insurance protocol etherisc decentralized€¦ · etherisc decentralized insurance protocol dip...

TRANSCRIPT

Etherisc DecentralizedInsurance Protocol

DIP Token Generating Event

JULY 2018

Mission Statement

Etherisc develops a decentralized insurance protocol to collectively build insurance products.

A common infrastructure, product templates and insurance license-as-a-service make a platform that allows anyone to design, launch and distribute their own insurance products.

As a result, independent workers and risk capital providers earn fair share of created value, regardless of age, wealth, or personal connections.

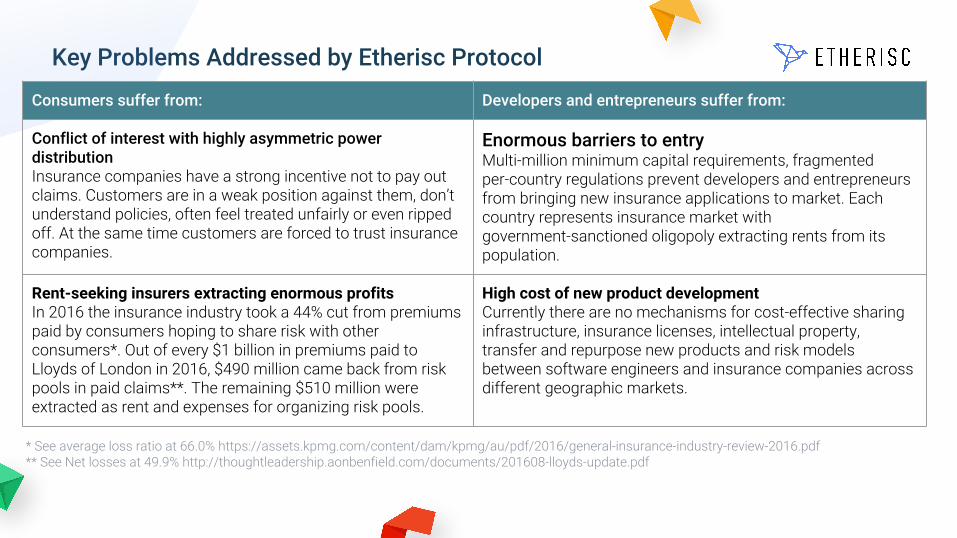

Key Problems Addressed by Etherisc Protocol

Consumers suffer from: Developers and entrepreneurs suffer from:

Conflict of interest with highly asymmetric power distributionInsurance companies have a strong incentive not to pay out claims. Customers are in a weak position against them, don’t understand policies, often feel treated unfairly or even ripped off. At the same time customers are forced to trust insurance companies.

Enormous barriers to entryMulti-million minimum capital requirements, fragmented per-country regulations prevent developers and entrepreneurs from bringing new insurance applications to market. Each country represents insurance market with government-sanctioned oligopoly extracting rents from its population.

Rent-seeking insurers extracting enormous profitsIn 2016 the insurance industry took a 44% cut from premiums paid by consumers hoping to share risk with other consumers*. Out of every $1 billion in premiums paid to Lloyds of London in 2016, $490 million came back from risk pools in paid claims**. The remaining $510 million were extracted as rent and expenses for organizing risk pools.

High cost of new product developmentCurrently there are no mechanisms for cost-effective sharing infrastructure, insurance licenses, intellectual property, transfer and repurpose new products and risk models between software engineers and insurance companies across different geographic markets.

* See average loss ratio at 66.0% https://assets.kpmg.com/content/dam/kpmg/au/pdf/2016/general-insurance-industry-review-2016.pdf** See Net losses at 49.9% http://thoughtleadership.aonbenfield.com/documents/201608-lloyds-update.pdf

