insurance in central europe - efma - home · pdf fileinsurance in central europe on the path...

TRANSCRIPT

Insurance in Central Europe

ON THE PATH TOWARDS FULL AUTOMATION OF THE BACK OFFICE

1

CONTENT

PREFACE

EXECUTIVE SUMMARY

CHAPTER I – INTRODUCTION: OBJECTIVE, INSIGHT SOURCES AND FRAMEWORK OF ANALYSIS

CHAPTER II – DIGITALIZATION AND THE BACK OFFICE: THE MEANS OF SURVIVAL AND DIFFERENTIATION

CHAPTER III – THE APPROACH TO DIGITALIZATION: FIRST DEFINE THE GOAL AND THEN SET THE PRIORITIES

CHAPTER IV – CURRENT STATUS: STEP-BY-STEP DIGITALIZATION OF FIELD PROCESSES AND PARTIAL DIGITALIZATION OF BACK OFFICE PROCESSING

CHAPTER V – TARGET PICTURE: FIELD PROCESSES ARE HIGHLY DIGITAL AND THE BACK OFFICE PROCESSING IS AUTOMATED AND PAPERLESS

SUMMARY AND RECOMMENDATIONS

METHODOLOGY AND SCOPE OF THE STUDY

ABOUT US

3

5

9

13

19

27

35

43

46

47

2

3

PREFACE

Frigyes Schannen

Managing Partner

CEE Financial Services

Roland Berger

Vincent Bastid

Secretary General

Efma

The expectations of consumers have increased as a result of tech-native companies, which define

the new digital standard for other industries as well. Unsurprisingly, insurance companies also need

to join and shape the trend of digitalization in order to maintain their business. Digitalization can

come in many different forms such as social network based sales, behavior based targeting or use of

connected devices. To realize any of these, significant adaptions have to happen in the back office.

It is important to see, that most of these developments in the back office can be extremely time and

capital consuming. Therefore, a comprehensive strategy is required with clearly defined priorities.

This year Roland Berger and Efma conducted a holistic study to capture the status and ambition

level of insurers in back office digitalization. More specifically, the aim of this study is to assess the

current status of back office digitalization, identify the target picture of Central European insurers

and provide a set of KPIs that could serve as a reference point along the digitalization path. Our

envisioned aim is to provide you with an ideal roadmap.

In this booklet, we summarized the key findings of our assessment supported by the consolidated

view of the insurance industry in Central Europe. The report contains insights on the approach

insurance companies are pursuing, in order to adapt to the disruptive force of digitalization. It is

structured into six chapters:

I. Introduction: Objective, insight sources and framework of analysis

II. Defining digitalization for the back office: The means of survival and differentiation

III. The approach to digitalization: First define the goal and then set the priorities

IV. Current status: Step-by-step digitalization of field processes and partial digitalization of back

office processing

V. Target picture: Field processes are highly digital and the back office processing is automated

and paperless

VI. Summary and outlook

In order to get a crisp picture, we have carried out interviews with the executives (CEOs, Board

Members, mainly COOs) of leading insurers in the Central European region. The insights gathered

during these interviews have been combined with the knowledge from our primary research on

regional customer insights, which we have collected by interviewing about 1,700 consumers.

We are convinced this report and the insights will support you in developing, refining and

challenging your approach to digitalization overall, but especially your attitude towards digitalization

of the back office.

Yours faithfully,

4

5

EXECUTIVE SUMMARY

Digitalization of consumer behavior is driven by tech-native companies.

Improving the operating efficiency and the client experience are two main motivators of digitalization.

CUSTOMER EXPECTATIONS ARE INCREASING

Tech-native companies are setting the pace for the digitalization of consumer behavior

by providing never before seen options to consumers and cherishing them with all the

benefits of ICT developments. As a result, consumers expect the same service level

from other companies as well, even from the ones in completely different industries.

Consumers demand omni-channel access to their products/services. This results in

a headache for many industries. The integration of online and offline channels into

one system, providing the same experience at any time, is by itself a difficult task.

New generations are demanding more and more online channels, while the older

generations are staying either with the well-known brick-and-mortar channels or they

are going hybrid! Hybrid clients are the ones switching between the online and offline

channels along their customer journey. A generational shift is on the horizon, which

will boost the online sales of insurance products. The emergence of generations Y and

Z is irreversible and due to their digital nativity they have higher digital expectations

towards insurers, than the current clients.

Compared to these client expectations, insurers are lagging behind in many areas.

As an example, an average client in Central Europe expects to spend 12 minutes to

purchase an MTPL and to fill-in seven data points. Most of the insurers cannot match

this expectation and ask the consumers to spend double, sometimes triple this time

and effort. Some insurers have already reacted to this question and offer fast quoting

tools. These tools drastically reduce the time and effort needed from the consumers by

the integration of external databases.

BACK OFFICE IS A KEY ENABLER IN MATCHING THE DIGITAL

EXPECTATIONS OF CLIENTS

The aforementioned trends create a challenging cocktail for insurers. Adding new

capabilities to match the digital requirements of the consumers will necessitate large

changes in the back office with significant capital investments and time required.

Therefore, the back office will be the key enabler in this and the digitalization of

back office processes is essential for insurers to survive and differentiate themselves.

This digital transformation requires a comprehensive approach with a clearly defined

purpose and priorities.

APPROACH OF INSURERS TO DIGITALIZATION AND SETTING

THE PRIORITIES

Insurers define digitalization as the integration and usage of information technology

with the aim to (63%) improve operating efficiency, (37%) lift the client experience,

(21%) strengthen data management capabilities and (11%) to tap on new

opportunities, in order to reach a competitive advantage.

The approach of insurers largely differs. Only 58% of insurers capture digitalization in

a separate strategy document or handle it as a strategic priority. 21% of insurers have

a comprehensive approach to digitalization with an appointed Chief Digital Officer as

6

Back office processes are digitally underdeveloped and leave large room for improvement.

EXECUTIVE SUMMARY

the sole owner at senior management level. Additionally, 37% of insurers handle this

topic with strategic importance, mostly captured within their business (60%), IT (30%)

or operations strategy (10%).

Insurers define their priorities with the aim to improve the skills which ensure them

a competitive advantage. The majority of insurers aim to shorten the servicing time,

improve the service quality and reach lower cost positions. In terms of the processes,

insurers see a significant digitalization potential in claims, document management and

policy management. More importantly, many insurers have ongoing/planned projects

in these fields. Furthermore, there are interesting patterns in the priority setting of

insurers according to their size and focus.

BACK OFFICE PROCESS ARE DIGITALLY UNDERDEVELOPED

We have split the back office processes into two parts, the field processes and the

processes within the back office. Both segments are underdeveloped and show

significant improvement potential. Underwriting, policy management and claims field

processes are unevenly digitalized. Underwriting was clearly more in focus of insurers,

given the higher level of digitalization compared to the other two processes.

The underwriting field process is mostly supported by the front end system across

all steps. However, a new tool is on the rise – online and offline quoting. These tools

have a much shorter time to market and require less effort to develop. Therefore,

an increasing number of insurers are using them. On the other hand, paper based

processes are still in place. A large share of this is driven by external channels as they

often hesitate to connect to the system of the insurers.

Field processes of policy management are paper based at most of the insurance

companies. This part of the business was less in focus of insurers and there are major

improvement areas. Online forms and self-service portals are not in place at many

insurance companies – i.e. leaving their customers only the option to communicate

with their insurer using paper. In some institutions the call center is taking the lead

in receiving these notification calls from the clients and directly recoding them in the

front end.

Claims field processes are somewhat more digitalized than policy management. Still,

it leaves a major improvement area for most of the insurers. This means, processes are

mostly paper based without an integral support of a mobile claim front end system.

