international reinsurance pricing and challenges casualty actuarial society seminar on ratemaking...

TRANSCRIPT

International Reinsurance Pricing and Challenges

Casualty Actuarial Society

Seminar on Ratemaking

March 9 - 10, 2000

Agenda

EQECAT Overview Catastrophe Modeling Overview Pricing and Challenges

— Exposure Data Cresta level information Limited, if any, structural information

— Modeling Data Varies from Country to Country Soil Information Terrain Information Building Vulnerabilities Frequency & Severity of events

EQECAT

Leading provider of Consulting Services and Catastrophe Modeling Software to the Insurance Industry and Financial Community

EQECAT was founded in 1994 and is a wholly owned subsidiary of EQE International.

Headquartered in Oakland

Other offices in Irvine, Philadelphia, Boston, London, Paris, Sydney and Tokyo

Note: EQE has been providing Software and Consulting Services to the Insurance Industry since

1986.

Top U.S. Risk Management Consultants

1. PricewaterhouseCoopers$60,840,000 2,645209

2. Arthur Andersen $54,647,759 861198

3. Deloitte & Touche L.L.P.$54,300,000 1,000334

4. EQE INTERNATIONAL $42,300,000 1,100250

5. Ernst & Young L.L.P. $31,038,000 900170

6. Tillinghast-Towers Perrin$28,356,000 85071

1998 Total Risk Mgmt.Company Revenues Clients Professionals

Reference: Business Insurance, February 1999

(Ranked by risk management consulting services)

EQECAT

Over 45 companies license EQECAT’s software— Primary Insurance Companies — Reinsurance Companies— Global Insurers (Non-US)— Brokers and Financial Institutions

EQECAT has worked with over 100 insurance companies on a consulting basis— Portfolio Analysis— Pricing and Product Analysis— Education & Training— Claims & Loss Control Support— Securitization

Securitization Experience

California Earthquake Authority (1996) SR Earthquake Fund, Ltd. (1997) Parametric Re (1997) Mitsui Marine (1998) Hedge Financial Products (CNA

Insurance) (1998) Concentric Ltd./Circle Maihama Ltd.

(Oriental Land)(1999). Namazu Re (Gerling Global

Reinsurance) (1999)

EQECAT

Geographic Areas: — United States

Earthquake - All 50 States + Puerto Rico Hurricane - Gulf Coast & Eastern Seaboard,

Hawaii & Puerto Rico

— International - (Earthquake, Windstorms, Flood) Over 70 countries including: Canada, UK,

Western Europe, Eastern Europe, Japan, Caribbean, Israel, Italy, Philippines, Chile, Australia, New Zealand, Mexico, Taiwan, Indonesia and Turkey

Catastrophe Modeling Overview

Catastrophe Modeling Methodology

First Step - Define the Hazard

HURRICANECentral PressureRadius to Max WindTranslational SpeedWind FieldTerrain

HURRICANECentral PressureRadius to Max WindTranslational SpeedWind FieldTerrain

FAULTStrike-slipThrustMax. MagnitudeRupture LengthDuration

FAULTStrike-slipThrustMax. MagnitudeRupture LengthDuration

Catastrophe Modeling Methodology

Second Step - Overlay Portfolio

Individual Risk InformationLocationConstruction type AgeInsured value

Individual Risk InformationLocationConstruction type AgeInsured value

Individual Locations

WIND SPEEDCalculated for each LocationVw = f(Pc, d, regional topography)

WIND SPEEDCalculated for each LocationVw = f(Pc, d, regional topography)

GROUND MOTION Calculated for each LocationPGA=f(M1,d,regional geology)MMI = f(PGA, soil)

GROUND MOTION Calculated for each LocationPGA=f(M1,d,regional geology)MMI = f(PGA, soil)

Local Site Factors (Terrain/Soil)

Distance (d)

