interim report january-march 2015 saab - … · interim report january-march 2015. magnus Örnberg,...

TRANSCRIPT

INTERIM REPORTJANUARY-MARCH 2015

Magnus Örnberg, EVP and CFO

7 January 2016

SAAB - OVERVIEW

AN OVERVIEW OF OUR COMPANY

14,700EMPLOYEES

SALES

23,527MSEK (2014)

Geographic sales distribution

CUSTOMERS IN

100COUNTRIES

45

22

14

108

Air

Land

Naval

Security

Commercialaeronautics

%

2

HISTORICAL PERSPECTIVESALES AND EBIT MARGIN1998-2014

0%

2%

4%

6%

8%

10%

12%

14%

0

5 000

10 000

15 000

20 000

25 000

30 000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MSE

K

Sales, Sweden Sales, outside Sweden EBIT margin

Acquisition ofCelsius in 2000

Acquisition ofGrintek in 2005

Acquisition ofEMW

in 2006

Divestment ofSaab Space in

2008

Aquisition ofKockums in 2014

Divestment of share inC3-technologies in

2011

Aquisition of Sensis in2011

3

4

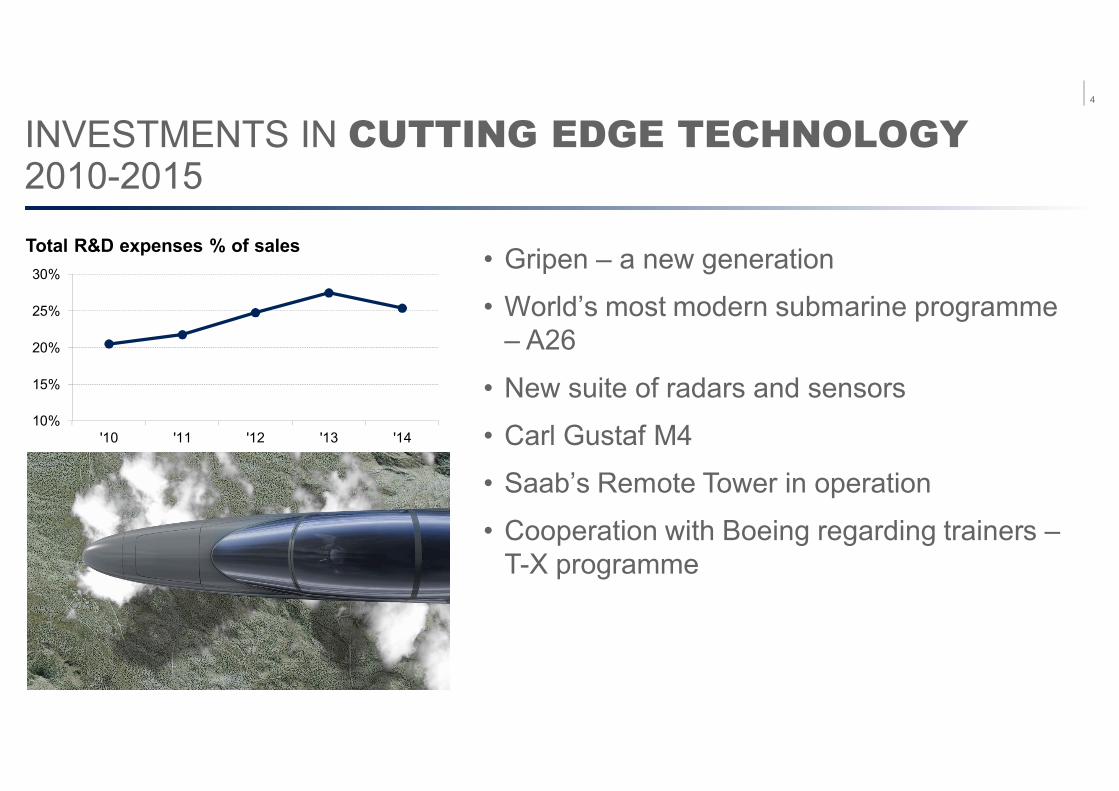

• Gripen – a new generation

• World’s most modern submarine programme– A26

• New suite of radars and sensors

• Carl Gustaf M4

• Saab’s Remote Tower in operation

• Cooperation with Boeing regarding trainers –T-X programme

10%

15%

20%

25%

30%

'10 '11 '12 '13 '14

