international tax alert - 3 february 2012 - turkish tax ... tax authority issues explanatory...

TRANSCRIPT

Turkish Tax Authority issues explanatory guidance on taxation of derivativesOn 19 January 2012, the Turkish Tax Authority published three new Communiqués by related to the application of the Income Withholding Tax, the Corporate Tax and the Banking and Insurance Transactions Tax (BITT) to derivatives transactions. Because these communiqués are explanatory in nature, they are effective immediately.

Income Tax Code Communiqué (Withholding Tax)Income Tax Code Communiqué Serial No. 282 provides information regarding application of the withholding tax under temporary article 67 of the Income Tax Code to derivative and option transactions performed by resident and nonresident investors.

Within the framework of the explanations provided in the Communiqué, the income withholding taxation treatment is as follows:

• Ifanonresidentcorporationisabankorafinancialinstitution,theincome and gains derived from derivative transactions and option contracts would not be subject to income withholding tax under temporary article 67 of the Income Tax Code. In addition, , as explained in the Corporate Tax Code Communiqué, the income and gains would be regarded as commercial income and would not be subject to corporate withholding taxation or declaration in Turkey.

•The income and gains derived from derivative transactions and options that are based on equities or equity indices are subject to 0% income withholding tax for all types of resident and nonresident investors.

•The income and gains derived from derivative transactions and options that are not based on equities or equity indices will be taxed as follows:

3 February 2012

International Tax Alert

International Tax Alert 2

• Income Tax Code Communiqué series no.282 provides detailed explanations on how the income and gains derived from derivative transactions and option contracts should be taxed for withholding tax purposes for investors. According to the sample calculations, the taxation of the income from forward, money swap, option and Turkdex transactions will be done at the maturity of the transactions, but for interest swap contracts taxation will be done at the date of interest payments.

•The same Communiqué further explains that warrant transactions performed at the Istanbul Stock Exchange that are based on equities or equity indices are subject to 0% income withholding

taxation for all types of resident and nonresident investors. Gains derived from other warrants will be subject to withholding tax under the general rules provided in the table above.

• In case more than one trading transaction is conducted in connection with the same type of marketable security or other capital market instrument within the quarterly period, for purposes of withholding application, such transactions shall be considered a single transaction. , For the grouping of the same type of marketable securities and other capital market instruments, the new Communiqué changes the classificationofsecuritiesthefollowing:

•Marketablesecuritieswithfixedincome

•Marketable securities with variable income

•Other marketable securities and capital market instruments

•Participationcertificatesofmutual funds and shares of marketable securities investment trusts

The Communiqué further explains that the derivative transactions and options and warrants quoted in the Istanbul Stock Exchange that are based on equities or equity indices willbeclassifiedinthesecondgroup. Furthermore, warrants that are based on underlying assets other than equities or equity indices willbeclassifiedinthethirdgroup.

Investor type Market type

Turkdex (VOB) Over-the-counter

a. Resident real persons 10% withholding tax 10% withholding tax

b. Resident companies with capital shares (Including the mutual funds that are subject to the supervision and audit of Capital Markets Board)

0% withholding taxNot subject to

withholding tax

c. Other Resident Companies 10% withholding taxNot subject to

withholding tax

d. Non-resident real persons 10% withholding tax 10% withholding tax

e. Non-resident companies with capital shares and other foreign corporate investors that: (1) operate exclusively for deriving capital gains from marketable securities and other capital market instruments and for using the related rights; (2) are determined to be corporate taxpayers similar in nature to the investment funds and investment trusts established according to the Capital Markets Law no 2499; and (3) do not have a permanent establishment/permanent representative and are not banks or financialinstitutions

0% withholding tax 0% withholding tax

f. Nonresident investors apart from the ones listed in item ”e” above that do not have a permanent establishment/permanent representativeandarenotbanksorfinancialinstitutions

10% withholding tax 10% withholding tax

g. Nonresident companies that have a permanent establishment or permanent representative in Turkey

0% withholding taxNot subject to

withholding tax

h.Nonresidentcompaniesthatarebanksorfinancialinstitutions 0% withholding taxNot subject to

withholding tax

3International Tax Alert

Corporate Income Tax Code CommuniquéThe Corporate Tax General Communiqué Serial No. 5 explains the taxation of corporate income earned from derivatives.

