international financial reporting standards ready to … · under international financial reporting...

TRANSCRIPT

1 Ready to take the plunge?

International Financial Reporting Standards

Ready to take the plunge?*

Survey of over 300 European companies’ readiness for IFRSMay 2004

www.pwc.com/ifrs

AustriaAslan [email protected]: +43 1 501 88 0

BelgiumYves [email protected]: +32 2 710 4029

DenmarkJens Otto [email protected]: +45 39 45 39 45

FinlandTomi Seppälä[email protected]: +358 9 22800

FranceThierry [email protected]: +33 1 56 57 58 59

GermanyManfred [email protected]: +49 211 981 0

GreeceNick [email protected]: +30 210 6874 400

ItalyRoberto [email protected]: +390 422 542726

LuxembourgPhilippe [email protected]: +352 49 48 48 1

NetherlandsLeandro van [email protected]: +31 20 568 6666

NorwayTrond Tø[email protected]: +47 95 26 00 00

PortugalNasser [email protected]: +351 213 197 000

SpainFrancisco [email protected]: +34 91 568 44 00

SwedenJan [email protected]: +46 8 555 330 00

SwitzerlandDavid [email protected]: +41 22 748 51 11

United KingdomIan [email protected]: +44 20 7583 5000

PricewaterhouseCoopers (www.pwc.com) provides industry-focused assurance, tax and advisory services for public and private clients. More than 120,000people in 139 countries connect their thinking, experience and solutions to build public trust and enhance value for clients and their stakeholders.

© 2004 PricewaterhouseCoopers. All rights reserved. PricewaterhouseCoopers refers to the network of member firms of PricewaterhouseCoopersInternational Limited, each of which is a separate and independent legal entity. Designed by studio ec4 (16565 05/04).

Contacting PricewaterhouseCoopers

IFRS conversion leaders for the countries participating in this survey are listed below. Please contact them or yourlocal PricewaterhouseCoopers office to discuss how we can help you make the change to International FinancialReporting Standards. See inside back cover for further details of publications, products and services.

European IFRS Transition Steering GroupYves [email protected]: +32 2 710 4029

IFRS Services, Global CorporateReporting GroupIan [email protected]: +44 20 7804 2676

Contents

Ready to take the plunge? 1

Foreword 3Delay is not an option

Executive summary 4Don’t underestimate what’s involved

About the survey 6Who is ahead of the curve?

IFRS transition project 11Is it set up and resourced?

Communicating the impact 13Do stakeholders understand?

Embedding IFRS into the organisation 18Is IFRS the new ‘business as usual’?

Balancing the key issues 22How are technical preparations progressing?

Checklist 27What action can the board take?

Delay is not an option*PricewaterhouseCoopers

Foreword

Ready to take the plunge? 3

The IFRS transition date for mostcompanies passed on 1 January 2004

ForewordInternational Financial Reporting Standards (IFRS) are no longer somethingfor the future – they are here. Delay is not an option for those companiesmoving to IFRS for 2005. The IFRS transition date for most companiespassed on 1 January 2004. Other milestones for IFRS comparativeinformation will follow in rapid succession.

Some companies delayed getting ready for IFRS while they waited for the final text of the standards. However, on 31 March 2004, the InternationalAccounting Standards Board (IASB) completed its final platform of standardsthat are compulsory for 2005. Some amendments are expected, but these willbe minor for most companies.

Companies now have the certainty they need to make rapid progress with IFRS implementation while the European Commission arranges for these final standards to be endorsed for use in Europe.

The Committee of European Securities Regulators (CESR) has already givencompanies a wake-up call, asking them to provide markets with appropriate and useful information in a phased process. It recommended that a narrative of IFRS transition progress and key accounting differences between IFRS andprevious generally accepted accounting principles (GAAP) should be includedearly: as early as with the 2003 financial statements.

Analysts and investors are also starting to call for more information on IFRS.Some investment analysts have reported that readiness for IFRS will beincluded in their evaluation of management performance. This suggests that ifcompanies are unable to demonstrate during 2004 that they have ‘IFRS 2005’under full control, they risk damaging themselves in stakeholders’ eyes.

The results of this survey show that some companies have made significantprogress and should be well placed to meet their IFRS deadlines. Conversely, a majority of companies still have a lot to do to make a successful transition.

This is the biggest accounting change in a generation, and it comes at the same time as other big corporate reporting changes such as the Sarbanes-Oxley and Basel II requirements. IFRS is intended to give investors and otherstakeholders access to high-quality financial information that, for the first time,is comparable across borders.

The clear message from those that have already made the change is: ‘Don’t underestimate what’s involved.’

4 Ready to take the plunge?

Don’t underestimate what’s involved*Survey participant

This survey assesses the readiness of companies in 16 countries to reportunder International Financial Reporting Standards from 2005 (see Aboutthe survey, page 6).

The results show that the vast majority of the 310 companies surveyed stillhave a lot of work to do to make the change to IFRS. This is a concern,though perhaps not surprising given that the final text of the standardsthey are being asked to implement has only recently been released.Companies must now forge ahead with their plans and make fastprogress in the next few months.

Three quarters of European companies surveyed have at least some understanding of the impact of IFRS on their business (see page 13)

A majority of companies have at least started to assess the impact of IFRS on their reporting and key performance indicators. A quarter, however, have not started this crucial part of making the change to IFRS.

Investors and analystshave indicated that

companies are at risk ifthey are unable to

demonstrate this yearthat they have ‘IFRS

2005’ under full control

Executive summary

Executive summary

Ready to take the plunge? 5

‘The later you leave it, the bigger theresourcing issue becomes’Survey participant

A majority of companies have set up their IFRS project framework (see page 11)

Most companies have set up their IFRS project and begun the process ofplanning the change, even though some of these are still finalising their projectmanagement and procedures. The rest have either made very limited progressor not started at all (10%). Those that are behind the curve will need to catchup quickly, as a clear project framework helps to give the capital marketsconfidence that companies can deliver timely and reliable IFRS information.

20% of companies have already focused oncommunicating to the market (see page 16)

20% of respondents have already determined how they will communicate changesin their financial information to the markets. The challenge for other companiesis to avoid ‘surprise’ changes that can trigger negative market reactions.

Shortage of skilled resources is one of the toughestchallenges companies face (see page 12)

Most companies have at least some full-time resource working on their IFRStransition projects. However, just 10% of respondents are confident that theyhave the right people and skills in place to help them complete the change intime. Smaller companies, in particular, are finding it difficult to commit full-timeresources to IFRS implementation. The concern for companies is whether thepeople they need will be available as the demand for IFRS specialists reachesits peak in 2004/2005.

Training and communication strategies are still pending for the majority of companies (see page 15)

Just over a quarter of companies either have their training/communicationsstrategies in place and in action, or they are in the process of a comprehensiveneeds analysis. This leaves a majority with a lot of work to do in this area. Staff at all levels in an organisation need to understand the new reportinglanguage and how it affects their working practices.

