internal control of transactions operation in the

TRANSCRIPT

Internal control of transactions operation in the sustainable management system of organizations

Alsou Zakirova1,*, Guzaliya Klychova1, Angelina Dyatlova2, Gamlet Ostaev3, and Elena

Konina3

1Kazan State Agrarian University, 65, Karl Marx str., 420015, Kazan, Russia 2Moscow University Ministry of Internal Affairs of Russian named after V. J. Kikot, Academic Volgin str., 12, 117997, Moscow, Russia 3Izhevsk State Agricultural Academy, 11, Studencheskaya str., 426069, Izhevsk, Russia

Abstract. In modern conditions one of the main problems of economic entities is the increase in accounts receivable and payable, which is influenced by objective and subjective factors. In this connection the role of internal control of settlement operations is increasing. The aim of the article is to improve methodological support of internal control of settlement operations for increasing the quality of audit, providing information about the state of settlements with contractors to the management of enterprise for making operational and strategic management decisions. The proposed methodological support is based on

stage-by-stage audit of settlement operations including the following main stages: audit planning; implementation of control procedures; execution of audit results. the peculiarity of internal control of settlement operations is determined by a variety of normative and information support of the audit. For the purpose of improvement of control procedures in the course of the study working documents of internal control have been developed. The working document «Verification of the availability of the agreement with a separate counterparty» can be used by the controller to identify errors arising in the preparation of the contract, as well as to determine the

completeness and timeliness of the parties to fulfill their obligations, With the proposed in the study working document «Confirmation of the status of settlements with counterparties» can identify cases of fraud and misstatement of data contained in the financial statements. In the course of the study it was proposed to perform a point-rating assessment of debtor reliability based on a system of key indicators in the internal control process. The suggested rating estimation of counterparties will make it possible to carry out their comparative analysis and grouping as well as to

identify those counterparties that have a high probability of non-payment of existing debts. The practical significance of the study lies in the possibility of using the developed approaches to determine the information base, to set the purpose and definition of control tasks, to the rational choice of control procedures, to the use of working papers in the process of internal control of settlement operations.

* Corresponding author: [email protected]

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

© The Authors, published by EDP Sciences. This is an open access article distributed under the terms of the CreativeCommons Attribution License 4.0 (http://creativecommons.org/licenses/by/4.0/).

1 Introduction

For any actively functioning economic entities in modern conditions of great

importance is accounting for settlements with counterparties, Improving the efficiency of

settlement relations depends directly on the independence and responsibility of economic

entities in the development and adoption of management decisions [1-3]. For acceptance of

effective administrative decisions the effectively functioning system of information

maintenance which directly depends on creation within the enterprises of system of internal

control of settlement operations is necessary [4-6].

To improve the state of settlements with counterparties it is necessary to control the

ratio of accounts receivable and payable [7-9]. A large amount of accounts receivable

negatively affects the financial stability and causes the need to attract additional resources [10-14]. At the same time, an increase in accounts payable leads to insolvency of the

economic entity, reducing the investment attractiveness 15-17].

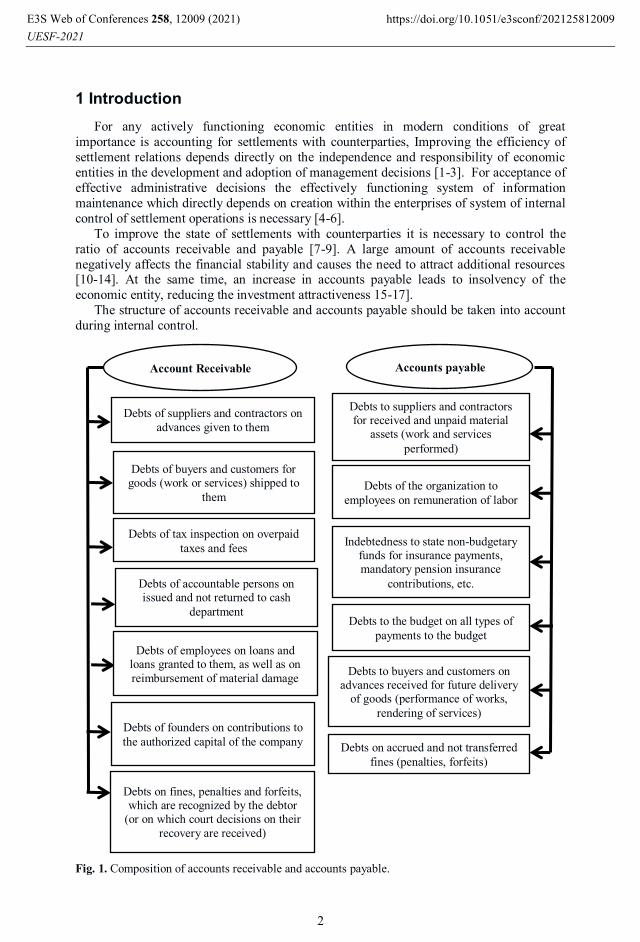

The structure of accounts receivable and accounts payable should be taken into account

during internal control.

Fig. 1. Composition of accounts receivable and accounts payable.

Account Receivable

Debts of suppliers and contractors on

advances given to them

Accounts payable

Debts to suppliers and contractors for received and unpaid material

assets (work and services

performed)

Debts of buyers and customers for goods (work or services) shipped to

them

Debts of tax inspection on overpaid

taxes and fees

Debts of accountable persons on issued and not returned to cash

department

Debts of employees on loans and loans granted to them, as well as on

reimbursement of material damage

Debts of founders on contributions to

the authorized capital of the company

Debts on fines, penalties and forfeits, which are recognized by the debtor

(or on which court decisions on their

recovery are received)

Debts of the organization to

employees on remuneration of labor

Indebtedness to state non-budgetary funds for insurance payments, mandatory pension insurance

contributions, etc.

Debts to the budget on all types of

payments to the budget

Debts to buyers and customers on advances received for future delivery

of goods (performance of works,

rendering of services)

Debts on accrued and not transferred

fines (penalties, forfeits)

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

2

As can be seen from Figure 1, accounts receivable represents the amount of debts that

counterparties owe to the audited economic entity. Accounts payable is represented by the

indebtedness of the audited economic entity to counterparties to fulfill certain obligations.

