integrating a revised competing values framework to...

TRANSCRIPT

Integrating a Revised Competing Values Framework to Identify Perceived

Values of Certified Environmental Management Systems Firms in Japan and

the United States

Eunjung Shin, PhD Candidate, University of Illinois at Chicago1

Eric W. Welch, Associate Professor, University of Illinois at Chicago

Prepared for the Public Value Consortium Biennial Workshop, Chicago, June 4-6 2012

Abstract:

Studies on environmental management systems (EMSs) are often dominated by economic

approaches explaining organizational behavior as a function of utility. However, values that

cannot be reduced to economic utility have also been discussed as critical elements of EMS

policy. It is therefore appropriate to investigate the range of firm organizational values related to

environmental practices and to better understand the role that values play in firms’ willingness to

adopt EMS programs.

This paper takes an alternative approach by applying Quinn and Rohrbaugh’s (1981; 1983)

competing values framework to examine organizational environmental strategy. The revised

competing values framework developed in this paper embraces tensions among organizational

values (i.e. internal control versus external adaptability) and delineates the tensions between

environmental and economic values.

Using data from two comparative national surveys of environmental practices in US and Japan

firms, this paper empirically examines the multi-dimensionality of organizational values that are

associated with private environmental management practices. It considers the potential for

variation in public values at the national level and identifies different value trade-offs that may

exist across nations of similar socio-economic status. The multi-dimensionality of competing

values revealed will increase understanding about why economic uni-dimensional rational

models are unlikely to fully explain organizational behavior.

1

Corresponding author, Email: [email protected]

1

I. Introduction

Environmental management systems (EMSs) have been widely adopted across sectors and

nations since the mid-1990s (Rennings et al. 2006; Mori and Welch 2008; Potoski and Prakash

2005). Still, most discussions have focused on the economic values associated with the adoption

of EMSs in the private sector by simply assuming that companies are driven by economic utility

(Anton, Deltas, and Khanna 2004; Khanna and Anton 2002). Only a few studies address

individual beliefs or organizational values associated with firms’ adoption of EMSs (El Dief and

Font 2012; Rivera and de Leon 2005). They identify that organizational or managers’

commitment to environmental values or that altruistic values heavily influence organizational

decisions to adopt environmental management practices.

Despite the limited acknowledgement of the complexity of firms’ values related to

environmental practices, organizational values have been continuously identified as critical

factors driving organizational behavior and action (Van Der Wal, Graaf, and Lasthuizen 2008;

Cyert and March 1963). One of the meaningful insights on organizational values is Quinn and

Rohrbaugh’s (1983, 1981) competing value framework. Based on this framework, we propose to

develop a competing value framework that includes two main dimensions – internal control and

external adaptability – and two primary values – economic and environmental.

Using data from a comparative survey on facility-level environmental practices in the US and

Japan, this paper empirically examines the applicability of the competing values framework for

understanding private environmental management practices. Perceptual maps, developed using

multi-dimensional scaling, visualize the distances among different organizational values and

strategies and allows comparison of organizations across two national cases.

The rest of this paper consists of five sections. The next section presents a brief introduction on

environmental management systems (EMSs) including its history and global practices. The

following section critically reviews previous literature on the adoption of EMSs and presents a

new competing values framework explaining firm adoption behavior. The next section

introduces particular features of national EMS cases, Japan and US and explains the data

collection conducted in both countries. This is followed by findings from the descriptive

2

statistics and the multi-dimensional scaling for two national cases. The paper concludes with a

discussion of the implications of the findings for current and future public values research.

II. Environmental Management Systems

Environmental Management Systems (EMSs) broadly refer to a set of management processes

that enable facilities to systematically reduce their impact on the natural environment. EMSs

often involve multiple activities such as developing and implementing a written environmental

policy, devising environmental performance goals and indicators and evaluating performance

with them, providing an environmental training program for employees, and conducting internal

environmental audits (Darnall and Kim 2012; Anton, Deltas, and Khanna 2004).

Various programs for EMSs have been developed since the middle 1990s (Shin and Welch 2012).

They include public-private partnership programs (e.g. the National Biosolids Partnership) that

are mainly adopted in local or national levels. They also include international initiatives and

certification standards, such as the International Standards Organization’s ISO 14001, the

European Union’s the Eco-Management and Audit Scheme (EMAS), and the EU ISO 14001 that

integrates ISO 14001 into EMAS. Adoption of EMSs among firms has continuously increased

over time. For instance, ISO 14001, one of the most widely adopted EMSs, has been increasingly

adopted by facilities in the world since its establishment in 1996 (Melnyk, Sroufe, and Calantone

2003). As of 2010, over two million facilities in 155 countries have been ISO 14001 certified

(ISO 2010).

EMSs are primarily voluntary environmental programs (Khanna and Anton 2002). Several

national and regional governments including the United States, European Union, Australia and

Japan have encouraged firms to adopt EMSs in order to minimize administrative and monitoring

costs associated with mandated regulations and to help firms self-manage environmental

performance (Darnall and Kim 2012). The firm self-reporting and self-regulation parts of EMSs

are also advocated as an alternative way to create incentives for firms to produce environmental

public goods beyond the requirements imposed by government regulations (Prakash and Potoski

2012).

3

Prior research has intensively examined the linkage between economic utility and firms’

practices regarding EMSs. Firms’ adoption of EMSs is often understood as a rational choice in a

response to the expected benefits overweighing costs (Khanna and Anton 2002; Delmas and

Terlaak 2001). Expected economic benefits include cost reductions based on the integrated

resource management and improved energy efficiency, tax incentives and government subsidies,

sale increase and new market opportunities (Khanna and Anton 2002). Moreover, economic

utility associated with ISO 14001 certification is described as club goods which can be accessed

and shared only by club members (Potoski and Prakash 2005b). In other words, firms can get

access to other club members, ISO certified suppliers and buyers. Potoski and Prakash (2005)

add that ISO certification functions as a signal to outside entities so that firms can be recognized

by regulators or customers. Furthermore, recent studies understand certification to be an

instrument for reducing the risk and uncertainty associated with information asymmetry between

suppliers and potential buyers (Potoski and Prakash 2009; King, Lenox, and Terlaak 2005).

Nonetheless, firms’ value-orientations beyond economic utility have been rarely examined (Mori

and Welch 2008). Only a few studies address individual beliefs or organizational values

associated with firms’ adoption of EMSs (El Dief and Font 2012; Rivera and de Leon 2005;

Anderson and Bateman 2000). Top decision makers or managers who are involved in

environmental activities (Prakash 1999) or others who are critical sources of knowledge (Rivera

and de Leon 2005) are found to be influential for firms’ environmental practices. Anderson and

Bateman (2000) show that a strong “environmental paradigm” embodied in an organization

generates environmentally desirable organizational practices and outcomes in U.S. businesses. El

Dief and Font (2012) report that Egyptian hotels tend to plan or implement EMSs when

environmental engineers of the hotels show stronger commitment to environmental or altruistic

values.

