institute of actuaries of india mumbai vikamsey.pdf · 17 october 2011 ca nilesh s vikamsey 22. n...

TRANSCRIPT

InstituteofActuariesofIndiaMumbaiCA.NileshS.VikamseyOctober 17 2011October17,2011

Contents

Introduction

Benefits of Convergence

Conceptual Changes and ImpactCo ceptua C a ges a d pact

Applicability in India

K Ch llKey Challenges

17 October 2011 2CA Nilesh S Vikamsey

IntroductionIntroduction

17 October 2011 3CA Nilesh S Vikamsey

IFRSConvergenceIndia – Convergence & Not Adoption

Two sets of Accounting Standardsg

IFRS Converged Indian Accounting Standards – Ind AS

Existing Accounting Standards – AS

Present Status

35 Ind AS notified by MCA35 Ind AS notified by MCA.

Effective Dates not yet notified––implementation in a phasedmanner after various issues including tax related issues areresolved with the concerned Ministries/ Departments andappropriate amendments are made to the relevant laws.

17 October 2011 4CA Nilesh S Vikamsey

International Accounting Standard (IAS)

StructureofIFRSIssued by the International Accounting Standard Committee (IASC) from 1973to 2000.

International Financial Reporting Standard (IFRS)International Financial Reporting Standard (IFRS)The IASB replaced the IASC in 2001 and have amended some IASs, replacedsome IASs with new IFRSs, issued certain new IFRSs.

Standing Interpretation Committee and International Financial ReportingStanding Interpretation Committee and International Financial Reporting Interpretation Committee (SIC and IFRIC)Interpretation on standards issued by IFRIC. IFRIC replaced the formerStanding Interpretations Committee (SIC) in 2002Standing Interpretations Committee (SIC) in 2002.

IASIAS IFRSIFRS SICSIC IFRICIFRICIAS 41

(29 Eff ti )IFRS 13

(8 Eff ti )SIC 33

(11 Eff ti )IFRIC 19

(16 Eff ti )(29 – Effective)(12 – Withdrawn)

(8 – Effective)(5 – To be effective from future date)

(11 – Effective)(22 – Withdrawn)

(16 – Effective)(3 – Withdrawn)

Separate IFRS for Small and Medium–sized Entities (SMEs)

17 October 2011 5CA Nilesh S Vikamsey

Separate IFRS for Small and Medium sized Entities (SMEs)

IAS Ind AS Name of Standard

ListofIAS/Ind ASIAS Ind AS Name of Standard

1 1 Presentation of financial statements

2 2 Inventories

7 7 Cash flow statement

8 8 Accounting Policies, Changes in Accounting Estimates and Errors

10 10 Events after balance sheet date

11 11 Construction contracts

12 12 Income taxes

16 16 Property, plant, and equipment

17 17 Leases

18 18 Revenue Recognition

19 19 Employee Benefits19 19 Employee Benefits

20 20 Accounting for Government Grants & Disclosure of Govt. Assistance

21 21 The Effect of Changes in Foreign Exchange Rates

23 23 Borrowing Costs

6

23 23 Borrowing Costs

17 October 2011 CA Nilesh S Vikamsey

ListofIAS/IndASIAS Ind AS Name of StandardIAS Ind AS Name of Standard

24 24 Related Party disclosures

26 NA Accounting and Reporting by Retirement Benefit Plans

27 27 Consolidation and Separate Financial Statements27 27 Consolidation and Separate Financial Statements

28 28 Investments in associates

29 29 Financial Reporting in Hyperinflationary Economies

31 31 Joint Ventures31 31 Joint Ventures

32 32 Financial Instruments: Presentation

33 33 Earnings per share

34 34 I t i Fi i l R ti34 34 Interim Financial Reporting

36 36 Impairment of assets

37 37 Provisions, Contingent Liabilities and Contingent Assets

38 38 I ibl38 38 Intangible assets

39 39 Financial instruments: Recognition & Measurements

40 40 Investment Property

7

41 NA Agriculture

17 October 2011 CA Nilesh S Vikamsey

IFRS Ind AS Name of Standard

ListofIAS/Ind AS1 101 First time adoption of IFRS

2 102 Share based Payment

3 103 Business Combination3 103 Business Combination

4 104 Insurance Contracts

5 105 Non–current Assets held for Sale and Discontinued Operations

6 106 Exploration for and Evaluation of Mineral Resources6 106 NA

Exploration for and Evaluation of Mineral Resources

7 107 Financial Instruments: Disclosures

8 108 Operating Segments8 108 Operating Segments

9 NA Financial Instruments (current effective date 01–01–2013, proposed 01–01–2015, with early adoption permitted)

10 NA Consolidated Financial Statements (effective date 01–01–2013)10 NA Consolidated Financial Statements (effective date 01 01 2013)

