interim results for six months ended 30 june 2010 market position - international name global...

TRANSCRIPT

Interim results for six months ended 30 June 2010

2

What is Cello?

Large independent UK based market research and consulting GroupSplit into 2 divisions:

Research and Consulting (c.65% operating income)Tangible (c.35%)

Primary strength in pharmaceutical sectorGood spread across different industry sectorsStrong and growing online credentialsSignificant business base in the UK, Europe and USAGlobal expansion a key strategic intent

3

Highlights

Operating income up 3% to £29.9m (2009: £29.1m*)Headline operating profit up 25% to £3.3m (2009: £2.6m*) Headline operating margin 10.9% (2009: 8.9%)Interim dividend per share 0.525p (up 5.0%)Net debt £11.7m – continued strong operating cash flowStrong new business performanceMomentum in Q3 2010 continuesRobust non-UK pipeline in Research and ConsultingGood revenue visibility in Tangible

*after removing discontinued operations

4

Market position - UK

Name Turnover £m (2009)1. TNS UK 1662. Ipsos Mori 1283. GfK UK 1254. Cello 525. Mintel 506. Research Now 487. Hall and Partners 208. Harris Interactive 209. ICM Research 1910. BDRC Continental 15

*Source: Marketing Market Research Leagues September 2010

Cello (Research and Consulting) Tangible

Name Gross Profit £m (2009)1. Gyro HSR 442. Iris Worldwide 433. Digital Marketing Group 424. Tangible 245. Tullo Marshall Warren 226. The Marketing Store 227. CHI & Partners 208. The Direct Marketing Gp 169. Billington Cartmell 1510. Transactis 14

*Source: Marketing magazine published March 2010

5

Market position - International

Name Global revenue$m (2009)

1. The Nielsen Co. 4,6282. Kantar 2,8233. IMS Health Inc. 2,1904. GfK SE 1,6235. Ipsos S.A. 1,3156. Synovate 8167. Symphony IRI Group 7068. Westat Inc. 5029. Arbitron Inc. 38510. INTAGE Inc. 36911. JD Power and Associates 24512. The NPD Group Inc. 22613. Dunnhumby Ltd. 203

Name Global revenue$m (2009)

14. Video Research Ltd. 20115. Harris Internative Inc. 16716. Maritz Research 15517. IBOPE Group 14618. comScore Inc. 12719. Opinion Research Corp. 9820. Abt SRBI Inc. 9021. Mediametric 8922. Lieberman Research WW 8823. Cello 8224. Market Strategies Int. 8025. Macromill Inc. 72

Cello (Research and Consulting)

*Source: Inside Research published August 2010

6

Client profile

7

R&C 2010

R&C 2009

Top client = 4.4% of operating incomeTop 20 clients = 39.2% of operating income and average 12 year relationship

9/20 top clients are pharmaceutical

Tangible 2010Tangible 2009

0

5%

25%

10%

20%

15%

Client sector focus30%

8

Major client projects in 2010Pharmaceuticals 3M Healthcare, Astra Zeneca, Roche, Boehringer, GSK, Kimberly Clark, Allergan, Bayer,

Novartis, Pfizer, Harley Medical Group, Johnson and Johnson, Procter and Gamble,

Public Sector Cambridgeshire County Council, Energy Saving Trust, The National Archives, Festivals Edinburgh, Home Office, Creative Scotland, London Councils, Sports Council for Wales, Manchester City Council, Metropolitan Police, Tfl, Glasgow City Council, Scottish Enterprise.

Financial Services Scottish Widows, Abbey, Zurich Financial Services, Chartis, Ernst and Young, HSBC, Grant Thornton, Lloyds TSB, NS&I, Standard Life, FSA, Bank of Ireland, Rothschild, Sainsbury’s Finance, BUPA.

Telecoms/IT Vodafone, Brother International, Xerox, Apple Europe, HP, Microsoft, Nokia, Braun, O2, Orange, Epson, Panasonic, Philips, Canon, Samsung UK, Carphone Warehouse, Sony, Dell.

Leisure EA, Book Tokens, Virgin, UK Cycling, Sadler’s Wells, Tottenham Hotspur, Alcan.

Charity WWF, Barnados, Macmillan, UNICEF UK, Breakthrough Breast Cancer, Salvation Army, British Heart Foundation, Cancer Research UK, CLIC Sargent, Deafness Research UK, Diabetes UK, NSPCC, Duke of Edinburgh’s Award, Medecins Sans Frontieres.

Retail Boots, Lush, TK Maxx, Gum Tree, Expedia, John Lewis, Seven Seas, Matalan, Argos, Tesco, Ebay, Crabtree and Evelyn, B&Q, Waterstones.