The actual processing of cases within the back office is developed at a medium level.

We have assessed the performance of insurers along the degree of paperless, level

of automation and process dependence. Only 52% of insurers have a paperless back

office – they are mostly large insurers. STP (Straight-Through-Processing) rates vary

between the processes. The highest rates are in underwriting and the lowest rates are

in claims. In general, large insurers have higher STP rates. In process dependencies, it

is especially the life insurers who are limiting the potential speed of digital solutions, in

order to filter out fraudulent cases.

7

By 2018, back office processes will become increasingly paperless, more automated and significantly faster.

EXECUTIVE SUMMARY

LARGE AMBITIONS BY 2018

Insurers have large ambitions to digitalize the processes in the field and within the

back office. Field processes will undergo a major improvement for underwriting, policy

management and claims as well. Though, some commonalities are foreseeable.

Starting with the client data collection and form fill-out, front end and different

online tools will take the lead in enabling the customers and intermediaries a digital

communication with the insurers. In client signature collection, two directional

developments will take place. One is the massive deployment of digital signature

solutions, e.g. biometric signatures. The other one is the avoidance of requiring the

client signature. This will be driven by legal simplification of products and processes

all together. In digitalization of underlying documents, the on-spot digitalization

capabilities will be deployed. This will enable the intermediaries and the claim adjuster

seamless digitalization of all documents as an integral part of the client servicing

process. The majority of data and documents will be sent to the back office only in

a digital format, while the papers necessary for archiving will follow an independent

path.

Processing of cases within the back office will also significantly improve in terms

of automation, paperless and turnaround time. The standard level in automation

will be 65-85%. Still, claims will be the least automated area. In terms of paperless

processing, insurers plan to reach 70-80% across all cases. This will especially be an

area of improvement for the small insurers. Faster response time will be crucial in the

upcoming years. Therefore, insurers set ambitious turnaround targets of 1.5-5 days

depending on the complexity of the cases.

8

9

CHAPTER I

Introduction: Objective, insight sources and framework of analysis

10 INTRODUCTION

OBJECTIVE AND INSIGHT SOURCES

While most insurance companies focus mainly on the front office perspective of

digitalization, in order to have instant customer involvement, we believe that the back

office offers great opportunities for digitalization. The reason for this is that most of the

customer interaction, products and services flow through the back office and they are

highly dependent on it. It forms a base for the products and their proper marketing,

sales and servicing. This is further upheld by all support functions and systems, which

are the operative enablers of any digitalization effort an insurer might attempt.

The purpose of the study is to develop guiding principles and cornerstone KPIs for the

back office digitalization of insurers. More precisely, the objective of the study is to

provide regional insight into the motivation for digitalization, as well as the current

status and ambition level for back office digitalization. To provide insurers with the

possibility of comparing themselves to their peers, we have collected and compiled a

thorough list of KPIs and recommendations.

This study builds on the insights of two different surveys. One executive survey

conducted with top executives of Central European insurance companies and

one market survey conducted with consumers in Central Europe on their digital

expectations towards insurers.

EXECUTIVE SURVEY

We have conducted around 30 interviews with executives of leading insurance

companies in the Central European region. We have collected their experience,

opinion and ambition on back office digitalization. During these expert interviews our

counterparts were mainly COOs, Operations managers and managers responsible for

the digital transformation of the organization. We have structured the interviews and

our questionnaire in a top-down manner, outlined by the following three main areas:

Definition and vision of the digital back office:

In this section we asked questions with the aim of getting an overview of what

digitalization means to the different insurance companies as well as what they see

as drivers and obstacles of it. We also defined the specific processes that still have

potential for further digitalization and built a picture of what the fully digitalized back

office should look like. The results of this area are presented in Chapters II and III of

our study.

Current status of back office digitalization:

The second set of questions was targeted at understanding the current status of back

office digitalization and this became the topic of Chapter IV in the study. First we took

a detailed look at the current operating model of underwriting, policy management

and claim processes. This included analyzing their degree of automation and the share

of paperless processes. To summarize this section we defined the current tools used to

digitalize the back office activities.

Ambition level for digitalizing the back office in the next three years:

Finally we ended our survey with asking questions about the ambition level for

digitalizing the back office in the next three years. Our questions here were aimed

11INTRODUCTION

at achieving an understanding of the target picture for the operating model of

underwriting, policy management and claim processes. Within this, the focus was on

the share of STP (Straight-Through-Processing) and paperless processes in the future,

as well as the target turn-around time. These results are summarized in a form of

target picture of digital back office in Chapter V of this study.

MARKET SURVEY

We have conducted a regional customer insight research which provided the second

leg of our analysis and study. In this customer survey we aimed to map the digital

expectations of consumers towards the insurers. In doing so, we have carried out

about 1,700 surveys across Central Europe. The scope of this market research

included three main areas:

> Determine the behavior and digital expectations of consumers from their insurance

companies

> Evaluate the insurers’ online performance and the extent, to which they match the

expectations of the clients.

> Outline the consumer insight based implications for insurers to assist them in

shaping their digital agenda

COMPARISON TO PEERS

For better interpretation, we have clustered the results throughout the study by the

following three different perspectives:

Market

In order to allow insurance companies to understand the performance range, we have

statistically evaluated the Central European insurers’ opinions and provided not only

the average performance of the market, but also the top quartile performance and the

low quartile performance.

Size

We interviewed both leading insurance companies in the region as well as smaller,

innovative and agile ones. As the size of the insurer was often a decisive factor

we have introduced two different size segments, which we defined based on the

respondents’ Gross Written Premiums (GWP). The first category is that of large

insurers and we defined this segment as insurance companies with annual EUR 200 m

GWP or more. The second category is that of small insurers and this segment includes

insurance companies which have less than annual EUR 200 m GWP.

Focus

The nature and environment of life and non-life businesses are very different and

besides the size of the insurer it was the second most differentiating factor. To account

for this we have segmented the participating insurers into two further categories: life

focused insurers and composite insurers. We defined the category of life insurers as the

companies with 80% or more GWP from life products and the category of composite

insurers as the companies with more than 20% GWP from non-life products. The

analysis of the results along these segments has shown a pattern throughout the study.

12

13

CHAPTER II

Digitalization and the back office: The means of survival and differentiation

14

It is no surprise that tech companies perform better in digital services, but the client requires those high standards from other industries as well.

DIGITALIZATION AND THE BACK OFFICE

CUSTOMER EXPECTATIONS ARE INCREASING

The client easily gets used to enjoying high-quality services. In the case of digital

services, tech-native companies are setting the trends. Their performance defines the

standard, which is currently demanded from all companies regardless of their industry.

It is no surprise that tech companies do much better on home ground than any other

industry’s players do.

However, the only participant of the deal who is not interested in excuses is the

client. Clients’ functional and simplicity expectations are exactly the same while using

social media or buying insurance for their car. Insurance companies must accept this

challenge in order to keep up with the pace of digital expectations.

Figure 1. Technology trends

Lifted expectation

of consumers that

defines the new

standard both for the

online and offline

world

Gamification

Addresses the competitiveness ofcustomers to foster cross- and up-sell

Behavior based targeting

Cookies used to remind customers about their visit and offer them

relevant products

Augmented reality tool

Tool used to lift attention and assist in selecting the right product

Superior sales capabilities

Intuitive browsing, integrated checkoutand delivery

Connected devices (IoT)

Monitoring of behavior to offer additional products or customize the existing ones

Social network based sales

Platform used to market and sell products and services

Emerging technological trends shown in Figure 1 are components of the digital

trendsetting process, which creates new expectations day by day. The outcome of this

process is an evolving set of standards, which are valid for the customers of insurance

companies as well.