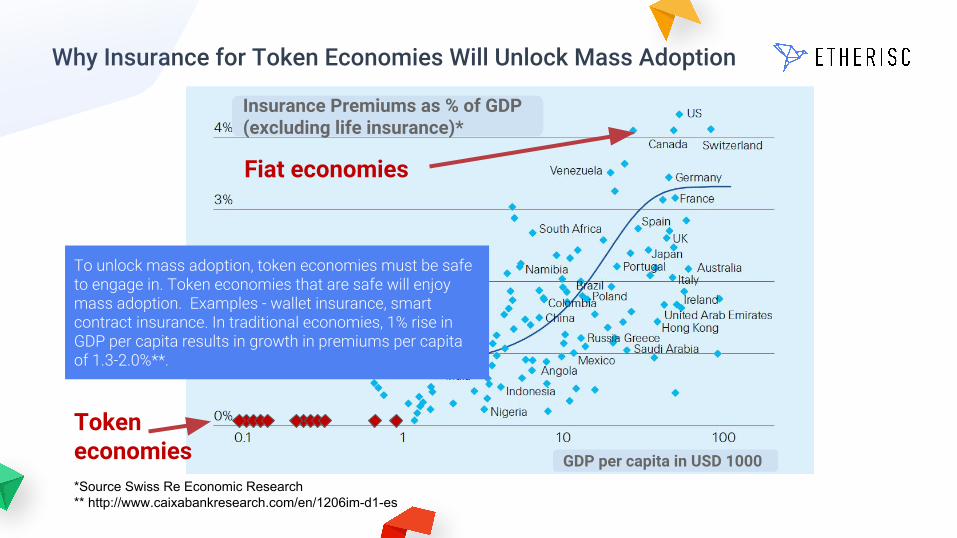

Why Insurance for Token Economies Will Unlock Mass Adoption

Fiat economies

*Source Swiss Re Economic Research** http://www.caixabankresearch.com/en/1206im-d1-es

Token economies

To unlock mass adoption, token economies must be safe to engage in. Token economies that are safe will enjoy mass adoption. Examples - wallet insurance, smart contract insurance. In traditional economies, 1% rise in GDP per capita results in growth in premiums per capita of 1.3-2.0%**.

GDP per capita in USD 1000

Insurance Premiums as % of GDP (excluding life insurance)*

The Solution: Blockchain and Smart Contracts

Immutable and incorruptible smart contracts decide about policy underwriting and payouts

DIP utility token: Staking DIP as incentive to provide great service for customers (cf. Augur REP, Numerai)

Risk Pool Tokens make risks tradable on exchanges, the blockchain version of Insurance Linked Securities

Oracles with authoritative data for parametric insurance

Decentralized oracles to incentivize claims assessors

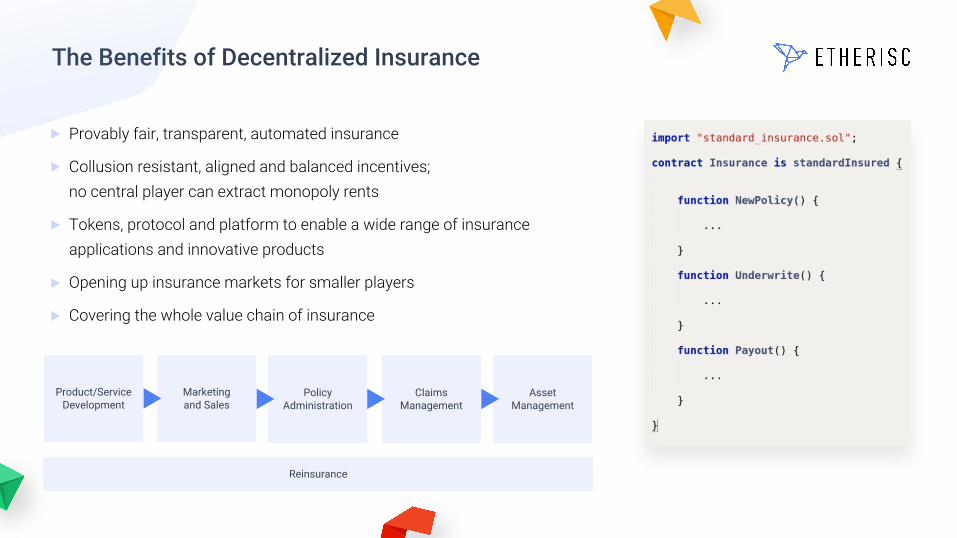

The Benefits of Decentralized Insurance

Provably fair, transparent, automated insurance

Collusion resistant, aligned and balanced incentives; no central player can extract monopoly rents

Tokens, protocol and platform to enable a wide range of insurance applications and innovative products

Opening up insurance markets for smaller players

Covering the whole value chain of insurance

Product/Service Development

Marketingand Sales

PolicyAdministration

ClaimsManagement

AssetManagement

Reinsurance

Revenue Model For Protocol Users and Crypto Investors

Claims paid

Insureds

Up to $2300

Risk Pool$800 + $1500

of leverage

Premium

$1000

Premium-fee

$900

Reinsurance Market

Claims, if primary Risk Pool is depleted

Reinsurance Premium

Risk Pool Tokens (optional)

Tokenized Risk (Insurance Linked

Security)

OR

Stake$1500

Get $100 Reinsurance Premium + release of stake after 12 months

Organizes new product development, earns % of premium, underwriting

profit

Keeper Registry

Fixed Fee, configured by Keeper and Distributor

$100(Developers, Distributors...)

