instructional materials for benford’s law: conceptual ...mysite.du.edu/~hkim162/pdf/instructional...

TRANSCRIPT

1

Instructional Materials for Benford’s Law: Conceptual

Background and Guided Software Instruction with

Supporting Teaching Notes

Abstract

Developing teaching materials suitable for audit professionals is an important step towards

increasing the understanding and usage of the Benford’s Law feature within Generalized Audit

Software. This teaching material provides both a conceptual background about Benford’s Law

and guided instructions about using the Benford’s Law feature of ACL to perform fraud

detection procedures. The associated teaching notes augment the instructional material with post

tests and an assignment covering Benford’s Law with accounting data.

Keywords: Generalized audit software; ACL; Benford’s Law; Digital Analysis

Introduction

Generalized audit software (GAS) has the potential to increase the efficiency of auditors in

performing many audit processes. However the usage of GAS is still relatively low, especially

the advanced features of GAS (i.e. Benford’s Law), in part because auditors perceived that

advanced features are useful but not easy to use (Kim, Mannino, and Nieschwietz 2009).

Advanced feature training can increase not only auditors’ perceptions of usefulness and ease of

use, but also the usage of advanced features of GAS among audit professionals (Kim, Mannino,

and Nieschwietz 2011).

Benford’s Law, developed by Frank Benford, is based on Benford’s findings that low first digits

occurred more frequently in most sets of data (Benford 1938). It has been implemented in GAS

(i.e. ACL and IDEA) as an advanced analytic tool to detect potential anomalies. Students can

apply this feature to most accounting data except invented, contrived, or manipulated numbers.

Novices with Benford’s Law, either audit professionals or students majoring in accounting, will

2

learn the background knowledge of Benford’s Law and how to use the Benford’s Law feature of

ACL to find fraudulent data through the materials provided in the appendices.

The teaching materials provide a short lecture on Benford’s Law, an exercise with guided

instructions, and a case-based assignment to apply the Benford’s Law feature of ACL. The

lecture on the conceptual background of Benford’s Law provides the foundation for students to

effectively use the Benford’s Law feature of ACL. In the initial exercise (Appendix 1), students

should follow all directions from the exercise to practice the Benford’s Law feature of ACL with

expense reimbursement data1. In the case-based assignment (Appendix 2), they will practice

what they learned from the exercise to answer the questions provided in the assignment.

These instructional materials were used by professional internal auditors in the data collection of

a study focusing on the impact of advanced feature training for Generalized Audit Software (Kim,

Mannino, and Nieschwietz, 2011). Fifty internal auditors used the lecture, guided exercise,

quizzes, and assignment. Before conducting the study, the material was developed through pilot

testing conducted using a master’s level advanced auditing class and several internal auditors.

Teaching notes for lecture, exercise, and assignment

Summary of the lecture

A web-based lecture is produced by the authors to improve the understanding of theory behind

the advanced analytic feature of GAS. Students will gain an understanding of the conceptual

knowledge of Benford’s Law through the lecture. This lecture covers the definition, history,

examples, applications, and exceptions of Benford’s Law. The lecture is available on the

1 Data file from “Auditing: A Business Risk Approach; 6th edition; South-western; 2008; L. E. Rittenberg, B. J.

Schwieger, K. Johnston.”

3

YouTube2 and the lecture slides are also available at the public link

3. It will take approximately

15 minutes.

Summary of the exercise

The exercise is a guided self-tutorial asking students to find suspicious employees among 1000

expense reimbursement records. They should follow the numbered steps to learn how to perform

digital analysis with expense reimbursement data. This exercise covers downloading a data file,

creating a project, importing a table, performing a first digit analysis, graphing the output of the

first digit analysis, performing a first two digits analysis, graphing the output of the first two

digits analysis, changing the format of data to ASCII to summarize the data, and summarizing

the data file to identify employees having suspicious transactions. The original excel file4 is

available on the Cengage Learning website without cost, but we ask students download the data

file from the link in the exercise.

Summary of the assignment

The assignment is a case-based practice of Benford’s Law with invoice data. Students will be

given simple instructions to find suspicious vendors among 2000 records in the invoice data of

Wake County. This case-based assignment deepens the understanding of students how Benford’s

Law can be applied in real situations. The original excel file5 is available on the EZ-R Stats

website without cost, but we ask students to download the file from the link in the assignment

because the file we provide is already prepared for the assigned audit tasks.

2 http://www.youtube.com/watch?v=D-JNc8RXT6w, http://www.youtube.com/watch?v=zH6CCg9Rhhk (April,

2011) 3 http://ouray.ucdenver.edu/~h1kim/BenfordsLaw/ConceptualBackground/ConceptualBackground.ppt (April,

2011) 4

http://www.thomsonedu.com/accounting/book_content/0324375581_rittenberg/biltrite_data_files/Expense

Reimbursements.xls (April 2011)

5 http://www.ezrstats.com/CS/CS_Wake_County.htm (April, 2011)

4

Teaching objectives and target audience

Through the teaching material, we are intended for students to acquire the knowledge and skills

to

Understand the conceptual background of Benford’s Law

Understand how to perform the Benford’s Law feature of ACL with accounting data.

Learn how to graph the output of Benford’s analysis in ACL.

Understand how to interpret the result of Benford’s analysis.

