interest rates chapter 4. valuing debt in 1945, u.s. treasury bills offered a return of 0.4%. at...

TRANSCRIPT

Interest RatesInterest Rates

Chapter 4Chapter 4

Valuing DebtValuing Debt

In 1945, U.S. Treasury bills offered a In 1945, U.S. Treasury bills offered a return of 0.4%. At their 1981 peak, they return of 0.4%. At their 1981 peak, they offered a return of over 17%. offered a return of over 17%.

Why does the same security offer radically Why does the same security offer radically different yields at different times?different yields at different times?

Valuing DebtValuing Debt

In January 2000, the U.S. Treasury could In January 2000, the U.S. Treasury could borrow for 1 year at an interest rate of borrow for 1 year at an interest rate of 6.2%, but it had to pay a rate of about 7% 6.2%, but it had to pay a rate of about 7% for 20-year loans. for 20-year loans.

Why do bonds maturing at different dates Why do bonds maturing at different dates offer different rates of interest?offer different rates of interest?

Valuing DebtValuing Debt

In January 2000, the U.S. government In January 2000, the U.S. government could issue long-term bonds at a rate of could issue long-term bonds at a rate of about 7%. about 7%.

You could not have borrowed at that rate. You could not have borrowed at that rate. Why not?Why not?

INTEREST RATES SERVE AS AINTEREST RATES SERVE AS A

YARDSTICK FOR COMPARINGYARDSTICK FOR COMPARING

DIFFERENT TYPES OFDIFFERENT TYPES OF

SECURITIES AND MATURITIES.SECURITIES AND MATURITIES.

5 Major Sources of Rate 5 Major Sources of Rate Differences in BondsDifferences in Bonds

1.1. Term to maturityTerm to maturity2.2. Default riskDefault risk

– To default on a bond is to fail to pay the interest To default on a bond is to fail to pay the interest when interest is due or to fail to pay the principal when interest is due or to fail to pay the principal at maturityat maturity

– Bond ratingsBond ratings

3.3. Tax treatmentTax treatment– The value of the tax factors to the investor The value of the tax factors to the investor

depends on the investor’s marginal income tax depends on the investor’s marginal income tax rate rate

– After tax yield=Before tax yield (1-T)After tax yield=Before tax yield (1-T)

4.4. MarketabilityMarketability– time required to effect the saletime required to effect the sale– spread between the current market price and spread between the current market price and

realized price at the time of the sale.realized price at the time of the sale.

5.5. Special featuresSpecial features– call option.call option.– put option.put option.– convertible option.convertible option.

Characteristics of BondsCharacteristics of Bonds

Details contained in the indenture.Details contained in the indenture.

Administered through a trustee.Administered through a trustee.

Secured versus unsecured.Secured versus unsecured.– Mortgage/debentureMortgage/debenture

Senior or junior or subordinated.Senior or junior or subordinated.

Call features.Call features.

Bond rating.Bond rating.

Types of BondsTypes of Bonds

Coupon/Zero-coupon bondsCoupon/Zero-coupon bonds

Municipal bondsMunicipal bonds– Revenue/General ObligationRevenue/General Obligation

Junk bondsJunk bonds

ConsolsConsols

Eurobonds/Foreign bondsEurobonds/Foreign bonds

Sources of Bond InformationSources of Bond Information

http://www.moodys.comhttp://www.moodys.com

http://www.bondsonline.com/http://www.bondsonline.com/

http://www.wsj.comhttp://www.wsj.com

http://bonds.yahoo.comhttp://bonds.yahoo.com

Bond FeaturesBond Features

When a corporation (or government) wants to When a corporation (or government) wants to borrow money, it often sells a borrow money, it often sells a bondbond. .

An investor gives the corporation money for the An investor gives the corporation money for the bond. bond.

The corporation promises to give the investor:The corporation promises to give the investor:– Regular Regular couponcoupon payments every period until the payments every period until the

bond matures.bond matures.– The The face valueface value of the bond when it matures. of the bond when it matures.

The Bond Pricing FormulaThe Bond Pricing Formula

CC11 C C22 C C33 CCnn + F + Fnn

P =P = ++ + + + … + + … + (1 + r)(1 + r)11 (1 + r) (1 + r)22 (1 + r) (1 + r)33 (1 + r)(1 + r)TT

The price of the bond today is the present The price of the bond today is the present value of all future cash flows (coupon value of all future cash flows (coupon payments and principal).payments and principal).

