interim investor december 2016 - distell

TRANSCRIPT

1

Interim investor – December 2016

Richard Rushton – Managing Director

Lucas Verwey – Financial Director

Investor Presentation Interim results as of December 2016

2

Interim investor – December 2016

Overall sales volumes lower mainly due to: o High H1 2015/16 base as a result of RSA price

increase timing o Ciders impacted by trade down as

disposable incomes come under pressure in SA

o Intensified beer pricing and pack activities in formal channels as well as recent RTD launches

o Challenging conditions in Africa

On a normalised FX basis, EBITDA increased by

17.2% and HLE by 22.8%

EBITDA & HLE impacted by strengthening of the Rand compared to prior year

The improved performance is driven by efficiencies, optimised A&P spend and cost reductions

NormalisedNormalised

FX#

Sales volumes -3.1% -3.1%

Revenue 2.4% 3.0%

EBITDA* -0.3% 17.2%

Headline earnings 1.1% 22.8%

Headline earnings per share 1.0% 22.6%

Growth in total assets 2.8% 3.9%

Salient features of our performance to

December 2016

# Throughout this presentation, “normalised FX” refers to normalised performance excluding exchange rate movements

Salient features and key performance metrics H1 Strong efficiencies and cost containment improved like-for-like profitability

3

Interim investor – December 2016

Continued growth in wine – 4th Street achieved high double digit

growth, with further growth coming from Perle wine brands

Brandy volume growth , led by double digit growth in Viceroy

Gin recorded another year of strong double digit growth

Weaker performance in Whisky

Cider volumes impacted by pricing, high base and increased competition

Mainstream momentum continues – RTD’s and Wines

Significant progress made across priority initiatives:

o COGS efficiencies – returnable bottles, crate project, cost savings

o Champion wine in mainstream – 4th Street leading mainstream market penetration

o Extract benefits of SFE – Incorporation of “Accelerated Competency Development

Program” to build sales capability

o Luxury brand portfolio – new influencer and hospitality teams established

o Marketing effectiveness – portfolio optimisation, marketing effectiveness including

planning and tracking through CRM

South Africa performance highlights Growth in wine and spirits in South Africa despite tough market conditions

Volume growth in wine and spirits

Revenue growth despite volume decline

Gross profit margin relatively flat

Operational efficiencies and cost containment contributed to EBIT growth

Volume Revenue Revenue % Distell

South Africa -1.1% 5.1% 76.2%

4

Interim investor – December 2016 Africa (incl BLNS) performance highlights Challenging macro-economic conditions across the continent

Africa – +/- 70% of volume decline due to Angola excl BLNS

Other markets show mixed results due to slower economic growth

BLNS – impacted by subdued growth in Namibia

Prudent cost management delivers 3.9% EBIT growth

Volume Revenue Revenue % Distell

Africa (Incl BLNS) -12.8% -8.0% 12.7%

Revenue % Africa

BLNS -3.9% 2.2% 65.7%

Mozambique -12.4% -15.8% 6.9%

Zambia -14.1% -13.4% 6.4%

Angola -61.7% -66.4% 3.6%

Kenya -9.4% -3.1% 3.5%

Nigeria 12.5% -11.3% 3.5%

Ghana -19.9% 4.0% 2.9%

Other -6.0% -3.7% 7.5%

5

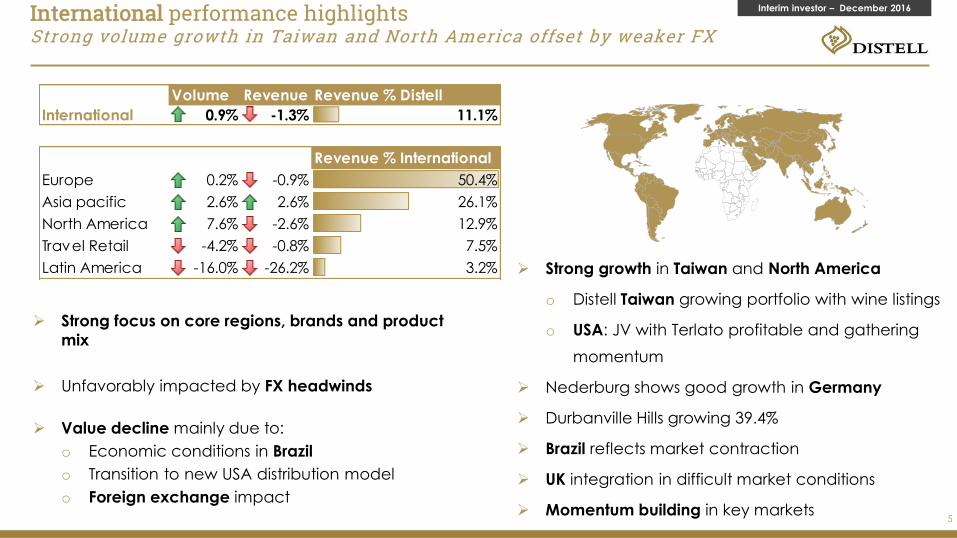

Interim investor – December 2016 International performance highlights Strong volume growth in Taiwan and North America offset by weaker FX