Most companies have significant work ahead to embedIFRS as ‘business as usual’ (see page 18)

Identifying missing information that will be needed for IFRS reporting is a critical step for companies changing to IFRS. This must now be made a priorityfor almost three-quarters of companies that have yet to complete this step.Companies will need IFRS comparative data for 2004 in their 2005 accounts.

The experience of existing IFRS reporters has shown that adapting IT systemsto produce the required information is one of the most challenging and time-consuming steps. So far, just 11% have sourced their IFRS data and completedthe priority information systems enhancements. Only once these steps havebeen taken can companies generate audited financial statements for the 2005financial year and be sure that they will not surprise the market.

‘Transparentcommunications arean important part ofour overall strategy’Survey participant

6 Ready to take the plunge?

About the surveyWith less than a year to go before public companies in the European Union are required to use IFRS as the basis of their published accounts, this surveyassesses how ready companies are to make the change.

The information in this report is based on structured interviews with 310company officers – generally the IFRS transition project leader – based in 16 European countries. The vast majority of these companies are publiclylisted. All of them are in the process of changing to IFRS for 2005. In mostcases, interviews were conducted by PricewaterhouseCoopers professionals,either in person or over the telephone, in the first quarter of 2004.

The primary aim was to help companies to assess their readiness for IFRS and highlight areas that will need further attention before the first IFRS financialstatements are published. This report covers the summary results for the 310participating companies.

Companies’ readiness for IFRS was assessed in the following main areas:• Project set-up and resourcing• Communications and training• Embedding – data, systems, process and controls • Key technical issues

All the companies were asked the same key questions, and their readinessassessed on a scale of 0 to 4 against specific criteria for each question. The extent of readiness was analysed as follows:0 – No progress yet in this area1 – Initial analysis started with high-level considerations2 – Thought-process completed with relevant analysis and decisions in place3 – Actions started to address this issue4 – Actions completed, issues resolved and changes embedded in the business

x

Who is ahead of the curve?*

About the survey

PricewaterhouseCoopers has tracked the progress of Europe’s listedcompanies towards IFRS closely over the past four years. In 2000, the firmpublished 2005 or now?, a report based on independent research into theperceptions and understanding of IFRS (previously known as InternationalAccounting Standards) among chief financial officers in more than 700 Europeancompanies. In 2002, a follow-up survey, 2005 – Ready or not, examined whatprogress had been made and how the debate over IFRS had moved on. While the present survey differs from its predecessors, because it is a moredetailed examination of practical readiness it can be viewed alongside them as a useful insight into corporate Europe’s progress towards IFRS.

Which companies participated in the survey?

The survey focused on companies listed in their country of incorporation (92%). 16% of survey participants also have US listings. Non-listed companiesmade up 8% of participants.

The survey covered a wide range of companies from small to large marketcapitalisation, and included companies from a wide range of industries. Most of the companies questioned (82%) have financial year-ends of 31 December; 8% have their year-end at 31 March.

The countries covered by the survey were: Austria, Belgium, Denmark, Finland,France, Germany, Greece, Italy, Luxembourg, the Netherlands, Norway,Portugal, Spain, Sweden, Switzerland, the United Kingdom.

What was the impact of company size on survey results?

Ready to take the plunge? 7

IFRS readiness – by market capitalisation

Over €10bn12%

Ave

rage

sco

re

Project status & resourcing

Scoring: 0 = no progress 4 = completely ready

Communication& reporting

Data, systems, process & controls

Key technical issues

0

1

2

3

4Under €1bn

55%European average

scores€1-10bn

33%

Large companies have made more progresstowards implementingIFRS than smaller onesSurvey result

Number of listed participants: 283

About the survey

Large companies (over €10bn market capitalisation) have made more progresstowards implementing IFRS than smaller ones. A gap between the largest andthe smallest companies may be expected, given both the perceived scale ofthe task and the relative quantities of resources available to tackle the changeprocess. However, identifying and producing the IFRS data could prove to bemore difficult for some smaller companies with less sophisticated data systems.Much depends on the complexity. The more complex the company, in terms ofbusiness segment and geographical locations, the more challenging thetransition to IFRS is likely to be.

Companies with a market capitalisation of more than €10bn (12% of the listedcompanies surveyed) scored consistently and comfortably above the average.Companies with a market capitalisation under €10bn were closer to the mean.However, smaller companies were well represented among the top performersin the survey as a whole.

Are companies in certain industries more prepared than others?

No industry group is significantly better prepared for IFRS implementation thanany other. However, financial services companies (21% of the survey) appear to be slightly more advanced than other sectors, perhaps because they recognisethat their systems and processes are often more complex, and they will need theextra time to complete the changes in a controlled way. This sector often hasmore pervasive and complex issues to deal with, particularly in accounting forfinancial instruments.

Technology, communications and entertainment companies (23% of the sample)are at or above average on most measures. Consumer, industrial products andservices companies (53%) are slightly below average in certain areas such asproject management, and on preparation of IFRS data, systems, processes andcontrols. However, this may reflect the higher proportion of smaller companiesin this sector.

