integrated transmission plan 2016 - transpower · integrated transmission plan : 2016 1 1....

TRANSCRIPT

INTEGRATED TRANSMISSION PLAN 2016

INTEGRATED TRANSMISSION PLAN : 2016 II

FOREWORD

ITP2016isoursecondstandaloneIntegratedTransmissionPlan(ITP).BuildingonITP2015,itprovidesanupdateonourbusinesstransformationprocessandprovidesourcurrent,bestviewofourRCP2expenditureprogrammes.

WerecentlypublishedanupdatetoourTransmissionTomorrowstrategy.Itlooksatthechallengesandopportunitiesfacingtheelectricityindustryoverthenextfortyyears.

Itsetsoutourviewthat,overthelongterm,newtechnologiesinstalledwithinhomesandbusinesses,andbydistributors,mayalterhowthepowersystemisoperated.

Whilethechangesmayleadinthelongertermtothegridplayingadifferentrole,itwillalwaysbebeneficialforNewZealandtohaveastrong,resilienttransmissionnetwork.Wethereforestillneedtoprudentlyandsafelymanagethelong-livedassetsandcomplexsystemsthatprovidethisessentialservice.

Wearecontinuingtotransformourbusinesstomeetourefficiencytargets,andaremid-waythroughamulti-yeartransformationprogramme.Wehavemadesignificantprogressandarebeginningtoseethebenefits.Theseincludeincreasedcost-effectivenessinouractivitiesandfewerworkplaceinjuries.

WearemakingprogresswiththefoundationsofourRCP3proposal.Thisincludesfurtherdevelopmentofourserviceperformancemeasures,onwhichwesoonplantoengagewithstakeholders.

WetrustyouwillfindITP2016ausefulresource.Ifyouwanttoengagewithusonhowweshouldsetourperformancemeasuresfrom2020werecommendyoulookoutforourengagementprocesslaterthisyear.

AlisonAndrewChiefExecutiveAugust2016

INTEGRATED TRANSMISSION PLAN : 2016 III

TABLE OF CONTENTS FOREWORD .......................................................................................................................................... II1. INTRODUCTION ........................................................................................................................ 11.1. Purpose ...................................................................................................................................... 11.2. Structure of the ITP .................................................................................................................... 21.3. ITP Narrative Content ................................................................................................................. 32. OUR BUSINESS ........................................................................................................................ 42.1. Our Role in the Electricity Sector ............................................................................................... 42.2. Our Stakeholders ....................................................................................................................... 52.3. Strategy Framework ................................................................................................................... 62.4. Transmission Tomorrow ............................................................................................................. 72.5. 2016/17 Focus Areas ................................................................................................................. 93. SERVICE PERFORMANCE .................................................................................................... 113.1. Background .............................................................................................................................. 113.2. Current Service Measures and Targets ................................................................................... 113.3. Future Refinements .................................................................................................................. 134. EXPENDITURE OVERVIEW ................................................................................................... 144.1. Expenditure Categories ............................................................................................................ 144.2. Major Capex ............................................................................................................................. 154.3. Base Capex .............................................................................................................................. 164.4. Operating Expenditure ............................................................................................................. 175. ENHANCEMENT AND DEVELOPMENT ................................................................................ 195.1. Development Outlook ............................................................................................................... 195.2. E & D Capex ............................................................................................................................. 206. ASSET LIFECYCLE MANAGEMENT ..................................................................................... 246.1. Background .............................................................................................................................. 246.2. R & R Capex ............................................................................................................................ 246.3. Grid Opex ................................................................................................................................. 267. ICT AND BUSINESS SUPPORT ............................................................................................. 297.1. ICT Capex ................................................................................................................................ 297.2. ICT Opex .................................................................................................................................. 307.3. Business Support Capex .......................................................................................................... 317.4. Corporate Opex ........................................................................................................................ 32

INTEGRATED TRANSMISSION PLAN : 2016 1

1. INTRODUCTION

ThischapterintroducesourIntegratedTransmissionPlan(ITP)anditssupportingdocuments.Thechapter:

− setsouttheoverallpurposeandaimsoftheITP− explainsthattheITPcomprisesfourrelateddocumentsandasetofsupportingschedules− setsoutthestructureofthisdocument,theITPNarrative.

1.1. PURPOSE TheITPsetsoutourplansforourregulatedtransmissionbusinessduringthecurrentandsubsequentregulatoryperiods.Itprovidesanoverviewofourbusinessandthestrategiesandgoalsthatinformourdecision-making.AkeyelementofourstrategicframeworkistherecentlypublishedTransmissionTomorrowdocument.1WediscussitsroleinChapter2.

TheITPhasbeendevelopedtoalignwithregulatoryrequirements2andtomakeiteasierforstakeholderstounderstandandengagewithourbusiness.

OurfirstITPwascompletedin2013aspartofourproposalforthefive-yearregulatorycontrolperiodbeginning1July2015(knownasRCP2).SubsequenttothiswepublishedourfirststandaloneITPinSeptember2015(ITP2015).ThisITPprovidesanupdatetotheITP2015,settingoutourrefinedforecastsupto2025(ITPPeriod).

BuildingonITP2015,wehavefocusedonthefollowingaspectswhenpreparingITP2016:

− providingourcurrent,bestviewofourRCP2investmentprogrammes− signallingourRCP3investmentneeds− providingupdatesonourbusinesstransformationprocesses− startingtoincorporateTransmissionTomorrowintoourplans− reflectingfeedbackonITP2015fromstakeholdersincludingtheCommenceCommission.

ITP2018willformpartofourproposalfortheregulatoryperiodbetween2020and2025(RCP3).

NoteonForecastsITP2016reflectstheforecastsproducedduringour2016/17businessplanninground.Theprojectsandactivitiesdescribedareourbestviewofourassetmanagementandinvestmentintentions.

Muchofourplannedworksarestillsubjecttofurtherinternalgovernanceprocesses,includingfinalfinancialapprovalsandinsomecasescustomerconsultation.Theymaybesubjecttofurtherreviewandrefinement,whichmayaltertheirscope,timingandcost.

1 Thiscanbedownloadedfromhttps://www.transpower.co.nz/transmission-tomorrow-publication.2 TheTranspowerCapitalExpenditureInputMethodologiesDetermination(CapexIM)requiresustoprepareITP

documentsandspecifiesthetimingandfrequencyoftheirpublication.

INTEGRATED TRANSMISSION PLAN : 2016 2

1.2. STRUCTURE OF THE ITP Asillustratedbelow,theITPincludesthisdocument(theITPNarrative),threesupportingdocuments,andasetofsupportingschedules.

Figure1:StructureoftheITP

Asset Management Plan

TheAssetManagementPlan(updatedin2016)setsoutouroverallassetmanagementframework.Itprovidesbackgroundinformationonourassetsanddescribesthestrategieswehaveinplacetomanagethemthroughouttheirlifecycle.

Services Report

TheServicesReport(producedin2015)describestheserviceperformanceframeworkforourregulatedtransmissionbusiness.Itsetsoutourserviceperformancemeasures,whichweareprogressivelyintroducingintoourinvestmentdecision-making.WedevelopedthemeasuresaspartofITP2013.WeplantoundertakefurtherstakeholderengagementonrefinementstothemeasuresandtargetsforRCP3andbeyond(seeChapter3).

Transmission Planning Report (TPR)

TheTPR(producedin2015)identifiespotentialdevelopmentstothecapabilityandconfigurationofthegrid.Itidentifieswherefutureenhancementanddevelopment(E&D)investmentsmayberequired.Chapter5providesanupdateonourE&Danalysis.

ITP Schedules

TheITPincludesanumberofschedulesthatsummariseourexpenditureforecasts.Thesealsosetoutrelateddeliverablesincludingforecastvolumesofassetreplacements.

1. Expenditureoverview2. Basecapitalexpenditure3. Basecapitalexpenditure—deliverables4. Operatingexpenditure5. Majorcapitalexpenditure—approvedprojects6. Majorcapitalexpenditure—outputs7. Majorcapitalexpenditure—projectsunderdevelopment8. Outputmeasures

INTEGRATED TRANSMISSION PLAN : 2016 3

1.3. ITP NARRATIVE CONTENT TheremainderoftheITPNarrative(thisdocument)isstructuredasfollows.

Figure2:ITPNarrativeContent

ServicePerformanceExplainsourserviceperformancemeasuresandourplanstorefinetheseinthelead-uptoRCP3.Chapter 3

OurBusinessProvidesanoverviewofourbusinessandourstrategyframework,includingTransmissionTomorrow.Chapter 2

ExpenditureOverviewProvidesanoverviewofourITP2016expenditureforecastsandcomparesthemwithITP2015.Chapter 4

NetworkEnhancementandDevelopmentProvidesanoverviewofourE&DexpenditureforecastsfortheITPPeriod.Chapter 5

AssetLifecycleManagementProvidesanoverviewofourR&RCapexandnetworkOpexforecastsfortheITPPeriod.Chapter 6

ICTandBusinessSupportProvidesanoverviewofourICTandBusinessSupportforecastsfortheITPPeriod.Chapter 7

Throughoutthesechaptersweincludereferencestothesupportingdocumentstohelpdirectreaderstofurtherinformation.

1.4. 1.4 INFORMATION DISCLOSURE DETERMINATION TheTranspowerInformationDisclosureDetermination2014requiresustopublishasetofschedulesorinformation“inorasacompaniontotheintegratedtransmissionplan”.Threeofthoseschedules,ScheduleG6(adetailedbreakdownofassetages,remaininglivesandadditions,disposalsandothermovements)andSchedulesG7andG8(detailsofourassetmanagementmaturityassessment),fittedmorenaturallyinourmainInformationDisclosuredocument,withtheotherdisclosuresrequiredbytheDetermination.TheCommerceCommissionhasthereforegivenusanexemptionfromprovidingthosedisclosuresinthisdocument,onthebasisthattheywillbeprovidedinourmainInformationDisclosuredocument.

