interim results 2001 21 may 2001. 2 results overview financial review current trading and prospects...

TRANSCRIPT

INTERIM RESULTS2001

21 May 2001

2

Results Overview

Financial Review

Current Trading and Prospects

Future Strategy

The Case for Investment

Holidaybreak plcINTERIM RESULTS 2001

3

On course for another successful year

First half losses inevitable because of seasonal

nature of Camping

Hotel Breaks and Adventure profitable year round

Interim dividend up 12.5% to 5.4p

Current trading strong in all businesses

Continuation of profits and dividend growth

Interims 2001OVERVIEW

4

Interims 2001PROFIT AND LOSS ACCOUNT

(six months to 31 March 2001)

Unaudited Unaudited Audited6 months to 6 months to 12 months to31 March '01 31 March '00 30 Sept '00

£'000 £'000 £'000Turnover 37,177 20,721 164,518Operating (Loss)/Profit (5,039) (6,282) 23,667(Loss)/Profit Before Tax (6,697) (7,798) 20,709(Loss)/Earnings Per Share (10.5p) (13.1p) 34.0pDividend Per Share 5.4p 4.80p 16.0p

All stated before goodwill amortisation

5

Interims 2001PROFIT & LOSS ACCOUNT - DIVISIONAL ANALYSIS

(six months to 31 March 2001)

Camping Hotel Adventure GroupBreaks

£'000 £'000 £'000 £'000Turnover 2001 - 23,713 13,464 37,177

2000 - 18,571 2,150 20,721Operating (Loss)/Profit 2001 (8,301) 1,965 1,297 (5,039)

2000 (8,137) 1,586 269 (6,282)

All stated before goodwill amortisation

6

Interims 2001BALANCE SHEET

Unaudited Unaudited Audited31 March '01 31 March '00 30 Sept '00

£'000 £'000 £'000Fixed Assets/Investments 61,796 55,262 54,858Goodwill 31,913 28,856 32,753Net Current Liabilities (18,717) (10,698) (29,113)Non Current Liabilities (1,521) (1,051) (1,521)Net Debt (56,237) (61,432) (32,203)Net Assets 17,234 10,937 24,774

7

Interims 2001CASH FLOW

(six months to 31 March 2001)

Unaudited Unaudited Audited31 March '01 31 March '00 30 Sept '00

£'000 £'000 £'000Operating Cash Flow (13,628) (10,713) 39,726Interest (1,658) (1,516) (2,958)Tax (1,716) (1,278) (5,080)Capex (Net) (4,277) (6,388) (4,356)Acquisitions - (24,205) (28,911)Dividends - - (6,569)Loans, Shares & H.P. (17,972) 24,763 30,308Net Cash Flow (39,251) (19,337) 22,160

8

Bookings 5% up on 2000 - all markets performing well

c.93% of anticipated final sales (90% of bookings) now received

Spring Bank and June filling - important for low season occupancy

Little left to sell in peak season

Mobile-homes account for 54% of bookings (50% in 2000)

Interims 2001CAMPING - TRADING AND PROSPECTS

9

Existing market moving away from tents and into more profitable mobile-homes

Aim to broaden appeal by addressing misconceptions about camp-site holidays and mobile-homes

‘Self-catering’ rather than ‘camping’

Low-cost airlines making southern destinations more accessible

TV advertising tested extensively alongside traditional media and direct mail

Internet now an important and cost effective distribution channel

Camping2001 UK MARKETING CAMPAIGN

10

Camping2001 UK MARKETING CAMPAIGN

[]