The Bond-Pricing EquationThe Bond-Pricing Equation

t

t

r)(1

F

rr)(1

1-1

C Value Bond

Bond FeaturesBond Features

Consider a bond with three years to maturity, a coupon Consider a bond with three years to maturity, a coupon rate of 8%, and a $1000 face value. If the current rate of 8%, and a $1000 face value. If the current market rate is 10%, what is the price of the bond.market rate is 10%, what is the price of the bond.

$80 $80 $1080 $80 $80 $1080

P =P = ++ + + (1.10)(1.10)11 (1.10) (1.10)22 (1.10) (1.10)33

P=$80(0.9091)+$80(0.8264)+$1080(0.7513) P=$80(0.9091)+$80(0.8264)+$1080(0.7513)

P=$950.24 P=$950.24

Bond Rates and YieldsBond Rates and Yields

The The coupon ratecoupon rate is the annual dollar coupon expressed is the annual dollar coupon expressed as a percentage of the face value.as a percentage of the face value.

Coupon rateCoupon rate = $80/$1000 = 8.0% = $80/$1000 = 8.0%

The The current yieldcurrent yield is the annual coupon divided by the is the annual coupon divided by the price:price:

Current yieldCurrent yield = $80/$950.24 = 8.42% = $80/$950.24 = 8.42%

The The yield to maturityyield to maturity is the rate that makes the price is the rate that makes the price of the bond just equal to the present value of its future of the bond just equal to the present value of its future cash flows. cash flows.

YTMYTM = 10% = 10%

ExampleExample

Bond A has 4 years remaining to Bond A has 4 years remaining to maturity. Interest is paid annually; maturity. Interest is paid annually; the bond has a $1,000 par value; the bond has a $1,000 par value; and the coupon interest rate is 9%.and the coupon interest rate is 9%.– What is the current yield and yield to What is the current yield and yield to

maturity at a current market price of $829?maturity at a current market price of $829?– What is the current yield and yield to What is the current yield and yield to

maturity at a current market price of maturity at a current market price of $1,104?$1,104?

Par, Premium and Discount Par, Premium and Discount BondsBonds

If a bond’s coupon rate is equal to the If a bond’s coupon rate is equal to the market rate of interest (the bond’s yield), market rate of interest (the bond’s yield), the bond will always sell at the bond will always sell at parpar..

Bonds selling at below par are called Bonds selling at below par are called discount bonds.discount bonds.

Bonds selling above par are called Bonds selling above par are called premium bonds.premium bonds.

Pure Discount BondPure Discount Bond

Zero-coupon bondsZero-coupon bonds pay no coupon pay no coupon payment but promise a single payment at payment but promise a single payment at maturity.maturity.

Value of a pure discount bond:Value of a pure discount bond:

P = F / (1 + r)P = F / (1 + r)TT

Perpetual BondsPerpetual Bonds

A consol pays coupons forever. It never A consol pays coupons forever. It never matures.matures.

P=C/rP=C/r

Bond Pricing Theorem IBond Pricing Theorem I

Bond prices and market interest rates move in Bond prices and market interest rates move in opposite directions.opposite directions.

600

700

800

900

1000

1100

1200

1300

1400

1500

0% 2% 4% 6% 8% 10% 12% 14%

Bond Pricing Theorem IIBond Pricing Theorem II

When coupon rate = YTM, price = par When coupon rate = YTM, price = par value.value.

When coupon rate > YTM, price > par When coupon rate > YTM, price > par value (premium bond)value (premium bond)

When coupon rate < YTM, price < par When coupon rate < YTM, price < par value (discount bond)value (discount bond)