Catastrophe Modeling Methodology

Third Step - Determine Site Hazard Severity

Catastrophe Modeling Methodology

Fourth Step - Estimate Ground up Damage

Hazard Severity

Vulnerability FunctionsCalculated damage for each Location

PDF Probability density function of damage

Distribution of damagebased on hazard severity

Distribution of hazardseverity at the site

Intensity

Damage Calculation Uncertainty Reflected in Damage

Estimate

Dam

age

Catastrophe Modeling Methodology

Step Five - Compute Insured Loss

Insurance Data- Insured value- Deductible- Occurrence, site & policy limits- Facultative- Treaties

Insurance Data- Insured value- Deductible- Occurrence, site & policy limits- Facultative- Treaties

site & policy losses

Loss

Pro

bab

ilit

y

Deductible

DamageDistribution

Catastrophe Modeling Methodology

Compute Insured Loss

Catastrophe Modeling Methodology

Portfolio Results

Statistically combine individual results taking Correlation into account— Correlation of performance is a real issue

It is computationally intense It lengthens the tail of the curve

— PML understated without correlationPDF

$ Dmg

Ret. 20%

Ded

uctib

le

Reten

tion

Ret.

40%

Rein

suran

ce

60%

Rein

s.

40%

Rein

s.

40%

Rein

s.

50%

Rein

s.

50%

Reten

tion

Catastrophe Modeling Methodology

Probabilistic Analysis

Requires the development of a extensive Stochastic Event Set

Repeat analysis process for Events 1 through N

The above analysis enables the development of the Annual Loss and Loss Distribution

Event 1 Freq 1 Dmg 1 Loss 1Event 2 Freq 2 Dmg 2 Loss 2

: : : :: : : :

Event N Freq N Dmg N Loss N

International Reinsurance Pricing and Challenges

International Reinsurance Pricing and Challenges

Exposure Data— Cresta level information— Limited, if any, structural information

Modeling Data Varies from Country to Country— Soil Information— Terrain Information— Building Vulnerabilities

Building Codes Building Practices Code Enforcement

— Frequency & Severity of events (Stochastic event set)

Premiumby country, etc. Decreasing

Uncertainty

IncreasingQualityof Data Cresta

ZonesOccupancy

(Residential,Commercial)

Premiumor TSI

PostalCode

Standard StructuralClassification

TSI/Risk

Address,Log/Lat, etc.

Material, age, height, engineering report, etc.

Value, limits, ded., etc.

Specificaddress

DetailedOccupancy Codes

TSI, value, limits, etc.

Location Structural Insurance

Exposure Data

Level of Data Impacts Pricing

Cresta Prefecture

Ku Shi

Aggregate vs. Detail Data

Japan Typhoon

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Cresta Miyazaki-ken Kagoshima-ken Kumamoto-ken Fukuoka-een Oita-ken Saga-ken

