integrated cad/cae i - kingsfield consulting€¦ · integrated cad/cae for example, ... in the...

TRANSCRIPT

INTEGRATED CAD/CAE

For example, in their paper “Spotlight onoil and gas megaprojects”, Ernst & Young

advised and foresaw that “the oil and gas in-dustry is witnessing an unprecedented waveof capital spending, driven by the need tobuild capacity to meet growing energydemand from emerging markets and toreplace depleting supply sources. Thiscapital expenditure has, to date, beenunderpinned by consistently higher oilprices, globally and gas prices outside NorthAmerica. This trend is expected to continue”(1). Reality though, turned out to be quitedifferent.The impact of the oil price collapse hasmigrated to other industrial plant con-struction sectors not normally directlyaffected by oil price fluctuations and this,together with depressed commodity prices,

is having a profound impact on the E&C in-dustrial plant sector.In the same paper, Ernst & Young presentedthe results of a study aimed to understandthe challenges associated with the deliveryof megaprojects in the Oil & Gas industry.The key findings were (among others):S 64 percent of the projects are facing cost

overruns73 percent of the projects are reportingschedule delays59 percent higher completion costs.

These findings are consistent with otherresearch, including Edward Merrow in 2011(2), which not only considered Oil & Gasprojects but also other industrial plant projects. The combination of under-performingprojects and the abrupt drop in oil and commodity prices has created a crisis.

Tricad MS provided by VenturislT GmbHbased in Bad Soden, Germany. Last but notleast, a convincing factor was the scope ofapplication of this tool family.

Data consistency guaranteedTricad MS with its diversity of designmodules is unique worldwide as an ‘allinclusive’ CAD/CAE solution: A product forall disciplines in building, factory and plantplanning technologies (HVAC, electricity,sanitary, transport technology, steel con-struction, painting technology, and so on).This is an important advantage; even if thedesigner has to work in widely diverse pro-jects, different tools are not necessary andhe can always remain in familiar surround-ings. A small design office or a medium-sized EPC can therefore cover all trades anddisciplines. The method of working is thesame in each module, at the same time thedata are universally available — they onlyneed to be entered once. “That makesworking in a team very much easier, theworkflow is more secure as the dataconsistency is ensured”, said SaschaKühner, Sales Manager for Plant Planningtools with VenturislT.Simply set up, working with Tricad MS canbe learned in a few days, Mr Kühner said:“Each module is structured in the same way— if you know one module, you know themall! All components are available in a pa-

L rametrisable geometry which can be configured as desired. All technical informationcan be called up via an information buttonwithout Tricad MS having to be running atthe time.”Essential advantages in the design processwith this 3D CAD/CAE solution are (shortlist):

Modifications can be implemented muchmore quickly

Thomas Koller

Planning efforts required for new projectsdrops significantlyCollisions can be almost completelyexcluded by the plant designIntegral and coupled calculation methodssupport the design processUniform ‘look & feel’ in all modules.

A special feature for plant designer in thefield of energy production is working withthe specification in accordance with the KKSsystem (power plant identification system) —

with this tool it is possible, for example, todetect in which part of the plant a particularvalve is installed.What convinced Mr Koller and the boardabout Tricad MS? — in addition to the generalengineering tool requirements already men-tioned. It was especially the proximity of thegood support to be expected (not unimportant: German language!). This expectation has obviously been fulfilled, asMr Koller confirmed: “The developers atVenturislT have implemented a very flexibleadaptation of the software to our needs”. Asa special example, the copy functions in theschematics module have been extended andimproved; in the schematic lists, the pro-grammers have implemented a coordinateinput for objects. A hanger design has alsobeen made possible using the Lisegasystem. The implementation of an AKSstructure (KKS in accordance with VGB stan-dard) was also important to the Caliqua designers. Mr Koller appreciates also the goodoverall price/performance ratio in terms ofprocurement, licence, customising, maintenance and training.Renergia Zentralschweiz has erected a newrefuse incineration plant as a replacementfor the previous 40-year old plant in the cityof Lucerne, Switzerland. The location of theplant next to the paper mill of Perlen Papier(PEPA) is ideal as the paper production

requires large amounts of heat as well as aconstant, secure supply of power. Thanks tothe new incineration plant, PEPA can reduceits heating oil requirement by 40 millionlitres per year and lower the CO2 emission by90 000 metric t.In November 2012, Renergia awardedCaliqua the contract for supplying the com