INVESTMENTS IN CUTTING EDGE TECHNOLOGY2010-2015

Total R&D expenses % of sales

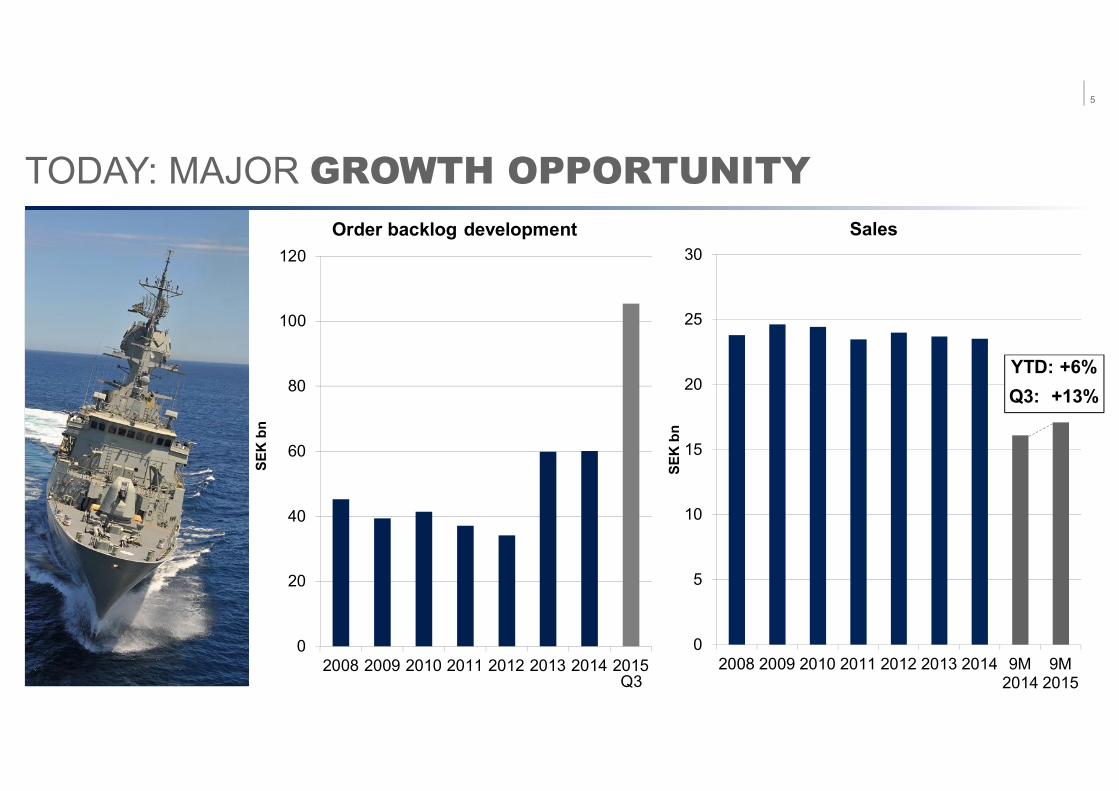

TODAY: MAJOR GROWTH OPPORTUNITY

0

20

40

60

80

100

120

2008 2009 2010 2011 2012 2013 2014 2015

SEK

bn

Order backlog development

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 9M2014

9M2015

SEK

bn

Sales

5

Q3

YTD: +6%Q3: +13%

Brasilia,Brazil

Washington DC,USA

Stockholm,Sweden

London,United Kingdom

Bangkok,Thailand

ORGANISATION

Aeronautics

Security and Defence Solutions

Dynamics

Support and Services

Electronic Defence Systems

Industrial Products and Services

BUSINESS AREASBUSINESS AREAS

CEOCEO

GROUP FUNCTIONSGROUP FUNCTIONSMARKET AREASMARKET AREAS

Asia Pacific

North America

Europe, Middle East & Africa

Latin America

Nordic & Baltic

BOARDBOARD

Our headquarters…

6

SAAB’S BROAD OFFERING

7

GRIPENA GLOBAL SUCCESS STORY

• High performance andoutstanding availability

• Extremely agile andmanoeuvrable, full multirolecapabilities

• Small logistic footprint - cost-effective operations andupgrades

• Superior information sharing

• Very high weapon flexibility

Operated by airforces in fivecountries and theEmpire Test Pilots’School in the UK.

