international business plan - royal bank of canada

TRANSCRIPT

FITT: International Business Management Royal Bank Of Canada

FITT ID 306549

1 | P a g e

Executive Summary

2 | P a g e

Executive Summary

Royal Bank of Canada is one of the oldest and largest banks in Canada. Its operations are mostly

restricted towards North America and the Caribbean Islands. RBC is a very conservative

financial institution. It stood strong during the subprime crisis in the USA. In 2012 it has been

rated as the safest bank by Moody’s.

South Africa provides huge potential for growth. It is one of the largest economies of Africa and

has grown at a GDP rate of 7% over past 5 years. Most of the world has taken notice of the

potential that South Africa holds and many firms have, especially the automobile sector has set

its operations there.

RBC will be able to maximize its profits and increase its market share if it moves in to South

Africa. It will also be able to use South Africa as a test market to explore other African markets.

Taking into consideration the long term objectives of RBC I recommend moving in to South Africa through acquisition strategy

Corporate Profile

3 | P a g e

COMPANY PROFILE

Royal Bank of Canada (RBC) is a public limited company providing financial services for over a

century. It was founded in 1864 in Halifax, Nova Scotia as Merchant’s Bank of Halifax. In 1901

it changed its name to Royal Bank of Canada and currently all its subsidiaries across the globe

operate under the name ‘RBC’. It currently operates in 20 countries across North America, South

America and the Caribbean Islands. In 2008 it established a representative office in India. It is

listed on the Toronto Stock Exchange (TSE) and New York Stock Exchange (NYSE). It is one of

the largest banks in the world based on market capitalization. Bloomberg Markets magazine in

2013 named RBC as the second strongest bank in North America and the fourth strongest bank

in the world. This global ranking confirms RBC’s financial strength and stability not only in the

domestic market but also in the international market.

VISION

Strive to earn the right to be the customer’s first choice for all their financial needs.

MISSION

To be a top performing diversified financial institution in the emerging markets of the world by

2025.

STRATEGIC GOALS

ϒ To be a dominant leader in providing financial services in the domestic market.

ϒ To be the leading provider of commercial banking services and wealth management

solutions globally.

ϒ To be best in class provider of trade and finance services in select target markets

CORPORATE VALUES

ϒ Excellent services to the internal and external stakeholders.

ϒ Emphasis on team work for success.

ϒ Diversity is the key pillar for growth and innovation.

ϒ Conduct business with trust and integrity.

4 | P a g e

ϒ Responsible corporate citizen of the globe.

ϒ Foster a sustainable business environment.

ϒ Growth fuelled by the growth of the society.

BUSINESS VERTICALS

RBC has come a long way from the traditional banking services it provided decades ago.

Keeping in view its long term objectives RBC’s businesses are broadly classified in five

segments.

Personal and Commercial Banking

Under this segment RBC provides host of savings accounts, chequing accounts, credit and loans,

investments and international trade solutions services for the individuals and the corporates both.

Wealth Management

It serves affluent, high net worth and ultrahigh net worth customers with tailor made investment,

trust and other wealth management products and services.

Investor and Treasury Services

RBC serves the institutional investors by providing them custodial, advisory and financing

services. It also assists them in managing their risks by safeguarding their assets and maximizing

liquidity.

Capital Markets

It provides market research services pertaining to investment banking and trading of stocks to

public and private companies, institutional investors, central banks and governments.

Insurance

RBC provides a wide range of insurance products for travel, life, health, home and auto for

individuals. It also provides insurance to safeguard the businesses. It provides insurance facility

through its operating entities.

5 | P a g e

KEY MILESTONES

ϒ RBC was the first Canadian bank to offer online banking services in Canada in 1995.

ϒ RBC was awarded the “Best Bank” in Canada by The Banker (banking magazine) in

2007.

ϒ RBC re-acquired majority stake in Royal Bank of Trinidad and Tobago.

ϒ Macleans magazine named RBC as one of Canada’s “Top 50 Most Socially Responsible

Corporations” in 2013.

ϒ RBC recognized as a leader in retail banking at the Retail Banker International Awards in

2013.