According to our latest customer insight study, no matter whether consumers intend

to gather information, purchase a product or get service support, they seek more and

more digital channels to interact. They would like to begin a process on one device

and continue it on another: the Omni-channel access has become a hygiene factor.

If insurance companies want to meet their clients’ expectations, they must apply

appropriate new digital tools to create an engaging and convenient way for consumers

to get things done quickly.

15DIGITALIZATION AND THE BACK OFFICE

Low complexity and standardized features make a product ready to be successful online.

GENERATIONS Y AND Z WILL SOON DRIVE ONLINE PURCHASES

Figure 2. Purchase channel preference of consumers by products

Share of digital

channels1)

Age groups [years]

35 - 4425 - 3415 - 24 45 - 54 55 - 64 55+

1) Online, Call center and smart phone apps

30%

25%

20%

15%

35%

10%

5%

0%

40%

Investment life Property MTPL CASCO Accident life

Consumer preferences are clear; it is the middle-aged customers who are currently

purchasing through digital channels. As shown above, the 35-44 age group has the

highest (approximately 40%) preference to purchase MTPL through digital channels.

A generation shift is likely to come. This will be propelled by the emergence of

Generations Y and Z. They are practically digital natives and by their emergence, i.e.

collection of assets, wealth and purchasing power, the importance of digital channels

will further grow.

MTPL and CASCO are, besides travel insurance, the current flagship online insurance

products. Customer preferences show household & property and accident life

insurance to be the next online-driven insurance products. Their low complexity and

standardized features are the key characteristics, which position them as the next

potential online flagships.

DIGITAL CONSUMERS HAVE STRICT TIME AND EFFORT

EXPECTATIONS

The choice of consumers to purchase through digital channels and online is driven

by many factors, but before all else it is driven by their aim to save time and effort

in obtaining the necessary insurance. In general, the pace of life is increased and

especially, but not only, younger generations are used to fast, easy and frictionless

online purchases.

16 DIGITALIZATION AND THE BACK OFFICE

Simple, cheap products can be a good offer for digital customers.

A simple and quick quoting process is the way to avoid drop-out risk.

Online sales skills of insurers do not match the expectations of clients. As shown in

Figure 3, the client expectations regarding time and effort required to purchase MTPL

insurance are lower than what most of the insurers are offering. Our regional mystery

shopping results revealed that some insurers have really simple online offering. Yet, all

of them require more time and effort than clients are aiming to spend (13 minutes and

7 fields).

Figure 3. Client expectation vs. insurers’ offering for time and effort to get an MTPL quote online

55

Nr. of fields willing to fill-out [#]

Very high

drop-out

risk

Sweet

spot

Time willing to invest [minutes]

50

45

40

35

30

25

20

15

10

5

0

0 4 8 12 16 20 24 28 32 36 40

SI averageSK average

CZ average

Consumers Insurers

HR averageHU average

Certainly, insurance is more complex than the purchase of a book, but insurers need

to further simplify their offering. And this is true not only for their online offering

but also for their offline offering. Simplifying the purchase process requires not only

product simplification but also a high degree of process automation and the use of an

external database.

In order to match the speed and effort requirements of the nowadays consumer,

insurers need to invest more into the development of back office processes, speed

them up and look for shortcuts. Some leading insurers already cracked this question

and introduced fast quoting tools, which aim to minimize the effort and time required

from the consumers. These tools allow quick identification of the client, based on only

3-5 details. Once the client is identified the rest of his/her details are wired in from

third party external databases (e.g. car registry for MTPL). Following this, the client is

only asked to check his/her details and proceed to check-out.

The concept of mobile quote further simplifies this and enables the generation of

an MTPL quote based only on the photo of the car registry document. This surely

has only marginal value added compared to the fast quote based on 3-5 inputs, but

demonstrates the possibilities and the power of available digital technology.

17DIGITALIZATION AND THE BACK OFFICE

Figure 4. The concept of mobile quotes

Client takes a photo

Back office

Offer is immedia-tely generated

30 sec 15 sec MTPL offer delivered in ~45 seconds

Car register documentName

Car type

Plate number

Car register document

Name

Car type

Plate number

MTPL offer for car

with plate number:

€ 99

Name

Car type

Plate number

...

...

...

ABC-1234

Accept & Pay

BACK OFFICE CAPABILITIES ARE CRUCIAL FACTORS TO WIN

THE DIGITAL GAME

Front office digital solutions cannot work properly without a constantly high

performing back office. The evolving client expectations, regulatory requirements and

competition are putting the insurers’ back office under multi-directional pressure by

demanding:

> Fast, transparent and individualized solutions

> Multi-channel access

> Real time processing of online cases

> Low cost and price position

> Advanced technological solutions

Digitalization is a must for insurers to survive and differentiate and the back office

plays a major role as the key enabler. Without implementing the digitalization

measures, which are now becoming the standard faster than expected, an insurer

will fall behind and lose customers. Customers expect low prices and insurers tend

to focus on this current aspect. They should not forget to come up with ways to

differentiate their products either. Without these measures they could be a cost

effective insurer but fail to stand out in the large pool of competitors.

18

19

CHAPTER III

The approach to digitalization: First define the goal and then set the priorities

20 THE APPROACH TO DIGITALIZATION

Insurers define digitalization through their motivation, drivers and objectives.

The Group has to support local management to overcome local obstacles.

DEFINING DIGITALIZATION

The definition of the process of digitalization relies on various aspects of the term. It

has to be taken into account what the underlying motivation is. Based on this, four

definition categories can be distinguished: Data management, new opportunities,

operating efficiency and client experience. These aspects are taken under

consideration in different intensities based on the type of the insurer. Our analysis

looks into the different levels of importance based on the focus (composite vs. life) and

size (small vs. large) of insurers.

Figure 5. Motivation according to insurers’ focus and size

Focus Size

Operating efficiency

Client experience

Data management

New opportunities

SmallComposite LargeLife

SmallComposite LargeLife

SmallComposite LargeLife

SmallComposite LargeLife

Operating efficiency

The largest portion of the surveyed insurers (63%) sees digitalization as a tool to

improve operational efficiency. This is driven by increasing pressure to reduce costs,

processing times and the improvement of overall efficiency. This cost pressure is

understandably more noticeable at smaller insurers, due to the increased pressure

to achieve a fast return of investment with their lower total revenues. Regarding the

focus of insurers, this factor is more important for life specialized insurers. Among

others this is probably driven by the increasing regulatory pressure on life products’

transparency and cost loading.

Client experience

The second most frequently (37% of responses) mentioned motivation for

digitalization is the opportunity of increasing client experience through digitalization.

Providing a unique experience could be the differentiating factor, which sets one

insurer apart from the others. To convey the lifted client experience, increased

frequency and quality of client contact have to be reached. In this, mobile solutions,

simplified sales processes and fast quoting tools are the recent trends. This aspect is

mostly important for composite insurers and large insurers.

Data management

Many insurers are motivated by acquiring skills to better manage and utilize data.

The underlying reason for this is to better understand the customers and enable the

automation of processes. This factor was mentioned by 21% of survey respondents in

their personal definition of digitalization. It was especially emphasized by composite

and large insurers.

21THE APPROACH TO DIGITALIZATION

58% of insurers have given digitalization a moderate to high strategic focus.

The two most common practices are either a separate document or a separate section in the strategy.

Telematics and other connected devices provide insurers with large amounts of data,

which can be converted into tailor-made pricing, services and offerings. Furthermore,

it allows for the identification of cross- and up-selling opportunities through big data

analytics, e.g. cardlytics based tailored insurance offer of bank-insurers.