Sovereign Workers

Earns fee per oracle call, API call, or processed

claim

Oracles Registry(Pricing/Claims)

Earns %of premium for renting licenses, filing

compliance reports

Licence Provider Registry

Earns % of premium or fixed fee for distributing

to consumers

DistributorRegistry

Earn interest on staked ETH, BTC, USD without

selling the staked assets

Sovereign Investors

Up to $1500

$100

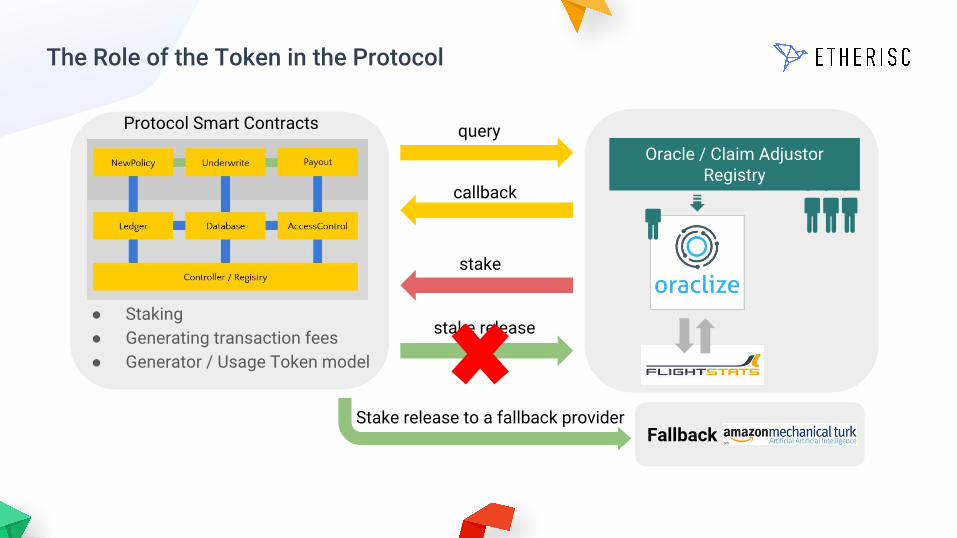

query

callback

stake

Fallback

Protocol Smart Contracts

Oracle / Claim Adjustor Registry

stake release

Stake release to a fallback provider

The Role of the Token in the Protocol

● Staking● Generating transaction fees● Generator / Usage Token model

User Who are these users? What can such user get as a result of using Etherisc? Why does this user need to hold Etherisc Token (DIP)?

Keepers Keepers collectively maintain the network by creating and managing risk pools. Examples: Developers and data scientists, entrepreneurs with ideas of insurance products who can organize teams and most existing insurtech startups.

Examples of Keepers currently operating on Etherisc Protocol - HurricaneGuard.io https://fdd.etherisc.com

Earn transaction fees (which Keepers set on their own). Keepers can set the following Transaction Fees: % of premium % of underwriting profits% of investment income on float

Examples of transaction fees - which Etherisc team operates Flight Delay Insurance https://fdd.etherisc.com as a Keeper, charging 5% transaction fee on premiums of insurance.

Every user earning transaction fees (percentage of revenue or profits generated by insurance products), must hold and stake DIP token worth of 15-25% of their annual earnings as a bond ensuring availability, quantity and completion of their services.

Staking DIP token replaces the need to enter/enforce services agreements using contract law and court systems of countries where users reside. Many users will not be associated with any country.

Stake is released after service period (30-365 days) is lapsed without a challenge by the Monitoring Oracle or Keeper.

DIP token effectively disintermediates trust between network participants because it replaces the legacy trust model powered by jurisdiction-specific contract agreements.

License providers

Insurance fronting services like AIG, Zurich, State National, Atlas Insurance PCC, Clear Blue, etc.

Earn transaction fees which are set by license provider as % of premium charged for renting licenses (insurance fronting). Typical fee currently charged in the US and EU is 3%-7% of revenue.

Pricing, Claims Oracles, Underwriters

- Full stack developers and UI/UX designers- Data scientists with risk models - Data providers - Claim adjustment services (aka Third Party Administrators)

Earn transaction fees for their service (for example for setting up a trusted data feed to pricing algorithm, or estimating the loss under policy (adjusting claims).

Relayers - Entrepreneurs and technology companies with large user base (mobile apps, wallets)- Crypto protocols, platforms and dApps- Established insurance companies

Relayers are distributors who earn one or more of the following: % of premium (transaction fee)% of underwriting profits

Risk capital providers

- Individual crypto-investors interested in passive income or security tokens- Hedge funds- Institutional investors

Investors earn passive reinsurance income on existing assets (ETH, BTC, USD) by buying risk pool tokens, without selling the staked assets.

To access tokenized risk pools, investors must hold DIP token IF such risk pool was configured by the Keeper to be accessible to DIP holders.