6 | P a g e

Management and Human Resource

7 | P a g e

ORGANIZATION STRUCTURE

CHAIRMAN OF THE BOARD DAVID O’BRIEN

BOARD OF DIRECTORS

* JACQUES LAMARRE

* BRANDT LOUIE

* KATHLEEN TAYLOR

* MICHAEL McCAIN

* TIMOTHY HEARN

* ALICE LABERGE

* GEOFFREY BEATTIE

* VICTOR YOUNG

* RICHARD GEORGE

* BRIDGET VAN KRALINGEN

* DAVID DENISON

* EDWARD SONSHINE

* HEATHER MUNROE-BLUM

* PAULIE GAUTHIER

PRESIDENT & CEO GORDON NIXON

CFO & ADMIN

JANICE FUKAKUSA

RISK MGMT

CHIEF RISK OFFICER

MORTEN FRIIS

CAPITAL MARKETS CO-GROUP HEAD

MARK STANDISH

HEAD OF HUMAN

RESOURCE

ZABEEN HIRJI

WEALTH MGMT GROUP HEAD

GEORGE LEWIS

US INVESTMENT BANKING HEAD BLAIR FLEMING

CANADIAN BANKING

GROUP HEAD DAVE McKAY

INTERNATIONAL BANKING & INSURANCE

GROUP HEAD JAMES

WESTLAKE

8 | P a g e

LEADERSHIP TEAM

The thinking tank of the bank is fuelled by prudent bankers who have illustrious years of

experience. The leadership team has served the bank in various verticals in different capacities.

President and CEO

Gordon Nixon was appointed as the President and CEO of RBC on April 1, 2001. He has been a

transformational leader, having said so in 2004; he initiated a major change in the organization

structure and management. The restructuring process was undertaken to focus the resources of

RBC towards only one goal i.e. customer satisfaction. The change was symbolically called as

“Client First”. Under the leadership of Mr. Nixon RBC has delivered one of the best shareholder

returns amongst the big five banks of Canada. RBC was able to cruise through the financial crisis

of 2000 because of Mr. Nixon’s unconventional approach towards banking. Mr. Nixon was

awarded the Order of Ontario in 2007. He was also appointed a Member of the Order of Canada

in 2010.

Chief Financial Officer and Chief Administrative Officer

Janice Fukakusa is the CFO and CAO of RBC. She is one of the key members of RBC’s Group

Fukakusa has held key positions in all the businesses of the bank since joining them in 1985. Ms.

Fukakusa has earned the designation of FCA from the Institute of Chartered Accountants of

Ontario and holds a MBA from Schulich School of Buisness.

Group Head International Banking and Insurance

W. James Westlake is the Group Head for RBC’s international banking and insurance initiatives.

Mr. Westlake is responsible for setting the strategic direction for global expansions. He was

previously working with the Metropolitan Life Insurance Company for 19 years, before joining

RBC in 1995.

Risk Management

Mr. Friis was appointed as the Chief Risk Officer in 2004. Mr. Friis is responsible for taking

strategic decisions for mitigating and managing the risks. He has served the bank for more than

9 | P a g e

30 years and has been a motivational leader. Mr.Friis holds an MBA from the Harvard School of

Business.

HUMAN RESOURCES REQUIREMENT FOR SETTING BUSINESS IN NEW TARGET

MARKET

ϒ Research Analysts

ϒ Legal Advisors

ϒ Mergers and Acquisition specialist

ϒ Regional Head

ϒ Underwriters

ϒ Public Relations Personnel

ϒ Product Engineering Specialist

ϒ Marketing and Sales Manager

ϒ Trainers

10 | P a g e

Target Market Environmental Scan

11 | P a g e

SUB-SAHARAN MARKET

Africa’s economic growth has accelerated over the last five years. The robust growth has

attracted attention of global executives and investors as the rate of return on foreign investment

is higher in Africa than in any other developing regions. The major drivers of the African

economy have been countries like South Africa, Nigeria and Ghana, which have contributed

approximately 70% to the real GDP of the continent. The growth figures of the three African

countries put together are higher than their Asian counterparts (India & China).

TARGET MARKET: SOUTH AFRICA

Business Destination

South Africa is referred as the business gateway of Africa. The government policies and the

infrastructure complemented by the consumer spending have made South Africa a quintessential

business hub. The economy is driven through significant contribution made by the mining,

services and manufacturing sector. The services sector contributes approximately 60% to its

GDP, followed by mining and manufacturing at 20% and 15% respectively. Banking and

Financial Sector is the seventh most important sector (see Appendix A) which contributes 4.9%

to its GDP and has grown at an average rate of 3.1% per annum. Since South Africa is a

developing economy the exposure of the Banking and Financial sector towards the GDP shows

ample scope of growth.