I plete thermal plant and the remote steamc line to PEPA. The contract included a 28 MW

: steam turbine, the air-cooled condenser withQ-

a rated power of around 62 MW, the remotesteam line to PEPA to supply a rated 75 t/hand the option for 22 MW district heatingsupply including three hot water storagetanks, each with 100 m3 capacity. Contractvalue: around 30 million CHF. Mr Kollerremembered: “We started the 3D planningwith Tricad MS immediately without anygreat preparation, although the tool had onlybeen introduced in-house a short timebefore. The team therefore had to learn andmaster an almost completely new engineering tool on the basis of the MicroStationCAD system — including the optionallyconnectable database function of Tricad MS.This also included generating the requiredpipe classes in the material database.” Thechoice of Tricad MS proved to be a success:“It showed, as declared by the vendor, that arapid, productive use is really possible aftera short period of training. It is also possibleto select whether a project can be pro-cessed with or without database; thedatabase can even be used later on.”Was the decision in favour of Tricad MS thenthe right one? Does Mr Koller recommendthis tool? “We are very satisfied with TricadMS. Particularly the use of the Piping 3Dmodule was problem-free from the very be-ginning. We are able to usefully supplementthe planning with the additional modulesSteel Construction, Ventilation 3D andElectrical 3D. Creating isometrics withIsogen can be well utilised with properplanning.” However, there is room for improvement in the sheet adaptation by theadministration.But nobody is perfect: In the Schemamodule, there were greater problems initiallyin the implementation of the KKS identification and KKS management in the AKSdatabase and in the data exchange with theVDB, which the vendor could only graduallyadapt to the needs of the designer. MrKoller: “The management and assignment ofthe KKS identification could still be moreuser-friendly; we are still losing too muchtime here.” Perhaps the Windows ‘drag &drop’ functionality could ease this problemhere — Mr KUhner gave the assurance thatthe programmers are working on this.

HANS-JORGEN BITTERMANN

Sascha Kühner

/. r

The unexpected rapid

decline in the oil price

has triggered circum

stances that could not

have been foreseen one

year ago. In 2014 indus

try commentators were

predicting a very

different situation,

writes ANDRÉ L. MARTINS

Satisfied with Tricad MSThe Tricad MS modules used at Caliqua are Schema-Pipe 2D, Piping 3D, Pipe Class Manage-ment, Venturis database, Isogen, Steel Construction, Electrical 3D, and Ventilation 3D.www.venturisitde

24 economicPLANT 3-2015 economicPLANT 3-2015 45

DIGITAL PLANT COST CONTROL

What do plant designer expect most fromtheir engineering tool? Those, like

Thomas Koller, Design Manager with theBasle-based Caliqua, who have had goodand not-so-good experience with tools overthe years, has very clear ideas: Theseinclude functional requirements (datareconciliation between P&ID and 3D modeland display of changes, revision manage-ment/archiving of models, easy editing!

maintenance of database information); onthe other hand that the easy operation is justas important as multi-user capabilities. Oneexpectation that stands out from all others:“An engineering tool must create the highestpossible productivity for our planners!”Founded in 1931, Caliqua regards itself a theleading provider in Switzerland of thermalplants for municipal service providers andfor industry: With its 88 employees, the com

pany implements energy centres for wasteincineration plants, combined heat andpower plants, CCPP plants, plants for theutilisation of biomass and geothermal energy, district heating centres and steam distribution networks. A further focus is pipe-line construction for the process industry.The decision four years ago to replace thevarious existing tools by another, unifiedengineering tool was made in favour of