INTEGRATED TRANSMISSION PLAN : 2016 4

2. OUR BUSINESS

Thischapterprovidesanoverviewofourbusinessandourstrategicframework,includingTransmissionTomorrow.Thechapter:

− explainsourroleintheNewZealandelectricitysector− describessomeofourkeystakeholders− outlinesourstrategicframework− discussesourrecentlypublishedstrategydocument,TransmissionTomorrow− summarisesourcompanyfocusareasfor2016/17.

2.1. OUR ROLE IN THE ELECTRICITY SECTOR Weareastate-ownedenterprise,withtwomainrolesintheNewZealandelectricitysector:gridownerandsystemoperator.TheITPcoversourroleasgridowner.Assuch,itexcludesservicesdeliveredby,andcostsfundedthrough,oursystemoperatorservice.

ThefollowingdiagramillustratesourplaceintheNewZealandelectricityindustry.

Figure3:OurplaceintheNewZealandelectricityindustry

Asdepictedabove,thereareanumberofstakeholdersthatweinteractwithinourrolesasgridownerandsystemoperator,includingtheCommerceCommissionandtheElectricityAuthority.WediscussourkeystakeholdersinSection2.2.

INTEGRATED TRANSMISSION PLAN : 2016 5

2.1.1. FINANCIAL OVERVIEW Theprovisionofregulatedtransmissionservicesaccountsforaround90percentofourrevenue.Thesystemoperatorserviceandcustomer-fundedgridconnectionsaccountforafurther4percenteach.Thebalanceofourbusinessinvolvesnon-regulatedservices,suchasincomefromouremsTradepointnaturalgasmarket.

Weownandmanageover$5bnoftransmissionassets,andplantoinvestover$2.6bnontheseandadditionalassetsduringtheITPPeriod.

2.1.2. NETWORK OVERVIEW Wehave169substationsacrosstheNorthandSouthIslandsand11,066km(routelength)ofoverheadtransmissionlines.Wehaveapproximately88km(routelength)ofundergroundtransmissionHVACcablesand114kmofsubmarineHVDCcables.Ourtelecommunicationsassetsinclude1,923kmoffibreopticcables.

FurtherinformationonourgridassetscanbefoundinPart3ofourAssetManagementPlan.

2.2. OUR STAKEHOLDERS Beingopenandconsultingeffectivelywithourstakeholdersisakeyaimofourbusiness.Belowwesetoutanoverviewofourmainexternalstakeholders.

− Customers:ourultimatecustomersareelectricityconsumersacrossNewZealand.Thesecustomersincluderesidential,commercialandindustrialusersthatareservedthroughthenetworksof29distributioncompanies.Thesedistributorsmakeupmostofourdirectcustomers.Inaddition,wehave6grid-connectedgeneratorcustomersand11largeindustrialcustomers.

− Communities:ourassetscanhaveasignificantimpactonthecommunitiesinwhichweoperate.Itisimportantthatweconsulteffectivelywithcommunitiesatanearlystagewhenplanningouractivitiessowecanbetterunderstandpotentialimpactsandmitigatetheseasfaraspracticable.

− Landowners:weoftenrequireaccesstoprivatelandtoundertakeworkonourassets.Constructiverelationshipswithlandownersarethereforeessential.Wearecommittedtoworkingopenlyandhonestlywithlandownersandoccupierswhenundertakingouractivities.

− ServiceProviders:weoutsourcefieldmaintenance,capitalprojectconstructionandanumberofothertechnicalrolestoagroupof‘serviceproviders’.Theyarekeystakeholdersinthemaintenanceanddevelopmentofthegrid.

− OurRegulators:ouractivitiesaremainlyregulatedbytwobodies.TheCommerceCommissionregulatesourtransmissionservicerevenues,workswithustosetservicemeasures,andgovernsincentivearrangements.TheElectricityAuthoritysetsreliabilitystandards,governsourpricingmethodologyandgridaccessframework.

− OurShareholders:ourinvestorsseekconfidencethatfinancialreturnswillbecommensuratewithinvestmentriskandreflectthepreservationofbusinessvalue.WorkingwithourBoardandexecutiveteamtheyseektoensurethatweareaneffectivelymanagedbusinesswithappropriategovernanceprocesses.

INTEGRATED TRANSMISSION PLAN : 2016 6

2.3. STRATEGY FRAMEWORK Weuseastrategicframeworkacrossourbusinesstosupportastructuredwayofaligningourlong-termplansandeverydayprioritieswithstakeholderinterests.

ThisyearweupdatedTransmissionTomorrow,whichprovidesakeyconnectionbetweenourenduringpurposeandourongoingstrategiesandplans.

Asimplifiedversionofourhigh-levelframework,highlightingkeygrid-focusseddocumentation,isillustratedbelow.

Figure4:Simplifiedstrategyframework

2.3.1. OUR PURPOSE OurbusinessoperatesattheheartofNewZealand,poweringoureconomyandwayoflife.Ourpurposereflectsthisandemphasisessafety,ourdrivetofindsmartsolutions,andourlongtermperspective.

2.3.2. TRANSMISSION TOMORROW WerecentlypublishedacomprehensiveupdatetoourTransmissionTomorrowreport.Firstdevelopedin2011,TransmissionTomorrowisourlong-termviewofpossiblefuturesfortheNewZealandelectrictysector.InSection2.4wediscussstrategicprioritiesidentifiedinTransmissionTomorrow,whilelatersectionsexplainhowweareincorporatingtheseprioritiesintoourplans.

2.3.3. OUR GRID STRATEGIES InJuly2014,webecameoneofthefirstelectricitycompaniesinNewZealandtoachievecertificationagainsttheinternationalassetmanagementspecificationPAS55.In2015PAS55waswithdrawnandreplacedwiththeISO55000standard.WearecurrentlymovingtowardscertificationagainsttheISO55000standard.

Purpose

TransmissionTomorrow

Grid Strategies

Grid Plans

Values

Asset Management FrameworkStrategic Asset Management Plan

Asset Class Strategies

Asset Management PlanTransmission Planning Report

INTEGRATED TRANSMISSION PLAN : 2016 7

Embeddedwithinourstrategicframeworkisoursuiteofenduring,grid–relatedassetmanagementdocuments.

− GridAssetManagementFramework:setsoutthescopeofourassetmanagementsystemandprovidesthehigh-leveldirectionforourassetmanagementactivities.

− StrategicAssetManagementPlan(SAMP):weareevolvingourcurrentassetmanagementdocumentsuiteintoamoreintegratedSAMP.Itwillsetoutandexplaintheobjectivesofourassetmanagementactivities,andthestrategiesinplacetoachievethem.TheSAMPwillinformthedevelopmentandimplementationofourAssetClassStrategiesandAssetManagementPlan.

− AssetClassStrategies(ACS):setoutobjectivesandstrategiesspecifictothemanagementofparticularassets.TheyprovidethedirectionrequiredtodevelopourAssetManagementPlan.

2.3.4. OUR PLANS FOR THE GRID Thereareanumberofgrid-relatedplanningdocumentsthatformpartofouroverallstrategicframework.

− TransmissionPlanningReport:identifiespotentialdevelopmentstothecapabilityandconfigurationofthegrid.ItidentifieswherefutureEandDinvestmentsmayberequired.

− AssetManagementPlan(AMP):setsoutourapproachestomanagingourvariousassetclassesthroughouttheirlifecycle.ThisincludesE&DInvestments,operationalplansandindividualprogrammesthatfocusonparticularassetclasses.

Furtherdetailsonourassetmanagementframework,includingourover-archingassetmanagementobjectivesandstandards,canbefoundinChapters2-4oftheAssetManagementPlan.

2.3.5. OUR VALUES Ourvaluescaptureourviewofhowweoperatewhenweareatourbest.Theyprovideacommonlanguageandafoundationforpromotingthebestaspectsoftheculturewithinourorganisation.

ThevaluesaboveemphasisethatweneedtoworkhardandefficientlytokeepthelightsonforourfellowKiwis.Todosowestrivetodeliverexcellencebychanging,adapting,andimprovingwhatwedo.Wecometogethertomakethingshappen,focusingontheneedsofthecommunitiesweserveandtheneedtokeepeverybodysafe.

2.4. TRANSMISSION TOMORROW TransmissionTomorrowlooksatthechallengesandopportunitiesfacingtheelectricityindustryoverthenextfivetofortyyears.Itactsasakeyconnectionbetweenourpurposeandourgridstrategiesandactivities.

INTEGRATED TRANSMISSION PLAN : 2016 8

Itreflectsourviewsonlong-termpossiblefuturesfortheelectricityindustry.Itrecognisesthatelectricityconsumershaveanexpandingrangeofoptionsformeetingtheirenergyneedsasnewtechnologiesbecomemoreaffordable.Thiscombinedwithchangingsocietalfactors,continualchangesinelectricitygeneration,andrelativelyflatdemandgrowthleadstoincreasinguncertaintyinthenearfuture.

TocaptureandconsidertheseissuesweundertookawiderangeofanalysisandresearchtoinformTransmissionTomorrow.Thisincludedthefollowingelements.

− Environmentscan–reviewofkeytrends,ourvaluepropositionandcriticalelementsofoursociallicencetooperate.

− Scenariotesting–modellingtheNewZealandpowersystemto2050underawiderangeofpossiblefutures.

