international financial reporting and analysis, 5th edition david alexander, anne britton and ann...

TRANSCRIPT

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Part two

Annual Financial Statements

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Fixed assets versus current assets

Definition

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Current assets – definition (IAS 1)

• An asset shall be classified as current when:

– It expects to realise the asset, or intends to sell or consume it, in its normal operating cycle;

– It holds the asset primarily for the purpose of trading;

– It expects to realise the asset within twelve months after the reporting period;

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Current assets – definition (IAS 1) (cont’d)

– The asset is cash or a cash equivalent (as defined in IAS 7) unless the asset is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period

• An entity shall classify all other assets as non-current (IAS 1 – par 66)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Non-current assets

• Non- current assets are defined by IAS as those assets which are not current assets

• IAS 1 uses the term “non-current” to include tangible, intangible and financial assets of a long-term nature

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Assets: structure of the discussion

• Initial measurement of the asset or measurement at initial recognition

• Measurement after recognition

– Changes in value during the useful live of the asset

• Derecognition

– Disposal or sale of the asset

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Contents

• Principles of accounting for depreciation• Determining the cost of a fixed asset• Government grants• Borrowing costs• Property, plant and equipment• Investment properties

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Definition of an asset

• Assets have been defined as follows: (Framework para. 49a):

– An asset is a resource controlled by the enterprise as a result of past events and from which future economic benefits are expected to flow

• Assets are divided in current assets and non-current assets

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Fixed or non-current assets

• With a finite live:

– Needs to be depreciated (see IAS 16)• With an indefinite live:

– Needs to be value-adjusted (see IAS 36 – impairment of assets)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Useful life

• Also called service life or economic life• Useful life = The period over which an asset

is expected to be available for use by an entity; or

• The number of production or similar units expected to be obtained from the asset by an entity

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Why depreciation?

• Depreciation of fixed assets results from the matching convention which requires that the corresponding expense needs to be matched with the benefit in each period

• The total expense for the asset’s life is spread over the total beneficial life in proportion to the pattern of benefit

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Depreciation

• Depreciation (amortization) is the systematic expensing of the cost of an asset over the period which benefits from its use

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Central issues

• How do we systematically recognize the expensing of the total cost of the asset over time?

• Depreciation is an “allocation issue”• The depreciation method shall reflect the

pattern in which the asset’s future economic benefits are expected to be consumed

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Information needed to calculate the amount of depreciation

• What is the cost of the asset? • What is the estimated useful life of the asset

to the business? (This may be equal to, or considerably less than, its technical or physical useful life.)

• What is the estimated residual selling value (“scrap value”) of the asset at the end of the useful life as estimated?

• What is the pattern of benefit or usefulness derived from the asset likely to be (not the amount of the benefit)?

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

The depreciable amount

• The total figure to be depreciated, known as the depreciable amount, will consist of the cost of the asset less the scrap value. This depreciable amount needs to be spread over the useful life in proportion to the pattern of benefit. Once the depreciable amount has been found, with revision if necessary to take account of material improvements, several recognized methods exist for spreading, or allocating, this amount to the various years concerned.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Residual value or scrap value

• Also called salvage value or terminal value• Estimated amount that an entity would

currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Methods of calculating depreciation

• Time based depreciation methods

– Straight line method– Reducing balance method– Sum of the digits method

• Methods based on activity level

– Defined as output of the asset– Defined as service quantity of the asset

(usage)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Characteristics of depreciation methods

• Time based depreciation methods: – Depreciation expense will be determined

regardless of the level of activity during the period

• Depreciation methods based on output or usage– Depreciation expense will be determined in

relation to the output produced in the relevant period by the asset or the level of service quantity used

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Straight line method

• The depreciable amount is allocated on a straight line basis, i.e. an equal amount is allocated to each year of the useful life. If an asset is revalued or materially improved then the new depreciable amount will be allocated equally over the remaining, possibly extended, useful life.

• Assumes uniform consumption pattern of economic benefits

• The depreciation expense: – Depreciable amount/ estimated useful live =

depreciation expense

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Activity 12.3 straight line method

• Calculate the annual depreciation charge

– Cost €12 000– Useful life 4 years– Scrap value €2 000

• Annual charge = (€12 000 – €2000)/4

= €2 500 EUR

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Reducing balance method

• Under this method, depreciation each year is calculated by applying a constant percentage to the net book value (NBV) brought forward from the previous year. (Note that this percentage is based on the cost less depreciation to date.) Given the cost (or valuation) starting figure and the useful life and ‘scrap’ value figures, the appropriate percentage needed to make the NBV at the end of the useful life exactly equal to the scrap value can be found from a formula:

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

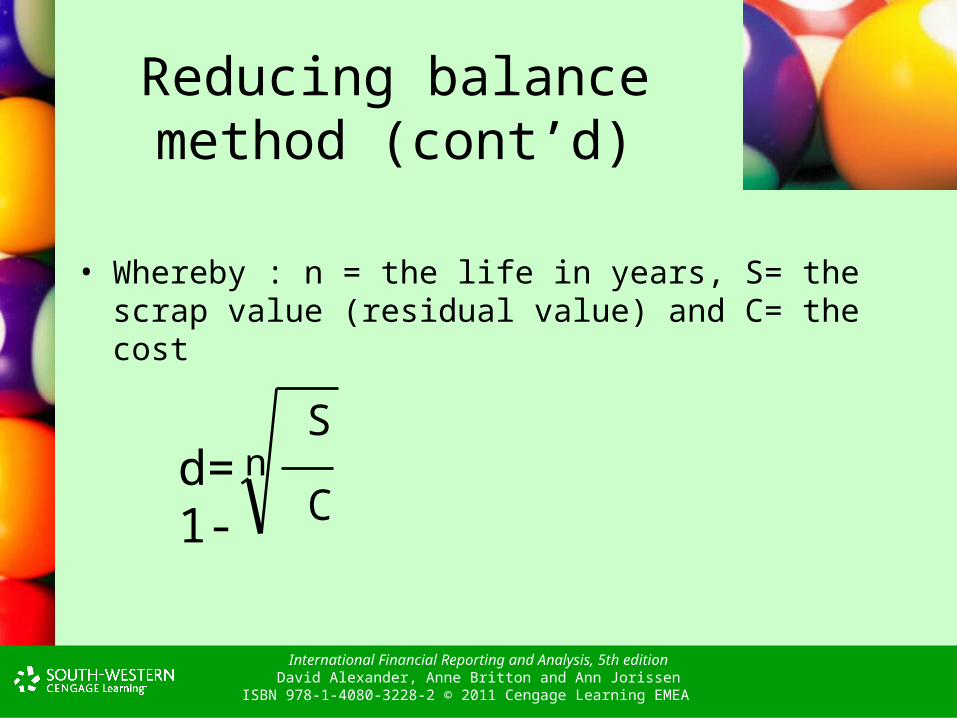

Reducing balance method (cont’d)

• Whereby : n = the life in years, S= the scrap value (residual value) and C= the cost

nC

Sd= 1-

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Reducing balance method (cont’d)

• Allocates a high proportion of expenses to the early years of the asset’s useful life

• Depreciation expense is calculated as percentage of the asset value after deduction of previous years’ accumulated depreciation (“the balance of the asset”)

• Depreciation rate can be mathematically derived, but will usually be approximated

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

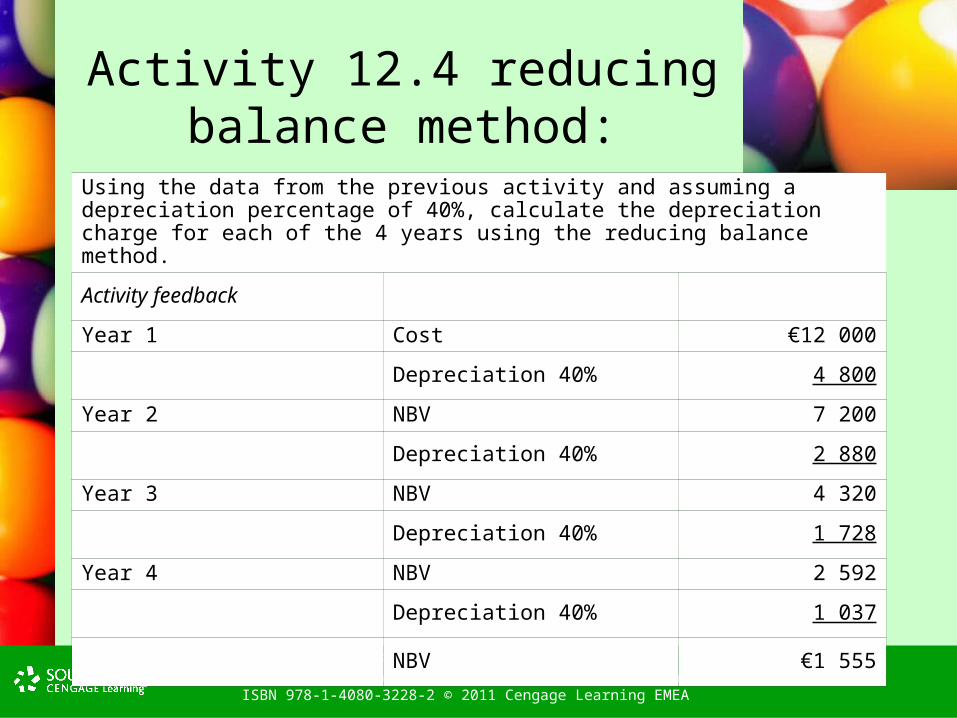

Activity 12.4 reducing balance method:

Using the data from the previous activity and assuming a depreciation percentage of 40%, calculate the depreciation charge for each of the 4 years using the reducing balance method.

