international lpg supply and demand trends aegpl … · international lpg supply and demand trends...

TRANSCRIPT

London

Houston

Washington

New York

Portland

Calgary

Santiago

Bogota

Rio de Janeiro

Singapore

Beijing

Tokyo

Sydney

Dubai

Moscow

Astana

Kiev

Porto

Johannesburg

Market Reporting

Consulting

Events

International LPG supply and demand trends AEGPL 2015 Nick Black Principal, LPG Argus Consultancy Services Argus Media

illuminating the markets

Argus Consultancy Services analyses global LPG trends…

Copyright © 2015 Argus Media Ltd. All rights reserved.

illuminating the markets

Argus Consultancy Services includes LPG outlook and forecasting

Copyright © 2015 Argus Media Ltd. All rights reserved.

Argus LPG Outlook: Quarterly supply and demand trends Monthly price trends Global and regional balances

illuminating the markets

International LPG supply and demand trends

Copyright © 2015 Argus Media Ltd. All rights reserved.

• 6 signs of strain • Global Trends and anomalies • US • Europe • Asia-Pacific & Middle East • Shipping

illuminating the markets

Signs of strain

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Production outstrips consumption • Infrastructural Strains and stresses • Unusual price relationships

• Between regions • Between products

• Demand not conforming to forecast patterns • Government commitments not as strong as hoped • Shipping

• VLGC expansion, LGC boom times • Different story for pressurised

Market Reporting

Consulting

Events

Global trends and anomalies

US supply has found international buyers

Copyright © 2015 Argus Media Ltd. All rights reserved.

US Export Strength pre-Panama Canal

Latin America soaked up US exports in 2013 and 2014

2013/4: US Gulf Terminal expansion Enterprise: 7.8mn t/yr Targa: 2.1 t/yr Nederlands in January

Europe Petchems began sustained US imports in 2013. Some quality issues at first. Europe+ Med imports 2.7mn t/yr US LPG in 2014 Europe exports to US Northeast in Q1 2014 and 2015

Meanwhile, Russia exports keep growing

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Ust Luga starts up 2013, petchems are mostly the buyers

• Product moves to Ust Luga in 2014 rather than Black Sea

• Russia ports of Taman, Temyruk favoured over Kerch (Crimea): political troubles not over yet

• Sibur makes 73pc of all Russia exports

Asia import patterns have shifted again

Copyright © 2015 Argus Media Ltd. All rights reserved.

China imports rose strongly in 2013 and even more strongly in 2014: Over 7mn t/yr (+68pc yr-on-yr) 2015 import rise continues

US exports head to east Asia before Panama Canal upgrade

Thai imports continue to grow

Japan imports fall in 2014: 10.9mn t/yr (-3pc) Meti forecasts autogas decline, robust household

India imports become a significant influence

“The dog that did not bark”: some anomalies

Copyright © 2015 Argus Media Ltd. All rights reserved.

How have Middle East exporters responded to a threat to their market share of Asian customer base? Why would Asia buyers buy US supply even when arb collapses?

Where is the promised rise in Algerian exports? They are showing up

If the US is such a key exporter, why did it import from Europe in Q1 2013 and 2014?

What happened in Angola when exports were supposed to rise in 2013?

Focus on US has distracted market from the narratives of other key exporters

Market Reporting

Consulting

Events

US trends

Production will outstrip export growth

Copyright © 2015 Argus Media Ltd. All rights reserved.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US NGL production actual + forecast

Gas processing Refinery

0

20,000

40,000

60,000

80,000

100,000

120,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US output and exports

Total NGL supply US exports Propane Butane Ethane

• Output will rise strongly

• Shale Gas fields still mostly economic at $50/bl oil

• Gas processing is still key source for US NGL output

• Ethane dominates supply growth

• Ethane can be rejected, LPG cannot

• Ethane rejection was about 5.6mn t/yr and could be as much as 8.6 mn t/yr by 2016

• Ethane exports on the way

Arbitrage is not as it was, while US stocks build

Copyright © 2015 Argus Media Ltd. All rights reserved.

$600/t… Asia buyers excited!

US northeast big freeze

Arb settles to range limit of $300/t

Arb range limit now $200/t

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

C3

/nap

hth

a ra

tio

US

C3

sto

cks

5yr average 2013 2014

2015 C3/naphtha ratio

• Arbitrage drove Asian term deals

• “Glory days” over since 2012

• US winter if cold will always close arb

• US stocks way above 5 year average

• Where will it be stored?