− Planningtrajectory–developingastorylineofhowweseethesectordeveloping,withaviewtoprovidinga‘least-regret’basisforourplanning.

− Strategicpriorities–identifyingsixpriorityareasforourbusiness,withsupportingrationaleandguidanceonactionsweshouldtake.

Belowwesummarisethestrategicprioritiesinformedbythisanalysisandoutlinehowtheseflowthroughtootherpartsofourstrategicframework.

Ensurecompetitivecostsandservices–NewZealand’straditionalelectricitysupplychainfacesincreasingcompetitivepressure,soweneedtoreduceourcostswhileensuringwetargettherightservicesandperformancelevels.Ourplanswillbeunderpinnedbygoodassetmanagementandcustomerengagement.

Playanactiveroleinshapingourindustry–therearenewchallengesandopportunitiesduetouncertaintiesindemand,carbonpolicy,anduptakeofnewtechnologies.Wehaveastrongstakeinthesuccessfuladaptationoftheindustryandaroletoplayinenablingarenewablefuture.Weplantoplayanactiveandconstructiveroleinshapingthefutureoftheindustry.

Sustainoursociallicencetooperate–itisessentialthatwemaintainpublicsupportforouractivities.Wewillcontinuetoplaceapriorityonsafety,gridsecurityandreliability,transmissioncorridors,sustainability,andgoodcorporatecitizenship.Oneofthekeyfocusesisonsustainingourcommitmenttoworkerandpublicsafety.

Matchbuildtoneed–ourplanningtrajectoryindicatesaneedtoanticipateandrespondtochangemorerapidly.Weplantoundertakecarefulandcautiousmanagementofcapacityinvestmentpressuresoveralongertimeframe,andswiftlyadapttoanewmodeofoperationinthelongterm.

Improveassetmanagement–wemanagehundredsofthousandsofassetsvaluedatmorethan$5bnandrequiringapproximately$400mintotalexpenditureeachyear,makingassetmanagementcentraltoourbusiness.Wewillcontinuetoimproveourcompetencies,systemsandprocessestoensureweprovidevalued,cost-effectiveservicesthatmeetourcustomers’changingneeds.

Increaseorganisationaleffectiveness–tosupportourotherpriorities,weneedtocontinuouslyimproveourorganisationaleffectiveness.Wewillcontinuetoembedandrefineoperationalapproachesacrossthebusiness.

ThefutureNewZealandelectricitysectormaybedramaticallydifferenttowhatitistoday.Overalong-termhorizon,batteryorotherstoragetechnologiesinstalledwithinhomesandbusinesses,electricvehicles,anddistributionnetworksmayfundamentallyalterhowthepowersystemisoperated.

Thesechangesmayleadtothegridplayingadifferentrole,however,itwillalwaysbebeneficialforNewZealandtohaveastrong,resilienttransmissionnetwork.Wewillthereforestillneedto

INTEGRATED TRANSMISSION PLAN : 2016 9

prudentlyandsafelymanagethelong-livedassetsandcomplexsystemsthatprovidethisessentialservice.

2.5. 2016/17 FOCUS AREAS EachyearweidentifyanumberoffocusareaswithinourAnnualBusinessPlanthatwillhelpusadvanceourstrategicgoals.Thefocusareashelpguidedivisionaloperatingplansandareusedtoinformourinvestmentdecision-making.

For2016/17wehaveselectedsixkeyfocusareasalignedwithensuringorganisationaleffectiveness.WesummarisethesebelowandexplainhowtheysupportthestrategicprioritiessetoutinTransmissionTomorrow.

Health and Safety

Operatingsafelyremainsourtopfocus.

Forthecomingyear,ourfocusisoninvestinginimprovedidentificationandmitigationofhighconsequencerisksandmakingiteasyforpeopletoworksafelythroughconsistent,simpleprocessesandsafebehaviours.

Thisfocusareaassistswithourstrategicprioritytosustainoursociallicencetooperate.

Transformation

Transformationreferstoourpreparationsforachangingenvironmentandensuringthattheorganisationiseffectiveinmeetingthechangingexpectationsofourcustomers,stakeholders,andregulators.

Inthecomingyearwewillcontinueworkonoperationalinitiatives.Akeyareaisstrengtheningthefocusonleadershipcapabilityandembeddingbehavioursthatsupporttheseinitiatives.Ourrevisedgridoperatingmodelwillcontinuetobeembeddedandrefinedtosupportourobjectives,includingthesefocusareas.

Therevisedmodelwillhelpsupportourstrategicprioritiestoimproveassetmanagementandensurecompetitivecostsandservices.

Increased Service Orientation

InDecember2018wewillbeputtingforwardarevenueproposaltosupportourprovisionoftransmissionservicesduringRCP3.Theproposalwillsetouttheserviceperformanceweaimtodeliver,andourviewoftheefficientcostofdeliveringthoseservices.

Thecomingyearisimportantforputtinginplacestrongfoundationsforourproposal,includingengagingwithourcustomersandotherstakeholdersonwhattransmissionservicestheyvalue.Thisincludesexploringwhatattributesofourserviceareimportant;howweshouldmeasureperformance;andwhetherweshouldbeholding,liftingoreasingourperformance.ThisisdiscussedfurtherinChapter3.

Thisfocusareaassistswithourstrategicprioritytoensurecompetitivecostsandservices.

Network Pricing

Networkpricingwillbeabigfocusfortheindustryinthecomingyear,andthereareclearbenefitstoourselvesandthewidersectorinsuccessfullyaddressingpricingdesignchallenges.

Thisfocusareaincludesengagingonthetransmissionpricingmethodologyreviewtoimprovecertaintyforplanningandinvestmentdecisions.Thiswillbeakeyfocus,particularlyasthereview

INTEGRATED TRANSMISSION PLAN : 2016 10

movesintodetaileddesignandimplementation.Otherareasincludeproposalsforchangestogenerationfundingapproachesandtheneedtorefreshourapproachtocontractingfornewgridconnections(andcustomer-drivenenhancementstoexistingconnections).

Effortstoincreaseconsistencyandtointroducemorecost-reflectivemethodologiesintodistributionpricingregimeswillalsobeanimportantinitiativeforthewiderindustry.

Thisfocusareaassistswithourstrategicprioritytoplayanactiveroleinshapingtheindustry’sfuture.

Adaptation

TransmissionTomorrowdescribesaneedtoliftourawarenessandagilitytonavigateachangingelectricitysector.Issuessuchaslowgrowth,tightsecuritymarginsandtheprospectofemergingtechnologiesmayrequiresignificantoperationalchangesinthemediumterm.

Thisfocusareabringstogetherseveralitemsrelatingtothedevelopmentofthegrid.Theseincludedevelopmentofplanstodeliverreliablepowerto,within,andthroughAucklandintheshortandlongterm.

Weplantoevolvethewayweforecastinvestmentneeds(e.g.demandandgenerationchanges)andhowwemanageourforwardinvestmentprogramme.Thiswillincludeincreasingourunderstandingofthepotentialimpactsofemergingtechnologies,andunderstandinghowtousethesetoimproveourservices.

Thisfocusareaassistswithourstrategicprioritytomatchbuildtoneed.

Grid Works Delivery

Improvingthesystemsandprocessesweusetodeliverworkwillhelpensurethatourstakeholderscanbeconfidentinourabilitytocompletetheworkcost-effectively.

Thisrequiresthatwecontinuallyreviseandoptimiseourworkplanstoensuretheseworkscanbedeliveredcost-effectivelyandasplanned.Wehaverevisedourprogrammefor2016/17tosmoothworkflowandbroughtworksforwardfrom2017/18.Smooth,predictableworkflowsallowourserviceproviderstooptimisetheirresourcelevels,reducingoveralldeliverycosts.

WeareincreasingthelevelofcertaintyaroundtheworksrequiredinlateryearsofRCP2.Thisisbeingachievedbyimprovingourconditionassessmentregimeandrefiningthewaywemakeinvestmentdecisions.Improvedstabilityacrossourworksplanwillprovideopportunitiestofurtherreducecosts.

Thisfocusareaassistswithourstrategicprioritytoimproveassetmanagement.InparticularitwillhelpensurewedevelopthecapabilityneededduringRCP3.

INTEGRATED TRANSMISSION PLAN : 2016 11

3. SERVICE PERFORMANCE

Thischapterexplainsourserviceperformancemeasuresandourplanstorefinetheseinthelead-uptoRCP3.Thechapter:

− providesbackgroundonhowourserviceperformanceframeworkhasdeveloped− setsoutourcurrentservicemeasuresandourrecentperformanceagainstthem− discussesourprocesstoupdateandrefinethesemeasuresintheleaduptoRCP3.

3.1. BACKGROUND AspartofITP2013wedevelopedanewservicemeasuresframeworktoapplyduringRCP2.Thisincludedanewsetofmeasuresandtargetsthatweredevelopedthroughastakeholderconsultationprocess.ThemeasureswereformalisedaspartoftheRCP2resetprocess.

WehavenowcompletedonefullyearofRCP2andthemeasuresandassociatedtargetsarenowineffect.Wearethereforebetterplacedtobeginconsideringhowthesecanberefinedandmoreeffectivelyembeddedintoourdecision-makingprocesses.

Wearenowplanningtoengagewithstakeholdersonpotentialrefinements.ThisprocessisdiscussedinSection3.3below.

Ourperformanceagainstthemeasuresisdiscussedinthefollowingsection.Wesuccessfullymetthemajorityofourtargetsduring2015/16.Whiletheseannualperformanceresultsprovideanindicationofourperformanceandthatofourassets,areviewofresultsoveranumberofyears(onceavailable)willallowustomorefullyassessourunderlyingperformance.