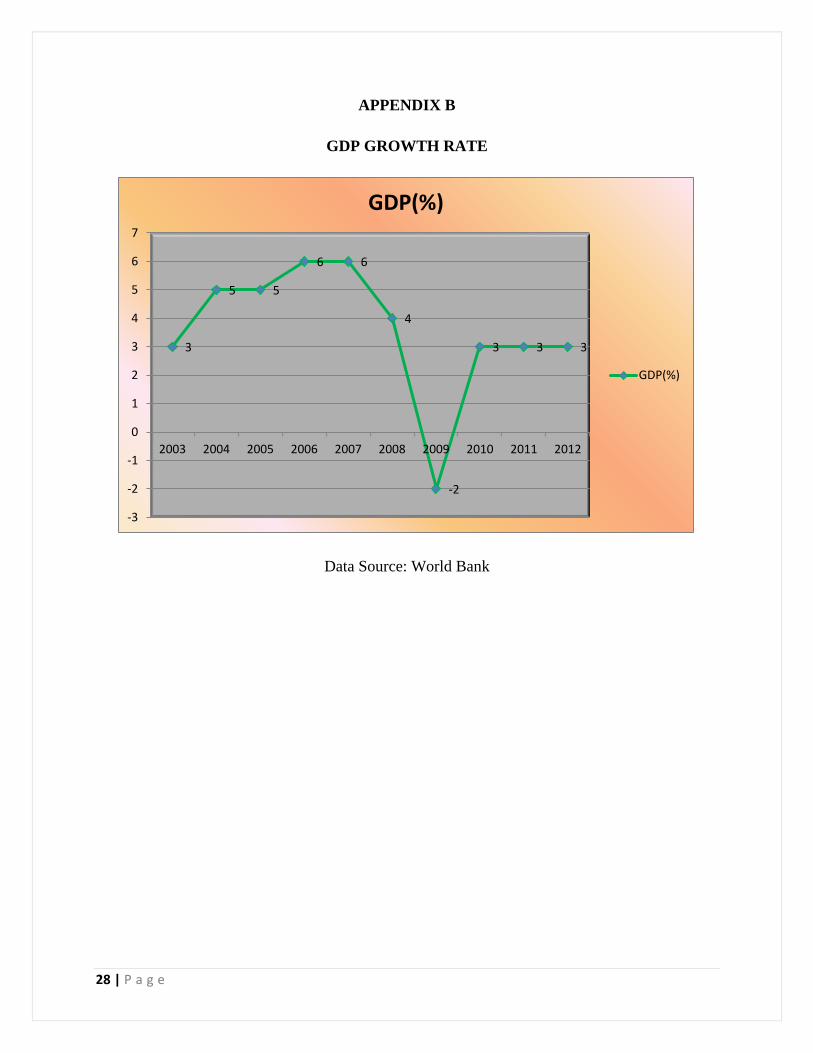

Economic Outlook

South Africa is quoted as the economic giant of the sub-Saharan economy. Over the last decade

South African economy has consistently grown at an average GDP of 3.6 % (see Appendix B).

The average projected growth rate (GDP) over the next five years is 4.1% (see Appendix C).

South Africa has managed to maintain its inflation at 5.6% in 2012 and as the forecasted data

suggests the Central Bank of South Africa will maintain the inflation around the 5% mark for the

next five years (see Appendix D). The maintenance of inflation just below the upper inflation

band of 6% portrays healthy signs for the economy as it promotes consumer spending driven

economy.

12 | P a g e

Political Scenario

Post-apartheid the political situation in South Africa has stabilized and consolidated. South

Africa has a multi-party democratic system. The coalition government is led by President Jacob

Zuma of African National Congress (ANC) party. ANC’s economic resources and liberation

credentials make it difficult for the opposition parties to break into electoral politics. President

Jacob Zuma was under pressure recently to declare a populous budget which would have

increased government’s expenditure; however his party choose to announce a budget which

promotes business and trade in South Africa. The current political leadership is favourable for

the corporates and people both. The reform work undertaken by the current leadership for the

people has made them popular and the chances of President Jacob Zuma being re-elected in 2014

elections is bright.

Business Infrastructure

South Africa has one of the best business environments in the African region. International

Finance Corporation has awarded 53rd rank to South Africa amongst 185 countries in the overall

ease of doing business rankings. South Africa is very well connected to all the major domestic

cities through road and rail. The fixed land line and mobile connectivity is dense within South

Africa. The broadband subscription has significantly in South Africa over the last three years;

however it still remains expensive as compared to other developing economies. The government

in April 2013 had called for new internet service providers to bid for licence in order to tackle

expensive internet issue.