With the spread of connected medical devices and wearables, data management will

gain further importance in the life segment. It will enable for analytics similar to the

aforementioned telematics.

New opportunities

11% of respondents said that their motivation for digitalization is to explore and

exploit new business opportunities. The increasing use of online portals, mobile

applications and connected devices (e.g. telematics) leads to more customers having

convenient contact points to the insurers, creating new business opportunities through

an easier conversion into leads. Especially small and life insurers see large potential in

tools for lead management in order to achieve further business potential.

Figure 6. Definition of digitalization – quotes by interviewees

"Cost pressure is the driver of the optimization"

"Process, time and cost effectiveness are also important"

"It's the client who generates most of the needs for digital development"

"Better understanding data""Capturing and automated processing of data"

"Digital journey creates new tasks and technological needs"

"Digitalization can enable new business models"

"Provide unique customer experience"

FORMULATION AND ORGANIZATIONAL SUPPORT OF A

DIGITALIZATION STRATEGY

The practice of formulating a digitalization strategy has not yet spread throughout

the entire industry. Only 58% of surveyed insurers have actually created a separate

strategy for their digital initiatives. This can be split into two sub-categories. The ones

that have formulated a separate strategic document for digitalization (21%) and the

ones that have integrated the topic of digitalization into an existing strategic document

in the form of a chapter or section (37%). Only 16% of the insurers do not have any

roadmap for digitalization at a strategic level and thus also do not have any mention

of digitalization in a strategic document. The remaining 26% do address the topic, but

do not have a separate section dedicated to it, but have distributed parts in several

strategic documents.

If an insurer decides on a separate digitalization strategy, usually the Chief Digital

Officer is appointed as the sole owner. Otherwise, the Chief Executive Officer is

responsible for the initiatives. This way a comprehensive view is ensured and the

planning & execution is conducted on a business need basis. When digitalization

22 THE APPROACH TO DIGITALIZATION

is approached holistically, it is possible to avoid coexistent systems and to exploit

synergies. The backside of this approach is that the digitalization efforts are not

completely interconnected with other business processes, as they are limited to the

confines of the strategic document.

With regards to the field of focus, there is no dominant cluster that responded with

having a separate strategy for digitalization. However, the difference when comparing

small and large insurance companies is significant. It is more likely to be a characte-

ristic of small insurers to have such a large focus on the digital strategy. Perhaps it is

simpler to have oversight over a smaller scale system and process landscape.

At the same time, in 37% of the cases digitalization is approached as part of the overall

strategy, making it a part of the responsibility of either the Chief Operations Officer or

the Chief Information Officer. Respondents indicated that digital initiatives are mostly

contained in the business strategy or the IT strategy and it is split into front office

and back office specific initiatives. In a small number of cases, it is included into the

operations strategy. Interestingly, there is no difference with regards to size of insurer.

However, life insurers are more prone to include digitalization as part of a strategy

than their composite peers.

EXPECTED COMPETITIVE ADVANTAGES TARGETED THROUGH

DIGITALIZATION

The main areas targeted by insurers in terms of competitive advantages are the

servicing time, service quality and the cost position achieved through digitalization.

Targeting of these areas can differ based on the focus and size of insurers. At some

areas there is significant difference in the focus of insurers, e.g. product innovator and

lead management.

Figure 7. Competitive advantages targeted through digitalization

3.7

3.6

3.4

3.3

3.2

3.1

3.0

2.9

2.8

2.7

2.6

Short servicingtime

Importance [pts]

Servicequality

Low costposition

Excellence Competitiveagility

Leadmanagement

Productinnovator

Average

3.5

3.8

Large Small Life Composite

23THE APPROACH TO DIGITALIZATION

The rise of the individual risk based scoring development is foreseeable, as digital tools allow for more efficient assessment of individual risk levels.

The largest difference in the views of insurer types can be seen in the area of product

innovator. Large and composite insurers give it an above average level of importance.

The additional driver for composite insurers is the utilization of IoT/connected tools in

order to prepare and advance smart offerings to the customer. Life insurers however,

don’t see any current competitive advantages in product innovation.

The second category, where the large spread of clusters is determined by the differing

views of composite and life insurers, is achieving a low cost position. Life insurers

see a very high relevance in a low cost position. Composite insurers don’t want to

consider this, as they already have comparably lower cost position.

A short servicing time is mostly a determining factor for large and life players.

Composite and small insurers are located somewhat below the average. Large

insurance companies show a high level of interest in the quality of their service.

Both of these points show the overall ambition of large insurers to provide high

quality services in the fastest possible time, which could be achieved through the

implementation of STP workflows.

Excellence on the other hand is the opposite. Here, large players and composite

insurers see below-average possibilities to distinguish themselves from their peers

through targeting this point. It is rather the small and life insurers, who see potential

in excellence.

The only competitive advantage which all insurers agree on is competitive agility,

which received the same score from every type of insurer.

One interesting thing that can be observed is the large deviation between small and

large insurers regarding lead management. It is observable, that small insurers put high

emphasis on leads as opposed to their large peers. This can be explained by the large

insurers’ reliance on their existing portfolio.

24 THE APPROACH TO DIGITALIZATION

Almost all insurers see a high potential in the digitalization of claims management.

FOCUS OF DIGITALIZATION EFFORTS

The decision to digitalize a process is based on detailed business case projection. Some

processes are worth of digitalizing while other processes do not guarantee return

of investments. In our survey we assessed in details the decision making process of

insurers.

Figure 8. Digitalization potential of selected processes

Claims management

Document management

Policy administration

Client data management

Billing (core business) andcommission calculation

Underwriting

Fraud, litigation andrecovery management

Very high High Low Very low

100%

100%

100%

100%

100%

100%

100%

52% 45%

18% 32% 43% 7%

59% 31% 3% 7%

66% 21% 10% 3%

59% 24% 17%

52% 24% 24%

34% 28% 38%

3%

Claims processes have the highest digitalization potential according to the vast

majority of insurers. This area was less in focus in the past and insurers see room

for improvement. Moreover, 33% of insurers have on-going or planned projects in

this field. Typically these projects aim to digitalize the claim processes, BPR and

development of tablet/mobile solutions for the claim adjusters. From a focus and size

perspective, it is mainly the small insurers who see a high potential in this area.

The second high potential area for digitalization is document management. The

majority of life insurers sees a large potential and the composite insurers consider it

less relevant. 17% of insurers have on-going or planned projects in this field. Typical

projects in this area are introduction of workflow, an archiving system and a central

Document Management System.

Policy management is the third area with a high potential for digitalization. These

processes were less in focus in the past, but insurers nowadays see the need to

optimize it due to cost constraints. 11% of insurers have or plan projects in this field.

Typically the scope of these projects is the merging or changing of core systems and

the introduction of self-service portals.

Although client data management is considered to have the fourth largest potential

among the surveyed processes, it shows the highest number of projects initiated by

insurers (39%). These include incremental CRM developments, data clean-up and

paperless Customer Relationship Management.

25THE APPROACH TO DIGITALIZATION

Most activities of insurers are in data management, claim management and billing.

The remaining processes from the highest potential to lowest are Billing & commission

calculation, Underwriting and Fraud, litigation & recovery management. Out of these,

only Underwriting shows differences between the insurers with regards to their focus.

22% of insurers are running projects related to billing and commission calculation.

Examples include electronic billing and payment digitalization. 11% of insurers have

or plan projects in the areas of underwriting capabilities. Examples are typically tablet

solutions for demonstration and quotation, improvement of on-spot policy issuing,

including mobile printing capabilities. In the area of fraud, litigation and recovery

management only 6% of insurers have on-going or planned projects. In this area,

insurers are typically introducing fraud detection mechanisms and anti-fraud analytical

models.