Prefectures within Cresta Zone

Rat

e p

er

$1,0

00

Pricing varies significantly within a Cresta Zone

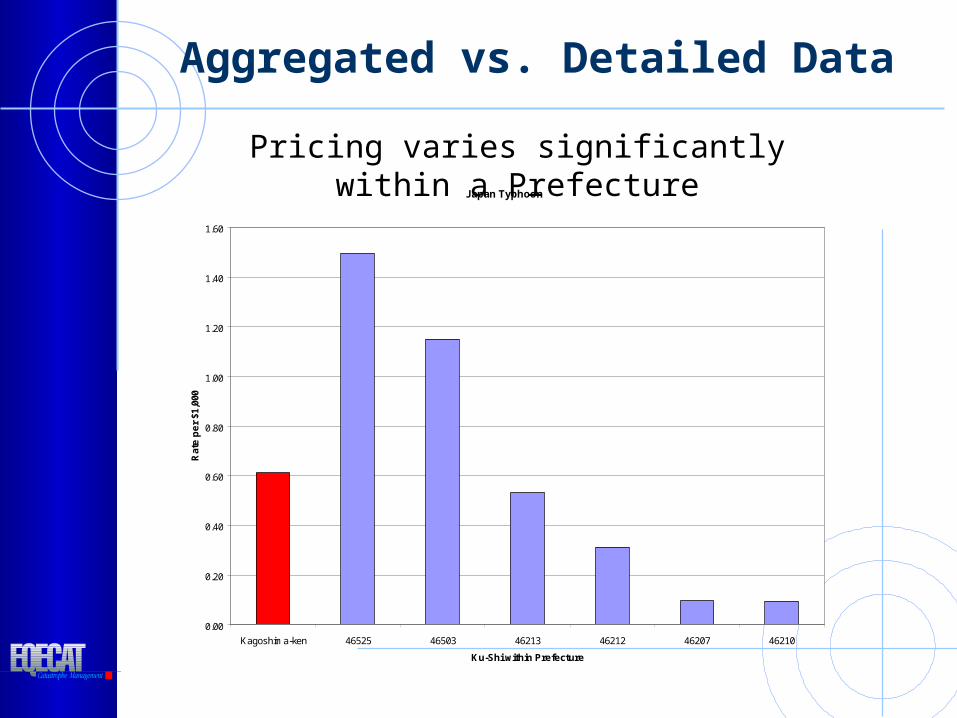

Aggregated vs. Detailed Data

Japan Typhoon

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Kagoshima-ken 46525 46503 46213 46212 46207 46210

Ku-Shi within Prefecture

Rat

e p

er

$1,0

00

Pricing varies significantly within a Prefecture

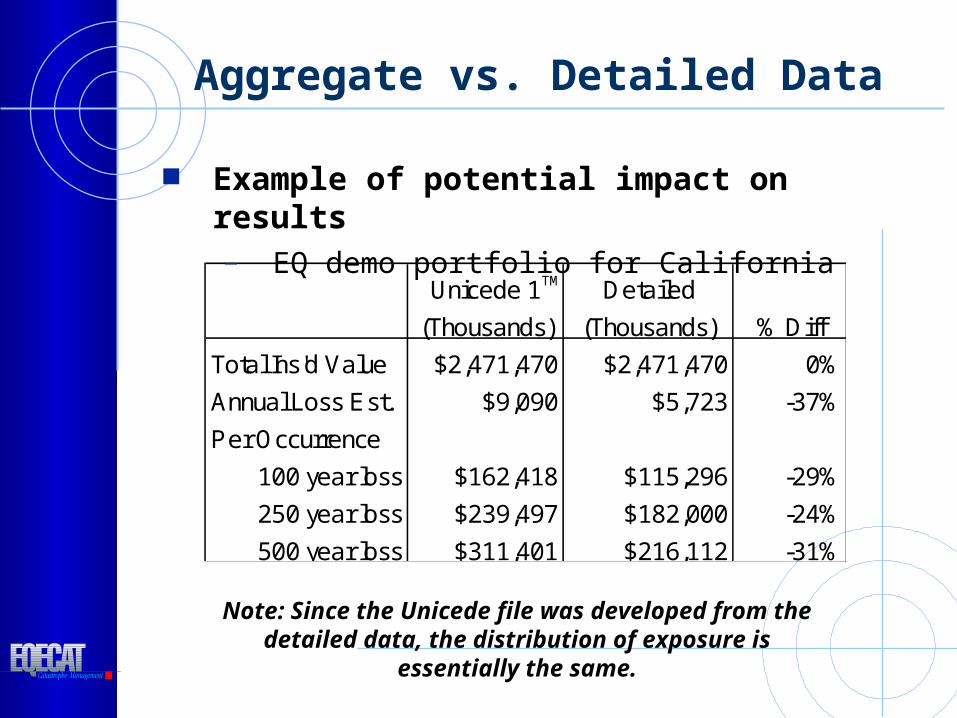

Aggregate vs. Detailed Data

Unicede 1 Detailed

(Thousands) (Thousands) % Diff

Total Ins'd Value $2,471,470 $2,471,470 0%

Annual Loss Est. $9,090 $5,723 -37%

Per Occurrence

100 year loss $162,418 $115,296 -29%

250 year loss $239,497 $182,000 -24%

500 year loss $311,401 $216,112 -31%

Example of potential impact on results— EQ demo portfolio for California

Note: Since the Unicede file was developed from the detailed data, the distribution of exposure is essentially the same.

