institutional equity research q3fy19 results...

TRANSCRIPT

INSTITUTIONAL EQUITY RESEARCH

Page | 1 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 Results Preview

Banks to contribute positively; other sector trends persist

INDIA | Result Preview

9 January 2019

PAT growth will be driven by banks (mainly PSUs), IT, capital goods, and FMCG. We expect contraction for auto, pharma, and cement and muted performance from NBFC and infra segments. Banks will benefit from lower G-sec yields/robust trading income. NPAs are likely to drop, even if banks recognize ILFS exposure in Q3. We see robust deal-flow in IT, strong execution in capital goods. As the entire festive season was in one quarter, price hikes for the FMCG sector will also drive earnings growth for 3Q. We forecast PC-universe* EBITDA growth of 13%. 3Q: Key drivers for the PC universe:

++ Financials – Stable NIMs and strong credit growth to result in robust NII growth (+16% yoy). Higher trading incomes and gains from NPA resolutions to positively influence earnings. GNPA expected to fall, even after accounting for ILFS NPA recognition in Q3.

++Speciality chemicals – Will continue to deliver strong performance led by improved domestic and external demand scenario. Better product mix, favourable currency, and increased realisation from value-added products will drive operating performance.

+ Capital goods – Robust earnings growth to continue, led by strong operating profitability and margin expansion. Order flows to turn weak. We will be closely tracking election impact on order flow guidance, margins, and working capital.

+ FMCG – Retail and consumer discretionary companies will see strong growth vs. staples due to formalisation. Strong revenue growth due to the festive season. Margins are under pressure due to RM cost escalation.

- Automobiles – Tepid festive sales caused broad-based weakness; margins come under pressure due to higher incentives and negative leverage.

- NBFCs – Earnings growth muted at 13% due to margin contraction and moderation in AUM growth. Asset quality to remain stable.

-- Pharma – Earnings to contract by 3% due to weak operating performance. Margins to decline led by on-going price pressure in the US generics business, and higher raw material cost due to Chinese supply disruption.

GNPAs to fall, lower yields are a positive: Within financials, retail banks will continue to report strong performance with NII growth of +23% yoy. Services (NBFCs) and retail (unsecured) will keep driving credit growth. Deposit growth was also strong. MCLR rates have increased by c.10bps on average, while FD rates have increased by c.5-10bps. Slippage should remain in line with Q2FY19. Higher slippages likely from the corporate segment while those in retail and agri should moderate. Key plays: SBI, HDFC Bank, ICICI Bank, Mahindra Finance, Manappuram Finance. Capital goods – operationally strong, order inflows to decline: We estimate 18% yoy rise in earnings in Q3, but adjusting for BHEL and BDL (favourable base) this tapers to 11%, down substantially. After strong 1HFY19 (+50% yoy), we expect order inflows to contract by 21% yoy on a high base – this is because of a significant decline in new orders of L&T (ex-services -40% yoy) and BHEL (-55%), which contributed 78% of 3Q orders. Our key earnings play: Positive: ABB, TMX. Negative: L&T, BHE, VATW, COCHIN. Consumption – FMCG to gain from festive season, not automobiles: FMCG revenues to accelerate due to festive season, price hikes, recovery in CSD channel, and higher penetration. However, margins will moderate due to commodity inflation, no GST related savings. Our earnings play: Jubilant Foodworks, Titan, Nestle, Asian Paints, Marico. Broad-based weakness (in revenues and margins) expected in the auto sector. Tyre companies to see sequential margin pressure due to high-cost inventory. Our earnings play: Escorts.

PAT growth distribution: Q3FY19

Source: PhillipCapital India Research Estimates

Anjali Verma (+ 9122 6246 4115) [email protected] Neeraj Chadawar (+91 22 6246 4116)

PhillipCapital India Research

(6)

(3)

(2)

2

2

9

15

18

21

28

70

149

(50) 0 50 100

Automobiles

Pharma

Cement

Midcap

Infrastructure

NBFC

FMCG

Capital Goods

IT Services

PC - Universe

Specailty Chemicals

Banks

PAT - YoY

Page | 2 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

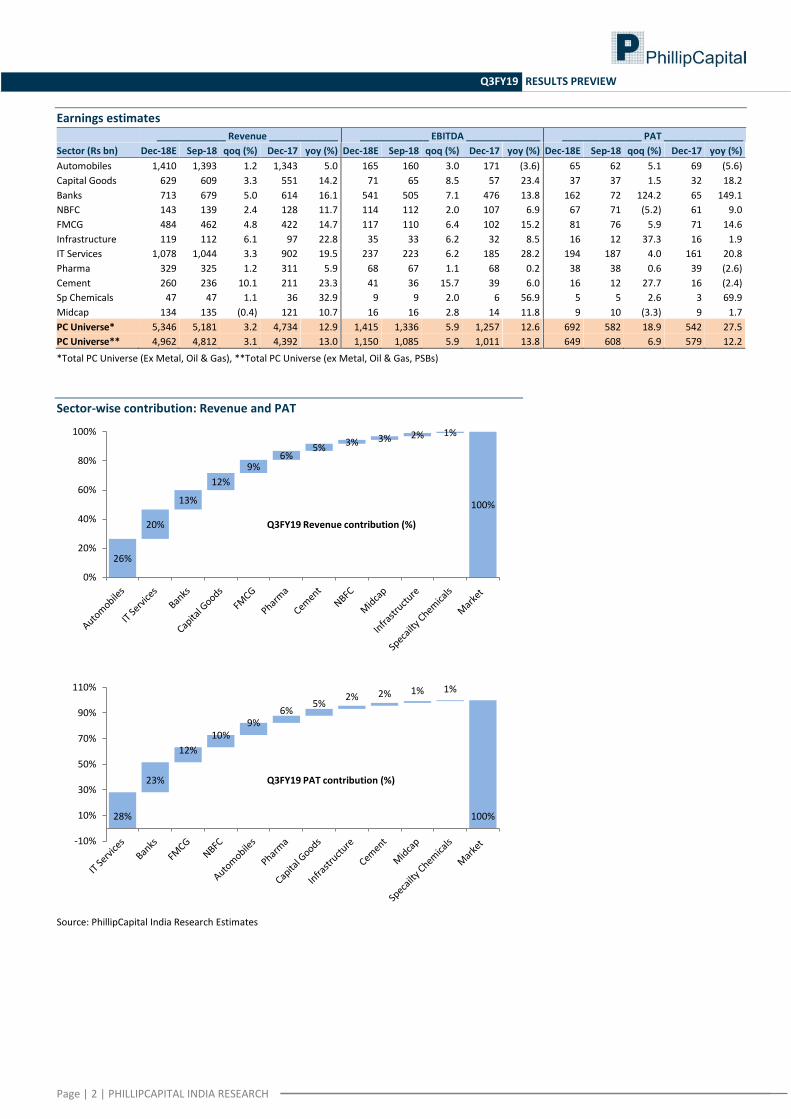

Earnings estimates

_____________ Revenue _____________ _____________ EBITDA ______________ _______________ PAT _______________

Sector (Rs bn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%)

Automobiles 1,410 1,393 1.2 1,343 5.0 165 160 3.0 171 (3.6) 65 62 5.1 69 (5.6)

Capital Goods 629 609 3.3 551 14.2 71 65 8.5 57 23.4 37 37 1.5 32 18.2

Banks 713 679 5.0 614 16.1 541 505 7.1 476 13.8 162 72 124.2 65 149.1

NBFC 143 139 2.4 128 11.7 114 112 2.0 107 6.9 67 71 (5.2) 61 9.0

FMCG 484 462 4.8 422 14.7 117 110 6.4 102 15.2 81 76 5.9 71 14.6

Infrastructure 119 112 6.1 97 22.8 35 33 6.2 32 8.5 16 12 37.3 16 1.9

IT Services 1,078 1,044 3.3 902 19.5 237 223 6.2 185 28.2 194 187 4.0 161 20.8

Pharma 329 325 1.2 311 5.9 68 67 1.1 68 0.2 38 38 0.6 39 (2.6)

Cement 260 236 10.1 211 23.3 41 36 15.7 39 6.0 16 12 27.7 16 (2.4)

Sp Chemicals 47 47 1.1 36 32.9 9 9 2.0 6 56.9 5 5 2.6 3 69.9

Midcap 134 135 (0.4) 121 10.7 16 16 2.8 14 11.8 9 10 (3.3) 9 1.7

PC Universe* 5,346 5,181 3.2 4,734 12.9 1,415 1,336 5.9 1,257 12.6 692 582 18.9 542 27.5

PC Universe** 4,962 4,812 3.1 4,392 13.0 1,150 1,085 5.9 1,011 13.8 649 608 6.9 579 12.2

*Total PC Universe (Ex Metal, Oil & Gas), **Total PC Universe (ex Metal, Oil & Gas, PSBs)

Sector-wise contribution: Revenue and PAT

Source: PhillipCapital India Research Estimates

26%

20%

13%

12%

9% 6%

5% 3% 3% 2% 1%

100%

0%

20%

40%

60%

80%

100%

Q3FY19 Revenue contribution (%)

28%

23%

12%

10% 9%

6% 5%

2% 2% 1% 1%

100%

-10%

10%

30%

50%

70%

90%

110%

Q3FY19 PAT contribution (%)

Page | 3 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Revenue, EBITDA, PAT growth (yoy)

Source: PhillipCapital India Research Estimates

PC universe: Sector-wise EPS (Rs)

Source: PhillipCapital India Research Estimates

(20)

-

20

40

60

80

100

120

140

160 Revenue (Rs mn) EBITDA (Rs mn) PAT (Rs mn)

0

50

100

150

200

250

Q3FY19E Q3FY18

Page | 4 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Key sector highlights

Sector Key observations / outlook Earnings plays

Auto Weak volumes across OEMs as festive season sales fizzle out. Positive: Escorts

Margins to be under pressure across the board led by higher incentives and

negative leverage.

Tyre companies to see some qoq margin pressure due to high cost inventory.

Banking Our banking universe will see +16% yoy (+5% qoq) growth in NIIs, driven by credit

growth and stable NIMs.

Positive: SBI, ICICI Bank and HDFC Bank

Decline in G-Sec yields in the quarter should lead to higher trading income.

Expect GNPAs (%) to decline by c.40bps qoq in Q3 to 11% for the system.

Cement Industry volume growth seen at +8% yoy, 10% qoq. Positive: Shree Cement, JK Cement

Realisations expected to remain flattish qoq in most regions.

Opex/tonne expected to reduce by 1-2% qoq.

EBITDA/tonne for the sector seen at c.Rs 750/tonne (6% yoy; -2% qoq).

Capital Goods Expect our coverage of capital-goods companies to report 18% yoy growth in earnings in Q3. However, excluding BHEL and BDL, which have a low base yoy, the sector PAT growth would be 11% yoy. Revenues should rise 14%. EBITDA growth of 23% yoy is skewed by strong operational results for L&T’s IT Services and Development Project segments and improved margins for majority of the companies (led by BDL, BHEL, GETD). The key highlight for the quarter is weak order inflows announced by L&T and BHEL.

Positive: ABB, TMX

Key monitorables would be: (1) Management outlook on any slowdown on execution and award of new orders due to general election in 1QFY20, (2) impact of lower raw material costs on gross margins, and (3) pressure on working capital.

Negative: L&T, BHE, VATW, COCHIN

Consumer/FMCG Consumer sector’s revenue growth to accelerate qoq on: (1) Entire festive season

falling in 3QFY19, (2) judicious price hikes in key segment, (3) CSD channel on a

recovery path, and (4) increased distribution reach.

Positive: Titan, Jubilant Foods, Nestle, Asian Paints,

Marico

Retail and consumer discretionary companies should see strong growth vs. staples

as the larger theme of formalization remains intact.

Negative: Bajaj Corp, Emami, GCPL

Margins to moderate significantly on: (1) Inflationary pressure in key commodities,

(2) late start to the winter season, and (3) anniversary of GST-related savings.

IT Services Moderate topline growth in constant currency terms – negative CC impact will

lower reported growth.

Positive: TCS, Wipro, LTTS

Margins to expand for most companies due to INR depreciation. Negative: Persistent, TechM

Guidance by Infosys, HCLT, and Wipro will be keenly watched.

Management commentary on deal flow and digital business will be of utmost

importance.

Infrastructure Strong revenue growth for most EPC companies – driven by strong orderbooks. Negative: KNR, IRB, ADSEZ

Margins to decline yoy due to exceptionally high margins last year (GST impact). Positive: NCC, PNC, Ahluwalia

Earnings to report strong yoy growth - topline growth partly mitigated by lower

margins and higher tax.

NBFC We see NII growth for NBFCs under our coverage at a moderate 13% yoy due to

margin contraction and moderation in AUM growth.

Positive: Mahindra Finance and Manappuram

Finance

Margin to see 5-25bps contraction in Q3 as cost of funds shot up after IL&FS’

default in September.

Negative: Shriram City Union

Asset-quality to remain stable.