Progress in changing to IFRS has reached

similar levels in all industries

Survey result

8 Ready to take the plunge?

IFRS Readiness – by Industry

Project status & resourcing

Communication& reporting

Data, systems, process & controls

Key technical issues

0

1

2

3

4

Ave

rage

sco

re

Scoring: 0 = no progress 4 = completely ready

Technology, communications and entertainment

Consumer, industrial products and services eg. energy, pharmaceuticals, retail

European average

Financial services

Public sector

Number of participants: 310

About the survey

Ready to take the plunge? 9

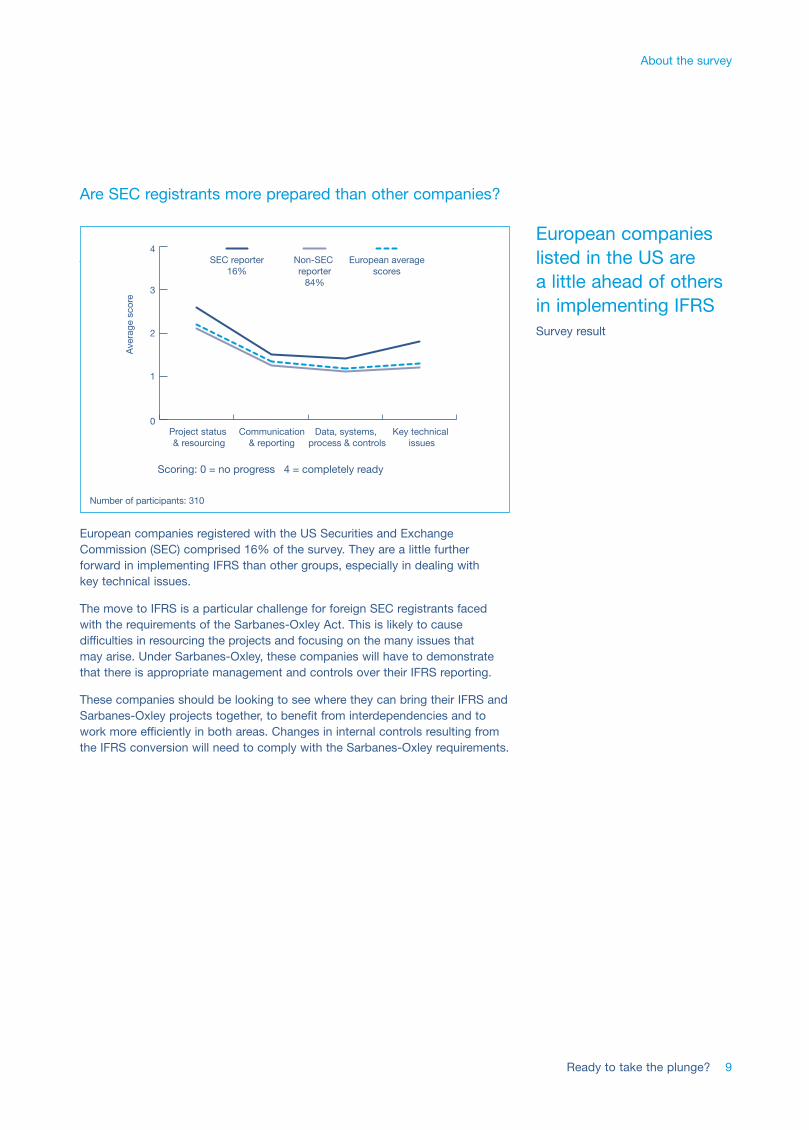

Are SEC registrants more prepared than other companies?

European companies registered with the US Securities and ExchangeCommission (SEC) comprised 16% of the survey. They are a little furtherforward in implementing IFRS than other groups, especially in dealing with key technical issues.

The move to IFRS is a particular challenge for foreign SEC registrants facedwith the requirements of the Sarbanes-Oxley Act. This is likely to causedifficulties in resourcing the projects and focusing on the many issues that may arise. Under Sarbanes-Oxley, these companies will have to demonstratethat there is appropriate management and controls over their IFRS reporting.

These companies should be looking to see where they can bring their IFRS andSarbanes-Oxley projects together, to benefit from interdependencies and towork more efficiently in both areas. Changes in internal controls resulting fromthe IFRS conversion will need to comply with the Sarbanes-Oxley requirements.

European companieslisted in the US are a little ahead of others in implementing IFRSSurvey result

Ave

rage

sco

re

Project status & resourcing

Communication& reporting

Data, systems, process & controls

Key technical issues

0

1

2

3

4Non-SEC reporter

84%

European averagescores

SEC reporter16%

Scoring: 0 = no progress 4 = completely ready

Number of participants: 310

10 Is your company ready?

One of the toughest challengesis finding skilled people*Survey participant

IFRS transition projectIs it set up and resourced?

As a starting point for assessing readiness for conversion to IFRS, we askedcompanies to describe their progress in setting up their IFRS programmeand securing appropriate board-level sponsorship and resources.

How many companies have set up their IFRS conversionproject and management?

A majority of companies have set up their IFRS project framework and begunthe process of planning the change. Half of these are still finding resources andfinalising procedures, while the other half have dedicated conversion projectsfully up and running. This means, as a minimum, that the projects have:operational steering and technical committees; regular progress reporting; auditcommittee oversight; the commitment of key stakeholders within the company;and the necessary project management resources. Properly-constitutedprojects also assign responsibility for managing the interdependencies betweenIFRS conversion and other financial reporting projects, such as compliance withthe Sarbanes-Oxley regulations.

At the other end of the scale, 42% of companies have yet to set up a formalproject framework for conversion to IFRS. This includes one in 10 that have not yet started, and around a third that are in the early stages of consideringhow they might run a successful conversion exercise.

What progress has been made at group and business unit level?

The survey showed that project teams are typically managed through the groupfinance function and often have limited involvement of people at subsidiary/business unit level. While around 80% of companies reported that, as a minimum,they recognised the project issues and needs at group level, 25% revealed thatthey had made no progress at the subsidiary/business unit level.

IFRS transition project

Ready to take the plunge? 11

Not started Limited progressFully set up and running

Framework in place, resources needed

29%29%32%10%

IFRS project set-up and management progress

‘There is no quickway of doing this –you just have to startfrom somewhere’Survey participant

‘We took the views of every subsidiaryseparately andinvestigated thechanges needed for each’Survey participantNumber of participants: 310

Do companies have the resources in place to ensure successful conversion?

One in 10 companies are confident that they have the right people with theright skills in place to help them complete IFRS conversion on time andproduce the required information for external reporting. This means they haveenough dedicated, appropriately skilled resources available – internally orexternally – to manage and implement the project effectively at group level and in the company’s subsidiaries.

Companies that have already completed their transition (not included in thissurvey) have needed a wide range of skills, including: knowledge of IFRS andthe business, investor relations, actuarial, taxation, training, IT/systems designand implementation, and change management.

Almost half have yet to dedicate any full-time resources to IFRS conversion.68% of companies will require significant additional resources if they are goingto be ready on time. The largest companies are more likely to have committedsignificant resources to the project.

Comment

The capital markets are looking for assurance that companies have the abilityto deliver timely, relevant and consistent financial information that is highlyreliable. Existing IFRS reporters have found that a clear project framework with well-defined roles and responsibilities has helped to give managementconfidence that its IFRS processes are reliable and will deliver robust informationon time, internally and externally. The bigger and more complex the company,the more important it is to be able to demonstrate effective management of theIFRS conversion.

Companies are taking action at group level, but more involvement at entity level will be needed. Some companies that have almost completed their transitionto IFRS report that they have involved people at entity level from the outset.

One of the toughest challenges in an IFRS conversion project is finding enoughpeople with appropriate knowledge and experience to implement IFRS andoversee its integration, so that the organisation is comfortable with its new wayof operating.

12 Ready to take the plunge?

IFRS transition project

‘Converting to IFRS is much more than a

change in accounting – it should change the waypeople work throughout

an organisation’PricewaterhouseCoopers

None

Some part-timeMany part- and full-time available; some extra resources needed

Some part-time and full-time, many more resources needed

10%22% 22%31%15%

Fully resourced

Progress in allocating resources for IFRS conversion

Number of participants: 310

Communicating the impactDo stakeholders understand?