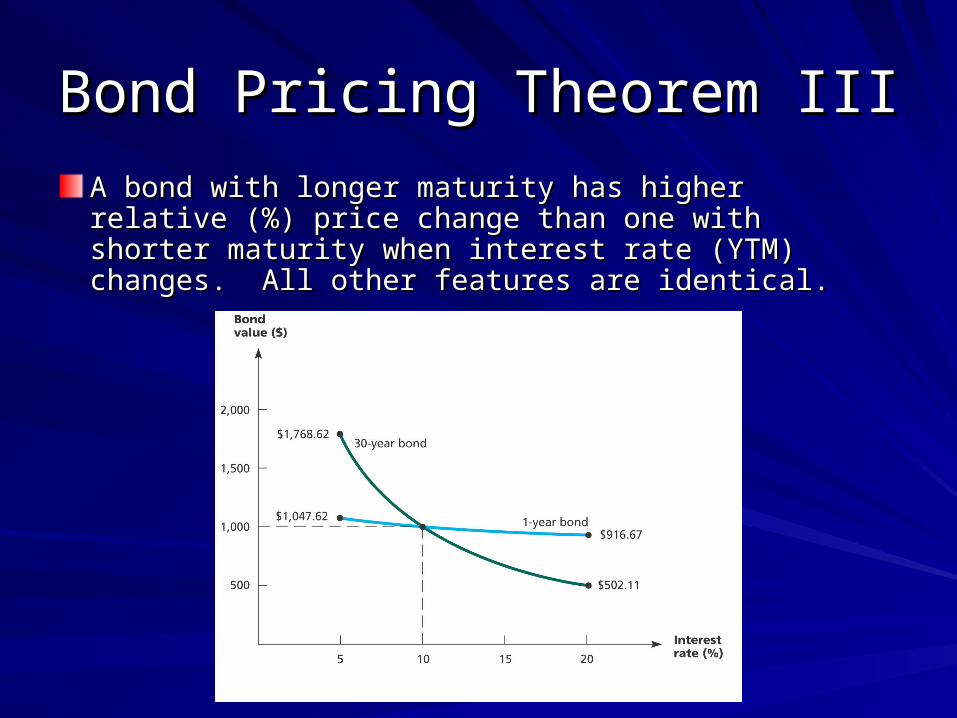

Bond Pricing Theorem IIIBond Pricing Theorem III

A bond with longer maturity has higher relative (%) A bond with longer maturity has higher relative (%) price change than one with shorter maturity when price change than one with shorter maturity when interest rate (YTM) changes. All other features are interest rate (YTM) changes. All other features are identical.identical.

Bond Pricing Theorem IVBond Pricing Theorem IV

A lower coupon bond has a higher relative A lower coupon bond has a higher relative (%) price change than a higher coupon (%) price change than a higher coupon bond when interest rate (YTM) changes. bond when interest rate (YTM) changes. All other features are identical.All other features are identical.

Coupon Rate and Bond Price VolatilityCoupon Rate and Bond Price Volatility

Consider two otherwise identical bonds.

The low-coupon bond will have much more volatility with respect to changes in the

discount rate

Discount Rate

Bon

d V

alu

e

High Coupon Bond

Low Coupon Bond

Interest Rate RiskInterest Rate Risk

Price Risk.Price Risk.

Reinvestment Risk.Reinvestment Risk.

Price Risk versus Reinvestment Risk.Price Risk versus Reinvestment Risk.

Duration.Duration.

Interest Rate Risk ExampleInterest Rate Risk Example

Suppose you buy three securities:Suppose you buy three securities:– A one-year bill with a face value of $10,000.A one-year bill with a face value of $10,000.– A 5-year strip with a face value of $10,000.A 5-year strip with a face value of $10,000.– A 30-year strip with a face value of $10,000.A 30-year strip with a face value of $10,000.

The market interest rate is 6%, so their prices The market interest rate is 6%, so their prices are:are:– T-bill: P=$10,000/1.06=$9,434T-bill: P=$10,000/1.06=$9,434– 5-year strip: P=$10,000/(1.06)5-year strip: P=$10,000/(1.06)55=$7,473=$7,473– 30-year strip: P=$10,000/(1.l06)30-year strip: P=$10,000/(1.l06)3030=$1,741=$1,741