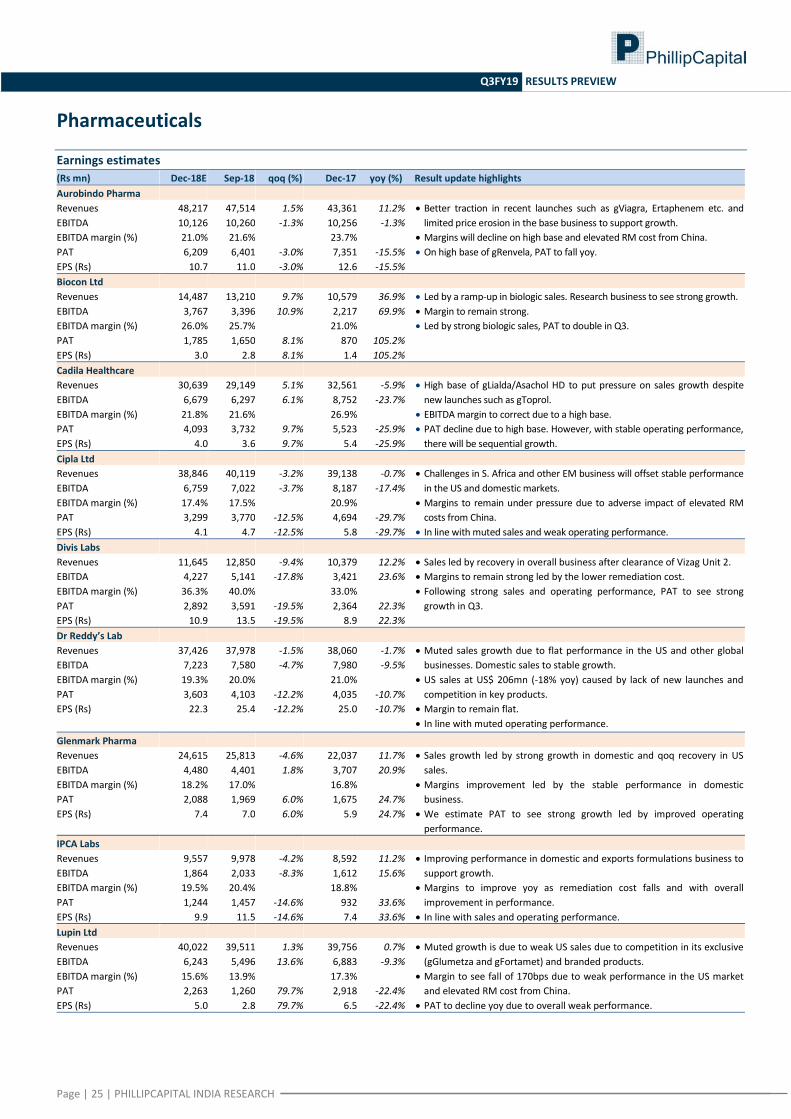

Pharmaceutical We estimate muted 6% yoy growth in revenues for our coverage universe due to

adverse impact of ongoing pricing pressure and incremental competition in the US

generics business.

Positive BIOS IN: Ramp-up in biologic sales will help

earnings to double.

We estimate EBITDA margin to decline at 20.5% for PC’s Pharma universe as

elevated RM prices from China keep operating profits under pressure. As a result,

EBITDA to see flat yoy growth.

Positive DIVI IN: Recovery in overall profitability, led

by reduction in remediation expenses and advantage

of supply disruptions in China.

On weak operating performance, PC’s pharma universe should see an earnings

decline of 3% yoy.

Positive SUNP IN: Stable performance in the US and

currency to support earnings growth.

Negative CIPLA IN: Slow ramp-up in the US and

business challenges in ROW will impact earnings.

Negative LPC IN: Competition in its key drugs and

lack of new launches will cause a fall in earnings.

Specialty Chem Sales to grow by 33%, led by sustained growth across the board and improved

demand scenario in domestic and exports markets. However, due to a lean period

in the global market, revenues will remain muted qoq.

Positive Aarti: Strong performance in the specialty

chemicals segment, led by rising contribution from

value-added products and improved realisation in its

key products, will lead to 30%/70% yoy growth in

overall sales/PAT

Better product mix, favourable currency, and increased realisation from value- Positive VO: Robust sales growth led by the strong

Page | 5 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

added products will drive operating performance. EBITDA margin to expand by

c.295bps yoy, but due to no growth in product pricing qoq and INR appreciation,

there would be no expansion in margin sequentially.

performance in ATBS business, despite temporary

demand issue in IBB business, will result in 42% yoy

growth in sales. On a low base, earnings to double

yoy (+2% qoq).

In line with strong sales/operating performance, earnings growth should be

healthy at 70% yoy, but it will remain muted qoq – with a growth of 3%.

Positive CFIN: Sales growth of 9% yoy, led by strong

performance in the blends operations and

incremental sales from its China vanillin facility.

Margin to see smart recovery at 9.7% with improved

product mix, resulting in continuous improvement in

profitability

Positive ATLP: Healthy growth in both life sciences

and performance chemicals will lead to a 21% yoy

growth in sales. Mainly strong prices in agro and

aromatics will expand margin by 300bps yoy, which

will lead to strong yoy earnings growth of 31% yoy (-

2% qoq)

Source: PhillipCapital India Research

Page | 6 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Automobiles

Earnings estimates

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Maruti Suzuki

Revenues 195443 222332 -12.1% 192832 1.4% Revenue to improve 1% yoy led by realisation.

EBITDA margin to compress 150bps qoq led by higher incentives,

negative leverage, and adverse forex impact.

EBITDA 25450 32313 -21.2% 30378 -16.2%

EBITDA margin (%) 13.0% 14.5% 15.8%

PAT 15753 20404 -22.8% 17990 -12.4%

EPS (Rs) 52 68 -22.8% 60 -12.4%

JLR

Revenues 6628 5635 17.6% 6310 5.0% Revenue to grow by 5% yoy led by 4% realisation improvement.

EBITDA margin to rebound 230bps qoq, led by operating leverage and

cost saving.

EBITDA 755 511 47.7% 685 10.2%

EBITDA margin (%) 11.4% 9.1% 10.9%

PAT 142 -101 -240.8% 89 59.7%

Tata Motors

Revenues 158555 177587 -10.7% 161016 -1.5% Revenue to decline by 2% yoy due to flat volumes and higher

discounts.

Margin to decrease by 150bps qoq due to operating leverage.

EBITDA 8360 12000 -30.3% 15200

EBITDA margin (%) 5.3% 6.8% 9.4%

PAT -1084 1091 -199.3% 1837 -159.0%

EPS (Rs) 0 0 1

Mahindra & Mahindra

Revenues 129096 127902 0.9% 114915 12.3% 12% yoy revenue growth backed by 11% growth in automotive and

tractor volumes.

Operating leverage to aid EBIDTA margin increase of 30bps qoq.

EBITDA 19080 18493 3.2% 16926 12.7%

EBITDA margin (%) 14.8% 14.5% 14.7%

PAT 10346 17788 -41.8% 13057 -20.8%

EPS (Rs) 17 29 -40.2% 20 -11.9%

Ashok Leyland

Revenues 62799 76080 -17.5% 71132 -11.7% Revenue to decrease by 12% yoy led 17% decrease in MHCV volume.

Margins to shrink by 250 bps qoq on higher discounting and negative

leverage.

EBITDA 5065 8059 -37.2% 7884 -35.8%

EBITDA margin (%) 8.1% 10.6% 11.1%

PAT 2623 4596 -42.9% 4499 -41.7%

EPS (Rs) 0.9 1.7 -44.8% 1.6 -41.7%

Bajaj Auto

Revenues 75085 79868 -6.0% 63693 17.9% 26% yoy jump in volumes helps revenue grow by 18%.

Margins to decline by 70bps qoq, despite higher volumes, due to

weak mix and high discount.

EBITDA 12062 13422 -10.1% 12315 -2.1%

EBITDA margin (%) 16.1% 16.8% 19.3%

PAT 10569 11517 -8.2% 9524 11.0%

EPS (Rs) 37 40 -8.2% 33 11.0%

Hero MotoCorp

Revenues 76802 90909 -15.5% 73055 5.1% Revenue to increase by 5% sequentially led by volume.

Margin to decline 120bps qoq due to high RM cost pressure and

operating leverage.

EBITDA 10780 13787 -21.8% 11580 -6.9%

EBITDA margin (%) 14.0% 15.2% 15.9%

PAT 7736 9763 -20.8% 8054 -4.0%

EPS (Rs) 39 49 -20.8% 40 -4.0%

Apollo Tyres

Revenues 46881 42574 10.1% 40501 15.8% We expect consolidated revenue to grow by 16% yoy. Standalone

revenue growth momentum to slowdown to 15% yoy.

EBITDA margin to remain flat. Margin pressure in India due to high

cost inventory, abetted by operating leverage, and seasonality in

Europe.

EBITDA 5157 4672 10.4% 4964 3.9%

EBITDA margin (%) 11.0% 11.0% 12.3%

PAT 2209 1460 51.3% 2453 -9.9%

EPS (Rs) 4 3 18.8% 4 -9.9%

Bharat Forge

Revenues 15474 16792 -7.9% 13580 14.0% Revenue to rise 14% yoy led by realisation.

Margins to increase by 50 bps qoq. EBITDA 4464 4754 -6.1% 3837 16.3%

EBITDA margin (%) 28.8% 28.3% 28.3%

PAT 2426 2685 -9.7% 1956 24.0%

EPS (Rs) 10 12 -9.7% 8 24.0%

Mahindra CIE

Revenues 18834 19326 -2.5% 16184 16.4% Revenue of European business to grow 20% yoy, India business up 9%

yoy.

Margins to decline by 60bps qoq led by negative operating leverage.

EBITDA 2429 2610 -6.9% 2419 0.4%

EBITDA margin (%) 12.9% 13.5% 14.9%

Page | 7 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Ceat

Revenues 17901 17546 2.0% 15742 13.7% Revenue to rise 14% yoy, led by 8% yoy volume growth, as OEM sales

slowed.

EBITDA margins to decline 50bps qoq due to existing high cost

inventory.

EBITDA 1543 1592 -3.1% 1870 -17.4%

EBITDA margin (%) 8.6% 9.1% 11.9%

PAT 604 657 -8.1% 831 -27.3%

EPS (Rs) 15 16 -8.1% 20 -27.3%

Escorts

Revenues 16138 13984 15.4% 12050 33.9% Revenue growth of 34% yoy led by 36% yoy tractor volume growth.

Margin to improve led by operating leverage. EBITDA 2005 1575 27.3% 1450 38.2%

EBITDA margin (%) 12.4% 11.3% 12.0%

PAT 1272 1027 23.9% 920 38.3%

EPS (Rs) 11 9 23.9% 8 38.5%

RK Forgings

Revenues 4329 4615 -6.2% 4001 8.2% Revenues to grow by 8% yoy led by strong exports and weak

domestics. EBITDA 913 979 -6.7% 771 18.4%

EBITDA margin (%) 21.1% 21.2% 19.3%

PAT 293 328 -10.7% 277 5.6%

EPS (Rs) 10 11 -10.7% 10 5.6%

Source: Company, PhillipCapital India Research

Page | 8 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Banking

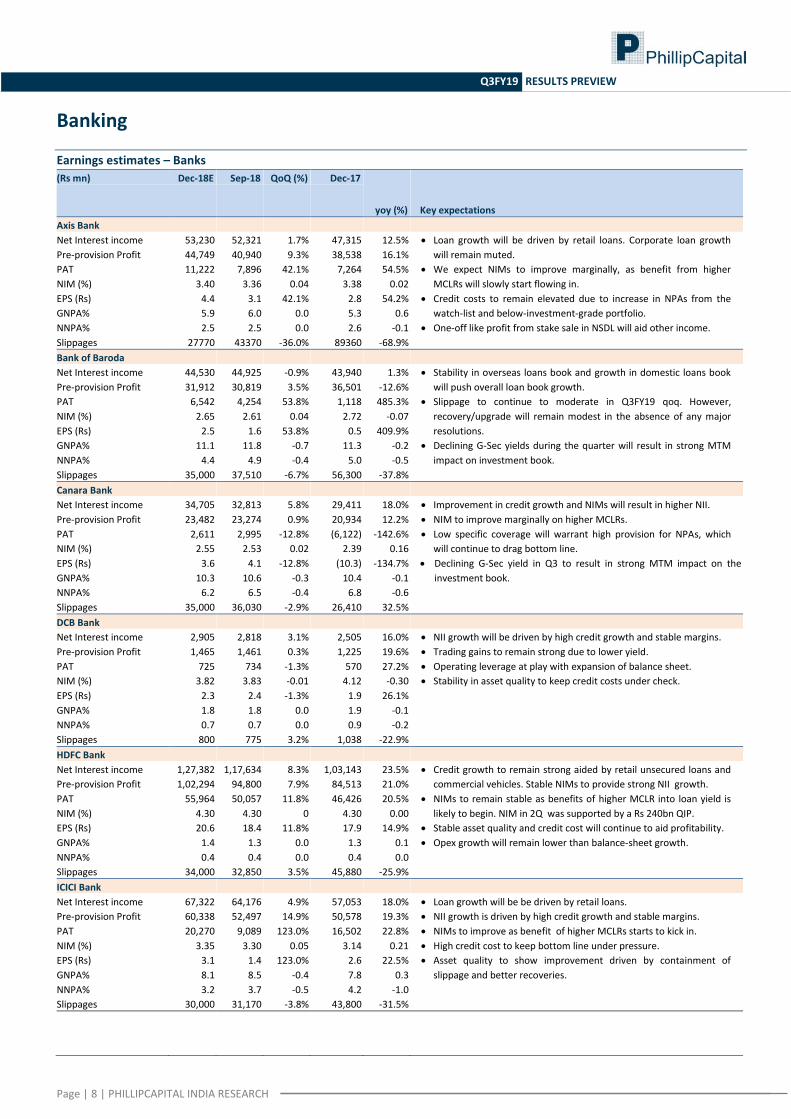

Earnings estimates – Banks

(Rs mn) Dec-18E Sep-18 QoQ (%) Dec-17

yoy (%) Key expectations

Axis Bank

Net Interest income 53,230 52,321 1.7% 47,315 12.5% Loan growth will be driven by retail loans. Corporate loan growth

will remain muted.