Activity feedback

Year 1 Cost €12 000

Depreciation 40% 4 800

Year 2 NBV 7 200

Depreciation 40% 2 880

Year 3 NBV 4 320

Depreciation 40% 1 728

Year 4 NBV 2 592

Depreciation 40% 1 037

NBV €1 555

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Sum of digits method

• This is another example of a reducing charge method. It is based on a convenient “rule of thumb” and produces a pattern of depreciation charge somewhat similar to the reducing balance method.

• In general terms we give the n years weights of n, n 7 1, . . ., 1 respectively, and sum the total weights, the sum being n(n + 1)/2. The depreciable amount is then allocated over the years in the proportion that each year’s weighting bears to the total.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Activity 12.6Use the sum of the digits method to calculate annual depreciation charges for the data in the previous activities.

Activity feedback

1 4 + 3 + 2 + 1 = 10 (the “sum” of the “digits”)

2 Depreciable amount = €12 000 – €10 000

Depreciation charges are:

Year 1 4/10 x 10 000 = €4 000

Year 2 3/10 x 10 000 = €3 000

Year 3 2/10 x 10 000 = €2 000

Year 4 1/10 x 10 000 = €1 000

This gives NBV figures in the balance sheet of €8 000, €5 000, €3 000 and €2 000 for year ends 1–4, respectively.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Depreciation methods based on output or usage

• This is particularly suitable for assets where the rate of usage or rate of output can be easily measured

• Depreciable amount =

– (Rate of usage in period/total usage over the useful live) X (depreciable amount) or

– (rate of output in the period/total output over the useful live) x (depreciable amount)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Some misconceptions

• The process of depreciation calculation is not designed to produce meaningful balance sheet numbers

• The depreciable amount is the annual charge based on actual or implied assumptions as to the pattern of benefit being derived

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

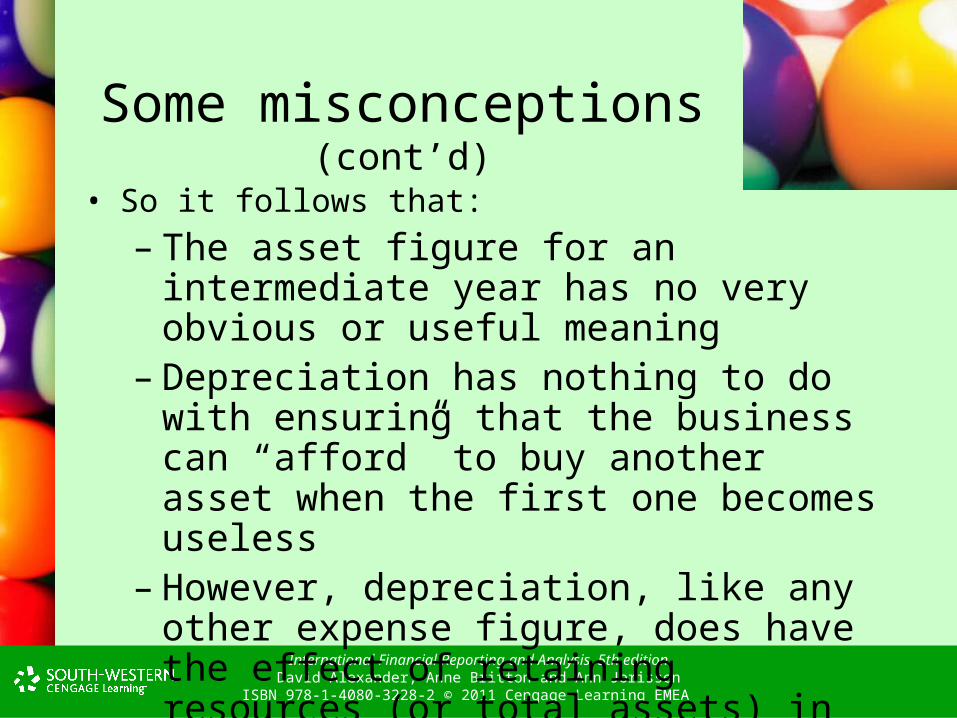

Some misconceptions (cont’d)

• So it follows that:

– The asset figure for an intermediate year has no very obvious or useful meaning

– Depreciation has nothing to do with ensuring that the business can “afford” to buy another asset when the first one becomes useless

– However, depreciation, like any other expense figure, does have the effect of retaining resources (or total assets) in the business