Legal Framework

South Africa was formerly a British colony; hence it has adopted the British legal system. The

judiciary system has been effective in resolving disputes and enforcing contracts. Intellectual

Property Rights law, labour and key commerce legislations are well-developed. South Africa is a

member of WTO and has signed the TRIPS agreement for protection of intellectual property

rights. Hence any disputes related to intellectual property is reported and resolved in the

international forum.

13 | P a g e

Foreign Investment Policy and Corporate Tax Structure

South Africa`s monetary policies are structured to attract foreign direct investment. 100%

foreign ownership is permitted in South Africa and the capital repatriation policies are liberal.

No prior approval is required from the government for foreign investment. The South African

Companies Act of 1973 provides guidelines for setting up foreign companies in South Africa.

South Africa`s tax regime is foreign investor friendly. If the foreign investments are routed

through the Strategic Industrial Project (SIP) allowances of 50% or 100% are available. The tax

rate for foreign companies is 34%.

14 | P a g e

Market Entry and Marketing Strategy

15 | P a g e

Market Entry Strategy

Royal Bank of Canada will be offering trade and finance products to the small and medium

domestic and international traders. I recommend RBC to enter the South African market by

acquiring a non-banking financial institution (NBFI). RBC will be able to provide trade and

finance services under the South African law, by holding a non-banking licence.

Rationale for the Proposed Strategy

ϒ South Africa allows 100% foreign direct investment which does not require prior

approval from the government.

ϒ Local presence in the South African market will increase consumer confidence, thereby

attracting more business.

ϒ Through this strategy RBC will get access to the large customer base of the acquired

company.

ϒ RBC will also get access to the immovable assets of the acquired company.

ϒ The trained pool of human resource of the acquired company will enable RBC to save on

the recruitment and training cost.

Marketing Strategy

RBC structures its marketing strategy keeping in view that the customer is the king of the

market. RBC understands that building long term relationship with the customer through prompt

and quality service is valuable and rewarding. The major difference between the marketing

strategy adopted by RBC and its competitors is that RBC concentrates on creating value for the

customer, whereas the competition merely focuses in selling the service.

Product

RBC has engineered the products keeping in view the business requirements of its consumers.

The trade finance products offered are stated as under:-

16 | P a g e

ϒ Pre-Shipment Credit

This product will enable the exporters to meet their working capital requirements from

the date of manufacturing the product till the shipping of the product. The loan will be

provided for a maximum period of 180 days at prime lending rate.

ϒ Post-Shipment Credit

The pre-shipment credit can be converted to post shipment credit for a maximum period

of 270 days at prime lending rate plus 1%. This loan will allow the exporter to meet their

operating expenses from the date of shipment till they receive their payment.

ϒ Letter of Credit

Import and export letter of credit will be provided to the customer at a fixed fee which

will be 0.5% of the letter of credit amount. The consumer will be able to route the

documents, receive or make payment and get the document scrutinized under the letter of

credit.

ϒ Documentary Collection

This product will enable routing of payment and documents through the bank to the

foreign bank or to the foreign trader. The fee charged for this service is US$ 5 per

transaction.

Product Modification

• The interest rate at which credit will be extended to the market will be decided by the

benchmark interest rate set by the Central Bank of South Africa.

• The maximum credit period that can be given to the customer will be governed by the

policies set by the Central Bank of South Africa.

Product Differentiation

• The trade products provided to the customer will be similar in nature to the competition;

however the main differentiating factor is the quality of service provided to the customer.

17 | P a g e

RBC is reputed in the North American market for the prompt and efficient customer

service provided to the customer.

• The trade products will be made available to the customer through online internet

banking, this a special feature of RBC`s trade products. The competition in South Africa

has not yet started offering trade products online.

Price

RBC will deploy value added pricing in the South African market. The customer will be given

the option of paying extra for the value added services availed. The competition currently uses

static pricing method. The value added pricing will be expensive than the competition, however

the customer takes a call for what services he wants to pay. The pay as per your use is the value

statement supporting this pricing strategy.

RBC uses full cost pricing method in order to arrive at the cost of the product. All the direct and

indirect costs and variable and fixed costs are taken into consideration from conceptualizing step

to finally making the product available to the customer. This enables RBC to fully recover the

cost and add its profit margin for the selling price.

Place

Documentary Collection (Import Documents)

The documents received from the overseas party is informed to the customer over a phone call

by the trade desk officer, then depending on the terms of payment stated on the bill of exchange

the documents are handed over to the customer via local courier service or the customer receives

it when he visits the branch.