At internal control of settlement transactions it is recommended to use a unified

methodological technique, which consists in standardization of conducting an audit and

implementation of control procedures [18-20]. In the most general form the process of

internal control includes [21-24]:

1. Setting the goal and formulating the tasks of internal control;

2. Determination of the normative and informational support of the internal control of

settlement operations.

3. Specification of the methods used in the course of control; 4. Detection of violations and formation of the conclusion on the results of inspection.

The experience of foreign authors is very useful for deepening theoretical and

methodological foundations of internal control [25-28].

At the same time, the practical importance of solving the issues of optimizing the state

of settlement relations with counterparties, intensified in the conditions of economic crisis,

causes the need for further development of the methods of internal control of settlement

operations [29, 30].

2 Materials and Methods

The purpose of internal control of settlement operations is to establish their legality,

reliability and expediency, timely detection of inadmissible increase or non-payment of receivables and payables, optimization of settlement relations with counterparties, reduction

of risk of arrears.

In the process of internal control of settlement operations the following tasks are solved:

- contractual and payment discipline is monitored;

- timely adjustments are made to accounting procedures with due regard for newly

adopted regulations;

- the accuracy of documents recording settlement transactions is assessed;

- the reality, completeness and timeliness of the debt repayment on settlements with the

contractors is confirmed;

- assessment of the correctness of the analytical accounting on the accounts of

payments, check whether the data of synthetic and analytical accounting figures in the general ledger and balance sheet;

- correctness of correspondence of accounts for accounting transactions is checked;

- the periodicity of the inventory of payments in accordance with the regulations and

provisions of accounting policies is determined, the results of the inventory are analyzed;

- correctness of tax calculations and timeliness of payments is assessed;

- the validity of claims made as a result of breach of contractual obligations is analyzed;

- the causes of accounts receivable and payable are established;

- the management bodies are provided with the information necessary to make effective

managerial decisions;

- it is determined how effectives are the measures taken by the economic entity to

minimize accounts receivable and liquidate accounts payable [31-33].

In order to assess the legality and validity of settlement transactions, as well as to solve other internal control tasks, the controller must be fully provided with the regulatory and

informational framework that governs the object of inspection (Figure 2).

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

3

Fig. 2. Regulatory and information support of internal control of settlement transactions.

Figure 2 shows the regulatory and legal acts and sources of information that are used by

the controller in the process of checking settlement transactions. Internal sources of

information necessary for checking of settlement transactions are enterprise accounting

Payroll, payroll for FSS funds,

individual cards recording the

amount of accrued payments

and the amount of accrued insurance premiums

Tax returns, tax accounting

registers, tax policy on tax

accounting, tax cards on

personal income tax

Employment contracts, orders

on hiring, transfer, dismissal,

personal accounts of employees

Accounting policy of the

organization

The procedure for

issuing funds on

account, the timeliness

of the report on the

amounts issued

System of synthetic and

analytical accounts, sub-

accounts

Composition and content of

financial statements,

requirements for them,

evaluation of items,

information accompanying financial statements

Calculation procedure,

procedure and terms for

payment of insurance premiums

Formation of accounting

policies, disclosure of

accounting information

Basic requirements for

book keeping

Contracts of sale, supply,

services

Accounting (financial)

statements of the company

Accounting policy of the organization

Accounting policy on

accounting, the working plan

of accounts of the

organization, typical

correspondence

Payment documents, invoices,

business contracts

Advance report

Instruction of the Bank of Russia «On

the procedure for cash transactions by

legal entities and the simplified

procedure for cash transactions by

individual entrepreneurs and small

businesses»

Timeliness of payments,

formation of accounts

receivable and payable

Civil Code of the

Russian Federation

Normative act The object of

regulation

Sources of

information

Availability and correctness

of contracts

Tax Code of the Russian

Federation

Objects of taxation, tax

base, tax rates, tax benefits

Labor Code of the Russian

Federation

Issues related to compliance

with labor legislation,

registration of labor relations

Federal Law «On

Accounting»

Federal Law «On

Mandatory Social

Insurance for Temporary

Incapacity for Work and

Maternity»

Accounting Regulation

1/08 «Accounting Policy»

Accounting Regulation

4/99 «Accounting

Reports»

Plan of accounts for

financial and economic

activities of organizations

and instructions for its

application

Regulations of the Bank

of Russia «On the rules of

money transfers»

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

4

policy, economic contracts, employment contracts, orders, administrative documents,

accounting documents (invoices, bills of lading, payroll, payment documents, advance

reports, registers of synthetic and analytical accounting, general ledger, etc.), reporting, tax

accounting registers, tax declarations.

Fig. 3. Control procedures during internal control of settlement transactions.

Co

nt

ro

l

Pr

oc

ed

ur

es

Arithmetic control is used to confirm the reliability of arithmetic calculations of amounts

on settlement transactions and the accuracy of their reflection in the accounting accounts.

Confirmation is used when receiving information about the reality of balances on the

accounts of settlements.

Regulatory check involves determining compliance with current legislation, checking the

availability of documents and other conditions that confirm the validity and legality of

certain business transactions to account for settlements with counterparties.

Formal verification - check the availability of documents, registering the fact of settlement transactions, and the presence of the necessary requisites in it.

Reconciliation involves checking the identity of different copies of the same document,

which are in different companies. This method is one of the effective control tools that

allow you to provide objective information to the verification process.

Request - a written request to various departments of an enterprise (internal request) and

to various enterprises and institutions (external request) to provide data on settlement

transactions, which are necessary for analysis and comparison.

Tracing - a method of control, which involves checking individual primary documents on

the accounting of settlement transactions, their subsequent reflection in the accounting

registers, determining the final correspondence of accounts, confirming the correctness of the accounting of the relevant business transactions.

Logical verification - a method of control, which compares the data on the settlement

transactions contained in the documents, with the various circumstances and phenomena

that confirm the very possibility of its commission.

Inventory - a method of control, which establishes the correctness of settlements with

counterparties and the validity of the amounts recorded in the appropriate accounts.

Analytical check - a method of control, which involves the analysis of objects of control,

comparing actual data with forecasts, similar data from past periods, the indicators of

similar enterprises, industry averages; study of unexpected deviations; analysis of the

action of unanticipated factors; evaluation of the analysis in the light of information

received from other.

Legal assessment of contracts - a thorough analysis of the terms, form and other key

points of contracts, checking for compliance with the law.