The target audience for the lecture, exercise, and the assignment are novices with Benford’s Law,

either audit professionals or accounting students who could become auditors. In order to

complete these exercise and assignment, they need to have basic knowledge of computers and

the functionalities of ACL6

Teaching approach

We suggest instructors to present the web-based lecture on Benford’s Law first because most

advanced features of GAS (i.e. Benford’s Law) require an understanding of theories behind the

software. Then instructors can ask students to follow the instructions of the exercise to

familiarize themselves with the Benford’s Law feature of ACL. Once students understand how to

use the Benford’s Law feature of ACL, instructors can give students the assignment to practice

Benford’s Law with invoice data. If students already know the theoretical background of

Benford’s Law, instructors can skip the lecture part. We suggest four test questions to ensure

students to understand the conceptual part of Benford’s Law.

6 Import, Age, Classify, Duplicates/Gaps/Sequence, Export, Extract, Filters, Join Files, Sampling, Sort, Statistics,

Stratify, Summarize, Verify, etc.

5

Lecture quiz

1. What is Benford’s Law?

a. The primary mechanism for retrieving information from a database.

b. A form of digital analysis based on the findings that low first digits occur more

frequently in most sets of data.

c. A statistical technique whether there are differences between the average value, or

mean, across several population groups.

d. The application of audit procedures to less than 100% of the items within a

population to obtain audit evidence about a particular characteristic of the population.

2. What is the typical usage of Benford’s Law?

a. Predict membership of an individual observation in a predefined group.

b. Discover a mathematical relationship between two or more variables using a set of

individual observations.

c. Detect potential fraud, possible errors, manipulated biases, and costly processing

inefficiencies or other irregularities.

d. Calculate and compare ratios which are derived from the information in a company’s

financial statements or from other non-financial information.

3. Which data typically conform to Benford’s Law?

a. NYSE stock quotes

b. Invoice numbers

c. Account payable amounts

d. Hourly wage rates

4. What procedure is not recommended to identify fraudulent data?

a. Make sure if data conform to Benford’s Law.

b. Examine the negative peaks if actual proportion exceeds Benford’s Law-predicted

proportion.

c. Verify if there is any abnormal level of duplication for a certain digit.

d. Check the amounts just below a limit, the rounded amounts, and repeated digit

patterns through digit tests.

Lecture quiz answers

The answers to lecture questions are as follows.

6

1. What is Benford's Law? b

2. What is the usage for Benford's Law? c

3. Which data typically conform to Benford's Law? c

4. What procedure is not recommended to identify fraudulent data? b

Analysis of Exercise

An abnormal level of items is processed at transactions started with 49 and 24. EMP_NO 265

has 10 transactions right below the approval level of $5,000. These transactions need detail

review.

The answers to lecture questions are as follows.

1. How many transactions are started with 24? 71 records

2. How many transactions are between 2,400 and 2,500? 22 records

3. When you summarize the transactions between 2,400 and 2,500 by EMP_NO, are there any

suspicious employees? No

Analysis of Assignment

All transactions are under $2,500. Vendor A11 accounts for almost 50% of the transactions. As

the fiscal year end approached, A11 submitted lots of invoices. Many invoices were paid to

vendor A11 in the same invoice date and same invoice number.

The answers to lecture questions are as follows.

1. How many transactions were started with 16? 146 records.

2. How many transactions are between 1,600 and 1,700? 22 records

3. When you summarize the transactions between 1,600 and 1,700 by EMP_NO, are there any

suspicious vendors? A11

4. How many transactions were started with 17? 125 records

7

5. How many transactions are between 1,700 and 1,800? 112 records

6. When you summarize the transactions between 1,700 and 1,800 by EMP_NO, are there any

suspicious vendors? A11

Concluding remarks

Theses instructional materials are designed for instructors to present the Benford’s Law feature

of ACL with theoretical lecture and practical cases. Students can enhance their knowledge of

Benford’s Law through the web-based conceptual lecture and have hand-on practices with

Benford’s Law using ACL. After completing the instructional materials, students will improve

their understanding of Benford’s Law in theory, and be more proficient in using the software so

that the usage of advanced features of GAS in practice will be increased, improving their audit

efficiency.

References

Benford, F. (1938) The law of anomalous numbers. Proceedings of the American Philosophical

Society, March, 551–572

Kim, H., Mannino, M., and Nieschwietz, R. J. (2009) “Information Technology Acceptance in

the Internal Audit Profession: Impact of Technology Features and Technology Complexity,”

International Journal of Accounting Information Systems 10, 4 (December 2009), 214-228.

Kim, H., Mannino, M., and Nieschwietz, R. J. “Technology Training of Internal Auditors:

Impact of Advanced Features of Generalized Audit Software,” CSIS Program Working Paper,

University of Colorado Denver, 2011.

8

Appendix 1: ACL Exercise with Expense Reimbursement

Data

Learning Objectives

After this exercise, you should have acquired the knowledge and skills to

Understand how to perform Benford’s Law in ACL with accounting data.

Learn how to graph the output of Benford’s analysis in ACL.

Understand how to interpret the result of Benford’s Law.

Conventions Used in the Exercise

To facilitate your reading of this tutorial, some conventions are useful. Table 1 lists the

conventions along with examples.