We expect NIMs to improve marginally, as benefit from higher

MCLRs will slowly start flowing in.

Credit costs to remain elevated due to increase in NPAs from the

watch-list and below-investment-grade portfolio.

One-off like profit from stake sale in NSDL will aid other income.

Pre-provision Profit 44,749 40,940 9.3% 38,538 16.1%

PAT 11,222 7,896 42.1% 7,264 54.5%

NIM (%) 3.40 3.36 0.04 3.38 0.02

EPS (Rs) 4.4 3.1 42.1% 2.8 54.2%

GNPA% 5.9 6.0 0.0 5.3 0.6

NNPA% 2.5 2.5 0.0 2.6 -0.1

Slippages 27770 43370 -36.0% 89360 -68.9%

Bank of Baroda

Net Interest income 44,530 44,925 -0.9% 43,940 1.3% Stability in overseas loans book and growth in domestic loans book

will push overall loan book growth.

Slippage to continue to moderate in Q3FY19 qoq. However,

recovery/upgrade will remain modest in the absence of any major

resolutions.

Declining G-Sec yields during the quarter will result in strong MTM

impact on investment book.

Pre-provision Profit 31,912 30,819 3.5% 36,501 -12.6%

PAT 6,542 4,254 53.8% 1,118 485.3%

NIM (%) 2.65 2.61 0.04 2.72 -0.07

EPS (Rs) 2.5 1.6 53.8% 0.5 409.9%

GNPA% 11.1 11.8 -0.7 11.3 -0.2

NNPA% 4.4 4.9 -0.4 5.0 -0.5

Slippages 35,000 37,510 -6.7% 56,300 -37.8%

Canara Bank

Net Interest income 34,705 32,813 5.8% 29,411 18.0% Improvement in credit growth and NIMs will result in higher NII.

NIM to improve marginally on higher MCLRs.

Low specific coverage will warrant high provision for NPAs, which

will continue to drag bottom line.

Declining G-Sec yield in Q3 to result in strong MTM impact on the

investment book.

Pre-provision Profit 23,482 23,274 0.9% 20,934 12.2%

PAT 2,611 2,995 -12.8% (6,122) -142.6%

NIM (%) 2.55 2.53 0.02 2.39 0.16

EPS (Rs) 3.6 4.1 -12.8% (10.3) -134.7%

GNPA% 10.3 10.6 -0.3 10.4 -0.1

NNPA% 6.2 6.5 -0.4 6.8 -0.6

Slippages 35,000 36,030 -2.9% 26,410 32.5%

DCB Bank

Net Interest income 2,905 2,818 3.1% 2,505 16.0% NII growth will be driven by high credit growth and stable margins.

Trading gains to remain strong due to lower yield.

Operating leverage at play with expansion of balance sheet.

Stability in asset quality to keep credit costs under check.

Pre-provision Profit 1,465 1,461 0.3% 1,225 19.6%

PAT 725 734 -1.3% 570 27.2%

NIM (%) 3.82 3.83 -0.01 4.12 -0.30

EPS (Rs) 2.3 2.4 -1.3% 1.9 26.1%

GNPA% 1.8 1.8 0.0 1.9 -0.1

NNPA% 0.7 0.7 0.0 0.9 -0.2

Slippages 800 775 3.2% 1,038 -22.9%

HDFC Bank

Net Interest income 1,27,382 1,17,634 8.3% 1,03,143 23.5% Credit growth to remain strong aided by retail unsecured loans and

commercial vehicles. Stable NIMs to provide strong NII growth.

NIMs to remain stable as benefits of higher MCLR into loan yield is

likely to begin. NIM in 2Q was supported by a Rs 240bn QIP.

Stable asset quality and credit cost will continue to aid profitability.

Opex growth will remain lower than balance-sheet growth.

Pre-provision Profit 1,02,294 94,800 7.9% 84,513 21.0%

PAT 55,964 50,057 11.8% 46,426 20.5%

NIM (%) 4.30 4.30 0 4.30 0.00

EPS (Rs) 20.6 18.4 11.8% 17.9 14.9%

GNPA% 1.4 1.3 0.0 1.3 0.1

NNPA% 0.4 0.4 0.0 0.4 0.0

Slippages 34,000 32,850 3.5% 45,880 -25.9%

ICICI Bank

Net Interest income 67,322 64,176 4.9% 57,053 18.0% Loan growth will be be driven by retail loans.

NII growth is driven by high credit growth and stable margins.

NIMs to improve as benefit of higher MCLRs starts to kick in.

High credit cost to keep bottom line under pressure.

Asset quality to show improvement driven by containment of

slippage and better recoveries.

Pre-provision Profit 60,338 52,497 14.9% 50,578 19.3%

PAT 20,270 9,089 123.0% 16,502 22.8%

NIM (%) 3.35 3.30 0.05 3.14 0.21

EPS (Rs) 3.1 1.4 123.0% 2.6 22.5%

GNPA% 8.1 8.5 -0.4 7.8 0.3

NNPA% 3.2 3.7 -0.5 4.2 -1.0

Slippages 30,000 31,170 -3.8% 43,800 -31.5%

Page | 9 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

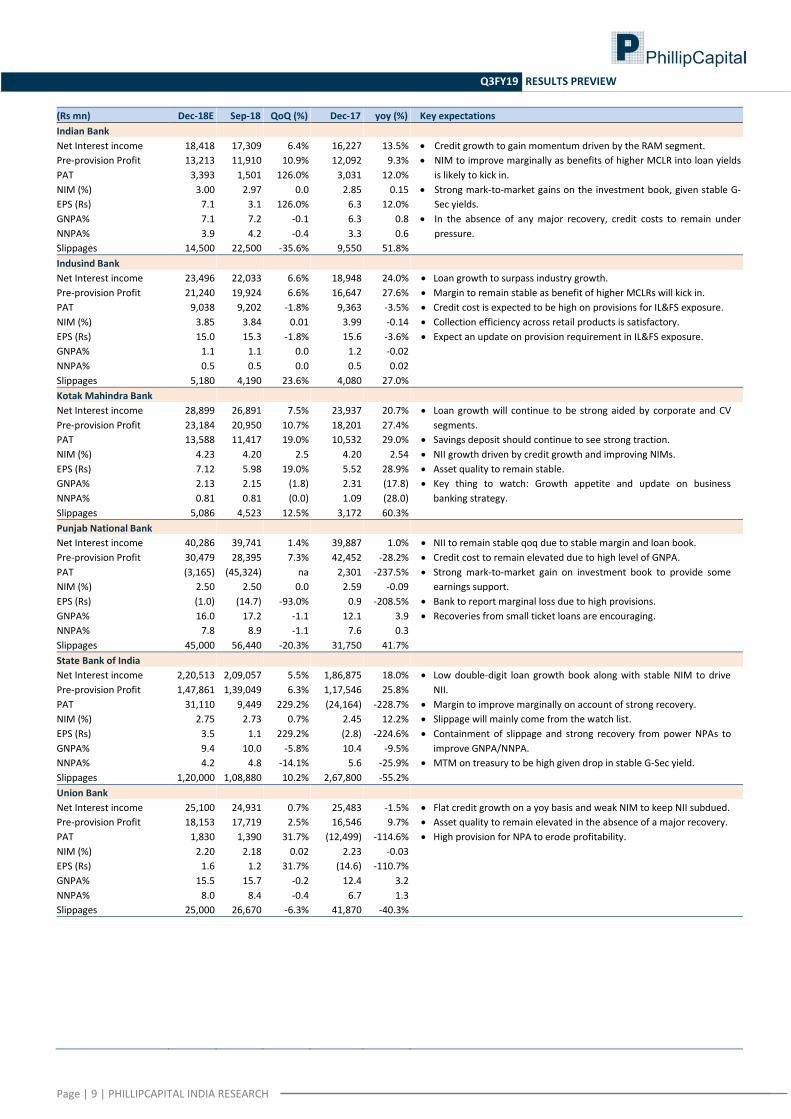

(Rs mn) Dec-18E Sep-18 QoQ (%) Dec-17 yoy (%) Key expectations

Indian Bank

Net Interest income 18,418 17,309 6.4% 16,227 13.5% Credit growth to gain momentum driven by the RAM segment.

NIM to improve marginally as benefits of higher MCLR into loan yields

is likely to kick in.

Strong mark-to-market gains on the investment book, given stable G-

Sec yields.

In the absence of any major recovery, credit costs to remain under

pressure.

Pre-provision Profit 13,213 11,910 10.9% 12,092 9.3%

PAT 3,393 1,501 126.0% 3,031 12.0%

NIM (%) 3.00 2.97 0.0 2.85 0.15

EPS (Rs) 7.1 3.1 126.0% 6.3 12.0%

GNPA% 7.1 7.2 -0.1 6.3 0.8

NNPA% 3.9 4.2 -0.4 3.3 0.6

Slippages 14,500 22,500 -35.6% 9,550 51.8%

Indusind Bank

Net Interest income 23,496 22,033 6.6% 18,948 24.0% Loan growth to surpass industry growth.

Margin to remain stable as benefit of higher MCLRs will kick in.

Credit cost is expected to be high on provisions for IL&FS exposure.

Collection efficiency across retail products is satisfactory.

Expect an update on provision requirement in IL&FS exposure.

Pre-provision Profit 21,240 19,924 6.6% 16,647 27.6%

PAT 9,038 9,202 -1.8% 9,363 -3.5%

NIM (%) 3.85 3.84 0.01 3.99 -0.14

EPS (Rs) 15.0 15.3 -1.8% 15.6 -3.6%

GNPA% 1.1 1.1 0.0 1.2 -0.02

NNPA% 0.5 0.5 0.0 0.5 0.02

Slippages 5,180 4,190 23.6% 4,080 27.0%

Kotak Mahindra Bank

Net Interest income 28,899 26,891 7.5% 23,937 20.7% Loan growth will continue to be strong aided by corporate and CV

segments.

Savings deposit should continue to see strong traction.

NII growth driven by credit growth and improving NIMs.

Asset quality to remain stable.

Key thing to watch: Growth appetite and update on business

banking strategy.

Pre-provision Profit 23,184 20,950 10.7% 18,201 27.4%

PAT 13,588 11,417 19.0% 10,532 29.0%

NIM (%) 4.23 4.20 2.5 4.20 2.54

EPS (Rs) 7.12 5.98 19.0% 5.52 28.9%

GNPA% 2.13 2.15 (1.8) 2.31 (17.8)

NNPA% 0.81 0.81 (0.0) 1.09 (28.0)

Slippages 5,086 4,523 12.5% 3,172 60.3%

Punjab National Bank

Net Interest income 40,286 39,741 1.4% 39,887 1.0% NII to remain stable qoq due to stable margin and loan book.

Credit cost to remain elevated due to high level of GNPA.

Strong mark-to-market gain on investment book to provide some

earnings support.

Bank to report marginal loss due to high provisions.

Recoveries from small ticket loans are encouraging.

Pre-provision Profit 30,479 28,395 7.3% 42,452 -28.2%

PAT (3,165) (45,324) na 2,301 -237.5%

NIM (%) 2.50 2.50 0.0 2.59 -0.09

EPS (Rs) (1.0) (14.7) -93.0% 0.9 -208.5%

GNPA% 16.0 17.2 -1.1 12.1 3.9

NNPA% 7.8 8.9 -1.1 7.6 0.3

Slippages 45,000 56,440 -20.3% 31,750 41.7%

State Bank of India

Net Interest income 2,20,513 2,09,057 5.5% 1,86,875 18.0% Low double-digit loan growth book along with stable NIM to drive

NII.