Figure 9. Views of insurer segments and initiated/planned projects

Claims management

Process% of insurerswith project

39%

33%

22%

17%

11%

11%

6%

Document management

Policy administration

Client data management

Billing (core business) andcommission calculation

Underwriting

Fraud, litigation andrecovery management

Focus

Large difference

Composite LifeSize

Small Large

26

27

CHAPTER IV

Current status: Step-by-step digitalization of field processes and partial digitalization of back office processing

28

Overall process should be analyzed in two phases: field process and the back office process.

Field services are underdeveloped and leave significant room for improvement.

CURRENT STATUS

CURRENT SITUATION

In the scope of this study, we have applied an end-to-end approach to the analysis of

the back office digitalization. To gain full transparency of the degree of development,

the back office processes have to be split into two parts:

> Field process: the journey of the data and documents from the moment when the

client or the intermediary fills it in until its arrival into the back office for processing

> Back office process: the journey of the data and document within the back office. It

is the actual processing of the case, including generating and sending the answer to

the client or intermediary

In the scope of our study, we have covered both of the processes; however the

emphasis was on the field processes. Therefore, the assessment of the field process

provides more of an in-depth insight.

FIELD PROCESSES

Overall, these processes are underdeveloped from a digital perspective and they hide

a significant potential for improvement. Three main processes were in focus of the

analysis: underwriting; policy management and claims. The processes were analyzed

along four process steps, shown below in Figure 10.

Figure 10. Degree of development of field processes

0% 100% 0% 100% 0% 100%

Under-writing

Policymgmt

Claim

0% 100%

DigitalNon digital

DigitalNon digital

On/spotRetrospective

DigitalPaper

36% 64%

62% 38%

27% 73%

17% 83%

19% 81%

85%

23% 77%

32% 68%

32% 68%

23% 77%

34% 66%

25% 75%

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

15%

Comparing the three processes to each other, underwriting is digitally the most

developed. These processes were in focus of insurers in the past and they reach the

highest digital share at most of the steps.

Overall, the form fill-out step is the most developed. Leading insurers offer self-service

portals and dynamic online forms to their clients in order to communicate any policy

management or claim case. These digital tools allow them to automatically process the

request or to process it with higher efficiency as opposed to paper forms.

Collecting client signature is a common hurdle across all processes. The current

legislation does not allow for the usage of digital signature. In Central Europe, 15-19%

of insurers use some kind of a digital signature, but they only use it for negligible

administrative cases. The actual need for a physical signature of the client limits

the possibility to fully digitalize the field processes. This means, that currently the

sales process ends with at least one paper output where the signature of the client is

29

Collecting the client signature is a common hurdle across all cases.

CURRENT STATUS

physically captured. This and some other underlying documents have to be digitalized.

Some progress is made with the authorities and the legal simplification of products;

however there was no break-through reached by the time of our survey.

Digitalizing the underlying documents is a major task for any field process

digitalization. In general, this step is not developed from a digital perspective. This

means that insurers do not utilize the capabilities offered by the technology and most

of them make the papers travel from the field to the back office for digitalization,

instead of on-spot digitalization by the intermediaries.

Data and document sending to the back office is the most developed in case of

underwriting. Most advanced insurers have integrated the front end with their back

office workflow. The actual processing is performed based on the data sent from the

field and the flow of paper documents is completely separated. Real time processing is

more of a standard for retail non-life products and proprietary channels.

Underwriting

The underwriting process is the most developed from a digitalization perspective. This

is driven by the competition and the need for speed, agility and a differentiated image.

Therefore the digitalization of these processes is more in the focus of insurers.

From the perspective of channels, proprietary channels are more digital and better

integrated with the back office. External channels often hesitate to use or to connect

to the front end system of the insurer, due to privacy reasons. Therefore, external

channels often create the majority of the paper traffic in the back office – their cases

are more time consuming and expensive to process.

Figure 11. Journey of underwriting cases from the client contact to the back office

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

Electronically

Signature not required

On paper In the BO

In the FO by salesperson

No digitalization

In the FO by BO

Only paper

Only data electronically

Paper and data

On paper forms

Other

Quoting tool

In the FE

54%

8%8%

30%

44%

12%

32%

12%

81%

19% 62%

34%

4%

The front end system of intermediaries is the main tool used by the insurers to

digitalize the sales/underwriting process. A new platform – quoting tools – is on the

rise. These online/offline tools are gaining importance as they have shorter time to

market and ensure the insurers agility in the fast changing regulatory environment. On

the other hand, the online tools are fully integrated with the back office. This allows

for real time and automated processing.

30 CURRENT STATUS

Collecting the client signature is regulated by law, which does not allow for the use of

digital signatures on a touchpad, as for parcel services. Flexibility of the regulation is

region/country specific, but overall for the CE region some progress is visible. Leading

insurers solved the need for client signature with the legal simplification of products

and hybrid solutions through online quoting tools.

Underwriting process of certain products requires underlying documentation of the

asset, health, etc. For the digitalization (scanning and indexing) of these documents

there are two general models: either it is done in the front office or it is done in the

back office. Both models have their pros and cons, but overall the front office model

is more digitalized and allows for better overall performance. The majority (56%) of

insurers follows the back office model and relies on logistics of paper, which makes

their processes more expensive and prolonged.

62% of insurers apply a hybrid model and send both documents and data to the back

office for processing. Only 34% of insurers have a full digital model in place which

would work only based on the flow of data between the field and the back office. On

the end of the scale, 4% of insurers rely only on the physical flow of documents. The

more digital the data and document sending between the field and back office, the

shorter the turn-around time, less expensive the processing and the more competitive

in the sales efficiency is.

Policy management

Insurers admit high relevance and importance of digitalizing these processes.

However, this area was less in focus and in general it can be marked as an area for

improvement.

The sophistication of insurers is polarized. Low performing insurers are channeling

their clients to fill-out paper forms if they want to communicate changes regarding

their policy. Leading insurers offer their client self-service portals, online forms and/or

the possibility to conduct changes through the call center.

Figure 12. Journey of policy management cases from the client contact to the back office

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

Electronically

Signature not required

On paper In the BO

In the FO by salesperson

No digitalization

In the FO by BO

Only paper

Only data electronically

Paper and data

On paper forms

Other

Quoting tool

In the FE

36%

55%

9% 23%

41%

13%

23%

83%

17% 18%

59%

23%

The majority, 55% of insurers uses paper forms to receive change requests from their

clients. 36% of insurers record the changes directly into the front end system, which

is entered by the call center and the proprietary intermediaries. On the other hand,

Policy management was less in focus, but the self-service platform and call center will change it significantly.

31CURRENT STATUS

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

Electronically

Signature not required

On paper In the BO

In the FO by salesperson

No digitalization

In the FO by BO

Only paper

Only data electronically

Paper and data

On paper forms

Other

Quoting tool

In the FE

58%

23%

15%

4%

8%

36%

24%

32%70%

15%

15%

21%25%

54%

only few insurers offer dynamic online forms or client portal which allows clients to

communicate digitally and paperless with their insurers.

Collecting client signature is required in most cases. However, remote verification of

the clients is the way of the future – based on the opinion of most of the insurers. This

means use of personal client accounts and/or use of call center identification.

Digitalization of underlying documents is mostly conducted in the back office (41%) or

in the middle office (23%) by the back office people. Some 23% of cases are digitalized

by the front office.

Sending cases from the field to the back office is mostly conducted in a hybrid model

– sending paper documents and data in parallel. Only 23% of insurers use the fully

digital model and send only data to the back office.

Claims

Claims management process is underdeveloped at most of the insurance companies

and it has considerable digitalization potential. Interestingly, the performance of

insurers polarizes into two groups: insurers having a mobile claims adjuster system

and those who do not have one.