Users, their motivation, reasons to hold token

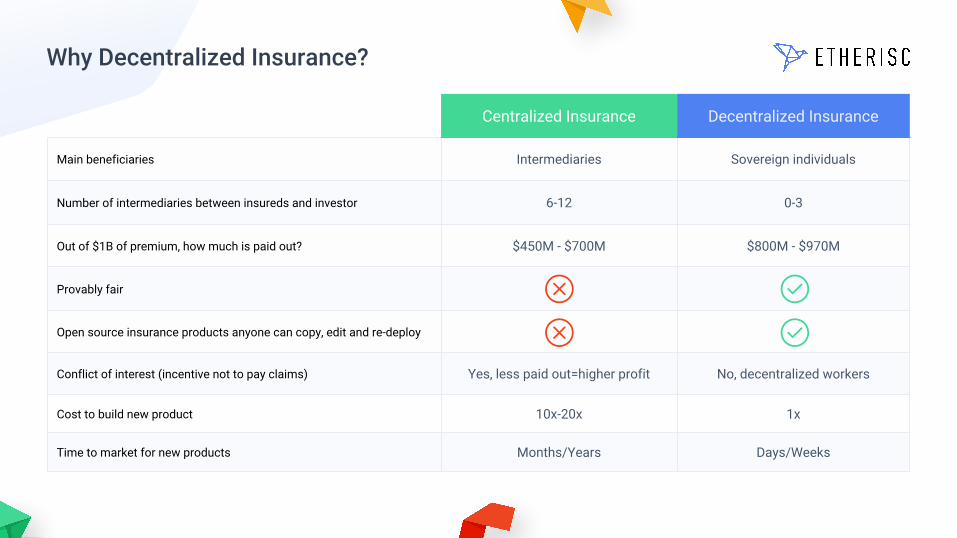

Why Decentralized Insurance?

Centralized Insurance Decentralized Insurance

Main beneficiaries Intermediaries Sovereign individuals

Number of intermediaries between insureds and investor 6-12 0-3

Out of $1B of premium, how much is paid out? $450M - $700M $800M - $970M

Provably fair

Open source insurance products anyone can copy, edit and re-deploy

Conflict of interest (incentive not to pay claims) Yes, less paid out=higher profit No, decentralized workers

Cost to build new product 10x-20x 1x

Time to market for new products Months/Years Days/Weeks

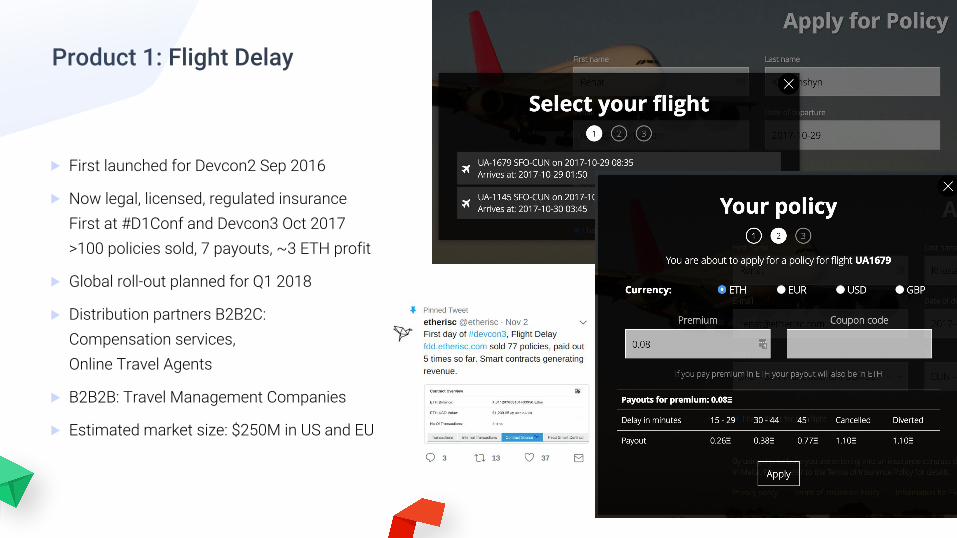

Product 1: Flight Delay

First launched for Devcon2 Sep 2016

Now legal, licensed, regulated insuranceFirst at #D1Conf and Devcon3 Oct 2017>100 policies sold, 7 payouts, ~3 ETH profit