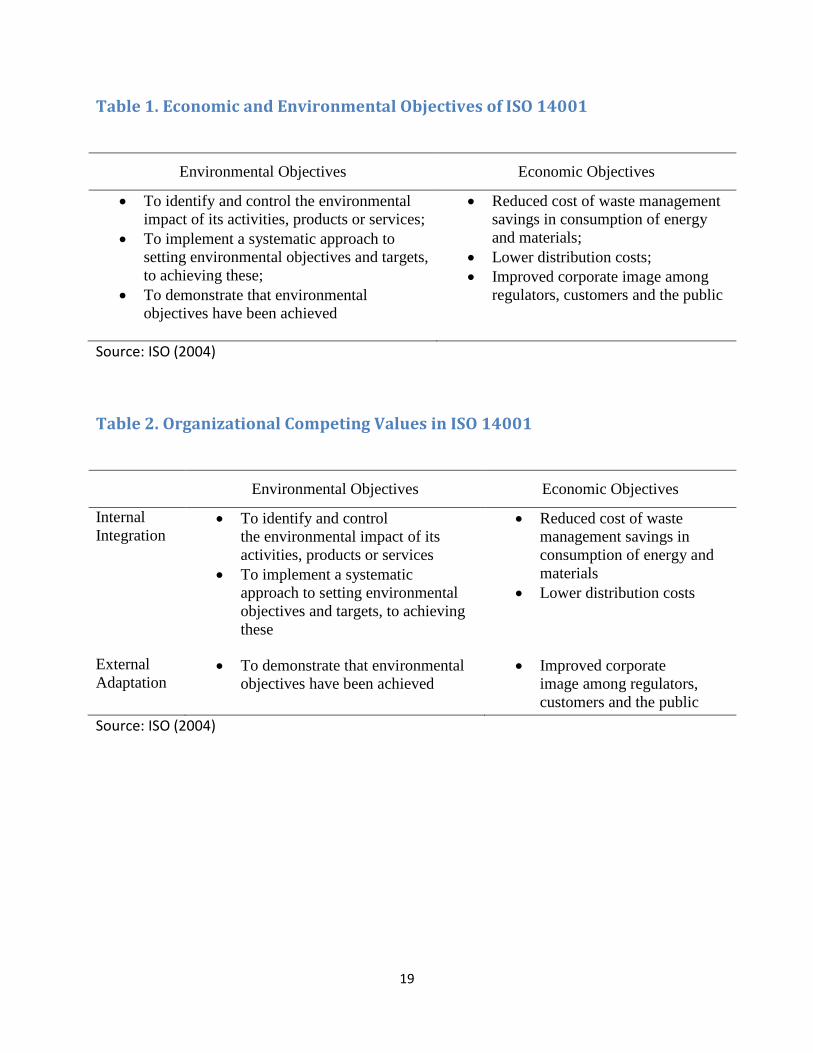

[Table 1 Here]

Because EMS programs highlight both environmental and economic objectives, firm adoption

likely involves the expression of both environmental and economic values. While the dual

objectives are explicitly discussed in EMS programs or EMS-related policies, prior studies on

have not fully examined a role that firm value orientations have on adoption. For instance, ISO

14001 embraces two intentions: (1) enhancing environmental performances, and (2) reducing

4

costs and increasing profits (Melnyk, Sroufe, and Calantone 2003). Table 1 briefly shows the

major economic and environmental ISO 14001 objective statements. EMAS further articulates

environmental objectives emphasizing organizations’ environmental obligations (EU 2012).

Margot Wallstrom, the former official in the European Commission for the Environment

elaborates the dual objectives of EMSs:

“An EMS is a tool that provides organizations with a method to systematically manage and

improve the environmental aspects of their production processes. It helps organisations to

achieve their environmental obligations and performance goals” (excerpted from EU 2012).

Given the dual objectives in several EMS programs, it is reasonable that both economic utility

and environmental commitment influence organizational adoption decisions. Moreover, whether

or not organizations adopt EMS programs likely depends upon the mix of values they hold.

II. Competing Values in EMSs

Organizational studies have continuously identified organizational values having a potential

influence on particular organizational behaviors and actions (Van Der Wal, Graaf, and

Lasthuizen 2008; Cyert and March 1963). Scott (2003), for example, suggests that organizations

adopt different objectives depending on whether they perceive themselves to operate according

to a rational system, an open system or a natural system. Organizations in a rational system value

productivity or efficiency of internal systems, whereas those in a natural system consider both

productivity and internal cohesion and morale, which contribute to sustaining the unit.

Organizations perceiving an open system search for focal organizational values vis a vis their

external environment in ways that enable adaptation, resource acquisition, and survival.

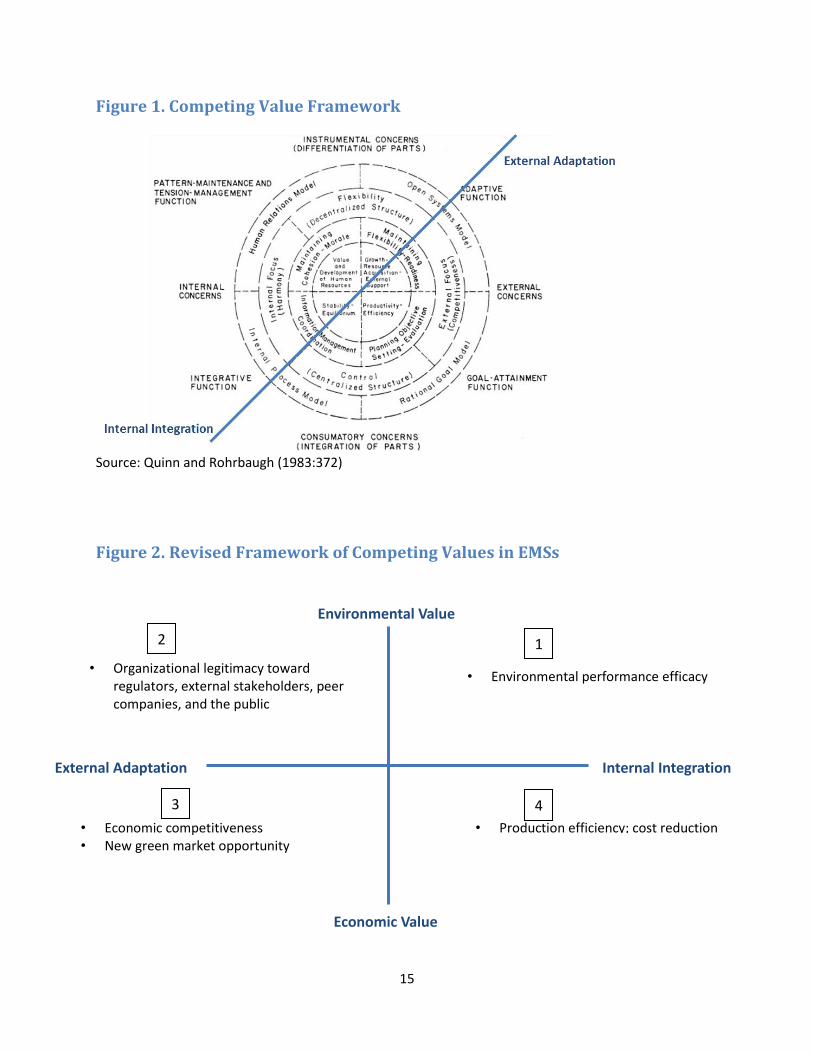

Quinn and Rohrbaugh’s (1983, 1981) competing value framework delineates the multiple

tensions among underlying organizational approaches; they test the framework using multi-

dimensional scaling analysis to assess organizational effectiveness. They first identify the three

major tensions that exist between 1) flexibility in an open system and internal control in a closed

system, 2) organizational structure and people, and 3) means and goals (Quinn and Rohrbaugh

1981). In later work, they further develop the competing values framework by mapping the

arrays of competing values into one framework (Quinn and Rohrbaugh 1983) (Figure 1).

5

[Figure 1 Here]

This framework shows how organizational core values, instrumental values, effectiveness criteria,

and strategies align and contrast. Four different organizational outcomes in the inmost circle are

aligned with the four different middle-range models of organizational effectiveness in the outer

most circle. For example, the core value of flexibility is aligned with the open system model,

whereas the core value of efficiency is associated with the rational system model.

The competing values framework contrast two main dimensions, one contrasts internal values

and external values, the other contrasts flexibility and control. Shown as a highlighted line in

Figure 1, an axis captures the tensions that exist between two competing middle-range values:

internal integration and external adaptation (Figure 1). We borrow this axis of internal

integration vs. external adaptation as one dimension of our revised public values framework for

understanding firm adoption of EMSs. We can now return to the stated objectives of ISO 14001

(Table 1) to further specifying economic and environmental dimensions as related to internal

integration or external adaptation (Table 2).

[Table 2 Here]

Internal integration is closely related to internal control mechanisms which are designed for

productivity or efficiency in a closed system (Scott 2003). It can be also associated with internal

communication and socialization processes through which individual members operate as a

cohesive and collective unit (Scott 2003; Quinn and Rohrbaugh 1983). Internal integration of

firm economic and environmental activity is an inherent value of EMSs (Karapetrovic and

Jonker 2003). To establish a successful EMS, it is necessary to understand how resources and

energy flow throughout the entire facility. Linking financial accounting with environmental

accounting is also recommended for an integrated management (De Moor and De Beelde 2005).

Moreover, employee training and education is emphasized in order to increase the awareness of

EMSs and build an internal consensus on EMSs.