Letter of Credit (Export LC)

If an export LC is received from the foreign bank, the same is informed by the trade desk officer

over a phone call and simultaneously a soft copy of LC is emailed to the customer with a hard

copy through the local courier services.

18 | P a g e

Online Trade Customers

The internet service must be of high speed in order to facilitate quality service to the online trade

customers.

Promotion

Print Media must be used to in order to promote RBC`s entry in the South African market. A

dinner night for the existing customers of the company acquired by RBC must be arranged, to

promote its products. The dinner invite must state that the existing customers are allowed to get

their business friends as well. This will enable promoting the bank to new prospective customer.

The promotion activity may be outsourced to an advertisement company specialized in arranging

advertisement campaign for companies dealing in financial and trade services.

People

Durban and Cape Town are the port towns of South Africa. The import export trade takes place

though these ports, hence many import export companies are set across this region. RBC is

targeting these customers for its trade and finance services. The South Africa`s trade and finance

market is valued at USD 1.2 billion as quoted by Trade Finance Magazine in 2013.

After Sales Service

The relationship management team of the bank provides after sales service to the customer. In

the banking industry after sales service is more like cross selling a different banking product at

reduced price to the customer for their loyalty. The loyalty benefits will be provided to the

customer till the time it is actively using the banking services.

19 | P a g e

Operations Overview

20 | P a g e

Operations Overview

Software

• Society for Worldwide Interbank Financial Telecommunication(SWIFT)

It is a platform used by all the banks across the globe for communication and transferring

of funds.

• Nostro A/c

It is a dollar a/c maintained by a South African with an American bank.

• Vostro A/c

It is a South African Rand (currency) A/c maintained by a foreign bank with a bank

operating in South Africa

Each and every trade finance products has its unique process. It goes through various check

points where in the documents are first scrutinized to see whether it meets the international trade

rules and then it is compared with the rules of the customers. If the documents comply with both

international and local rules and regulations, the document is cleared for payment by the

importer.

Sample Working of a Letter of Credit (LC) (see Appendix E)

• The importer (applicant) visits his bank (issuing bank) for the issuance of letter of credit

based on the order confirmation received from the exporter (beneficiary).

• The issuing bank issues the LC in favour of the beneficiary and sends the LC to the

exporter’s bank (negotiating bank) via the SWIFT system.

• The negotiating bank informs the beneficiary regarding the receipt of LC.

• The beneficiary ships the goods and sends the documents via negotiating bank to the

issuing bank

21 | P a g e

• The issuing bank scrutinizes the documents to comply with the terms and conditions of

the LC and informs the applicant about receiving of documents

• The applicant agrees to release the documents on immediate payment; concurrently

issuing bank agrees to make the payment to the negotiating bank on behalf of the

applicant.

• The payment is effected by the issuing bank to the negotiating bank via SWIFT.

• The negotiating bank pays the beneficiary by crediting his a/c and deducting the charges

for the entire transaction.

22 | P a g e

Financial Risk and Management Strategy

23 | P a g e

Financial Performance

RBC posted strong results for the second quarter ended 30th April 2013. Its net income increased

by 26% from the first quarter. Its current net income stands at CAD 1,936 million. The stock

price of RBC on the Toronto Stock Exchange is CAD 65.11 as on 29th July 2013. RBC has been

posting good results for the past five years (see Appendix E,F & G). The earnings per share is

CAD 5.40. The stock prices have gone up steadily since July 2012 when it was trading at CAD

50.50

Sourcing of Funds for Acquisition in South Africa

RBC could raise funds in the following way:

• 30% of the capital can be raised through follow up public offer (FPO)

• 30% of the capital can be invested from its profits. As of 2012 its cash flow showed a

balance of CAD 1,239 million

• 10% can be raised through issue of preferential shares

• 20% can be raised through providing a stake to the Non-banking financial institution that

the bank is acquiring in South Africa.

Risks Associated with the Acquisition

• The government may come up with the policy which may make the deal impossible. In

such scenario political risk insurance can be availed from EDC.

• Currency Fluctuation risk may make the deal expensive for RBC. This risk can be

mitigated by hedging the funds.

24 | P a g e

Conclusion and Recommendations

25 | P a g e

CONCLUSION

RBC is one of the largest banks of Canada. Since the 1900’s the Canadian banks have

concentrated on the North American and the Caribbean markets only. The emerging economies

like South Africa, Brazil, India, Thailand and Russia are prospective markets for financial

institutions. The financial system in the emerging economies is evolving and there is a need for

financial enterprises to boost their growth through structured financing.