Term Convention Examples

Data files, typed input Italics ExpenseReimbursements.xls

Icons, commands, equations Bold File | New | Project

Field names FULL CAPS AMOUNT Table 1 Convention Used

Time estimation: Approximately 20 minutes

Assume that you are auditing the expense reimbursement records of ABC Company for 2007.

Company policy requires receipts for expenses greater than $25 for the travel, entertainment, and

meal reimbursements. All reimbursements over $5,000 require management approval separately.

Use Benford’s Law in ACL to identify employees who is circumventing this policy.

ExpenseReinbursements.xls contains 1,000 transaction records with document number, employee

number, and amount.

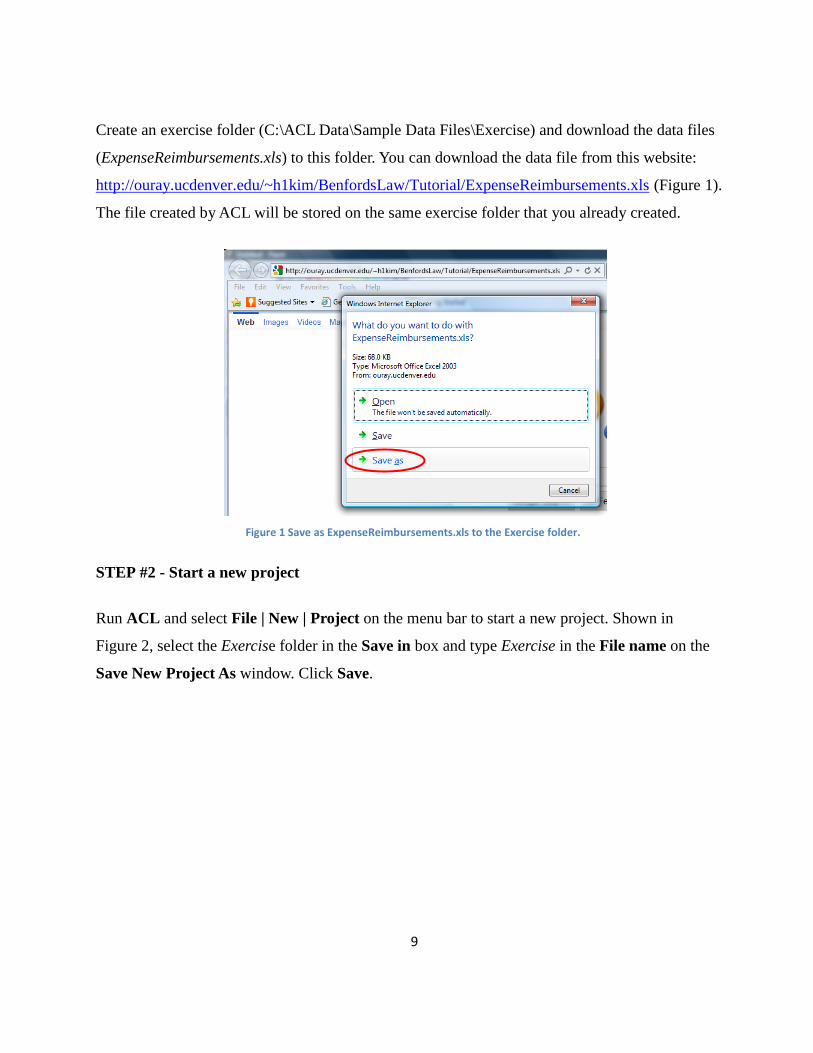

STEP #1 - Obtaining the data files from the website and loading onto the PC

9

Create an exercise folder (C:\ACL Data\Sample Data Files\Exercise) and download the data files

(ExpenseReimbursements.xls) to this folder. You can download the data file from this website:

http://ouray.ucdenver.edu/~h1kim/BenfordsLaw/Tutorial/ExpenseReimbursements.xls (Figure 1).

The file created by ACL will be stored on the same exercise folder that you already created.

Figure 1 Save as ExpenseReimbursements.xls to the Exercise folder.

STEP #2 - Start a new project

Run ACL and select File | New | Project on the menu bar to start a new project. Shown in

Figure 2, select the Exercise folder in the Save in box and type Exercise in the File name on the

Save New Project As window. Click Save.

10

Figure 2 Create the Exercise project in the Exercise folder.

STEP #3 – Import a table

To import a file, click Next on the Data Definition Wizard window. Click Next on the Select

Data Source window. Shown in Figure 3, select ExpenseReimbursements.xls on the Select File

to Define window. Click Open.

Figure 3 Select ExpenseReimbursements.xls to import.

11

Click Next three times. Give the file a new name – ExpenseReimbursements. Click Save | Finish,

and OK on the Table ‘Untitled’ changed, save as window. If you successfully import the

expense reimbursements table, you can see the table shown in Figure 4.

Figure 4 Correctly imported Expense Reimbursement data file into ACL.