11

Camping2001 UK MARKETING CAMPAIGN

SUPERIOR SELF CATERING ACCOMMODATION CHOOSING YOUR HOLIDAY HOME

LUXURY ACCOMMODATIONHOLIDAY HOMES

a higher quality self-catering six styles to choose from

12

Sales revenues 24% ahead year on year

c.70% of anticipated final figure received

Successful year despite rail problems, flooding and

foot and mouth

Direct and internet bookings particularly strong

Rainbow acquisition has proved beneficial

Interims 2001HOTEL BREAKS - TRADING AND PROSPECTS

13

Hotel BreaksINTERNET

Distribution channel forSuperbreak product range

Superbreak.com Hotelnet.co.uk

On-line HotelBookings

Specialist internethotel booking portal

45,000 hotelslower commission rates

1,500 hotels at full margin

14

Hotel BreaksINTERNET

Remarkable growth since on-line bookings introduced(Nov ‘99) - now c.10% of core business salesOne third of bookings direct - balance is commissionable (Hotelnet, Leisurehunt, Thos Cook etc)Taking share in overall UK hotel breaks marketHotelnet - worldwide product range with

preferential links to superbreak.com- small deficit in 2001 (c.£300k) due to

investment programme- should move into profit thereafter

Many visitors to both sites from overseas

15

Bookings up 13% year on year

c.85% of anticipated final sales now received - some

overhead pressures

Europe/shorter holidays selling particularly well

for Explore

Non-Red Sea sales growing strongly for Regal

First quarter winter bookings now coming in well

Interims 2001ADVENTURE - TRADING AND PROSPECTS

16

Explore Worldwide acquired February 2000Simon Tobin (ex-Keycamp) appointed MDMarketing Director appointedSo far we have - improved sales effectiveness in call

centre- thoroughly researched customers

and competitors- reviewed office systems- introduced a more strategic view- investigating potential acquisitions

Regal acquired August 2000 - stable and trading well

AdventurePOST ACQUISITION REVIEW

17

Concentrate on strong market leading businesses -avoid volatile, low margin, short-haul packages

Organic growth combined with ‘bolt-on’ acquisitions to existing divisions and acquisition of travel businesses in new sectors

Characteristics of Group businesses provide an excellent platform for growth and a template for future acquisitions

Holidaybreak plcFUTURE STRATEGY

18

Market leading businesses in specialist sectors

Healthy margins

Low fixed cost commitments

Highly cash generative

Growth opportunities

Holidaybreak plcCOMMON CHARACTERISTICS

19

CAMPING Eurocamp and Keycamp combined have a sectorshare of over 60% in all the main markets andare recognised as the leading brands in pre-sitedcamping and mobile-home holidays

HOTEL BREAKS Superbreak and its subsidiary brands currentlyaccount for over 60% of hotel breaks bookedthrough UK travel agents

ADVENTURE Explore Worldwide is the largest adventuretravel operator in Europe with an estimated UKmarket share of 40%.Regal Holidays has an estimated 25% of the UKscuba diving market

Common CharacteristicsMARKET LEADERSHIP

20

1999 2000

CAMPING 15.6% 16.6%

HOTEL BREAKS 9.8% 9.5%

ADVENTURE - 14.1%

GROUP 12.7% 13.4%

Compared to:

AIRTOURS 2.8% 1.8%

FIRST CHOICE 2.4% 3.4%

Common CharacteristicsHEALTHY OPERATING MARGINS

21

CAMPING No commitments to travel costsNo site ownershipFlexible camp-site contracts allow flexing of capacityto match demand and ensure healthy load factors

HOTEL BREAKS No commitments to hotel rooms (sale or returnallocations)Consistent gross margin (30%)No commitments to travel costsTravel agency commissions (av. 14.5%) linked to sales

ADVENTURE Scheduled air seats – no commitments (except Regal)Tours only run if target load factors achievedTours added if demand warrantsOverseas operational costs almost all variable

Common CharacteristicsLOW FIXED COSTS

22

CAMPING Substantial but flexible capex rewardedby rapid payback

HOTEL BREAKS IT and office capex onlyNegative working capitalYear round positive cash flowStrong cash generation

ADVENTURE IT and office capex onlyNegative working capitalYear round positive cash flowStrong cash generation