South Africa is one of the largest economies of Africa; it will also provide RBC an opportunity

to enter other emerging African economies like Nigeria and Ghana. RBC could use South Africa

as a test market to enter the neighbouring African countries.

The major risk involved in South Africa is the political risk. President Zuma has led a campaign

to empower the Black community, which has not been viewed very positively by the gatekeepers

of the world. The regional politics is detrimental to the growth of South Africa. However these

problems are common with most of the emerging world.

Recommendation

I suggest RBC to undertake a detailed research of the competition in the South African market. A

detailed research will assist RBC to understand the driving force of the financial sector. The

report will also flash data about the weak financial institutions, which RBC can decide to acquire

in order to enter the South African market.

26 | P a g e

Appendices:

27 | P a g e

APPENDIX A

TOP 10 SECTORS OF SOUTH AFRICA

2012 Level

(Billion. US$)

2013 Percent Change

(Real Terms)

Percent Share of

GDP

(Nominal Terms)

1. Public Admin. &

Defence

57.6 3.0 16.5

2. Retail Trade-Total 33.2 2.1 9.5

3. Mining 25.2 3.8 7.2

4. Real Estate 21.0 2.7 6.0

5. Wholesale Trade 18.5 3.1 5.3

6. Land Transport 18.1 1.8 5.2

7. Banking &

Finance

17.1 3.1 4.9

8. Construction 13.6 5.0 3.9

9. Business Services 12.9 3.1 3.7

10. Agriculture 9.0 0.6 2.6

Total 226.0 64.8

Data Source: World Industry Service, IHS Global Insight Inc.

28 | P a g e

APPENDIX B

GDP GROWTH RATE

Data Source: World Bank

3

5 5

6 6

4

-2

3 3 3

-3

-2

-1

0

1

2

3

4

5

6

7

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

GDP(%)

GDP(%)

29 | P a g e

APPENDIX C

FORCASTED GDP

Data Source: IHS Global Insight Inc.

2.9

3.5 4

4.9 5.2

0

1

2

3

4

5

6

2013 2014 2015 2016 2017

GDP(%)

GDP(%)

30 | P a g e

APPENDIX D

INFLATION RATE

Data Source: IHS Global Insight Inc.

0

1

2

3

4

5

6

7

8

9

2010 2011 2012 2013 2014 2015 2016 2017

Consumer Price Index (%change)

Wholesale Price Index (%change)

31 | P a g e

APPENDIX E

Process Flow of Letter of Credit

Data Source: Bank of China (New York)