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

5

The efficiency of internal control is influenced by the correct application of audit

methods and their interaction with the tasks that should be performed to achieve the

purpose of the audit. To increase the efficiency of control at the same time reducing the

time to conduct it, it is necessary to develop its clear methodology, defining control

procedures in the planning of internal control.

Internal control of settlement transactions uses control procedures shown in Figure 3.

The use of control procedures presented in Figure 3 will increase the effectiveness of

control, to achieve the desired results of the audit, to observe the rights and legitimate

interests of controlled entities and ensure the normal functioning of the economic entity.

3 Results

The internal control of settlement operations includes the following main stages: planning

of inspection; execution of control procedures; execution of inspection results.

An independent and obligatory stage is the planning of internal control of settlement

operations in the course of which the information is obtained that allows to form an

objective opinion on the reliability of accounting of settlement operations. At planning of

internal control the program of internal control is made. The recommended form of the

internal control working document (ICWD) «Internal Control Program of Settlement

Transactions» is presented in Table 1.

Table 1. ICWD «Internal Control Program of Settlement Transactions».

Dir

ecti

on

s o

f

co

ntr

ol

No

rm

ati

ve b

ase

So

urces

of

info

rm

ati

on

Co

ntr

ol

perio

d

Na

me o

f

co

ntr

oll

er

Na

ture o

f

verif

ica

tio

n

Co

ntr

ol

pro

ced

ures

1. Assessment

of the

correctness of

the execution

of contracts

Civil Code of the

Russian

Federation

Economic contract 17.02.2020 Ivanov

I.I.

Selective Regulatory

review, formal

verification,

legal

evaluation of

the contract

2. Checking

the primary

accounting of

settlement

transactions

Federal Law «On

Accounting»

Invoices,

consignment

notes, payment

documents; forms

of primary

accounting

documents on

settlement

operations,

attached to the

order on

accounting policy

of the

organization,

schedule of

document flow

18-20.02.

2020

Ivanov

I.I.

Selective Normative

verification,

formal

verification,

logical

verification

3. Checking

the data

contained in

the registers of

accounting

transactions,

reconciliation

Accounting

Regulation 4/99

«Accounting

Reports», Plan of

accounts for

financial and

economic

Registers of

synthetic and

analytical

accounting,

General Ledger,

the working plan

of accounts of the

21.02.2020 Ivanov

I.I.

selective Tracing,

arithmetic

check,

confirmation,

formal check

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

6

with the

accounts in the

General Ledger

activities of

organizations and

instructions for

its application

organization, the

technology of

processing

accounting

information

4. Verification

of claims

settlement

Civil Code of the

Russian

Federation,

Accounting

Regulation 9/99

«Income of the

organization»,

Accounting

Regulation 10/99

«Expenses of the

organization»

Business contract,

claims acts,

accounting

registers

25.02.

2020

Ivanov

I.I.

Solid Normative

verification,

arithmetic

verification,

inquiry,

formal

verification

5. Analysis of

the results of

the settlement

inventory

Methodical

instructions on

the inventory of

property and

financial

liabilities. Order

of the Ministry of

Finance of the

Russian

Federation of

13.06.1995 г. №

49

Inventory sheets,

checklists, Plan of

inventory of

property and

liabilities

26-27.02.

2020

Ivanov

I.I.

Solid Inventory,

arithmetical

check

6. Checking

correctness of

correspondence

of accounts for

accounting of

settlement

transactions

Plan of accounts

for financial and

economic

activities of

organizations and

instructions for

its application

Registers of

synthetic and

analytical

accounting,

General Ledger,

chart of accounts,

standard

correspondence of

accounts

28.02.

2020

Ivanov

I.I.

selective Tracking,

arithmetic

control,

inspection

7. Checking

the reality of

settlements

with

counterparties

Civil Code of the

Russian

Federation;

Methodical

instructions on

the inventory of

property and

financial

liabilities. Order

of the Ministry of

Finance of the

Russian

Federation of

13.06.1995 г. №

49

Business contract,

invoice,

consignment note

and other primary

documents,

inventory results

02.03.

2020

Ivanov

I.I.

selective Request,

confirmation,

inventory,

reconciliation

8. Checking

the correctness

of tax

accounting of

settlements

with

counterparties

Tax Code of the

Russian

Federation

Business contract,

invoice, tax

registers, Tax

Accounting Policy

03.02.

2020

Ivanov

I.I.

selective Formal

verification,

arithmetic

verification,

confirmation

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

7

The peculiarity of this program is that it contains a list of control areas, regulatory basis

and sources of information, defines the nature of the audit and control procedures, which

are necessary to achieve the purpose and practical solution of the audit tasks.

The internal control program contains the list of control directions, regulatory basis and

information sources, defines the character of control and control procedures that are

necessary to achieve the purpose and practical solution of the audit tasks. The proposed

program is a detailed inspection instruction and a means of quality control. The internal

control program may be revised as the audit environment and the results of the control

procedures change. Having approved the internal control program, you should proceed to

the check of settlements with counterparties.

The technique of the internal control of the settlement operations includes the following stages.

The first stage of internal control involves the study of forms of settlements with

counterparties and implementation of legal assessment of contracts for their compliance

with current legislation.

During the analysis of settlements with counterparties on the basis of data in the general

ledger determined by the forms of settlements with counterparties used in the enterprise (in

the case of cash settlements accounts 60, 62, 76, etc. are debited in correlation with credit

account 51; for cash settlements - with credit account 50).

The basis of the relationship between an economic entity and counterparties are

contracts, which determine the legal nature of the settlement relationship.

First of all, the controller checks the availability of contracts with individual

counterparties. To do this on the basis of registers of analytical accounting counterparties with which the economic entity performs calculations for the audited period are determined.

Then the names of counterparties are compared with the existing business contracts. The

results of this check can be issued by the working document of internal control (table 2).

Table 2. ICWD «Verification of the availability of the agreement with a separate counterparty».

No

p/p

Name of the

counterparty

according to

the analytical

accounting data

Existence and

type of

contract

Contract

number and

date

Amount

under the

contract,

rubles.

Name of

materials, works

and services

under the

contract

1. LLC «Alliance» Contract of

purchase and sale

№ 1987 from 04.09.2019

98 000 Construction

materials

2. LLC «Legion» Work contract № 1987 from 06.10.2019

141 000 Auto repair shop

4. LLC «Tax»

Agreement for the rendering

of paid services

№ 145 from 17.11.2019

25 000 Consulting

services

The peculiarity of this working document is that it accumulates information about

counterparties; about the types, numbers and dates of contracts concluded with them; the

amount of transactions under the contract and the object of the contract.