• Brine issues

• US floating storage not an option, unlike crude

• Houston Ship Channel:

◦ Disruptions once again in March (Fog, Collision of Carla Maersk)

• Rapid build up: vessel logjams

• 40 inbound and 32 outbound vessels

• Pacific West Coast:

◦ Pembina runs into pipeline battle

◦ Haven Longview project rejected by port commissioners

• 1.4mn t/yr

• 11 days to East Asia

• Rail:

◦ US rail traffic up 10pc in Q4 2014, highest for 5 years

◦ Rail yards face overcrowding

• Arbitrage:

◦ This is getting squeezed

◦ Terminalling Fee needs to be factored in

◦ Freight rate strength is not always even

US export logistics get more complex

Copyright © 2015 Argus Media Ltd. All rights reserved.

Market Reporting

Consulting

Events

European trends

FRANCE

ANDORRA

GERMANY

POLAND

ROMANIA

BULGARIA

GREECE

TURKEY

BALEARIC

SWITZ.

AUSTRIA

UKRAINE

Crete

Rhodes

Andorra

Rome

Athens

Bucharest

Budapest

Bratislava

Prague

Chisinau

Kiev

Krakow

Rivne

Barcelona

Balearic

Ionian

Sea

Black

Sea

Adriatic

Sea

Ligurian Sea

Mediterranean Sea

Odesa

Palermo

Cagliari

Genoa

Geneva

Naples

ALGERIA

ALB.

TUNISIA

ISLANDS

BELGIUM

LUX.

SERBIA

LIECH

Sicily

Paris

Bern

Tirana

Sofia

Belgrade

Sarajevo

Zagreb

Berlin

Brussels

Sea

Sea

Munich

Leipzig

RUSSIA

RUSSIA

FINLAND

SWEDEN

NETHERLANDS

ISLANDS

ALAND

ISLANDS

DENMARK

ICELAND

BELARUS

UNITED

KINGDOM

Gotland

Oland

Bornholm

Minsk

Riga

Helsinki

Moscow

Stockholm Oslo

Copenhagen

Amsterdam

Luxembourg

London

Doublin

Reykjavik

Murmansk

Gulf of Finland

White Sea

Barents Sea

Gulf

of

Bothnia

Baltic

Sea

Irish

Bay of

Biscay

North

Sea

Norwegian

Sea

Leeds

Bordeaux Lyon

Stavanger

Strasbourg

Bremen

Hamburg

Kaliningrad

Belfast

Goteborg

SPAIN

MOROCCO

NORWAY

MOLDOVA

F.Y.R.O.M.

IRELAND

PORTUGAL

MALTA

ITALY MONACO

BOSNIA AND

HERZEGOVINA

SLOVENIA

HUNGARY

SLOVAKIA CZECH REPUBLIC

NORTHERN

IRELAND

FAROEF

LITHUANIA

LATVIA

ESTONIA

Corsica FRANCE

Sardinia I TALY

La Vella

Madrid

Lisbon

Rabat

Algiers

Tunis Valletta

Vaduz

Podgorica

Pristina

Skopje

CROATIA

Ljubljana

Vienna

Vilnius

Warsaw

Tallin

Brest

MONTENEGRO KOSOVO

Lake Ladoga

Sea

Alborin Sea

Tyrrhenian

Edinburgh

Marseille

Sevilla

Gibralta

Valencia

Gdansk

St. Petersburg

Venice

Porto

Le Havre

Donges

• US imports now a fact of life • Ust Luga heads to petchems • German/Poland rail link changes • Turkey eases Algeria dependence • Algeria fine-tunes pricing • ARA rail car displacement • Ukraine/Russia and Black Sea issues

Europe Trade Flow changes

Copyright © 2015 Argus Media Ltd. All rights reserved.