32 | P a g e

APPENDIX E

Balance Sheet for Five Years

2012 2011 2010 2009 2008

Cash and Due from Banks 12,617 12,428 8,440 8,353 11,086

Fed Funds Sold/Securities Purchased

112,257 84,947 72,698 41,580 44,818

Interest-Bearing Dep at Other Banks 10,255 6,460 13,254 8,923 20,041

Investment Securities, Net 40,828 39,214 38,594 46,210 48,626

Net Loans 378,244 347,530 273,006 280,963 289,540

Premise and Equipment 2,691 2,490 2,139 2,367 2,471

Due from Customers Acceptance - 7,689 7,371 9,024 11,285

Trading Account Securities 120,783 128,128 144,925 140,062 122,508

Other Receivables - - - - -

Accrued Interest - - - - -

Deferred Acquisition Cost - - - - -

Accrued Investment Income - - - - -

33 | P a g e

Separate Account Business Liability - - - - -

Time Deposit Placed - - - - -

Intangible Assets 15,585 9,725 8,370 10,401 12,019

Other Assets 214,202 155,222 157,409 107,106 161,465

Total Assets 825,100 793,833 726,206 654,989 723,859

Liabilities [+] in Millions of Dollars

Oct-12 Oct-11 Oct-10 Oct-09 Oct-08

Non-Interest Bearing Deposits - - - - 43,724

Interesting Bearing Deposits 508,219 479,102 414,561 398,304 394,851

Short Term Debt 40,756 44,284 46,597 41,359 5,402

Other Liabilities 59,960 169,811 162,309 116,792 144,688

Bankers Acceptance Outstanding - 7,689 7,371 9,024 11,285

Fed. Funds Purchased/Securities Sold

64,032 42,735 41,207 35,150 59,560

Accrued Taxes - - - - 2,468

Accrued Interest Payables - - - - 2,925

Other Payables - - - - 10,311

34 | P a g e

Capital Lease Obligations - - - - -

Claims and Claim Expense - - 6,273 8,922 7,385

Future Policy Benefits - - - - -

Unearned Premiums - - - - -

Policy Holder Funds - - - - -

Participating Policyholder Equity - - - - -

Separate Accounts Business - - - - -

Minority Interest 1,761 1,761 2,256 2,071 2,371

Long Term Debt 7,615 8,749 6,681 6,461 8,131

Total Liabilities 780,833 754,131 687,255 618,083 693,101

Preferred Shareholder's Equity 4,813 4,813 4,813 4,813 2,663

Common Shareholder's Equity 39,454 34,889 34,138 32,093 28,095

Total Equities 44,267 39,702 38,951 36,906 30,758

Data Source: TMX Money

35 | P a g e

APPENDIX F

INCOME STATEMENT OF FIVE YEARS

Income [+] 2 3 4 5 Oct-12 Oct-11 Oct-10 Oct-09 Oct-08

Total Interest Income 20,852 20,813 17,746 20,578 25,344

Total Interest Expense -8,354 -9,456 -7,408 -9,037 -15,984

Net Interest Income 12,498 11,357 10,338 11,541 9,360

Loan Loss Provision -1,301 -1,133 -1,240 -3,413 -1,595

Net Interest Income After Loan Loss Provision

11,197 10,224 9,098 8,128 7,765

Non-Interest Income 14,834 16,281 15,744 17,565 12,222

Non-Interest Expense 8,354 -17,525 -17,015 -21,167 -13,982

Special Income/Charges -1,442 - - 1,000 -

Net Income Before Taxes 32,943 8,980 7,827 5,526 6,005

Premium Tax (Credit) - - - - -

Minority Interest 97 -101 -99 -100 -81

Income Taxes -2,100 -2,010 -1,996 -1,568 -1,369

36 | P a g e

Net Income from Continuing Operations

7,590 6,970 5,831 3,858 4,555

Net Income from Discontinued Operations

-51 -526 -509 - -

Net Income from Total Operations

7,539 6,444 5,322 3,858 4,555

Extraordinary Income/Loss - - - - -

Income from Cum. Effect of Acct Change

- - - - -

Income from Tax Loss Carryforward

- - - - -

Other Gains - - - - -

Total Net Income 7,442 6,343 5,223 3,858 4,555

Results [+] in Dollars

(Preferred Dividends in

Millions) Oct-12 Oct-11 Oct-10 Oct-09 Oct-08

Dividends Paid Per Share 2.28 2.08 2 2 2

Preferred Dividends - - 258 233 101

37 | P a g e

Basic EPS from Continuing Operations

5.01 4.62 3.85 2.59 3.41

Basic EPS from Discontinued Operations

-0.03 -0.37 -0.36 0 0

Basic EPS from Total Operations

4.98 4.25 3.49 2.59 3.41

Basic EPS from Extraordinary Inc

0 0 0 0 0

Basic EPS from Cum. Effect of Acct Chg

0 0 0 0 0

Basic EPS from Tax Loss Carryforward

- 15,236 12,494 13,539 14,983

Basic EPS from Other Gains(Loss)

0 0 0 0 0

Basic EPS, Total 4.98 4.25 3.49 2.59 3.41

Basic Normalized Net Income/Share

5.96 4.62 3.85 1.92 3.41

Diluted EPS from Continuing Operations

4.93 4.55 3.82 2.57 3.38

38 | P a g e

Diluted EPS from Discontinued Operations

-0.03 -0.36 -0.36 0 0

Diluted EPS from Total Operations

4.93 4.19 3.46 2.57 3.38

Diluted EPS from Extraordinary Inc

0 0 0 0 0

Diluted EPS from Cum. Effect of Acct Chg

0 0 0 0 0

Diluted EPS from Tax Loss Carryforward

0 0 0 0 0

Diluted EPS from Other Gains(Loss)

0 0 0 0 0

Diluted EPS, Total 4.93 4.19 3.46 2.57 3.38

Diluted Normalized Net Income/Share

5.9 4.55 3.82 1.9 3.38

Data Source: TMX Money

39 | P a g e

APPENDIX G

CASH FLOW FOR FIVE YEARS

6 2 3 4 5

Cash Flow in

Millions of

Dollars

Oct-12 Oct-11 Oct-10 Oct-09 Oct-08

Net Income 7,539 6,444 5,732 3,858 4,555

Provision for Loan Loss 1,418 1,133 1,240 3,413 1,595

Depreciation and Amortization

1,153 958 821 1,851 674

Deferred Income Taxes

123 -124 119 -97 -455

Change in Assets (Receivables)

599 28,942 -1,542 47,894 -44,514

Change in Liabilities (Payables)

21,842 -7,609 -4,376 -52,298 56,787

Investment Securities Gain

-203 -293 -235 -17 1

Net Policy Acquisition Cost

- - - - -

Realized Investment Gains

- 106 2 5 -220

Net Premiums Receivables

- - - - -

Change in Income Taxes

-826 807 -1,748 3,546 -2,705

40 | P a g e

Other Non-Cash Items 1,473 -25,885 11,160 -752 -4,286

Net Cash from Operating Activities

-2,074 4,479 11,173 7,403 11,432

Proceeds from Sale/Mat. Inv.