At the same time, external adaptation is a means of organizational survival and growth since

most organizations are influenced by the external environment (Katz and Kahn 1966; Thompson

2003). In a large sense, firm viability depends on ability to adapt to market changes. In addition,

firms attempt to reduce their dependence on external entities, increase their control over them,

6

and eventually enhance their viability in the market. In a complex networked society, external

entities linked to firms include regulators, suppliers, consumers, and other stakeholders at the

local, regional, national and international levels. Firms sometimes adopt EMSs in order to signify

other business partners that they are equipped with an acceptable level of environmental

performance standards (Melnyk, Sroufe, and Calantone 2003; Potoski and Prakash 2009). Firms

sometimes adopt EMSs in order to reduce regulatory oversight by government and non-profit

entities or maintain good relationships with other stakeholders such as environmental groups or

consumer groups (Lyon and Maxwell 2004). Dowling and Pfeffer (1975) interpret the external

adaptation as an organizational strategy to obtain organizational legitimacy from external

environments. Organizational legitimacy can be driven by market values but also be driven by

other societal and public values that are possessed by business partners, regulatory entities,

consumers, watch groups and stakeholders and the public.

In sum, we propose an environmental competing values framework that can be used to

understand firm adoption of EMS programs (Figure 2). The framework has two dimensions: one

that captures environmental versus economic values and another that distinguishes of internal

integration versus external adaptation. The two different dimensions give rise to four quadrants.

[Figure 2 Here]

Quadrant one and two address environmental values. Quadrant one – environmental values as

internal integration – depicts the situation in which, based on the organization’s commitment to

the environment, it aims to enhance environmental performance of internal systems, such as a

reduction of wastewater or increased energy efficiency. Quadrant two – environmental values as

external adaptation – identifies a situation in which an organization values environmental

practices as a means of gaining legitimacy and social support from an external actors, such as

environmental groups or regulatory entities.

Quadrants three and four identify economic values associated with environmental behavior of

organizations. Quadrant three presents a situation in which an organization considers that

environmental behavior leads to economic competitiveness, creation of new markets or business

opportunities. It captures realization of economic utility through interaction with external entities,

such as increased sales, tax reduction or government subsidies, or other benefits associated with

7

the access to environmentally-conscious suppliers and buyers in national, regional and

international levels. Quadrant four depicts the case in which an organization is primarily driven

by attainment of economic utility through internal systems, such as when costs of production are

reduced through improved internal efficiencies.

III. Cases, Data, and Methods

In the remainder of this paper the proposed competing value framework is applied to empirically

examine managers’ responses on organizational values obtained from a comparative national

survey of environmental practices in US and Japan firms.

The analysis compares US and Japan cases in terms of the way in which multiple competing

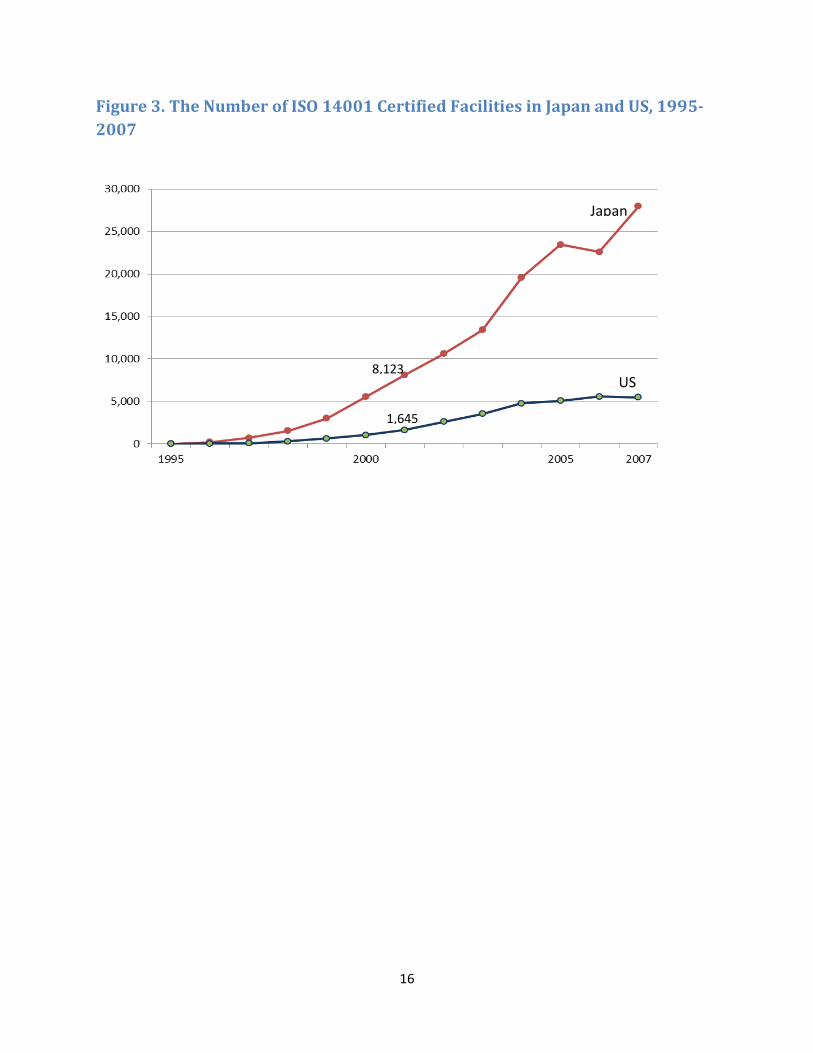

values are constructed in the private firm level. A comparison of US and Japan cases are

meaningful given the big difference in firms’ adoption of EMSs. Japan is by far the world leader

in ISO 14001 since over twenty percent of ISO certified facilities are Japanese facilities as of

2002. On the other hand, the US remains as a moderate participant of ISO 14001 with relatively

low adoption rates (Welch, Rana, and Mori 2003). The gaps in adoption between US and Japan

has increased over time (Figure 3), which further motivates a comparative study investigating a

difference in underlying value components associated with firms’ environmental practices.

[Figure 3 Here]

Survey data were simultaneously collected from private firms in Japan and the United States

between March and May 2001. For both surveys, a sample frame was constructed with one

primary stratum - ISO adoption – in which populations of adopter and non-adopter firms in the

US and Japan were identified. The Japanese sample was further stratified by four industry

substrata: electronics, electrical power, electric machinery and chemical manufacturing. The US

sample was stratified with nine industry substrata. They include five more industry substrata in

addition to the ones used in the Japan survey: chemicals and allied products, rubber and plastics,

primary metal industries, fabricated metal products, paper and allied products, transportation

equipment. These five industry substrata were added to the US sample mainly because too few

firms in the original four industry substrata had adopted ISO 14001. For both surveys, firms were

randomly selected within the substrata, and a manager of each firm was invited to the survey.

8

In the US case, a initial random sample of 726 ISO adopter facilities and a random sample of

1,675 non-adopter facilities was reduced after verification to a sample of 698 valid ISO adopters

and 1,489 non-adopters. In total, 2,187 facilities were invited. Of the invitees, 143 (20.5%)

adopters and 97 (6.5%) non-adopters returned their completed or partially completed responses,

which results in a combined total response rate of 11.0%. This low response rate creates

potential for bias; however, it is not an unusual rate for environmental surveys of private-sector

firms (Melnyk, Sroufe, and Calantone 2003). Additional analysis indicates that, in general,

responses by industry and by size do not differ significantly from proportions in the random

sample (Welch, Rana, and Mori 2003). Nevertheless, generalization from this US sample to the

population of US facilities in these industries is limited and should be done with care.

For the Japanese survey, a total of 3,227 facilities were randomly selected: 1,515 ISO adopters

and 1,712 non-adopters. Of the total invitees, 1,237 (82%) adopters and 481 (28%) non-adopters

returned complete or partially complete responses, which resulted in a total response rate of 56%.