2.7mn t of US exports to

Europe in 2014, 2mn t to NWE

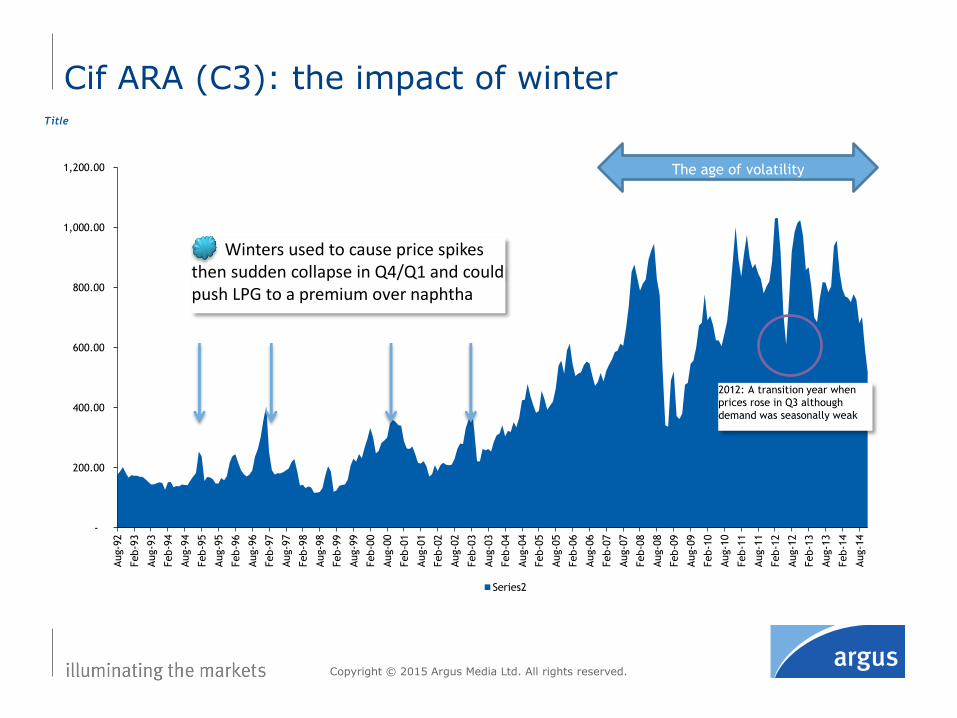

Cif ARA (C3): the impact of winter

Copyright © 2015 Argus Media Ltd. All rights reserved.

-

200.00

400.00

600.00

800.00

1,000.00

1,200.00

Aug-9

2

Feb-9

3

Aug-9

3

Feb-9

4

Aug-9

4

Feb-9

5

Aug-9

5

Feb-9

6

Aug-9

6

Feb-9

7

Aug-9

7

Feb-9

8

Aug-9

8

Feb-9

9

Aug-9

9

Feb-0

0

Aug-0

0

Feb-0

1

Aug-0

1

Feb-0

2

Aug-0

2

Feb-0

3

Aug-0

3

Feb-0

4

Aug-0

4

Feb-0

5

Aug-0

5

Feb-0

6

Aug-0

6

Feb-0

7

Aug-0

7

Feb-0

8

Aug-0

8

Feb-0

9

Aug-0

9

Feb-1

0

Aug-1

0

Feb-1

1

Aug-1

1

Feb-1

2

Aug-1

2

Feb-1

3

Aug-1

3

Feb-1

4

Aug-1

4

Title

Series2

2012: A transition year when

prices rose in Q3 although

demand was seasonally weak

The age of volatility

Winters used to cause price spikes then sudden collapse in Q4/Q1 and could push LPG to a premium over naphtha

Europe: winter has greater effect on spot prices than overall demand

Copyright © 2015 Argus Media Ltd. All rights reserved.

Winter Q1 Winter Q4

Cold winter Mild winter

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2000 2010 2011 2012 2013

Chemical

Refinery

Transport

Industry

Agriculture

Residential

Note unusual consumption mix for Europe. Domestic demand is not dominant

• Old rules

• Propane rises above naphtha when cold weather winter demand kicks in

• C3 falls to 95pc of naphtha or below in Q2 or Q3

• New rules

• C3/4/Naph volatility less extreme

• Pro establishes new range of value to naphtha

• Even if C3 at advantage, petchems not necessarily buyers

Europe looks at naphtha, but the rules change

Copyright © 2015 Argus Media Ltd. All rights reserved.

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Jan-9

3

Jul-

93

Jan-9

4

Jul-

94

Jan-9

5

Jul-

95

Jan-9

6

Jul-

96

Jan-9

7

Jul-

97

Jan-9

8

Jul-

98

Jan-9

9

Jul-

99

Jan-0

0

Jul-

00

Jan-0

1

Jul-

01

Jan-0

2

Jul-

02

Jan-0

3

Jul-

03

Jan-0

4

Jul-

04

Jan-0

5

Jul-

05

Jan-0

6

Jul-

06

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

Jul-

14

Title

Series2

Sustained

Petchem

Winters used to push LPG to a sharp premium over naphtha

• Butane emerges stronger • Propane below 80pc crude in

April • Winter demand lacklustre

• Petchem buying is key • Petchem demand is main spot

market support and dominant in market discussion, but do not want leadership

• When petchems donm’t buy, prices tumble

• US imports now a fact of life • Even as far as Gdansk, Baltic Sea

in 2014 • Quality issues for petchems:

different specs Targa/Enterprise • Q1 sees US supply head to

Asia/Lat Am not Europe • Q2 seeing similar pattern

• Exports to US northeast • Consequence of last year’s US

winter

• Butane length in ARA • Moerdijk problems takes up to

40,000t/month away from demand

European market: recent developments

Copyright © 2015 Argus Media Ltd. All rights reserved.