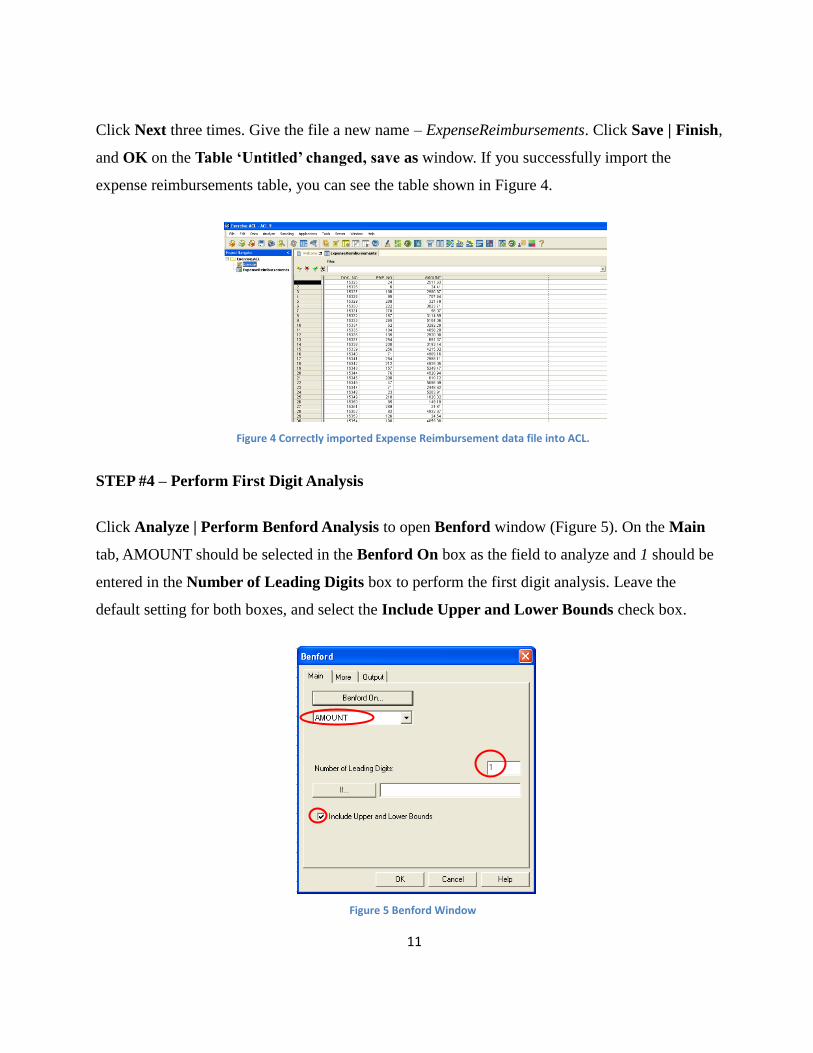

STEP #4 – Perform First Digit Analysis

Click Analyze | Perform Benford Analysis to open Benford window (Figure 5). On the Main

tab, AMOUNT should be selected in the Benford On box as the field to analyze and 1 should be

entered in the Number of Leading Digits box to perform the first digit analysis. Leave the

default setting for both boxes, and select the Include Upper and Lower Bounds check box.

Figure 5 Benford Window

12

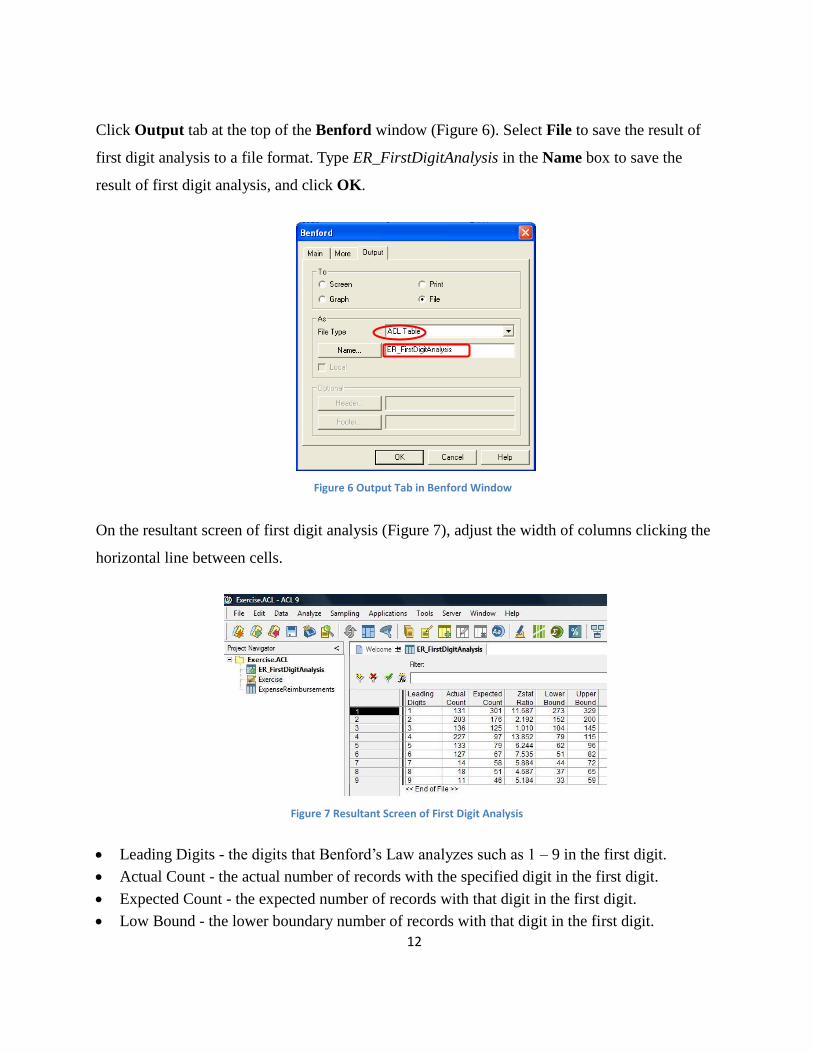

Click Output tab at the top of the Benford window (Figure 6). Select File to save the result of

first digit analysis to a file format. Type ER_FirstDigitAnalysis in the Name box to save the

result of first digit analysis, and click OK.