Strong focus on core regions, brands and product

mix

Unfavorably impacted by FX headwinds

Value decline mainly due to:

o Economic conditions in Brazil

o Transition to new USA distribution model

o Foreign exchange impact

Strong growth in Taiwan and North America

o Distell Taiwan growing portfolio with wine listings

o USA: JV with Terlato profitable and gathering

momentum

Nederburg shows good growth in Germany

Durbanville Hills growing 39.4%

Brazil reflects market contraction

UK integration in difficult market conditions

Momentum building in key markets

Volume Revenue Revenue % Distell

International 0.9% -1.3% 11.1%

Revenue % International

Europe 0.2% -0.9% 50.4%

Asia pacific 2.6% 2.6% 26.1%

North America 7.6% -2.6% 12.9%

Travel Retail -4.2% -0.8% 7.5%

Latin America -16.0% -26.2% 3.2%

6

Interim investor – December 2016 Power and luxury brands Our unique brand crafting capabilities position Distell to grow our consumer base

• Hunter’s: 660ml delivering value at the right price point

•4th Street: Recruiting new consumers to the wine category and our brands

•Amarula: Successfully building premium cues for our core assets

•Savanna Loco: Transcending traditional category boundaries

CATEGORY EXPANSION

BRAND RENOVATION

OFFERING VALUE

CONSUMER BASE

EXPANSION

H1 2017 H1 2016

Value growth Value growth

Power Brands 3.9% 11.3% 89.7%

Luxury brands -0.5% 13.1% 10.3%

Contribution to

Distell

INSIGHTS:

Heavy discounting and acceleration in

consumer trading down trends in RSA

Increased competition in blended whisky in

all key markets

Premium offerings under pressure; strategy

review being finalised

Core brand renovation completed for all

focus brands

Rate of innovation increased in RTD

segment

7

Interim investor – December 2016

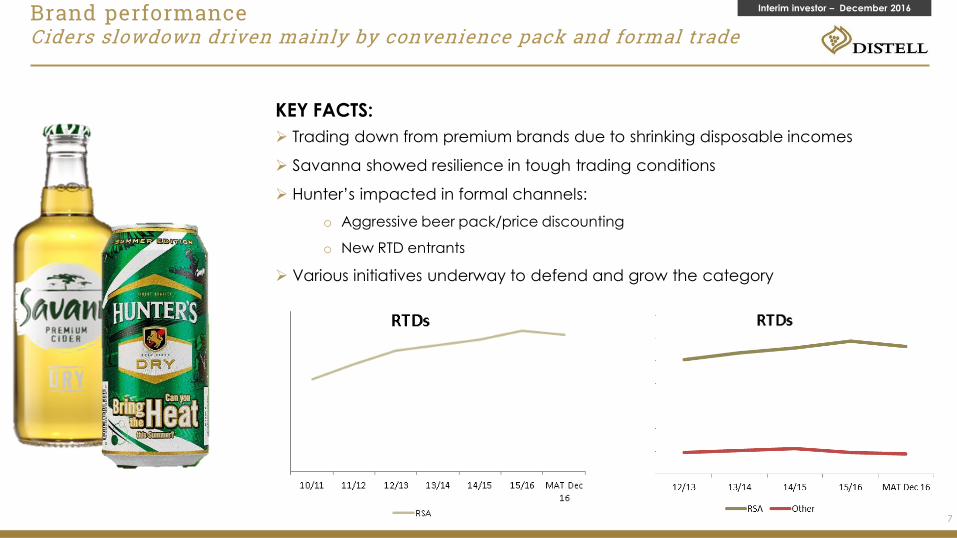

KEY FACTS:

Trading down from premium brands due to shrinking disposable incomes

Savanna showed resilience in tough trading conditions

Hunter’s impacted in formal channels:

o Aggressive beer pack/price discounting

o New RTD entrants

Various initiatives underway to defend and grow the category

Brand performance Ciders slowdown driven mainly by convenience pack and formal trade