11 NA Joint Arrangements (effective date 01–01–2013)

12 NA Disclosure of Interests in Other Entities (effective date 01–01–2013)

13 NA F i V l M t ( ff ti d t 01 01 2013)

17 October 2011 8

13 NA Fair Value Measurement (effective date 01–01–2013)

CA Nilesh S Vikamsey

StatusofIndASSN Standards StatusSN Standards Status1 Standards notified by MCA 352 Standards not being notified currently 2

Total 37

Standards not being notified currently

• Ind AS corresponding to IAS 26 Accounting and Reporting byRetirement Benefit Plans has not been notified as this standardis not applicable to companiesis not applicable to companies

• Ind AS corresponding to IAS 41, Agriculture, is being redrafted

• Exposure Drafts issued/ being issued for latest 5 IFRS however• Exposure Drafts issued/ being issued for latest 5 IFRS—howeverIFRS 9 would be considered & made effective only after it iscompleted by IASB & reviewed

917 October 2011 CA Nilesh S Vikamsey

StructureofIFRS/IndASHow to read?

Introduction

Main Text– Objective, scope, Definitions, Recognition & measurements, Disclosures, Effective dates and Transition provisionsprovisions

Illustrative Examples (Appendix to Ind AS)

Application guidance (Appendix to Ind AS)pp g ( pp )

Basis for Conclusions (Not there in Ind AS)

Dissenting Opinions (Not there in Ind AS)g p ( )

17 October 2011 10CA Nilesh S Vikamsey

IFRS– Global(G20)Status of listed Companies as of April 2010 Source: www.ifrs.orgCountryCountry Current StatusCurrent Status CountryCountry Current StatusCurrent StatusItaly India India is converging with IFRSs at a date to

be confirmed.European Union Korea Required from 2011

p p g

All member states of the EU are required to use IFRSs as adopted by the EU for listed companies since 2005

Argentina Required for fiscal years beginning on or after 1 January 2011

France

Japan Permitted from 2010 for a number of international companies; Mandatory adoption may be by 2016

Germany

i d i d adoption may be by 2016United Kingdom Canada Required from 1 Jan 2011 for all listed

entitiesChina Substantially converged national

standardsIndonesia Convergence process ongoing; a decision

about a target date for full compliance with IFRSs is expected to be made in 2012

Australia Required for all private sector reporting entities and as the basis for public sector reporting since 2005

United States Allowed for foreign issuers in the US since 2007; FASB and IASB combine project for convergence is in process

2005 South Africa Listed entities since 2005 Mexico Required from 2012Turkey Required for listed entities since

2005Russia Required for bank and some securities

issuers; permitted for other companiesBrazil Banks and Listed companies from Saudi Arabia Not permitted for listed companies

Dec 2010

17 October 2011 11CA Nilesh S Vikamsey

IFRS– Global(G20)IFRSs are increasingly being recognised as Global Financial ReportingStandards

More than 122 countries, such as countries of European Union, Australia,pNew Zealand and Russia currently require/permit use of or have policy ofconvergence with IFRSs→ Brazil & Canada announced convergence from 2010 & 2011g

respectively→ China and Canada have announced their intention to adopt IFRS→ Securities & Exchange Commission (SEC) USA has permitted filing of→ Securities & Exchange Commission (SEC), USA has permitted filing of

IFRS–compliant financial statements without requiring presentation ofreconciliation statement between US GAAPs and IFRSs.

→ SEC roadmap permitting US domestic companies to prepare financial→ SEC roadmap permitting US domestic companies to prepare financialstatements as per IFRSs:˃ Will examine this proposal and take a decision in 2011˃ If considered fit allow them to do so from 2014

17 October 2011 12CA Nilesh S Vikamsey

˃ If considered fit, allow them to do so from 2014

Benefits of ConvergenceBenefitsofConvergence

17 October 2011 13CA Nilesh S Vikamsey

To Industry –BenefitsofConvergence

Benchmarking with global peersNew global reporting standards, would improve comparability, transparencyand credibility of financial statements and in a globalized world, would lead to

i ffi i igreater economic efficiencies.Improved access to international capital markets and reduction in cost ofcapitalForeign Direct Investors (FDI) overseas Financial Institutional Investors (FII)Foreign Direct Investors (FDI), overseas Financial Institutional Investors (FII)are more comfortable with compatible accounting standards and companiesaccessing overseas funds feel the need for recast of accounts in keeping withglobally accepted standards.globally accepted standards.Avoidance of multiple reportingIFRS convergence will enable entities across the group residing in differentcountries to adopt single financial reporting platform, these will result in costp g p g pand time benefit.To Indian Professionals –Will enable to get jobs or provide services in different parts of the world sincemore than 100 countries are either adopting/ Converging with IFRS