This document can be used by the controller to identify errors arising in the preparation

of the contract and are the basis for further improper performance of the counterparties of

their contractual obligations, as well as to determine the completeness and timeliness of the

parties to fulfill their obligations, at internal control should be widely used such control

procedures as the legal assessment of contracts.

With the help of this control procedure can be timely revealed violations made during

the drawing up and conclusion of contracts. In particular, the text of the agreement may not

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

8

contain a decoding of the subject of the agreement; when determining the liability of the

parties, disproportionate liability for non-fulfillment of contractual obligations may be

determined; circumstances that are not such are indicated in the contract as force majeure,

etc.

The second stage - checking the primary accounting of settlement transactions is

presented in detail in figure 5. As can be seen from Figure 4 at this stage the reliability

(accuracy and completeness) of the facts of settlement transactions; promptness of

registration of business transactions; legality of the primary accounting documentation that

formalizes settlement transactions; compliance with the schedule of document flow;

accuracy and completeness of accounting documents in registers; process of document

storage and organization of access to the primary accounting documentation. The third stage involves checking the identity of the data of synthetic and analytical

accounting. This check is carried out selectively to establish the completeness and accuracy

of the data, which are reflected in the accounts of analytical and synthetic accounting of

settlements with counterparties.

By means of arithmetic check the data of synthetic accounting with data on analytical

accounts are reconciled. The final data should coincide with the balances and turnovers of

analytical accounts.

In addition, at this stage, the correctness and reliability of accounts receivable and

payable, reflected in the balance sheet and explanations to it, is checked. The reconciliation

algorithm is shown in Figure 4.

Fig. 4. Algorithm of reconciliation of the data of accounting registers with the indicators of the balance sheet.

Debit balance of settlement

accounts Balance sheet data (page 1230 «Accounts

receivable».

Credit balance in the accounts

for accounting of settlement

transactions

Balance sheet data (page 1520 «Accounts

payable»)

Debit and credit balances in

settlement accounts

Data on the composition of accounts receivable and payable, which are

specified in the notes to the accounting

balance sheet

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

9

Fig. 5. Procedure for checking the primary accounting of settlement transactions.

Verification of

reliability

(accuracy and

completeness) of

the facts of

settlement

transactions

Selection of primary documentation

Checking the availability of primary documents for each specific operation

Comparison of data contained in the primary documents with the warehouse data

(or with the data from the accounting department on the works or services

accepted for accounting)

Checking the

timeliness of the

registration of

business

transactions

Determination of the causes of discrepancies (if any) between the dates of

business transactions and the dates of their registration in the books

Determination of the nature of the discrepancies detected: one-time or systematic

Verification of the

legality of primary

accounting

documents that

formalize

settlement

transactions

Obtaining the necessary amount of evidence that the entire array of primary

accounting records is legally valid and regulatory

Identification of the general level of compliance with the rules of execution of

documents for accounting transactions and their reflection in the act of inspection

Checking

compliance with

the document flow

schedule

Determination of the availability of a document flow schedule for settlement

transactions

Establishing the reality of the document flow schedule

Checking the

accuracy and

completeness of

documents in the

registers

Establishment of the required number of grounds for the accounting of each document

Establishing the completeness of registration of all documents that formalize

the verifiable settlement transactions

Determining the timeliness and accounting of all documents

Determining whether all documents have been properly reflected in accordance

with the economic substance of the procedure and whether all documents have

accurate qualitative and quantitative data transfer

Determination of the timeliness of business transaction registration

Establishment of acceptance for accounting and registration of each document once

Check the process of

document storage

and organization of

access to primary

accounting documents.

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

10

On the basis of registers of synthetic and analytical accounting participants of settlement

relations, their number; forms of payments; directions of analytical accounting; presence of

atypical accounting entries are determined.

At the fourth stage - check of settlements on claims:

1. It is defined whether the documents on pretensions arising during settlements are well

grounded, timely and correctly executed; whether calculations under pretensions are

correctly and completely reflected in accounting; whether debts under pretensions on the

books are real; whether analytic accounting is kept for each claim;

2. The analysis of reasons of occurrence of claims; terms of arrears on claims;

3. Amounts on claims which are presented with violation of terms specified in

contracts; amounts on which limitation period has expired; amounts which are not confirmed by documents are revealed.

The fifth stage of internal control of settlement transactions confirms the reality of

receivables and payables resulting from settlement transactions; the correctness of

organization and conduct of inventory; the validity of the results of the inventory;

completeness and timeliness of the reflection of the results of the inventory.

The sixth stage implies a mandatory check on the correctness of the correspondence of

accounts for each type of calculation. In particular, it is checked whether accounts

receivable and payable arising during settlements with counterparties are reflected in the

accounts correctly. If necessary, check individual doubtful, in the opinion of the controller,

settlement transactions. Determines whether receivables and payables are properly reflected

in the balance sheet.

At the seventh stage of control, the reality of settlements with debtors and creditors is checked, and confidence is achieved that the amount of accounts receivable and payable,

which exist in the accounting accounts, is reflected in real amounts. This should be carried

out continuous or sample inventory of settlements. In the process of such an audit the

following facts are established:

- the timing of receivables and payables;

- availability of overdue accounts receivable with counterparties;

- the validity and correctness of the amounts owed for shortages and thefts that are on

the balance sheet of the enterprise, as well as the measures taken to recover them;

- the presence of operations to write off bad debts, their validity and correctness;

- reality of debt repayment.

When checking the reality of settlements it is necessary to make inquiries to counterparties to obtain information about the state of settlement relations on a certain date.

To confirm the state of settlements we propose to use working document «Confirmation of

the status of settlements with the counterparties» (table 3).

Table 3. ICWD «Confirmation of the status of settlements with counterparties».

SECTION 1 - Reply to request from the counterparty (to be filled in by counterparty)

Name of

counterparty

Bill of lading/receipt/invoice

Total, rub.

Have all

goods/services been

delivered/provided as

of [reporting date]?