Figure 13. Journey of claim cases from the client contact to the back office

Overall, the first step of notifying and filling out the form with client data is mostly

paper based, 60% of insurers do it this way. On the other hand, 23% of insurers have

an integrated front end for clients and adjusters which digitalize this step.

Collecting client signature is less of an issue in the case of claims. 15% of insurers use

some kind of digital signature solution and an additional 15% require no signature

from the clients, in most cases.

Digitalization of underlying documents is the most developed. About 32% of insurers

use on-spot digitalization solutions. This is mostly done within the mobile solution

of the claim adjusters, as the adjusters need to take pictures of the damage, the same

functionality can be used to digitalize documents as well. An interesting development

is the online claim monitoring tool, which allows the client to upload documents to

his/her case.

Only few insurers have an integrated mobile solution for the claim adjusters.

32 CURRENT STATUS

Data and document sending into the back office mostly (54%) follows the hybrid

model. On the other hand, 21% of documents are sent to the back office only in paper

form – large share of these are documents sent by the clients after the adjuster visit. In

these cases, the online claims monitoring tools are of big help as they allow clients to

attach these documents to their cases in a digital format.

BACK OFFICE PROCESSES

Once the data has arrived into the back office, insurers perform the actual processing

of cases. We mapped the sophistication level of the back office processes along the

following three criteria:

> Degree of paperless

> Level of automation

> Process dependence

Degree of paperless

A paperless back office is the must have standard in every target picture. It is difficult

to introduce it. As the results of our survey confirm only 52% of insurers have a

paperless back office. These insurers use workflow and DMS systems to facilitate

the work within the back office. On top of these 52% some insurers follow a hybrid

model, having part of their products or processes paperless and the other part still

paper based.

Size is a common denominator of insurers having a paperless back office. It means that

those insurers with a paperless back office are mostly the large ones. While the group

of insurers with a paper based back office is dominated by small insurers.

Overall, executives claim the largest obstacle in the transformation of the back office

to a paperless one is employee resistance and the habit to use paper. Therefore, the

key recommendation is to start the change with the field services/intermediaries and

then to continue with the back office processes.

Level of automation

Automation of case processing within the back office is an important area in reaching

cost efficiency and speed. In our survey, we have measured the level of automation

through the STP rate. This indicator is suitable for the measurement of the strategic

automation level, but for more detailed operational benchmarking, lead-time analysis

and comparison is suggested – this indicator captures the impact of partial automation

as well.

Overall, the automation level of the back office is at a medium level as the results of

our survey show in the Figure 14.

Size matters! Throughout all of the categories large insurers have reported a higher

level of automation. It is most probably due to the high cost of automation, as it can

be very expensive. In comparison to the human aided processing it is often more

expensive. This is a specificity of relatively low wage countries, such as the Central

Europe countries. Insurers mostly tackle this business case issue with overwriting

the transaction cost view with TCO and strategic perspectives. Otherwise they often

reach out for a local IT solution provider which can be much cheaper compared to the

global solution.

33CURRENT STATUS

4446

41

55

10%

20%

50%

60%

70%

40%

30%

0%Investmentlife (unit-linked)

House-hold & property

MotorInvestmentlife (unit-linked)

House-hold & property

MotorInvestmentlife (unit-linked)

House-hold & property

Motor

UNDERWRITING POLICY MGMT CLAIM

54

38

26

32 32

STP rate of small insurers STP rate of all insurers STP rate of large insurers

The automation level of non-life products is higher compared to those from the life

segment. Especially investment life insurance underwriting has a low automation

level. This is due to the complexity of the product and the legal framework. In this

product category most of the insurers lack economies of scale and they cannot afford

to develop a full-fledged automated process.

Policy management processes as a whole show the highest potential for improvement.

As shown in Figure 14, the usual automation level is around 40%. Clearly, this was

not the target area for insurers in the past.

The automation level of claim processing is polarized. Large insurers have significantly

better automation levels as opposed to their small peers. This leaves the small insurer

with a significant efficiency gap across all products.

Figure 14. Automation level of case processing within the back office [STP rate]

Process dependence

48% of insurers do the processing of cases in the back office based on the data from

the front end and the images from DMS. This allows for real-time processing and a

fast reaction. This model is mostly applied by small composite players. Moreover, it is

connected to their challenger attitude and acceptance of a higher operational risk in

order to provide a fast response.

26% of insurers does the processing based on the data from front end and the images

of DMS, however the back office also have to wait for the physical documents. This

is due to compliance reasons and these insurers are mostly life specialized. Their

aim with this is to make sure the contracts are valid and comply with all formal

requirements while accepting a prolonged turnaround time.

The remaining 26% of insurers do the processing solely based on the physical

documents as no document digitalization system is in place. These insurers are mostly

small composite players.

34

35

CHAPTER V

Target picture: Field processes are highly digital and the back office processing is automated and paperless

36 TARGET PICTURE

Underwriting, policy management and claim processes will be highly digitalized from end-to-end by the utilization of major front-end developments.

TARGET PICTURE FOR FIELD PROCESSES

After analyzing the current status of field processes in Section IV, we concluded that

field processes are digitally underdeveloped and they have a significant potential for

digitalization. Subsequently, we asked the insurance companies about their target

picture for these field processes for the next three to five years. To easily interpret the

findings compared to the current status, we once again focused our analysis on the

three main processes: underwriting; policy management and claims. The processes

were then mapped along the four main process steps as shown in Figure 15 below.

Figure 15. Digitalization ambition by process and process step

0% 100% 0% 100% 0% 100%

Under-writing

Policymgmt

Claim

0% 100%

DigitalNon digital

DigitalNon digital

On/spotRetrospective

DigitalPaper

87%

87%

73% 27%

78% 22%

78% 22%

26%

38% 62%

48% 52%

29% 71%

68% 32%

64% 36%

68% 32%

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

74%

13%

13%

Comparing the three processes to each other, the highest degree of digital

improvement is projected to be seen in policy management and claim processes,

as those are the two fields with currently lower development levels. Although

underwriting will remain the mostly digitalized, it will cease to have an overwhelming

advantage compared to the other two processes. In terms of sending the documents to

the back office, the other two are even projected to outperform it.

Overall, the form fill-out step will remain the most developed in the future as well,

the same way as it is currently. Data collection and recording will be highly digitalized

and in all processes the front end will take the lead. Online, self-service tools on the

website will gain in significance and offline visits at the front office or by the claims

adjuster will be supported with e-forms.

In terms of process steps, the collection of client signatures is projected to undergo

the highest degree of development. While currently the share of insurers using digital

solutions for this step is less than 20% across all processes, this number is predicted

to be over 70% in case of all three processes. It is forecasted that electronic signature

will be the standard across all types of cases. In remote verification, client portals with

authentication and eIDs will take the lead and the deployment of biometric solutions

is likely in front end and claim adjuster tools.

Digitalization of underlying documents will be changed in two directions: avoidance

of underlying document digitalization and on-spot digitalization. On-spot digitalization

will be conducted through the front end system in the future.

Sending the cases by the intermediaries and claim adjusters will be increasingly digital

and integrated with the workflow. Paper flow between the field and the back office

will exist only for important cases, e.g. large life contracts.

37TARGET PICTURE

Underwriting

The underwriting process will keep its leading position from a digitalization

perspective. Although there will be improvements throughout this process, it will

be insignificant. In the case of policy management and claims more significant

improvements are expected. Figure 16 below summarizes the changes in the

underwriting process, with the current situation presented in the outer circle and the

future projections in the inner one.