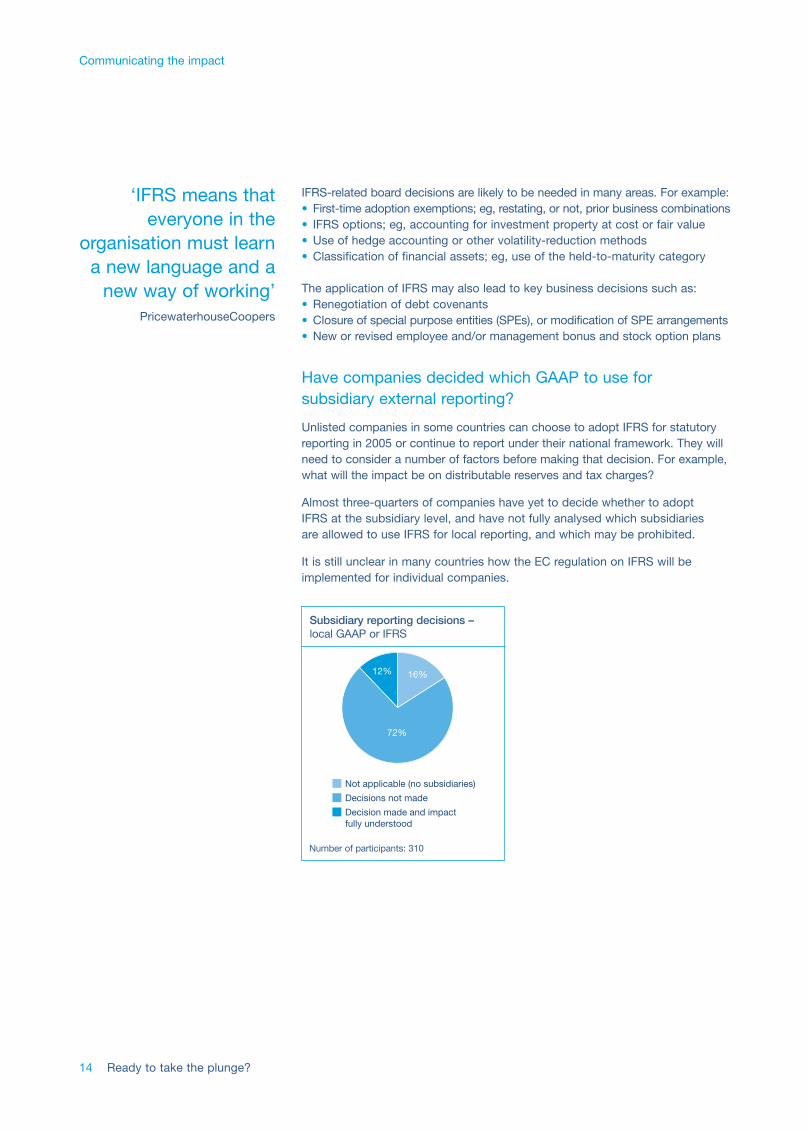

Have companies assessed the high-level impact ofconversion on their business?

Three quarters of European companies surveyed have at least someunderstanding of the impact of IFRS on their business. A quarter, however, have not started this crucial part of making the change to IFRS. A high-levelassessment highlights the key implications of the change for the business –including possible effects on the reported results and key performance indicators.Board-level understanding and awareness of the likely strategic impact of IFRSis a vital step towards setting appropriate parameters for the IFRS project.

Just over a third of companies have completed their high-level assessment. But of those, only 8% have determined their approach at board level to thepotential changes to key performance indicators.

Ready to take the plunge? 13

Avoid market disruption with clearexternal communications*

PricewaterhouseCoopers

No progress Some preliminary analysisBoard decisions communicated to IFRS project team

Assessment presented to the Board

8%27%40%25%

Understanding of the high-level impacts of IFRS

‘IFRS is helping somefunctions to speakwith other functions,which is a good thing’Survey participant

Number of participants: 310

IFRS-related board decisions are likely to be needed in many areas. For example:• First-time adoption exemptions; eg, restating, or not, prior business combinations• IFRS options; eg, accounting for investment property at cost or fair value• Use of hedge accounting or other volatility-reduction methods• Classification of financial assets; eg, use of the held-to-maturity category

The application of IFRS may also lead to key business decisions such as:• Renegotiation of debt covenants• Closure of special purpose entities (SPEs), or modification of SPE arrangements• New or revised employee and/or management bonus and stock option plans

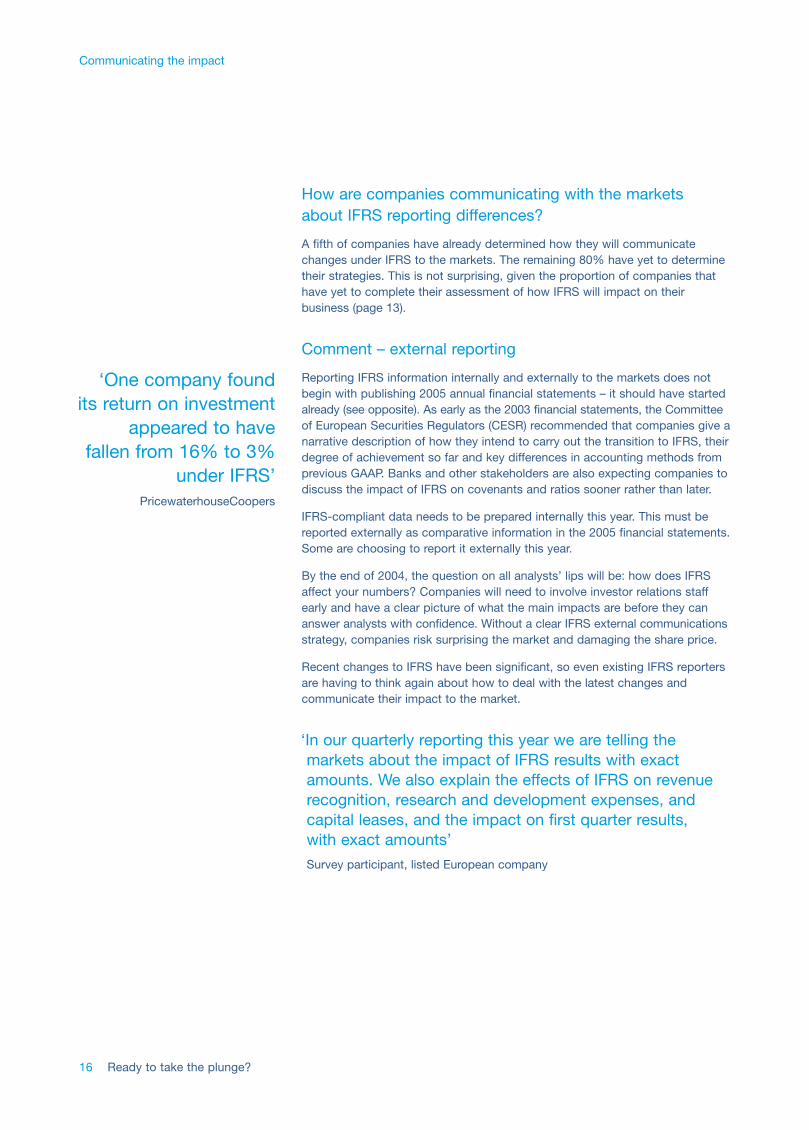

Have companies decided which GAAP to use for subsidiary external reporting?

Unlisted companies in some countries can choose to adopt IFRS for statutoryreporting in 2005 or continue to report under their national framework. They willneed to consider a number of factors before making that decision. For example,what will the impact be on distributable reserves and tax charges?

Almost three-quarters of companies have yet to decide whether to adopt IFRS at the subsidiary level, and have not fully analysed which subsidiaries are allowed to use IFRS for local reporting, and which may be prohibited.