Also purchased byOPERATIONAL AND

MAINTENANCE COST

OPERATIONAL

EFFECT

COST

PRODUCTION ANDDEVELOPMENT COST

Target: 300-450 aircraft sold overthe next 20 years

This represents 10 per cent of theaccessible market

Gripen has won 50 per cent ofcompeted business opportunities

1950 2015

8

SAAB AS A PARTNER

• Technology transfer – is a win-win situation forus and our customers

• Innovation – we spend about 25 per cent ofsales on R&D

• Anticorruption – we have an absolute zerotolerance towards corruption

• Swedish Defence Export regulations

9

HIGHLIGHTS 2015

• Gripen NG contract with Brazil effective; order intake SEK 39.3 bn• Contract with Sweden for the construction of two Type A26 submarines

• UAE ordered New Advanced Airborne Surveillance Systems, USD 1.27 bn

• Margins in the period impacted by loss in Dynamics and continuedinvestments in the T-X* programme

• Positive operating cash flow in Q3 due to milestone payments related toGripen and submarine programmes

• Organisational change as of 1 January: business area Security DefenceSolutions dissolved

• Increased focus on performance management

PROFITABLEGROWTH

PERFOR-MANCE

PORTFOLIO& PEOPLE

*Saab cooperates with Boeing in order to participate in the U.S. Air Force’s upcoming procurement regarding trainer aircraft

STRENGTHENED MARKET POSITION

10

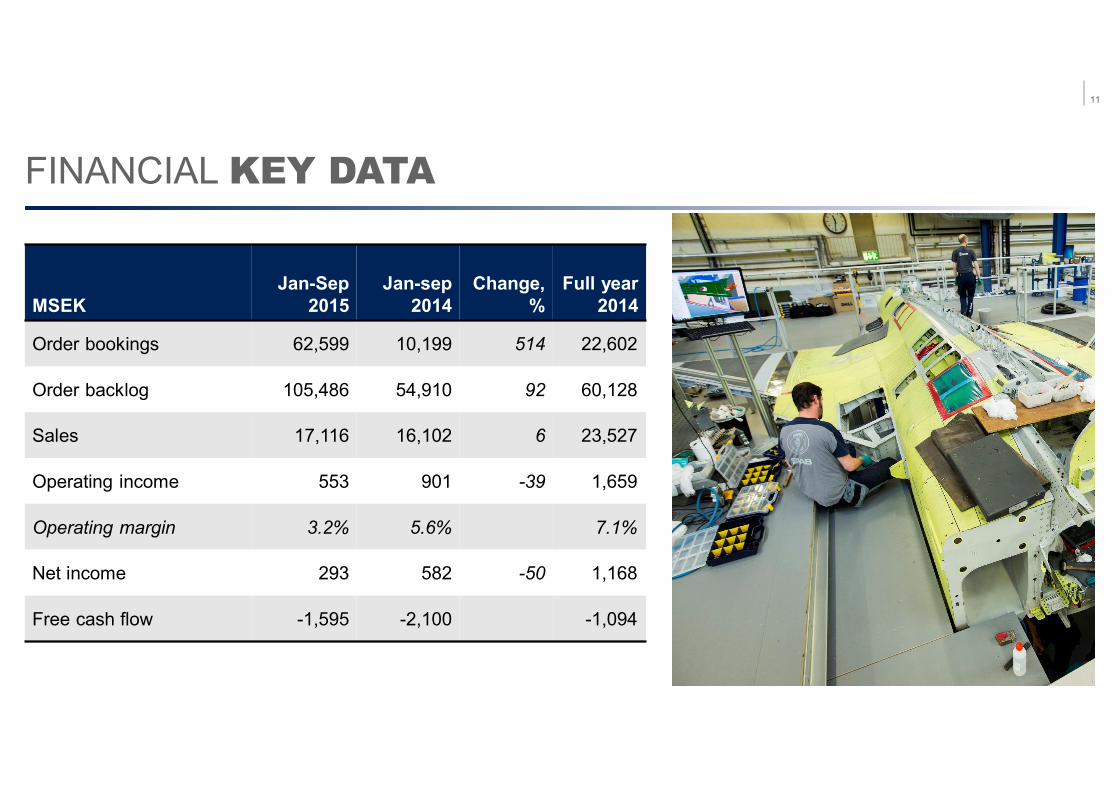

FINANCIAL KEY DATA

MSEKJan-Sep

2015Jan-sep

2014Change,

%Full year

2014

Order bookings 62,599 10,199 514 22,602

Order backlog 105,486 54,910 92 60,128

Sales 17,116 16,102 6 23,527

Operating income 553 901 -39 1,659

Operating margin 3.2% 5.6% 7.1%

Net income 293 582 -50 1,168

Free cash flow -1,595 -2,100 -1,094

11

ORDER BACKLOG

Order backlog duration, SEK bn

30 Sept 2015 31 Dec 2014 30 Sept 20142015: 7.7 2015: 17.8 2014: 6.92016: 18.2 2016: 10.2 2015: 14.42017: 14.0 2017: 5.7 2016: 8.42018: 10.9 2018: 5.6 2017: 5.0After 2018: 54.7 After 2018: 20.8 After 2017: 20.2Total: 105.5 Total: 60.1 Total: 54.9