(yes / no) Number Date

LLC «Alpha» Invoice №567840 05.07.2019 1 019 672 Yes

JSC «Idel» Invoice №567356 10.04.2019 546 945 Yes

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

11

SECTION 2 - Reconciliation results (to be filled out by the controller)

Name of

counterparty

According to

the request,

thousand

rubles.

According to

accounting

data, thousand

rubles.

Control method Control Results

LLC «Alpha» 1 019 672 1 019 672 Reconciliation, inquiry, inspection,

confirmation

Accounting data is confirmed by

the counterparty

JSC «Idel» 546 945 546 945 Reconciliation, inquiry, inspection, confirmation

Accounting data is confirmed by the counterparty

In the working document for counterparties, the first and second paragraphs are the

amount of receivables and payables requested by the controller. This information is

especially important during the audit, because the audited economic entity may

intentionally overstate its accounts receivable or understate its accounts payable, and the

counterparties, by responding to the inquiry letter, can help identify these violations.

By using a working document and conducting a control procedure - an inquiry to

counterparties - fraud and misrepresentation in the financial statements can be detected.

The eighth stage - checking the correctness of the organization of tax accounting for settlements with counterparties includes the following areas (Figure 6).

Fig. 6. Block diagram of checking the correctness of the organization of tax accounting of settlements with counterparties.

Based on the results of the control procedures performed, the auditor should perform the

actions shown in Figure 7.

Verification of primary documents, on the basis of which accounting records of

payments for taxes and levies were made

Confirmation of the correctness of the calculation of certain taxes

Verification of the correctness of the application of rates for various taxes and fees by comparing the actual rates with their values, regulated by regulatory documents

Checking the accuracy of accrual, completeness and timeliness of the transfer of tax

payments; establishing the correctness of the allocation of taxes to their respective

sources of payment

Checking the correctness of tax reporting

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

12

Fig. 7. Algorithm of actions of the internal controller by the results of control procedures.

In case of detection of deviations during implementation of control procedures, the

reasons of deviations are investigated, reasonable conclusions on the results of internal

control are formulated, as well as the evaluation of the effectiveness of implementation of

control procedures is given.

To summarize the results of the audit and reflection of violations and errors detected in

the course of internal control we recommend to use the working document of internal

control developed by us (Table 4). This document contains a list of violations, systematized

by areas of inspection and recommendations for their elimination.

Control procedures

Deviations from the set parameters,

standards are detected Deviations from the specified parameters,

standards were not identified

Do not correspond to the

expected indicators

Additional information

requested

Additional documents

are being reviewed

Identity and divergence of information obtained during the control, with the

actual evidence of the auditor is established

Conclusions on the results of internal control

Assessment of the effectiveness of the implementation of control procedures

Deviations contradict the

current legislation

Causes of deviations are

investigated

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

13

Table 4. ICWD «Identified violations in settlements with counterparties».

Dir

ecti

on

s of

con

trol

Iden

tifi

ed

vio

lati

on

s

Norm

ati

ve

base

Sou

rces

of

info

rmati

on

Con

trol

Pro

ced

ure

Am

ou

nt,

thou

s. r

ub

.

Rec

om

men

d

ati

on

s fo

r

corr

ecti

ng

vio

lati

on

s

1. A

sses

smen

t of

the

corr

ectn

ess

of

contr

acts

1)

Ther

e is

no a

gre

emen

t

wit

h t

he

counte

rpar

ty

Civ

il C

ode

of

the

Russ

ian

Fed

erat

ion

Com

mer

cial

Agre

emen

t

Norm

ativ

e ver

ific

atio

n

-

Rec

om

men

dat

ions

for

dra

win

g u

p a

contr

act

in

acco

rdan

ce w

ith t

he

law

2)

Inco

nsi

sten

cy o

f th

e

agre

emen

t ty

pe

Civ

il C

ode

of

the

Russ

ian

Fed

erat

ion

Com

mer

cial

Agre

emen

t

Leg

al r

evie

w o

f th

e

contr

act

-

Rec

om

men

dat

ions

for

dra

win

g u

p a

contr

act

in

acco

rdan

ce w

ith t

he

law

3)

The

agre

emen

t w

as s

igned

by a

per

son w

ho d

oes

not

hav

e

the

legal

rig

ht

to d

o s

o

Civ

il C

ode

of

the

Russ

ian

Fed

erat

ion

Com

mer

cial

Agre

emen

t

Form

al v

erif

icat

ion

-

Rec

om

men

dat

ions

for

signin

g a

contr

act

by a

per

son w

ho h

as

the

legal

rig

ht

to d

o s

o

2. C

hec

kin

g t

he

pri

mar

y a

ccounti

ng

of

sett

lem

ent

tran

sact

ions

1. In

voic

es l

ack

cert

ain r

equis

ites

Fed

eral

Law

«O

n

Acc

ounti

ng

»

Invoic

es

Form

al v

erif

icat

ion

-

Rec

om

men

dat

ions

for

fill

ing i

n a

ll

det

ails

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

14

2. N

o d

ocu

men

ts

confi

rmin

g s

ettl

emen

t

oper

atio

ns

Fed

eral

Law

«O

n

Acc

ounti

ng

»

Invoic

es,

consi

gnm

ent

note

s

Norm

ativ

e

ver

ific

atio

n, fo

rmal

ver

ific

atio

n

-

Rec

om

men

dat

ions

for

reques

ting a

pri

mar

y d

ocu

men

t

from

a c

ounte

rpar

ty

and f

illi

ng a

mis

sing

copy f

rom

an

econom

ic e

nti

ty

3. C

hec

kin

g t

he

dat

a co

nta

ined

in t

he

regis

ters

of

acco

unti

ng t

ransa

ctio

ns,

reco

nci

liat

ion w

ith t

he

acco

unts

in t

he

Gen

eral

Led

ger

1. O

ffse

ttin

g v

ario

us

item

s of

deb

t am

ong

them

selv

es

Acc

ounti

ng R

egula

tion 4

/99 «

Acc

ounti

ng

Rep

ort

s», P

lan o

f ac

counts

for

finan

cial

and

econom

ic a

ctiv

itie

s of

org

aniz

atio

ns

and

inst

ruct

ions

for

its

appli

cati

on

Reg

iste

rs o

f sy

nth

etic

and a

nal

yti

cal

acco

unti

ng, G

ener

al L

edger

Tra

ckin

g, ar

ithm

etic

chec

k

35781.6

Rec

om

men

dat

ions

on t

he

refl

ecti

on o

f

bal

ance

s

4. V

erif

icat

ion o

f cl

aim

s se

ttle

men

t

1. F

ailu

re t

o m

eet

clai

ms

dea

dli

nes

Civ

il C

ode

of

the

Russ

ian F

eder

atio

n,

Acc

ounti

ng R

egula

tion 9

/99 «

Inco

me

of

the

org

aniz

atio

n», A

ccounti

ng R

egula

tion

10/9

9 «

Exp

ense

s of

the

org

aniz

atio

n»