58,525 53,610 48,178 63,529 23,689

Purchase of Investment Securities

-55,690 -46,877 -34,590 -32,268 -24,864

Net Increase Fed. Funds Sold

- - -31,118 3,238 19,650

Purchase of Property & Equipment

-1,351 -1,452 -960 -700 -1,265

Acquisitions -853 -1,300 -82 -27 -974

Other Investment Changes, Net

N/A 1,221 -33,002 -17,854 -60,889

Net Cash from Investing Activities

3,765 5,202 -51,574 15,918 -44,653

Net Change in Deposits - - 36,104 -40,742 61,271

Cash Dividends paid

-3,364 -3,125 -3,027 -2,748 -2,688

Repayment of Long Term Debt

-1,006 -404 -1,305 -1,659 -500

41 | P a g e

Change in Short Term Debt

21 -615 12,181 14,982 -21,746

Issuance of Long term Debt

- 1,500 1,500 - 2,000

Issuance of Preferred Stock

- - - 2,150 313

Issuance of Common Stock

5,410 6,323 7,068 2,511 223

Purchase of Treasury Stock

-5,261 -6,080 -6,929 -60 -131

Other Financing Activities

N/A -750 -4,167 -217 456

Cash from Financing Activities

-4,200 -3,151 41,425 -25,783 39,198

Effect of Exchange Rate Changes

-18 76 -168 -271 883

Net Change in Cash & Equivalents

-2,509 6,606 856 -2,733 6,860

Cash at Beginning of Period

15,144 8,538 7,584 11,086 4,226

Cash at End of Period 12,617 15,144 9,330 8,353 11,086

Total Risk-Based Capital Ratio

0.15 0 0 0 11.1

Data Source: TMX Money

42 | P a g e

References

43 | P a g e

References

Country Intelligence. (n.d.). IHS Home Page. Retrieved July 24, 2013, from

http://www.ihs.com/products/global-insight/country-analysis/index.aspx

The World Bank DataBank | Explore . Create . Share. (n.d.). The World Bank

DataBank | Explore . Create . Share. Retrieved July 24, 2013, from

http://databank.worldbank.org/data/views/reports/tableview.aspx#

Six months in South African politics — in 2013 | Politics Blog | BDlive

. (n.d.). Home | BDlive

. Retrieved July 24, 2013, from

http://www.bdlive.co.za/blogs/politics/2012/08/29/six-months-in-south-african-politics--

in-2013

Freeland, C. (n.d.). | Analysis & Opinion | Reuters.com. Analysis & Opinion | Reuters. Retrieved

July 24, 2013, from http://blogs.reuters.com/chrystia-freeland/2012/10/19/africa-the-

next-economic-tiger/

Leke, A., Lund, S., Roxburgh, C., & Wamelen, A. V. (n.d.). What’s driving

Africa’s growth | McKinsey & Company. McKinsey & Company | Home Page.

Retrieved July 24, 2013, from

http://www.mckinsey.com/insights/economic_studies/whats_driving_africas_growth

OMD South Africa. (n.d.). OMD South Africa. Retrieved July 24, 2013, from

http://www.omd.co.za

(2013). South Africa Country Monitor. Country Intelligence, 1, 1-25.

South Africa, 2012: A survey that explains a lot | Daily Maverick. (n.d.). Home | Daily Maverick.

Retrieved July 24, 2013, from http://www.dailymaverick.co.za/article/2012-01-24-south-

africa-2012-a-survey-that-explains-a-lot/#.Ue_JJ421H4Z

44 | P a g e

South Africa’s political situation | Green Passport. (n.d.). Südafrika hautnah erleben..

Retrieved July 24, 2013, from http://www.greenpassport.co.za/en/south-africa/south-

africa%E2%80%99s-political-situation/

World Wide Worx - Business Technology Research South Africa. (n.d.). World Wide Worx -

Business Technology Research South Africa. Retrieved July 24, 2013, from

http://www.worldwideworx.com APA formatting by BibMe.org.