8

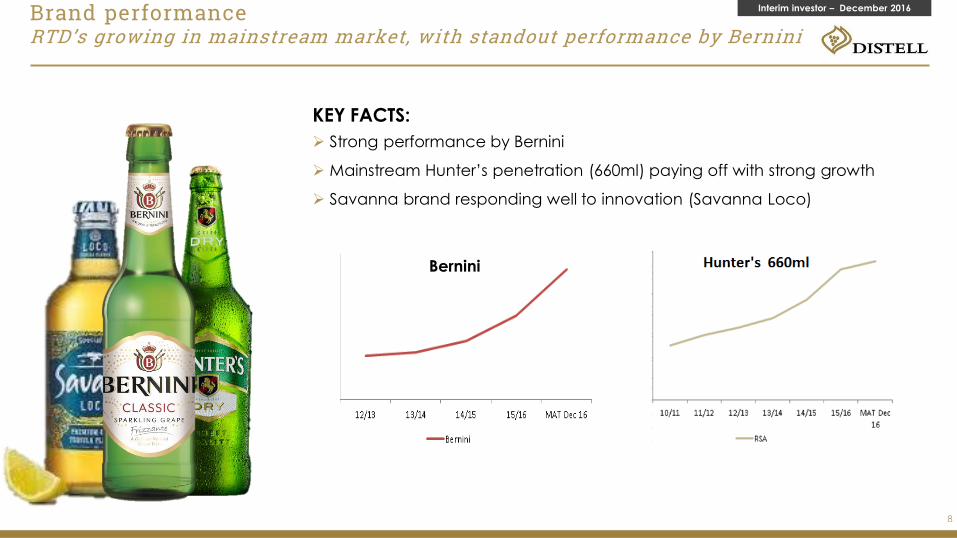

Interim investor – December 2016 Brand performance RTD’s growing in mainstream market, with standout performance by Bernini

KEY FACTS:

Strong performance by Bernini

Mainstream Hunter’s penetration (660ml) paying off with strong growth

Savanna brand responding well to innovation (Savanna Loco)

Bernini

9

Interim investor – December 2016 Brand performance 4th Street continues strong double digit growth

KEY FACTS:

SA Market leadership momentum continues

Worlds fastest growing wine brand (IWSR)

KEY INITIATIVES:

Pack upgrade & new mix to launch Q1

Up weighted on-con presence to drive perfect serve

Outdoor increased in mainstream hubs

10

Interim investor – December 2016 Brand performance JC le Roux comes back with strong SA growth

KEY FACTS:

Volume growth in RSA

SA sparkling leadership position strengthened

Angolan economy put pressure on performance

KEY INITIATIVES:

Launch of Vibrazio a new drier range in progress, with key focus on listings and trial

11

Interim investor – December 2016 Brand performance Two Oceans delivers growth across all focus markets

KEY FACTS:

SA volume share up +0.8%; SA 3l BIB driving growth

No 1 standard price wine in Ontario

Canada’s strong momentum continues

KEY INITIATIVES:

Global IWSR Silver award applied to all Sauvignon Blanc

Pinot Noir Canada launch & Fruity upgrade Europe Q3

12

Interim investor – December 2016 Brand performance Durbanville Hills – continued growth across territories

KEY FACTS:

Continued growth across multiple countries

Launched Terlato range in the USA

Successful launch of Sparkling Sauvignon Blanc (Nov ’16)

KEY INITIATIVES:

Drive on-con listings for Sparkling Sauvignon Blanc

Ensure successful introduction of Durbanville Hills in Brazil

Continued support to Terlato Wines to drive volumes in USA

Launched Atlantic View (Off-trade offering) in the UK

13

Interim investor – December 2016 Brand performance Nederburg– Ultra premium tier performance delivering good results

KEY FACTS:

Heritage Heroes & 5600 tiers continued growth

Entrenching quality credentials due to multiple awards

Germany delivering good volume growth (26.0%) on back of pack upgrade

KEY INITIATIVES:

Leverage IWSC Producer of the year

Continued collaboration with Team Dimension Data for Qhubeka

Entrenching new positioning “Curiously the best of both worlds”

14

Interim investor – December 2016 Award-winning brands Nederburg – multiple award winning wine

IWC 2016

o International Trophy – Nederburg Eminence 2012

IWSC 2016

o South African producer of the year

o Gold Outstanding – Nederburg private Bin Cabernet Sauvignon 2013

o Trophy – Best Cabernet Sauvignon in the world – Nederburg Private Bin Cabernet

Sauvignon 2014

Platters Wine Guide 2016

o Producer of the year

o 5 Stars – Nederburg Winemasters Noble Late Harvest 2015

o 5 Stars – Nederburg Cabernet Sauvignon Private Bin R163 2013

o 5 Stars - Nederburg Heritage Heroes Brewmaster Bordeaux 2014

Michelangelo International Wine & Spirits Awards 2016

o Grand D’Or – Nederburg Heritage Heroes Brewmaster Bordeaux 2013

Veritas 2016

o Gold - Nederburg Ingenuity White Blend 2014

15

Interim investor – December 2016 Brand performance Viceroy double digit growth continues

KEY FACTS:

Affordability and residual equity paying dividends

KEY INITIATIVES:

Makoya 3 year statement to launch Q3

Packaging upgrade 5year Q2-3 in SA, Kenya & Zimbabwe

Viceroy 10 launched in Kenya

16

Interim investor – December 2016 Brand performance Early indicators of success for Amarula global premiumisation journey

KEY FACTS:

Won 2017 IWRC Medal New York

Markets where pack up grade implemented showing uplift in sales

Strong global consumer response from Amarula Trust “Name them save them” campaign

KEY INITIATIVES:

Aggressive drive behind global campaign

Amarula Trust Limited edition bespoke label together with consumer campaign

17

Interim investor – December 2016 Brand performance Scottish Leader – positive consumer uptake in Taiwan continues

KEY FACTS:

Europe remains a tough market for blended Scotch

Brand campaign “New Perspective, Richer Possibilities” building brand equity

Range extension (Original) in Taiwan opened new channels

12 YO launched in SA

KEY INITIATIVES:

Further innovation

New digital campaign to follow “New Perspectives”

18

Interim investor – December 2016

USA Africa JV structure now fully

operational

Distribution network being

integrated

Focus on rate of sale &

quality of distribution

New leadership team

Improvement drive continues

Build partner trust and add value

Drive share and scale RTM in core

categories

Own the last mile Select African & International partnerships are positioning Distell for the future

JV company established

Savanna in-market from

December 2016; Bernini

from April 2017

JV staffing and integration

process advanced

Breaking ground on local

production February 2017

China

19

Interim investor – December 2016 Sustainability initiatives Some of the highlights of our recent Enterprise and Supplier Development activities

Majority black, women-owned enterprise established by Distell

70% of our Amarula Tassels volume

28 full time jobs created

Safe and secure work environment

Top 5 biggest SA factory solar installation projects

Majority black owned enterprise established by Distell

4440 panels and start to end in 83 days

Delivering up to 35% of the site’s power

Innovative apple and vine co-planting with government

New low-chill apple varietals trialled

Empowered farm and plant models for beneficiaries

BBBEE: Achieved level 4 status within one year (up from level 8)

Created businesses in our value chain to support local economies: Local sourcing across categories & geographies

Lead in diversity and transformation: Integrated BBBEE strategy driving sustainability and job creation

Nurture our environment: Focussed initiatives to ensure we operate in a sustainable and ethical manner

20

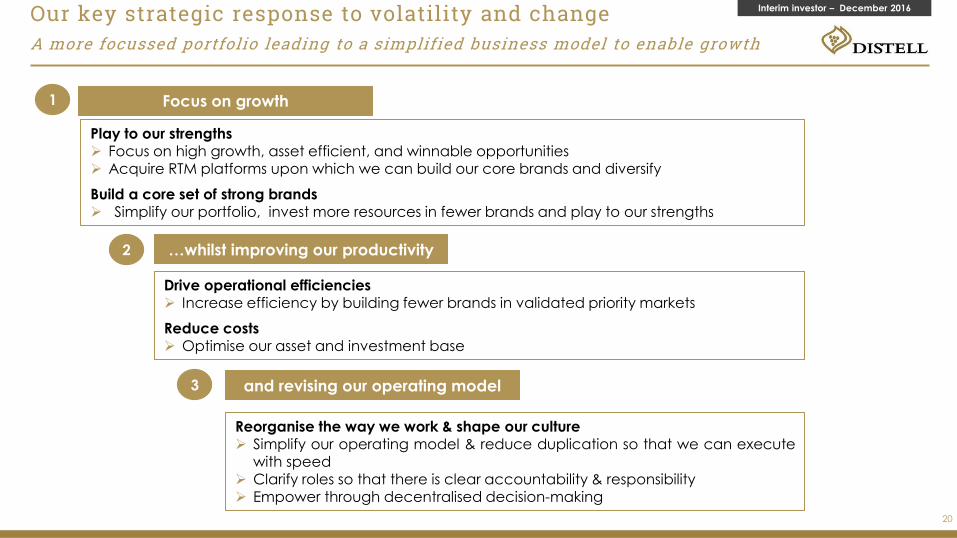

Interim investor – December 2016 Our key strategic response to volatility and change A more focussed portfolio leading to a simplified business model to enable growth

Reorganise the way we work & shape our culture Simplify our operating model & reduce duplication so that we can execute

with speed

Clarify roles so that there is clear accountability & responsibility Empower through decentralised decision-making

Play to our strengths Focus on high growth, asset efficient, and winnable opportunities Acquire RTM platforms upon which we can build our core brands and diversify

Build a core set of strong brands Simplify our portfolio, invest more resources in fewer brands and play to our strengths

Drive operational efficiencies Increase efficiency by building fewer brands in validated priority markets