17 October 2011 14CA Nilesh S Vikamsey

Conceptual Changes and ImpactConceptualChangesandImpact

17 October 2011 15CA Nilesh S Vikamsey

BasicConceptsofIFRS/IndASSubstance over form

F i V l f t tiFair Value of transaction

Time value of money/ Effective rate of Interest

Greater Transparency

17 October 2011 16CA Nilesh S Vikamsey

BasicConceptsofIFRS/IndASSubstance over Form

Ind AS lay down treatments based on the economicInd AS lay down treatments based on the economicsubstance of various events and transactions rather thantheir legal form

Events and transactions are presented in a mannerdifferent from their legal form.

To illustrate, as per Ind AS, preference shares that providefor mandatory redemption by the issuer are presented as aliability

17 October 2011 17CA Nilesh S Vikamsey

BasicConceptsofIFRS/IndASFair Value against Transaction Value

Fair Value to be identified is different from the Transaction Value

Revenue recognition to be split between different categories→ Interest element to be segregated for e.g. Auto sale with

service, Interest component in payment terms etc.

Fair value of financial instruments

17 October 2011 18CA Nilesh S Vikamsey

Time Value of MoneyBasicConceptsofIFRS/IndAS

Time Value of MoneyEffective Rate of Interest to be calculated and not theContractual Rate of InterestUse of Discounting

Effective Rate of InterestMethod of calculating the amortized cost of the financial asset orgliability & of allocating the interest income or expense over therelevant period.Rate that exactly discounts estimated future cash payments orRate that exactly discounts estimated future cash payments orreceipts through the expected life of the instrument.To consider all contractual terms (prepayments, call and similaroptions) but not future credit lossesTo include all fees and amounts paid or received between thepartiesp

17 October 2011 19CA Nilesh S Vikamsey

BasicConceptsofIFRS/IndASGreater Transparency

Retrospective restatement of Errors

Concept of Other Comprehensive Income – Distinguishes between Income for the Year from Operations and Other Income such as Revaluation Reserves etc.

More disclosures by way of Notes

17 October 2011 20CA Nilesh S Vikamsey

Applicability in IndiaApplicabilityinIndia

17 October 2011 21CA Nilesh S Vikamsey

IndAS– IndiaOverviewProposed Roadmap for CompaniesProposed Roadmap for Companies

01 April 2011 01 April 2013 01 April 2014*a Nifty 50 and BSE – Sensex All Companies having a net Listed Companiesa. Nifty 50 and BSE Sensex

30b. Companies whose shares

or other securities are

All Companies having a net worth exceeding Rs.500 Crore but not exceeding Rs.1,000 Crore

Listed Companies which have a net worth of Rs.500 Crore or less.

listed on stock exchanges outside India

c. All Companies having net

,(whether Listed or Not)

worth in excess of Rs.1,000 Crore

* Si Ph I i i l d f 01 A il 2011 ICAI h l* Since Phase–I is not implemented from 01 April 2011, ICAI has recentlyrecommended to MCA to cover all companies having net worth above Rs.500Crore from 01 April 2013

17 October 2011 22CA Nilesh S Vikamsey

N B ki Fi C i

Ind AS– IndiaOverviewNon Banking Finance Companies

01 April 2013 01 April 2014a. Nifty 50 and BSE – Sensex 30 a. All listed NBFCs yb. All Companies having net worth

in excess of Rs.1,000 Crore b. Unlisted NBFCs having net worth exceeding Rs.500 Crore but notexceeding Rs.500 Crore but not exceeding Rs.1,000 Crore

Banks

01 April 2013 01 April 2014a. All scheduled commercial banksb. UCBs having net worth in excess

UCBs having net worth in excess of Rs.200 Crore but not exceeding g

of Rs.300 Crore g

Rs.300 CroreAll Insurance companies will convert their opening Balance Sheet as at April 01 2012

17 October 2011 23CA Nilesh S Vikamsey

April 01, 2012

Ind–AS– IndiaOverviewEarlier Voluntary Adoption is Possible

But U Turn – Not Possible

Migration is 1 way traffic

2417 October 2011 CA Nilesh S Vikamsey

CompaniesinaGroupinDiff t PhDifferentPhases

Parent In Phase I but Subsidiaries, Associates, JVs in different phases

Stand–alone Financial StatementsParent As per Ind ASGroup Co As per Non Converged AS