It is still unclear in many countries how the EC regulation on IFRS will beimplemented for individual companies.

14 Ready to take the plunge?

Communicating the impact

Decision made and impact fully understood

Not applicable (no subsidiaries)

Decisions not made

16%12%

72%

Subsidiary reporting decisions – local GAAP or IFRS

Number of participants: 310

‘IFRS means thateveryone in the

organisation must learna new language and a

new way of working’PricewaterhouseCoopers

How much progress have companies made with internalcommunications, knowledge transfer and training?

Training and communications are vital to ensure that everyone in theorganisation is committed to the change and understands their role in theprocess. Almost one in 10 companies have their training and communicationsstrategies in place and in action, and a further 18% are progressing with a fullanalysis of their training and communications needs. This analysis helps todetermine the training needs of all staff, as well as business users of IFRSbalances and reports. However, over 70% of companies have not yetundertaken a training needs analysis and have not considered their internalcommunications strategies.

Comment – internal communications and training

IFRS is a change in primary GAAP, which means that everyone in the organisationmust learn a new language, and a new way of working. Training finance staffis crucial, but the training and communications strategy does not stop there.How can senior management or audit committee members make informed,strategic decisions without the appropriate knowledge and understanding?Similarly, staff responsible for reporting financial and operational informationabout individual business units need to understand what is going on and beengaged in the process early.

CFOs reported in the 2002 PricewaterhouseCoopers survey (2005 – Ready ornot) that training was one of the biggest barriers to conversion. It is still one of the toughest issues for companies. A training programme that continuesbeyond publication of the first IFRS financial statements is often needed.

Communicating the impact

Ready to take the plunge? 15

‘If we could start again,I would train earlier.People are stilldiscovering issues a bit late – during the first internal IFRSreporting’Survey participant

‘Training employees is one of the mainobstacles to conversion’Participant, PricewaterhouseCoopers’2002 IFRS survey

Needs analysis not undertaken Analysis under wayStrategies being implemented

9%18%73%

Training and communications progress

Number of participants: 310

‘One company found its return on investment

appeared to have fallen from 16% to 3%

under IFRS’PricewaterhouseCoopers

How are companies communicating with the markets about IFRS reporting differences?

A fifth of companies have already determined how they will communicatechanges under IFRS to the markets. The remaining 80% have yet to determinetheir strategies. This is not surprising, given the proportion of companies thathave yet to complete their assessment of how IFRS will impact on theirbusiness (page 13).

Comment – external reporting

Reporting IFRS information internally and externally to the markets does notbegin with publishing 2005 annual financial statements – it should have startedalready (see opposite). As early as the 2003 financial statements, the Committeeof European Securities Regulators (CESR) recommended that companies give anarrative description of how they intend to carry out the transition to IFRS, theirdegree of achievement so far and key differences in accounting methods fromprevious GAAP. Banks and other stakeholders are also expecting companies todiscuss the impact of IFRS on covenants and ratios sooner rather than later.

IFRS-compliant data needs to be prepared internally this year. This must bereported externally as comparative information in the 2005 financial statements.Some are choosing to report it externally this year.

By the end of 2004, the question on all analysts’ lips will be: how does IFRSaffect your numbers? Companies will need to involve investor relations staffearly and have a clear picture of what the main impacts are before they cananswer analysts with confidence. Without a clear IFRS external communicationsstrategy, companies risk surprising the market and damaging the share price.

Recent changes to IFRS have been significant, so even existing IFRS reportersare having to think again about how to deal with the latest changes andcommunicate their impact to the market.

16 Ready to take the plunge?

Communicating the impact

‘In our quarterly reporting this year we are telling themarkets about the impact of IFRS results with exactamounts. We also explain the effects of IFRS on revenuerecognition, research and development expenses, and capital leases, and the impact on first quarter results, with exact amounts’

Survey participant, listed European company

Some companies, such as the ones below, recognise theimportance of communicating progress on IFRS externally:

IFRS narrative in Lloyds TSB’s 2003 financial statements

‘A significant amount of work has already been performed to prepare for thetransition to international accounting standards. Detailed analyses have beenperformed within each of the Lloyds TSB Group’s principal businesses toidentify those areas where changes to existing accounting practice will berequired and plans developed to make amendments to the systems andprocesses to address the revised requirements.

The international accounting standards likely to have the most significant effectare… IAS 32…and IAS 39…. Implementation of these standards will result in changes to the way in which many of the transactions entered into by theLloyds TSB Group are accounted for and presented in the balance sheet. In particular, these standards will require a much wider use of fair values withinthe financial statements which is likely to result in greater volatility in bothearnings and shareholders’ equity…’

Volkswagen case studyPriority: clear and timely communications to the market

When Volkswagen moved to IFRS in 2002, it found that the capitalisation of development costs under IFRS (prohibited under German GAAP) had animpact of €4bn on its equity position.

Communications with stakeholders were a priority during Volkswagen’sconversion, to ensure that they were not surprised by the results andunderstood the reasons for key differences under IFRS. Workshops wereheld for analysts to explain the expected changes, and preliminary IFRS data for profits before tax were included in its 2001 quarterly reports, theyear before full IFRS reporting.

Communicating the impact

Ready to take the plunge? 17

‘We need to find a smart way tocommunicate whatwe did, why we did it and how it worksunder IFRS’Survey participant

Embedding IFRS into the organisationIs IFRS the new ‘business as usual’?

Deciding on accounting policies is a crucial step in successfully implementingIFRS, once the high-level impact analysis has been completed (see page 13). It is only after such decisions have been made that companies can identifyexactly what data needs to be captured. Reporting under IFRS brings significantnew data requirements for most companies, and these have to be addressedand managed consistently across the organisation.

Companies well advanced in their transition to IFRS have found that they needadditional systems functionality to collect this data. Associated processes andinternal controls often need improving to ensure – and demonstrate – that the data is reliable.

18 Ready to take the plunge?

‘Our vision was veryclear: we needed to

have our data-gatheringsystems in place for

1January 2004.We made it’Survey participant

You are forced to streamline your systems,which is healthy for the whole company*Survey participant

Policy, data, systems, processes and controls

What accounting policies will you follow under IFRS?

Companies clearly recognise the accounting policy review as crucial, identifying it as their second most important technical issue. Over three-quarters ofcompanies are already acting on this issue. But almost a quarter have yet tostart working on it, which means that they cannot make progress with the restof their IFRS implementation process.

Embedding IFRS into the organisation

Ready to take the plunge? 19

‘It is the wholeaccounting mindset,the thinking, whichmust change – we have to see thingscompletely differently’Survey participant

‘We have theaccounting policies but we are missing the more practicalinformation anddetailed examples’

Survey participant

0

%

20 40 60 80 100

2 At least for high priority areas

3 IFRS implemented across business units and used for management reporting

1 At least preliminary assessment

% of companies that have reached each stage

11%IFRS embedded3Step 7

10%Internal controls enhanced Step 6

10%Processes in place Step 5

11%Systems adapted2Step 4

26%Missing data identified Step 3

46%Accounting policies decided2Step 2

75%Business impact assessed1 Step 1

Seven-step IFRS embedding process – level of achievement so far

Number of participants: 310

No progress

Decisions made at least in priority areasHigh-level review only

46%

22%

32%

Accounting policy review progress

Number of participants: 310

What are the IFRS data, systems and controls requirements?