Reduce costs Optimise our asset and investment base

Focus on growth

…whilst improving our productivity

and revising our operating model

1

2

3

21

Interim investor – December 2016

Key strategic initiatives to drive change and enhance performance

Lead selected emerging markets

Craft distinctive & compelling Brands

Own the last mile

Shape the future

Scale up excellence

Care & contribute

Make clearer deliberate choices on which brands and markets where we

have the right to win

Defend and grow SA

Accelerate our geographic diversification

Optimise our supply chain

Invest in

management systems

Invest in the front-end

Own the

relationship with the

customer and the

consumer

Change our operating

model

Deepen our talent

pipeline

Shape our culture

Build our

corporate reputation

Influence regulatory

policy

Transform and diversity our

business

Implement world class

sustainability

practices

22

Interim investor – December 2016

Financials

23

Interim investor – December 2016

Reported

'mReported Normalised

Normalised

FX#

Sales volumes 385.1 -3.1% -3.1% -3.1%

Revenue 12,516.4 2.4% 2.4% 3.0%

EBITDA* 1,864.9 -3.4% -0.3% 17.2%

Headline earnings 1,176.9 1.1% 1.1% 22.8%

Headline earnings per share 536.8c 1.0% 1.0% 22.6%

Growth in total assets 2.9% 2.8% 3.9%

Salient features Cost control assists to maintain growth in tough conditions

*Main difference between normalised and reported EBITDA (these impairments do not

form part of HLE):

o R38.8m impairment of Brand Phoenix investment o R20.0m impairment of Angola industrial property rights

# Throughout this presentation, “normalised FX” refers to normalised performance excluding exchange rate

movements

24

Interim investor – December 2016

South Africa

• Volumes down 1.1%

• Revenue up 5.1%

• High prior year base due to timing of price increase

• Increased domestic RTD competition

International recovering volumes

Sub-Sahara Africa (incl BLNS)

• Angola still challenging

Revenue on a NDP basis outside RSA comprises 28.9% of group revenue

Savings initiatives impact positively on group EBIT increase

79.9%

6.0%

14.1%

-12.8%

0.9%-1.1%

76.2%

11.1%

12.7%

South Africa

International

Africa (incl BLNS)

-8.0%

5.1%

-1.3%

Volumes

down 3.1%Revenue up

2.4%

77.6%

6.3%

16.1%

EBIT (before Service

Centres) up 9.8%

10.1%

22.5%

3.9%

EBIT = Earnings before

interest and taxIncrease/decrease

from previous year

Contribution per region Markets outside RSA contributing almost a quarter of revenue

25

Interim investor – December 2016 Contribution per category Strong growth in spirits adj GP; balanced revenue contribution

Note: Calculated excluding cash discounts and DVC where applicable

• High prior year base due to timing of price increase

• Increased domestic RTD competition

• Wine and spirits show revenue growth of 3.5%

• 4th Street showing strong revenue growth of 38.3%

• Viceroy revenue up 66.8%

9.2%

36.1%53.4%

-5.6%

0.6%

0.1%

33.1%

28.7%

38.1%

Spirits Wine

Cider/RTD Other

2.1%

Volumes

down 3.1%

Revenue up

2.4%

19.5%

29.4%

46.3%

Adjusted Gross Profit

up 6.1%

5.2%2.4%

7.6%3.5%

3.5%

Increase/decrease

from previous year

26

Interim investor – December 2016

Exchange rates Weaker pound creating drag on revenue growth

Currency 2016/17 2015/16

Change

on History

GBP 17.90 20.80 -13.9%

EUR 15.38 14.97 2.7%

USD 14.00 13.56 3.2%

CAD 10.62 10.27 3.4%

YTD December 2016

average rates

Average exchange rate strengthening 2.9% on History

27

Interim investor – December 2016

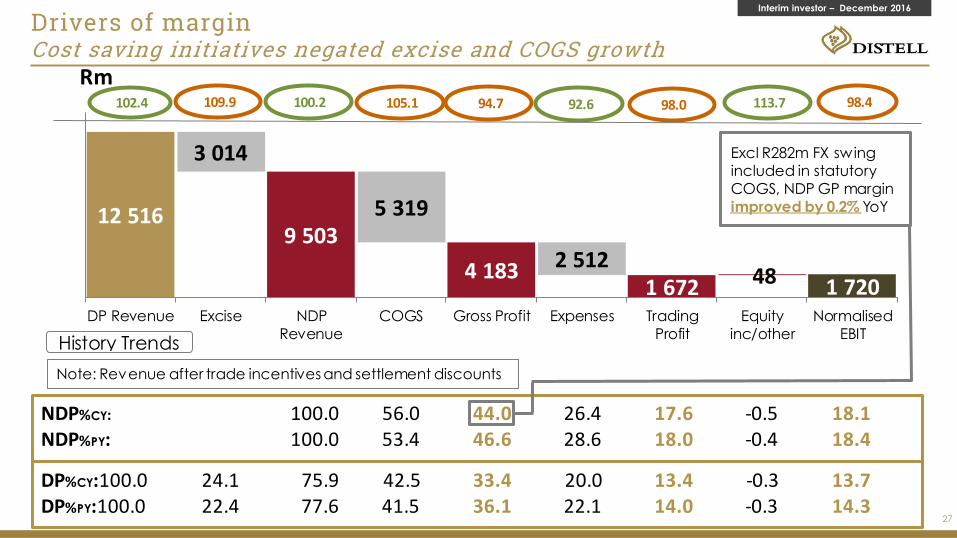

Drivers of margin Cost saving initiatives negated excise and COGS growth strategies