Margin to improve marginally on account of strong recovery.

Slippage will mainly come from the watch list.

Containment of slippage and strong recovery from power NPAs to

improve GNPA/NNPA.

MTM on treasury to be high given drop in stable G-Sec yield.

Pre-provision Profit 1,47,861 1,39,049 6.3% 1,17,546 25.8%

PAT 31,110 9,449 229.2% (24,164) -228.7%

NIM (%) 2.75 2.73 0.7% 2.45 12.2%

EPS (Rs) 3.5 1.1 229.2% (2.8) -224.6%

GNPA% 9.4 10.0 -5.8% 10.4 -9.5%

NNPA% 4.2 4.8 -14.1% 5.6 -25.9%

Slippages 1,20,000 1,08,880 10.2% 2,67,800 -55.2%

Union Bank

Net Interest income 25,100 24,931 0.7% 25,483 -1.5% Flat credit growth on a yoy basis and weak NIM to keep NII subdued.

Asset quality to remain elevated in the absence of a major recovery.

High provision for NPA to erode profitability.

Pre-provision Profit 18,153 17,719 2.5% 16,546 9.7%

PAT 1,830 1,390 31.7% (12,499) -114.6%

NIM (%) 2.20 2.18 0.02 2.23 -0.03

EPS (Rs) 1.6 1.2 31.7% (14.6) -110.7%

GNPA% 15.5 15.7 -0.2 12.4 3.2

NNPA% 8.0 8.4 -0.4 6.7 1.3

Slippages 25,000 26,670 -6.3% 41,870 -40.3%

Page | 10 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 QoQ (%) Dec-17 yoy (%) Key expectations

Yes Bank

Net Interest income 25,812 24,176 6.8% 18,888 36.7% Credit growth expected to slow down to 3.6% qoq vs. 11% in 2Q.

NIMs to remain stable; we see NIMs to begin rising from FY20.

Slippage to spike up due to RBI’s AQR report. We have built in Rs

40bn divergence in our numbers. Credit cost to be higher.

Watch: Divergence, update on management transition.

Pre-provision Profit 23,024 23,664 -2.7% 20,018 15.0%

PAT 8,992 9,646 -6.8% 10,769 -16.5%

NIM (%) 3.28 3.30 -2.17 3.50 -22.17

EPS (Rs) 3.9 4.1 -3.8% 4.6 -15.3%

GNPA% 3.1 1.6 146.5 1.7 135.8

NNPA% 2.0 0.8 113.6 0.9 104.9

Slippages 47,925 16,316 193.7% 4,949 868.3%

Earnings estimates – Housing Finance Companies

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

HDFC Limited

Net Interest income 34,437 30,261 13.8% 29,687 16.0% Has adopted Ind-AS accounting standard. Our estimates are based

on Indian GAAP.

Loan growth driven by individual segment. Sold loans worth Rs

69.6bn to HDFC Bank.

Spread to remain stable as rise in cost would be offset by an increase

in rate and high corporate loan growth.

Dividend received is Rs 20mn vs. Rs 1,510mn last year. Asset quality

to remain stable.

Watch: Management commentary on capital allocation.

Pre-provision Profit 32,843 28,904 13.6% 28,805 14.0%

PAT 22,609 24,671 -8.4% 19,934 13.4%

EPS (Rs) 13.3 14.5 -8.4% 12.5 6.8%

LIC Housing Finance

Net Interest income 10,233 10,123 1.1% 8,976 14.0% Has adopted Ind AS. Our estimate is based on Indian GAAP.

Loan growth of 15% to be driven housing loans.

Favourable base to reflect NII growth.

Asset quality likely to remain stable.

Pre-provision Profit 9,252 9,633 -4.0% 8,050 14.9%

PAT 5,881 5,732 2.6% 4,911 19.8%

EPS (Rs) 11.7 11.4 2.6% 9.7 19.8%

Repco Home Finance

Net Interest income 1,200 1,115 7.6% 1,071 12.0% Adopted Ind AS. Our estimate is based on Indian GAAP.

Disbursement to improve yoy but decline qoq.

Loan growth seen in lower double digits.

NIM will remain stable as increase in yields offset rise in cost of

funds.

Seasonally weak quarter in terms of asset quality. Expect some spike

in GNPA.

Pre-provision Profit 1,041 969 7.4% 935 11.2%

PAT 634 666 -4.8% 485 30.7%

EPS (Rs) 10.1 10.6 -4.8% 7.7 30.8%

Indiabulls Housing Fin

Net Interest income 14,321 14,240 0.6% 13,960 2.6% Adopted Ind AS. Our estimate is based on Indian GAAP.

Loan book to moderate due to the liquidity crisis in Q3.

NIM to contract as cost of fund rose sharply.

Some loan segments such as home loan and construction finance

may remain flat qoq.

Pre-provision Profit 12,280 14,266 -13.9% 18,867 -34.9%

PAT 8,807 10,442 -15.7% 11,677 -24.6%

EPS (Rs) 20.7 24.5 -15.3% 21.9 -5.3%

Dewan Housing Finance

Net Interest income 4,595 8,310 -44.7% 6,256 -26.5% Adopted Ind AS. Our estimate is based on Indian GAAP.

Loan growth to see de-growth qoq due to standstill in new business

impacted by liquidity crisis.

Sharp decline in disbursement and sell down of loan will lead to

decline in loan book qoq.

NIMs under pressure, but asset quality stable.

Pre-provision Profit 6,055 7,656 -20.9% 5,617 7.8%

PAT 3,301 4,387 -24.8% 3,060 7.9%

EPS (Rs) 10.5 14.0 -24.8% 9.8 7.8%

Source: Company, PhillipCapital India Research Estimates

Page | 11 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Earnings estimates – NBFC

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Shriram Transport Fin

Net Interest income 20,482 20,553 -0.3% 17,094 19.8% NIIs to decline qoq as disbursement declines and margin contracts.

Operating profit growth broadly in line with topline growth.

Asset quality to remain stable.

Higher cost of funds to drive contraction in NIMs.

Pre-provision Profit 16,044 16,226 -1.1% 13,486 19.0%

PAT 5,942 6,096 -2.5% 4,956 19.9%

NIM (%) 7.8 8.0 -0.27 7.8 0.00

EPS (Rs) 26.2 26.9 -2.5% 21.8 19.9%

Cholamandalam Fin.

Net Interest income 8,362 8,119 3.0% 7,930 5.5% Lower NIMs due to higher cost of funds leads to lower NII growth, even

as AUM growth remains healthy at 26%.

Favourable base helps drive operating profit growth.

Asset quality to remain stable.

Higher cost of funds to lead to lower NIMs.

Pre-provision Profit 5,378 5,207 3.3% 4,694 14.6%

PAT 2,878 3,047 -5.5% 2,492 15.5%

NIM (%) 6.9 7.0 -0.10 8.4 -1.50

EPS (Rs) 18.4 19.5 -5.5% 15.9 15.5%

Mah & Mah Finance

Net Interest income 12,809 11,666 9.8% 10,711 19.6% Strong growth in disbursements to drive growth in NII.

With lower increase in opex, operating profit growth to be higher at

27%.

Asset quality to improve helped by higher collections.

Higher cost of funds to lead to lower NIMs.

Pre-provision Profit 8,364 7,869 6.3% 6,553 27.6%

PAT 4,096 3,814 7.4% 3,420 19.8%

NIM (%) 8.4 7.9 0.50 8.7 -0.26

EPS (Rs) 6.7 6.2 7.4% 5.6 19.8%

Shriram City Union Fin

Net Interest income 9,913 10,197 -2.8% 9,157 8.3% Decline in disbursement and lower NIMs to lead to moderation in NII

growth.

NIMs to contract 71bps yoy led by higher cost of funds.

Asset quality to remain stable.

Decline in disbursement and lower NIMs to lead to moderation in NII

growth.

Pre-provision Profit 6,143 6,243 -1.6% 5,449 12.7%

PAT 2,106 2,493 -15.5% 2,255 -6.6%

NIM (%) 13.6 13.8 -0.24 14.3 -0.71

EPS (Rs) 31.9 37.8 -15.5% 34.2 -6.6%

Manappuram Finance

Net Interest income 6,915 6,971 -0.8% 6,153 12.4% Lower NIMs to keep NII growth moderate.

Implementation of cellular vaults to drive further reduction in opex.

Asset quality to remain stable.

Rising share of lower yielding products and higher cost of funds driving

margin contraction.

Pre-provision Profit 3,850 3,662 5.1% 3,056 26.0%

PAT 2,350 2,240 4.9% 1,733 35.6%

NIM (%) 15.7 16.2 -0.52 16.8 -1.10

EPS (Rs) 2.8 2.7 4.9% 2.1 35.6%

Muthoot Finance

Net Interest income 11,416 11,143 2.4% 10,538 8.3% Higher base to impact NII growth.

Higher opex growth to keep operating level growth muted.

Rising share of lower yielding products and higher cost of funds driving

margin contraction.

Pre-provision Profit 7,703 7,478 3.0% 7,767 -0.8%

PAT 5,141 4,838 6.3% 4,637 10.9%

NIM (%) 14.0 14.1 -0.08 15.1 -1.09

EPS (Rs) 12.8 12.1 6.3% 11.6 10.8%

Magma Finance

Net Interest income 3,602 3,498 3.0% 3,593 0.3% NII growth flat as AUM remains broadly stable.

NIMs to contract due to higher cost of funds.

Favourable base to drive strong earnings growth.

NII growth flat as AUM remains broadly stable.

Pre-provision Profit 2,018 1,913 5.5% 1,942 3.9%

PAT 852 766 11.3% 650 31.1%

NIM (%) 8.6 8.6 -0.04 9.3 -0.74

EPS (Rs) 3.6 3.3 11.3% 2.8 31.1%

Source: Company, PhillipCapital India Research Estimates

Page | 12 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Capital Goods & Engineering

Earnings estimates

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations / assumptions

Capital goods

Order inflows 6,08,185 7,86,515 -22.7% 7,68,281 -20.8% 21% yoy decline in new orders mainly due to weak L&T (-31%) and BHEL (-

55%) order inflows.

Revenue likely to grow 14% yoy driven by strong order book of 2.7x TTM

sales. Execution will be driven by L&T, ENGR, BHE, TMX, and SIEM.

EBITDA growth of 23% yoy, mainly on strong operational results for L&T’s IT

Services and Development Project segments and improved margins on a low

base in most of the companies (led by BDL, BHEL, GETD, KKC, TMX).

Excluding L&T services, our coverage EBITDA should grow by 14% yoy.

PAT to grow 18% yoy; excluding BDL and BHEL, PAT growth would be 11%.

Order book 53,09,923 52,93,169 0.3% 48,90,275 8.6%

Revenues 6,28,981 6,08,786 3.3% 5,50,858 14.2%

EBITDA 70,901 65,323 8.5% 57,458 23.4%

EBITDA Margin (%) 11.3% 10.7% 54bps 10.4% 84bps

PAT 37,307 36,760 1.5% 31,562 18.2%

ABB India

Order inflows 31,026 23,550 31.7% 29,111 6.6% Expect slow growth in new orders due to weak Power Grids segment orders.

Revenues to be driven by strong execution on a weak base across all

segments excluding Power Grids.

EBITDA margins to improve 45bps yoy, supported by improved gross

margins.

Order book 1,13,471 1,13,680 -0.2% 1,15,340 -1.6%

Revenues 31,235 25,154 24.2% 27,794 12.4%

EBITDA 3,436 1,940 77.1% 2,937 17.0%

EBITDA Margin (%) 11.0% 7.7% 329bps 10.6% 43bps

PAT 2,085 1,083 92.5% 1,715 21.6%

EPS (Rs) 9.8 5.1 92.5% 8.1 21.6%

Bharat Dynamics

Revenues 9,047 6,060 49.3% 8,225 10.0% Revenues to be supported by pick up in production of missiles which was

impacted due to a technical snag during 2Q.

Expect strong expansion in EBITDA margins as gross margins will improve

because of better sales mix.

EBITDA 1,508 660 128.4% 445 239.1%

EBITDA Margin (%) 16.7% 10.9% 577bps 5.4% 1126bps

PAT 1,035 283 265.1% 62 1574.5%

EPS (Rs) 5.6 1.5 265.1% 0.3 1574.5%

Bharat Electronics Order inflows 57,300 1,07,550 -46.7% 11,460 400.0% Robust new orders led by award of Akash 7 sqdn project (Rs 53bn).

Expect strong growth in revenues on a high base yoy led by execution of

EVM/VVPAT orders.

EBITDA margins likely to shrink on a weaker sales mix.

PAT will be further impacted by lower other income.