Figure 6 Output Tab in Benford Window

On the resultant screen of first digit analysis (Figure 7), adjust the width of columns clicking the

horizontal line between cells.

Figure 7 Resultant Screen of First Digit Analysis

Leading Digits - the digits that Benford’s Law analyzes such as 1 – 9 in the first digit.

Actual Count - the actual number of records with the specified digit in the first digit.

Expected Count - the expected number of records with that digit in the first digit.

Low Bound - the lower boundary number of records with that digit in the first digit.

13

Upper Bound - the upper boundary number of records with that digit in the first digit.

Zstat Ratio - the probability of the deviation between the actual count and the expected count

of the digit.

Any Zstat Ratio greater than 2.58 would indicate a 99% chance of deviation between actual

count and expected count, a very rare occurrence. You will focus on the largest Zstat Ratio to

find unusual transactions processed in the data file. Right click the title bar of the ZSTAT

RATIO column, and click Quick Sort Descending. Actual and expected counts of first digit are

most significantly different at digit 4 with Zstat Ratio of 13.852. Double click the

ExpenseReimbursement in the left pane of Project Navigator to go back to the original data file.

STEP #5 – Graph the output of First Digit Analysis

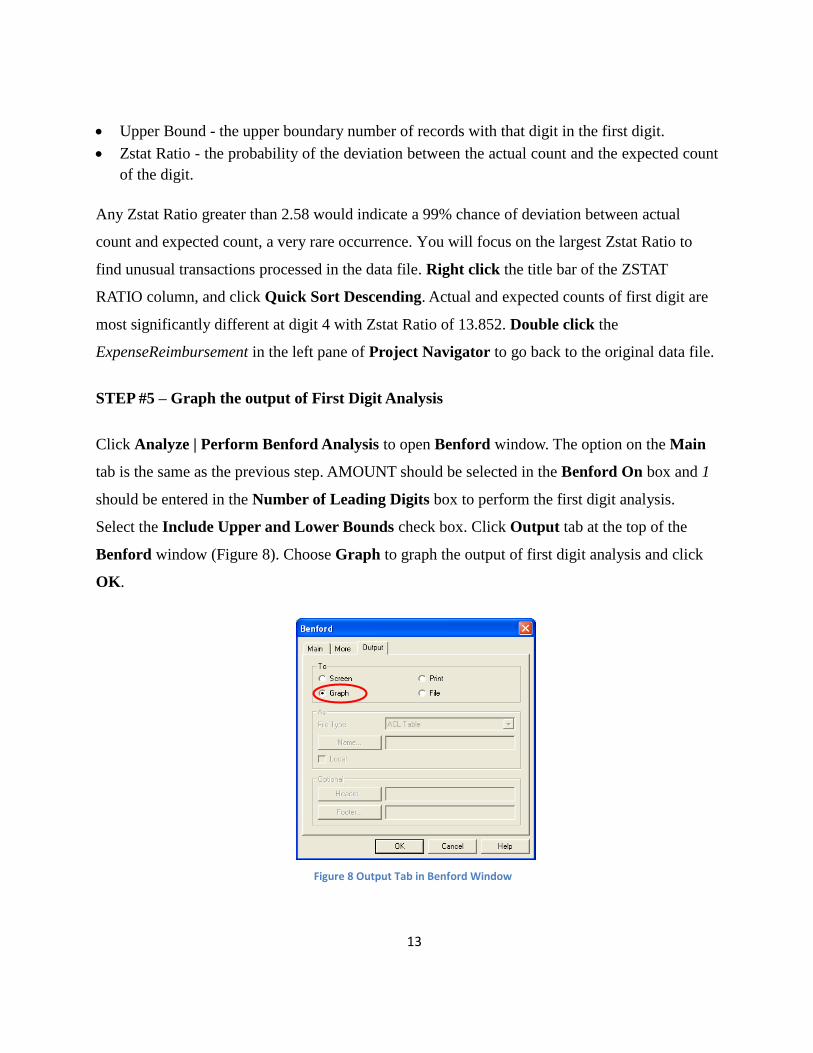

Click Analyze | Perform Benford Analysis to open Benford window. The option on the Main

tab is the same as the previous step. AMOUNT should be selected in the Benford On box and 1

should be entered in the Number of Leading Digits box to perform the first digit analysis.

Select the Include Upper and Lower Bounds check box. Click Output tab at the top of the

Benford window (Figure 8). Choose Graph to graph the output of first digit analysis and click

OK.

Figure 8 Output Tab in Benford Window

14

Figure 9 is the first digit graph of the Expense Reimbursements data file. It shows the actual,

expected, lower bound, upper bound numbers of the digits appeared in the first digit. The digit 4

is the highest positive spike indicating an abnormal level of items being processed at digit 4 in

the first digit, which is just below the additional approval level of $5,000.

