interbank loans, collateral, and monetary policy

TRANSCRIPT

Interbank Loans, Collateral

and Modern Monetary

Policy

SYstemic Risk TOmography:

Signals, Measurements, Transmission Channels, and Policy Interventions

Michiel van de Leur (a)

Marcin Wolski (b)

(a)VU Amsterdam (b)European Investment Bank

Université Paris I Sorbonne

February 2016

Introduction

Interbank markets played a central role in propagating the distressduring the financial crisis.

Secured transactions are settled with collateral. The riskdepends on quality of collateral, and distress originates fromcommon-factor shocks.

The risk of unsecured trades depends on the counterparty, andmalaise spreads through contagion.

In general, the unsecured market is much smaller market in size,and with higher rates.

Both interbank markets are heavily interdependent as in equilibriumthere should be no arbitrage opportunities between them.

Interbank Loans, Collateral and Modern Monetary Policy 2 / 23

Research questions

There does not exist a clear-cut analytical framework which allowspolicy makers to track the developments of the interbank lendingpatterns and evaluate various policy scenarios.

Can we confirm these stylised facts (size and rates ofinterbank markets)?

In what sense does network formation occur?

What is the effect of Modern Monetary Policy?

Interbank Loans, Collateral and Modern Monetary Policy 3 / 23

Model

1 update forecasting strategies,

2 update deposits,

3 realize profits from maturing investment loans and bonds,

4 realize profits from maturing interbank loans and declarebankruptcies,

5 form risk and return expectations,

6 calculate the optimal portfolio allocation,

7 trade in the interbank market,

8 store the variables and go to the next period.

Interbank Loans, Collateral and Modern Monetary Policy 4 / 23

Balance sheet

Assets Liabilities

LI ,t Dept

LIB,t Eqt

Bt DIB,t

Ret Dt

Table: Stylized balance sheet of an individual bank in period t. On theasset side LI ,t are the investment loans, LIB,t are the interbank loans, Bt

are the bond holdings and Ret are the reserves. On the liability side Deptare the deposits, Eqt is the equity capital, DIB,t is the interbank debt andDt are other debt obligations.

Interbank Loans, Collateral and Modern Monetary Policy 5 / 23

Markets

An unlimited amount of bonds are available, which price yields aminimal volatility.

Investments last for 4 periods. For every bank in each period onebusiness project is available. The projects expected return isknown, and yields a higher riskiness if the expected return is high.

Deposits equal a random multiple of equity.

Liquidity backstop, borrowing from a central bank at adiscouragingly high interest rate.

Interbank Loans, Collateral and Modern Monetary Policy 6 / 23

Interbank markets

Interbank loans last for 4 periods.

Banks form expectations about the future interbank rates, whichinclude the number of bankruptcies for the unsecured rate.

In the secured market collateral has te be transferred, equal to thesize of the loan multiplied by the haircut level.

Interbank Loans, Collateral and Modern Monetary Policy 7 / 23

Trading mechanism

For simplicity we assume that traders are submitting their rateforecast as offer. This situation is equal to a situation in which theranking of offers remains (it just slightly increases the number oftrades).

Orders are matched, the highest bid with the lowest ask and so on,until no further trades are possible.

Interbank Loans, Collateral and Modern Monetary Policy 8 / 23

Allocation strategy

Banks allocate to market segments using the optimal portfolioselection strategy from Markowitz (1952).

This maximizes the Constant Relative Risk Aversionnext-period utility, where the risk is represented by thevariance-covariance matrix between all the markets. Moreover riskaversion increases with maturity.

Expectations on bonds and interbank rates are formed, investmentreturn distribution is known and a minimum cash reserve is held.

We additionally restrict the weights corresponding to the targetleverage ratio set by a policy maker.

Interbank Loans, Collateral and Modern Monetary Policy 9 / 23

Expectations

Trend-following rule: ETi ,trt = rt−1 + g(rt−1 − rt−2) + ε2,t ,

ε1,t ∼ N(0, d1).