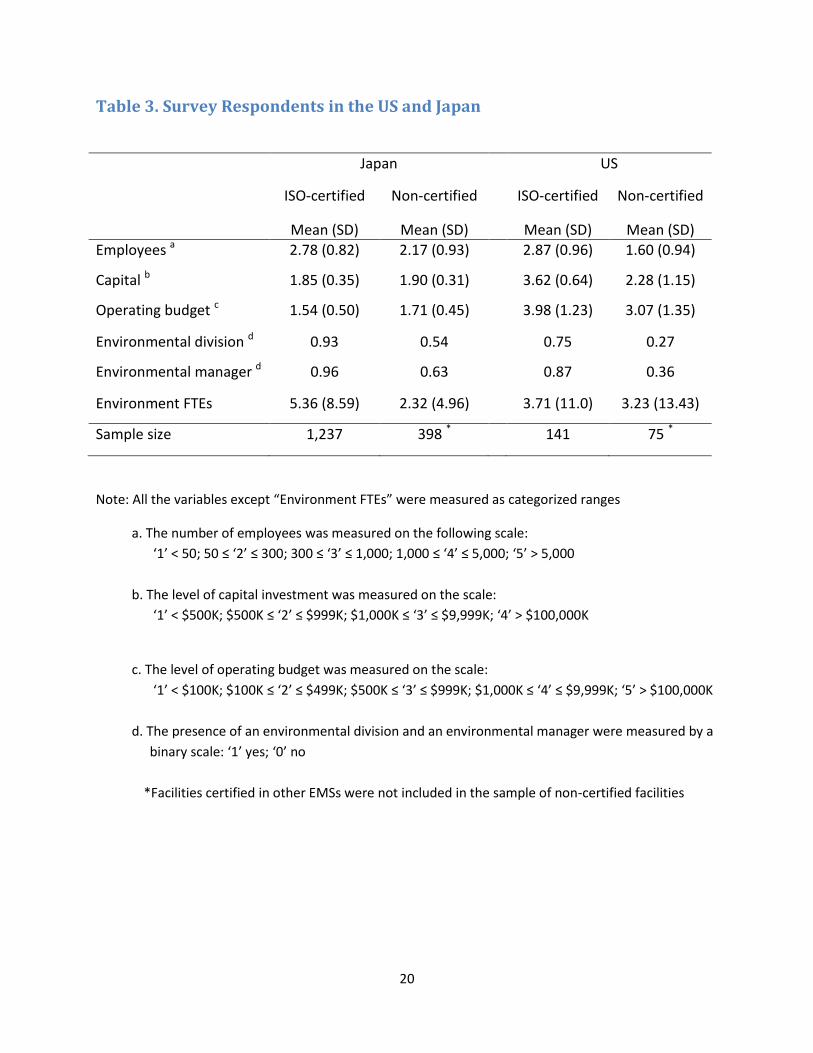

Table 3 provides basic information for the survey respondents. On average, US firms have

relatively larger capital and operating budgets than their Japanese counterparts. The proportion

of facilities having an environmental division or an environmental manager is Japan is higher

than in the US. At the same time, ISO certified facilities reported having more full-time

employees who spend a majority of their time on environmental issues compared to non-certified

facilities both in Japan and the US.

[Table 3 Here]

Both surveys included identical questions on environmental vs. economic values of EMSs in

addition to organizational characteristics. Firm manager responses to questions about the value

of EMS programs and ISO 14001 were used as measures of competing values at the

organizational level. Based on the environmental competing value framework developed in this

paper, four sets of organizational values were measured; they are (1) environmental values as

internal integration, (2) environmental values as external adaptation, (3) economic values as

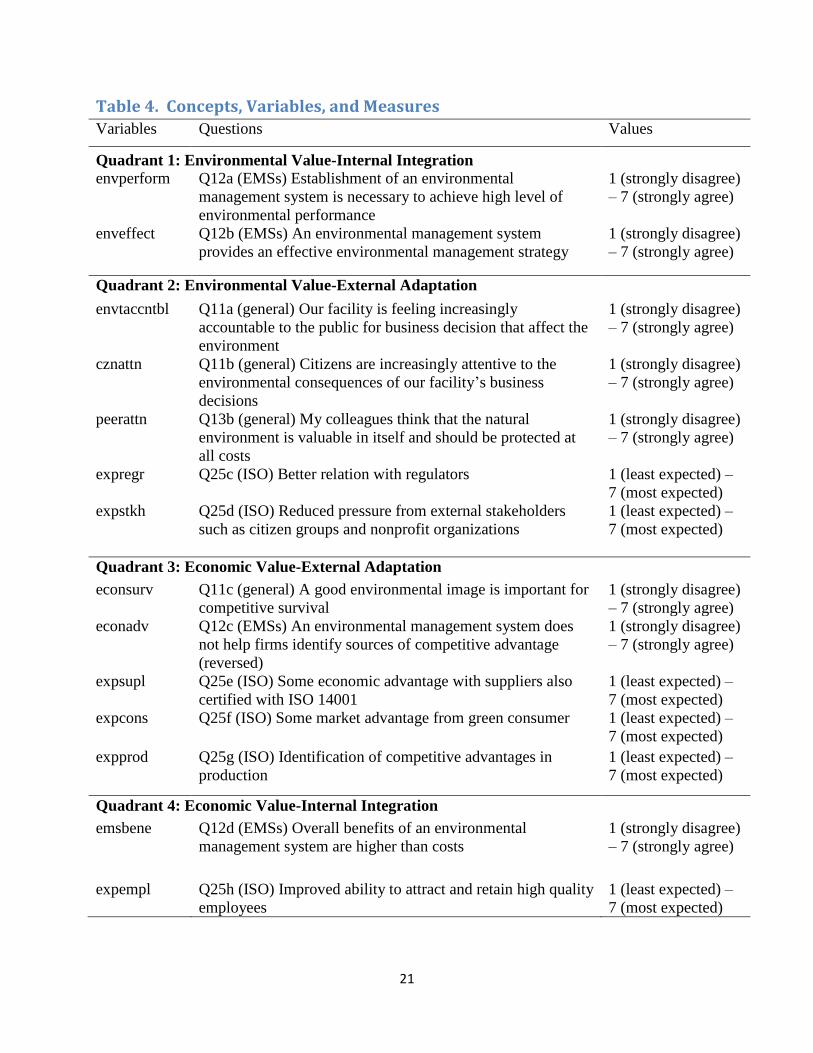

external adaptation, and (4) economic values as internal integration. Table 4 presents the details

of value measures.

[Table 4 Here]

9

We first compare value orientations of Japanese firms with the value orientations of US firms.

We further compare national differences overall and national differences among ISO-certified

facilities. For each nation, ISO adopters and non-adopters were further compared. Chi-square

tests were used to identify significant differences across nations.

Second, we conducted multi-dimensional scaling in order to empirically test the relevance of the

proposed environmental competing value framework in this paper. Multi-dimensional scaling

allows us to assess the distances among different value measures and pinpoint each measure in a

multi-dimensional space (Jacoby 1991). This method is especially useful for developing middle-

range models depicting similarity and dissimilarity among sets of measures and linking them

with theoretical constructs or grand concepts (Quinn and Rohrbaugh 1983).

For the analysis, a Euclidean distance matrix was created based on the individual survey

responses on value questions. Then, a set of points were identified in a multi-dimensional space

where each point represents one of the objects and the distances between points. We used

ALSCAL (Alternating Least Squares SCALing) algorism developed by Takan, Young and de

Leeuw (1977). It is a relatively flexible and versatile method because it allows us to analyze

various types of data and data having some missing observations (Cox and Cox 2001). The

dissimilarity among value measures in Japan and US was examined respectively, whereas values

reported by ISO adopters and non-adopters were simultaneously analyzed using individual

difference scaling for each nation.