Order book 5,16,596 4,89,950 5.4% 4,04,690 27.7%

Revenues 30,904 33,814 -8.6% 25,128 23.0%

EBITDA 5,184 8,544 -39.3% 4,852 6.9%

EBITDA Margin (%) 16.8% 25.3% -849bps 19.3% -253bps

PAT 3,260 5,713 -42.9% 3,308 -1.5%

EPS (Rs) 1.3 2.3 -42.9% 1.3 -1.5%

BHEL

Order inflows 54,594 51,590 5.8% 1,21,320 -55.0% Order inflows likely to be weak on a strong base yoy on a delay in award of

large L1 projects.

Revenue growth to be supported by strong execution in industrials on a

weak base and healthy growth in the power segment.

Improved gross margins on better sales mix and operating leverage benefits

will lead to a 270bps expansion in EBITDA margin.

Consequently, PAT would grow at 71% yoy.

Order book 11,32,956 11,53,300 -1.8% 10,22,000 10.9%

Revenues 74,938 67,799 10.5% 67,052 11.8%

EBITDA 6,223 (332) nm 3,741 66.3%

EBITDA Margin (%) 8.3% -0.5% 879bps 5.6% 272bps

PAT 3,605 (772) nm 2,108 71.0%

EPS (Rs) 1.0 (0.2) nm 0.6 80.3%

CG POWER

Order inflows 18,918 20,010 -5.5% 17,090 10.7% Expect growth in order inflows driven by overseas power systems.

Revenues growth to be driven by strong growth in industrial systems and

overseas power systems segment sales.

Margins to expand by 80bps yoy supported by higher gross margins

Consequently, recurring PAT from continued operations to report a strong

growth on a weak base.

Order book 56,364 54,720 3.0% 45,610 23.6%

Revenues 17,271 16,500 4.7% 15,161 13.9%

EBITDA 1,588 1,624 -2.2% 1,271 24.9%

EBITDA Margin (%) 9.2% 9.8% -65bps 8.4% 81bps

PAT 479 502 -4.6% 327 46.6%

EPS (Rs) 0.8 0.8 -4.6% 0.5 46.6%

Cochin Shipyard

Revenues 6,773 7,994 -15.3% 6,150 10.1% Revenues would be supported by strong healthy growth in the shipbuilding

segment while ship-repair sales will remain flat yoy.

Expect 270bps yoy contraction in margins, as shipbuilding margins will

contract because of unfavourable sales mix.

EBITDA 1,328 1,881 -29.4% 1,372 -3.2%

EBITDA Margin (%) 19.6% 23.5% -393bps 22.3% -270bps

PAT 1,088 1,477 -26.3% 1,138 -4.3%

EPS (Rs) 8.3 10.9 -23.8% 8.4 -1.1%

Cummins

Revenues 15,144 14,869 1.8% 13,547 11.8% Expect healthy growth in revenues on a low base led by both domestic sales

across all segments, as well as exports sales, partly supported by favourable

exchange rates.

Margins to expand 120bps yoy.

EBITDA 2,377 2,509 -5.3% 1,967 20.9%

EBITDA Margin (%) 15.7% 16.9% -118bps 14.5% 118bps

PAT 1,981 2,116 -6.4% 1,722 15.1%

EPS (Rs) 7.1 7.6 -6.4% 6.2 15.1%

Source: PhillipCapital India Research

Page | 13 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations / assumptions

Engineers India

Order inflows 1,392 49,623 -97.2% 1,161 19.9% Revenue growth to be driven by strong execution in the turnkey segment.

EBITDA margins to contract 355bps yoy due to a higher share of low-margin

turnkey revenues, partly offset by improved consultancy margins.

Do not expect any major provision write backs in 3QFY19.

Order book 1,09,598 1,14,640 -4.4% 83,010 32.0%

Revenues 6,434 6,814 -5.6% 4,034 59.5%

EBITDA 885 915 -3.3% 698 26.8%

EBITDA Margin (%) 13.7% 13.4% 32bps 17.3% -355bps

PAT 797 959 -17.0% 665 19.8%

EPS (Rs) 1.3 1.5 -17.0% 1.0 27.7%

GE T&D

Order inflows 9,790 7,235 35.3% 7,832 25.0% Expect good growth in new orders on a weak base yoy.

Muted growth in revenues on a high base yoy due to depleting opening

order book (-24% yoy in 2QFY19).

EBITDA margins to expand 410bps yoy driven by improved gross margins.

Expect 30% yoy growth in PAT led by strong operating performance.

Order book 57,620 62,000 -7.1% 72,000 -20.0%

Revenues 14,170 9,933 42.7% 14,386 -1.5%

EBITDA 1,295 921 40.6% 728 77.9%

EBITDA Margin (%) 9.1% 9.3% -13bps 5.1% 408bps

PAT 764 515 48.4% 589 29.7%

EPS (Rs) 3.0 2.0 48.4% 2.3 29.7%

KEC

Order inflows 45,050 21,700 107.6% 43,540 3.5% Expect muted growth in new orders – announced Rs 45bn orders in 3QFY19.

Likely to miss its FY19 order-inflow guidance.

Revenue to be supported by growth in railways, civil, and solar, as power

T&D to be muted due to slow /deferment of execution in some projects.

EBITDA margins to remain flat yoy.

PAT would decline due to higher in interest costs and effective tax rate.

Order book 1,89,388 1,71,210 10.6% 1,40,180 35.1%

Revenues 26,672 24,085 10.7% 24,049 10.9%

EBITDA 2,702 2,532 6.7% 2,441 10.7%

EBITDA Margin (%) 10.1% 10.5% -38bps 10.2% -2bps

PAT 1,095 963 13.7% 1,118 -2.0%

EPS (Rs) 4.3 3.7 13.7% 4.3 -2.0%

L&T

Order inflows 3,32,180 4,19,210 -20.8% 4,81,300 -31.0% Expect a 30% yoy (-40% ex-services) decline in new orders – announced Rs

214bn of orders in 3Q contributed by hydrocarbons, power T&D, and water.

Revenue to grow at 15% yoy aided by strong growth in IT and financial

services, while its core E&C segment will grow 12%.

EBITDA margins to expand 60bps yoy, led by expansion in IT services and

development projects margins.

Order book 28,11,852 28,11,660 0.0% 27,07,270 3.9%

Revenues 3,31,988 3,20,808 3.5% 2,87,475 15.5%

EBITDA 38,257 37,705 1.5% 31,430 21.7%

EBITDA Margin (%) 11.5% 11.8% -23bps 10.9% 59bps

PAT 16,903 19,357 -12.7% 15,037 12.4%

EPS (Rs) 6.0 6.9 -12.7% 5.4 12.3%

Siemens

Order inflows 35,176 37,187 -5.4% 32,570 8.0% Revenue growth would be driven by strong growth in mobility and digital

factory segments along with healthy growth across all others.

EBITDA margins to contract 50bps yoy due to decline in Power & Gas and

Energy Management segments’ margins.

Order book 1,30,573 1,23,520 5.7% 1,30,905 -0.3%

Revenues 28,123 38,947 -27.8% 24,295 15.8%

EBITDA 3,011 3,741 -19.5% 2,724 10.5%

EBITDA Margin (%) 10.7% 9.6% 110bps 11.2% -51bps

PAT 2,137 2,509 -14.8% 1,905 12.2%

EPS (Rs) 6.0 7.0 -14.8% 5.3 12.2%

Thermax

Order inflows 14,616 13,440 8.7% 14,130 3.4% Expect 24% yoy revenue growth driven by strong growth across all

segments.

EBITDA margins to expand 90bps yoy, driven by operating leverage benefits.

Order book 64,694 64,110 0.9% 55,560 16.4%

Revenues 13,812 14,276 -3.3% 11,170 23.7%

EBITDA 1,307 1,100 18.8% 955 36.9%

EBITDA Margin (%) 9.5% 7.7% 176bps 8.5% 92bps

PAT 867 745 16.4% 586 48.0%

EPS (Rs) 7.7 6.6 16.4% 5.2 48.0%

VA Tech Wabag

Order inflows 2,200 24,620 -91.1% 3,187 -31.0% Order inflows to be weak due to a delay in awarding large domestic orders.

Revenue to decline 18% yoy as large PETRONAS order nearing completion

and execution yet to pick up for new orders won YTD (35% of order book).

EBITDA margins to contract 135bps yoy due to weak execution resulting in

negative operating leverage.

Key monitorable will be progress on the receivables from TSGENCO (post

state election) as well as from APGENCO.

Order book 80,702 85,549 -5.7% 65,210 23.8%

Revenues 7,096 7,520 -5.6% 8,647 -17.9%

EBITDA 524 498 5.3% 757 -30.7%

EBITDA Margin (%) 7.4% 6.6% 77bps 8.8% -136bps

PAT 194 274 -29.3% 288 -32.7%

EPS (Rs) 3.6 5.0 -29.3% 5.3 -32.7%

Voltas

MEP Order inflows 5,943 10,800 -45.0% 5,580 6.5% Revenue growth to be driven by strong execution in MEP (projects) business

along with Engineering Products (on a low base); while UCP (AC business) to

report a moderate growth of c.8% yoy.

Margins to remain flat as impact of contraction in UCP margins (10% vs.

13%) is likely to be neutralize by improved margins in the MEP segment.

PAT growth to be muted due to higher effective tax rate.

MEP Order book 46,109 48,830 -5.6% 48,500 -4.9%

Revenues 15,374 14,214 8.2% 13,747 11.8%

EBITDA 1,276 1,085 17.5% 1,142 11.7%

EBITDA Margin (%) 8.3% 7.6% 66bps 8.3% -1bps

PAT 1,017 1,035 -1.7% 995 2.2%

EPS (Rs) 3.1 3.1 -1.7% 3.0 2.2%

Source: PhillipCapital India Research

Page | 14 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Cement

Earnings estimates

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

ACC

Revenues 37,805 33,640 12% 34,171 11% Volume growth: 7% yoy; 13% qoq.

Realisations: Flattish.

EBITDA/tonne at Rs 657 (37% yoy; 15% qoq).

EBITDA 4,839 3,743 29% 3,317 46%

EBITDA margin (%) 12.8% 11.1% 9.7%

PAT 2,836 2,091 36% 1,715 65%

EPS (Rs) 15.1 11.1 9.1

Ambuja Cements

Revenues 30,486 26,139 17% 27,126 12% Volume growth: 8% yoy; 15% qoq.

Realisations: 1% qoq.

EBITDA/tonne at Rs 782 (-15% yoy; 20% qoq).

EBITDA 4,959 3,582 38% 5,406 -8%

EBITDA margin (%) 16.3% 13.7% 19.9%

PAT 2,765 1,786 55% 3,345 -17%

EPS (Rs) 1.4 0.9 1.7

UltraTech Cement

Revenues 92,783 81,515 14% 80,192 16% Volume growth: 13% yoy; 15% qoq.

Realisations: -1% qoq.

EBITDA/tonne at Rs 731 (-8% yoy; 1% qoq)

EBITDA 13,958 12,263 14% 13,376 4%

EBITDA margin (%) 15.0% 15.0% 16.7%

PAT 4,810 3,768 28% 4,563 5%

EPS (Rs) 17.5 13.7 16.6

Shree Cement

Revenues 27,376 25,866 6% 22,962 Volume growth: 12% yoy; 6% qoq.

Realisations: Flattish qoq.

EBITDA/tonne (blended) at Rs1,110 (12% yoy; 4% qoq).

EBITDA 6,618 6,037 10% 5,293

EBITDA margin (%) 24.2% 23.3% 23.1%

PAT 3,219 3,115 3% 2,930

EPS (Rs) 92 89 84

Dalmia Bharat

Revenues 22,785 21,580 6% 20,905 19% Volume growth: 7% yoy; 8% qoq.

Realisations: -1% qoq.

EBITDA/tonne at Rs893 (-18% yoy; -5% qoq)

EBITDA 3,966 3,900 2% 4,546 25%

EBITDA margin (%) 17.4% 18.1% 21.7%

PAT 45 20 123% 1,181 10%

EPS (Rs) 0.5 0.2 13.3

JK Cements

Revenues 11,702 10,881 8% 11,261 9% Volume growth: flat yoy; -7% qoq.

Realisations: -1% yoy; 1% qoq.

EBITDA/tonne: Rs 659 (-27% yoy; 1% qoq).

EBITDA 1,938 1,572 23% 1,702 -9%

EBITDA margin (%) 16.6% 14.4% 15.1%

PAT 881 647 36% 731 -85%

EPS (Rs) 12.6 9.3 10.4

JK Lakshmi

Revenues 9,337 8,514 10% 8,374 4% Volume growth: 9% yoy and qoq.

Realisations: Flattish

EBITDA/tonne: Rs 475 (6% yoy; 9% qoq).

EBITDA 1,088 916 19% 943 14%

EBITDA margin (%) 11.6% 10.8% 11.3%

PAT 189 78 142% 84 21%

EPS (Rs) 1.6 0.7 0.7

India Cements

Revenues 12,921 13,871 -7% 12,131 11% Volume growth: 7% yoy; -5% qoq.

Realisations: -2% qoq.

EBITDA/tonne at Rs 506 (-18% yoy; flat qoq).