Three out of four companies do not yet have a detailed picture of the new data required for IFRS reporting, and of their organisation’s ability to collect that data. Of these, 37% have yet to start on carrying out an assessment, but36% have begun examining data requirements at the highest level. It follows,therefore, that most companies have yet to carry out a preliminary analysis oftheir IT systems requirements under IFRS.

So far, 11% have sourced their data and completed their priority informationsystem enhancements. Of these, 3% are completely ready, which means theyhave: quantified all data requirements; identified system sources for new dataand addressed all data gaps; taken steps to ensure data is consistent andreliable; and introduced additional controls where necessary in order to maintainthe quality of data.

Large companies have made the most progress in this critical area. While theaverage company in the survey has barely completed a high-level analysis of its data and system requirements, the largest companies are already engagedin work on finalising detailed requirements. The results show that the smallestcompanies are the least likely to have made a preliminary assessment.

What are the implications of IFRS for your internal controls?

Given the high proportion of companies that have not yet determined their data and systems needs, it is not surprising that some 71% of companies have not yet taken steps to upgrade their IFRS internal controls. Over half have no additional controls in place yet and have not reviewed their controlenvironment. Even the largest companies in the survey are unlikely to haveundertaken a detailed review of their control environment, although they doscore a little higher than medium and small market capitalisation companies.

IFRS is the new ‘business as usual’, so how will internalmanagement reporting change?

11% of companies have demonstrated that IFRS is being embedded in their organisation by putting detailed plans in place to make the change tomanagement reporting under IFRS (internally) instead of national GAAP. The majority of companies have yet to assess how IFRS will affect the reportsthat management uses to monitor the financial performance of the business.

20 Ready to take the plunge?

Embedding IFRS into the organisation

‘Searching for data from previous periods

was one of the toughestissues – the capacity

to run data from 5 to 10years ago is a big ask’

Survey participant

Comment

Identifying the missing data is the most important thing that companies have to do in the short term. Only by doing this will they be able to work out howthey are going to collect that data. Companies need IFRS data for the whole of 2004 for their 2005 comparatives. In some cases, 2004 data will need to becollected ‘as it happens’: retrieving it retrospectively could be complicated.

It is only when these steps have been taken that companies can generateaudited financial statements for the 2005 financial year and be sure that they willnot surprise the market. The best strategy for providing information of auditablequality is to fully embed IFRS into the company’s everyday systems andprocesses so that IFRS information is generated as part of ‘business as usual’.

This means moving internal management reporting to IFRS as well, becauseIFRS is a change in the primary reporting language. Volkswagen found that itsswitch to IFRS made its reporting system less complex, with the same basis for internal and external reporting.

However, some companies have already recognised that they do not haveenough time before 2005 to embed IFRS fully into their systems. This meansthat their primary source of information will not be IFRS-compliant in the short-term: ‘workaround’ or short-term solutions to produce information for the firstIFRS financial statements must be found while the main strategic implementationproject is still in progress. Experience has shown that these ‘workarounds’ are often labour-intensive and difficult to control without an effective internal control system.

In these cases, companies must take care that their short-term solutions arerobust and acceptable to their auditors. Directors must be satisfied that thecompany’s internal control system, including financial controls, are adequate.Internal audit staff can help ensure that the changes needed to comply withIFRS also meet corporate governance requirements on internal controls. This is particularly important for US reporters facing compliance with theSarbanes-Oxley requirements.

Embedding IFRS into the organisation

Ready to take the plunge? 21

‘Once IFRS is embedded, it becomesthe currency by which all operations in thegroup are measuredand the basis ofincentive arrangements’

Thomas Rabe, CFO at media group RTL

Balancing the key issues*How are technical preparations progressing?

22 Ready to take the plunge?

‘You need expertknowledge of IFRS to

understand how to implement it and

to reflect a true and fair view’

Survey participant

Not started

Revenue recognition

% of companies

Interim reporting

Accounting for deferred tax

Employee benefits

IAS 32 and IAS 39

1

2

3

4

5

6

First time adoption/business combinations

High-level impact complete

Detailed evaluation complete

0 20 40 60 80 100

27% 58%

49%

41%

37%

43%

48%29%

45%

49%

39%

35%

15%

16%

20%

14%

12%

23%

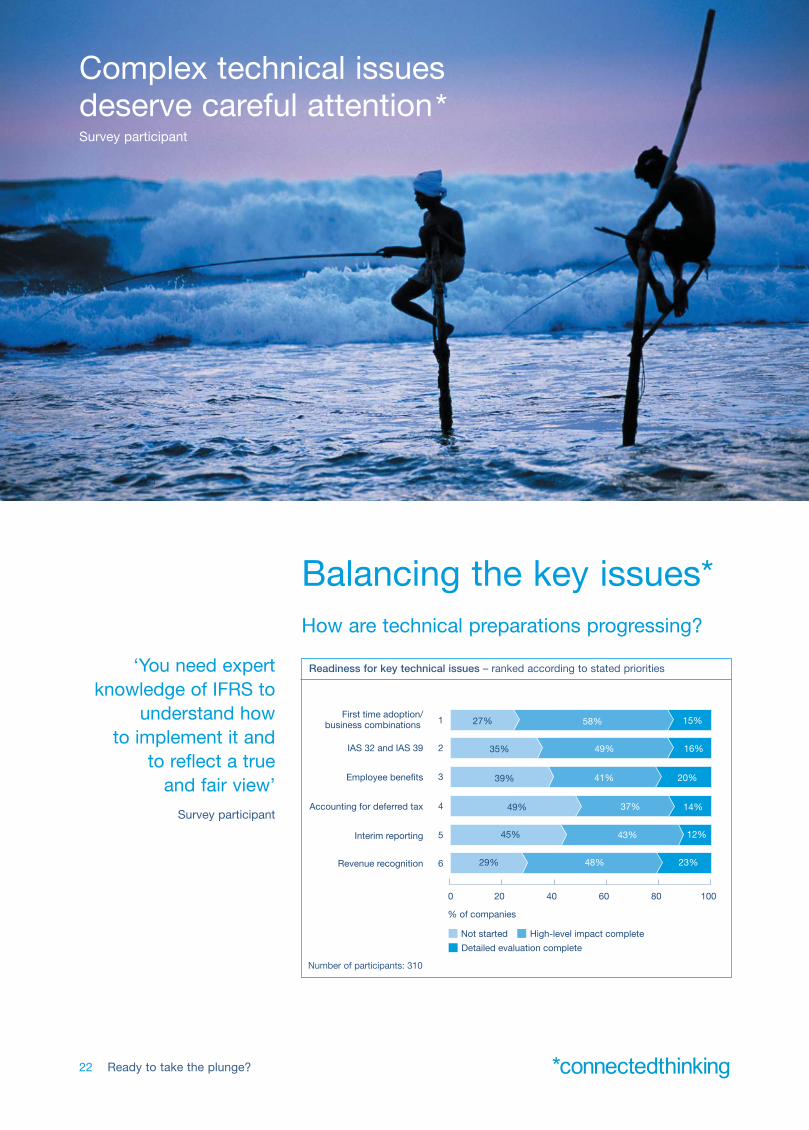

Readiness for key technical issues – ranked according to stated priorities

Number of participants: 310

Complex technical issues deserve careful attention*Survey participant

These issues will affect all companies moving to IFRS to some extent. Most companies have carried out a high-level impact assessment of the IFRS technical issues that are likely to have the most far-reaching practicalimplications in terms of the work required before implementation. However, up to half of companies have yet to address these issues at all. The vastmajority have significant work left to do to complete their detailed evaluationsand implement policies on these issues.