Global roll-out planned for Q1 2018

Distribution partners B2B2C: Compensation services, Online Travel Agents

B2B2B: Travel Management Companies

Estimated market size: $250M in US and EU

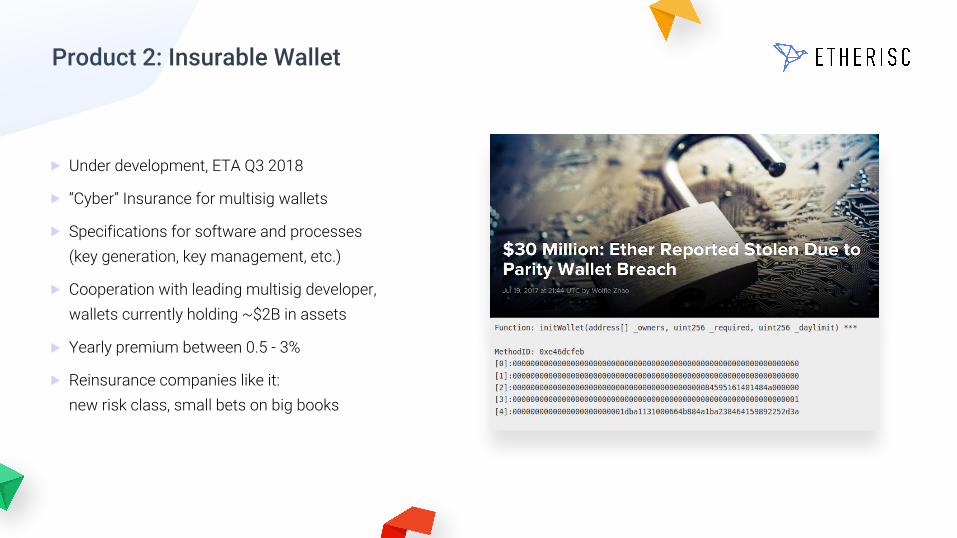

Product 2: Insurable Wallet

Under development, ETA Q3 2018

“Cyber” Insurance for multisig wallets

Specifications for software and processes(key generation, key management, etc.)

Cooperation with leading multisig developer,wallets currently holding ~$2B in assets

Yearly premium between 0.5 - 3%

Reinsurance companies like it: new risk class, small bets on big books

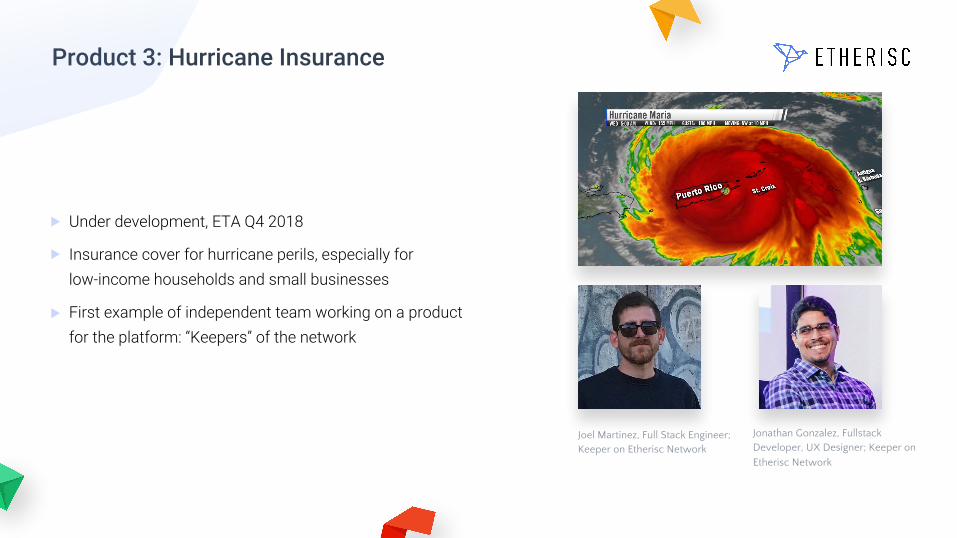

Joel Martinez, Full Stack Engineer; Keeper on Etherisc Network

Jonathan Gonzalez, Fullstack Developer, UX Designer; Keeper on

Etherisc Network

Product 3: Hurricane Insurance

Under development, ETA Q4 2018

Insurance cover for hurricane perils, especially for low-income households and small businesses

First example of independent team working on a product for the platform: “Keepers” of the network

Platform Value and Commercial Entities

DIP token represents platform value, market cap increases with usage

Protocol and platform development bootstrapped by the DIP tokenand maintained by the DI foundation, incorporated 22 Dec 2017 in Zug, CH

Commercial insurance entities owned by the foundation

Sell insurance products to customers

provide sub-licenses for third parties

Current focus on Malta PCC/SCC structures

Community and Cooperations

Aigang: Focus on IoT solutions, similar mindset, protocol and platform, token sale. Main difference is regulatory strategy, cooperation possible.

iXledger, Blocksure: Focus on insurance companies as customers, cost reduction and efficiency gains, cooperations planned.

Chainthat, Surematics: Service providers for existing insurance industry, focus on cost reduction and efficiency gains, no systemic change.