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

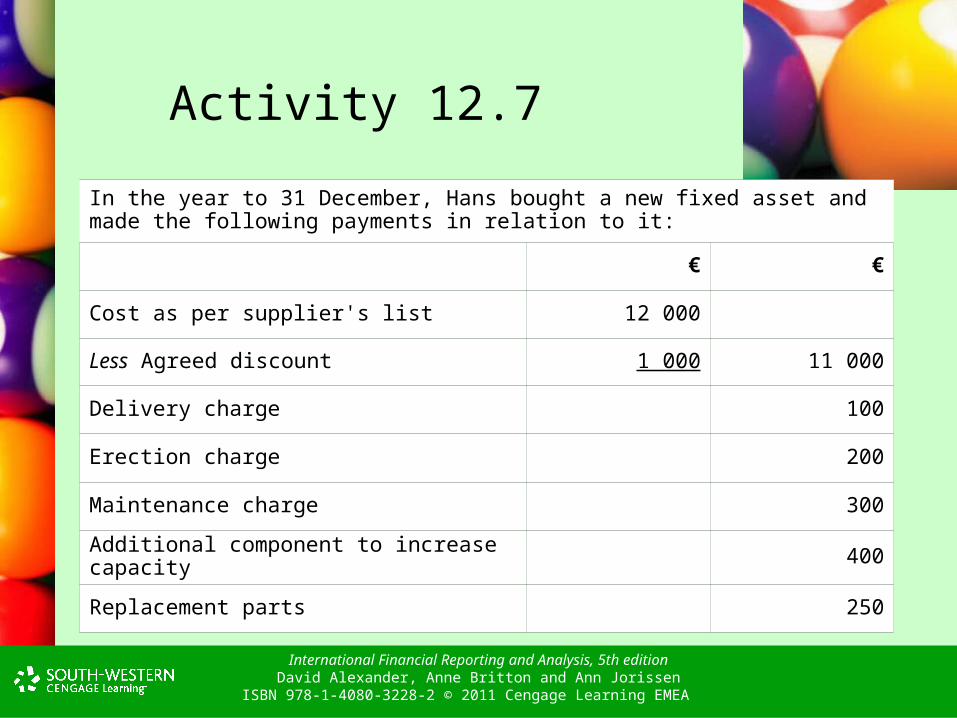

Activity 12.7

In the year to 31 December, Hans bought a new fixed asset and made the following payments in relation to it:

€ €

Cost as per supplier's list 12 000

Less Agreed discount 1 000 11 000

Delivery charge 100

Erection charge 200

Maintenance charge 300

Additional component to increase capacity 400

Replacement parts 250

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

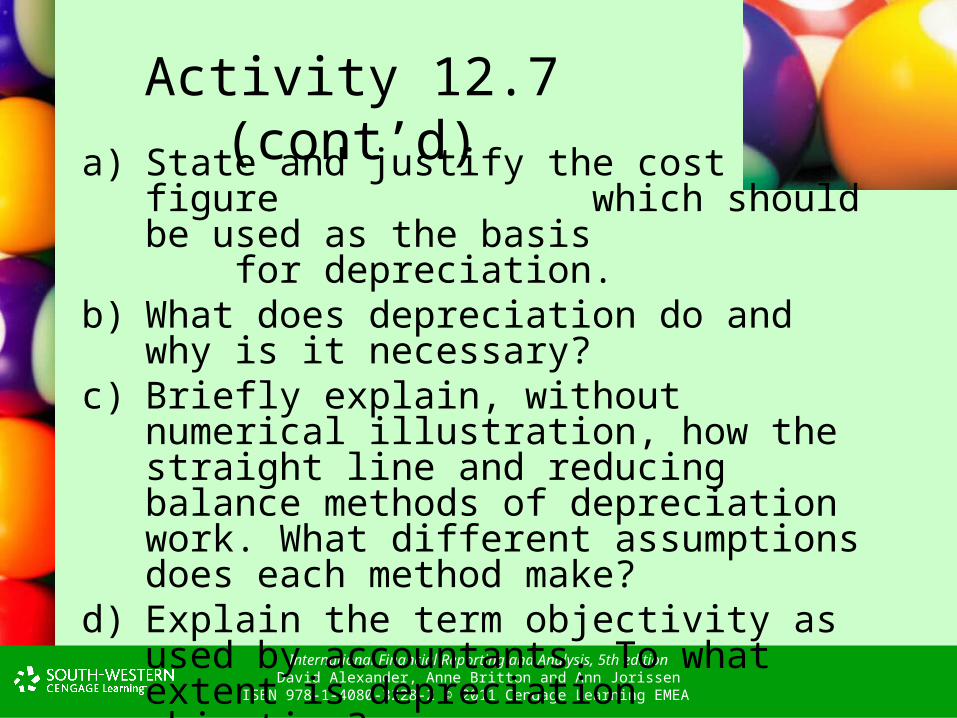

Activity 12.7 (cont’d)

a) State and justify the cost figure which should be used as the basis for depreciation.

b) What does depreciation do and why is it necessary?

c) Briefly explain, without numerical illustration, how the straight line and reducing balance methods of depreciation work. What different assumptions does each method make?

d) Explain the term objectivity as used by accountants. To what extent is depreciation objective?