Large companies are more advanced in their investigation of all the keytechnical issues highlighted in the bar chart (left). The gap between thereadiness of large companies (worth over €10bn) and the rest is most notablefor tax, IAS 32 and IAS 39, and interim reporting.

First-time adoption of IFRS: top-priority issue

Companies rate IFRS 1, First-time Adoption, as the most important of the sixissues highlighted. Almost three quarters have already taken action on thisissue. However, around 25% have yet to make a move. This may be becausecompanies found it difficult to decide which options in IFRS 1 to adopt beforethe final platform of standards for 2005 was completed (31 March 2004).Companies considering the restatement of old mergers under IFRS 1, forexample, may have waited for the final business combinations standard (IFRS 3) before making a decision.

Most companies will want to establish their new accounting policies underIFRS before making decisions about which of the IFRS 1 options to adopt. So far, almost half (46%) of companies have made decisions about the policiesto be adopted (see page 19).

Financial instruments under IFRS: markets will watch closely

Accounting and disclosure for financial instruments (IAS 32 and 39) is an issue that the markets are expected to be particularly interested in. Two thirdsof companies have made a preliminary assessment in these areas. In the caseof accounting for derivatives, the lack of action from the remaining third may be due, partly, to the fact that the revised financial instruments standards were published relatively recently, just before the beginning of 2004. 60% ofcompanies clearly see it as an important issue, rating it as a high or mediumpriority. Indeed, the implications of IAS 39’s impact on risk managementstrategies and the possible volatility in earnings arising from this standard are quite significant, even for non-financial services companies.

Revenue recognition: reasonable progress

Half of respondents place revenue recognition (IAS 18) high on their list of IFRSpriorities. This may be rated as a slightly lower priority than some other issuesbecause progress in this area is slightly ahead: 71% of companies have at least analysed the high-level impacts.

Balancing the key issues

Ready to take the plunge? 23

‘Markets are highlysensitive to changes in revenue recognition –this issue warrants more attention than it’s getting’PricewaterhouseCoopers

‘The two keydeterminants of ourprofit are both affectedby IAS 39’Survey participant

Employee benefits schemes: tough issues

Accounting for employee benefits is a high or medium priority for 59% of companies. This area is a particular challenge for companies that havepension schemes based on final salaries, and for senior executives’ share-option awards that contain individual performance criteria.

IFRS 2 is expected to highlight important differences between companies.Today, earnings look the same for companies that use share options extensivelyand those that do not. In future, these costs will show in the income statement.

Companies’ first concern will be to understand the scope of the standard anddetermine data requirements. After that, companies will have to explain anynew charges in the income statement to the outside world.

Deferred tax accounting: few prepared

Accounting for deferred tax has attracted the attention of half the companiessurveyed, roughly the same percentage as those that attached medium or high importance to this topic. Some companies may be delaying examinationof deferred tax because they are accustomed to treating the tax calculation asthe final piece of the accounting puzzle, since it depends on having many ofthe other numbers in place. However, experience has shown that this is a bigissue that many companies struggle with. Training is often needed to providethe right level of understanding for staff to tackle deferred tax.

Interim reporting: lower priority

Similarly, companies have made less progress on preparing for 2005 interimreporting than for other issues. This may be because they are focused on the IFRS deadlines that they must meet beforehand. The 2004 IFRS openingbalance sheet, for example, will be needed first to provide a definitive startingposition for interims. CESR has also recommended that companies publish this balance sheet alongside their 2004 national GAAP financial statements and provide an explanation of reconciling items.

The most prepared companies are already producing monthly or quarterly IFRS information, at least internally, for the 2004 comparatives that will beincluded in the 2005 interims and annual accounts.

It is not yet clear in some countries whether or not companies will be requiredto produce IFRS interim financial statements in 2005. However, even whereIFRS interims are not mandatory, many are expected to publish them anyway to prepare the markets for their IFRS annual financial statements anddemonstrate their preparedness for the new reporting regime.

24 Ready to take the plunge?

Balancing the key issues

‘It is a big deal to be accounting

for deferred tax for the first time’

Survey participant

Readiness for key technical issues that do not apply to all companies, but are important for those they do affect:

Special purpose entities and derecognition: market hot topic

High-profile corporate failures involvingspecial purpose entities (SPEs) havemade this a very hot topic for themarkets. IFRS requirements could havea very significant impact on results forcompanies with SPEs that have neverbeen consolidated under national GAAP.For example, one company is predictingthat when an SPE is brought onto thebalance sheet for the first time underIFRS, its balance sheet total will double.

The survey shows that this is a toppriority issue for 5% of companies. These companies will need to plantheir communications to the marketscarefully. The arrival of SPEs on the

balance sheet for the first time is one of the IFRS issues most likely to triggerthe interest of analysts and investors and could impact on the share price,especially if it comes as a surprise.

Foreign entities: will records be in a new currency?

IFRS transition is much morecomplicated for companies that havemany foreign entities. However, almost30% of companies with foreign entities have not started to assess the impactof IFRS on their ‘functional’ currencies.Under IFRS, entities must use the‘functional’ currency of their operations,which could result in some of themhaving to change the currency in which they record all their transactions.The big question for companies toconsider is whether they have thesystems and processes in place to measure transactions and keep records in an entirely new currency.

Balancing the key issues

Ready to take the plunge? 25

‘We took everythingthat we could fromIFRS to use in ournational accounting in 2004’Survey participant

Not applicable

High-level impact complete Detailed evaluation complete

Not started

14% 20%

29%37%

Foreign entities’ progress

Number of participants: 310

Not applicable

High-level impact complete Detailed evaluation complete

Not started

11%

47%

20%

22%

Derecognition and SPEs progress

Number of participants: 310

Segment reporting: new concept for some

Segment reporting under IFRS isrequired both for lines of business andgeographies – for some countries(including France and the Netherlands) this is a completely new concept. The disclosures are often much moreonerous than under national GAAP.

Companies will need to establishquickly the systems enhancementsneeded to collect any information that is not already gathered formanagement reporting.

Some of the most prepared companiesreport that this raises tough issues for them because they will be revealinginformation that was traditionally not

disclosed to the markets, and thus competitors. If certain segments are notprofit-making, for example, this will be visible to the markets under IFRS andexplanations will be expected. IFRS segment reporting may also result inimpairment charges.