FurtherbackgroundonourcurrentserviceperformancemeasurescanbefoundinITPSchedule8andChapter3oftheServicesReport.

3.2. CURRENT SERVICE MEASURES AND TARGETS Ourservicemeasuresandtargetsaresummarisedinthefollowingtables.3Ourperformanceforthe2015/16yearcanbecomparedwiththerespectivetargets.

Thecurrentmeasuresarebasedon:

− thefrequencyanddurationofinterruptionsexperiencedbycustomersandbyrelativepriorityofpoints-of-service

− availabilitytargetsfor27HVACcircuitshavingthebiggestimpactontheenergymarket− forward-lookingtargetsforHVDCenergyavailability.

Thebasisforthetargets,caps,andcollarsisdiscussedinChapter3oftheServicesReport.

3 ThemeasuresandtargetsexcludeinterruptionsduetotheAutomaticUnder-FrequencyLoadShedding(AUFLS)system.

INTEGRATED TRANSMISSION PLAN : 2016 12

Table1:Performance15/16—numberofinterruptions

GP1:Numberofinterruptions RCP2targetsCategory 15/16performance Target Cap CollarHighpriority 0 2 0 4

Important 2 9 4 14Standard 14 26 21 31Generator 4 11 6 16N-security 22 56 38 74

Wesuccessfullymetournumberofinterruptiontargetsforallcategoriesduring2015/16.

Insomeinstances,weexceededtheperformancelevelsetbythe‘cap’,forexampletheImportantandStandardcategoriesabove.Anumberoffactorsledtothisgoodperformanceincludingrelativelybenignweatherduringtheyearandfewerequipment-relatedinterruptions.

Table2:Performance15/16—averageinterruptiondurations

GP2:Averagedurationofinterruptions(minutes) RCP2targetsCategory 15/16performance Target Cap CollarHighpriority 0 70 30 110

Important 14 100 30 170Standard 42 65 0 130Generator 162 130 50 210N-security 167 80 45 115

Wesuccessfullymetouraveragedurationtargetsforthemajorityofcategoriesduring2015/16.However,ourperformanceforgeneratorandN-securitysitesdidn’tmeettherespectivetargets.

TheGP2Generatortargetwasmissedmainlyduetoequipment-relatedinterruptionsatonesite.ThemainreasonfornotachievingtheN-securitytargetsforGP2andGP3(below)wasanextendedoutageatOhakuneinDecember2015resultingfromatrippedsupplytransformer.Followinganinvestigationoftheincidentwehaveputinplaceadditionalpreventivemaintenancetargetedatreducingthepotentialforsimilarfutureincidents.

Table3:Performance15/16—P90interruptiondurations

GP3:P90longestdurations(minutes) RCP2targets

Category 15/16performance Target Cap CollarHighpriority 0 120 80 160Important 17 240 170 310Standard 116 130 60 200Generator 234 350 260 440

N-security 341 215 170 260

WesuccessfullymetourP90durationtargetsforthemajorityofcategoriesduring2015/16.TheN-securitytargetwasn’tmetduetothesupplytransformerinterruptionatOhakune,discussedabove.

INTEGRATED TRANSMISSION PLAN : 2016 13

Table4:Performance15/16—circuitavailability

Availability(%) RCP2targets 15/16performance Target Cap CollarAP1:HVDC 98.9 98.5 99.5 97.5

AP2:HVAC 99.0 99.6 100 99.2

WesuccessfullymetourHVDCavailabilitytargetduring2015/16.HoweverwedidnotmeetourHVACavailabilitytarget.ThiswasduetothevolumeofscheduledmaintenanceandprojectworkrequiredonkeySouthIslandcircuits.

3.2.1. HOW WE USE THE MEASURES Theserviceperformancemeasuresareanimportantpartofourday-to-dayactivities.Weusethereliabilitytargetsaspartofourrenegotiationofserviceprovidercontracts,andarefactoringthereliabilityandavailabilitytargetsintoourworksplanningprocesses.

Atahighlevel,weusethemeasures:

− todiscussourserviceswithcustomers:asthemeasuresshouldreflectwhatisimportanttocustomers.Havingclearmeasureshelpssupportdiscussionswithourcustomers,includingcommercialandoperationalnegotiations.

− asinputsintoassetmanagementdecisions:inparticular,themeasuresarebeingusedtoprioritiseourworkandweareworkingthroughhowwecansensiblyshiftfromtraditionaleconomicdecision-makingtoamorestronglyservices-drivenapproach.

3.3. FUTURE REFINEMENTS Asdiscussedabove,weplantoreviewourserviceperformancemeasuresinthelead-uptoRCP3.Thiswillbedonethroughengagementwiththeindustryandotherstakeholdersoverthecomingmonths.WewillpublishanengagementpaperonthistopicinOctober2016.

AtthetimeofcompletingthisITP,weenvisagethattheengagementprocesswillfocusonarangeofissues,including:

− theoverallpurposeofserviceperformancemeasures− reviewingtheserviceattributesthatcustomersvalue− comparingourservicemeasureswithotherjurisdictions− refinementstomeasures;allocationsacrosscategories;andservicelevels.

Furtherinformationonourengagementapproachandhowtoprovidefeedbackwillbeprovidedviaanengagementpaper,duetobepublishedinOctober2016.

INTEGRATED TRANSMISSION PLAN : 2016 14

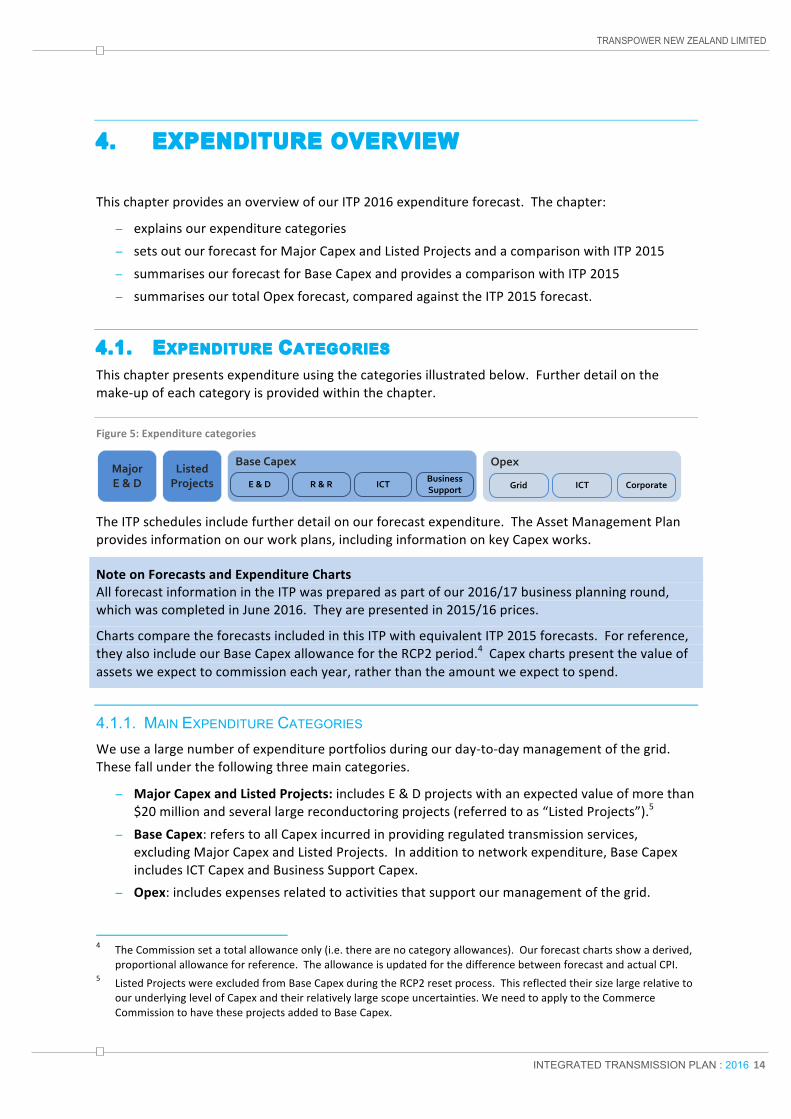

4. EXPENDITURE OVERVIEW

ThischapterprovidesanoverviewofourITP2016expenditureforecast.Thechapter:

− explainsourexpenditurecategories− setsoutourforecastforMajorCapexandListedProjectsandacomparisonwithITP2015− summarisesourforecastforBaseCapexandprovidesacomparisonwithITP2015− summarisesourtotalOpexforecast,comparedagainsttheITP2015forecast.

4.1. EXPENDITURE CATEGORIES Thischapterpresentsexpenditureusingthecategoriesillustratedbelow.Furtherdetailonthemake-upofeachcategoryisprovidedwithinthechapter.

Figure5:Expenditurecategories

TheITPschedulesincludefurtherdetailonourforecastexpenditure.TheAssetManagementPlanprovidesinformationonourworkplans,includinginformationonkeyCapexworks.

NoteonForecastsandExpenditureChartsAllforecastinformationintheITPwaspreparedaspartofour2016/17businessplanninground,whichwascompletedinJune2016.Theyarepresentedin2015/16prices.

ChartscomparetheforecastsincludedinthisITPwithequivalentITP2015forecasts.Forreference,theyalsoincludeourBaseCapexallowancefortheRCP2period.4Capexchartspresentthevalueofassetsweexpecttocommissioneachyear,ratherthantheamountweexpecttospend.