Taxation principles of the income earned from derivatives instruments by nonresident corporations depend on whether or not they operate via registeredofficesorpermanentrepresentatives in Turkey.

Taxation principles of income earned from derivatives by nonresident corporations that operate a permanent establishment or permanent representatives in TurkeyThe Communiqué explains the taxation principles of income earned from derivatives by nonresident corporations that have a permanent representative or a registeredofficeasfollows.

Forward transactionsThe earning of the income takes place at maturity. For that reason, evaluations that are made before maturity cannot be associated with the corporate earnings. In agreements that are terminated beforethematurity,profit/lossisadded to the corporate earnings at the date of termination.

Currency swap transactionsThe earning of income takes place at maturity. Therefore, evaluations before maturity cannot be associated with the corporate earnings. In agreements that are terminated before the maturity, profit/lossisaddedtothecorporateearnings at the date of termination.

Interest rate swap transactionsThe earning of income takes place when the interests are exchanged and is calculated according to the

interest rates. For that reason, the evaluations performed in the period before the interest rate exchange date will need to be adjusted. Interests paid or collected will be regarded as expense or income as of the periods of accrual of interest. If the interest rate exchanges coincide,netprofitorlossistakeninto account for the determination of the corporate earnings as of those dates. If they do not coincide, the income or expense provision of interest that does not coincide is to be taken into account for the determination of the corporate earnings.

Option agreementsOption premium is regarded by the seller of the option as income on the issue date of the agreement and as expense by the buyer of the option at the maturity date of the agreement. The earning of the income takes place by the usage of the option by transactions over the counter.

Accordingly, the evaluations performed until the usage date of the option will need to be adjusted. Derivatives and option agreements taking place on the Derivatives Exchange (VOB) are evaluated at fair value (compromised price that occurs in the market). (Tax Procedural Code, Article 289).

Taxation principles of income earned from derivatives by nonresident corporations that do not operate a permanent establishment or permanent representatives in TurkeyThe Communiqué explains the taxation essentials of income earned from derivatives by nonresident corporations that do not operate via a permanent representative or a registeredofficeasfollows.

Earnings which are gained from forward, currency swap, over the counter markets from option agreements and warrant transactions by nonresident corporations that do not operate permanent establishment or permanent representatives in Turkeyareidentifiedascommercialincome and thus, there is no withholding according to Article 30 of the Corporate Tax Law, and this income need not be further declared.

Earnings gained by nonresident corporations that do not operate a permanent establishment or permanent representatives in Turkey from interest rate swap transactions are regarded as interest and they are taxed pursuant to the subparagraph (ç)ofthefirstparagraphofArticle30 of the Corporate Tax Law via withholding tax in Turkey. Moreover, a withholding tax of 0% is to be applied to the earnings from those transactionsofbanksandfinancialinstitutions that are nonresident corporations that do not operate via aregisteredofficeorapermanentrepresentative in Turkey and a withholding tax of 10% is to be applied onto the earnings of other institutions.