9 503

4 1831 672 1 720

3 014

5 319

2 512

12 516

48

DP Revenue Excise NDP

Revenue

COGS Gross Profit Expenses Trading

Profit

Equity

inc/other

Normalised

EBIT

Rm109.9 100.2 105.1 94.7 92.6 98.0 113.7 98.4 102.4

History Trends

NDP%CY: 100.0 56.0 44.0 26.4 17.6 -0.5 18.1NDP%PY: 100.0 53.4 46.6 28.6 18.0 -0.4 18.4

DP%CY:100.0 24.1 75.9 42.5 33.4 20.0 13.4 -0.3 13.7DP%PY:100.0 22.4 77.6 41.5 36.1 22.1 14.0 -0.3 14.3

Note: Revenue after trade incentives and settlement discounts

Excl R282m FX swing

included in statutory

COGS, NDP GP margin

improved by 0.2% YoY

28

Interim investor – December 2016 Drivers of revenue growth Price increase and volume decline resulting in net marginal growth Drivers of revenue growth

12,516

41174

12,223

72

678

28

2015 History

Volume Sales Mix Currency Price New/Disc prod + Other

2016 Actual

Rm

Index 102.4 0.2 5.5 (0.6)0.6 (3.4)100.0

29

Interim investor – December 2016

Exlcuding R282m FX swing included in statutory COGS, GP trend =

Drivers of gross profit

4 183

124 117 126426

120

4418

678

2015 History Volume Mix Currency Price Revenue

Price COGS

New/Disc prod + Other

2016 Actual

Rm

Index 94.7 (2.7)(9.6)15.3 (2.9)(2.6)(2.8)100.0

101.1

Drivers of gross profit Price increase not sufficient to counter negative impacts

30

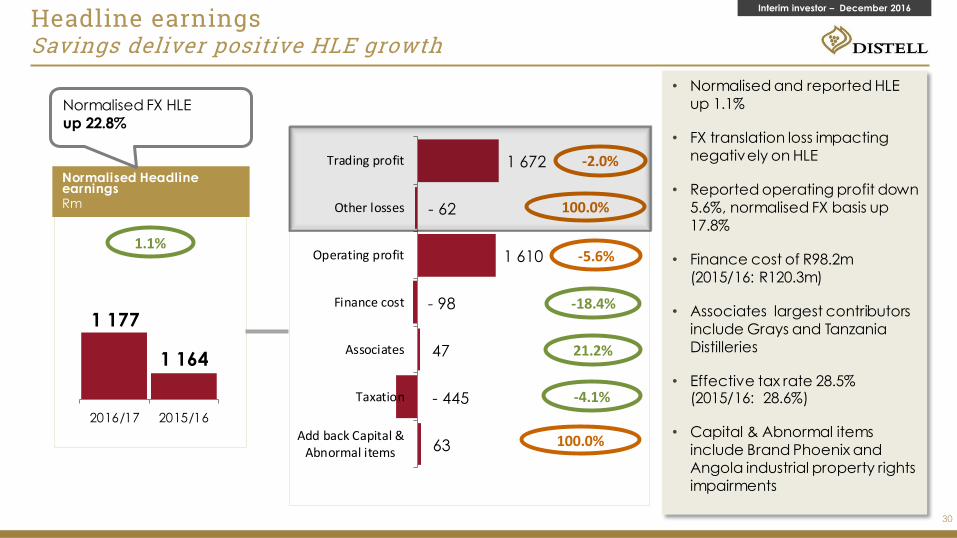

Interim investor – December 2016 Headline earnings Savings deliver positive HLE growth

• Normalised and reported HLE

up 1.1%

• FX translation loss impacting

negatively on HLE

• Reported operating profit down

5.6%, normalised FX basis up

17.8%

• Finance cost of R98.2m

(2015/16: R120.3m)

• Associates largest contributors

include Grays and Tanzania

Distilleries

• Effective tax rate 28.5% (2015/16: 28.6%)