Consequences for the industryIn a recent study, Morgan Stanley andBoston Consulting Group suggested that“The new period of cheap oil and ample sup-plies brought about by the boom in U.S.shale has raised a prospect unthinkable asrecently as a few months ago — that theworld no longer needs all the big, expensiveprojects planned by companies includingShell, Total and Exxon” (3). Indeed, at the Eu-ropean Construction Institute (ECI) con-ference in June 2015, Frank van Ewijk, General Manager for Project Controls with Shelladvised that “costs of new capital projectshave increased over the last decades, andthe need to turn this around has only beencompounded by the decreasing oil price overthe last year” (4). The culmination of thesefactors means projects are not affordableanymore.In the same study Morgan Stanley andBoston Consulting Group opined that“companies needed to ‘undergo a dramatic’drop in costs and, even more importantly,change the culture to sustain savings. Big Oilstill lacks a truly cost-conscious culture” (5).Clearly, the high price of oil and commod

ities has been a disincentive to generating asufficiently cost-conscious culture.That the industry is in crisis is not in doubt.However, does this mean all doom andgloom? Not if we follow the view of NiccoloMachiavelli, “that crises shake people out oftheir complacency, create opportunities tochallenge conventional wisdom and giveleaders some room to take on vestedinterests and achieve transformative

67%

68 %

may be the catalyst for a long neededchange as advocated by Morgan Stanley andBoston Consulting.The CEO of a leading EPC contractor observed recently that “the times ofcontinuous growth are a thing of the past”and commented that, in addition to thecollapsed oil price and the combination ofthe project delays, cost overruns anduncertainty of project outcomes, “thevolatility of individual economic regions has

-‘ E&CIndustrial Plantindustry: a changing world

Cal/qua was awarded the contract for supplying a completethermal plant including a remote steam line

Andrd L. Martins

$ 140

Brent Crude Prices

$ 120

$ 100

$80. $60

$40

Proportion of post-FID projects facing overruns

35 %

Engineering toolfires up energy

.

plant designerThe structure of the energy generation will also change in Switzerland due to a

dedicated ‘Energy Strategy 2050’ plan: The five existing nuclear power stations

will be shut down, smaller decentralised units based on renewable energy

sources and efficient storage technologies will gain in importance. Caliqua pro-

fits from this — and is increasing the productivity of its design process with the

Tricad MS engineering tool.

$20

$0Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-15 Oct-15

-•1I

(1)

; ‘Overrun

65 %On budget

62 %65 %

Proportion of projects facing cost overruns,schedule delays, and average project budget overruns