Adaptive rule: EAi ,trt = ωr̄ + (1− ω)Ei ,t−2rt−1 + ε1,t ,

ε2,t ∼ N(0, d2).

The error for of a rule equals: Er∗i ,t = −(rt−1 − E ∗i ,t−1rt−1)2,

where ∗ ∈ {A,T}.

An agent chooses forecasting rule ∗ ∈ {A,T} with probability

exp (βEr∗i,t)

exp (βErAi,t)+exp (βErTi,t), where β is the intensity of choice parameter.

Interbank Loans, Collateral and Modern Monetary Policy 10 / 23

Interbank network formation

A priori banks do not prioritize counterparties, but are onlyconcerned with the eventual transaction price, i.e. rate.

We still observe non-arbitrary network formation for tworeasons:

1 a difference in size of banks and therefore a difference indemand on the interbank market

2 in subsequent periods banks tend to use the sameexpectational rule

Letting lending banks prioritize counterparties that are less riskyin terms of their leverage, does not largely influence our results.

Interbank Loans, Collateral and Modern Monetary Policy 11 / 23

Model

1 update forecasting strategies,

2 update deposits,

3 realize profits from maturing investment loans and bonds,

4 realize profits from maturing interbank loans and declarebankruptcies,

5 form risk and return expectations,

6 calculate the optimal portfolio allocation,

7 trade in the interbank market,

8 store the variables and go to the next period.

Interbank Loans, Collateral and Modern Monetary Policy 12 / 23

Balance sheet distribution

Smoothened densities of the model and 2549 German banks:

0 1 2 3 4 5 6

0.0

0.5

1.0

1.5

Standardized size

Den

sity

ModelGerman banks in 2007German banks in 2013

−1 0 1 2 3 40.

00.

51.

01.

52.

0Log−leverage

Den

sity

ModelGerman banks in 2007German banks in 2013

0.0 0.2 0.4 0.6 0.8 1.0

02

46

8

Bonds

Den

sity

ModelGerman banks in 2007German banks in 2013

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Production loans

Den

sity

ModelGerman banks in 2007German banks in 2013

0.0 0.2 0.4 0.6 0.8 1.0

02

46

8

Interbank debt

Den

sity

ModelGerman banks in 2007German banks in 2013

0.0 0.2 0.4 0.6 0.8 1.0

02

46

8

Central bank debt

Den

sity

ModelGerman banks in 2007German banks in 2013

Interbank Loans, Collateral and Modern Monetary Policy 13 / 23

Balance sheet distribution

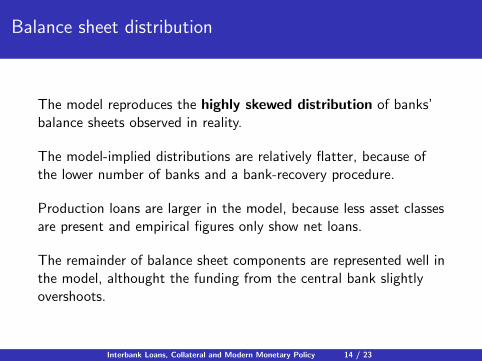

The model reproduces the highly skewed distribution of banks’balance sheets observed in reality.

The model-implied distributions are relatively flatter, because ofthe lower number of banks and a bank-recovery procedure.

Production loans are larger in the model, because less asset classesare present and empirical figures only show net loans.

The remainder of balance sheet components are represented well inthe model, althought the funding from the central bank slightlyovershoots.