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

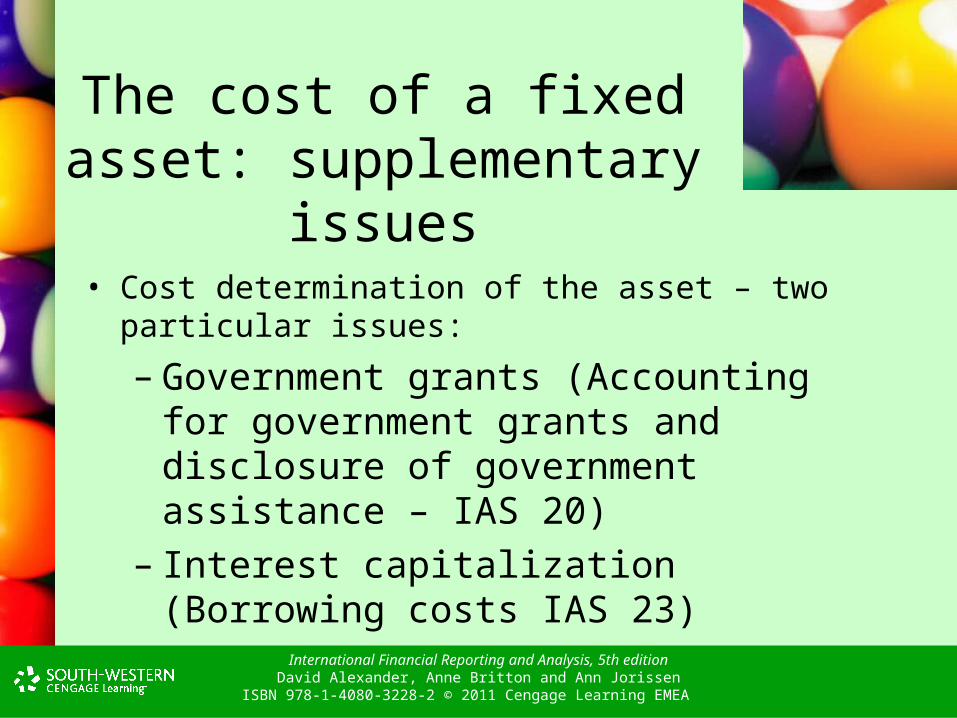

The cost of a fixed asset: supplementary issues

• Cost determination of the asset – two particular issues:

– Government grants (Accounting for government grants and disclosure of government assistance – IAS 20)

– Interest capitalization (Borrowing costs IAS 23)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Government assistance: definition

• Government assistance is action by government designed to provide an economic benefit specific to an enterprise or range of enterprises qualifying under certain criteria. Government assistance for the purpose of this standard does not include benefits provided only indirectly through action affecting general trading conditions, such as the provision of infrastructure in development areas or the imposition of trading constraints on competitors

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Government grants: definition

• Government grants are assistance by government in the form of transfers of resources to an entity in return for past or future compliance with certain conditions relating to operating activities of the entity. They exclude those forms of government assistance which cannot reasonably have a value placed upon them and transactions with government which cannot be distinguished from the normal trading transactions of the entity

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Government grants related to assets

• Grants related to assets are government grants whose primary condition is that an enterprise qualifying for them should purchase, construct or otherwise acquire long-term assets. Subsidiary conditions may also be attached restricting the type or location of the assets or the periods during which they are to be acquired or held

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Government grants related to income

• Grants related to income are government grants other than those related to assets.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Government grants: possible accounting treatments

• It is possible to suggest at least four possible different ways of treating the grant: – to credit the total amount of the grant immediately

to the income statement– to credit the amount of the grant to a non-

distributable reserve – to credit the amount of the grant to revenue over

the useful life of the asset by: (a) reducing the cost of the acquisition of the non-current asset

by the amount of the grant; or(b) treating the amount of the grant as a deferred credit, a portion

of which is transferred to revenue annually

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Illustration of the different accounting treatments

Using the data just given, the two ‘acceptable’ methods give the following results.

Method 3(a) € € € €

Profit before depreciation etc 20 000 20 000 20 000 20 000

Depreciation (2 500) (2 500) (2 500) (2 500)

Profit 17 500 17 500 17 500 17 500

Balance sheet extract at year end

Non-current asset at (net) cost 10 000 10 000 10 000 10 000

Depreciation 2 500 5 000 7 500 10 00

Carrying amount 7 500 5 000 2 500 ___0

Method 3(b)

Profit before depreciation etc. 20 000 20 000 20 000 20 000

Depreciation (3 000) (3 000) (3 000) (3 000)

Grant released __500 __500 __500 __500

Profit 17 500 17 500 17 500 17 500

Balance sheet extract at year end

Non-current asset at cost 12 000 12 000 12 000 12 000

Depreciation _3 000 _3 000 _3 000 _3 000

Carrying amount _9 000 _6 000 _3 000 ____0

Deferred credit

Government grant _1 500 _1 000 __500 ____0

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Borrowing costs: IAS 23

• Borrowing costs are defined (para. 4) as interest and other costs incurred by an entity in connection with the borrowing of funds. IAS 23 takes a broad view of what constitutes borrowing costs and include such items as amortization of ancillary costs incurred in connection with borrowings and preferred stock dividends if the preferred stock is classified as a liability in the balance sheet. By contrast, the imputed cost of financial instruments classed as equity capital is strictly excluded.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Borrowing costs: IAS 23

• An entity shall capitalise borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset as part of the cost of that asset. An entity shall recognise other borrowing costs as an expense in the period in which it incurs them.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