Nexusmutual, Wetrust focus on cooperative models.

We chair the Insurance Working Group of Enterprise Ethereum Alliance

We organized #D1Conf Oct 31 in Cancun as the first conference dedicated to decentralized insurance development, https://d1conf.com.

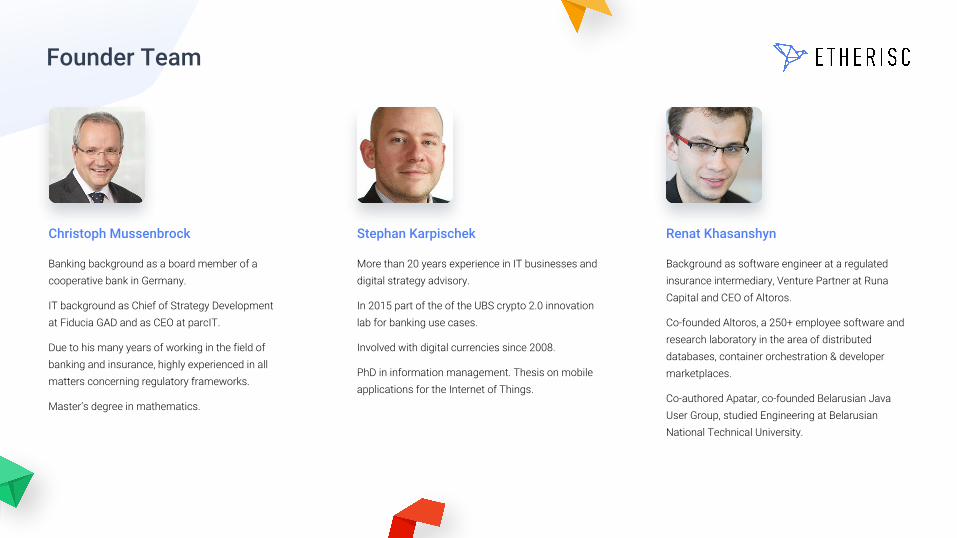

Founder Team

Christoph Mussenbrock

Banking background as a board member of a cooperative bank in Germany.

IT background as Chief of Strategy Development at Fiducia GAD and as CEO at parcIT.

Due to his many years of working in the field of banking and insurance, highly experienced in all matters concerning regulatory frameworks.

Master’s degree in mathematics.

Stephan Karpischek

More than 20 years experience in IT businesses and digital strategy advisory.

In 2015 part of the of the UBS crypto 2.0 innovation lab for banking use cases.

Involved with digital currencies since 2008.

PhD in information management. Thesis on mobile applications for the Internet of Things.

Renat Khasanshyn

Background as software engineer at a regulated insurance intermediary, Venture Partner at Runa Capital and CEO of Altoros.

Co-founded Altoros, a 250+ employee software and research laboratory in the area of distributed databases, container orchestration & developer marketplaces.

Co-authored Apatar, co-founded Belarusian Java User Group, studied Engineering at Belarusian National Technical University.

Advisors

Ron Bernstein Ralf Glabischnig William Mougayar

Jake Brukhman Tobias Noack Daniel Zakrisson

Journey so far

Christoph and Stephan met on the 2030 Slack in discussing insurance on the blockchain

July

First version of the Flight Delay Dapp was born,

presented at the Ethereum developer conference Devcon2 in Shanghai

September

Crop insurance proved that smart contracts can reduce operational costs to enables new markets

October

1 of 4 2016

Journey so far

Winner Blockchain startup contest, sharing the main

prize with Status.

November

First whitepaper on decentralized insurance markets. Most-funded project at hack.ether.camp.

December

Prototype for social insurance on blockchain at

Blockchain Virtual GovHack in UAE

January

Blockchain Oscar for “Most Innovative Blockchain Startup”