Interbank Loans, Collateral and Modern Monetary Policy 14 / 23

Baseline model

100 200 300 400 500

0.00

0.01

0.02

0.03

0.04

Time

Inte

rest

rat

esUnsecuredSecuredRisk free

100 200 300 400 500

010

0030

0050

00

Time

Inte

rban

k lo

ans

UnsecuredSecured

100 200 300 400 500

010

020

030

040

0

Time

Ave

rage

siz

e

TotalBondsInv. loansInterbank loansReserves

100 200 300 400 500

010

020

030

040

0

Time

Ave

rage

siz

eTotalEquityInterbank debtOther debtDeposits

Interbank Loans, Collateral and Modern Monetary Policy 15 / 23

Baseline network structure

100 200 300 400 500

0.05

0.10

0.15

0.20

Time

Ave

rage

hub

cen

tral

ityUnsecuredSecured

100 200 300 400 500

2.2

2.4

2.6

2.8

3.0

3.2

Time

Ave

rage

tota

l deg

ree

UnsecuredSecured

100 200 300 400 500

0.04

0.08

0.12

0.16

Time

Ave

rage

clu

ster

ing

UnsecuredSecured

100 200 300 400 500

2224

2628

3032

Time

Ave

rage

num

ber

of is

land

s UnsecuredSecured

Interbank Loans, Collateral and Modern Monetary Policy 16 / 23

Baseline model

Unsecured rate is significantly higher, leading to a smaller market.

The secured rate yields a higher volatility, making it less risky totrade in that market.

The network statistics suggest:

the unsecured network consists of many star-like communitieswith the hubs being connected between each other

the secured network is more interlinked but has a smallfraction of central hubs (dealer banks)

Interbank Loans, Collateral and Modern Monetary Policy 17 / 23

Scenarios

Exogenous shocksdecrease of collateral qualitynegative production shock

Policy actionsforward guidancedecrease of the bond rate to the negative territorydecrease of the bond rateimproved collateral qualityincrease in the target leverage ratiodecrease in the target leverage ratiocapped availability of collateral securities

Interbank Loans, Collateral and Modern Monetary Policy 18 / 23

Scenarios

Exogenous shocksA decrease in quality of collateral increases the secured rate andthe unsecured market, yielding more bankruptcies. This isconsistent with the so-called “pop-corn” effect.

Lower production loan returns decrease the overall size of thebanking sector and shifts banks’ preferences towards safer assets.

Policy actionsForward guidance reduces bankruptcies and restores marketconfidence, with a lower unsecured rate and debt to central banks.

A bond rate decrease urges banks to invest in higher-yieldinstruments and finance from central banks.

Improved collateral quality shows no significant effect, indicatingthat effects of collateral are asymmetric.

Interbank Loans, Collateral and Modern Monetary Policy 19 / 23

Scenarios

Shifts in the leverage constraint influence the entire dynamics: ahigher allowance increases average profits but also bankruptcies.Moreover, banks pose more demand for unsecured funds so thatthe unsecured rates increase. Decreasing the leverage targetsresults in the opposite dynamics.

A capped availability of collateral, due to asset-purchaseprograms, leads bank to engage less in interbank transactions andkeep higher capital buffers and deposit bases. As a result, thenumber of bankruptcies decreases.

Interbank Loans, Collateral and Modern Monetary Policy 20 / 23

Summary

We have developed an agent-based model of the interbankmarkets which allows to study the effectiveness of ModernMonetary Policy.

We confirm stylized facts of the balancesheet distribution, andthe relationships between the interest rates and volumes of theinterbank markets.

Clustering occurs in both interbank markets, where dealer banksemerge in the secured, and star-like connections in the unsecuredmarket.

Moreover the model has allowed us to determine the effect ofexogenous shocks and different policies, which sketchesinteresting guidelines for central banks and regulators.

Interbank Loans, Collateral and Modern Monetary Policy 21 / 23

Future research

Timing and strategic behavior in the interbank market.

Varying maturities of loans and investments.

A quantity constraint of the liquidity backstop.

Improve distribution of leverage.

Endogenize investment projects.

Interbank Loans, Collateral and Modern Monetary Policy 22 / 23

This project has received funding from the European Union’s

Seventh Framework Programme for research, technological

development and demonstration under grant agreement no° 320270

www.syrtoproject.eu

This document reflects only the author’s views.

The European Union is not liable for any use that may be made of the information contained therein.