A qualifying asset: definition

• A qualifying asset (for the purposes of the “alternative” treatment) is an asset that necessarily takes a substantial period of time to get ready for its intended use or sale

– e.g. inventory: wine, spirits, ships and aircraft to be build or capitalized development costs or internally constructed assets

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Borrowing costs: measurement

• To the extent that an entity borrows funds specifically for the purpose of obtaining a qualifying asset, the entity shall determine the amount of borrowing costs eligible for capitalisation as the actual borrowing costs incurred on that borrowing during the period less any investment income on the temporary investment of those borrowings

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Borrowing costs: measurement (cont’d)

• To the extent that an entity borrows funds generally and uses them for the purpose of obtaining a qualifying asset, the entity shall determine the amount of borrowing costs eligible for capitalisation by applying capitalisation rate to the expenditures on that asset.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Borrowing costs: measurement (cont’d)

• The capitalisation rate shall be the weighted average of the borrowing costs applicable to the borrowings of the entity that are outstanding during the period, other than borrowings made specifically for the purpose of obtaining a qualifying asset. The amount of borrowing costs that an entity capitalises during a period shall not exceed the amount of borrowing costs it incurred during that period.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Commencement of capitalisation

• An entity shall begin capitalising borrowing costs as part of the cost of a qualifying asset on the commencement date. The commencement date for capitalisation is the date when the entity first meets all of the following conditions:– (a) it incurs expenditures for the asset– (b) it incurs borrowing costs;– © it undertakes activities that are necessary to

prepare the asset for its intended user or sale

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Suspension of capitalisation

• An entity shall suspend capitalisation of borrowing costs during extended periods in which it suspends active development of a qualifying asset.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Cessation of capitalisation

• An entity shall cease capitalising borrowing costs when substantially all the activities necessary to prepare the qualifying asset for its intended use or sale are complete

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Cessation of capitalisation (cont’d)

• When an entity completes the construction of a qualifying asset in parts and each part is capable of being used while construction continues on other parts, the entity shall cease capitalising borrowing costs when it completes substantially all the activities necessary to prepare that part for its intended use or sale

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Borrowing costs: disclosures

• An enterprise should disclose in the notes to its financial statements: – the amount of borrowing costs capitalised during

the period; and– The capitalisation rate used to determine the

amount of borrowing costs eligible for capitalisation.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Property, plant and equipment: IAS 16

• IAS 16 deals with the following items in relation to property, plant and equipment:

– initial measurement – determination of cost– measurement after initial recognition– depreciation– disposal of the asset (for sale see IFRS 5)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Property, plant and equipment

• Property, plant and equipment are tangible items that:

– are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes, and

– are expected to be used during more than one period

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Definition of cost

• Cost is the amount of cash or cash equivalents paid or the fair value of other consideration given to acquire an asset at the time of its acquisition or construction, or when applicable, the amount attributed to that asset when initially recognized in accordance with the requirements of IFRS 2 (share-based payment)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

PPE: recognition

• An item of property, plant and equipment should be recognized (para. 7) as an asset if, and only if:

– it is probable that future economic benefits associated with the item will flow to the entity; and

– the cost of the item to the entity can be measured reliably

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

PPE: measurement

• Initial measurement• Subsequent costs• Measurement subsequent to initial

recognition• Derecognition

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

PPE: initial measurement

• An item of property, plant and equipment that qualifies for recognition as an asset should initially be measured at its cost

• The cost of an item of property, plant and equipment comprises– its purchase price, including import duties and

non-refundable purchase taxes and – any directly attributable costs of bringing the asset

to working condition for its intended use; – the initial estimate of the costs of dismantling

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

PPE: initial measurement (cont’d)

• Examples of directly attributable costs are: – cost of site preparation– initial delivery and handling costs – installation and assembly costs – professional fees such as for architects and engineers– the estimated cost of dismantling and removing the

asset and restoring the site, to the extent that it is recognized as a provision under IAS 37, Provisions, Contingent Liabilities and Contingent Assets

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

PPE: initial measurement (cont’d)

• The following costs are not included in the carrying amount of an item of property, plant and equipment: – costs incurred while an item capable of operating

in the manner intended by management has yet to be brought into use or is operated at less than full capacity

– initial operating losses, such as those incurred while demand for the item’s output builds up

– costs of relocating or reorganizing part or all of an entity’s operations

– costs of opening a new facility

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

PPE: initial measurement (cont’d)

• Elements not be included in the cost of a PPE– costs of introducing a new product or service

(including costs of advertising and promotional activities)

– costs of conducting business in a new location or with a new class of customer (including costs of staff training)

– administration and other general overhead costs

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

PPE: subsequent costs

• Under the recognition principle an entity recognizes in the carrying amount of an item of property, plant and equipment the cost of replacing such a part of an item when that cost is incurred if the recognition criteria are met. The carrying amount of those parts that are replaced is derecognized in accordance with the derecognition provisions of the Standard.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Measurement after recognition or subsequent to

initial recognition

• Two alternative approaches to subsequent measurement are allowed:– the cost model, or– the revaluation model