IV. Findings

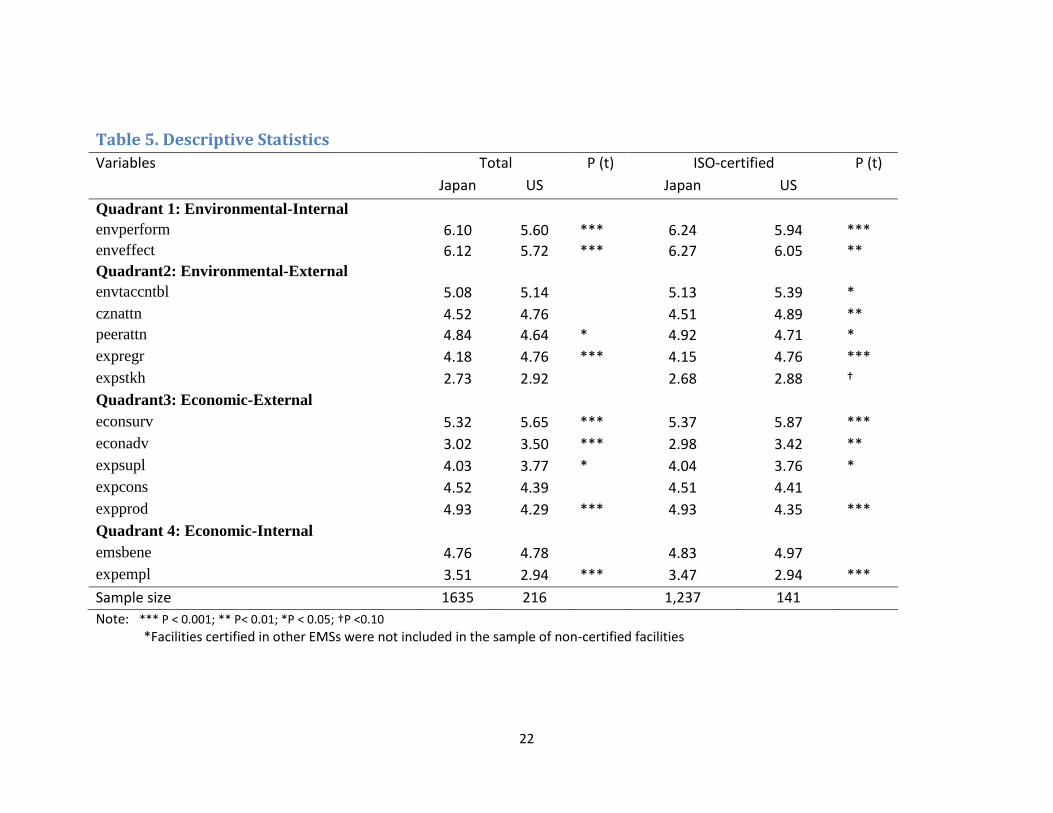

First, organizational values regarding EMSs were compared by country (Table 5). Japanese

firms scored higher in questions on the value of internal integration for both environmental and

economic aspects than US firms did. Compared to US firms, Japanese firms expressed stronger

agreements with the statements: “EMSs is necessary to achieve high level of environmental

performance” and “EMSs provide an effective environmental management strategy”. Japanese

firms also reported higher expectations of EMSs as a means of attracting and retaining high

quality employees. The positive view of EMSs as a means of internal management and

integration found in Japanese firms may be attributed to a strong tradition of total quality

10

management (TQM) in Japan. As one of the TQM initiators, Japanese firms have widely

developed an integrated quality management system. As EMSs generally include major policies

and quality management activities (Melnyk, Sroufe, and Calantone 2003), close linkage between

quality management system and the ISO 14001 has been observed previously (Karapetrovic and

Jonker 2003). A heritage of quality management in Japan may result in strong internal

integration values that favor EMS program adoption in that country.

[Table 5 Here]

By contrast, US firms value of EMSs effects on relations with outside entities, such as regulators,

suppliers and customers. Firms’ expectations on better relations with regulators are particularly

higher in US compared to ones in Japan. That may indicate national differences in government-

business relations. Scholars have found that business-government relations in the US are more

adversarial than in Japan (Welch, Rana, and Mori 2003; Kollman and Prakash 2002). US

governments are reported to rely more on command-and-control regulations compared to

Japanese governments which have built more reciprocal and cooperative relations with business

actors (Welch and Hibiki 2002). Given the adversarial relations with regulatory agencies, US

firms might have more proactively sought the benefits of EMSs in the relation with regulators.

Alternatively, US firms that adopted EMSs might have sought greater advantages with regulators

than Japanese firms. Since ISO certified facilities are fewer in US than ones in Japan, US

regulators might have recognized those firms’ commitment to environmental practices more

easily and granted business activities greater legitimacy, which eventually helps improve firms’

relations with regulators in the US. Similarly, firms’ marginal benefits granted by external

entities, such as suppliers, consumers, and citizens, might have been larger in the US because

firms’ EMS practices could be more visible and considered as more socially responsible in the

US society where there exist fewer firms adopting EMSs compared to Japan. US firms also

reported more positive attitudes to EMSs as a means of survival in a competitive market.

Compared to their Japanese counterparts, US facilities scored higher when they were asked about

the extent to which EMSs could be important for competitive survival or could help identify

sources of competitive advantage.

11

ISO-certified facilities tend to have more positive attitudes toward EMSs both in US and Japan.

As seen in Table 5, ISO adopters consistently reported favorable opinions on EMSs. To some

extent, it may indicate that value orientations can affect firms’ adoption of ISO 14001.