4.1.1. MAIN EXPENDITURE CATEGORIES Weusealargenumberofexpenditureportfoliosduringourday-to-daymanagementofthegrid.Thesefallunderthefollowingthreemaincategories.

− MajorCapexandListedProjects:includesE&Dprojectswithanexpectedvalueofmorethan$20millionandseverallargereconductoringprojects(referredtoas“ListedProjects”).5

− BaseCapex:referstoallCapexincurredinprovidingregulatedtransmissionservices,excludingMajorCapexandListedProjects.Inadditiontonetworkexpenditure,BaseCapexincludesICTCapexandBusinessSupportCapex.

− Opex:includesexpensesrelatedtoactivitiesthatsupportourmanagementofthegrid.

4 TheCommissionsetatotalallowanceonly(i.e.therearenocategoryallowances).Ourforecastchartsshowaderived,

proportionalallowanceforreference.TheallowanceisupdatedforthedifferencebetweenforecastandactualCPI.5 ListedProjectswereexcludedfromBaseCapexduringtheRCP2resetprocess.Thisreflectedtheirsizelargerelativeto

ourunderlyinglevelofCapexandtheirrelativelylargescopeuncertainties.WeneedtoapplytotheCommerceCommissiontohavetheseprojectsaddedtoBaseCapex.

OpexBaseCapex

ICTR&RBusinessSupport ICTGrid CorporateE&D

ListedProjects

MajorE&D

INTEGRATED TRANSMISSION PLAN : 2016 15

ThefollowingsubsectionssetoutourcurrentforecastsfortheITPPeriodineachoftheabovecategories.TheseforecastsarecomparedwithequivalentforecastsfromITP2015.WhererelevantwealsoincludeacomparisonagainstourRCP2allowance.

4.2. MAJOR CAPEX ThechartbelowpresentsourforecastforMajorCapexandListedProjectsduringtheITPPeriod.TheforecastiscomparedwithourequivalentforecastfromITP2015.Thechartpresentsthevalueofassets(in2015/16prices)weexpecttocommissioneachyear.

Figure6:MajorCapexandListedProjects

BasedonourrefinedMajorCapexandListedProjectforecastweexpecttocommissionassetswithatotalvalueof$293mduringRCP2.6Thisis$107mbelowtheITP2015forecast,areductionof27%.

MajorCapexisprimarilydrivenbygridconditions,includingdemandgrowth,changesinthelocationsandcapacityofgeneration,anddistributors’plansfortheirnetworks.

Ourplansevolvethroughourprocessesasweprogresssolutionstakingintoaccountupdatedinformationfrom:demandandgenerationchanges,optionsandcostanalysis,consultation,andregulatoryapprovals.Themaindriversforthechangesdepictedaboveincludethefollowing.

− RevisedcostestimatesfollowingroutesurveysontheBunnythorpe–Haywardsreconductoringproject.

− Reassessmentofexpectedneeddates:

- Pakuranga-WhakamaruseriescompensationhasbeenremovedfromRCP2andRCP3,butwillbeconsideredonthelong-listofoptionsassociatedwithourWaikatoandupperNorthIslandVoltageManagementinvestigation.

- WaitakiValleyprojecthasbeenmovedtoRCP3basedonrefinedloadforecastschangingtheneeddateandtheuseofinterimworks,includingspecialprotectionschemes.

- HVDCworksplannedfor2024/25havebeendeferredbeyondRCP3,thoughthistimingmaybesubjecttofurtherreview.

6 ThistotalincludesworksunderinvestigationthatifapprovedwouldbecommissionedinRCP2.Furtherdetailcanbe

foundinChapter5oftheAMP.

0

$50M

$100M

$150M

$200M

$250M

$300M

$350M

$400M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP3 Target

Major and Listed Capex - Commissioned Value

All figures in 2015/16 prices

Listed Capex includes large conductoring projects

INTEGRATED TRANSMISSION PLAN : 2016 16

- UpperSouthIslandGridUpgradeStage2–hasbeenmovedoutofRCP3basedonupdatedloadforecasts.

- WairakeiRing,ageneratordriveninvestment,hasbeenremovedfromRCP3aswecurrentlyhavenoconfirmedplansfornewgeneratorconnections.

Figure7:MajorCapexandListedProjects

ThechartabovepresentsourforecastofTotalCapexexpenditureincludingMajorandListed

Projects,inadditiontoBaseCapexduringtheITPPeriods.

FurtherdetailonourMajorCapexandListedProjectforecastscanbefoundinITPSchedules5,6and7andChapter6oftheAssetManagementPlan.

4.3. BASE CAPEX ThechartbelowpresentsourforecastforBaseCapexduringtheITPPeriod.TheforecastiscomparedwiththeequivalentforecastincludedinITP2015andtheassociatedRCP2allowance.

Figure8:BaseCapex

0

$50M

$100M

$150M

$200M

$250M

$300M

$350M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

Total Base Capex - Commissioned Value

All figures in 2015/16 prices

Base Capex does not include Identified Conductoring Projects

INTEGRATED TRANSMISSION PLAN : 2016 17

RCP2 Base Capex

Weexpecttocommissionassetswithavalueof$1,082mduringRCP2.Thisis$86mbelowtheITP2015forecast,whichequatestoareductionof7%inexpectedBaseCapex.

ThenewprofileforRCP2isgenerallyconsistentwiththeallowanceotherthananupliftin2019/20.Thisupliftreflectscurtaileddeliveryin2015/16andthereschedulingofworkstoensureamorestableworkplanwithimproveddeliverability.

Inadditiontosmoothingourworkflow,thefollowingaspectshaveledtotheupdatedprofile.

− Refinedinvestmentdecision-making:assignalledinITP2015weareimprovingourdecision-makingapproachtoallowimprovedprioritisationandmorecost-effectivedecisions.Continuedimplementationofthisapproachwillhelpimproveoverallefficiency.

− Findingefficiencysavings:wehaveaprogrammeunderwaytoactivelyseekefficiencysavingsduringRCP2.Thesesavingsareresultingfromimproveddesign,reviewofourstrategies,andcapturingsavingsfromimprovementsinourdecision-makingapproach.

− Aligningtoournewstructures:werestructuredallthreegriddivisionsinthefirsthalfof2015/16.Withthenewstructureinplacewearesteadilyextendingourplanninghorizonandcapabilitytoreleaseastableworkplantoserviceproviderswellaheadofdelivery.

− DeferringE&Dprojects:wehavebeenabletodefersomeprojectsthroughfurtherevaluationoftheirneeddateanddeliveryschedule,aswellasthroughtheuseoflowercostinterimsolutions,suchasvariablelineratings.

Overthecomingyearwewilluseournewdecision-makingframeworktofurtherrefineourplansforRCP3andtheremainingyearsofRCP2.

FurtherbackgroundonourBaseCapexcanbefoundinITPSchedules2and3andintheAssetManagementPlan.

RCP3 Base Capex

OurRCP3plansareinanearlystageofpreparationanddonotyetfullyreflectourimproveddecision-makingapproach.OurpreliminaryviewisthatthereisagoodprospectofreducingplannedworkforRCP3,butwewillnothaveaclearviewuntilwecompletefurtheranalysis.

ConsistentwithourTransmissionTomorrowstrategyofcontrollingcoststoremaincompetitivewehavesetaCapextargetforRCP3of$1.3bn.Thistotal,forthefiveyearRCP,includesBaseCapexandListedProjects.IthasbeensetbasedonourRCP2expenditurelevels,withaviewtoholdingpriceincreasesbelowinflation(allelsebeingequal).Overthecomingyearwewilltesttheviabilityofthistargetthroughourplanningprocesses.TheITPSchedulesincludeanindicationoftheCapexrequiredtomeetthistarget.

Thisapproachrequiresfurtherdisciplineinourdecision-makingwheretherearetrade-offsbetweenexpenditureandrisk,includingpotentialimpactsonserviceperformance.

4.4. OPERATING EXPENDITURE TheITPforecastsincludeOpexincurredinprovidingregulatedtransmissionservices.Thisexcludespass-throughandrecoverablecosts,7andcostrelatedtooursystemoperatorfunction8.

7 Pass-throughcostsincluderegulatoryleviesandlocalgovernmentrates.Recoverablecostsincludeinstantaneous

reservesavailabilitychargesandtransmissionalternativescosts(e.g.usingdemandresponsetodeferaproject).

INTEGRATED TRANSMISSION PLAN : 2016 18

OurOpexiscategorisedas:

− Grid:activitiesrelatedtofieldmaintenance,operations,andtechnicaltraining− ICT:includingfibreandequipmentleases,outsourcedsupport,andsoftwarelicences

− Corporate:activitiesandcostsincurredinprovidingthetransmissionservice.Itincludesnetworkandoperationalsupport,assetmanagementstaffcosts,andbusinesssupport.

ThechartbelowpresentsourtotalOpexforecastfortheITPPeriod.TheforecastiscomparedwithourequivalentforecastincludedinITP2015andtheassociatedRCP2allowance.

Figure9:TotalOpex

Weexpecttoincuratotalof$1,240mOpexduringRCP2.Thisis$72mbelowtheITP2015forecastand$101mbelowourRCP2allowance,leadingtoa5%reductioninexpectedOpexsinceITP2015.Thisreflectsthesignificantsavingsweexpecttomakeovertheperiodonmaintenancecosts,ICTleasecostsandbuildingleasecosts.

FurtherdetailonourOpexforecastsisprovidedintheremainingchapters.

8 Weallocatecoststooursystemoperatorbusinesswherewecanidentifythecostsas‘avoidable’—i.e.,wewouldnot

incurthecostsifwedidnotprovidesystemoperatorservices.ThisallocationmethodologymeansthatcommoncostsareincludedintheITP.

