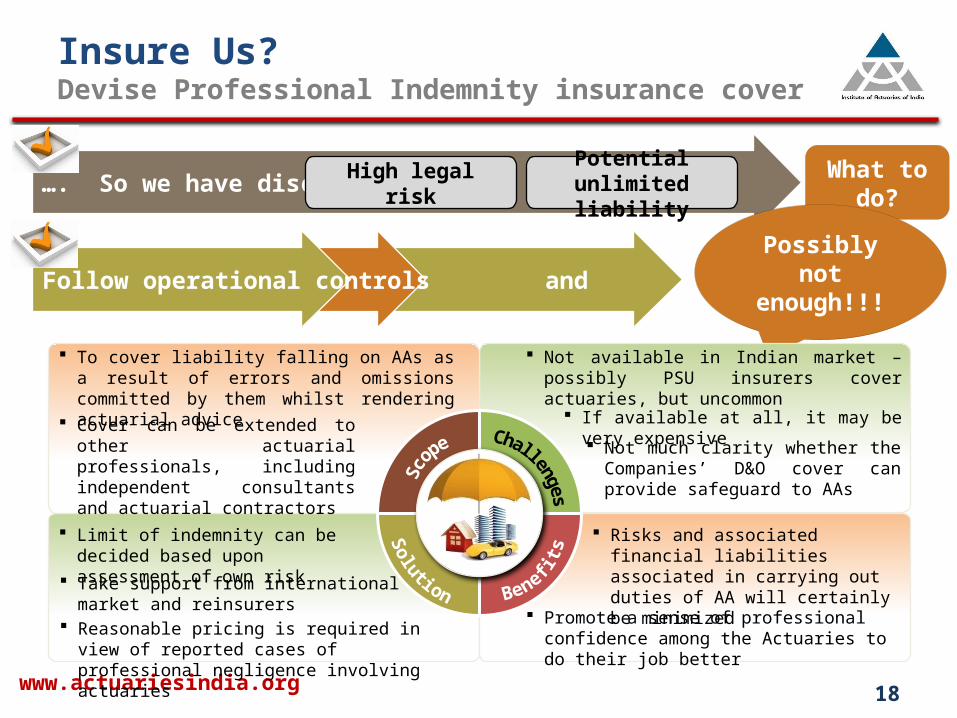

Insure Us?Devise Professional Indemnity insurance cover

…. So we have discussed High legal risk Potential unlimited liability

What to do?

Follow operational controls and professional guidance Possibly not enough!!!

Not available in Indian market – possibly PSU insurers cover actuaries, but uncommon

Risks and associated financial liabilities associated in carrying out duties of AA will certainly be minimized

Limit of indemnity can be decided based upon assessment of own risk

To cover liability falling on AAs as a result of errors and omissions committed by them whilst rendering actuarial advice

Cover can be extended to other actuarial professionals, including independent consultants and actuarial contractors

If available at all, it may be very expensive

Not much clarity whether the Companies’ D&O cover can provide safeguard to AAs

Promote a sense of professional confidence among the Actuaries to do their job better

Reasonable pricing is required in view of reported cases of professional negligence involving actuaries

Take support from international market and reinsurers

www.actuariesindia.org19

References

In preparing this, we have taken assistance from the following:

The Actuaries Act, 2006 (As passed by the House of Parliament) Insurance Regulatory and Development Authority (Appointed Actuary) Regulations,

2000 Guidance Note (GN) 21: Appointed Actuary and General Insurance Business Actuarial Practice Standard (APS) 1: Appointed Actuary and Life Insurance Business Actuarial Practice Standard (APS) 1: Appointed Actuary and Life Insurance Business Professional Conduct Standards (PCS Version 3.00) issued by the Institute of

Actuaries of India Other regulations and guidelines issued by IRDA and IAI “Appointed Actuary – Insure Thyself” by Sampad Narayan Bhattacharya http://actuariesindia.org/downloads/gcadata/8thGCA/Appointed%20Actuary-%

20Insure%20thyself_S%20N%20Bhattacharya.pdf “Actuaries’ Liabilities” by Jonathan Evans and Wilberforce Chambers for

Professional Indemnity Forum Conference, Cambridge, July 2009

www.actuariesindia.org20

Q & A