Busi

nes

s co

ntr

act,

cla

ims

acts

Reg

ula

tory

chec

k, ar

ithm

etic

chec

k,

inq

uir

y, fo

rmal

chec

k

-

Rec

om

men

dat

ions

on t

he

tim

ing o

f cl

aim

s

in o

rder

to p

reven

t th

eft

of

mat

eria

l as

sets

5. A

nal

ysi

s of

the

resu

lts

of

the

inven

tory

of

acco

unts

1. T

he

act

of

reco

nci

liat

ion o

f m

utu

al

suppli

es d

oes

not

indic

ate

the

fact

of

repay

men

t of

mutu

al d

ebts

by t

he

par

ties

Met

hodic

al i

nst

ruct

ions

on t

he

inven

tory

of

pro

per

ty a

nd f

inan

cial

liab

ilit

ies.

Ord

er o

f th

e M

inis

try o

f

Fin

ance

of

the

Russ

ian F

eder

atio

n o

f

13.0

6.1

995 г

. №

49

Bu

sines

s co

ntr

act,

inven

tory

rec

ord

s,

reco

nci

liat

ion a

ct

Inven

tory

, ar

ithm

etic

chec

k

54890.7

Rec

om

men

dat

ions

on t

he

refl

ecti

on i

n

the

act

of

reco

nci

liat

ion o

f th

e co

nse

nt

of

the

par

ties

to t

he

repay

men

t of

deb

ts

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

15

6. C

hec

kin

g c

orr

ectn

ess

of

corr

esponden

ce o

f ac

counts

for

acco

unti

ng o

f se

ttle

men

t

tran

sact

ions

1. In

corr

ect

corr

esponden

ce

of

acco

unts

Pla

n o

f ac

counts

for

finan

cial

and e

conom

ic

acti

vit

ies

of

org

aniz

atio

ns

and i

nst

ruct

ions

for

its

appli

cati

on

Reg

iste

rs o

f sy

nth

etic

and

anal

yti

cal

acco

unti

ng,

Gen

eral

Led

ger

Tra

ckin

g, ar

ithm

etic

contr

ol,

insp

ecti

on

18003.5

Rec

om

men

dat

ions

for

corr

ecti

ng a

ccounti

ng

entr

ies

7. C

hec

kin

g t

he

real

ity o

f se

ttle

men

ts

wit

h c

ounte

rpar

ties

1. U

nre

cord

ed d

ebts

of

the

buyer

are

revea

led

Civ

il C

ode

of

the

Russ

ian F

eder

atio

n,

Met

hodic

al i

nst

ruct

ions

on t

he

inven

tory

of

pro

per

ty a

nd f

inan

cial

lia

bil

itie

s. O

rder

of

the

Min

istr

y o

f F

inan

ce o

f th

e R

uss

ian

Fed

erat

ion o

f 13.0

6.1

995 г

. №

49

Busi

nes

s co

ntr

act,

invoic

e, b

ill

of

ladin

g

and o

ther

pri

mar

y d

ocu

men

ts, in

ven

tory

resu

lts

Inquir

y, in

ven

tory

, co

unte

r re

conci

liat

ion

20168.8

Rec

om

men

dat

ions

on a

ccounti

ng f

or

unac

counte

d d

ebts

8. C

hec

kin

g t

he

corr

ectn

ess

of

tax

acco

unti

ng o

f se

ttle

men

ts

wit

h c

ounte

rpar

ties

1. In

corr

ectl

y a

ppli

ed t

ax

rate

for

val

ue

added

tax

(VA

T)

Tax

Code

of

the

Russ

ian

Fed

erat

ion

Busi

nes

s co

ntr

act,

invoic

e, t

ax r

egis

ters

Norm

ativ

e ver

ific

atio

n

4108.7

Rec

om

men

dat

ions

for

the

corr

ect

appli

cati

on o

f th

e

tax r

ate

4 Discussion

In conditions of economic crisis there is an objective necessity in optimization of accounts

receivable with the purpose of acceleration of terms of its repayment. For this purpose it is

necessary to analyze constantly the state of accounts receivable to carry out the rational

policy concerning granting of loans and commodity credits. In practice of management of

accounts receivable the following stages of decision-making by an economic agent about

granting of commodity credits are distinguished: conditions of sale of production, rendering

of services and performance of works and tools of commercial credit are defined; credit

analysis of buyers is performed; decisions about granting of credit are made; mechanisms of return of funds are developed. Using this algorithm, internal controllers can assess the

main indicators of receivables, and heads of internal control services can carry out effective

planning of internal inspections.

Accounts payable management is inseparably connected with the analysis of accounts

receivable and accounts payable ratio. Management of payables and receivables implies the

establishment of contractual relations with suppliers and buyers, which ensure sufficient

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

16

and timely receipt of funds. This requires information that characterizes the real state of

payables and receivables and their turnover.

The level of accounts receivable and payable is influenced by external and internal

factors (Fig. 8)

Fig. 8. Factors influencing the level of receivables and payables.

The analysis of the factors considered allows us to conclude that internal factors are

relevant for the purposes of internal control, since they can not only be predicted, but also

their influence on the amount and state of debts can be regulated.

Acc

ou

nts

rec

eivab

le

Acco

un

ts pay

able

Ex

tern

al f

acto

r In

tern

al f

acto

rs

Ex

tern

al f

acto

r In

tern

al f

acto

r

Inflationary processes

Financial and credit policy of the state

Socio-economic situation in the country

Competition in the commodity and stock markets

Variety of products

Consumer demand

Political stability

Industry affiliation of the

enterprise

Scale of the enterprise

Assortment and production

volumes

Composition and structure of

company assets

Composition and structure of

company assets and sources

of their formation

Cash flow analysis and

planning

Credit policy with regard to

customers

Control system

Organization of supply and

procurement

Total purchases

Postpaid purchases

Terms of contracts with

payment counterparties

Terms of settlements with payment counterparties

Accounts payable management

policy

Quality of accounts payable

analysis

The settlement system adopted by the company

Industry specifics features

Tools influencing the balanced action of external and internal factors

1. Marketing policy; 2. Technical policy;

3. Investment policy; 4. Financial policy.

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

17

Besides it is necessary to note that some authors suggest to allocate the human factor as

one of the internal factors influencing size of accounts receivable and payable. The

personnel of the enterprise is the driving force, which activates assets, searches for

financing sources and influences the size and condition of accounts receivable and payable.