FMCG Camelot, Avon, Kelloggs, PZ Cussons, Cadburys, Unilever, Velux, Coca Cola, Nestle, Reckitts Benkiser, Heineken, Pepsico

Food and Drink Dairy Crest, Heineken, Britvic, McDonalds, Dominoes, Heinz, Pizza Express, Nando’s, Ben and Jerry’s, Pret A Manger, AG Barr, Tetley, Twinnings, Yo Sushi, Ginster.

Transport Eurostar, First Scotrail, British Airways.

Other Centrica, ITV, BP, Scottish Water, BSkyB, Channel 4, Calor, EDF, Scottish Power, EON, National Energy Services, Five, BBC, Radio Creative, British Gas, Miele.

9

International network

Research and Consulting overseas operating income c. 45%

Cello operational officesCello associate offices

10

Professional structure

plc

Managing Partner

Partner

Associate Partner

Employee

3 Execs, 3 Non-Execs

7 divisional heads

29 MDs, prime op-co board members

44 future MDs

c.680

Cash bonus+

Options+

Training

11

Core priorities

Investing in further growth in USAAppointment of CEO Cello USARe-organisation into Manhattan hub officeWest Coast and Chicago presence

Investing in service innovationMarketing science product suite for pharmaceutical clients to be extended into FMCG clientsOnline social network research capacity expandedOnline web-to-print and PURL campaign capability for charity clients expanded into non-charity sectors

Investing in pharmaceuticals and healthcare

12

Online social network research

Insight eVillage is a ongoing, interactive online community of healthcare professionals, where doctors and nurses are able to partake in a range of individual and group activities where they can share and exchange views on specific prompted themes.

diary task:

eVillage is unique in that it is designed and set up specifically to engender co-creation and long-term participation among healthcare professionals

in what is generally seen to be a ‘consumer space’Making the most of social media principles and new technology

forums, blogs, projective techniques, interactive discussions, patient diaries, multi-media format

Introduced to the pharma industry in the paper,‘Towards the Gold Standard in Qualitative Research’, at the BHBIA Annual Conference 2010

“The use of approaches drawn from Web 2.0 shouldn’t replace traditional market research but can, and should, be used to create real value over and above traditional research”

13

Online social network research (2)

14

Investing in pharmaceuticals and healthcare

Already have strong footprint in healthPharmaceutical sector specifically strong defensive sectorHealthcare sector characteristics ensure continued growth in demand for support servicesOpportunity for number of meaningful acquisitions

15

Investing in pharmaceuticals and healthcare

Ongoing demandAgeing populationBetter diagnostics identifying diseases earlierNew treatments allowing more conditions to be treated

Industry drivers work in our favourCan cost up to $1.3bn to bring a product to market Approx 4% success rate of products getting to marketIt can take up to 13 years to bring a product to market

Companies internal processes drive demandCompanies require critical commercial analysis and decision making throughout product development lifecycle

Asia and Latin America coming on stream

16

Overview of 2010 Interim Results

2010 2009* % change

Turnover £61.5m £55.4m 11%Operating income £29.9m £29.1m 3%Headline operating profit £3.3m £2.6m 25%Headline basic eps 3.41p 2.92p 17%Dividend 0.53p 0.50p 5%Net debt £11.7m £14.8m Anticipated earn outs over four years £4.6m £4.2m *after removal of discontinued operations