Figure 16. Journey of underwriting cases from the client contact to the back office – AS IS (outer circle) and TO BE (inner circle)

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

Electronically

Signature not required

On paper In the BO

In the FO by salesperson

No digitalization

In the FO by BO

Only paper

Only data electronically

Paper and data

On paper forms

OtherQuoting tool

In the FE

54% 57%

8%

30%

8%

30%13% 19%44%

12%

32%

12%

33%48%

81%

22%

78%

19% 62%31%

64%

34%

4%5%

Insurers will further digitalize the data collection and recording step of the

underwriting process. The development of the front end system will be a crucial part

of this. Quoting tools will also increase their share, due to the low effort/short time to

market these tools.

As we mentioned earlier, the collection of client signatures is currently one of

the largest hurdles of all the field processes, including underwriting cases as well.

However, insurers expect to overcome this obstacle within the next three years and

electronic signature will be the standard to collect clients’ approval. The way this

development can become reality is if insurers push for change of regulation and bring

in new technological solutions, such as biometric touch screens. Usage of eID in the

online sale process is not likely in the future.

Digitalization of documents in the back office will significantly decline. On-spot

document digitalization will replace scanning. Integrated solutions in the front end

will empower sales to perform digitalization of documents as an integral part of the

sales process.

Transfer of cases from the field will become highly automated with 64% of data

transfers sent only digital. Hybrid solutions will remain in place for 32% of the cases,

e.g. for large life contracts and other high stake cases.

Policy management

Policy management will be one of the areas with the highest improvement in

digitalization within three years. This is due to its high relevance and importance as

well as its currently low level of development.

38 TARGET PICTURE

Figure 17. Journey of policy management cases from the client contact to the back office – AS IS (outer circle) and TO BE (inner circle)

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

Electronically

Signature not required

On paper In the BO

In the FO by salesperson

No digitalization

In the FO by BO

Only paper

Only data electronically

Paper and data

On paper forms

Other

Quoting tool

In the FE

36%

55%

9%52% 35%

9%

4%

23%

29% 41%

13%

33%

38%23%

83%

78%

17%13%

9%

18%

5%

59%

23%

68%27%

The form fill-out step will be one of the focus points of policy management

digitalization. While currently 55% of insurers use paper forms to receive change

requests from their clients, this figure will drop to 9% and insurers will use different

solutions for this step. The front end will be the main platform to record change in

the policy, i.e. through the call center or intermediary. Other digital tools will also be

deployed, thus avoiding paper generation (e.g. client portals).

The same way as we have witnessed with underwriting, the collection of client

signatures is projected to undergo the highest degree of change in policy management

cases as well. Digital signatures will be the standard in case of front office visits.

More importantly secured client portals with identity verification will be deployed.

Moreover, an alternative technology could be the eID based client verification.

Although the changes in the digitalization of underlying documents will not be as

significant, there are still some improvements to come within this field as well. More

underlying documents will be digitalized by the front office, as they will act as main

interaction points and on-spot digitalization capability will be deployed.

Data transferring from the client and/or front office will be digital to a large extent.

Only the necessary paper flow will remain.

Claims

The claims management process is currently underdeveloped at most of the insurance

companies and as such, it is also projected to undergo drastic changes.

The form fill-out step will become significantly more paperless than it is currently.

The front end will become the primary tool to directly capture client information, e.g.

through the call center. Other digital solutions will be used as well, such as self service

tools on the website.

Electronic signatures will be the standard, especially in case of on-site visits of claim

adjustments. In case of remote claim servicing, client verification will be performed

through secured client portals/call center or potentially with the use of eID.

Policy management will be steered to online tools with remote client identification; at the offline channels the process will be digitalized.

Claims will become self-service online, while the must have adjuster visits will be fully paperless in data recording and sending to the BO.

39TARGET PICTURE

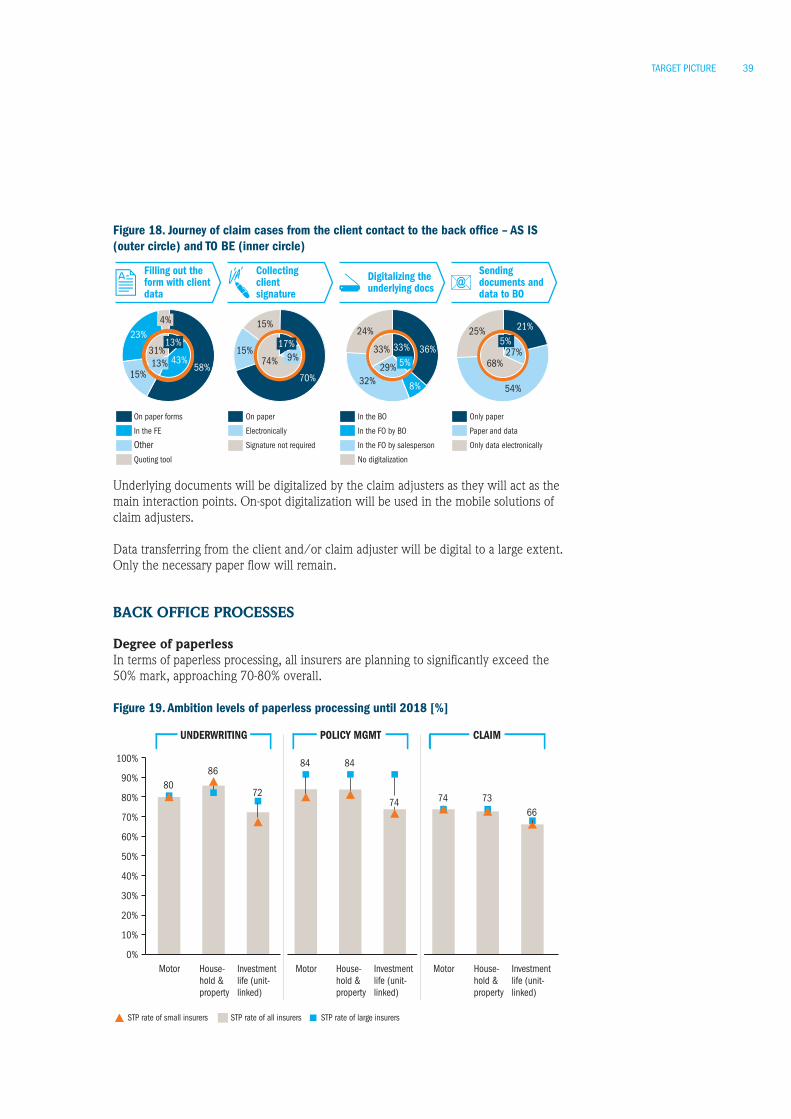

Figure 18. Journey of claim cases from the client contact to the back office – AS IS (outer circle) and TO BE (inner circle)

Filling out the form with clientdata

Collectingclientsignature

Digitalizing theunderlying docs

Sendingdocuments anddata to BO

Electronically

Signature not required

On paper In the BO

In the FO by salesperson

No digitalization

In the FO by BO

Only paper

Only data electronically

Paper and data

On paper forms

OtherQuoting tool

In the FE

58%43%

23%

31%

15%

13%

13%

4%

8%

36%33%

5%

24%

33%

29%32%70%

17%9%

15%

15%74%

21%5%

25%

54%

68%27%

Underlying documents will be digitalized by the claim adjusters as they will act as the

main interaction points. On-spot digitalization will be used in the mobile solutions of

claim adjusters.

Data transferring from the client and/or claim adjuster will be digital to a large extent.

Only the necessary paper flow will remain.

BACK OFFICE PROCESSES

Degree of paperless

In terms of paperless processing, all insurers are planning to significantly exceed the

50% mark, approaching 70-80% overall.