Proportion of projectofacing cost overruns

Proportion of projectsfacing schedule delays 79 %

78%

. L 70%Average protect ‘IhOl- —

budgetoverrsns 69 /o

53%

0% 20% 40% 60% 80% 100%

LNG • Pipeline Refining upstream— -

change”. A positive approach to this crisis

44 economicPLANT 3-2015 economicPLANT 3-2015 25

ECONOMICS NEXT GENERATION OF VISUALISATION

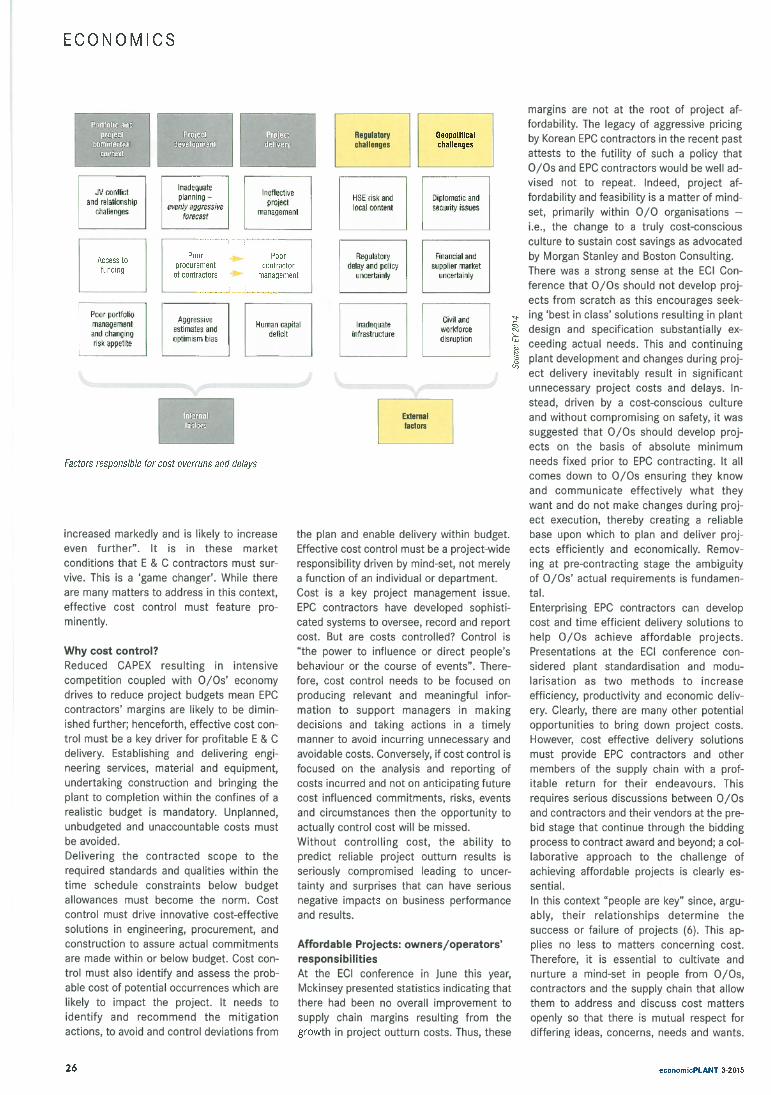

increased markedty and is likely to increaseeven further”. It is in these marketconditions that E & C contractors must survive. This is a ‘game changer’. While thereare many matters to address in this context,effective cost control must feature pro-minently.

Why cost control?Reduced CAPEX resulting in intensivecompetition coupled with 0/Os’ economydrives to reduce project budgets mean EPOcontractors’ margins are likely to be diminished further; henceforth, effective cost con-trol must be a key driver for profitable E & Cdelivery. Establishing and delivering engineering services, material and equipment,undertaking construction and bringing theplant to completion within the confines of arealistic budget is mandatory. Unplanned,unbudgeted and unaccountable costs mustbe avoided.Delivering the contracted scope to therequired standards and qualities within thetime schedule constraints below budgetallowances must become the norm. Costcontrol must drive innovative cost-effectivesolutions in engineering, procurement, andconstruction to assure actual commitmentsare made within or below budget. Cost con-trol must also identify and assess the probable cost of potential occurrences which arelikely to impact the project. It needs toidentify and recommend the mitigationactions, to avoid and control deviations from

Externalfactors

the plan and enable delivery within budget.Effective cost control must be a project-wideresponsibility driven by mind-set, not merelya function of an individual or department.Cost is a key project management issue.EPC contractors have developed sophisticated systems to oversee, record and reportcost. But are costs controlled? Control is“the power to influence or direct people’sbehaviour or the course of events”. There-fore, cost control needs to be focused onproducing relevant and meaningful information to support managers in makingdecisions and taking actions in a timelymanner to avoid incurring unnecessary andavoidable costs. Conversely, if cost control isfocused on the analysis and reporting ofcosts incurred and not on anticipating futurecost influenced commitments, risks, eventsand circumstances then the opportunity toactually control cost will be missed.Without controlling cost, the ability topredict reliable project outturn results isseriously compromised leading to uncertainty and surprises that can have seriousnegative impacts on business performanceand results.