TM

Structural Information

Impact of Structure Type

Building performance varies significantly from one building type to another

Vulnerability functions are used to develop damage estimates which are structure specific

Impact of Structure Type

Japan Aggregate Loss Distribution

400

600

800

1,000

1,200

1,400

1,600

99.00 99.10 99.20 99.30 99.40 99.50 99.60 99.70 99.80 99.90

Probability of Non-Exceedance

Lo

ss (

$ T

ho

usa

nd

s)

Structure Type 6 Structure Type 3

• Rate per $1,000 Structure Type 6 = 0.50• Rate per $1,000 Structure Type 3 = 0.17

Critical Modeling Data Varies from Country to Country

1:24,000

Taiwanby SoilType

SbSb-cScSc-dSdW

1:500,000

Section of LA

TaiwanCritical modeling data includes soil, terrain, frequency & severity of events, etc.

Adapazari - near total damage due to poor soil and

liquefaction.

Impact of Soil on Pricing

August 17, 1999 Izmit, Turkey

(M7.4 Earthquake)

Impact of Soil on Pricing

San Diego, CA 92118Annual Aggregate Loss Distribution

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

99.00 99.10 99.20 99.30 99.40 99.50 99.60 99.70 99.80 99.90

Probability of Non-Exceedance

PM

L

Soft Soil Stiff Soil Hard Rock

Rate per $1,000

Soft Soil - $4.80 Stiff Soil - $2.70 Hard Rock - $0.40

Impact of Terrain (Friction) on Pricing

Loss CostsStructure Type 1 - Frame

$1000 Deductible

Loss CostsStructure Type 1 - Frame

2 % Deductible

Building Codes

Taiwan— Building with height less than

50 meters No dynamic analysis is

required No third party review (by a

committee) is required Geotechnical engineers are

not required if the excavation is less than 10 meters deep

— Architects are in charge of planning, design, and construction inspection

Building practice varies from country to country

Building Codes/Practices

Most of the damaged high rise buildings in Taiwan were round 12 stories (less than 50 m high)

September 21, 1999 ChiChi, Taiwan (M7.6 Earthquake)

New high-end buildings (they “were” built to the California code)!

Building Code Enforcement

August 17, 1999 Izmit, Turkey (M7.4 Earthquake)

Earthquake Frequency and Severity

Western U.S. EarthquakesUSGS Catalog, Mw, Mmin = 5.0

5 to 6 (499)6 to 7 (134)7 to 8.2 (26)

Eastern U.S. EarthquakesUSGS Catalog, Mw, Mmin=4.0

4 to 5 (208)5 to 6 (23)6 to 7 (4)

7 to 8.3 (4)

TAITUNG

SUAO

TAIPEI

ILAN

HUALIEN

KAOSHIUNG

TAINAN

CHIAI

HSINCHU

Earthquakes in the Region of TaiwanMw Magnitude

4 to 55 to 66 to 7

7 to 8

8 to 8.1

Since earthquake are felt and measured around the world the historical data is fairly good for most countries.

Taiwan

U.S.

However, information on fault location, type and other characteristics varies. This is an issue since major earthquakes are infrequent events

Typhoon/Hurricane Frequency and Severity

Hurricane data is good for major industrialized countries, but largely antidotal for most other countries.

Conclusion

International Reinsurers are working with very limited data which can skew or bias results

Ability of models to effectively develop loss cost varies from country to country

There is a lot of uncertainty in the process which must be accounted for in reinsurance pricing

There are also other issues, not touched on in this presentation, that can impact results (e.g., Damage to Loss calculation, handling of uncertainty, etc.)In spite of the above, Catastrophe models are still the In spite of the above, Catastrophe models are still the

best tool available for pricing reinsurance. best tool available for pricing reinsurance.