0

$50M

$100M

$150M

$200M

$250M

$300M

$350M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

Total Opex

All figures in 2015/16 prices

INTEGRATED TRANSMISSION PLAN : 2016 19

5. ENHANCEMENT AND DEVELOPMENT

E&Dinvestmentsallowustodevelopthegridtocaterforexpectedchangesindemandorgeneration.ThischapterprovidesanupdateontheseinvestmentsovertheITPperiod.Itsetsout:

− thedevelopmentoutlook,includingthecontextthatinformsourinvestmentdecisions− ourE&DforecastsandacomparisonwithITP2015.

TheTransmissionPlanningReport(TPR)summariseshowweassesswhetherthegridcanaccommodateexpectedchangesindemandandgeneration.ItidentifieswherefutureE&Dinvestmentsmayberequired,andsummarisestheseneedsintheGridReliabilityReportandtheGridEconomicInvestmentReportthatidentifypotentialreliabilityandeconomicinvestmentsrespectively.

ThisyearwehavenotrevisedourTPR,withthelatestversionbeingincludedinITP2015.

5.1. DEVELOPMENT OUTLOOK TheTPRandtheE&Dportfolioareheavilyinfluencedbychangesindemandandgeneration.Fromthemid-1990stothemid-2000speaksystemdemandgrowthwasstrong.However,since2008systemdemandgrowthhasflattened.Thishasresultedinsignificantreductionsinourforecastsoverthelast6years.

Systemdemandgrowthisexpectedtobe1.1%perannumto2030.However,asshownbelow,wealsoconsiderthattheplausiblerangeoffuturedemandgrowthiswide,asillustratedbythehighandlowbounds,andthiscouldbefurtherinfluencedbytheuptakeofbatterystoragenotexplicitlyconsideredinthisfigure.Furtherinformationontheseforecastsandourapproachtoderivingthemcanbefoundonourwebsite.9

Whilesystemdemandgrowthhasbeenlowweexpecthigherlevelsofgrowthinsomeregions.SouthCanterbury,forexample,isaregionwhereplannedirrigationanddairyfactoryexpansioncontinuestoplacepressureonexistinggridcapacity.

RecentandplanneddecommissioningofgenerationintheUpperNorthIslandwillsignificantlyaffectpowerflowsandtheneedforvoltagesupportonthenetwork.Thesemayresultintheneedforinvestmentinthegrid.Thisissueiscurrentlythesubjectofamajorcapexinvestigation.10

Accuratelyforecastingdemandandgenerationexpansion(andcontraction)continuestobeachallenge.Futureinfluencesondemandgrowtharedifficulttopredict.ArecentexampleistheproposedchangestotheTransmissionPricingMethodologythatmayaffectincentivesforconsumerstomanagedemandatpeaktimes,althoughtheextentofthiseffectisunclear.Inaddition,bothconsumersandgeneratorscanannounceandimplementplansatshortnoticethatcansignificantlyimpactdemandandpowerflows.

Overthelong-term,TransmissionTomorrowhighlightsawidevarietyoffactorsthatcouldsignificantlyimpactfuturedemandandgenerationalthoughthescaleandtimingoftheeffectisnotyetclear.Examplesinclude:solarphotovoltaicpanels,batterystorage,energyusechanges,smartergrid,urbanisation,andelectrification.Whilewewillcontinuetodevelopourabilitytoanticipate

9 https://www.transpower.co.nz/about-us/our-purpose-values-and-people/planning-inputs10 https://www.transpower.co.nz/waikato-and-upper-north-island-voltage-management-investigation

INTEGRATED TRANSMISSION PLAN : 2016 20

thesechanges,weseeaneedtodeveloptheacuityandabilityofourplanningapproachessothatweareagileinourresponse.

Figure10:SystemPeakElectricityDemandForecasts

5.2. E & D CAPEX AsdiscussedinChapter4,ourE&DCapexissplitintotwocategories,MajorandBase.BelowwediscusstheseforecastsovertheITPPeriodandhowthesevaryfromITP2015.

FurtherinformationonourE&DforecastscanbefoundinITPSchedules2,3,5,6and7andinChapter6oftheAssetManagementPlan.

5.2.1. MAJOR E & D CAPEX IfthevalueofanE&Dinvestmentexceeds$20mitistreatedasaMajorCapexProject.Theseprojectsrequireindividualregulatoryapprovaloutsideofourfive-yearlyresetproposals.Theapprovalprocessformajorcapexprojectsinvolvesmultiplestagesofpublicconsultationdesignedtotesttheneeddateforinvestmentandtosupportselectionoftheinvestmentoptionthatprovidesthegreatestbenefitoverthelifeoftheinvestment.

OurMajorCapexforecastisdiscussedinSection4.2.TheremainingsectionsofthischapterincludediscussionsonfuturegridneedsandpotentialE&Dinvestmentstoaddressthem.

4000

5000

6000

7000

8000

9000

10000

1995

2000

2005

2010

2015

2020

2025

2030

MW

Actual 2016 Update - prudent 2016 Update - expected2016 Update - low bound 2016 Update - high bound TPR 2015 prudent

INTEGRATED TRANSMISSION PLAN : 2016 21

5.2.2. BASE E & D CAPEX BelowwediscussourBaseE&DforecastsfortheITPPeriodandhowthesehavebeenrefinedsincewepublishedITP2015.

Figure11:BaseE&DCapex

BasedonourrefinedBaseE&DCapexforecastsweexpecttocommissionassetswithatotalvalueof$53mduringRCP2.Thisis$49mbelowtheITP2015forecast,leadingtoa48%reductioninexceptedCapex.Adjustmentstotheforecastrelatemainlytothedeferralofworksthatwereduetobecommissionedin2018/19,revisedprojectestimates,andtheintroductionofadditionalprojects.

Theprimaryvariancedriversincludethefollowing.

− TheschedulefortheNorthTaranakiTransmissionCapacityprojecthasbeenrevisedbasedonacommissioningdateinearlyRCP3.Wearecontinuingourinvestigation,anddiscussionsaboutoptionswithcustomersandotherstakeholders.Thesemayleadtofurthertimingrevisions(includingcommissioninginlateRCP2)and,basedontheeventualsolution,itmaybecomeaMajorCapexproject.

− TheOtahuhu—WiriTransmissionCapacityprojecthasbeendeferredfromRCP2toRCP3.Weidentifiedthatvariablelinerating(VLR)couldbeappliedtothecircuitsifprotectionissueswereresolved.WiththerequiredprotectionchangesmadeandVLRapplied,thecircuitratinghasbeenincreased,shiftingtheneeddatefrom2015to2021.Thiswillcontinuetobemonitoredcloselyduetorapidurbanandindustrialdevelopmentintheregion.Furtherdetailedinvestigationintothepreferredsolutionforresolvingtheconstraintisongoing.

− Furtherdetailedeconomicinvestigationresultedinanumberofneedsnotprogressingtoapreferredsolutionuntilitisclearthatsufficientbenefitswillberealised(e.g.bussecurityimprovementsatBunnythorpeandMasterton).

− Identificationofadditionalconstraintshasadvancedtheneeddateforsomeprojects.(e.g.avoltagestabilityconstraintintheTimaruregionhasbroughttheneeddateforwardtoRCP2).

− Identificationofadditionalneedshasresultedinadditionalprojects(e.g.specialprotectionschemestofacilitatedemandconnections).

WeanticipatethatDemandResponsewillplayaroleinmanagingrisksassociatedwiththedeliveryofprojects,suchasinthelowerWaitakiValley.

0

$10M

$20M

$30M

$40M

$50M

$60M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

Base E & D Capex - Commissioned Value

All figures in 2015/16 prices

INTEGRATED TRANSMISSION PLAN : 2016 22

Asillustratedbytheabovevariances,E&Dexpenditurecanbechallengingtoforecastoverthemedium-term.Thisisparticularlythecaseduetovaryingexternalfactorssuchaschangingunderlyinggridconditions(e.g.changesindemandandgeneration)andtheactionsandpreferencesofconnected(orconnecting)parties.Atatimeoflowoveralldemandgrowth,timingorscopechangestothefew,relativelylargeprojectsinthiscategory,canoccurandleadtosignificantforecastvolatilityinandacrossRCPs.

5.2.3. KEY ASSUMPTIONS WeexpecttomakefurtherrefinementstoourforecastsovertheITPPeriod.Examplesofkeyuncertaintiesthatcouldinfluenceourforecastsinclude:

− persistentlowdemandgrowthleadingtofurtherreductionsinourforecasts− changesindemanddrivenbychangestotheTransmissionPricingMethodology− acommitmenttoclosetheTiwaialuminiumsmelter− acommitmenttochangethedecommissioningdatefortheRankineunitsatHuntly.

Inadditiontochangingdemandpatterns,wewillundertakefurtherinvestigationsofinvestmentneedsandconsideralternativeinvestmentoptions.

5.2.4. UPDATE ON OUR E & D INVESTIGATIONS ThisyearwehavenotrevisedourTPR,withthelatestversionbeingincludedinITP2015.AnupdatedreportwillbeincludedasasupportingdocumentinITP2017.

BelowwedescribeE&Dissuescurrentlyunderinvestigation,whichcouldresultinchangestotheforecastsweexpecttoincludeinITP2017.

Grid Needs that are currently under investigation

Wearecurrentlyinvestigatingsolutionstothefollowingissues.Ifpursued,wewouldexpectthesetoleadtoBaseCapexinvestments.