Common CharacteristicsCASH GENERATION

23

CAMPING Profitable mobile-homes growing andreplacing lower margin tentsOverseas markets, especially Germany,on a healthy growth trend

HOTEL BREAKS Sector growthDirect sales/internetInboundProduct Development/Hotelnet

ADVENTURE Sector growing stronglyProduct developmentConsolidation in fragmented sectorOverseas markets

Common CharacteristicsGROWTH PROSPECTS

24

Excellent growth prospects and good defensive

qualities

Strong record of earnings and dividend growth

Highly cash generative

Modest rating - discount to peer group

High yield

Holidaybreak plcTHE CASE FOR INVESTMENT

25

HistoricPER

(2000)

ProspectivePER

(2001)

DividendYield

(Historic)HOLIDAYBREAK(387.5p)

11.4x 10.2x 4.1%

AIRTOURS(300.25p)

32.9x 15.4x 3.2%

FIRST CHOICE(164.5p)

14.6x 13.7x 2.6%

Holidaybreak plcPEER GROUP COMPARISON

Based on closing share price (shown in brackets) on 14/05/01

26

Holidaybreak plc

APPENDICES

27

E xp lore W o rldw ide R eg al

A d ven tu re*(£27.5m )

S u ns ites K eycam p E u ro cam p E C In d ep end ent E u ro villag es

C am p ing(£102.3m )

S u perbreak G o ld en ra il L u xu ry H o teln et

H o te l B reaks(£46.1m )

H olidaybreak P lc

*As per last twelve month’s statutory accounts

Holidaybreak plcCURRENT BUSINESSES

28

Holidaybreak plcTHE BOARD

B o b B ad d e leyF in an ce D irec tor

J im C rewC am p ing

N ick C u stH o te l B reaks

M ark W rayH o te l B reaks

S im o n To b inA d ventu re

R ich ard Atk insonC h ie f Execu tive

E xecs

C live M cL in to ck P eter F o lkm an

A n gu s C rich ton -M illerC h a irm an

N o n -Execs Ju lie V icke rsC om pany S ecre ta ry

B oard

29

2000 1999Group Group£'000 £'000

Turnover 164,518 142,436 +15.5%Gross Profit 48,308 39,992 +20.8%Operating Profit 23,667 20,050 +18.0%Profit before Tax 20,709 17,271 +19.9%Earnings per Share 34.0p 29.3p +16.0%Dividend per Share 16.0p 14.0p +14.3%

Holidaybreak plc2000 PROFIT & LOSS ACCOUNT (1)

All stated before goodwill amortisation

30

Camping Hotel-Breaks Adventure Group£'000 £'000 £'000 £'000

Turnover 2000 102,357 46,054 16,107 164,5181999 103,739 38,697 - 142,436

Gross Profit 2000 34,703 8,742 4,863 48,3081999 32,470 7,522 - 39,992

PBIT 2000 17,001 4,390 2,276 23,6671999 16,231 3,819 - 20,050

Holidaybreak plc2000 PROFIT & LOSS ACCOUNT (2)

All stated before goodwill amortisation

31

Holidaybreak plc2000 BALANCE SHEET

2000 1999£'000 £'000

Fixed Assets/Investments 54,858 48,666Goodwill 32,753 -Net Current Liabilities (29,113) (16,038)Non-Current Creditors (900) (977)Deferred Tax (621) (74)Net Debt (32,203) (24,896)Net Assets 24,774 6,681

32

Holidaybreak plc2000 CAPITAL EXPENDITURE & DISPOSALS

£'000 Mobile- Camping Other Totalhomes Equipment Assets

Opening NBV 34,997 7,404 6,265 48,666Additions 13,464 4,991 1,159 19,614Acquisitions - - 553 553Disposals (3,738) - (34) (3,772)Depreciation (5,102) (4,972) (1,208) (11,282)Closing NBV 39,621 7,423 6,735 53,779