EBITDA 1,472 1,549 -5% 1,673 15%

EBITDA margin (%) 11.4% 11.2% 13.8%

PAT 4 15 -73% 152 125%

EPS (Rs) 0.0 0.0 0.5

Heidelberg Cement

Revenues 4,891 4,795 2% 4,839 7% Volume growth: -6% yoy; 2% qoq.

Realisations: Flattish

EBITDA/tonne: Rs 1000 (61% yoy; 2% qoq).

EBITDA 1,147 1,102 4% 754 -12%

EBITDA margin (%) 23.5% 23.0% 15.6%

PAT 530 501 6% 329 -97%

EPS (Rs) 2.3 2.2 1.5

Page | 15 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Mangalam Cement

Revenues 2,969 2,888 3% 2,920 1% Volume growth: -1% yoy; 2% qoq.

Realisations: 1% qoq

EBITDA/tonne: Rs 310 (185% yoy; 33% qoq).

EBITDA 229 169 35% 81 52%

EBITDA margin (%) 7.7% 5.9% 2.8%

PAT 91 31 192% 27 61%

EPS (Rs) 3.4 1.2 1.0

Sanghi Cement

Revenues 2,466 2,441 1% 2,796 2% Volume growth: -17% yoy; flat qoq.

Realisations: 1% qoq.

EBITDA/tonne: Rs 630 (-24% yoy; 21% qoq).

EBITDA 391 324 21% 618 182%

EBITDA margin (%) 15.9% 13.3% 22.1%

PAT 86 20 340% 322 238%

EPS (Rs) 0.3 0.1 1.5

Star Cement

Revenues 4,063 3,623 12% 3,774 -12% Volume growth: 15% yoy; 1% qoq.

Realisations: flat qoq.

EBITDA/tonne: Rs 1,323 (-48% yoy; 12% qoq).

EBITDA 852 687 24% 1,413 -37%

EBITDA margin (%) 21.0% 19.0% 37.4%

PAT 444 382 16% 914 -73%

EPS (Rs) 1.1 0.9 2.2

Source: Company, PhillipCapital India Research

Page | 16 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Consumer

Earnings Estimates

(Rs mn) Dec-18E Sep-18 qoq (%) Sec-17 yoy (%) Comments

ITC

Volume growth (est.) 3.0 7.0 (4.0) Cigarette volume growth to bounce back (6-7%) due to favourable

base (4% decline).

Cigarette EBIT growth to inch-up to double-digits on operating

efficiencies, price hikes (1%) taken in selected brands. Despite not

taking meaningful price hikes in cigarettes, EBITDA margins to expand

marginally due to positive contribution from FMCG and significant

improvement in cyclical and capex -intensive (hotels, paper)

businesses on an industry upturn.

Net income growth to be lower than EBITDA growth due to higher

taxation.

Revenues 1,07,202 1,08,912 -1.6% 96,726 10.8%

Gross Profit 66,251 66,116 0.2% 60,761 9.0%

Gross margin (%) 61.8 60.7 109bps 62.8 -102bps

EBITDA 43,168 42,060 2.6% 38,891 11.0%

EBITDA margin (%) 40.3 38.6 165bps 40.2 6bps

PAT 30,916 29,547 4.6% 28,202 9.6%

EPS (Rs) 2.5 2.4 4.6% 2.31 9.6%

Hindustan Unilever

Volume growth (est.) 8.0 10.0 11.0 Volume growth to taper to high single digits after seeing four

consecutive quarters of double-digit growth, as GST-related benefit

completes one year.

Gross margin to remain flat yoy due to lower contribution from

personal care because of a late start to winter and RM inflation for a

significant part of the quarter.

EBITDA margin expansion to continue yoy on healthy volume growth

and premiumization trends panning out.

Net income to be lower than EBITDA growth due to higher taxation.

Revenues 94,023 91,380 2.9% 83,230 13.0%

Gross Profit 49,926 47,030 6.2% 44,180 13.0%

Gross margin (%) 53.1 51.5 163bps 53.1 2bps

EBITDA 19,757 20,190 -2.1% 16,800 17.6%

EBITDA margin (%) 21.0 22.1 -108bps 20.2 83bps

PAT 13,916 15,220 -8.6% 11,980 16.2%

EPS (Rs) 6.4 7.0 -8.6% 5.5 16.2%

Dabur India Ltd

Volume growth 10.0 8.1 13.0 Volume growth to just inch-upto 10% as rural has not picked up as

expected

Gross margin to remain almost flat yoy due to higher contribution

from low-margin juice, limited price hikes.

EBITDA margin to remain flat yoy due to: (1) investment behind

creation of distribution infrastructure and higher A&P spends.

Revenues 22,010 21,250 3.6% 19,664 11.9%

Gross Profit 11,335 10,491 8.0% 10,141 11.8%

Gross margin (%) 51.5 49.4 213bps 51.6 -7bps

EBITDA 4,516 4,508 0.2% 4,035 11.9%

EBITDA margin (%) 20.5 21.2 -70bps 20.5 0bps

PAT 3,740 3,766 -0.7% 3,330 12.3%

EPS (Rs) 2.1 2.1 -0.7% 1.9 12.3%

Godrej Cons. Products

Revenues 28,708 26,418 8.7% 26,037 10.3% Domestic business: HI to remain weak due to increase penetration of

incense sticks from the unorganised sector; soaps and hair colours to

see moderate growth due to high base effect.

Reported international growth to look muted despite gradual

recovery in Indonesia, Africa, because of divestment of the UK

business.

Ebitda growth to remain subdued due to high ad intensity.

Gross Profit 15,933 13,860 15.0% 14,774 7.8%

Gross margin (%) 55.5 52.5 303bps 56.7 -124bps

EBITDA 6,168 4,865 26.8% 5,987 3.0%

EBITDA margin (%) 21.5 18.4 307bps 23.0 -151bps

PAT 4,326 3,180 36.0% 4,322 0.1%

EPS (Rs) 6.3 8.5 -25.1% 6.3 0.6%

Marico Industries

Volume growth (est.) 7 6 7 Volume growth of 7% on back of healthy recovery in coconut hair oil.

International business is likely to clock double digit sales growth

Gross margin pressure to ease qoq due to correction in copra price,

price hikes taken in the VAHO portfolio.

EBITDA margin to expand yoy on operating leverage & relatively soft

RM costs.

Revenues 19,817 18,368 7.9% 16,243 22.0%

Gross Profit 8,918 8,081 10.3% 7,556 18.0%

Gross margin (%) 45.0 44.0 100bps 46.5 -152bps

EBITDA 3,743 2,941 27.3% 3,021 23.9%

EBITDA margin (%) 18.9 16.0 288bps 18.6 29bps

PAT 2,651 2,142 23.8% 2,205 20.2%

EPS (Rs) 2.1 1.7 23.8% 1.7 20.2%

Jubilant Foodworks

SSSG 16.0 20.5 17.8 Solid SSS growth to continue as (1) entire festival season falls in 3Q

and (2) supply to railway stations seeing decent traction.

Gross margin to see some pressure due to higher discounting towards

the later part of the festive season.

PAT growth to be above EBITDA due to higher other income.

Revenues 9425 8814 6.9% 7952 18.5%

Gross Profit 7003 6575 6.5% 5926 18.2%

Gross margin (%) 74.3 74.6 -31bps 74.5 -22bps

EBITDA 1673 1475 13.4% 1369 22.2%

EBITDA margin (%) 17.8 16.7 101bps 17.2 54bps

PAT 912 777 17.4% 660 38.1%

EPS (Rs) 7.0 5.9 17.4% 5.0 38.1%

Page | 17 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 qoq (%) Sec-17 yoy (%) Comments

Colgate

Volume growth 8.0 7.0 12.0 Volume growth to inch-up despite high base on: (1) market share

gains in natural portfolio and (2) aggression on driving core product

portfolio.

Gross margin to decline c.70bps yoy due to higher corn (Sorbitol) price

and packaging costs.

Distribution expansion initiatives, higher promotion, RM inflation to

weigh on operating profitability.

Revenues 11,535 11,606 -0.6% 10,270 12.3%

Gross Profit 7,411 7,491 -1.1% 6,672 11.1%

Gross margin (%) 64.3 64.5 -29bps 65.0 -72bps

EBITDA 3,120 3,296 -5.3% 2,838 9.9%

EBITDA margin (%) 27.0 28.4 -135bps 27.6 -59bps

PAT 1,852 1,964 -5.7% 1,707 8.5%

EPS (Rs) 6.8 7.2 -5.7% 6.3 7.7%

Nestle

Volume growth 10.0 0.0 18.0 Innovation in existing categories, entry into new categories and

distribution revamp to drive high single-digit volume growth.

Margin expansion journey to continue on: (1) benign input costs, (2)

cost efficiencies, and (3) operating leverage.

Revenues 29,292 29,220 0% 25896 13.1%

Gross Profit 17,062 17,379 -1.8% 15204 12.2%

Gross margin (%) 58.3 59.5 -123bps 58.7 -46bps

EBITDA 6766 7252 -6.7% 5639 20.0%

EBITDA margin (%) 23.1 24.8 -172bps 21.8 132bps

PAT 3976 4461 -11% 3118 27.5%

EPS (Rs) 41.2 46.3 -10.9% 32.3 27.5%

Glaxo Smithkline Cons

Volume 8.0 13.7 16.0 High single-digit volume growth driven by good traction on sachets

portfolio, high-science based portfolio, and pick-up in Horlicks variants

& Boost

Gross expansion to moderate on inflationary pressure in barley,

packaging costs.

EBITDA margin to see healthy expansion on operating leverage.

Revenues 11437 12720 -10.1% 10382 10.2%

Gross Profit 7971 8861 -10.0% 7159 11.4%

Gross margin (%) 69.7 69.7 4bps 69.0 75bps

EBITDA 2540 3537 -28.2% 2075 22.4%

EBITDA margin (%) 22.2 27.8 -560bps 20.0 222bps

PAT 2045 2755 -25.8% 1637 25.0%

EPS (Rs) 48.6 65.5 -25.8% 38.9 25.0%

Britannia

Volume growth (est.) 8.0 12.0 13.0 High single-digit volume growth on foray into newer categories,

increasing distribution network in weaker areas, and premiumisation.

Gross margin to expand yoy as it has already covered RM at lower

costs.

EBITDA margin to see a c.100bps expansion on account of cost-savings

initiatives.

Revenues 28,459 28,548 0% 25,583 11%

Gross Profit 11,383 11,343 0% 9,838 16%

Gross margin (%) 40.0 39.7 27bps 38.5 154bps

EBITDA 4,730 4,544 4% 3,984 19%

EBITDA margin (%) 16.6 15.9 70bps 15.6 105bps

PAT 3,116 3,030 3% 2,636 18%

EPS (Rs) 26 25 3% 22 18%

Emami

Volume growth (est.) 2.0 (4.0) 6.0 Volume growth to be dented due to a late start to the winter season

and continued pressure on the wholesale channel.

Gross margin to remain under pressure due to higher mentha oil

prices, LLP, and packaging costs.

Negative operating leverage to weigh on operating profitability.

Net income to be lower than EBITDA growth despite lower interest

costs due to higher taxation.

Revenues 8,011 6,280 28% 7,552 6%

Gross Profit 5,528 4,308 28% 5,357 3%

Gross margin (%) 69.0 68.6 40bps 70.9 -193bps

EBITDA 2,611 1,894 38% 2,647 -1%

EBITDA margin (%) 32.6 30.2 244bps 35.0 -245bps

PAT 1,386 827 68% 1,472 -6%

EPS (Rs) 3.0 1.8 67% 3.2 -6%

Asian Paints

Volume growth (est.) 15.0 12.5 6.0 Mid-teen volume growth due to: (1) festival season falling entirely in

3Q vs. split in the base quarter, and (2) market share gains in the

distemper segment.

Gross margin pressure to ease qoq, despite spiralling Tio2 price,

because of annualized weighted average price hike of 5%.

Benefits of healthy volume growth to be negated by start -up costs

because of the Mysuru plant starting operations.