The most obvious influence of personnel on accounts receivable and payable can be traced

on such factor as organization of control system. An efficiently organized control system

makes it possible to timely identify the amount of accounts receivable and payable, the

facts of the formation of overdue debt and the reasons for them.

The issues of rating assessment of the reliability of debtors in order to make

management decisions regarding the provision of deferred payments for products sold,

work performed, services rendered are of particular relevance. Modern measures connected with stimulation of liquidation or partial repayment of

accounts receivable should be considered in accordance with developed credit policy,

which is based on credit rating of counterparts.

With an effectively designed credit policy regarding different groups of counterparties,

it is possible to effectively manage the emerging accounts receivable and improve the

financial condition of the enterprise. Carrying out the rating of debtors, it is possible to

carry out a comparative analysis of customers and to determine counterparties for which

there is a risk of non-repayment of debts.

The main purpose of credit rating is to provide the management of an economic entity

with information about the reliability of potential debtors.

In practice, economic services use various methods of scoring, which allow, by

analyzing the experience of interaction with the counterparty, to determine the degree of its reliability.

The reliability of the counterparty is evaluated on the basis of a system of key

indicators. We propose to assess the reliability of the customer to use the following

indicators: the time of joint work with the counterparty, the volume of transactions with the

counterparty in the total volume of business transactions, the term of repayment of accounts

receivable counterparty, prospective sales to the counterparty in the total volume of planned

sales, profitability of counterparty, the share of overdue debt of counterparty in total

overdue debts, the possibility of repayment of existing debts of counterparty, turnover ratio

of accounts receivable

Comprehensive assessment of credibility of debtors is based on the application of score-

rating assessment (Table 5).

Table 5. Rating assessment of counterparty reliability.

Assessment elements

Value levels

High (3

points)

Average

(2 points)

Low

(1 point)

1. Time of joint work with the counterparty. years

More 3 1-3 Less 1

2. Volume of transactions with the counterparty in the total volume of business transactions. %

More 20 10-20 Less 10

3. Term of repayment of accounts receivable by the counterparty. months

Until 1 1-3 More 3

4. Prospective volume of sales to the

counterparty in the total volume of planned sales. %

More 25 15-25 Less 15

5. Profitability of the counterparty. % More 50 25-50 Until 25

6. Share of overdue debt of the counterparty in the total amount of overdue debt. %

Less 10 10-20 More 20

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

18

7. Probability of repayment of existing debt by the counterparty. %

80-100 50-80 Less 50

8. Ratio of accounts receivable turnover 0.75-1 0.5-0.75 Less 0.5

24-20 - high degree of reliability of the counterparty

19-14 - medium degree of reliability of the counterparty

Less than 14 - low counterparty reliability

Based on the evaluation system, counterparties should be ranked according to the

following categories of reliability: high, medium and low reliability of the counterparty

(Table 6).

Table 6. Counterparties ranking by reliability categories.

Cou

nte

rpart

y

1 i

nd

icato

r

2 i

nd

icato

r

3 i

nd

icato

r

4 i

nd

icato

r

5 i

nd

icato

r

6 i

nd

icato

r

7 i

nd

icato

r

8 i

nd

icato

r

Tota

l

LLC «Kolos» 3 3 3 2 2 2 3 3 21

LLC «Lada» 1 1 2 2 1 2 2 2 13

LLC «Avangrad» 3 2 2 2 2 3 2 2 18

JSC «Lotos» 3 3 2 3 2 3 2 3 19

The proposed rating assessment of counterparties will allow for their comparative analysis and grouping, as well as to identify those of them, who have a high probability of

failure to repay the existing debt. The given technique can be widely used in development

of credit policy in order to decrease the amount of doubtful debts and in consequence

increase the efficiency of company`s activity.

4 Conclusions

Thus, the particularity of internal control of settlement transactions is due to the variety of

regulatory and informational support of the verification. The proposed methodological

support is based on a step-by-step verification of settlement transactions, which includes the

following main stages: planning of verification; implementation of control procedures;

registration of verification results. The proposed methodology identifies the areas of control, the regulatory framework and sources of information, the nature of verification and

control procedures that are necessary to achieve the objectives and practical solutions to the

objectives of the audit

In order to improve control procedures, working documents of internal control «Internal

Control Program of Settlement Transactions», «Verification of the existence of an

agreement with a separate counterparty», «Confirmation of the status of settlements with

counterparties» were developed in the course of the study. «Internal Control Program for

Settlement Transactions» is a detailed inspection instruction and quality control tool for the

work of the internal controller. The working document «Verification of the availability of

the agreement with a separate counterparty» can be used by the controller to identify errors

arising in the preparation of the contract, as well as to determine the completeness and timeliness of the parties to fulfill their obligations. With the help of the working document

«Confirmation of the status of settlements with counterparties» proposed in the course of

the study and when conducting the control procedure - inquiry to counterparties - it is

possible to identify cases of fraud and misstatement of data contained in the financial

statements.

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

19

In the course of the study, it was proposed in the process of internal control to carry out

a point-rating assessment of the reliability of debtors, based on the use of a system of key

indicators. The proposed rating assessment of counterparties will make it possible to carry

out their comparative analysis and grouping, as well as to identify those of them with a high

probability of non-repayment of existing debt. The presented methodology can be widely

used in the development of credit policy in order to reduce the amount of doubtful debts

and, as a consequence, increase the efficiency of the enterprise.

The implementation of the proposed recommendations in practical activities of the

control services of the enterprises will increase the efficiency of the control measures.