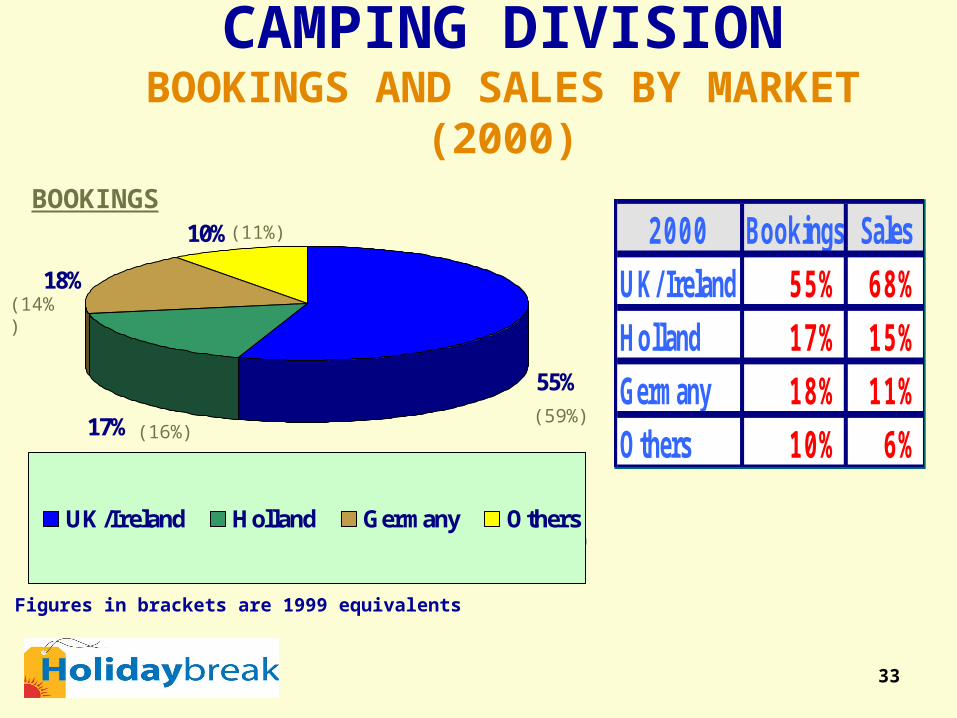

33

Switzerland, AustriaBelgium, Poland &Denmark

Figures in brackets are 1999 equivalents

(11%)

(14%)

(16%) (59%)

55%

17%

18%

10%

UK/Ireland Holland Germany Others

2000 Bookings SalesUK/Ireland 55% 68%Holland 17% 15%Germany 18% 11%Others 10% 6%

BOOKINGS

CAMPING DIVISIONBOOKINGS AND SALES BY MARKET (2000)

34

CAMPING DIVISIONBOOKINGS AND SALES BY BRAND (2000)

59%32%

2% 4%3%

Eurocamp Keycamp

Sunsites EurovillagesEurocamp Independent

Bookings SalesEurocamp 59% 53%

Keycamp 32% 38%

Sunsites 3% 4%

Independent 4% 3%

Eurovillages 2% 2%

BOOKINGS

35

CAMPING DIVISIONCOMPETITION & MARKET SHARE (2000)

UK Ireland Holland Germany Denmark Tents/m.homes

OwnSites

Holidaybreak(Eurocamp,Keycamp & Sunsites)

61% 70% 64% 71% 49% 45/55

Eurosites (Airtours) 20% 1% 16% 29% 51% 60/40

Haven 10% 12% 8% - - 20/80

Canvas Holidays 9% - 13% - - 75/25

Campotel - 17% - - - 60/40

Figures are for 2000. UK, Holland, Germany and Denmark show only those companies included in the AC Nielson pool. Figures for Ireland are local estimates and include the main local operator. In other markets (Switzerland, Belgium, Poland) no significant direct competition has been identified.