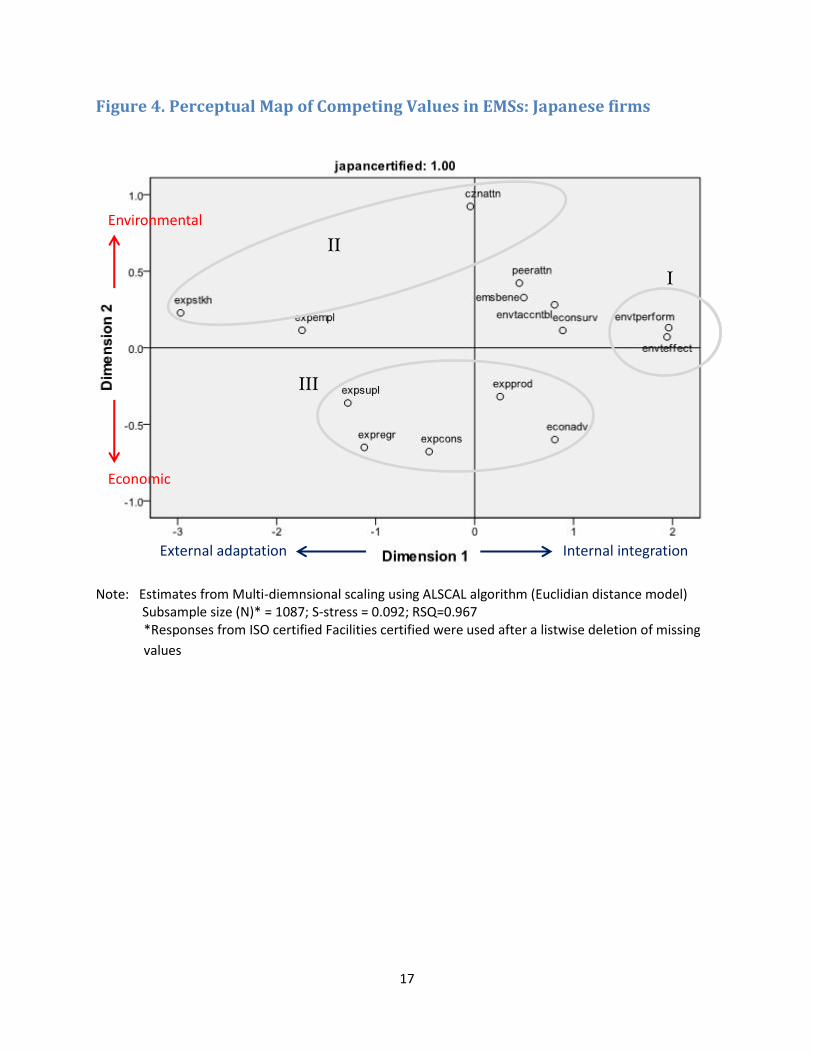

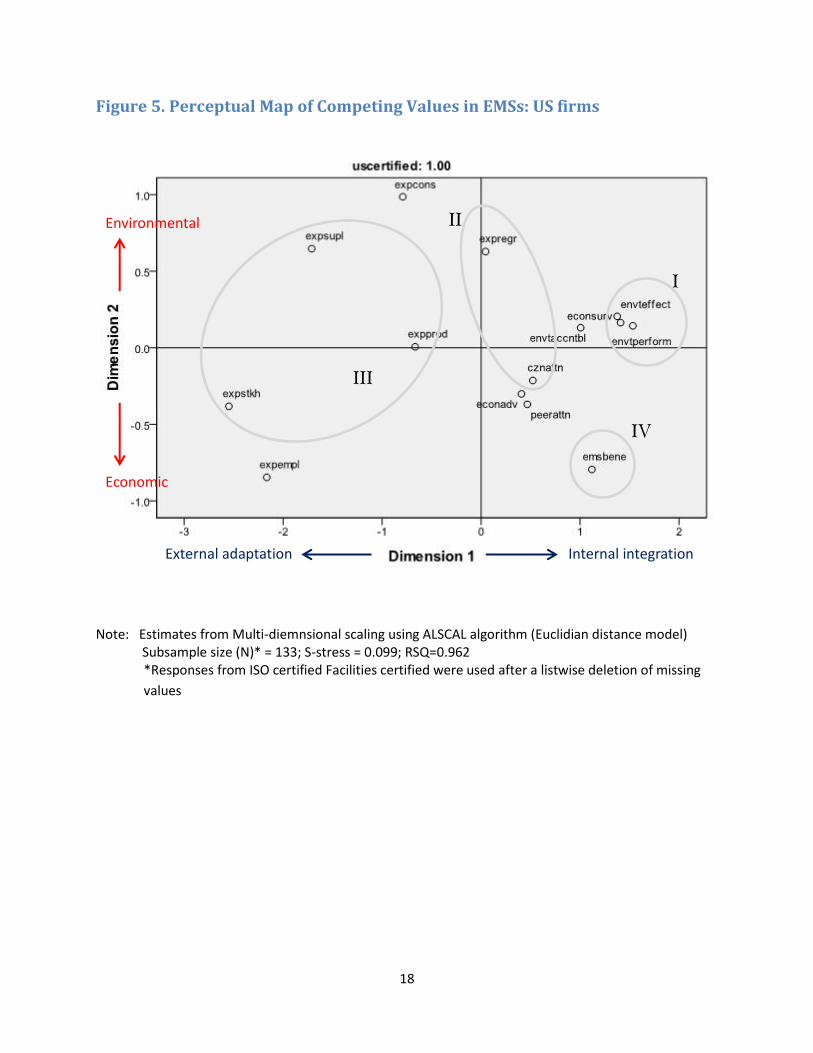

[Figure 4 Here]

[Figure 5 Here]

Second, we conducted multi-dimensional scaling and created perceptual maps in order to

uncover similarity and dissimilarity among sets of value measures and empirically examine the

relevancy of the competing value framework revised in this paper. Results from multi-

dimensional scaling are presented for Japan in Figure 4 and the US in Figure 5.

In general, we found that the value measures can be reduced into two dimensions as proposed in

the competing framework in this paper. Although multi-dimensional scaling specifically

indicates the most appropriate number of dimensions, a comparison of a two-dimensional model

with other models shows that the two dimensional model has the highest goodness of fit. Each

model’s goodness of fit was examined with Young’s S-stress index and RSQ. Young’s S-Stress

formula is a measure of statistical fit that ranges from 1 indicating the worst possible fit to 0

indicating a perfect fit. A rule of thumb is that a value of 0.1 or less is considered a good fit for a

two dimensional model (Blake, Schulze, and Hughes 2003). The RSQ value is the squared

correlation coefficient between the transformed distances and the raw data, which generally

indicates the variance explained by the distance model. The distance models in both Japan and

US reported relatively low stress with high explanatory power (notes in Figures 4 and 5).

The two dimensions depicted in the perceptual maps can be generally interpreted as the two

dimensions conceptualized in the framework: a dimension of economic versus environmental

values, and a dimension of internal integration and external adaptation.. Each quadrant in the

Japanese map depicts a set of value measures that reflect the framework (Figure 4). For instance,

quadrants 1 and 2 account for environmental values of EMSs, whereas quadrant 3 accounts for

economic values. At the same time, quadrant 2 and 3 include most of variables relating to a firms’

adaptation to external environment. Expected advantages from external entities are quite

distinctly set apart from internal values. However, the distinction between economic and

environmental values in the right quadrants (internal integration) are not as clear as expected.

12

The variable capturing benefits outweighing costs (‘emsbene’) is found near environmental

values, such as environmental performance and effectiveness (‘envperform’ and ‘envteffct’).

Similarly, the measure for competitive survival (‘econsurv’) is located close to other

environmental measures such as environmental performance (‘envtperform’) and environmental

effectiveness (‘envteffct’). This may indicate the tendency toward value congruence in which

economic and environmental values are closely linked together from the perspective of ISO

certified facilities in Japan. Hence, the proposed fourth quadrant on economic values in internal

integration is not separable enough from the first quadrant on environmental values in a case of

Japanese firms. At the same time, the expectation that ISO will have positive effects on attraction

and retention of high quality personnel (‘expempl’) is found near expectations about positive

effects on external stakeholders. This may indicate that firms perceive recruitment and

stakeholder interaction to both be elements of the external adaptation process. This may be also

attributed to measurement errors since the measures of expectations were captured in one multi-

item question. Measurement error issues can be also raised in the situation where environmental

accountability (‘envtaccntbl’) is similarly located near perceived importance of environmental

image for competitive survival (‘econsurv’). In general, the perceptual map of Japanese firms

distinguishes between internal and external values for both environmental and economic

perspectives. Still, the findings suggests a potential value congruence in which ISO certifiers

perceive simultaneous environmental and economic advantages when conceptualized as internal

integration.

The perceptual map of US firms also generally distinguishes between internal and integration

and external adaptation and environmental and economic values (Figure 5). Regarding firms’

orientation toward internal integration, we observe a certain level of clustering among value

measures. Like Japanese firms, US firms that are ISO 14001 certified perceive a certain level of

simultaneity among economic and environmental values as placement of competitive survival

(‘econsurv’) is near environmental performance (‘envtperform’) and environmental effectiveness

(‘envteffct’). Still, US firms differ from Japanese firms in that they consider the benefits

outweighing costs (‘emsbene’) to be distinctively different from the other environmental values.

This can reflect an early adoption stage in the US in which administrative and technical burdens

are high given the limited experience while realized economic returns are not large enough to

cover expenses. Regarding firms’ orientation toward external adaptation, the estimates are

13

somewhat puzzling because environmental values are not opposite to economic values but rather

parallel. This may indicate a potential mismatch between the estimated results and the conceptual

framework. This may also be attributed to unique contexts in which US firms associate their own

environmental performance with expectated benefits deriving from customers, producers, and

suppliers instead of the benefits accruing from stakeholders and employees.

All in all, findings show the potential applicability of the competing value framework to firms’

EMS practices. Distinction between internal integration and external adaptation is clearly evident

and economic values differ from environmental values. However, economic and environmental

values are somewhat intertwined for the firms who have already adopted ISO 14001 especially in

Japan. At the same time, findings raise questions on measurement errors because some variables

measured in the same question are found to be close each other despite expected conceptual

differences (e.g. ‘econsurv’ and ‘envtaccntbl’). Despite these concerns, the findings uncover the

multi-dimensionality of organizational values associated with EMSs.

V. Conclusion

As an exploratory study, this paper develops a revised environmental competing values

framework and identifies competing values in EMS practices of US and Japanese firms. It

compares US and Japan cases in terms of the way in which multiple competing values are

expressed using descriptive analysis and multi-dimensional scaling. Findings show some

similarities as well as differences between Japan and US firms in terms of their value

orientations. Discovery of differences in value orientations call for additional attention to

organizational values that are associated with broader institutional contexts and particular

organizational environmental practices including the adoption of EMSs.

This paper contributes to scholarly discussions on firms’ environmental practices. The identified

differences in organizational values encourage scholars to develop alternative approaches to the

rational economic model and to better link value commitment with environmental actions. The

interplay between regulatory and institutional arrangements and firms’ value orientations

represent a larger research agenda that would investigate further the findings in this paper.