Figure 9 First Digit Graph

Double click the bar of digit 4 to see the records started with digit 4. You can see (LEADING

(AMOUNT, 1) = “4”) in the Filter box. Click Analyze | Total Fields to see the total number of

records started with digit 4. On the Total window (Figure 10), click DOC_NO and then click

OK.

Figure 10 Click “DOC_NO” to see the number of records.

227 transactions are started with digit 4. Close the Total window. Double click

ExpenseReimbursements in the left pane of Project Navigator to go back to the records started

15

with digit 4. Delete (LEADING (AMOUNT, 1) = “4”) in the Filter box to see all records in the

original data file.

STEP #6 – Change the format of data

To find suspicious employees in the expense reimbursement data file, you need to summary data

by employee number. So the data type of employee number should be changed into the ASCII

format. Click Edit | Table Layout to open the table layout window. Double click EMP_NO on

the Edit Fields/Expressions tab (Figure 12).

Figure 11 Change the data format of EMP_NO to ASCII to summarize by EMP_NO.

Shown in Figure 12, change Type into ASCII. Click the Accept Entry icon and then click the

Close icon on the Table Layout window. This step can be done immediately after the data file is

imported.

16

Figure 12 Edit Fields/Expressions Window

STEP #7 – Perform First Two Digits Analysis

The first two digits analysis is a high level test and it has a same process to the first digit analysis

except the setup for the number of leading digits. Click Analyze | Perform Benford Analysis to

open Benford window. Shown in Figure 13, AMOUNT should be selected in the Benford On

box and 2 should be entered in the Number of Leading Digits box on the Main tab to perform

the first two digits analysis. Select the Include Upper and Lower Bounds check box.

Figure 13 Set up for first two digits analysis.

17

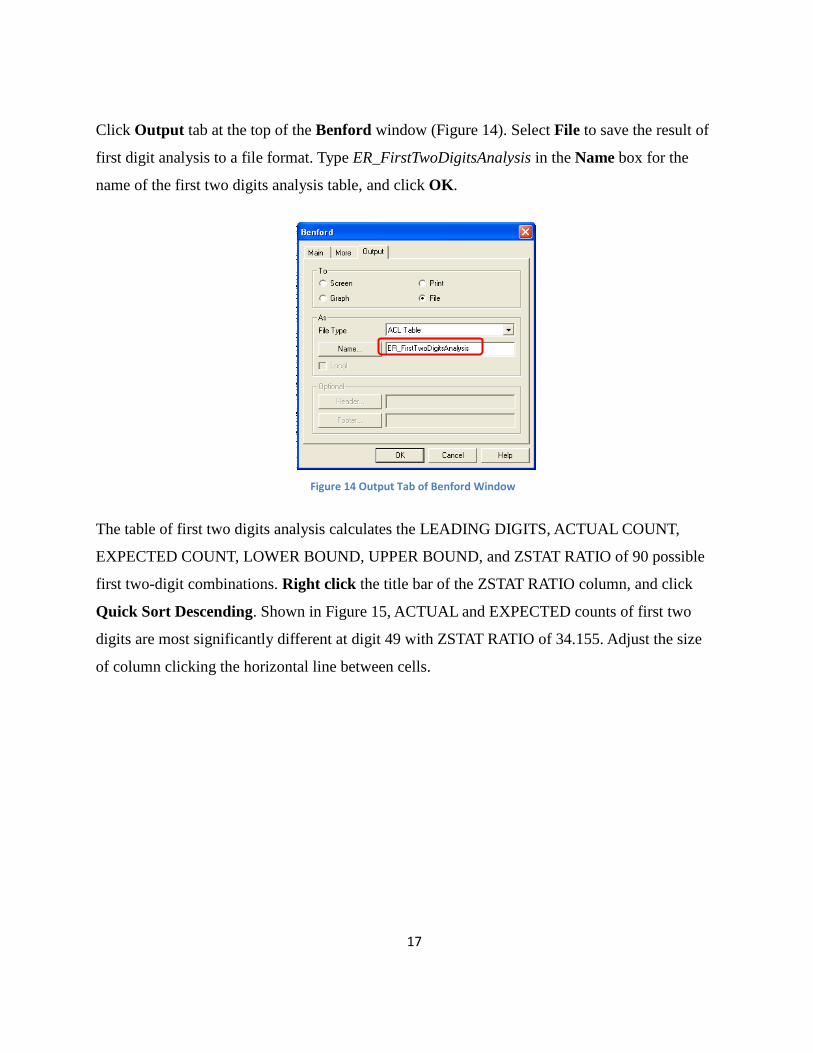

Click Output tab at the top of the Benford window (Figure 14). Select File to save the result of

first digit analysis to a file format. Type ER_FirstTwoDigitsAnalysis in the Name box for the

name of the first two digits analysis table, and click OK.

Figure 14 Output Tab of Benford Window

The table of first two digits analysis calculates the LEADING DIGITS, ACTUAL COUNT,

EXPECTED COUNT, LOWER BOUND, UPPER BOUND, and ZSTAT RATIO of 90 possible

first two-digit combinations. Right click the title bar of the ZSTAT RATIO column, and click

Quick Sort Descending. Shown in Figure 15, ACTUAL and EXPECTED counts of first two

digits are most significantly different at digit 49 with ZSTAT RATIO of 34.155. Adjust the size

of column clicking the horizontal line between cells.