Example, continuedExample, continued

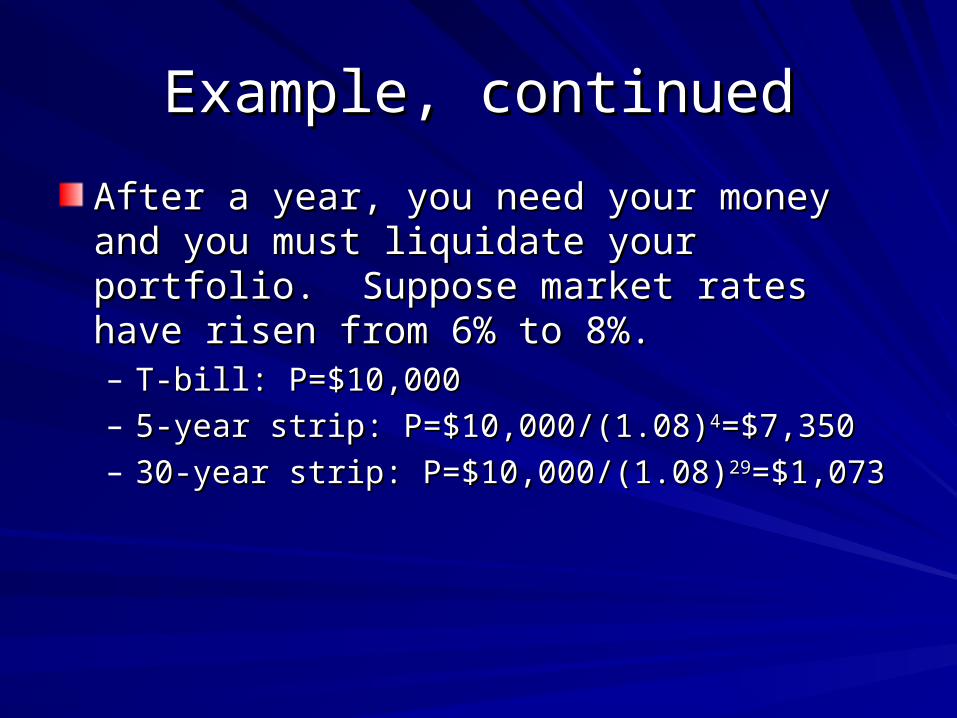

After a year, you need your money and you must After a year, you need your money and you must liquidate your portfolio. Suppose market rates liquidate your portfolio. Suppose market rates have risen from 6% to 8%.have risen from 6% to 8%.– T-bill: P=$10,000T-bill: P=$10,000– 5-year strip: P=$10,000/(1.08)5-year strip: P=$10,000/(1.08)44=$7,350=$7,350– 30-year strip: P=$10,000/(1.08)30-year strip: P=$10,000/(1.08)2929=$1,073=$1,073

Initial Holding-Period Yield after Holding for 1-Year Investment If interest rates are:

r=6% r=6% r=8% r=4%Value Value Yield Value Yield Value Yield

1-year strip $9,434 $10,000 6.0% $10,000 6.0% $10,000 6.0%5-year strip 7,473 7,921 6.0% 7,350 -1.6% 8,548 14.4%30-year strip 1,741 1,846 6.0% 1,073 -38.4% 3,207 84.2%

Reinvestment-Rate RiskReinvestment-Rate Risk

Suppose that you do not need your Suppose that you do not need your money after one year but want to leave money after one year but want to leave it invested until you retire in 30 years.it invested until you retire in 30 years.– On the 30-year strip, the holding-period yield On the 30-year strip, the holding-period yield

equals the market yield at the time you bought the equals the market yield at the time you bought the bond.bond.

– How much you make on the other two investments How much you make on the other two investments will depend on how you reinvest the money when will depend on how you reinvest the money when the bond matures.the bond matures.

Reinvestment-Rate RiskReinvestment-Rate Risk

Reinvestment-rate riskReinvestment-rate risk– the risk associated with reinvestment at the risk associated with reinvestment at

uncertain interest rates.uncertain interest rates.

Considerations:Considerations:– What is your time horizon?What is your time horizon?– Do you want to play it safe?Do you want to play it safe?– Do you think interest rates will rise or fall?Do you think interest rates will rise or fall?

LessonsLessons

If you hold a bill or strip to maturity, the holding-period If you hold a bill or strip to maturity, the holding-period yield will equal the market yield at the time that you yield will equal the market yield at the time that you bought it.bought it.

If you sell a bill or strip before maturity, the holding-If you sell a bill or strip before maturity, the holding-period yield depends on the market yield at the time of period yield depends on the market yield at the time of the sale.the sale.

The higher the market yield at the time of the sale, the The higher the market yield at the time of the sale, the lower the market price.lower the market price.

The greater the bill’s or the strip’s remaining time to The greater the bill’s or the strip’s remaining time to maturity, the greater the sensitivity of its market price to maturity, the greater the sensitivity of its market price to market yield.market yield.