0

20 000

40 000

60 000

80 000

100 000

120 000

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 Q3'15

MSE

K

Order backlog development

40%

60%

Order backlog distribution

SwedenRoW

12COMPANY UNCLASSIFIED | NOT EXPORT CONTROLLED

© Saab

ORDER BACKLOG STRENGTHENEDIN ALL BUSINESS AREAS Q3 VS. DEC ’14

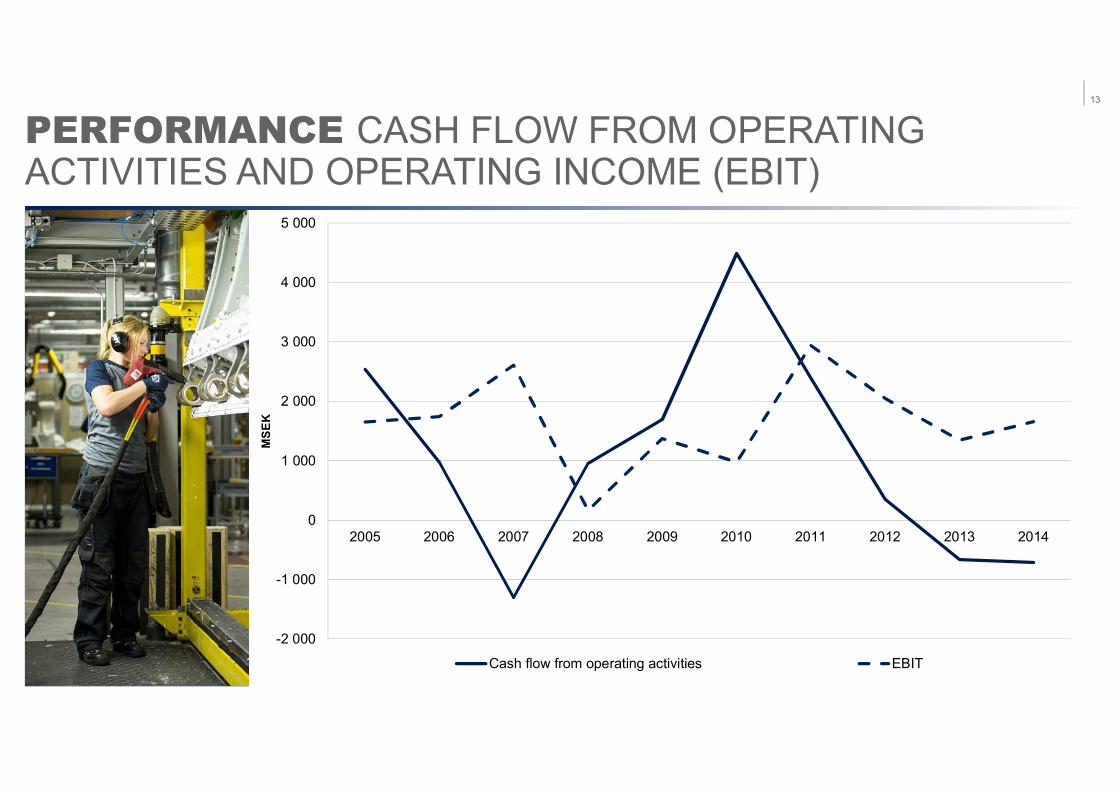

PERFORMANCE CASH FLOW FROM OPERATINGACTIVITIES AND OPERATING INCOME (EBIT)

-2 000

-1 000

0

1 000

2 000

3 000

4 000

5 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MSE

K

Cash flow from operating activities EBIT

13

FINANCIAL POSITIONDevelopmentQ3 2015, MSEK

Net liquidity (+) / Net debt (-), 31 December 2014 -2,113Cash flow from operating activities -799