References

1. F. Casalin, G. Pang, S. Maioli, T. Cao, International Journal of Production Economics

193, 148-159 (2017) https://doi.org/10.1016/j.ijpe.2017.07.010

2. Q. Wang, J. Wu, N. Zhao, Q. Zhu, Resources, Conservation and Recycling 145, 78-85

(2019) https://doi.org/10.1016/j.resconrec.2019.02.024

3. H. Nam, K. Uchida, Journal of Banking & Finance 102, 116-137 (2019)

https://doi.org/10.1016/j.jbankfin.2019.03.010

4. A. Zakirova, G. Klychova, G. Ostaev, E. Zaugarova, A. Nigmetzyanov, E. Zaharova,

E3S Web of Conferences 164, 10009 (2020) https://doi.org/10.1051/e3sconf

/202016410009

5. V.N. Azarskov, L.S. Zhiteckii, K.Yu. Solovchuk et al, IFAC-Papers On Line 50,

10154-10159 (2017) https://doi.org/10.1016/j.ifacol.2017.08.1762

6. Dz. Faizrakhmanov, A. Zakirova, G. Klychova, A. Yusupova, A. Klychova, E3S Web

of Conferences 91, 06004 (2019) https://doi.org/10.1051/e3sconf/20199106004

7. A. Suhányiová, L. Suhányi, M. Mokrišová, J. Horváthová, Procedia Economics and

Finance 34, 311-318 (2015) https://doi.org/10.1016/S2212-5671(15)01635-4

8. M. Edmonds, T. Miller, A. Savage, Journal of Accounting Education 47, 75-92 (2019)

https://doi.org/10.1016/j.jaccedu.2019.04.001

9. R.P. Boisjoly, T.E. Conine, M.B. McDonald, Journal of Business Research 108, 1-8

(2020) https://doi.org/10.1016/j.jbusres.2019.09.025

10. W. Dbouk, L. Moussawi-Haidar, M.Y. Jaber, International Journal of Production

Economics 230, 107888 (2020) https://doi.org/10.1016/j.ijpe.2020.107888

11. G. Klychova, A. Zakirova, S. Alibekov et al, Advances in Intelligent Systems and

Computing 1258 AISC, 669–686 (2021) https://doi.org/10.1007/978-3-030-57450-

5_58

12. J. Enqvist, M. Graham, J. Nikkinen, Research in International Business and Finance

32, 36-49 (2014) https://doi.org/10.1016/j.ribaf.2014.03.005

13. T.-Sh. Wang, Y.-M. Lin, H. Chang, International Review of Economics & Finance 58,

312-329 (2018) https://doi.org/10.1016/j.iref.2018.04.003

14. J. Leontieva, E. Zaugarova, G. Klychova, A. Zakirova, A. Klychova, MATEC Web of

Conferences 170, 01087 (2018) doi.org/10.1051/matecconf/201817001087

15. G. Klychova, A. Zakirova, R. Mannapova, K. Pinina, Y. Ryazanova, E3S Web of

Conferences 110, 02075 (2019) doi.org/10.1051/e3sconf/201911002075

16. S.G. Mun, S. Jang, International Journal of Hospitality Management 48, 1-11 (2015)

DOI: 10.1016/j.ijhm.2015.04.003

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

20

17. P.G. Thacker, R.J. Witte, R. Menaker, Clinical Imaging. 64, 80-84 (2020)

https://doi.org/10.1016/j.clinimag.2020.03.015

18. A. Zakirova, G. Klychova, R. Nurieva, A. Nigmetzyanov, E. Zaugarova, U. Raheem,

Advances in Intelligent Systems and Computing 1259 AISC, 98–123 (2021)

https://doi.org/10.1007/978-3-030-57453-6_10

19. M. Roussy, Critical Perspectives on Accounting 24, 550-571 (2013)

https://doi.org/10.1016/j.cpa.2013.08.004

20. K. Chalmers, D. Hay, H. Khlif, Journal of Accounting Literature 42, 80-103 (2019)

https://doi.org/10.1016/j.acclit.2018.03.002

21. J. Wang, K. Hooper, Critical Perspectives on Accounting 49, 18-30 (2017)

https://doi.org/10.1016/j.cpa.2017.04.003

22. G.S. Klychova, A.R. Zakirova, E.R. Kamilova, International Business Management 10,

5254-5260 (2016) DOI: 10.3923/ibm.2016.5254.5260

23. M. Hanskamp-Sebregts, P.B. Robben, H. Wollersheim, M. Zegers, Health Policy 124,

216-223 (2020) https://doi.org/10.1016/j.healthpol.2019.11.013

24. A. Klychova, G. Klychova, A. Zakirova, R. Sungatullina, K. Mukhamedzyanov, E.

Philippova, E3S Web of Conferences 110, 02072 (2019) doi.org/10.1051/e3sconf/201911002072

25. Y.-T. Chang, H. Chen, R.K. Cheng, W. Chi, Journal of Contemporary Accounting &

Economics 15, 1-19 (2019) https://doi.org/10.1016/j.jcae.2018.11.002

26. Y. Li, X. Li, E. Xiang, H.G. Djajadikerta, Journal of Contemporary Accounting &

Economics 16, 100210 (2020) https://doi.org/10.1016/j.jcae.2020.100210

27. Sh.-I. Chang, L.-M. Chang, J.-C. Liao, Information & Management 57, 103335 (2020)

https://doi.org/10.1016/j.im.2020.103335

28. D.B. Bryan, Advances in Accounting 36, 11-26 (2017)

https://doi.org/10.1016/j.adiac.2016.09.005

29. E. Demirakos, The International Journal of Accounting 53, 253-254 (2018)

https://doi.org/10.1016/j.intacc.2018.07.001

30. Schantl, S.F., Wagenhofer, A. Journal of Accounting and Public Policy 1, 106803

(2020) https://doi.org/10.1016/j.jaccpubpol.2020.106803

31. X.-D., Ji, W. Lu, W. Qu, Journal of Contemporary Accounting & Economics 14, 266-

287 (2018) https://doi.org/10.1016/j.jcae.2018.07.002

32. W. Shu, Y. Chen, B. Lin, Y. Chen, China Journal of Accounting Research 11, 407-427

(2018) https://doi.org/10.1016/j.cjar.2018.09.002

33. H. Li, J. Dai, T. Gershberg, M.A. Vasarhely, International Journal of Accounting

Information Systems 28, 59-76 (2018) https://doi.org/10.1016/j.accinf.2017.12.005

E3S Web of Conferences 258, 12009 (2021)

UESF-2021https://doi.org/10.1051/e3sconf/202125812009

21