Affordable Projects: owners/operators’responsibilitiesAt the ECI conference in June this year,Mckinsey presented statistics indicating thatthere had been no overall improvement tosupply chain margins resulting from thegrowth in project outturn costs. Thus, these

margins are not at the root of project affordability. The legacy of aggressive pricingby Korean EPC contractors in the recent pastattests to the futility of such a policy that0/Os and EPC contractors would be well ad-vised not to repeat. Indeed, project affordability and feasibility is a matter of mind-set, primarily within 0/0 organisations —

i.e., the change to a truly cost-consciousculture to sustain cost savings as advocatedby Morgan Stanley and Boston Consulting.There was a strong sense at the ECI Con-ference that 0/Os should not develop projects from scratch as this encourages seek-

: ing ‘best in class’ solutions resulting in plantdesign and specification substantially ex

‘ceeding actual needs. This and continuing

I plant development and changes during project delivery inevitably result in significantunnecessary project costs and delays. In-stead, driven by a cost-conscious cultureand without compromising on safety, it wassuggested that 0/Os should develop projects on the basis of absolute minimumneeds fixed prior to EPC contracting. It allcomes down to 0/Os ensuring they knowand communicate effectively what theywant and do not make changes during project execution, thereby creating a reliablebase upon which to plan and deliver projects efficiently and economically. Removing at pre-contracting stage the ambiguityof 0/Os’ actual requirements is fundamental.Enterprising EPC contractors can developcost and time efficient delivery solutions tohelp 0/Os achieve affordable projects.Presentations at the ECI conference con-sidered plant standardisation and modularisation as two methods to increaseefficiency, productivity and economic delivery. Clearly, there are many other potentialopportunities to bring down project costs.However, cost effective delivery solutionsmust provide EPC contractors and othermembers of the supply chain with a profitable return for their endeavours. Thisrequires serious discussions between 0/Osand contractors and their vendors at the prebid stage that continue through the biddingprocess to contract award and beyond; a collaborative approach to the challenge ofachieving affordable projects is clearly essential.In this context “people are key” since, arguably, their relationships determine thesuccess or failure of projects (6). This applies no less to matters concerning cost.Therefore, it is essential to cultivate andnurture a mind-set in people from 0/Os,contractors and the supply chain that allowthem to address and discuss cost mattersopenly so that there is mutual respect fordiffering ideas, concerns, needs and wants.

A to read in a corresponding pressrelease, the vendor is committed to

I extending the ways in which its clients canaccess and interact with their Digital Assets,the information coreof every project or operating asset. Entirelytouch driven, and capable of running on thelargest format touch screens, Aveva Engageseamlessly combines powerful whole-modelvisualisation with immediate contextually-filtered access to validated, relevant documents and information. By putting the rightinformation directly at the fingertips ofdecision makers, precisely when and wherethey need it, the user can design, review,plan and execute work safely and efficiently.“Aveva Engage redefines what is possible inengineering”, said Dave Wheeldon, CTO withthe vendor during his presentation at the

World Summit, adding: “Delivering qualityinformation through a highly intuitive in-terface, Aveva Engage gives users immediate access to the wealth of resources withintheir Digital Asset. Simple and dynamic, itsunrivalled touch user experience is bothvisually breathtaking and amazingly insight-ful when combined with the huge UHDtouch-screen devices available today.Presenting information that resides in aDigital Asset in its full context is invaluableto EPCs and OOs. Early adoption of this tech-nology has clearly demonstrated just howgame-changing Aveva Engage can be to ourcustomers’ business.”Over the past six months, ten companieshave enrolled on the Early Access Pro-gramme (EAP) across the Oil & Gas, Power,and Mining sectors, taking a voyage to

realise the full potential of the provided newtechnology and to redefine the ‘Future ofDecision Support’.