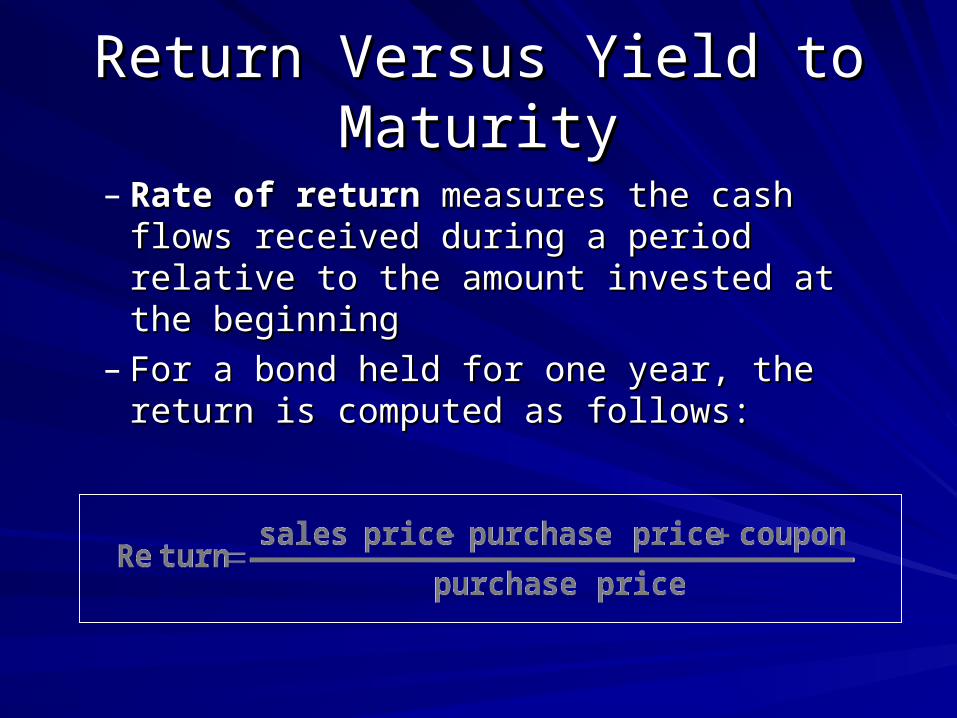

Return Versus Yield to MaturityReturn Versus Yield to Maturity

– Rate of returnRate of return measures the cash flows measures the cash flows received during a period relative to the received during a period relative to the amount invested at the beginningamount invested at the beginning

– For a bond held for one year, the return is For a bond held for one year, the return is computed as follows:computed as follows:

Nominal versus Real RatesNominal versus Real Rates

The The real rate of interestreal rate of interest is the fundamental is the fundamental long-run interest rate in the economy. It is called long-run interest rate in the economy. It is called the “real” rate of interest because it is the “real” rate of interest because it is determined by the real output of the economy.determined by the real output of the economy.– It is estimated to be on average about 3 percent. It It is estimated to be on average about 3 percent. It

varies between 2 and 4 percent.varies between 2 and 4 percent.

The nominal rate of interest is the observed rate The nominal rate of interest is the observed rate of interest.of interest.

Nominal rate Nominal rate ~ ~ Real rate + InflationReal rate + Inflation

Real interest rate = Nominal rate – Inflation rate

Calculating Interest RatesCalculating Interest Rates

Nominal Versus Real Interest RatesNominal Versus Real Interest Rates– Nominal Interest RatesNominal Interest Rates—Money amount of —Money amount of

interest receivedinterest received– Real Interest RatesReal Interest Rates——Purchasing powerPurchasing power of of

interest receivedinterest received– Real interest rate is the nominal interest adjusted Real interest rate is the nominal interest adjusted

for inflationfor inflation

Where:• “ex-ante” is based on the expected rate of inflation• “ex-post” is based on the actual or realized rate of inflation

Supply and Demand Determine Supply and Demand Determine the Interest Ratethe Interest Rate

Interest rate is Interest rate is priceprice of credit or borrowing of credit or borrowing moneymoneyMarket for Market for CreditCredit or or Loanable FundsLoanable Funds – Supply of FundsSupply of Funds——Upward slopingUpward sloping, lenders are , lenders are

willing to extend willing to extend more creditmore credit at higher interest at higher interest ratesrates

– Demand for FundsDemand for Funds——Downward slopingDownward sloping, , borrowers are willing to borrowers are willing to borrow lessborrow less at higher at higher interest ratesinterest rates

– EquilibriumEquilibrium—Intersection of supply and demand, —Intersection of supply and demand, no tendency to changeno tendency to change