April

2 of 4

2017

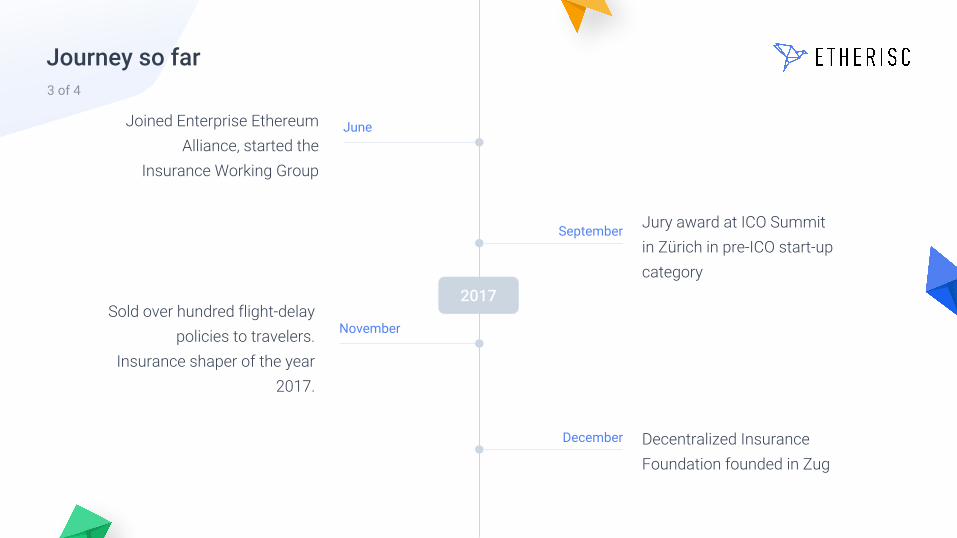

Journey so far3 of 4

Joined Enterprise Ethereum Alliance, started the

Insurance Working Group

June

Jury award at ICO Summit in Zürich in pre-ICO start-up category

September

Sold over hundred flight-delay policies to travelers.

Insurance shaper of the year 2017.

November

Decentralized Insurance Foundation founded in Zug

December

2017

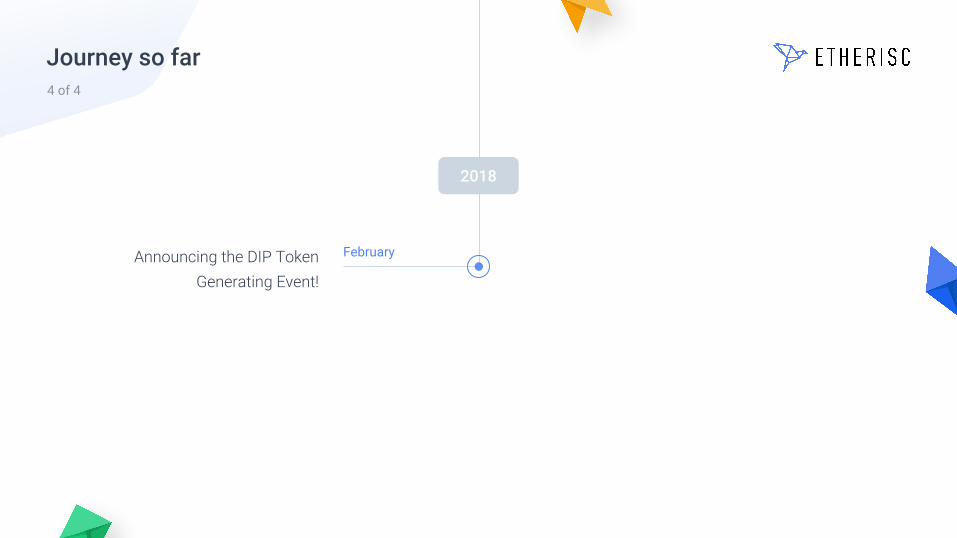

Journey so far4 of 4

Announcing the DIP Token Generating Event!

February

2018

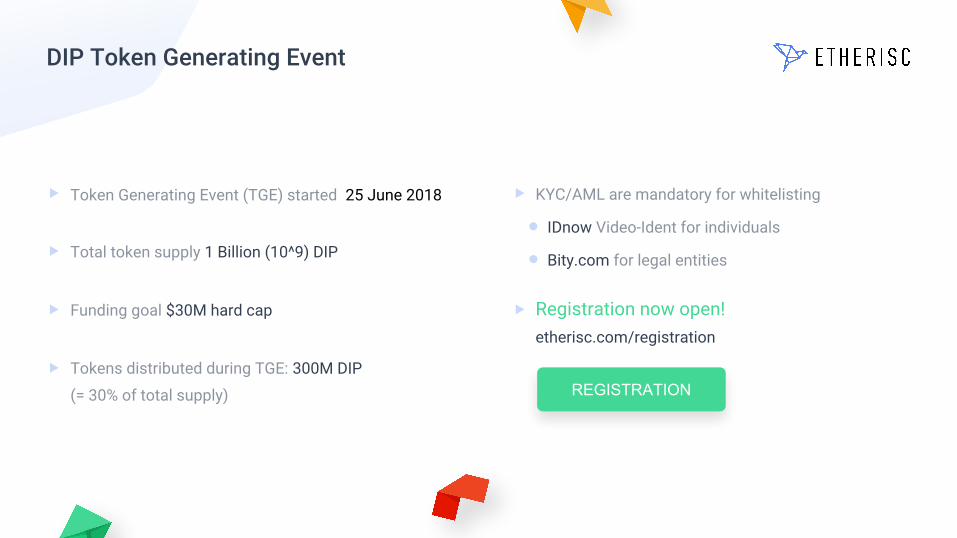

DIP Token Generating Event

Token Generating Event (TGE) started 25 June 2018

Total token supply 1 Billion (10^9) DIP

Funding goal $30M hard cap

Tokens distributed during TGE: 300M DIP

(= 30% of total supply)