Acquisitions: new approach under IFRS?

Most companies have not examined the impact of IFRS on future acquisitionsactivity. 17% of companies are however taking steps to understand thepossible effects on post-acquisition earnings. Companies making acquisitionsin 2004 will have to account for them under IFRS 3, so this is an issue theyneed to think about now. The exemption in IFRS 1, First-time Adoption, onlyapplies to acquisitions undertaken before the transition date (1 January 2004).

Under IFRS 3, the success of acquisitions will be more transparent because of the requirement to identify and subsequently track many intangible assetsand to test goodwill for impairment each year. Management must understandthe implications of the new standard before undertaking any acquisitions,because it will affect the way these transactions are accounted for and howthey need to be explained to the market.

26 Ready to take the plunge?

Balancing the key issues

RTL case study

Under IFRS the appraisal of acquisitions has been subjectto greater scrutiny and rigour by management, which led to a non-cash goodwill write-off of €2.4 billion.

Not applicable

High-level impact complete Detailed evaluation complete

Not started

24%27%

4%

45%

Segment reporting progress

Number of participants: 310

‘For us, secondarysegment informationhas been the biggest

headache – with the biggest implications

for systems’Survey participant

‘Segment reporting willimprove subsidiaries’

efficiency because theirprofitability will be

seen externally for thefirst time’

Survey participant

This is a major project...start work urgently*

Survey participant

ChecklistWhat action can the board take?

The results of this survey show that although some progress has been made,the vast majority of companies have a lot to do to get ready. This is consistentwith the findings of previous PricewaterhouseCoopers research on this subject,which showed that some companies may be underestimating the challenge ofmaking the change to IFRS. For those companies yet to start or in the early stagesof their IFRS transition project, the following points are particularly relevant:

Boards and audit committees

The board has ultimate responsibility for ensuring a successful and sustainabletransition to IFRS. It must understand the key risks associated with getting thefinancial data right and communicating the impact to the market on a timelybasis to maintain shareholder value. The audit committee has a vital role to play here on the board’s behalf.

• Audit committee members must understand how the change to IFRS willaffect the company’s reported results. They should ensure that they havereceived a high-level assessment of the key impacts as soon as possible.

• The audit committee must be satisfied that the company is on course tomake the transition to IFRS in good time and in a way that ensures itscontinuing ability to produce reliable financial information. Practically, thismeans ensuring that the right IFRS project structures are established and that regular feedback to the project steering group is maintained. Particularattention should be given to management’s plans to address more complexareas, such as financial instruments, goodwill and deferred tax.

• Regular communication with external auditors is a key role for the auditcommittee. In the context of IFRS transition, discussions should now be takingplace about developments in the company’s accounting policies, controlenvironment and other key influences on the overall quality of the company’sfinancial reporting.

• The audit committee will need to approve the IFRS accounting policies(including the options in IFRS 1 that are selected) and sign off on any IFRSinformation that is to be published.

Ready to take the plunge? 27

‘Transition to IFRS is a good way to checkthat we are doingthings in the best wayfor our business’Survey participant

Management

• For companies that have not made much progress to date, management will need to take action fast and ensure that there is a steering group in placewith overall responsibility for the IFRS transition project. Top management mustback the IFRS project so that it is recognised as a high priority for every part of the business.

• Resource allocations should reflect the importance of the change. Training in IFRS should extend to managers outside the finance function and shouldinclude executive and non-executive directors.

• Management must understand what IFRS will mean for the company’s key data and ratios and the impact on strategic business decisions. For example, it should be aware of the IFRS impact on: bonus and reward schemes,treasury operations, tax liabilities and debt covenants.

• Management has a key responsibility for helping the market to understand inadvance any changes to company results under IFRS. The timing and extent of communications to the market will need careful planning to manage theirexpectations and ensure that interim information does not mislead. Analystslooking for guidance on 2005 data will expect to hear about the likely effects of IFRS.

• Management should take the opportunity to make IFRS the basis of internalmanagement reporting so that the changeover is part of a new ‘business as usual’.

• Management should ensure that there is consistency and efficiency in the way the company sets about meeting various reporting requirements.SEC registrants based in Europe, for example, have to implement the USSarbanes-Oxley requirements as well as IFRS.

• Management should ensure that all the new practices under IFRS meet theapplicable corporate governance codes.

Chief Financial Officers

• As the leader of the company’s IFRS transition (in most cases), the CFO will oversee the whole transition process, including changing the financialdata, changing the processes, and training the people.

• The CFO must ensure that key deadlines are met and oversee communicationsthroughout the business so that the whole company and all its stakeholdersunderstand the implications of the changeover, not just those in the centralfinance function.

• The CFO must make sure the new financial reporting process is robust andruns as smoothly as possible, within the usual reporting timetable.

28 Ready to take the plunge?

Checklist

‘Our CFO was veryclear that changing toIFRS is not something

you can do as anafterthought – he

kicked off the project16 months ago’

Survey participant

IFRS products and servicesPricewaterhouseCoopers has a range of tools, publications and industry experience to help companiesapply IFRS. For further advice on how we can help you make the change to IFRS, please contact yournational IFRS conversion leader (see inside front cover) or your local office.

IFRS Readiness QuestionnaireThe IFRS Readiness Questionnaire enables you to assessyour IFRS readiness with PricewaterhouseCoopers. Thefeedback highlights areas that need further attention andenables you to benchmark your company’s progress againstthe aggregate results of companies across Europe.

For further information contact your national IFRSconversion leader (see inside front cover).

Applying IFRSApplying IFRS is PwC’s authoritative guidance on theinterpretation and application of IFRS. The interactive toolincludes links to over 1,000 real-life solutions, as well as directlinks to applicable text in the IFRS standards and interpretations.

Applying IFRS is available on our electronic research tool,Comperio IFRS. To order see www.pwc.com/ifrs

P2P IAS – from principle to practiceP2P IAS is PwC’s interactive electronic learning solution. Users build their knowledge easily and conveniently with 21 hours of learning in 34 interactive modules.

For further information, network licence prices ordemonstrations, send an email to:[email protected]

TransitionIFRS e-PlatformThe TransitionIFRS e-Platform is an integral part of the PwC TransitionIFRS service offering. It is a web-basedcommunication platform from which you can launch andcontrol your IFRS conversion project. It enables you to workcollaboratively with your advisers, access support andguidance and transfer knowledge within your organisation.

For further information contact implementation [email protected].

IFRS NewsIFRS News is a monthly newsletter focusing on the businessimplications of IASB proposals and new standards.

Copies are available free on the websitewww.pwc.com/ifrs. For further information, send an emailto the editor: [email protected]

World WatchWorld Watch magazine contains opinion articles, case studiesand worldwide news on IFRS, governance and other initiativesto improve corporate reporting.

Copies are available free on the websitewww.pwc.com/ifrs. For hard copies and furtherinformation, send an email to the editor:[email protected]

www.pwc.com/ifrs