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

The cost model

• IAS 16 describes this treatment as:

– after recognition as an asset, an item of property, plant and equipment shall be carried at its cost less any accumulated depreciation and any accumulated impairment losses

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Depreciable amount and depreciation period: IAS 16

• The depreciable amount of an asset shall be allocated on a systematic basis over its useful life

• The depreciable amount of an asset is determined after deducting its residual value. In practice, the residual value of an asset is often insignificant and therefore immaterial in the calculation of the depreciable amount

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Depreciable amount/ depreciation period: IAS 16

(cont’d)• The future economic benefits embodied in an

asset are consumed by an entity principally through its use. However, other factors, such as technical or commercial obsolescence and wear and tear while an asset remains idle, often result in the diminution of the economic benefits that might have been obtained from the asset. Consequently, all the following factors are considered in determining the useful life of an asset:

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Depreciable amount /depreciation period: IAS 16

(cont’d)– expected usage of the asset. Usage is

assessed by reference to the asset’s expected capacity or physical output

– expected physical wear and tear, which depends on operational factors such as the number of shifts for which the asset is to be used and the repair and maintenance programme, and the care and maintenance of the asset while idle

– technical or commercial obsolescence arising from changes or improvements in production, or from a change in the market demand for the product or service output of the asset

– legal or similar limits on the use of the asset, such as the expiry dates of related leases

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Depreciation method: IAS 16

• The depreciation method used shall reflect the pattern in which the asset’s future economic benefits are expected to be consumed by the entity

• The depreciation method applied to an asset shall be reviewed at least at each financial year end, if there has been a significant change in the expected pattern of consumption of the future economic benefits embodied in the asset, the method shall be changed to reflect the changed pattern

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Components approach of IAS 16

• Each part of an item of PPE with a cost that is significant in relation to the total cost of the item shall be depreciated separately (para. 43)

• An entity is required to determine the depreciation expense separately for each significant part (component) of an item of PPE

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

The revaluation model

• After recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, being its fair value at the date of revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses.

• Revaluations shall be made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the balance sheet date.

• If an item of PPE is revalued, the entire class of PPE to which the asset belongs shall be revalued

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

The revaluation model (cont’d)

• If an asset’s carrying amount is increased as a result of a revaluation, the increase shall be credited directly to equity under the heading of revaluation surplus. However the increase shall be recognized in P&L to the extent that it reverses a revaluation decrease of the same asset previously recognized in profit or loss

• If an asset’s carrying amount is decreased as a result of a revaluation, the decrease shall be recognized in profit or loss. However, the decrease shall be debited directly to equity under the heading of revaluation surplus to the extent of any credit balance existing in the revaluation surplus in respect of that asset.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

The revaluation model (cont’d)

• When an item of property, plant and equipment is revalued, any accumulated depreciation at the date of the revaluation is treated in one of the following ways:

– restated proportionately with the change in the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals its revalued amount. This method is often used when an asset is revalued by means of an index to its depreciated replacement cost; or

– eliminated against the gross carrying amount of the asset and the net amount restated to the revalued amount of the asset. This method is often used for buildings.

• The amount of the adjustment arising on the restatement or elimination of accumulated depreciation forms part of the increase or decrease in carrying amount that is accounted for in accordance with paras 39 and 40.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Activity 12.10

• Suppose we have an asset to which IAS 16 applies, cost 10 000, useful life 5 years, estimated residual value nil, now 3 years old. The asset is then revalued to a new gross figure of 15 000, that is the new “cost” is 15 000, for the purpose of treatment (a). Alternatively the asset is now revalued to a current fair value in its existing state of 6 000, for the purpose of treatment (b). Show the implications of each of these two treatments.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Activity 12.10 feedback

(a) Suggests the following:

Cost Depreciation Carrying amount

10 000 6 000 4 000

The asset is now revalued, by index or otherwise, to a new gross figure of 15 000, i.e. the new ‘cost’ is 15 000. The depreciation is now ‘restated proportionately’, i.e. it is also increased by 50%. We thus end up with:

Gross revaluation Depreciation Carrying amount

15 000 9 000 6 000

This increase in carrying amount of 2 000 is then dealt with as discussed later.