36

CAMPING DIVISIONBRANDS AND OFFICE LOCATIONS

S U T T O N (U K )C O R K (IR E L A N D )

L E ID E N (H O L L A N D )

K E Y C A M P(£ 3 8 .2 m )

H A R T F O R D (U K )A M E R S F O O R T (H O L L A N D )

H A M B U R G (G E R M A N Y )D IE S S E N H O F E N (S W IT Z E R L A N D )

E U R O C A M P(£ 5 4 .9 m )

H A R T F O R D (U K )

S U N S IT E S (£ 3 .6 m )E U R O V IL L A G E S (£ 2 .2 m )

E U R O C A M P IN D E P E N D E N T (£ 3 .5 m )

C A M P IN GD IV IS IO N

2000 sales in brackets

37

HOTEL BREAKSSALES BY BRAND (2000)

55.4%

18.0%

4.0%

12.3%

10.3%

Superbreak

Hotel Breaks

Luxury Hotel Collection

Airport Hotels

Theatre

38

HOTEL BREAKSSALES DISTRIBUTION (2000)

36%

42%

19%3%

Multiple agents

Other agents

Direct

Internet

39

HOTEL BREAKS BRANDS AND PRODUCTS

BRANDS PRODUCT CHARACTERISTICS

Superbreak Core brand – 772 hotels in current programme. Railinclusive, theatre and event packages offered

Hotel Breaks Similar to Superbreak (500 hotels) but with moreemphasis on budget priced hotels

LuxuryCollection

197 top quality hotels – Elegant accommodation, finecuisine and outstanding hospitality

NationalTrust

Special National Trust endorsed brochure for NationalTrust members with 204 hotels

Theatrebreak Theatre and concert inclusive packages

Airport Overnight accommodation in 91 hotels at or close to allmajor UK airports and ferry ports

40

Operator CurrentShare

Estimate

Comment

Superbreak/Goldenrail/Rainbow

65% Multi-brand, multi-productstrategy

Highlife 13% Thistle

Embassy 8% Jarvis

LTS/Bridge 6% Airtours

Crystal 5% Thomson

Others 3% Forte, Best Western etc

HOTEL BREAKS COMPETITION AND MARKET SHARES (RETAIL)

41

ADVENTURE HOLIDAYS SALES (2000)

10%

16% 20%

10%

15%16%

13%

Egypt & Middle EastGreece & TurkeyEuropeAmericas & PacificAsiaIndia & NepalAfrica

42

Overseas holidays account

for 33% of passengers and

58% of expenditure

UK still important but now

primarily a secondary

holiday destination

12-13m inbound visitors to the UK

Travel Industry OverviewUK HOLIDAY MARKET

UK Holiday Market 2000

Domestic 73m pax(£11.0bn)

Overseas 35m pax (£15.2bn)

Source: MintelExcludes VFR

43

Overall sector growing at c.4% per annumDistribution fragmenting - multiple channels - high street agents in declineGrowth Areas include:- Short-breaks - Long-haul- Activity/Special Interest- Grey tourism- Tailor-made

Travel Industry OverviewOVERSEAS HOLIDAY MARKET

Overseas Holidays 2000

Source: MintelExcludes VFR

Scheduled Air Surface Travel

Independent Air Charter

5.5m

3.5m

16.1m

9.9m

44

Holidaybreak plcOUR RECORD (1)

Turnover Profit£m

164.5142.4

113.5106.4

104.7

70.0

90.0

110.0

130.0

150.0

170.0

1996 1997 1998 1999 2000

17.314.0

11.29.26

20.7

7

9

11

13

15

17

19

21

1996 1997 1998 1999 2000

£m

45

Holidaybreak plcOUR RECORD (2)

18.321.6

26.829.3

34.0

10

15

20

25

30

35

1996 1997 1998 1999 2000

14.012.5

11.511.0

16.0

7.00

9.00

11.00

13.00

15.00

17.00

1996 1997 1998 1999 2000

Earnings per Share DividendPence Pence