− TimaruInterconnectingTransformersCapacityUpgrade:thisprojectconsidersanincreaseininterconnectioncapacityatTimaruandisdrivenbytheneedtoensuretheregiondoesnotsufferfromvoltageinstabilityfollowinganoutageofa220kVcircuitorinterconnectingtransformer.

− Otahuhu-WiriTransmissionCapacity:thisprojectconsidersincreasesinthetransmissioncapacityintoBombayandWiriandisdrivenbyloadgrowthintheregion.TheuseofvariablelineratingshasdeferredtheneedforthisworktoRCP3.ThisprojecthasthepotentialtobecomeaMajorCapexProjectdependingonthepreferredsolution.

− OtahuhuandPenroseInterconnectionCapacity:thisprojectconsidersthereplacementofinterconnectingtransformersinAucklandandrelatestothelongtermdevelopmentofsupplyintoAuckland.

− NorthTaranakiTransmissionCapacity:thisprojectconsidersthedevelopmentofthegridinTaranakirelatedtothefutureoftheNewPlymouthsite.AsdiscussedinSection5.2.2thetimingofthisprojectisunderreviewandmaymoveforwardinRCP2.ItisalsopossibletheprojectcostmaymakethisaMajorCapexProject.

− SouthlandReactivePowerSupport:thisprojectconsidersprovidingadditionalreactivesupportinSouthland.

− UpperSouthIslandHighVoltageManagement:thisprojectisrelatedtothefutureofreactiveequipmentatIslingtonandtheupperSouthIsland.

INTEGRATED TRANSMISSION PLAN : 2016 23

Inaddition,wearecurrentlyinvestigatingthefollowingneedthatweexpecttoleadtoaMajorCapexinvestment.− WaikatoandupperNorthIslandVoltageManagement:thisprojectconsiderstheneedfor

voltagesupportviagridinvestmentsand/ornon-transmissionsolutionsintheWaikatoandupperNorthIslandregions.ThisprojectisdrivenbydemandgrowthandthermalgenerationretirementsintheupperNorthIsland.ThiscouldrequirebothBaseandMajorCapexinvestments.

WealsoplantofurtherinvestigatethefollowingneedsthatifpursuedcouldleadtoMajorCapexinvestments.− Pakuranga-WhakamaruSeriesCompensation:thisprojectconsiderstheneedtoimprove

sharingofpowerflowsbetweencircuitssupplyingAuckland.ThisinvestigationisdependentontheWaikatoandupperNorthIslandVoltageManagementinvestigation.

− WaitakiValley:thisprojectrelatestotheneedtoincreasetransmissioncapacityinthelowerWaitakiValleydrivenbyloadgrowthindairyingandirrigation.

− IncreasedHVDCcapacity:weareconsideringtheneeddateforadditionalcapacity,asdrivenbygenerationanddemandchanges.

− UpperSouthIslandGridUpgradeStage2:thisisthenextphaseoftheUpperSouthIslandGridUpgradeMajorCapexProjectandwillreconsidertheneeddateforfurtherinvestmentandthepreferredlong-termdevelopmentplantoresolvethisissue.

Grid Needs identified but not yet investigated

ThereanumberofissuesthathavenotbeeninvestigatedthatmaybereconsideredfortheITP2017.Theseincludethefollowing.

− AdditionalgenerationintheWairakeiRingandTaranakirequiringgridcapabilitytobeincreased.Theseneedsaredependentonpotentialgenerationconnections.

− CapacityconstraintfortheWaitakiinterconnectingtransformers.ThisislinkedtoapotentialnewGXPintheregion.

− CapacityconstraintfortheHamiltoninterconnectingtransformers.ThisisimpactedbyanyinvestmentoridentificationofapreferredsolutiontotheWaikatoandupperNorthIslandVoltageManagementinvestigation.

− InvestigationtorelievegenerationconstraintsintheRoxburgh/Clyde/Twizelregion.− Voltageandcapacityconstraintsinthe66kVnetworkontheWestCoast.

− Newgenerationconnectionsmayrequirespecialprotectionschemestoprotectassetsfromoverloadingduringspecificoperatingconditions.

INTEGRATED TRANSMISSION PLAN : 2016 24

6. ASSET LIFECYCLE MANAGEMENT

Effectivelymanaginggridassetsthroughtheirrespectivelifecyclesisoneofourkeyfunctions.Recurrentmaintenanceandassetrenewalaresignificantcomponentsofourexpenditure.ThischapterprovidesanupdateontheseinvestmentsovertheITPperiod.Itsetsout:

− ourapproachtomaintainingandrenewingourassets− RenewalsandRefurbishment(R&R)CapexforecastsandacomparisonwithITP2015− gridOpexforecastandacomparisonwithITP2015.

6.1. BACKGROUND Maintainingasafeandreliableservicewhilemanagingcostsarekeydriversinourapproachtoassetlifecyclemanagement.Totallifecyclecostisakeyconsiderationinourdecision-makingandrequiresustomaketrade-offsbetweenCapexandOpex.

Whenmakingdecisionsonassetintervention,weassesstotalrequiredCapexandOpex,including:

− theimpactofmaintenanceactivitiesonassetlifeandperformance− allsignificantlifecyclecosts− benefits(suchasreducedfailurerisk)ofreplacingorrefurbishingtheasset.

Ourapproachtolifecycle-basedassetmanagementisdiscussedinChapter3oftheAssetManagementPlan.

6.2. R & R CAPEX BelowwediscussourBaseR&RCapexforecastsfortheITPPeriodandhowthesehavebeenrefinedsincewepublishedITP2015.ThisCapexrelatestoreplacingexistingassets,orrefurbishingthemtoextendtheirusefullife.

FurtherdetailonourrenewalprogrammesareincludedinChapters8to21oftheAssetManagementPlan.Italsodiscusseshowweidentify,prioritiseandscheduletheseworks.

INTEGRATED TRANSMISSION PLAN : 2016 25

Figure12:BaseR&RCapex

BasedonourrefinedBaseR&RCapexforecastsweexpecttocommissionassetswithatotalvalueof$832mduringRCP2.Thisis$19mbelowtheITP2015forecast,whichequatestoa2%reductioninexpectedCapex.Changestotheexpenditureprofilerelatemainlytoworksbeingdeferredfromthe2015/16workprogrammetolaterinRCP2andchangestoindividualassetclassforecasts.Examplesoftheseassetclasschangesaresetoutbelow.

− Powertransformers:plannedexpenditureintheperiodislowerfollowingdetailedreviewofreplacementcriteriaandassociatedneeds.

− Grillages:forecastexpenditureassociatedwiththeconcreteencasementofsteelgrillageshasincreasedslightlyaswebegintoaddressmoreremoteanddifficulttoaccesssites.

− Outdoortoindoorconversions:forecastexpenditureintheperiodislowerfollowingare-prioritisationofsomesitesbetweenRCP2andRCP3aswellasloweringthecostofthebuildingsthroughbetterdesigns.

− Insulators:basedonupdatedconditioninformationandmodellingwehavereducedourforecastexpenditureoninsulatorreplacements.Wehavealsoachievedalowercostperunit.

− Substationfencing:plannedexpenditureislowerthanforecastduetoimprovementsinstandardisingconditionassessmentofsubstationsecurityfencingaswellasapplyingariskbasedapproachindecidingwhenelectricalfencesshouldbeinstalled.

Determiningtheoptimumrenewaltimingforcomplexassetsisdifficult.Therewillalwaysbeanelementofvarianceinthehealthofassetsduetovaryingenvironmentalconditions,componentrenewals,maintenance,andchangestoassetuse.Reflectingtheseissueswewillcontinuetorefineourforecastsoverthecomingyear.

0

$50M

$100M

$150M

$200M

$250M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

Base R & R Capex - Commissioned Value

All figures in 2015/16 prices

INTEGRATED TRANSMISSION PLAN : 2016 26

6.2.1. LONG-TERM CAPEX FORECASTS Aspartofourmid-RCPITPweareprovidingasetofextendedforecastsforassetclassesthathavethepotentialtohavelarge‘lumpy’expenditures.TheseforecastsaresetoutbelowbyRCP.

Table5:Long-termforecastsbyRCP(NZ$millions)

AssetType RCP4 RCP5 RCP6andbeyond

HVDC 164 TBC TBC

PowerTransformers 127 20 TBC

HVCables TBC TBC TBC

DynamicReactiveSupport 26 TBC TBC

Reconductoring 75 70 TBC

Theseforecastsreflectourcurrentbestviewonlikelyexpenditureintheseassetclasses.Giventheperiodoftheseforecaststheyshouldbeconsideredindicativeonly.Foranumberofclasseswehaveyettodevelopaspecificforecast.Thesearedenotedas“TBC”.BeyondRCP5wecurrentlydonothavespecificassetclassforecasts.

Wearecontinuingtorefineourlonger-termforecastsandwillprovidefurtherupdatesontheaboveexpenditurecategoriesaspartofITP2018.

6.3. GRID OPEX ThegridOpexcategoryincludesexpenditureonactivitiesundertakenbyourfieldserviceprovidersandexternaltrainingproviders.11Specifically,itincludescostsrelatedtothefollowingactivities.

− Routinemaintenance:includesscheduledactivitiesthatkeepassetsinanappropriateconditionandensurethattheyoperateasrequired.Routinemaintenanceseekstoproactivelymanagefailurerisk(preventive)aswellasrespondingtoactualfailuresastheseoccur(reactive).

− Maintenanceprojects:aretime-boundprogrammesthataddressprevalentassetconditionissues.Theytypicallyconsistofprogrammesofsmallrepairsorreplacementsofcomponentsoflargerassets.