Why Does the Interest Rate Why Does the Interest Rate FluctuateFluctuate

U.S. Treasury bond yields change day to day U.S. Treasury bond yields change day to day Movement along a single curveMovement along a single curve—Changes in —Changes in the interest rate results in a movement along a the interest rate results in a movement along a single demand or supply curve single demand or supply curve Shifts of a CurveShifts of a Curve—Change in determinants of —Change in determinants of supply or demand (other than interest rate) supply or demand (other than interest rate) causes the respective curve to shift causes the respective curve to shift Changes in EquilibriumChanges in Equilibrium—Shift of either the —Shift of either the supply or demand curve will reflect a change in supply or demand curve will reflect a change in the equilibrium interest ratethe equilibrium interest rate

Borrowing (Demand)Borrowing (Demand)

Business firmsBusiness firms– finance inventory or buy capital equipmentfinance inventory or buy capital equipment

HouseholdsHouseholds– buy cars, consumer goods, or homesbuy cars, consumer goods, or homes

State and local governmentState and local government– provide infrastructure or public servicesprovide infrastructure or public services

Federal governmentFederal government– finance Federal Budget Deficitfinance Federal Budget Deficit

INCREASES IN BORROWINGINCREASES IN BORROWING– SHIFT DEMAND TO RIGHT AND RAISE INTEREST SHIFT DEMAND TO RIGHT AND RAISE INTEREST

RATESRATES

Lending or Credit (Supply)Lending or Credit (Supply)

Financial institutions or individuals lend to Financial institutions or individuals lend to marketmarketGovernment authorities may restrict lending by Government authorities may restrict lending by banksbanksAbility of individuals to lend depends on their Ability of individuals to lend depends on their savings—less savings results in lower amount of savings—less savings results in lower amount of lendinglendingDECREASES IN LENDINGDECREASES IN LENDING– SHIFT SUPPLY TO LEFT AND RAISE INTEREST SHIFT SUPPLY TO LEFT AND RAISE INTEREST

RATERATE

The Importance of ExpectationsThe Importance of Expectations

Effect of a change in Effect of a change in expectations of expectations of increasing inflationincreasing inflation– DemandDemand—Borrowers increase demand since they will —Borrowers increase demand since they will

be repaying in depreciated dollars and desire to be repaying in depreciated dollars and desire to purchase before the prices increasepurchase before the prices increase

– SupplySupply—Lenders decrease supply since they will be —Lenders decrease supply since they will be repaid with money of diminished purchasing powerrepaid with money of diminished purchasing power

SHIFTS OF THE DEMAND AND SUPPLY SHIFTS OF THE DEMAND AND SUPPLY CURVE WILL CAUSE THE INTEREST RATE CURVE WILL CAUSE THE INTEREST RATE TO INCREASETO INCREASE

The Importance of ExpectationsThe Importance of Expectations

Self-fulfilling ProphesiesSelf-fulfilling Prophesies– If individuals and institutions expect inflation If individuals and institutions expect inflation

and interest rates to increase, they will alter and interest rates to increase, they will alter behavior that causes the higher rates that behavior that causes the higher rates that were anticipatedwere anticipated

Cyclical and Long-term Trends Cyclical and Long-term Trends in Interest Ratesin Interest Rates

Level of interest rates tends to rise during Level of interest rates tends to rise during cyclical expansion and fall during cyclical expansion and fall during recessions. recessions.

During economic expansion:During economic expansion:– Firms and households increase borrowing—Firms and households increase borrowing—

demand curve rightdemand curve right– FED usually tightens credit during expansionFED usually tightens credit during expansion

—supply curve left—supply curve left

Cyclical and Long-term Trends Cyclical and Long-term Trends in Interest Ratesin Interest Rates

Level of interest rates on upward long-term trend Level of interest rates on upward long-term trend between 1950 and 1981between 1950 and 1981– Large federal budget deficit forced US Treasury to Large federal budget deficit forced US Treasury to

increase borrowing—pushing up interest ratesincrease borrowing—pushing up interest rates– Expectations of increasing inflationExpectations of increasing inflation

Since 1981 rates have trended downwardSince 1981 rates have trended downward– Federal deficits continued to increase in 1980’sFederal deficits continued to increase in 1980’s– Expectations of Expectations of lowerlower inflation has been major reason inflation has been major reason

for fall of interest rates.for fall of interest rates.