• Capital & Abnormal items

include Brand Phoenix and

Angola industrial property rights

impairments

Normalised Headline earningsRm

1 177

1 164

2016/17 2015/16

1.1%

1 672

- 62

1 610

- 98

47

- 445

63

Trading profit

Other losses

Operating profit

Finance cost

Associates

Taxation

Add back Capital &Abnormal items

-5.6%

-18.4%

21.2%

-4.1%

100.0%

-2.0%

100.0%

Normalised FX HLE

up 22.8%

31

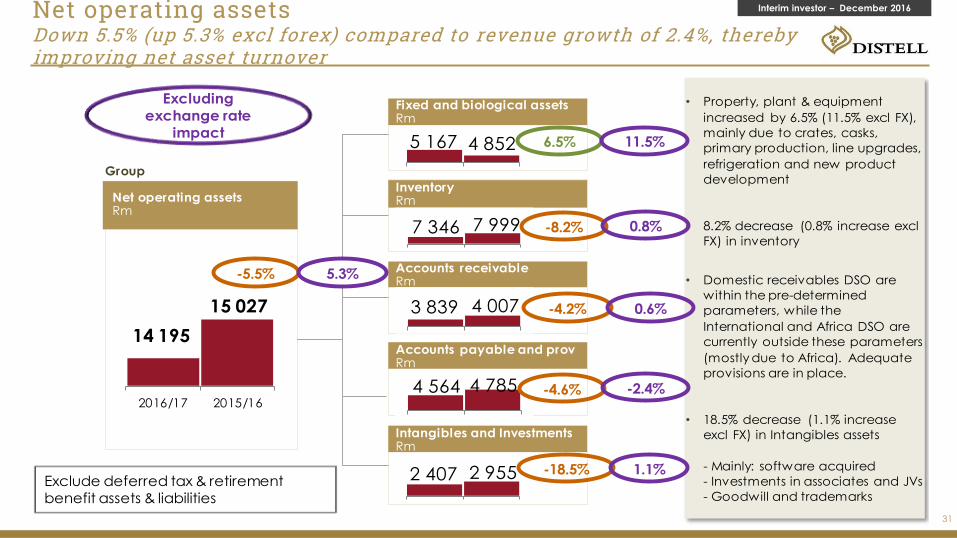

Interim investor – December 2016 Net operating assets Down 5.5% (up 5.3% excl forex) compared to revenue growth of 2.4%, thereby improving net asset turnover to net revenue growth of 2.4%, thereby improving net asset turn

18

• Property, plant & equipment

increased by 6.5% (11.5% excl FX),

mainly due to crates, casks,

primary production, line upgrades,

refrigeration and new product

development

• 8.2% decrease (0.8% increase excl

FX) in inventory

• Domestic receivables DSO are

within the pre-determined

parameters, while the

International and Africa DSO are

currently outside these parameters

(mostly due to Africa). Adequate

provisions are in place.

• 18.5% decrease (1.1% increase

excl FX) in Intangibles assets

- Mainly: software acquired

- Investments in associates and JVs

- Goodwill and trademarks

Fixed and biological assetsRm

InventoryRm

Accounts receivableRm

Accounts payable and provRm

Intangibles and InvestmentsRm

Group

Net operating assetsRm

14 195

15 027

2016/17 2015/16

5 167 4 852 6.5%

7 346 7 999 -8.2%

3 839 4 007 -4.2%

4 564 4 785 -4.6%

2 407 2 955 -18.5%

-5.5%

Exclude deferred tax & retirement

benefit assets & liabilities

5.3%

Excluding

exchange rate

impact11.5%

0.8%

0.6%

-2.4%

1.1%

32

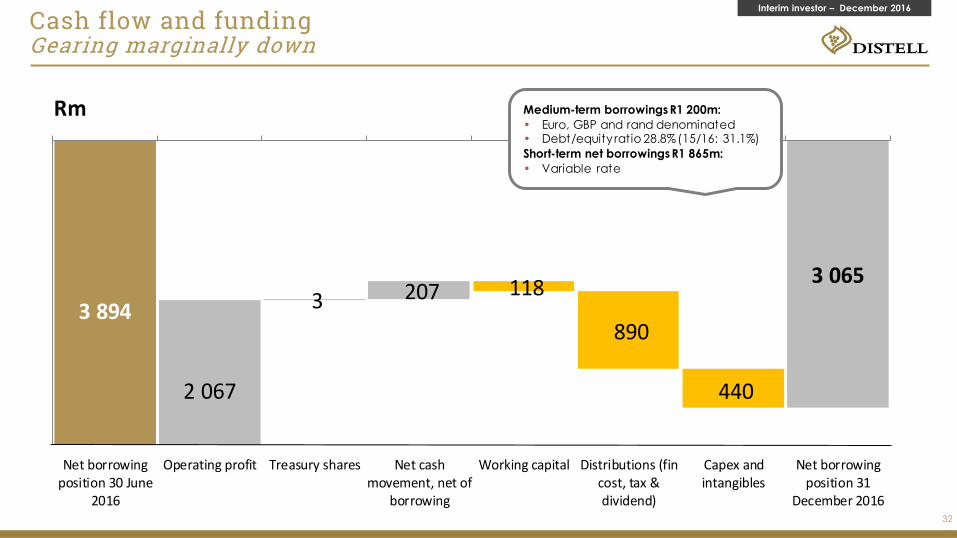

Interim investor – December 2016

Cash flow and funding Gearing marginally down Cash flow and funding

3.4311.393

3.233

2 067

3 2073 065

3 894118

890

440

Net borrowingposition 30 June

2016

Operating profit Treasury shares Net cashmovement, net of

borrowing

Working capital Distributions (fincost, tax ÷nd)