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

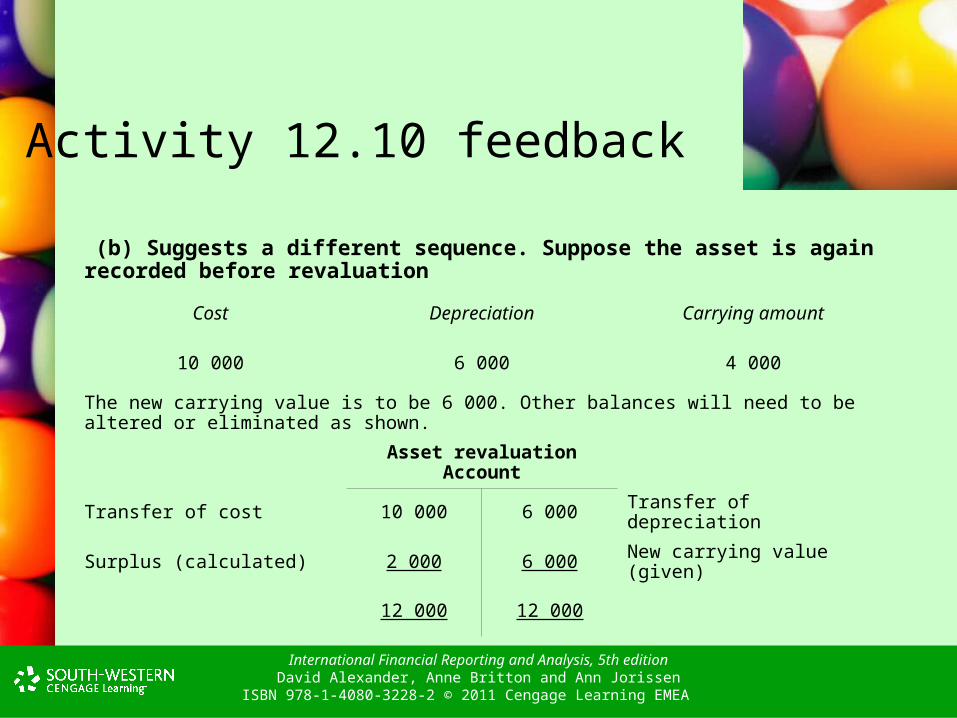

Activity 12.10 feedback

(b) Suggests a different sequence. Suppose the asset is again recorded before revaluation

Cost Depreciation Carrying amount

10 000 6 000 4 000

The new carrying value is to be 6 000. Other balances will need to be altered or eliminated as shown.

Asset revaluation Account

Transfer of cost 10 000 6 000 Transfer of depreciation

Surplus (calculated) 2 000 6 000 New carrying value (given)

12 000 12 000

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Impairment of Assets

• It is necessary to determine whether or not an item of property, plant and equipment has become impaired. This area is covered by IAS 36, Impairment of Assets

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Derecognition

• The carrying amount of an item of property, plant and equipment shall be derecognized:

– on disposal; or– when no future economic benefits are

expected from its use or disposal• Gain or loss on disposal is recognized in the income

statement

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Disclosures

• The financial statements shall disclose, for each class of property, plant and equipment:

a) the measurement bases used for determining the gross carrying amount;

b) the depreciation methods used;c) the useful lives or the depreciation rates used;d) the gross carrying amount and the accumulated

depreciation (aggregated with accumulated impairment losses) at the beginning and end of the period

e) a reconciliation of the carrying amount at the beginning and end of the period

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Accounting for investment properties: definition

• Investment property is property (land or a building or part of a building or both) held (by the owner or by the lessee under a finance lease) to earn rentals or for capital appreciation or both, rather than for: – use in the production or supply of goods or services, or for

administrative purposes; or – sale in the ordinary course of business

• Owner-occupied property is property held (by the owner or by the lessee under a finance lease) for use in the production or supply of goods or services or for administrative purposes

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Investment properties: recognition

• An investment property within the definition should be recognized as an asset when, and only when:

– it is probable that the future economic benefits that are associated with the investment property will flow to the entity

– the cost of the investment property can be measured reliably

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Accounting for investment properties: measurement

• Initial measurement:

– At cost, transaction costs shall be included in the initial measurement• Purchased investment property – purchase

price + any directly attributable expenditure• Self-constructed investment property – the

cost at the date when the construction or development is complete (until that date IAS 16 is applied)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Accounting for investment properties: measurement (cont’d)

• Subsequent measurement– Cost model – Fair value model– An entity may

• (a) choose either the fair value model or the cost model for all investment property backing liabilities that pay a return linked directly to the fair value of, or returns from, specified assets including that investment property; and

• (b) choose either the fair value model or the cost model for all other investment property, regardless of the choice made in (a)

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Cost model

• After initial recognition, an entity that chooses the cost model shall measure all of its investment property in accordance with IAS 16’s requirements

• If the investment property meets the criteria to be included in non-current assets held for sale, the assets shall be valued according to IFRS 5

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Fair value model

• After initial recognition, an entity that chooses the fair value model shall measure all of its investment property at fair value.

• There is a rebuttable presumption that an entity can reliably determine the fair value of the investment property on a continuing basis, if not it should choose the cost model

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Fair value model (cont’d)

• A gain or loss arising from a change in the fair value of investment property shall be recognized in profit or loss for the period in which it arises

• The fair value shall reflect the market conditions at the balance sheet date

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

Disposal of investment properties

• An investment property shall be derecognized (eliminated from the balance sheet) on disposal or when the investment property is permanently withdrawn from use and no future economic benefits are expected from its disposal

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA

International Financial Reporting and Analysis, 5th editionDavid Alexander, Anne Britton and Ann Jorissen

ISBN 978-1-4080-3228-2 © 2011 Cengage Learning EMEA