Propane diff to Naphtha NWE

Propane and Butane cif ARA

This is odd

European market: looking ahead

Copyright © 2015 Argus Media Ltd. All rights reserved.

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014 2015 2016

Northwest Europe production and imports

Total NWE NGL supply NGL imports Ethane LPG

• Steady supply

• Northwest Europe (esp Norway) is a key source of supply but production is steady, not growing

• Russia production set to rise to over 17mn t/yr by 2018 and export just under 9mn t/yr. where will it go?

• Europe now produces around 2.4mn t/yr ethane

• US ethane imports start to show this year

• Why imports?

• Two different markets, large/coasters

• Notice growth of imports despite flat demand

• Import growth down to petchems

Ethane imports begin in 2015

Market Reporting

Consulting

Events

Asian and Middle East trends

• China imports

• Resurgent imports

• Nov 2014 record 758,000t

• 2014 68pc higher than 2013 (7.1mn t)

• PDH demand already active, centred in east China

• East China imports up by 78pc

• But also big rise in S China imports

• Competitive international prices vs refinery prices

• US sourced imports up by 600pc

• 773,000t and now 2nd largest source, after UAE and above Qatar, Kuwait, Saudi Arabia

Asia market: import patterns are still shifting

Copyright © 2015 Argus Media Ltd. All rights reserved.

China LPG demand & imports

0

5

10

15

20

25

30

2011 2012 2013 2014

Demand Imports

0

1

2

3

4

5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

S China E China

China: E Coast vs S Coast imports The increase in E China demand (PDH) is being matched by S China demand

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

05 06 07 08 09 10 11 12 13 14

China Middle East Imports

UAE Qatar Saudi Arabia Kuwait Iran Bahrain

• Japan imports

• US has not broken Middle East dominance

• Saudi imports dwindle – or do they?

• No Saudi imports in April, but recover by June

• US sourced imports

• 1.4mn t 2014

• Even before Panama Canal

• But buying is erratic

• They are still cheaper!

Why is Japan buying more US LPG?

Copyright © 2015 Argus Media Ltd. All rights reserved.