Figure 19. Ambition levels of paperless processing until 2018 [%]

10%

20%

50%

60%

70%

80%

100%

90%

40%

30%

0%

84

House-hold & property

84

Motor

72

Investmentlife (unit-linked)

80

Motor House-hold & property

86

Investmentlife (unit-linked)

Motor

74

House-hold & property

73

Investmentlife (unit-linked)

6674

UNDERWRITING POLICY MGMT CLAIM

STP rate of small insurers STP rate of all insurers STP rate of large insurers

40 TARGET PICTURE

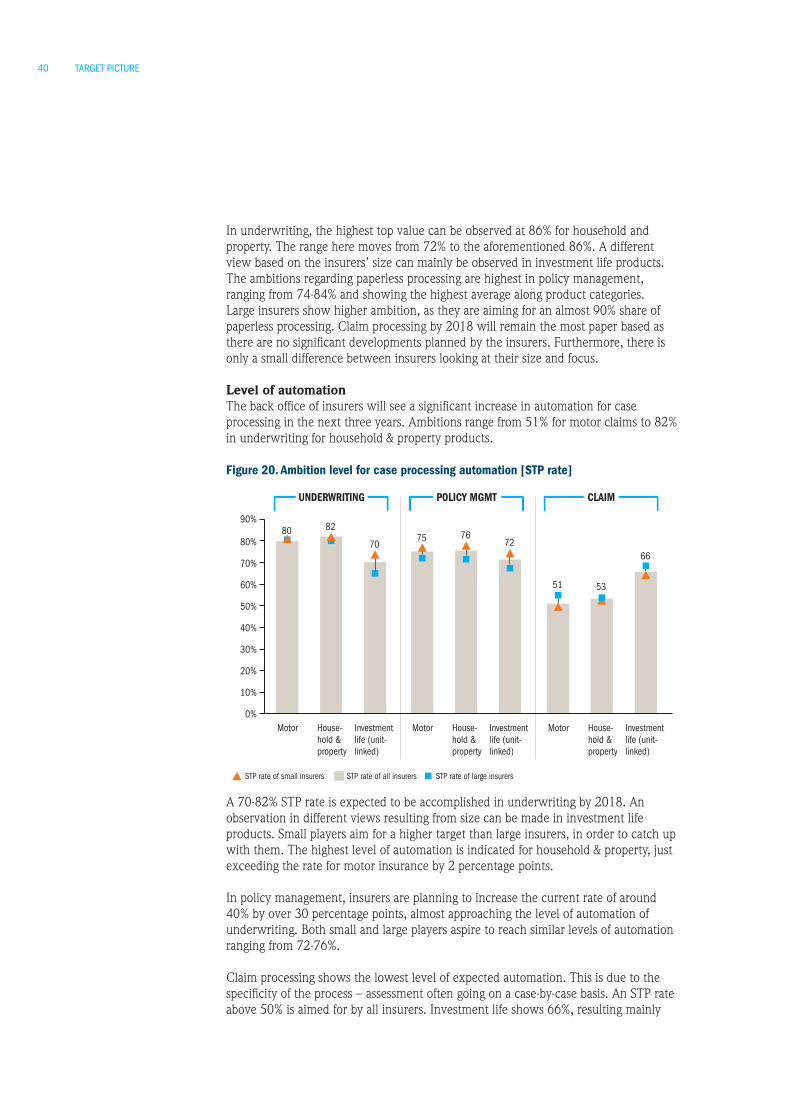

In underwriting, the highest top value can be observed at 86% for household and

property. The range here moves from 72% to the aforementioned 86%. A different

view based on the insurers’ size can mainly be observed in investment life products.

The ambitions regarding paperless processing are highest in policy management,

ranging from 74-84% and showing the highest average along product categories.

Large insurers show higher ambition, as they are aiming for an almost 90% share of

paperless processing. Claim processing by 2018 will remain the most paper based as

there are no significant developments planned by the insurers. Furthermore, there is

only a small difference between insurers looking at their size and focus.

Level of automation

The back office of insurers will see a significant increase in automation for case

processing in the next three years. Ambitions range from 51% for motor claims to 82%

in underwriting for household & property products.

Figure 20. Ambition level for case processing automation [STP rate]

10%

20%

50%

60%

90%

80%

70%

40%

30%

0%

76

House-hold & property

75

Motor

70

Investmentlife (unit-linked)

80

Motor

UNDERWRITING POLICY MGMT CLAIM

House-hold & property

82

Investmentlife (unit-linked)

72

Motor House-hold & property

53

Investmentlife (unit-linked)

66

51

STP rate of small insurers STP rate of all insurers STP rate of large insurers

A 70-82% STP rate is expected to be accomplished in underwriting by 2018. An

observation in different views resulting from size can be made in investment life

products. Small players aim for a higher target than large insurers, in order to catch up

with them. The highest level of automation is indicated for household & property, just

exceeding the rate for motor insurance by 2 percentage points.

In policy management, insurers are planning to increase the current rate of around

40% by over 30 percentage points, almost approaching the level of automation of

underwriting. Both small and large players aspire to reach similar levels of automation

ranging from 72-76%.

Claim processing shows the lowest level of expected automation. This is due to the

specificity of the process – assessment often going on a case-by-case basis. An STP rate

above 50% is aimed for by all insurers. Investment life shows 66%, resulting mainly

41TARGET PICTURE

from the pure buy-back cases. Large insurers plan only a small increase of automation

compared to the as-is, while small peers aim at significant improvements.

Turnaround time

Client satisfaction largely depends on the time it takes the insurer to respond to the

client’s initiated interaction. Respondents mostly consider a turnaround time of 5 days

to be the psychological threshold until some feedback has to be provided to the client.

Insurance companies aim to remain below this threshold. The fastest response is

expected in underwriting with 1.5 days, followed by policy management with a

turnaround time of 2 days. In case of claims, insurers are aiming for 5 days.

It can be observed that large insurance companies aim for overall longer targets, likely

depending on the hierarchical and organizational levels a case has to go through. This

way, smaller insurers have the opportunity to present a shorter response time to the

client, creating a competitive advantage for them.

FEASIBILITY AND KEY OBSTACLES OF FULLY AUTOMATED BACK

OFFICE PROCESSING

Although executives see a large potential in digitalization and also have a vision of

how to accomplish it, there are some obstacles that have to be overcome in order to

enable a full implementation of digital initiatives.

The main hurdle insurers have to overcome is the business feasibility compared to

labor costs, in a short term business plan. 62% indicated that the low labor costs make

a large investment into IT solutions very difficult to justify economically.

The next obstacle with 55% is the complexity and variability of certain products,

reducing the possibility of standardization. This is especially relevant for life insurers.

Around 40% of interviewees have also added, that corporate culture and regulation

play a significant role in certain digitalization initiatives. Regulative restriction like

privacy, data security and identification need to be handled accordingly in order to

fully automate processes.

Factors with somewhat lower importance are the incompatibility of the current

legacy system, the lack of client acceptance to digital communication and the lack of

capabilities and technology. The interviewees indicated the relevance of these between

21% and 31%.

Regarding the relevance according to insurer type, there are only a few yet significant

differences. As mentioned earlier, insurance companies with life products see the

complexity of the products as more of a problem than composite insurers. Based

on size it is observable that large insurers see a large opposition in regulation, more

than for any other obstacle mentioned in the interview. Small insurers see more of a

problem in their IT systems, meaning the incompatibility of their legacy system and

the lack of capabilities to overcome these technological obstacles.

42

43

Summary and recommendations

44

SUMMARY

Client behavior is digitalizing and it is propelled by the tech-native companies.

These companies are offering state-of-the-art digital tools to the customers and thus

increasing their expectations. This forces companies in other industries, such as