Consolidated Financial StatementsAs per Ind AS with necessary amendments to the accounts of the group companies which follow Non Converged AS

17 October 2011 25CA Nilesh S Vikamsey

TransitionAdjustments

on

Retained Earnings

Another category ofEx

ceptio

Earnings

Goodwill

Equity

Tax Impact

17 October 2011 26CA Nilesh S Vikamsey

InterpretationMatter InterpretationMatter Interpretation

Previous Period Numbers To be given as per existing AS, Option available to give additional column as per Ind AS

Voluntary adoption by phase 2 Can be done from year commencing April 01Voluntary adoption by phase–2 and phase–3 companies

Can be done from year commencing April 01, 2011 and there after

Cut–off date for application of criteria for Phase–1

Balance Sheet as at 31stMarch 2009criteria for Phase 1 March 2009

Cut–off date for application of criteria for Phase–1 (Banking and NBFC)

Balance Sheet as at 31stMarch 2011

Consolidated/Standalone Criteria to be applied on standalone basis

Net–worth Share Capital + Reserves – (RevaluationReserve, Miscellaneous,Expenditure and Debit Balanceof the Profit and Loss Account)

Dates given in above table will be revised based on revised timelines for applicability of d S

17 October 2011 27CA Nilesh S Vikamsey

Ind AS

IndAS/IFRIC/SICDeferredbyMCA

Ind AS 106 – Exploration for and Evaluation of Mineral Resources → It is under consideration of the Government

Ind AS 11 – Construction Contracts→ Appendix A (corresponding to IFRIC 12) Service Concession

Arrangements → Appendix B (SIC 29) Service Concession Arrangements:

Disclosures respectivelyDisclosures respectively

Ind AS 17 – Leases→ A di C ( di t IFRIC 4) D t i i Wh th→ Appendix C (corresponding to IFRIC 4), Determining Whether

an Arrangement contains a Lease

17 October 2011 28CA Nilesh S Vikamsey

Carve–outsinIndASInd AS 21 –The Effects of Changes in Foreign Exchange RatesInd AS 21 The Effects of Changes in Foreign Exchange RatesOption to recognise exchange differences arising on translation of certainlong–term monetary items in equity and the accumulated exchangedifferences to be amortised to profit or loss in an appropriate manner—UnderIAS 21 hi h b k P & LIAS 21 this has to be taken to P & L.Ind AS 24 – Related Party DisclosuresDisclosures which conflict with confidentiality requirements of statute/regulations are not required to be made since Accounting Standards cannotegu a o s a e o equ ed o be ade s ce ccou g S a da ds ca ooverride legal/ regulatory requirements.Ind AS 32 – Financial Instruments: Presentationexception to the definition of ‘financial liability’ Ind AS 32 considers equityconversion option embedded in a convertible bond denominated in foreigncurrency to acquire a fixed number of entity’s own equity instruments as anequity instrument if the exercise price is fixed in any currency (FCCB).Ind AS 28 Investment in AssociatesInd AS 28 – Investment in AssociatesIASIAS 2828 ––DifferenceDifference inin reportingreporting periodperiod ofof AssociateAssociate && InvestorInvestor notnot moremore thanthan 33monthsmonths && UseUse ofof samesame accountingaccounting policiespolicies byby AssociateAssociate && investorinvestor——inin IndInd ASAS2828 thethe wordswords ‘unless‘unless itit isis impracticable’impracticable’ hashas beenbeen addedadded atat relevantrelevant placesplaces..

17 October 2011 29CA Nilesh S Vikamsey

pp pp

Carve–outsinIndASI d AS 39 Fi i l I t t R iti d M tInd AS 39 – Financial Instruments: Recognition and MeasurementAny change in fair value of Liabilities designated FVTPL consequent tochanges in the entity’s own credit risk shall be ignored—IAS 39 treatmentP fit & L & IFRS 9 t t t OCIProfit & Loss & IFRS 9 treatment OCI.

Ind AS 103 – Business CombinationsInd AS 103 requires Bargain Purchase to be recognised in othercomprehensive income and accumulated in equity as capital reserve & ifthere is no clear evidence for the underlying reason for classification of thebusiness combination as a bargain purchase, it shall be recognised directlyin equity as capital reserve. IFRS 3 treatment Profit & Loss.

Ind AS 18 – Revenue→Rate Regulated Entities—Separate Guidance being prepared→ g p g p p→IFRIC 15 relating to real estate revenue recognition has not beenincluded in Ind AS 18. Such agreements have been scoped out from IndAS 18 and have been included in Ind AS 11, Construction Contracts.