Revenues 51,446 46,391 11% 42,605 21%

Gross Profit 21,093 18,467 14% 17,995 17%

Gross margin (%) 41.0 39.8 119bps 42.2 -124bps

EBITDA 10,782 7,842 38% 8,912 21%

EBITDA margin (%) 21.0 16.9 406bps 20.9 4bps

PAT 6,870 4,928 39% 5,546 24%

EPS (Rs) 7.2 5.1 39% 5.8 24%

Page | 18 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 qoq (%) Sec-17 yoy (%) Comments

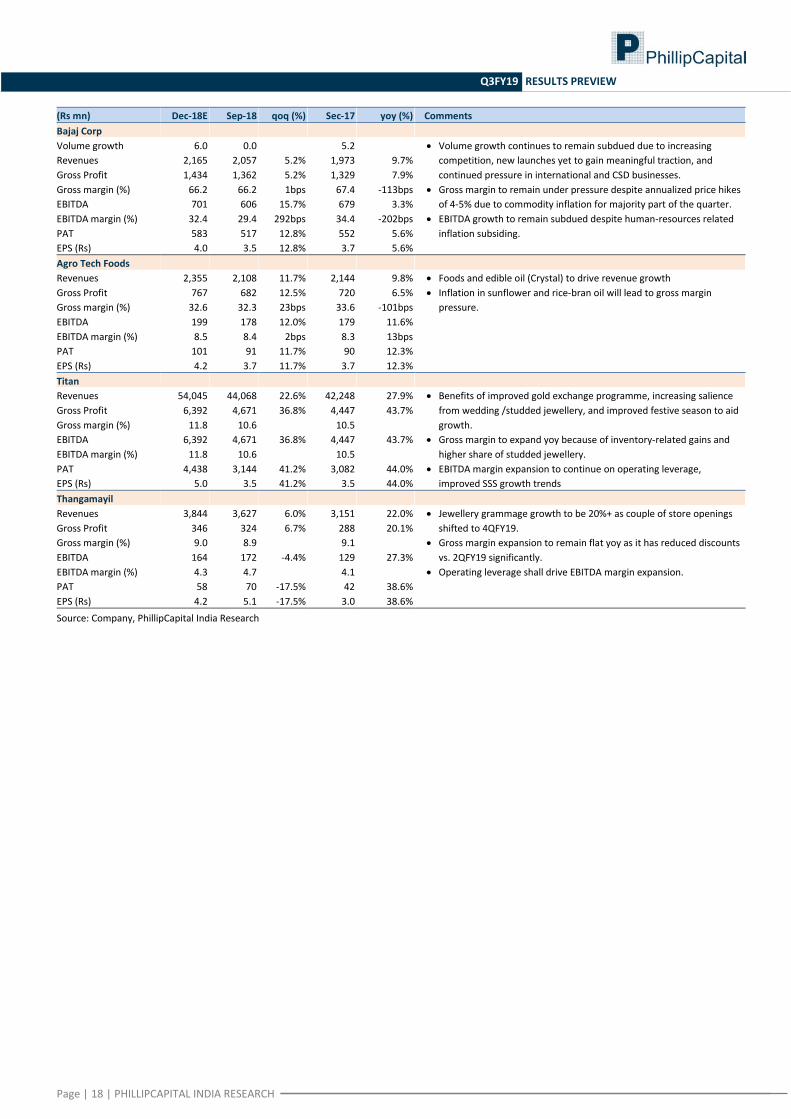

Bajaj Corp

Volume growth 6.0 0.0 5.2 Volume growth continues to remain subdued due to increasing

competition, new launches yet to gain meaningful traction, and

continued pressure in international and CSD businesses.

Gross margin to remain under pressure despite annualized price hikes

of 4-5% due to commodity inflation for majority part of the quarter.

EBITDA growth to remain subdued despite human-resources related

inflation subsiding.

Revenues 2,165 2,057 5.2% 1,973 9.7%

Gross Profit 1,434 1,362 5.2% 1,329 7.9%

Gross margin (%) 66.2 66.2 1bps 67.4 -113bps

EBITDA 701 606 15.7% 679 3.3%

EBITDA margin (%) 32.4 29.4 292bps 34.4 -202bps

PAT 583 517 12.8% 552 5.6%

EPS (Rs) 4.0 3.5 12.8% 3.7 5.6%

Agro Tech Foods

Revenues 2,355 2,108 11.7% 2,144 9.8% Foods and edible oil (Crystal) to drive revenue growth

Inflation in sunflower and rice-bran oil will lead to gross margin

pressure.

Gross Profit 767 682 12.5% 720 6.5%

Gross margin (%) 32.6 32.3 23bps 33.6 -101bps

EBITDA 199 178 12.0% 179 11.6%

EBITDA margin (%) 8.5 8.4 2bps 8.3 13bps

PAT 101 91 11.7% 90 12.3%

EPS (Rs) 4.2 3.7 11.7% 3.7 12.3%

Titan

Revenues 54,045 44,068 22.6% 42,248 27.9% Benefits of improved gold exchange programme, increasing salience

from wedding /studded jewellery, and improved festive season to aid

growth.

Gross margin to expand yoy because of inventory-related gains and

higher share of studded jewellery.

EBITDA margin expansion to continue on operating leverage,

improved SSS growth trends

Gross Profit 6,392 4,671 36.8% 4,447 43.7%

Gross margin (%) 11.8 10.6 10.5

EBITDA 6,392 4,671 36.8% 4,447 43.7%

EBITDA margin (%) 11.8 10.6 10.5

PAT 4,438 3,144 41.2% 3,082 44.0%

EPS (Rs) 5.0 3.5 41.2% 3.5 44.0%

Thangamayil

Revenues 3,844 3,627 6.0% 3,151 22.0% Jewellery grammage growth to be 20%+ as couple of store openings

shifted to 4QFY19.

Gross margin expansion to remain flat yoy as it has reduced discounts

vs. 2QFY19 significantly.

Operating leverage shall drive EBITDA margin expansion.

Gross Profit 346 324 6.7% 288 20.1%

Gross margin (%) 9.0 8.9 9.1

EBITDA 164 172 -4.4% 129 27.3%

EBITDA margin (%) 4.3 4.7 4.1

PAT 58 70 -17.5% 42 38.6%

EPS (Rs) 4.2 5.1 -17.5% 3.0 38.6%

Source: Company, PhillipCapital India Research

Page | 19 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

IT Services

Earnings estimates – Large-cap companies

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Tata Consultancy

US$ Revenues ($mn) 5,284 5,215 1.3% 4,787 10.4% CC revenue growth of 1.7% and negative CC impact of 40bps.

Margins to expand 30bps qoq due to INR depreciation and operational

efficiencies.

Watch: Commentary on client budgets, Diligenta, and outlook of BFSI

and retail.

Revenues 380,460 368,540 3.2% 309,040 23.1%

EBIT 101,878 97,710 4.3% 77,810 30.9%

EBIT margin (%) 26.8 26.5 30bps 25.2 160bps

PAT 81,560 79,050 3.2% 65,310 24.9%

EPS (Rs) 21.7 21.1 3.2% 17.1 27.2%

Infosys

US$ Revenues ($mn) 2,951 2,921 1.0% 2,755 7.1% CC revenue growth of 1.5% and negative CC impact of 50bps.

Margins to decline 20bps despite INR depreciation due to front-ended

variable bonus to curb attrition.

To maintain revenue growth guidance for FY19 with a brighter outlook

on dealflow.

Revenues 212,491 206,090 3.1% 177,940 19.4%

EBIT 50,100 48,940 2.4% 43,190 16.0%

EBIT margin (%) 23.6 23.7 -20bps 24.3 -70bps

PAT 41,511 41,100 1.0% 36,970 12.3%

EPS (Rs) 9.6 9.5 1.0% 8.1 17.6%

Wipro

$ Revenue – IT ($mn) 2,043 2,041 0.1% 2,013 1.5% IT services CC revenue growth of +2.5% (adjusting for India

PSU/Government business carve-out) - near the higher-end of adjusted

guidance of 1% to 3% and negative cross currency impact of 80bps.

Contribution from Alight Solutions to be US$ 25mn (incl. in CC growth)

EBIT margins to expand 340bps qoq due to the absence of settlement

impact with National Grid in the last quarter.

We expect 1-3% qoq growth guidance for 4QFY19

Watch: Commentary on BFSI, healthcare, E&U, and retail.

Revenues 147,832 145,410 1.7% 136,690 8.2%

EBIT 25,988 20,616 26.1% 19,775 31.4%

EBIT margin (%) 17.6 14.2 340bps 14.5 310bps

PAT 23,304 18,869 23.5% 19,361 20.4%

EPS (Rs) 5.2 4.2 23.3% 4.4 18.5%

HCL Technologies

US$ Revenues ($mn) 2,161 2,099 3.0% 1,988 8.8% CC growth of 3.7% (organic CC growth of 2.7%) and negative CC impact

of 70bps.

H&D acquisitions to provide US$ 21mn for the quarter.

Margins to expand 40bps qoq due to INR depreciation and better

growth in high-margin IP business.

Outlook, esp on IMS and ERD businesses, to be keenly watched – also

any details on IBM deals and the latest acquisition of H&D in Germany.

Revenues 155,628 148,610 4.7% 128,080 21.5%

EBIT 31,616 29,660 6.6% 25,090 26.0%

EBIT margin (%) 20.3 20.0 40bps 19.6 70bps

PAT 25,483 25,400 0.3% 21,940 16.1%

EPS (Rs) 18.8 18.2 3.3% 15.7 19.3%

Tech Mahindra

US$ Revenues ($mn) 1,243 1,218 2.0% 1,209 2.8% CC revenue growth of +2.5% and negative CC impact of 50bps.

Growth will be driven by the Telecom segment (+4.5% qoq) while

Enterprise will grow at a modest 1% due to furloughs.

Margins to expand 30bps qoq mainly due to INR depreciation.

Watch: Commentary on Telecom (5G spend).

Revenues 89,505 86,298 3.7% 77,760 15.1%

EBIT 13,997 13,243 5.7% 9,904 41.3%

EBIT margin (%) 15.6 15.3 30bps 12.7 290bps

PAT 11,382 10,559 7.8% 9,244 23.1%

EPS (Rs) 12.9 11.9 8.2% 10.7 20.0%

Source: Company, PhillipCapital India Research

Page | 20 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Earnings estimates – Mid-cap companies

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

L&T Infotech

US$ Revenues ($mn) 335 329 2.0% 294 14.2% CC revenue growth of 2.7% and negative CC impact of 70bps.

Margins to decline 60bps qoq due to the investments.

Commentary on BFSI and top clients growth to be keenly watched.

Revenues 24,124 23,312 3.5% 18,838 28.1%

EBIT 4,430 4,423 0.2% 2,813 57.5%

EBIT margin (%) 18.4 19.0 -60bps 14.9 340bps

PAT 3,639 4,003 -9.1% 2,828 28.7%

EPS (Rs) 21.3 23.5 -9.1% 16.5 29.4%

L&T Tech

US$ Revenues ($mn) 180 177 1.5% 151 19.1% CC revenue growth of 2.2% and negative CC impact of 50bps.

Margins to expand 40bps due to INR depreciation and operational

efficiencies.

Management commentary on future margin trajectory and

monetization of IP platforms will be important.

Revenues 12,952 12,661 2.3% 9,691 33.6%

EBIT 2,123 2,019 5.1% 1,340 58.4%

EBIT margin (%) 16.4 15.9 40bps 13.8 260bps

PAT 1,735 1,911 -9.2% 1,263 37.4%

EPS (Rs) 17.1 18.9 -9.6% 12.4 37.1%

MindTree

US$ Revenues ($mn) 250 246 1.4% 214 16.6% CC revenue growth of 2.1% and negative cross currency impact of

70bps.

Margins to expand 30bps qoq due to INR depreciation.

Commentary on digital growth and TCV to be keenly watched.

Revenues 17,989 17,554 2.5% 13,777 30.6%

EBIT 2,414 2,296 5.1% 1,655 45.9%

EBIT margin (%) 13.4 13.1 30bps 12.0 140bps

PAT 1,961 2,063 -5.0% 1,415 38.6%

EPS (Rs) 12.0 12.6 -5.0% 8.6 38.6%

Cyient

US$ Revenues ($mn) 169 169 -0.1% 152 11.0% IT services CC revenue growth of +1.9% qoq and negative cross

currency impact of 50bps.

DLM to decline 10% qoq, due to seasonality.

Margins to expand 100bps due to INR depreciation and lower

investments.

Watch: Guidance for FY19, outlook on DLM, and new deal wins.

Revenues 12,143 11,870 2.3% 9,834 23.5%

EBIT 1,488 1,339 11.2% 1,157 28.6%

EBIT margin (%) 12.3 11.3 100bps 11.8 50bps

PAT 1,342 1,267 5.9% 876 53.2%

EPS (Rs) 11.9 11.3 5.9% 7.8 53.2%

Persistent Systems

US$ Revenues ($mn) 123 118 3.7% 123 0.1% USD revenue growth of +3.7% qoq

Margins to expand 60bps due to INR depreciation.

Watch: Revenue growth outlook from the IBM-Watson deal.

Revenues 8,831 8,356 5.7% 7,919 11.5%

EBIT 1,151 1,038 10.9% 983 17.1%

EBIT margin (%) 13.0 12.4 60bps 12.4 60bps

PAT 967 881 9.7% 917 5.5%

EPS (Rs) 12.1 11.0 9.7% 11.5 5.5%

NIIT Tech

US$ Revenues ($mn) 135 131 2.8% 117 15.3% USD revenue growth of +2.8%, driven by strong growth in insurance,

travel, and digital segments.

Margins to expand 100bps driven by INR depreciation and operational

efficiencies.

Commentary on new order intake and strategy to be keenly watched.