14

This paper provides a meaningful study of public values at least for three reasons. First, as an

alternative view to an economic model, this paper presents a potential role of public values in

private firms’ environmental practices. It facilitates subsequent study of multi-dimensional

publicness (Bozeman and Bretschneider 1994; Rainey and Bozeman 2000) by further specifying

public dimensions of private firm environmental practices. It can be further developed as a study

of ‘realized publicness’ (Moulton 2009) and realized public outcomes, including environmental

performance. Second, the development of the conceptual model and its empirically testing

provide insights to help further develop an integrative framework of publicness, so-called

‘integrative publicness’ (Bozeman and Moulton 2011). As noted by Bozeman and Moulton

(2011), normative or empirical efforts have been not completely reconciled in previous

publicness literature. The conceptual model and perceptual mapping of this paper suggest an

alternative way to develop a middle-range theory. Lastly, this paper opens up a discussion on the

level of analysis in a study of public value by highlighting a need to specify values embedded at

specific entity types. Since public values are often discussed as inherent belief systems of

individuals or value-orientations embedded in public policies (Moulton and Bozeman 2011), an

effort to articulate organizational values in this paper is intended to motivate additional study on

public values at the organizational level.

15

Figure 1. Competing Value Framework

Source: Quinn and Rohrbaugh (1983:372)

Figure 2. Revised Framework of Competing Values in EMSs

Environmental Value

Economic Value

External Adaptation Internal Integration

• Organizational legitimacy toward regulators, external stakeholders, peer companies, and the public

• Economic competitiveness • New green market opportunity

• Environmental performance efficacy

• Production efficiency; cost reduction

2

3

1

4

16

Figure 3. The Number of ISO 14001 Certified Facilities in Japan and US, 1995-

2007

Figure 5. Euclidean Distances among Value Measures: US (certified)

Japan

US

1,645

8,123

17

Figure 4. Perceptual Map of Competing Values in EMSs: Japanese firms

Note: Estimates from Multi-diemnsional scaling using ALSCAL algorithm (Euclidian distance model) Subsample size (N)* = 1087; S-stress = 0.092; RSQ=0.967

*Responses from ISO certified Facilities certified were used after a listwise deletion of missing

values

Environmental

Economic

Internal integration External adaptation

I

II

III

18

Figure 5. Perceptual Map of Competing Values in EMSs: US firms

Note: Estimates from Multi-diemnsional scaling using ALSCAL algorithm (Euclidian distance model) Subsample size (N)* = 133; S-stress = 0.099; RSQ=0.962

*Responses from ISO certified Facilities certified were used after a listwise deletion of missing

values

Economic

Environmental

Internal integration External adaptation

I

II

IV

III

19

Table 1. Economic and Environmental Objectives of ISO 14001

Environmental Objectives Economic Objectives

To identify and control the environmental

impact of its activities, products or services;

To implement a systematic approach to

setting environmental objectives and targets,

to achieving these;

To demonstrate that environmental

objectives have been achieved

Reduced cost of waste management

savings in consumption of energy

and materials;

Lower distribution costs;

Improved corporate image among

regulators, customers and the public

Source: ISO (2004)

Table 2. Organizational Competing Values in ISO 14001

Environmental Objectives Economic Objectives

Internal

Integration

To identify and control

the environmental impact of its

activities, products or services

To implement a systematic

approach to setting environmental

objectives and targets, to achieving

these

Reduced cost of waste

management savings in

consumption of energy and

materials

Lower distribution costs

External

Adaptation To demonstrate that environmental

objectives have been achieved

Improved corporate

image among regulators,

customers and the public

Source: ISO (2004)

20

Table 3. Survey Respondents in the US and Japan

Japan US

ISO-certified Non-certified ISO-certified Non-certified

Mean (SD) Mean (SD) Mean (SD) Mean (SD)

Employees a 2.78 (0.82) 2.17 (0.93) 2.87 (0.96) 1.60 (0.94)

Capital b 1.85 (0.35) 1.90 (0.31) 3.62 (0.64) 2.28 (1.15)

Operating budget c 1.54 (0.50) 1.71 (0.45) 3.98 (1.23) 3.07 (1.35)

Environmental division d 0.93 0.54 0.75 0.27

Environmental manager d 0.96 0.63 0.87 0.36

Environment FTEs 5.36 (8.59) 2.32 (4.96) 3.71 (11.0) 3.23 (13.43)

Sample size 1,237 398 * 141 75 *

Note: All the variables except “Environment FTEs” were measured as categorized ranges

a. The number of employees was measured on the following scale:

‘1’ < 50; 50 ≤ ‘2’ ≤ 300; 300 ≤ ‘3’ ≤ 1,000; 1,000 ≤ ‘4’ ≤ 5,000; ‘5’ > 5,000

b. The level of capital investment was measured on the scale:

‘1’ < $500K; $500K ≤ ‘2’ ≤ $999K; $1,000K ≤ ‘3’ ≤ $9,999K; ‘4’ > $100,000K

c. The level of operating budget was measured on the scale:

‘1’ < $100K; $100K ≤ ‘2’ ≤ $499K; $500K ≤ ‘3’ ≤ $999K; $1,000K ≤ ‘4’ ≤ $9,999K; ‘5’ > $100,000K

d. The presence of an environmental division and an environmental manager were measured by a

binary scale: ‘1’ yes; ‘0’ no

*Facilities certified in other EMSs were not included in the sample of non-certified facilities

21

Table 4. Concepts, Variables, and Measures

Variables Questions Values

Quadrant 1: Environmental Value-Internal Integration

envperform Q12a (EMSs) Establishment of an environmental

management system is necessary to achieve high level of

environmental performance

1 (strongly disagree)

– 7 (strongly agree)

enveffect Q12b (EMSs) An environmental management system

provides an effective environmental management strategy

1 (strongly disagree)

– 7 (strongly agree)

Quadrant 2: Environmental Value-External Adaptation

envtaccntbl Q11a (general) Our facility is feeling increasingly

accountable to the public for business decision that affect the

environment

1 (strongly disagree)

– 7 (strongly agree)

cznattn Q11b (general) Citizens are increasingly attentive to the

environmental consequences of our facility’s business

decisions

1 (strongly disagree)

– 7 (strongly agree)

peerattn Q13b (general) My colleagues think that the natural

environment is valuable in itself and should be protected at

all costs

1 (strongly disagree)

– 7 (strongly agree)

expregr Q25c (ISO) Better relation with regulators 1 (least expected) –

7 (most expected)

expstkh Q25d (ISO) Reduced pressure from external stakeholders

such as citizen groups and nonprofit organizations

1 (least expected) –

7 (most expected)

Quadrant 3: Economic Value-External Adaptation

econsurv Q11c (general) A good environmental image is important for

competitive survival

1 (strongly disagree)

– 7 (strongly agree)

econadv

Q12c (EMSs) An environmental management system does

not help firms identify sources of competitive advantage

(reversed)

1 (strongly disagree)

– 7 (strongly agree)

expsupl Q25e (ISO) Some economic advantage with suppliers also

certified with ISO 14001

1 (least expected) –

7 (most expected)

expcons Q25f (ISO) Some market advantage from green consumer 1 (least expected) –

7 (most expected)

expprod Q25g (ISO) Identification of competitive advantages in

production

1 (least expected) –

7 (most expected)

Quadrant 4: Economic Value-Internal Integration

emsbene Q12d (EMSs) Overall benefits of an environmental

management system are higher than costs

1 (strongly disagree)

– 7 (strongly agree)

expempl Q25h (ISO) Improved ability to attract and retain high quality

employees

1 (least expected) –

7 (most expected)

22

Table 5. Descriptive Statistics

Variables Total P (t) ISO-certified P (t)

Japan US Japan US

Quadrant 1: Environmental-Internal

envperform 6.10 5.60 *** 6.24 5.94 *** enveffect 6.12 5.72 *** 6.27 6.05 **

Quadrant2: Environmental-External

envtaccntbl 5.08 5.14 5.13 5.39 *

cznattn 4.52 4.76 4.51 4.89 ** peerattn 4.84 4.64 * 4.92 4.71 *

expregr 4.18 4.76 *** 4.15 4.76 ***

expstkh 2.73 2.92 2.68 2.88 †

Quadrant3: Economic-External

econsurv 5.32 5.65 *** 5.37 5.87 ***

econadv 3.02 3.50 *** 2.98 3.42 **

expsupl 4.03 3.77 * 4.04 3.76 *

expcons 4.52 4.39 4.51 4.41

expprod 4.93 4.29 *** 4.93 4.35 ***

Quadrant 4: Economic-Internal

emsbene 4.76 4.78 4.83 4.97

expempl 3.51 2.94 *** 3.47 2.94 ***

Sample size 1635 216 1,237 141

Note: *** P < 0.001; ** P< 0.01; *P < 0.05; †P <0.10

*Facilities certified in other EMSs were not included in the sample of non-certified facilities

23

References

Anderson, Lynne M., and Thomas S. Bateman. 2000. INDIVIDUAL ENVIRONMENTAL INITIATIVE: CHAMPIONING NATURAL ENVIRONMENTAL ISSUES IN U.S. BUSINESS ORGANIZATIONS. Academy of Management Journal 43 (4):548-570.