Capex andintangibles

Net borrowingposition 31

December 2016

Rm Medium-term borrowings R1 200m:

• Euro, GBP and rand denominated• Debt/equity ratio 28.8% (15/16: 31.1%)

Short-term net borrowings R1 865m:

• Variable rate

33

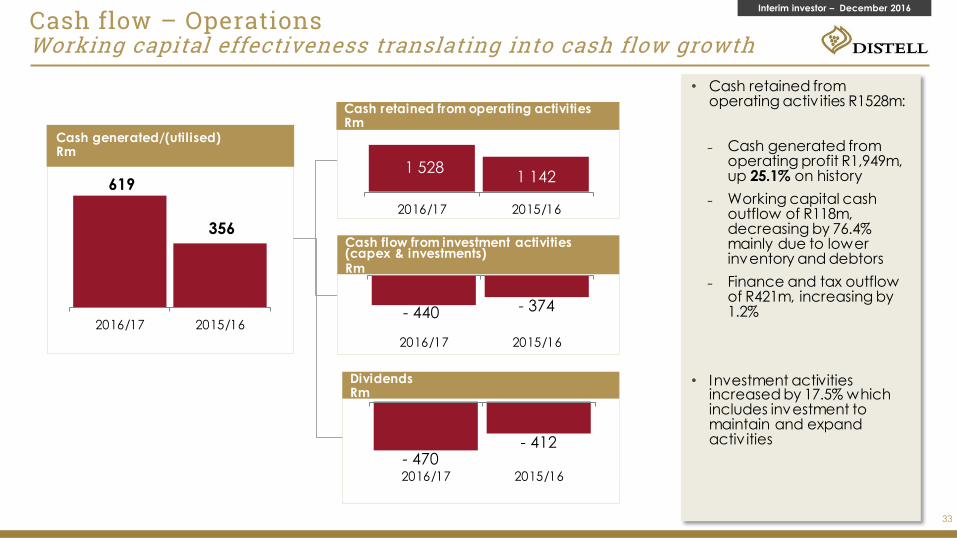

Interim investor – December 2016

Cash flow – Operations Working capital effectiveness translating into cash flow growth activities

• Cash retained from operating activ ities R1528m:

Cash generated from operating profit R1,949m, up 25.1% on history

Working capital cash outflow of R118m, decreasing by 76.4% mainly due to lower inventory and debtors

Finance and tax outflow of R421m, increasing by 1.2%

• Investment activities increased by 17.5% which includes investment to maintain and expand activ ities

Cash retained from operating activitiesRm

Cash generated/(utilised)Rm

Cash flow from investment activities (capex & investments)Rm

DividendsRm

619

356

2016/17 2015/16

1 5281 142

2016/17 2015/16

- 440 - 374

2016/17 2015/16

- 470- 412

2016/17 2015/16

34

Interim investor – December 2016

In conclusion

Looking ahead:

South Africa will drive mainstream penetration and review premium opportunities

We will defend our cider position in South Africa with innovation and investments

Drive the mainstream wines and spirits opportunity

Internationally focus is on markets where we have established platforms

Measured African expansion with considered investments in RTM platforms

Capture mainstream opportunities and build scale in priority African markets

Continue on our journey for growth to build a leaner, focused and more agile organisation:

Focused portfolio-tail brand, SKU and asset rationalisation

Optimised supply chain network-ensure low cost and consistent quality

Align our organisation design-optimal ‘create-demand’ and ‘meet demand’ model

Inorganic activity is crucial to enhance existing markets and unlock new markets:

Strong pipeline with interesting potential for diversification and step change

Interim investor – December 2016

This presentation contains ‘forward-looking’ statements, including specifically all statements that express market

forecasts; Distell’s commentary on macro and industry related market trends; and projections related to Distell’s

business strategy.

All forward-looking statements contained in this presentation involve risk and uncertainty since they are dependent

on assumptions of circumstances that will occur in the future. There are multiple variables which could cause actual

results to differ from the forward-looking statements which are not within Distell’s management control. Such

variables include, but are not limited to, political, macro and socio-economic changes; legal and regulatory

changes; litigation developments; technological changes; environmental risks and changes in consumer trends,

among others. As such, Distell is not liable for any financial or other losses incurred arising from investment decisions

made on the basis of forward-looking statements contained in this presentation.

As such, you are cautioned not to place undue reliance on the forward-looking statements contained herein, as

they apply only as at the date of this presentation.

All forward-looking statements made by Distell apply only as of the date they are made. There is no obligation on

Distell in the future to provide updates on forward-looking statements contained in this presentation to reflect any

changes in Distell’s projections with regard thereto or any changes in events or underlying assumptions on which

any such statement is based.

Disclaimer