Revenues 9,686 9,074 6.7% 7,565 28.0%

EBIT 1,497 1,315 13.9% 985 52.0%

EBIT margin (%) 15.5 14.5 100bps 13.0 240bps

PAT 1,201 1,118 7.4% 757 58.6%

EPS (Rs) 19.6 18.3 7.4% 12.4 58.6%

Intellect Design

US$ Revenues ($mn) 54 54 -0.6% 42 29.0% USD revenue to remain flat qoq, after strong growth in the last quarter.

Margins to expand 40bps due to INR depreciation and lower R&D cost.

Watch: Outlook on new deal wins and DSO improvement.

Revenues 3,886 3,804 2.2% 2,707 43.5%

EBIT 297 275 8.0% 96 211.1%

EBIT margin (%) 7.7 7.2 40bps 3.5 410bps

PAT 301 315 -4.5% 122 147.1%

EPS (Rs) 2.3 2.4 -4.5% 1.0 135.6%

Majesco

US$ Revenues ($mn) 35 34 2.8% 32 10.2% USD revenue growth of 2.8%, driven by organic growth and IBM IP

deal.

Margins to contract 230bps qoq, after strong expansion in the last

quarter.

Watch: Outlook on cloud segment traction. Management commentary

on IBM IP deal and new deal wins.

Revenues 2,520 2,425 3.9% 2,073 21.6%

EBIT 181 230 -21.6% 51 251.5%

EBIT margin (%) 7.2 9.5 -230bps 2.5 470bps

PAT 139 264 -47.2% -90 NA

EPS (Rs) 4.9 9.4 -47.2% -3.8 NA

Source: Company, PhillipCapital India Research

Page | 21 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Infrastructure

Earnings estimates

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

NCC

Revenues 27,758 31,048 -10.6% 18,507 50.0% Strong yoy growth in topline, driven by execution and low base.

Progress on FY19 revenue growth guidance of 45% will be keenly

watched.

Margins to remain stable in the 11.0-11.5% range - yoy decline due to

high base last year (GST impact).

Strong yoy earnings growth due to topline growth.

EBITDA 3,145 3,651 -13.8% 2,551 23.3%

EBITDA margin (%) 11.3% 11.8% -43 13.8% -245

PAT 1,303 1,257 3.7% 1,004 29.8%

EPS (Rs) 2.17 2.09 3.7% 1.81 20.1%

KNR Construction

Revenues 4,603 4,163 10.6% 4,332 6.3% Weak orderbook at the beginning of the quarter will lead to muted

growth in topline.

Margins to remain stable in the 15-17% range – yoy margins were

exceptionally high due to closure of few projects.

Yoy decline in earnings due to higher tax rate; 80IA benefits going away.

EBITDA 799 831 -3.9% 984 -18.8%

EBITDA margin (%) 17.4% 20.0% -261 22.7% -535

PAT 374 353 5.8% 483 -22.7%

EPS (Rs) 2.66 3.20 -17.0% 4.67 -43.1%

PNC Infratech

Revenues 6,127 5,586 9.7% 4,725 29.7% Strong topline growth with execution of 7 of the new/stuck projects.

Margins to remain stable in 13.5 14.0%.

Yoy decline in earnings due to higher tax rate, with 80IA benefit going

away.

EBITDA 824 746 10.5% 663 24.4%

EBITDA margin (%) 13.5% 13.4% 10 14.0% -57

PAT 401 351 14.2% 432 -7.2%

EPS (Rs) 1.56 1.37 14.2% 3.63 -56.9%

ITD Cementation

Revenues 6,758 6,204 8.9% 5,749 17.6% We expect decent topline growth, in line with last two quarters and the

annual run-rate expectations.

Margins expected to stabilize now, with the impact of legacy low-margin

orders moving out of the orderbook complete.

Strong earnings growth due to better execution and low base yoy.

EBITDA 791 781 1.2% 786 0.7%

EBITDA margin (%) 11.7% 12.6% -89 13.7% -196

PAT 303 274 10.8% 177 71.6%

EPS (Rs) 1.76 1.59 10.8% 1.14 55.0%

J Kumar Infra

Revenues 6,132 5,147 19.1% 4,572 34.1% Decent topline growth after strong performance in the last quarter,

which came after a string of disappointing quarters.

Margins to remain stable in 16-17% range.

Earnings to decline yoy due to exceptionally high margins in 2QFY18,

and higher interest/depreciation this quarter.

EBITDA 1,012 910 11.2% 776 30.3%

EBITDA margin (%) 16.5% 17.7% -117 17.0% -48

PAT 361 354 1.9% 329 9.5%

EPS (Rs) 4.77 4.68 1.9% 4.35 9.5%

Ahluwalia Contracts

Revenues 4,940 4,392 12.5% 3,611 36.8% Decent topline growth, driven by order won in 2HFY18 and 1HFY19.

Margins to remain stable in the range of 13-14%.

Strong yoy earnings growth - driven by topline growth and lower

interest expense (exceptionally high in 3QFY18).

EBITDA 655 574 13.9% 625 4.8%

EBITDA margin (%) 13.3% 13.1% 17 17.3% -405

PAT 374 312 20.2% 292 28.4%

EPS (Rs) 5.59 4.65 20.2% 4.35 28.4%

Adani Ports & SEZ

Revenues 28,097 26,080 7.7% 26,889 4.5% Decent 10% yoy growth in cargo volumes, driven by growth in container

and ramp-up at Dhamra and Katupalli.

Muted topline yoy growth - as 3QFY18 had exceptional SEZ income.

Port margins are likely to remain stable.

Updates on the FY19 cargo and revenue guidance will be keenly sought

– along with outlook for FY20.

EBITDA 18,438 17,035 8.2% 17,842 3.3%

EBITDA margin (%) 65.6% 65.3% 30 66.4% -74

PAT 9,636 6,142 56.9% 9,941 -3.1%

EPS (Rs) 4.65 2.97 56.9% 4.80 -3.1%

IRB Infrastructure

Revenues 16,491 14,854 11.0% 13,417 22.9% Toll collection to report strong yoy growth due to a ramp-up in

Rajasthan projects.

Like-for-like toll collection to report muted 5-7% growth

EPC revenues to report muted yoy growth due to weak executable

orderbook in the quarter.

Earnings to remain flat yoy, due to higher interest and depreciation.

EBITDA 7,225 6,701 7.8% 6,303 14.6%

EBITDA margin (%) 43.8% 45.1% -130 47.0% -317

PAT 2,065 1,729 19.4% 2,073 -0.4%

EPS (Rs) 5.87 4.92 19.4% 5.90 -0.4%

Page | 22 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Ashoka Buildcon

Revenues 8,339 7,644 9.1% 6,589 26.6% Strong topline growth - with execution picking up on HAM projects.

Margins to remain stable in 12-13% range.

Strong yoy earnings driven by topline growth.

EBITDA 1,098 1,037 5.9% 796 38.0%

EBITDA margin (%) 13.2% 13.6% -40 12.1% 109

PAT 669 621 7.7% 520 28.7%

EPS (Rs) 3.57 3.32 7.7% 2.78 28.7%

Sadbhav Engineering

Revenues 9,590 6,906 38.9% 8,394 14.3% Decent topline growth driven by execution on new HAM projects.

Margins to remain stable in 11-12% range.

Muted yoy growth in earnings due to higher tax rate, with 80IA benefit

going away.

EBITDA 1,163 833 39.6% 1,056 10.1%

EBITDA margin (%) 12.1% 12.1% 6 12.6% -46

PAT 687 383 79.3% 618 11.1%

EPS (Rs) 4.00 2.23 79.3% 3.60 11.1%

Source: Company, PhillipCapital India Research

Page | 23 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

Midcaps

Earnings estimates

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Concor

Revenues 16,350 17,223 -5.1% 14,537 12.5% Volume growth of 12% yoy – both in exim and domestic.

Yoy margin improvement with pricing and volume growth.

Assumed tax @ 28% in 3Q; SIES other income at c.Rs 900mn.

EBITDA 3,581 4,042 -11.4% 2,597 37.9%

EBITDA margin (%) 21.9 23.5 17.9

PAT 2,980 3,361 -11.3% 2,891 3.1%

EPS (Rs) 6.1 6.9 -11.3% 5.9 3.1%

Praj Inds.

Revenues 2,850 2,510 13.5% 2,483 14.8% Orderbook of Rs 9bn, recovery in execution.

Operating leverage due to employee cost. EBITDA 213 169 25.4% 168 26.6%

EBITDA margin (%) 7.5 6.7 6.8

PAT 139 121 15.5% 74 87.2%

EPS (Rs) 0.8 0.7 15.5% 0.4 87.2%

Pennar Inds.

Revenues 5,250 5,182 1.3% 4,149 26.5% Growth in railways, tubes; recovery in PEBS with OB of Rs 4.2bn.

Margins impact due to PEBS, raw material inflation.

Assumed tax provision of 30%. EBITDA 385 322 19.3% 435 -11.6%

EBITDA margin (%) 7.3 6.2 10.5

PAT 119 122 -2.7% 133 -10.2%

EPS (Rs) 1.0 1.0 -2.7% 1.1 -10.2%

Allcargo

Revenues 17,390 17,373 0.1% 14,799 17.5% Growth in MTO, recovery in P&E and CFS.

Impact of DPD on CFS and lower profitability MTO with growth in FCL. EBITDA 1,141 1,249 -8.6% 1,141 0.0%

EBITDA margin (%) 6.6 7.2 7.7

PAT 517 618 -16.4% 348 48.7%

EPS (Rs) 2.1 2.5 -16.4% 1.4 48.7%

Sintex Plastic

Revenues 13,044 11,722 11.3% 13,327 -2.1% Decline in Prefab; CM to see marginal growth.

Impact of prefab business yoy. EBITDA 1,809 1,663 8.8% 1,849 -2.2%

EBITDA margin (%) 13.9 14.2 13.9

PAT 403 404 -0.1% 518 -22.2%

EPS (Rs) 0.6 0.6 -0.1% 0.9 -25.6%

KDDL

Revenues 1,635 1,565 4.5% 1,422 15.0% 15% yoy recovery in retail, 14% yoy growth in mgf.

High base effect in retail margins, revenue mix in mgf. EBITDA 148 134 10.4% 179 -17.2%

EBITDA margin (%) 9.0 8.6 12.6

PAT 48 53 -9.5% 92 -47.5%

EPS (Rs) 4.5 4.9 -9.5% 8.5 -47.5%

VRL Logistics

Revenues 5,333 5,170 3.2% 4,893 9.0% Good transport growth of 13% yoy.

Increase in fuel cost and seasonal benefit in the bus segment. EBITDA 628 541 16.2% 618 1.6%

EBITDA margin (%) 11.8 10.5 12.6

PAT 253 206 22.7% 252 0.4%

EPS (Rs) 2.8 2.3 23.1% 2.8 0.4%

Gateway Distriparks

Revenues 878 885 -0.8% 804 9.2% Marginal recovery in container volume; capacity addition at

Krishnapattnam.

DPD, pressure on CFS profitability. EBITDA 148 147 0.7% 160 -7.3%

EBITDA margin (%) 16.9 16.6 19.9

PAT 58 55 5.0% 102 -43.8%

EPS (Rs) 0.5 0.5 5.0% 0.9 -43.8%

Navkar

Revenues 1,150 1,121 2.6% 1,065 8.0% Recovery in Vapi volume + weakness at JNPT.

Operating impact due Vapi volumes. EBITDA 352 272 29.4% 376 -6.4%

EBITDA margin (%) 30.6 24.3 35.3

PAT 116 33 250.9% 235 -50.5%

EPS (Rs) 0.8 0.2 250.9% 1.6 -50.5%

Page | 24 | PHILLIPCAPITAL INDIA RESEARCH

Q3FY19 RESULTS PREVIEW

(Rs mn) Dec-18E Sep-18 qoq (%) Dec-17 yoy (%) Key expectations

Indo Count Industries

Revenues 4,917 4,860 1.2% 4,600 6.9% Volumes up 8% yoy to 15.4mn mtr; higher in-house yarn consumption.

Yoy impact of lower export incentive and pressure on realization. EBITDA 583 498 17.2% 693 -15.9%

EBITDA margin (%) 11.9 10.2 15.1

PAT 273 218 25.5% 364 -25.0%

EPS (Rs) 1.4 1.1 25.5% 1.8 -25.0%

Havells

Revenues 22,719 21,910 3.7% 19,658 15.6% Havells S.A. to report a growth of 16% yoy, majorly driven by the CD

segment. We expect margin of 13.6% in 3QFY19.

In Lloyd, we expect revenue growth of 15% (channel stocking in ACs and

strong growth in LED driven by a festive season). EBITDA margin of 8.7%.

EBITDA 2,922 2,625 11.3% 2,622 11.4%

EBITDA margin (%) 12.9 12.0 13.3

PAT 1,956 1,786 9.5% 1,734 12.8%

EPS (Rs) 3.1 2.9 9.5% 2.8 12.8%