− Operating:activitiesrelatetofieldmaintenanceswitching,includingrequestsforfeederisolation,andswitchingfollowingcustomerfaults.

− Training:includesexpensesrelatedtoourmanagementofskillsandcompetenciesparticularlyintechnicalareas.

11 TheinternalstaffcostsrelatedtothemanagementandspecificationoftheseactivitiesareincludedinCorporateOpex,

discussedinSection7.4.

INTEGRATED TRANSMISSION PLAN : 2016 27

6.3.1. GRID OPEX FORECASTS BelowwediscussourGridOpexforecastsfortheITPPeriodandhowthesehavebeenrefinedsincewepublishedITP2015.

FurtherdetailonourGridOpexforecastscanbefoundinITPSchedule4.

Figure13:GridOpex

Weexpecttoincuratotalof$464mOpexduringRCP2.Thisis$35mbelowtheITP2015forecast,whichequatestoa7%reduction.OurforecastisbelowourRCP2allowanceandreflectsthesavingsweexpecttomakeovertheperiod,particularlyingridmaintenanceworks.

Thekeydriversforthesereductionsincludethefollowing.

− Routinemaintenance:expenditurewillcontinuetoreduceaswerealisethebenefitsofoursavingsinitiatives.Thesesavingsinitiativesincludepreventivemaintenanceoptimisation,changestoourvegetationstrategy,improvementsinwork-orderprioritisation,andtheresetofpriceswithserviceproviders.PreventivemaintenancesavingshavebeenrealisedbyrationalisingthetimeframesinwhichwecarryoutourscheduledtasksenablingustoreduceourforecastsacrossbothRCP2andRCP3.Ithasallowedustofurtheroptimiseworkandconcentrateonmorecriticalassets..

− Maintenanceproject:activityisexpectedtobeloweraswecandeferprogrammedworkbasedonimprovedaccuracyinourassetconditioninformation.Throughoptimisationandimprovedprioritisationofwork,wearemoreeffectivelyaddressingdeteriorationleadingtoareducedneedforinvasivemaintenanceprojectsandreducedcontactwitheachasset.Weexpecttofurtherimprovethisoptimisationaswemovetowardareliabilitycentredmaintenanceapproachandimplementimprovementstoourconditionassessmentprocess.

− Operating:weexpecttoreduceexpenditureontheseactivitiesin-linewiththelowermaintenanceworkvolumesdiscussedabove.Aswereducethenumberofinterventions,ourswitchingandassociatedexpenditurewillreduce.Additionally,asourremotemonitoringcapabilityincreasesweexpectlowerlevelsofon-siteactivity,reducingoverallcost.

− Training:expenditureontechnicaltrainingwilldeclineoverbothRCP2andRCP3.Thisisduetoanincreasedemphasisone-learning,ensuringtrainingistargetedandeffective,andthroughskillsandknowledgeretentionleadingtolowerlevelofre-training.Thismeansthatwhiletrainingstandards,particularlysafetyrelated,arebeingmaintained,reducedre-training

0

$20M

$40M

$60M

$80M

$100M

$120M

$140M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

Grid Opex

All figures in 2015/16 prices

INTEGRATED TRANSMISSION PLAN : 2016 28

willloweroverallcosts.Aimportantenablerofthisisreducedserviceproviderturnoverfacilitatedbyimprovedworkcertaintyandlonger-termplanning.

INTEGRATED TRANSMISSION PLAN : 2016 29

7. ICT AND BUSINESS SUPPORT

ThischapterincludestheremainderofourITPPeriodforecasts.Itssetsout:

− CapexandOpexforecastsforourICTfunctionsandacomparisonwithITP2015forecasts− BusinessSupportCapexandCorporateOpexandacomparisonwithITP2015forecasts.

7.1. ICT CAPEX WecontinuetoimprovetheprocesseswithwhichwemanageourICTexpenditure.DuringtheITPperiod,ourinvestmentfocushasshiftedfrombuildingnewcapabilitytoensuringcontinuedsupportandmaintenanceofourexistingsystems.Themainexceptiontothisisthecontinuinginvestmentindevelopingourassetmanagementcapability.

FurtherdetailonourICTprogrammesisincludedinPart4oftheAssetManagementPlan.ItdiscussesourapproachtomakingtheseinvestmentsandourkeyRCP2investments.

Figure14:ICTCapex

BasedonourrefinedICTCapexforecastsweexpecttocommissionassetswithatotalvalueof$166mduringRCP2.Thisis$9mbelowtheITP2015forecast,a5%reductioninexpectedCapex.Thechangingprofileismainlyduetotimingchangesinlargeprojectsandemergingrequirements,includingtheneedforincreasedsecurity.Examplesaresetoutbelow.

− SCADA:ourSCADA12andenergymanagementsystemswillrequireupgradesin2019/20.− Cybersecurity:wewillenhancetheprotectionofcriticalICTinfrastructurefrompotential

intrusion.

WhiletheoveralltrendinRCP2isdownward,weexpectexpendituretoincreasethroughtothemiddleofRCP3,duetothe‘lumpy’natureofcertainlargeprojectsandtheirtimingduringthe

12 SupervisoryControlandDataAcquisitionsystem.

0

$10M

$20M

$30M

$40M

$50M

$60M

$70M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

ICT Capex - Commissioned Value

All figures in 2015/16 prices

INTEGRATED TRANSMISSION PLAN : 2016 30

period.ThisincludestherenewalofourTransGOcommunicationsnetwork,andlifecyclereplacementofourunderseafibrecables.WeexpectthatRCP3willseeareductionininfrastructurerefreshexpenditureasweincreasetheuseofcloud-basedservicesfornon-criticalfunctions.

InsomeareasitisdifficulttopredictwithcertaintywhattechnologieswewillcommissionovertheITPperiodortheexacttechniquesthatwewillusetodeliverthem.Maintainingadegreeofflexibilityhastheadvantageofallowingustoconsideremerging,cost-effectivetechnologiesandtoadoptthemiftheyaresufficientlymature.Reflectingthiswewillcontinuetorefineourforecastsovertheperiod.

7.2. ICT OPEX ICTOpexincludestelecommunicationsandequipmentleases,outsourcedsupportandmaintenancefees,andsoftwarelicences.

FurtherdetailonourICTOpexforecastcanbefoundinITPSchedule4.

Figure15:ICTOpex

Weexpecttoincuratotalof$204mICTOpexduringRCP2.Thisis$11mbelowtheITP2015forecast,whichequatestoa5%reduction.OurforecastiswellbelowourRCP2allowanceandreflectsthesavingswearerealisinginthefollowingareas.

− Networkleasecosts:expenditurewillreduceaswerealisethebenefitsofsuccessfulcontractrenegotiationandscoperationalisation.

− Data-centrecosts:havebeenreducedbelowpreviousforecastsduetoinfrastructurerationalisation.

− Licensing:wearefocussingonimprovingourcapacityplanningandlicensingmanagement,andontheintroductionofopensourcetechnologiesinappropriateareas.

Weexpect thatRCP3expenditureswillbebroadlyconstant fromtheendofRCP2despiteupwardcostpressures.ThisreflectsthecostreductioneffortswhichwillcontinuethroughtheremainderoftheITPPeriod.

0

$10M

$20M

$30M

$40M

$50M

$60M

$70M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

ICT Opex

All figures in 2015/16 prices

INTEGRATED TRANSMISSION PLAN : 2016 31

7.3. BUSINESS SUPPORT CAPEX OurBusinessSupportcategorycoversthebalanceofourCapex,includingitemssuchasofficebuildings,officefurniture,andvehicles.

FurtherdetailonourBusinessSupportassetsareincludedinPart5oftheAssetManagementPlan.

Figure16:BusinessSupportCapex

BasedonourrefinedBusinessSupportCapexforecastweexpecttocommissionassetswithatotalvalueof$30mduringtheremainderofRCP2.Thisis$9mbelowtheITP2015forecast,whichequatestoanreductionof23%.OurrevisedforecastisbelowourRCP2allowance.

ThemainvarianceisduetonotgoingaheadwiththeIslingtonlogisticssupplydepotandlowercostsassociatedwiththeWellingtonheadofficeandPalmerstonNorthofficerelocations.

0

$5M

$10M

$15M

$20M

$25M

$30M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

Business Support Capex - Commissioned Value

All figures in 2015/16 prices

Base Capex does not include Identified Conductoring Projects

INTEGRATED TRANSMISSION PLAN : 2016 32

7.4. CORPORATE OPEX OurCorporateOpexforecastincludesexpenditureonactivitiesthatsupporttheprovisionoftransmissionservices.Itincludesdirectstaffcostsandexternalspecialistadvice,investigationcosts,insurance,travel,accommodation,andancillaryservices.Itincludesstaffcostsassociatedwithnetworkandoperationalsupport,andassetmanagement.

FurtherdetailonourCorporateOpexforecastcanbefoundinITPSchedule4.

Figure17:CorporateOpex

Weexpecttoincuratotalof$572mCorporateOpexduringRCP2.Thisis$26mbelowtheITP2015forecast,whichequatestoa4%reduction.Aspartofourtransformationprogramme,wehavesuccessfullytargetedandrealisedanumberofefficienciesacrossouroperations.ReflectingtheseandourexpectationsforfurthersavingsduringtheperiodwehavereducedourforecastbelowtheRCP2allowance.

WeexpectthatRCP3expenditureswillbebroadlyin-linewithour2019/20expenditure.Thisreflectsourcontinuingcostreductionefforts.

0

$20M

$40M

$60M

$80M

$100M

$120M

$140M

$160M

15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25

ITP 2015

ITP 2016

RCP2 Allowance

Corporate Opex

All figures in 2015/16 prices