‘The best in industry’Robert Samudio, Global Design/DraftingManager, Shell New Orleans, who hasworked with the vendor on the developmentof Aveva Engage, added, “We have workedwith Aveva for over 25 years in close part-nership, creating outstanding and essentialtechnologies, that have driven our industry.With Aveva we have pioneered touch-screentechnology and the ability to use 3D modelswith other disciplines across globallocations. We can use it for collaboration,decision-making and safety. It will help us todeliver multi-billion dollar projects, settingindustry benchmarks for quality, cost andspeed. More importantly, it will change theway we work, our processes, our tools, ourcollaboration and the promise on how wedeliver our projects. Our relationship withAveva is the best in the industry.”There were also comments during thelaunch in Dubai from Richard Longdon, CEOwith the vendor: “Aveva Engage reaffirms[our] position as a leader in the market bydelivering innovation that solves real-worldproblems for our customers.” And thefeedback the vendor received from itscustomers has been absolutely amazing.“From the moment they step up to a largetouch screen and begin engaging with theapplication, they instantly understand thebenefits of Aveva Engage. They are con-stantly suggesting new areas of theirbusiness that could benefit from thisdecision-support approach,” the CEO saidemphatically. The mission is to create tech-nology that is constantly pushing theboundaries of what customers can achieveand Aveva Engage is a great example of whatthe vendor can do by working together.A preview of the project, at that time code-named ‘Voyager’, was shown during the‘Glimpse into the Future’ session at theWorld Summit a year before, in Berlin.www.aveva.com

. . .

: c;’ Regulatory Geopoliticalr1!L4e 111fl

DIGITAL PLANT COST CONTROL

During its World Summit in Dubai, UAE, Aveva plc based in Cambridge, UK,

released Aveva Engage, a brand-new collaborative decision-support solution for

capital projects and operating assets. It combines the power of instant access to

a Digital Asset’s full contextually-integrated information with an impressively

simple and entirely intuitive touch-driven interface, all visualised and navigable

in a Ultra-High Definition (UHD) whole-model view. As part of the vendor’s

‘Future of Decision Support’ programme, Aveva Engage is bringing a new

dimension to decision support for better, faster decisions across the life cycle.

In the end it is vital to understand andaccept that all organisations are in businessto make money.While EPC contractors could and should playa leading role, it is for 0/Os to take the initiative to make their projects affordable.

Focus to be changedIn his guide to cost/schedule controlsystems criteria (C/CSC) Quentin W.Fleming expressed a view with which webelieve many industry professionals canassociate with “there are probably fewthings in life which will alienate theboss/worker relationship quicker than thatof being late on finishing a job, or of spending more money to complete it than wasoriginally planned” and yet the E & C Industrial Plant sector has a history of delayed andover budget projects (7). Why?Recognising that this is an engineering-ledindustry Fleming offers some explanation:“Some of the very smart people in today’sbusiness environment are engineers.Engineers, by nature are typically creativepeople who thrive on new ideas, oftenpushing the state of the technical arts. Mostengineers and scientists by education andexperience have spent a lifetime with an emphasis on the merits of high technical performance. Therefore, it is almost instinctiveto them that they would emphasize thosethings which seem most natural to them:high technical performance. Thus, when confronted with a choice of setting priorities,they will most likely opt for high technicalperformance, and if need be, at the expenseof both cost and schedule performance.”These seem to be traits exhibited in 0/Os,EPC contractors and vendors and are clearlya barrier to effective cost control and affordable projects.

New objectives to be setHowever, if the engineering focus is changedby challenging engineers to utilise theirexpertise and experience in developing innovative cost-effective and time efficientsolutions geared to actual business requirements for plant design and specification,then two key barriers to effective cost control would be dismantled.This is a management issue in setting objectives. In this context, since engineerstend to see their contributions in terms ofcapacity and efficiency and not cost, it is essential to start involving them in costmatters and to make them accountable fortheir design and specification decisions interms of cost implications and budgets.In this context, consider the effect uponowner/contractor relationships if discussions between their respective engineerswere focussed on designs that save rather