17 October 2011 30CA Nilesh S Vikamsey

,

Ind AS 101 – First–time Adoption of Indian Accounting Standards

Carve–outsinIndASInd AS 101 – First–time Adoption of Indian Accounting Standards

Comparative information as per existing standard, comparatives asper Ind AS on a memorandum basis is permissible

Accumulated exchange differences on translation of long termmonetary items deemed to be zero on date of transition if optionto spread unrealised gains/ losses is applied prospectivelyto spread unrealised gains/ losses is applied prospectively

Option to use carrying values of Property, Plant and Equipment(PPE), Intangible Assets, Investment Property as on date of

i i bl i i d d Stransition as an acceptable starting point under Ind AS

Non current Assets held for sale & Discontinued Operations—usetransition date for measuring lower of carrying value & fair valueg y gless cost to sell

Financial Instruments measured at fair value will be measured atfair value on date of transitionfair value on date of transition

17 October 2011 31CA Nilesh S Vikamsey

Statement of Changes in Equity not separate but part of Balance SheetO l i l t t t h f P fit & L (OCI t t ) ti

OtherChangesinIndASOnly single statement approach of Profit & Loss(OCI not separate) –no optionto follow two statement approachOnly nature–wise classification of expenses, no option to follow function wiseInd AS 19 – Employee BenefitsInd AS 19 – Employee Benefits→ Discounting Rate – Market yields on Government Bonds, as IAS 19, the

government bonds can be used only where there is no deep market ofhigh quality corporate bondshigh quality corporate bonds

→ Ind AS 19 requires recognition of actuarial gains/losses in othercomprehensive income and to be recognised immediately in retainedearnings and should not be reclassified to profit or loss in a subsequentperiod

Ind AS 20 – Accounting for Government Grants→ To measure non–monetary grants only at their fair value, option to

measure these grants at nominal value is not available→ To present grants relating to assets in balance sheet by setting up the

grant as deferred income, option to present such grants as deductionf i t f th t i t il blfrom carrying amount of the asset is not available