18

Figure 15 Actual and expected counts are most significantly different at digit 49.

Double click ExpenseReimbursements in the left pane of Project Navigator to go back to the

original file.

STEP #8 – Graph the output of First Two Digits Analysis

Click Analyze | Perform Benford Analysis to open Benford window. On the Main tab,

AMOUNT should be selected in the Benford On box and 2 should be entered in the Number of

Leading Digits box to graph the first two digits analysis. Select the Include Upper and Lower

Bounds check box. Click Output tab at the top of the Benford window. Choose Graph to create

the first two digits graph and click OK.

19

Figure 16 First Two Digits Graph

Shown in Figure 16, 49 that caused the spike in digit 4 in the first digit graph is clearly visible in

the first two digits graph. Double click the 49 spike to display the records started with 49. You

can see (LEADING (AMOUNT, 2) = “49”) in the Filter box. Click Analyze | Total Fields to see

the total number of records started with digit 49. On the Total window, click DOC_NO and then

click OK. Transactions start with digit 49 is 110. Close the Total Window. Right click the title

bar of the AMOUNT column and click Quick Sort Ascending to index data in the ascending

order. 109 transactions except for 1 transaction ($497.94) are just below the additional approval

level of $5,000. Shown in Figure 17, type AND ((AMOUNT >= 4900) AND (AMOUNT < 5000))

in the Filter box and click Set Filter icon to extract the transactions between $4,900 and $5,000.

Figure 17 Type this additional function to extract the records between $4,900 and $5,000.

Double click this bar to see the records started with 49.

20

STEP #9 – Summarize the data file by EMP_NO

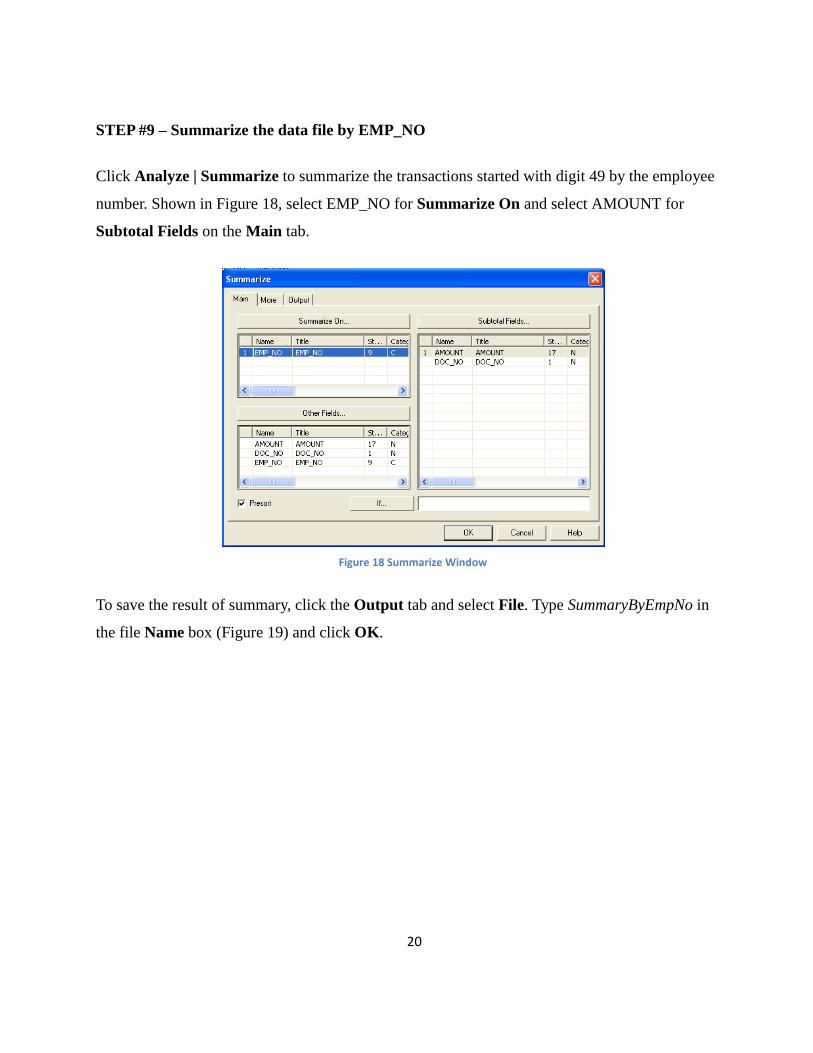

Click Analyze | Summarize to summarize the transactions started with digit 49 by the employee

number. Shown in Figure 18, select EMP_NO for Summarize On and select AMOUNT for

Subtotal Fields on the Main tab.