Japan import costs 2014 ’000Y/t

0

50

100

150

200

250

300

350

400

Jan Feb Mar April May Jun Jul Aug Sept Oct Nov Dec

Saudi Qatar US

84

86

88

90

92

94

96

98

Saudi Arabia Kuwait Qatar UAE USC3 C4

Japan imports from Saudi, US, Qatar 2014 ’000t

1,319,565

3,078,266

1,267,733

2,515,051

0 772,250

1,487,242

516,507

Saudi Arabia

Qatar

Kuwait

UAE

Iran

Australia

US

Others

Japan import share 2014

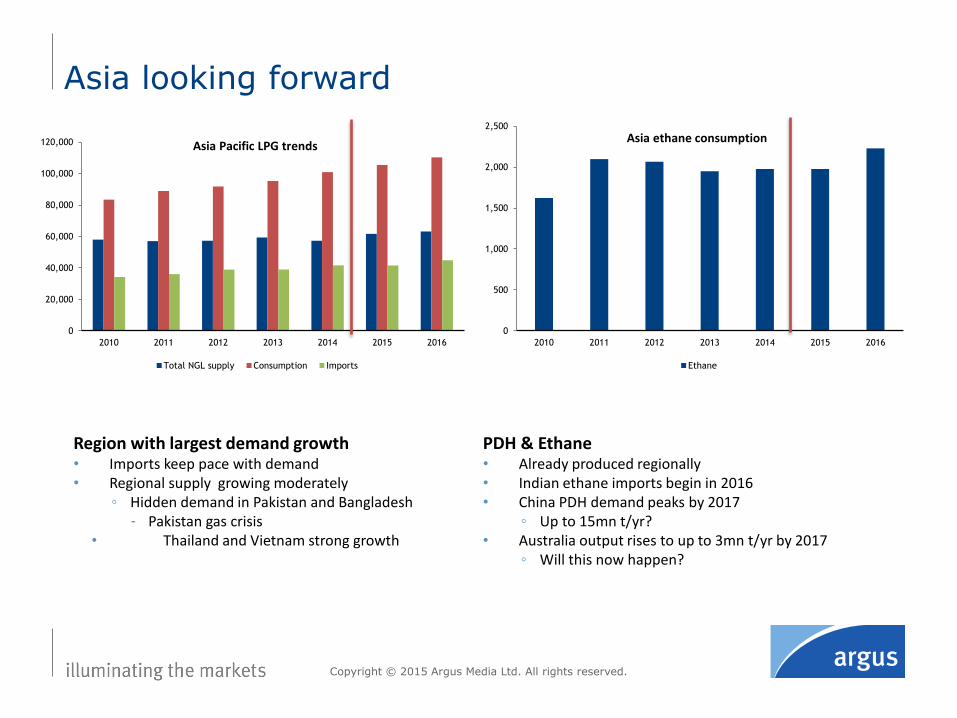

Asia looking forward

Copyright © 2015 Argus Media Ltd. All rights reserved.

0

20,000

40,000

60,000

80,000

100,000

120,000

2010 2011 2012 2013 2014 2015 2016

Asia Pacific LPG trends

Total NGL supply Consumption Imports

Region with largest demand growth • Imports keep pace with demand • Regional supply growing moderately

◦ Hidden demand in Pakistan and Bangladesh ‐ Pakistan gas crisis

• Thailand and Vietnam strong growth

PDH & Ethane • Already produced regionally • Indian ethane imports begin in 2016 • China PDH demand peaks by 2017

◦ Up to 15mn t/yr? • Australia output rises to up to 3mn t/yr by 2017

◦ Will this now happen?

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 2015 2016

Asia ethane consumption

Ethane

0

20,000

40,000

60,000

80,000

100,000

120,000

2010 2011 2012 2013 2014 2015 2016

Middle East supply/demand

NGL production Exports Consumption Ethane Supply

Middle East looking forward

Copyright © 2015 Argus Media Ltd. All rights reserved.

Production Growth • Modest rises • Unknowns:

◦ Iran (subject to sanctions) ◦ Iraq

• Qatar production will level off in 2016, then recover in 2017

Demand • Rise in Qatari petchem demand • Unknowns:

◦ Stronger than anticipated domestic cylinder demand in Saudi Arabia and UAE

Market Reporting

Consulting

Events

Shipping

0

5

10

15

20

25

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

%/yr

0

20

40

60

80

100

North Pacific China India Other Asia Pacific

via Cape via Panama

• Shipping rates • Record levels in 2014. Repeatable? • VLGC fleet: 34 new vessels in 2015, 46 in 2016 • What happens when capacity outstrips US

production?

• US exports • Will terminals be built given oil price crash? And

who will buy exports?

• Panama Canal • Will start as promised in 2016? • Tolls agreed Jan 2015 on sliding scale • Widened and deepened, but still depends on vol

of traffic and likely demurrage costs • Can it handle the volume of LPG exports?

• Other vessels will have priority

Shipping rates reflect high utilisation: can it last?

Copyright © 2015 Argus Media Ltd. All rights reserved.

VLGC Fleet growth Ras Tanura/Chiba VLGC rate

Voyage days (RV) to Houston (14 knots)

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

01/13

02/13

03/13

04/13

05/13

06/13

07/13

08/13

09/13

10/13

11/13

12/13

01/14

02/14

03/14

04/14

05/14

06/14

07/14

08/14

09/14

10/14

11/14

12/14

01/15

02/15

03/15

S/t

Copyright notice Copyright © 2015 Argus Media Ltd. All rights reserved. All intellectual property rights in this presentation and the information herein are the exclusive property of Argus and and/or its licensors and may only be used under licence from Argus. Without limiting the foregoing, by reading this presentation you agree that you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatsoever without the prior written consent of Argus. Trademark notice ARGUS, ARGUS MEDIA, the ARGUS logo, DEWITT, FMB, FUNDALYTICS, METAL-PAGES, JIM JORDAN & ASSOCIATES, JJ&A, ARGUS publication titles and ARGUS index names are trademarks of Argus Media Limited. Disclaimer All data and other information presented (the “Data”) are provided on an “as is” basis. Argus makes no warranties, express or implied, as to the accuracy, adequacy, timeliness, or completeness of the Data or fitness for any particular purpose. Argus shall not be liable for any loss or damage arising from any party’s reliance on the Data and disclaims any and all liability related to or arising out of use of the Data to the full extent permissible by law.

Nick Black Principal, LPG

Email:

Phone:

Office:

Web:

+44 20 7780 4200

London

www.argusmedia.com