17 October 2011 32CA Nilesh S Vikamsey

KeyDifferencesBetweenAS and Ind AS

Investment/ Financial Instruments

ASandInd AS/

Fixed Assets

Revenue

Business Combination

Consolidation

Other – PL Impact

Other – BS Impact

Other – Disclosure

17 October 2011 33CA Nilesh S Vikamsey

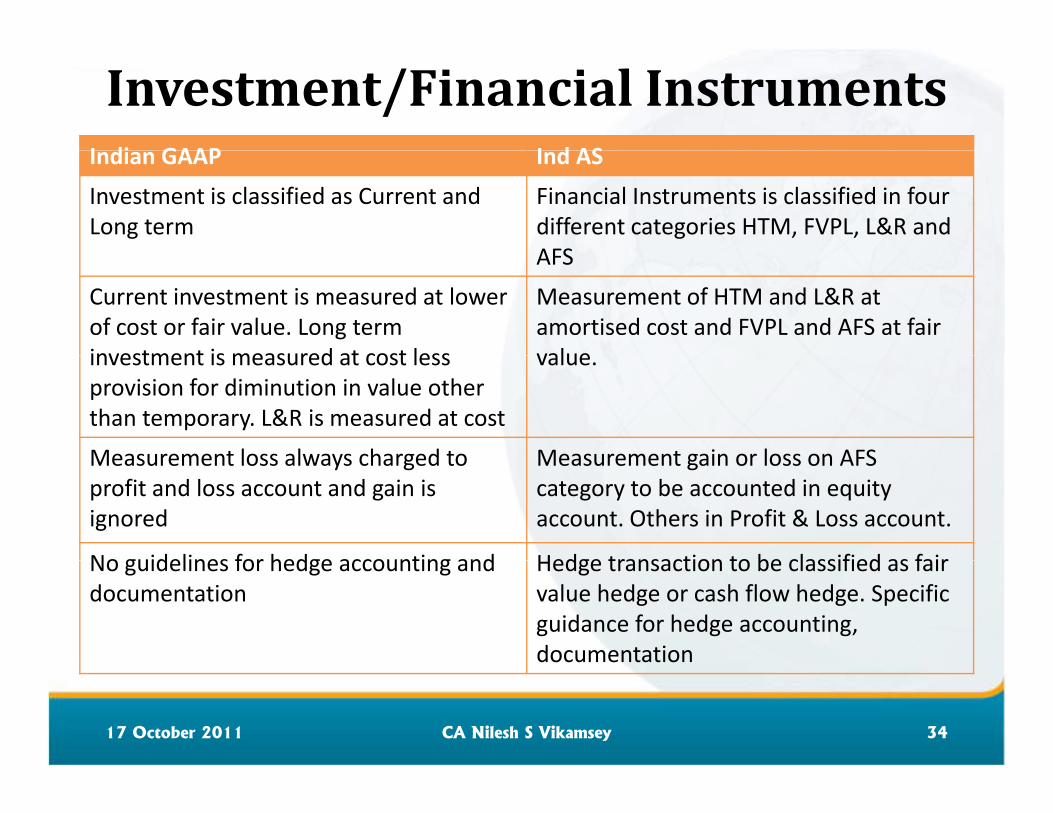

Investment/FinancialInstrumentsI di GAAP I d ASIndian GAAP Ind AS

Investment is classified as Current and Long term

Financial Instruments is classified in four different categories HTM, FVPL, L&R and AFSAFS

Current investment is measured at lower of cost or fair value. Long term investment is measured at cost less

Measurement of HTM and L&R at amortised cost and FVPL and AFS at fair valueinvestment is measured at cost less

provision for diminution in value other than temporary. L&R is measured at cost

value.

Measurement loss always charged to Measurement gain or loss on AFSMeasurement loss always charged to profit and loss account and gain is ignored

Measurement gain or loss on AFS category to be accounted in equity account. Others in Profit & Loss account.

No guidelines for hedge accounting and Hedge transaction to be classified as fairNo guidelines for hedge accounting and documentation

Hedge transaction to be classified as fair value hedge or cash flow hedge. Specific guidance for hedge accounting, documentation

17 October 2011 34CA Nilesh S Vikamsey

Investment/FinancialInstrumentsImpact

Unrealised measurement gain on FVPL will get recognised in PLAccount

Measurement gain/ loss of AFS will not affect PL Account. Onderecognition It will get transferred from equity to PL Accountderecognition, It will get transferred from equity to PL Account

Standardisation and documentation for hedge accounting sincespecific guidance availablep g

Strict provisions for classification of asset in HTM category,hence most of the investment will be classified as FVPL/ AFS andmeasured at fair value

All derivatives classified as FVPL and measured at fair value

17 October 2011 35CA Nilesh S Vikamsey

FixedAssetsIndian GAAP Ind ASFixed assets are not required to be componentized and depreciated separately

Fixed assets are required to be componentized and depreciated separately

Change in depreciation method is considered as change in accounting policy and requires retrospective re–

Change in useful life and depreciation method is considered as change in accounting estimates and applied

computation of depreciation prospectivelyFixed assets are measured at cost less accumulated depreciation

Option to carry at cost less accumulated depreciation or to adopt revaluation model. To carry out revaluation at regular interval

Impact

Each component will get identified, capitalised and depreciated separately. This will change the amount of depreciationIf fair value/revaluation model adopted, value of fixed assets will change on year on year basis

17 October 2011 36CA Nilesh S Vikamsey

RevenueIndian GAAP Ind ASInterest income to be recognizedon a time proportion basis

Interest income to be recognized ateffective interest rateon a time proportion basis effective interest rate

Income from service contract isrecognised as completed service

t t ti t

Income from services to berecognized only on percentage of

l ti th dcontract or proportionatecompletion method

completion method

Amount received ‘on behalf’ can Amount resulting in increase inbe grouped with revenue equity only to be recognised as

revenueContract is not segregated or Contracts needs to be eitherContract is not segregated orcombined for revenue recognition

Contracts needs to be eithersegregated or grouped for revenuerecognition

17 October 2011 37CA Nilesh S Vikamsey

RevenueImpactImpact

Income in financing transaction will spread over period oftransaction and restrict ballooning either at inception or end oftransactione.g. – Interest to be recognised on Effective Interest Rate (i.e. IRR)Income from services will get recognised as per stage ofIncome from services will get recognised as per stage ofcompletion i.e. matching with expenses incurred instead ofrecognizing it at completion of projecte g Income for free services will get recognised when services toe.g. – Income for free services will get recognised when services tobe providedMultiple element transactions will either get combined orp gsegregated as per substance or commercial sense of thetransactione.g.– telecom contractse.g. telecom contracts

17 October 2011 38CA Nilesh S Vikamsey

BusinessCombinationIndian GAAP Ind ASIndian GAAP Ind ASPooling of Interest or PurchaseMethod

Purchase method. All assets andliabilities are recorded at fairmarket value includingintangible assets not recognisedby seller like customer contractsby seller like customer contractsand Brand

Goodwill normally amortised Goodwill is not amortised andover five years tested for impairment

Impact Business Combination will represent true value of assets andliability acquired. This may lead to reduction in goodwillrecognition alsorecognition also