Change in net pension obligation 383

Net investments -796

Financial lease -444

Dividend -501

Currency impact and unrealised results from financialinvestments

-57

Net liquidity (+) / Net debt (-), 30 September 2015 -4,327

Net pension obligation, 30 September 2015 2,145

Total interest-bearing assets, 30 September 2015 -292

Liquidity -2,474

Equity/assets ratio, 30 September 2015 35.1

14

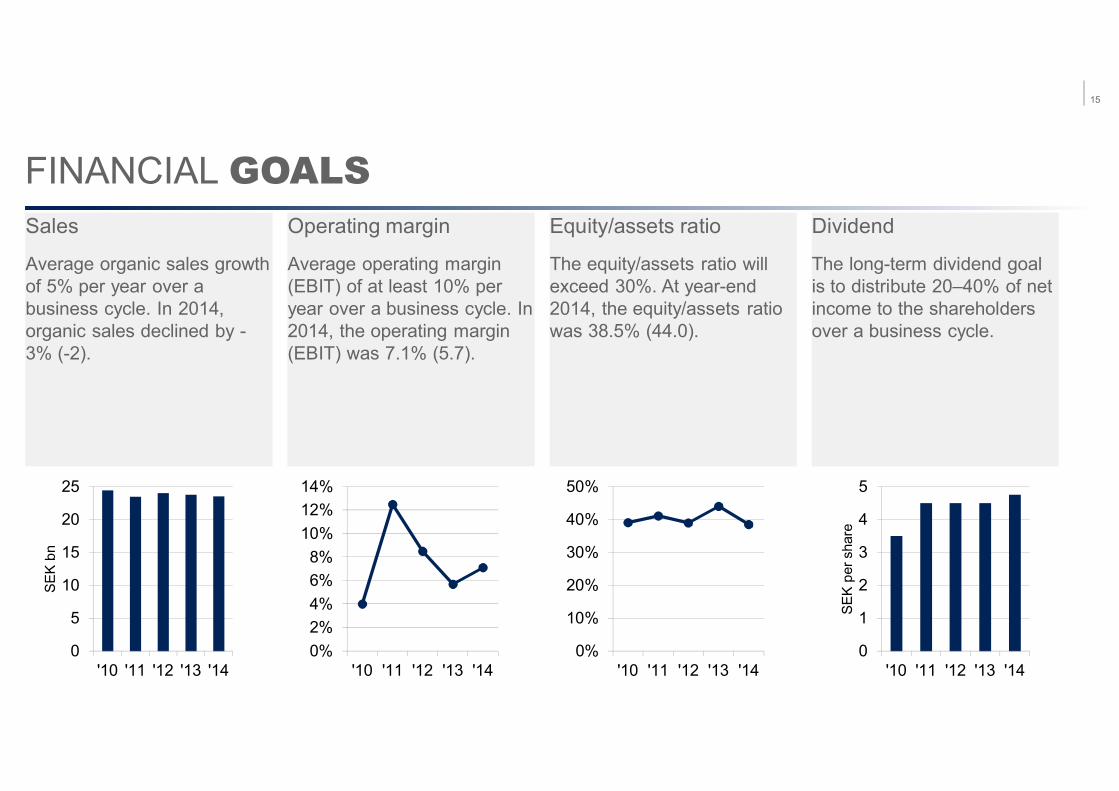

FINANCIAL GOALSSales

Average organic sales growthof 5% per year over abusiness cycle. In 2014,organic sales declined by -3% (-2).

Operating margin

Average operating margin(EBIT) of at least 10% peryear over a business cycle. In2014, the operating margin(EBIT) was 7.1% (5.7).

Equity/assets ratio

The equity/assets ratio willexceed 30%. At year-end2014, the equity/assets ratiowas 38.5% (44.0).

Dividend

The long-term dividend goalis to distribute 20–40% of netincome to the shareholdersover a business cycle.

0

5

10

15

20

25

'10 '11 '12 '13 '14

SEK

bn

0%

10%

20%

30%

40%

50%

'10 '11 '12 '13 '140%2%4%6%8%

10%12%14%

'10 '11 '12 '13 '140

1

2

3

4

5

'10 '11 '12 '13 '14

SEK

pers

hare

15

OUTLOOK STATEMENT 2015

• In 2015, we estimate sales to increase more than Saab’s long-term goal: annual organic sales growth of 5 per cent.

• The operating margin 2015 excluding material non-recurringitems is expected to be in line with the operating margin in 2014.In 2015, increased internally funded research and developmentefforts within Aeronautics will have a negative impact on theoperating margin.

16

UNIQUE MARKET POSITION

• Record high order backlog – strong platform forgrowth

• Portfolio with cutting edge products andsolutions

• Increasing local presence with establishedpartnerships

• Proven functionality and cost-efficient solutions

Focus going forward:Utilize market momentumIncrease efficiencyStreamline portfolio

17

APPENDIX