Anton, W. R. Q., G. Deltas, and M. Khanna. 2004. Incentives for environmental self-regulation and implications for environmental performance. Journal of Environmental Economics and Management 48 (1):632-654.

Blake, Brian F., Stephanie Schulze, and Jillian M. Hughes. 2003. Perceptual Mapping by Multidimensional Scaling. In Methodology Series: Cleveland State University. http://academic.csuohio.edu:8080/cbrsch/home.html.

Bozeman, Barry, and Stuart Bretschneider. 1994. The `publicness puzzle' in organization theory: A test of alternative explanations of. Journal of Public Administration Research & Theory 4 (2):197.

Bozeman, Barry, and Stephanie Moulton. 2011. Integrative Publicness: A Framework for Public Management Strategy and Performance. Journal of Public Administration Research & Theory 21 (suppl_3):i363-i380.

Cox, Trevor F., and Michael A. Cox. 2001. Multidimensional Scaling. 2nd edition ed. New York: Chapman and Hall/CRC.

Cyert, Richard Michael , and James G. March. 1963. A behavioral theory of the firm, Prentice-Hall international series in management; Prentice-Hall behavioral sciences in business series.;. Englewood Cliffs, N.J.: Prentice-Hall.

Darnall, Nicole, and Younsung Kim. 2012. Which Types of Environmental Management Systems Are Related to Greater Environmental Improvements? Public Administration Review 72 (3):351-365.

De Moor, P., and I. De Beelde. 2005. Environmental auditing and the role of the accountancy profession: A literature review. Environmental Management 36 (2):205-219.

Delmas, Magali A., and Ann K. Terlaak. 2001. A framework for analyzing environmental voluntary agreements. California Management Review 43 (3):44.

Dowling, J., and J. Pfeffer. 1975. ORGANIZATIONAL LEGITIMACY - SOCIAL VALUES AND ORGANIZATIONAL BEHAVIOR. Pacific Sociological Review 18 (1):122-136.

El Dief, M., and X. Font. 2012. DETERMINANTS OF ENVIRONMENTAL MANAGEMENT IN THE RED SEA HOTELS: PERSONAL AND ORGANIZATIONAL VALUES AND CONTEXTUAL VARIABLES. Journal of Hospitality & Tourism Research 36 (1):115-137.

EU. Eco-Management Audit Scheme: What is Environmental Management? 2012. Available from http://ec.europa.eu/environment/emas/about/enviro_en.htm.

ISO. 2010. The ISO Survey 2010: International Standards Organisation. http://www.iso.org/iso/iso-survey2010.pdf.

Jacoby, William G. 1991. Data Theory and Dimensional Analysis. Newbury Park: CA: Sage Publication. Karapetrovic, S., and J. Jonker. 2003. Integration of standardized management systems: searching for a

recipe and ingredients. Total Quality Management & Business Excellence 14 (4):451-459. Katz, Daniel , and Robert Louis Kahn. 1966. Organizations and the system concept. In The social

psychology of organizations, edited by D. Katz and R. L. Kahn. New York: Wiley. Khanna, M., and W. R. Q. Anton. 2002. Corporate environmental management: Regulatory and market-

based incentives. Land Economics 78 (4):539-558.

24

King, Andrew A., Michael J. Lenox, and A. N. N. Terlaak. 2005. THE STRATEGIC USE OF DECENTRALIZED INSTITUTIONS: EXPLORING CERTIFICATION WITH THE ISO 14001 MANAGEMENT STANDARD. Academy of Management Journal 48 (6):1091-1106.

Kollman, KELLY, and ASEEM Prakash. 2002. EMS-based Environmental Regimes as Club Goods:Examining Variations in Firm-level Adoption of ISO 14001 and EMAS in U.K., U.S. and Germany. Policy Sciences 35:43-67.

Lyon, Thomas P. , and John W. Maxwell. 2004. Corporate environmentalism and public policy: Cambridge, UK ; New York : Cambridge University Press.

Melnyk, S. A., R. P. Sroufe, and R. Calantone. 2003. Assessing the impact of environmental management systems on corporate and environmental performance. Journal of Operations Management 21 (3):329-351.

Mori, Yasuhumi, and Eric W. Welch. 2008. The ISO 14001 environmental management standard in Japan: results from a national survey of facilities in four industries. Journal of Environmental Planning and Management 51 (3):421 - 445.

Moulton, Stephanie. 2009. Putting Together the Publicness Puzzle: A Framework for Realized Publicness. Public Administration Review 69 (5):889-900.

Moulton, Stephanie, and Barry Bozeman. 2011. The Publicness of Policy Environments: An Evaluation of Subprime Mortgage Lending. Journal of Public Administration Research & Theory 21 (1):87-115.

Potoski, M., and A. Prakash. 2005. Covenants with weak swords: ISO 14001 and facilities' environmental performance. Journal of Policy Analysis and Management 24 (4):745-769.

Repeated Author. 2005b. Green clubs and voluntary governance: ISO 14001 and firms’ regulatory compliance. American journal of political science 49 (2):235–248.

Potoski, Matthew, and Aseem Prakash. 2009. Information asymmetries as trade barriers: ISO 9000 increases international commerce. Journal of Policy Analysis and Management 28 (2):221-238.

Prakash, A. 1999. A new-institutionalist perspective on ISO 14001 and Responsible Care. Business Strategy and the Environment 8:322–335.

Prakash, Aseem, and Matthew Potoski. 2012. Voluntary environmental programs: A comparative perspective. Journal of Policy Analysis and Management 31 (1):123-138.

Quinn, Robert E., and John Rohrbaugh. 1981. A Competing Values Approach to Organizational Effectiveness. Public Productivity Review 5 (2):122-140.

Repeated Author. 1983. A Spatial Model of Effectiveness Criteria: Towards a Competing Values Approach to Organizational Analysis. Management Science 29 (3):363-377.

Rainey, Hal G., and Barry Bozeman. 2000. Comparing Public and Private Organizations: Empirical Research and the Power of the A Priori. Journal of Public Administration Research & Theory 10 (2):447.

Rennings, K., A. Ziegler, K. Ankele, and E. Hoffmann. 2006. The influence of different characteristics of the EU environmental management and auditing scheme on technical environmental innovations and economic performance. Ecological Economics 57 (1):45-59.

Rivera, J., and P. de Leon. 2005. Chief executive officers and voluntary environmental performance: Costa Rica's Certification for Sustainable Tourism Policy Sciences 38 (2-3):107-127.

Scott, W. Richard. 2003. Organizations : rational, natural, and open systems. 5th ed. Upper Saddle River, N.J.: Prentice Hall.

Shin, E. , and E.W. Welch. 2012. Environmental Auditing and Compliance. In Handbook of Sustainable Management, edited by C. N. Madu and C. H. K. Kuei: World Scientific Publishing.

Takane, Y., F.W. Young, and J. de Leeuw. 1977. Nonmetric individual differences multidimensional scaling: an alternating least squares method with optimal scaling features. Psychometrika 42:7-67.

25

Thompson, James D. 2003. Organizations in action : social science bases of administrative theory, Classics in organization and management; Variation: Classics in organization and management series. New Brunswick, NJ: Transaction Publishers.

Van Der Wal, Zeger , Gjaltde De Graaf, and Karin Lasthuizen. 2008. What’s valued most? Similarities and differences between the organizational values of the public and private sector. Public Administration 86 (2):465–482.

Welch, Eric W., and Akira Hibiki. 2002. Japanese voluntary environmental agreements: Bargaining power and reciprocity as contributors to effectiveness Policy Sciences 35 (4):401-424.

Welch, Eric W., Ashish Rana, and Yasuhumi Mori. 2003. The Promises and Pitfalls of ISO 14001 for Competitiveness and Sustainability. Greener Management International (44):59-73.