17 October 2011 39CA Nilesh S Vikamsey

ConsolidationI di GAAP I d ASIndian GAAP Ind AS

Potential voting rights are not consideredfor determination of control

Potential voting rights currentlyexercisable or convertible are considered

Option to exclude from consolidation ifcontrol is temporary or operated undersevere long term restriction

All subsidiaries needs to be consolidated.No such exclusion permitted

SPVs are not consolidated if parent doesnot have more than one half of the votingpower or control over composition of BOD

When in substance control is establishedand benefit from SPV flows to parent,consolidation is mandatory

fMinority Interest can not be negative Losses in excess of investment allocated

Associates:Goodwill is recognised based on carryingl

Goodwill is recognised based on fairlvalue

Losses in excess of carrying value is notrecognised

valueLosses in excess of carrying value isrecognised as long term loans

17 October 2011 40CA Nilesh S Vikamsey

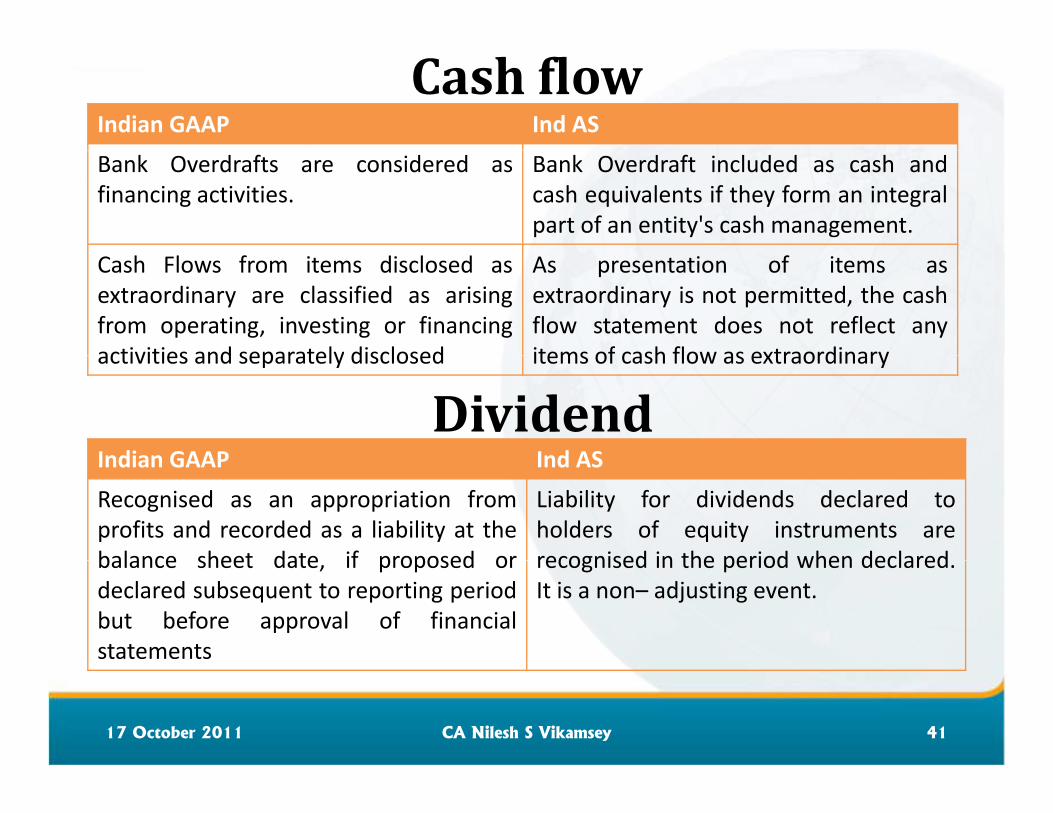

CashflowIndian GAAP Ind AS

Bank Overdrafts are considered asfinancing activities.

Bank Overdraft included as cash andcash equivalents if they form an integralpart of an entity's cash management.

Cash Flows from items disclosed asextraordinary are classified as arisingfrom operating, investing or financingactivities and separately disclosed

As presentation of items asextraordinary is not permitted, the cashflow statement does not reflect anyitems of cash flow as extraordinaryactivities and separately disclosed items of cash flow as extraordinary

DividendIndian GAAP Ind ASIndian GAAP Ind AS

Recognised as an appropriation fromprofits and recorded as a liability at thebalance sheet date if proposed or

Liability for dividends declared toholders of equity instruments arerecognised in the period when declaredbalance sheet date, if proposed or

declared subsequent to reporting periodbut before approval of financialstatements

recognised in the period when declared.It is a non– adjusting event.