Operating cash flow conversion 91%

14%

17

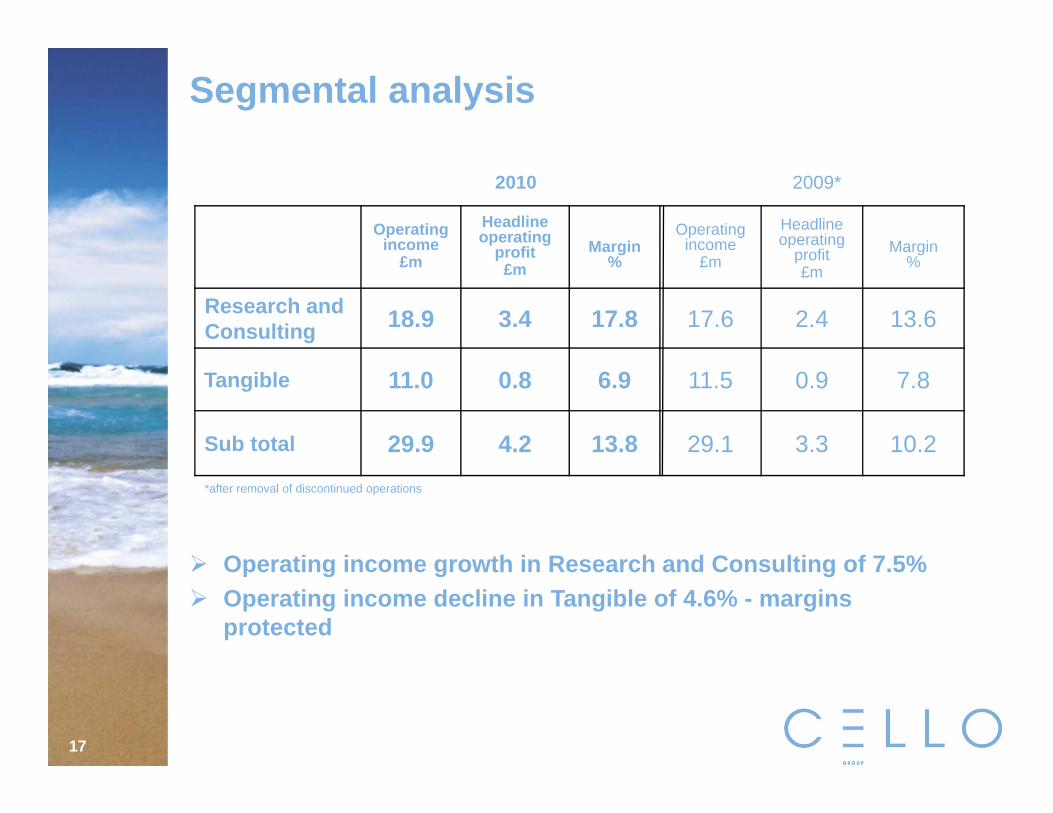

Segmental analysis

Operating income

£m

Headline operating

profit£m

Margin %

Operating income

£m

Headline operating

profit£m

Margin %

Research and Consulting 18.9 3.4 17.8 17.6 2.4 13.6

Tangible 11.0 0.8 6.9 11.5 0.9 7.8

Sub total 29.9 4.2 13.8 29.1 3.3 10.2

2010 2009*

*after removal of discontinued operations

Operating income growth in Research and Consulting of 7.5%Operating income decline in Tangible of 4.6% - margins protected

18

Profit before tax reconciliation2010£’000

2009*£’000

Headline operating profit 3,257 2,599Net interest payable (413) (496)Headline profit before tax 2,844 2,103Exceptional costs - (495)Amortisation of intangibles** (165) (266)Deemed remuneration** (60) 347Impairment of intangible assets** - (778)

Impairment of goodwill** - (4,548)

Impairment of available-for-sale investment** - (162)

Notional interest** (29) (68)Fair value gain on financial instruments 31 23Reported profit/(loss) before tax 2,621 (3,844)

**non cash *after removal of discontinued operations

Reductions in public sector focused headcount in H2 £0.7m exceptional charge for full year

19

Balance sheet

30 June 2010£m

30 June 2009 £m

Fixed assets GoodwillIntangible assetsFixed assetsInvestmentsDeferred tax asset

68.91.12.5-

0.8

69.61.32.90.10.9

Current non cash assets 23.7 26.6Cash 2.9 4.1

Creditors < 1 year (27.9) (27.8)

Net current assets/(liabilities) (1.3) 2.9Creditors > 1 yr (10.6) (16.5)Earn out liabilities/provisions (4.6) (4.2)Net assets 56.8 56.8

20

Earn out liabilities

Estimated deferred cash acquisition costs of £2.25m payable 2010-13Estimated deferred share element of acquisition costs of £2.55m to be issued 2011-13

2011 Estimate

£m

2012 Estimate

£m

2013 Estimate

£m

Total Estimate

£m

Cash/loan notes 1.3 - 0.95 2.25

Shares to be issued (£m) 1.6 - 0.95 2.55

Total 2.9 - 1.9 4.8

Earn out Obligations at 30 June 2010

Approximate Timetable

Earn out liabilities of £4.8m over three years (£4.6m plus £0.2m future P&L charges)

21

Cash flow

2010 £m

2009 £m

Net cash inflow from operating activities 3.0 (0.4)

Tax paid (0.1) -

Cash outflow from investing activities (1.1) (1.2)

Cash inflow from financing (1.5) 1.0

Dividends paid (0.5) (0.4)

Decrease in cash for period (0.2) (1.0)

Strong headline operating cash inflow for 2010 - 91% cash conversion (2009 full year: 86%)

22

Net debt position£m

Cash balance at 30 June 2010 (1.4)RCF drawn down 3.0Loan 10.0Finance leases 0.1

Net debt at 30 June 2010 11.7

Bank facilities renewed in March 2010£10m loan; £7m RCF, £2m overdraftRenewed until March 2013Amortises at £2m - £3m per annumNet Debt: EBITDA < 1.5 pricing dropped to 275 bps over LIBOR

23

Summary and Outlook for 2010

Solid H1 like for like revenue growth (boosts double digit profit growth)Continued detailed cost managementLong standing client relationships remain strong and growingMaintaining focus on Research and Consulting

Increasing international exposureFocus on pharmaceutical sector

Strong new client wins provide good visibility for remainder of H2

www.cellogroup.co.uk