than increase costs, it’s a win-win for bothand avoids adversarial debate about liabilityfor cost and who pays. Ultimately, it may enable the 0/0 to save money and the contractor to protect or improve margin.Fleming is no less critical of contractors:“Far too often contractors fail to analyse thevery data they compile each month and obligingly submit to their waiting customers.Far too often the first time contractors takethe necessary actions to assess what theyhave been saying all along is when thatcustomer confronts them with a series ofunfavourable conclusions the customer hasmade on their own, from the very data thecontractor has been providing”. In our experience this happens frequently. It oftenresults from focusing on delivering technicalexcellence rather than assuring delivery inaccordance with the contracted scopewithin approved cost estimates and budgets.This focus, combined with the reluctance toaddress cost and money issues becausepeople are often uncomfortable with thesediscussions, means cost matters are considered as taboo. If contractors are to embrace effective cost control there must be achange in attitude and approach to cost.Contractors must bear in mind that theyhave a fiduciary duty towards 0/Os andtheir own management and shareholders regarding keeping them apprised of, amongstother things, liability for project deliverycosts. This means contractors need to provide accurate and realistic cost estimatesand deliver exactly what they have contracted to do within the approved budgets.Contractors must perform what they arepaid to do, no more and no less. Actual orpotential deviations must be identified early,reported and dealt with in accordance withthe contract terms. Effective cost controldemands that there are no unaccounted forand unattributed costs on projects, otherwise predicable and reliable outturn projectresults are not possible and surprises areinevitable.As a project-wide responsibility, effectivecost control is a continuous process fromproject inception up to completion. It reliesupon realistic estimates and budgets for defined scopes of work and includes accurateassessments of expected delivery conditions, constraints and risks. All of thesemust be continually monitored so that thecontractor knows at any given time, as apriority, how much the project is going tocost and not simply how much it has cost sofar. Applied as an essential managementtool, reliable predicable outturn projectresults indicating deficits against expectations upon entry into the contract providethe opportunity for corrective managementactions; forecast costs can be controlled

whereas actual costs incurred are an immovable fact.

Cost — a common languageIn international E & C Industrial Plant contracting, the differences between culturesare unavoidable and yet a crucial factor inproject delivery. By not managing thesedifferences project delivery and results canbe diminished. Effective communication istherefore vital so that the parties understandeach other and can align on common goalsand objectives.However, achieving economic results seemsto be a common feature of most cultures.Indeed, in any culture it is unlikely that0/Os’ project teams will say they are notconcerned about project prices and contractors’ project teams are invariablyconcerned about project delivery costs.Money in any currency is therefore acommon language. Thus discussions between 0/Os and contractors about projectprices and costs should take and build uponthis common interest which appears totranscend cultural boundaries.

Final considerationsJudging from the Morgan Stanley and BostonConsulting Group report mentioned abovethat “in 1986, after a similar price collapse,major oil companies cut costs and improvedefficiency” history appears to be repeatingitself. Machiavelli’s advice is therefore mostappropriate, take advantage of the fact thatin a crisis, change stops being somethingthat may be done and becomes somethingthat has to be done.The question is therefore, how can youand your organisation benefit from thiscrisis through improved cost control asa contribution to affordable and viableprojects?

REFERENCES

The author is Senior Consultant with KingsfieldConsulting International Ltd based in WestByfleet, UK(1) Corporate paper, 2014,ey.com/oilandgas/capitalprojects(2) Merrow, E. W., “Industrial Megaprojects”,2011(3) “Big Oil: Toughen it Out, Or Business ModelReboot?”, joint corporate paper, 2015, MorganStanley, Boston Consulting Group(4) ECI(5) www.worldoil.com(6) Bakker, Hans L. M., Kleijn, Jaap P.,“Engineering Management of Projects”, 2015(7) Fleming, Quentin W., “Guide to C/CSC”,Chicago 1988kingsf ieldconsulting .com

42 economicPLANT 3-2015 economicPLANT 3-2015 27