17 October 2011 41CA Nilesh S Vikamsey

IFRS8– OperatingSegments

Indian GAAP Ind ASAS 17 requires an enterprise to Operating segments areidentify two segments(business and geographical)using a risks and rewards

identifiable based on thefinancial information that isevaluated regularly by the chiefusing a risks and rewards

approach with the enterprisesystem of internal financial

ti

evaluated regularly by the chiefoperating decision maker indeciding how to allocate

d i irepor.ting resources and in assessingperformance.

17 October 2011 42CA Nilesh S Vikamsey

Other – PLImpactIndian GAAP Ind–ASEmployee BenefitActuarial Gain/ Losses on employeebenefit is recognised immediately

To be taken to OCI (in IFRS Optionto amortise using corridorbenefit is recognised immediately to amortise using corridorapproach)

LeaseI iti l di t t f l b I iti l di t t h t bInitial direct cost of lessor can becharged to PL or amortised overperiod of lease

Initial direct cost has to beamortised over period of lease

Lease of land can be classified asLease of land is treated as sale oflease

finance lease or operating lease

Government GrantGovernment GrantMay be recognised undershareholders’ fund or income in PLover period

Can not be recognised undershareholders’ fund and to berecognised in PL over periodover period recognised in PL over period

17 October 2011 43CA Nilesh S Vikamsey

Other– BSImpactIndian GAAP Ind–ASInventoryValuation of inventory is notapplicable to WIP of service provider

Valuation of inventory is applicable toWIP of service provider alsoapplicable to WIP of service provider WIP of service provider also

Provisions and LiabilityAmount of provision should not bediscounted

Discounting is requireddiscountedLiability is recognised generally oncontractual obligation

Liability is recognised for constructiveobligation also

Liability/ EquityLiability/ EquityCompulsorily convertible debenturesare accounted as liability andmeasured either at fair value or

This are treated as equity if fixed tofixed condition is satisfied

measured either at fair value oramortised costRedeemable preference shares areaccounted as equity

Redeemable preference shares aretreated as liabilityaccounted as equity treated as liability

17 October 2011 44CA Nilesh S Vikamsey

Other– DisclosureImpactIndian GAAP Ind ASIndian GAAP Ind AS

No separate standard for disclosure.Specific formats have been specified byregulators like Co Act, Banking Regulation

Ind AS 1 prescribes minimum structure offinancial statements and contains guidanceon disclosuresg , g g

No requirements for disclosure of criticaljudgments

Disclosure of critical judgments made bymanagemente.g. Ratio of expenses to be incurred forfree services for proportion of revenuedeferment

Effect for prior period errors is given int ith di l

IAS 8 requires retrospective restatement ofi i d fi b t t t fcurrent year with disclosures prior period figures by restatement of

opening balances of assets, liabilities andequity for the earliest period practicable

Contingent Asset is not required to be Contingent Asset is required to beContingent Asset is not required to bedisclosed

Contingent Asset is required to bedisclosed

Non–executive director is not consideredas KMP

Non–executive director is considered asKMPas

17 October 2011 45CA Nilesh S Vikamsey

KeyChallenges

17 October 2011 46CA Nilesh S Vikamsey

KeyChallengesEconomic Environment

Some IFRS/ Ind AS require fair value approach to be followed, exampleIAS/ Ind AS 39, IFRS 13The markets of many economies such as India normally do not haveThe markets of many economies such as India normally do not haveadequate depth and breadth for reliable determination of fair valuesTill date, no viable solution of objective fair value measures is available

Training to PreparersTraining to PreparersSome IFRS/ Ind AS are complex like Ind AS 39, IFRS 9, IFRS 13There is lack of adequate skills amongst the preparers and users ofFinancial Statements to apply IFRS/ Ind ASpp y /Proper implementation of such IFRS/ Ind AS requires extensive educationof preparers

InterpretationpA large number of application issues arise while applying IFRS/ Ind ASThere is a need to have a forum which may address the application issuesin specific cases

17 October 2011 47CA Nilesh S Vikamsey

KeyChallengesNon–compatible Legal and Regulatory Environment

Format of Financial Statement (Schedule VI of the CompaniesAct RBI IRDA SEBI)Act, RBI, IRDA, SEBI)

Restatement of Financial Statements (Companies Act)

Business Combinations (High Court and RBI Order)Business Combinations (High Court and RBI Order)

Provisions against non–performing assets (RBI)

Accounting and disclosure of Financial Instruments (RBI IRDAAccounting and disclosure of Financial Instruments (RBI, IRDA,SEBI)

Recognition of Premium income & Acquisition Cost (IRDA)g q ( )

17 October 2011 48CA Nilesh S Vikamsey

Thank You…

17 October 2011 49CA Nilesh S Vikamsey