Figure 18 Summarize Window

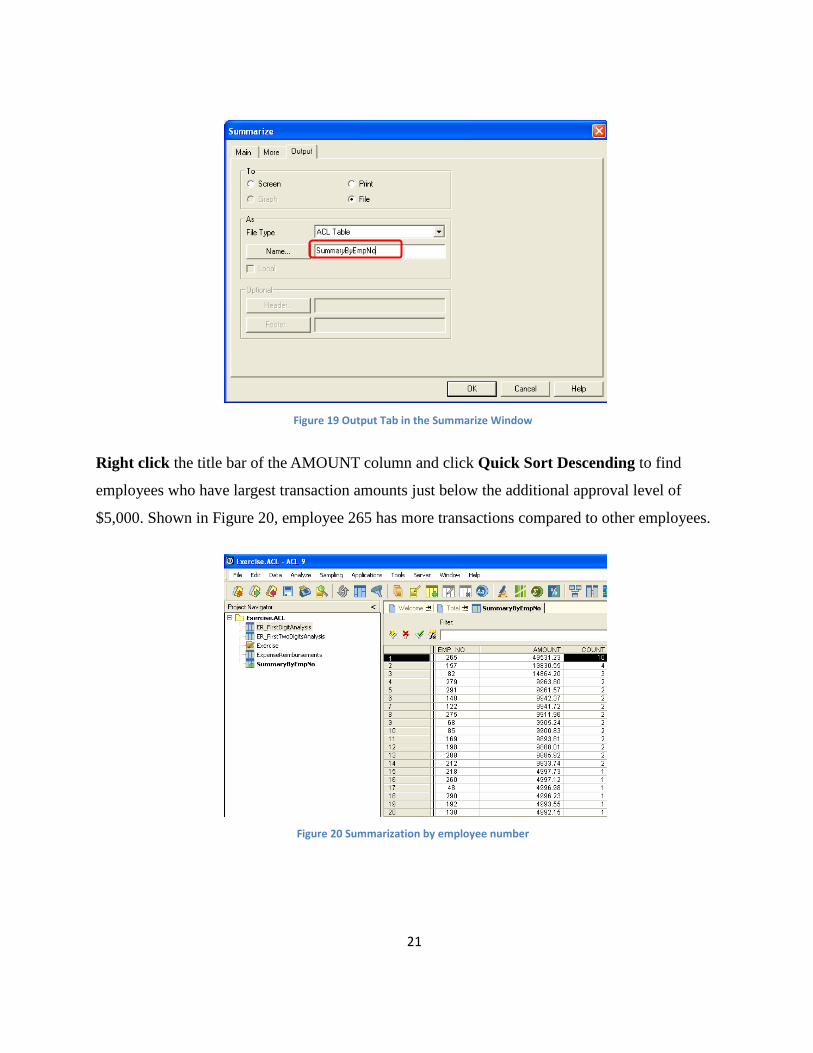

To save the result of summary, click the Output tab and select File. Type SummaryByEmpNo in

the file Name box (Figure 19) and click OK.

21

Figure 19 Output Tab in the Summarize Window

Right click the title bar of the AMOUNT column and click Quick Sort Descending to find

employees who have largest transaction amounts just below the additional approval level of

$5,000. Shown in Figure 20, employee 265 has more transactions compared to other employees.

Figure 20 Summarization by employee number

22

The first three digits analysis is a highly focused test to obtain a smaller sample, but the number

of records produced from the first two digits analysis is already small. In this exercise, you do

not need to perform the first three digits analysis.

Questions

In the first two digits analysis, 24 is another positive spike.

1. How many transactions are started with 24?

2. How many transactions are between 2,400 and 2,500?

3. When you summarize the transactions between 2,400 and 2,500 by EMP_NO, are there any

suspicious employees?

23

Appendix 2: Assignment about the Wake County Fraud Case

Time estimation: Approximately 15 minutes

Objectives: Wake County School employees in the school transportation department and Barnes

Motors & Parts Co. submitted fraudulent invoices for school bus and automotive parts. Much of

the money was used by the employees to buy personal items such as automobiles, campers, golf

carts and plasma-screen televisions. The county policy requires that each transaction was limited

to $2,500. The fiscal year end of this county is June 10, 2006. Assume that you are auditing the

invoices between January 11, 2006 and September 3, 2007 for Wake County School. Use

Benford’s Law in ACL to identify suspicious vendors having exceptional transactions.

WakeCounty.xls contains 2,000 transaction records with vendor identifier, invoice number,

invoice date, and amount.

1. Create the Assignment folder and download WakeCounty.xls into this folder from this website:

http://ouray.ucdenver.edu/~h1kim/BenfordsLaw/Tutorial/WakeCounty.xls

2. Create a project named Assignment. Import the WakeCounty.xls file into the project and name

the table as WakeCounty.

3. Perform the first digit analysis and save the file as FirstDigitAnalysis. Sort the result of first

digit analysis by the ZSTAT RATIO column in descending order.

4. Graph the output of the first digit analysis and double click the highest positive spike.

5. Perform the first two digits analysis and save the file as FirstTwoDigitsAnalysis. Sort the

result of first two digits analysis by the ZSTAT RATIO column in descending order.

6. Graph the output of the first two digits analysis and double click the highest positive spike.

7. Summarize the result of Step 6 by VENDOR and list any suspicious vendors processed the

unusual levels of transactions.

Questions

In the first two digits analysis, 16 and 17 were highest positive spikes.

24

1. How many transactions were started with 16?

2. How many transactions are between 1,600 and 1,700?

3. When you summarize the transactions between 1,600 and 1,700 by EMP_NO, are there any

suspicious vendors?

4. How many transactions were started with 17?

5. How many transactions are between 1,700 and 1,800?

6. When you summarize the transactions between 1,700 and 1,800 by EMP_NO, are there any

suspicious vendors? A11