KYC/AML are mandatory for whitelisting

IDnow Video-Ident for individuals

Bity.com for legal entities

Registration now open!etherisc.com/registration

REGISTRATION

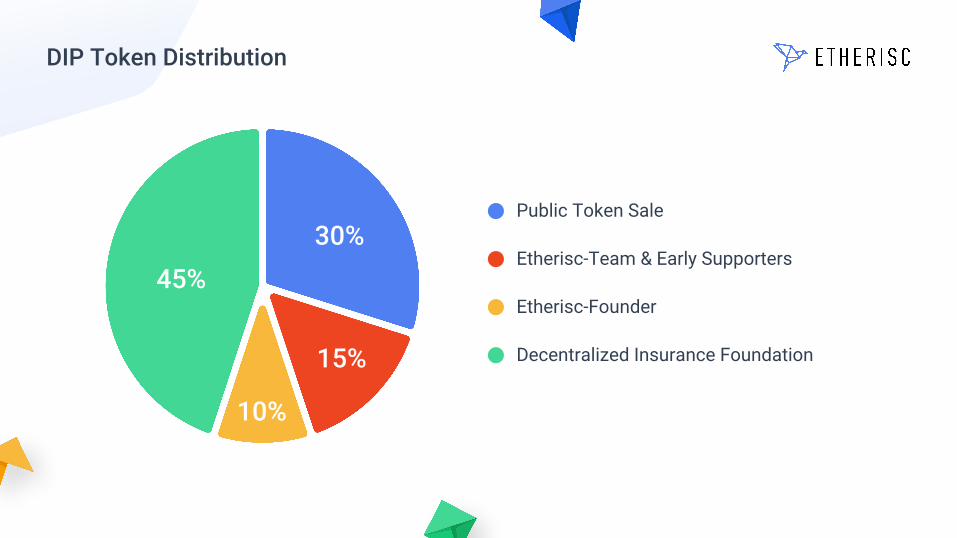

DIP Token Distribution

Public Token Sale

Etherisc-Team & Early Supporters

Etherisc-Founder

Decentralized Insurance Foundation

45%

10%

15%

30%

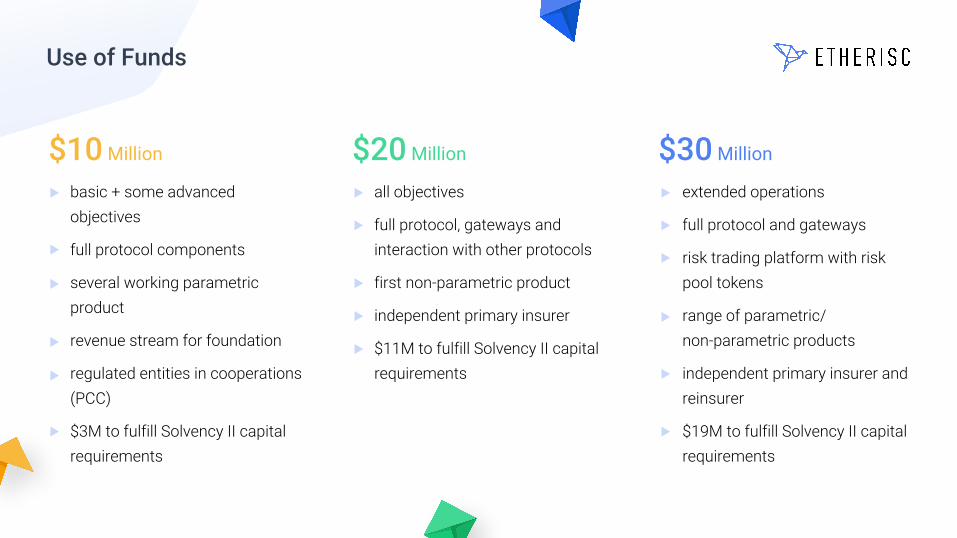

Use of Funds

$10 Million $20 Million $30 Million

basic + some advanced objectives

full protocol components

several working parametric product

revenue stream for foundation

regulated entities in cooperations (PCC)

$3M to fulfill Solvency II capital requirements

all objectives

full protocol, gateways and interaction with other protocols

first non-parametric product

independent primary insurer

$11M to fulfill Solvency II capital requirements

extended operations

full protocol and gateways

risk trading platform with risk pool tokens

range of parametric/ non-parametric products

independent primary insurer and reinsurer

$19M to fulfill Solvency II capital requirements