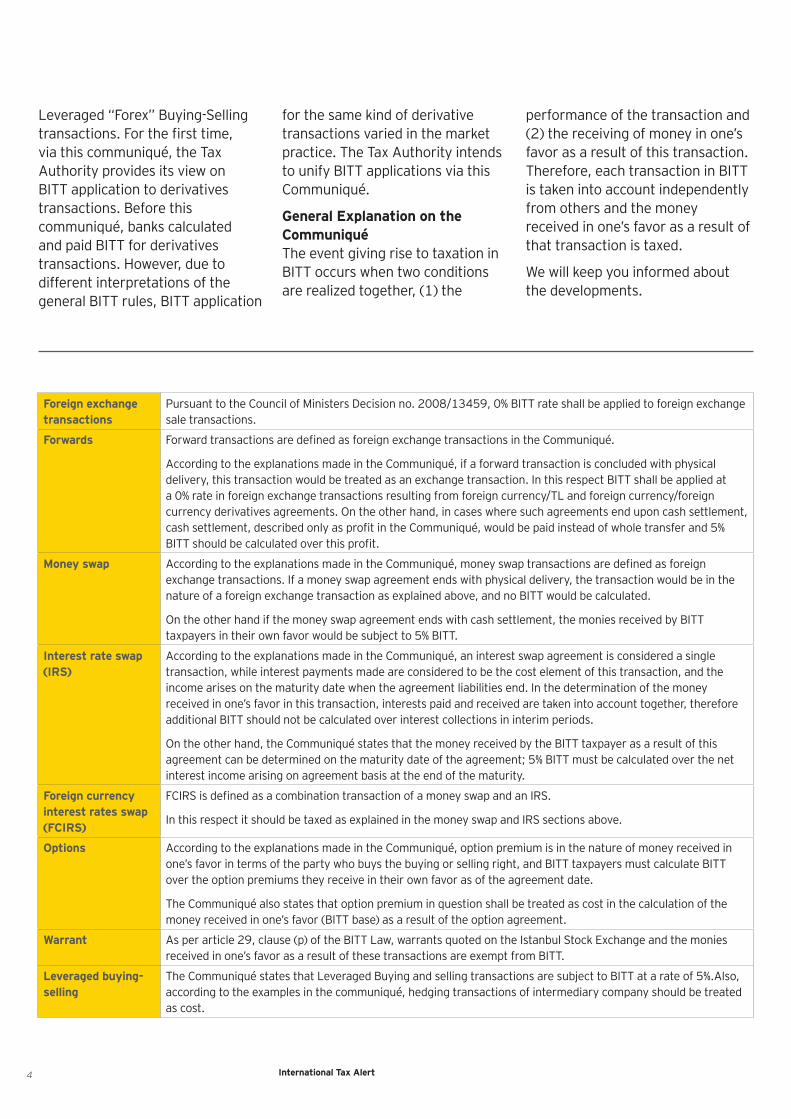

Banking and Insurance Transaction Tax Communiqué (BITT)The Tax Authority also provided detailed explanations related to the Banking and Insurance Transaction Tax (BITT) and its application to derivatives transactions. BITT isanindirecttaxonfinancialtransactions that should be paid by banks.

This communiqué covers Foreign Exchange Transactions, Forwards, Swap, Options Warrants, and

4 International Tax Alert

Leveraged “Forex” Buying-Selling transactions.Forthefirsttime,via this communiqué, the Tax Authority provides its view on BITT application to derivatives transactions. Before this communiqué, banks calculated and paid BITT for derivatives transactions. However, due to different interpretations of the general BITT rules, BITT application

for the same kind of derivative transactions varied in the market practice. The Tax Authority intends to unify BITT applications via this Communiqué.

General Explanation on the CommuniquéThe event giving rise to taxation in BITT occurs when two conditions are realized together, (1) the

performance of the transaction and (2) the receiving of money in one’s favor as a result of this transaction. Therefore, each transaction in BITT is taken into account independently from others and the money received in one’s favor as a result of that transaction is taxed.

We will keep you informed about the developments.

Foreign exchange transactions

Pursuant to the Council of Ministers Decision no. 2008/13459, 0% BITT rate shall be applied to foreign exchange sale transactions.

Forwards ForwardtransactionsaredefinedasforeignexchangetransactionsintheCommuniqué.

According to the explanations made in the Communiqué, if a forward transaction is concluded with physical delivery, this transaction would be treated as an exchange transaction. In this respect BITT shall be applied at a 0% rate in foreign exchange transactions resulting from foreign currency/TL and foreign currency/foreign currency derivatives agreements. On the other hand, in cases where such agreements end upon cash settlement, cashsettlement,describedonlyasprofitintheCommuniqué,wouldbepaidinsteadofwholetransferand5%BITTshouldbecalculatedoverthisprofit.

Money swap AccordingtotheexplanationsmadeintheCommuniqué,moneyswaptransactionsaredefinedasforeignexchange transactions. If a money swap agreement ends with physical delivery, the transaction would be in the nature of a foreign exchange transaction as explained above, and no BITT would be calculated.

On the other hand if the money swap agreement ends with cash settlement, the monies received by BITT taxpayers in their own favor would be subject to 5% BITT.

Interest rate swap (IRS)

According to the explanations made in the Communiqué, an interest swap agreement is considered a single transaction, while interest payments made are considered to be the cost element of this transaction, and the income arises on the maturity date when the agreement liabilities end. In the determination of the money received in one’s favor in this transaction, interests paid and received are taken into account together, therefore additional BITT should not be calculated over interest collections in interim periods.

On the other hand, the Communiqué states that the money received by the BITT taxpayer as a result of this agreement can be determined on the maturity date of the agreement; 5% BITT must be calculated over the net interest income arising on agreement basis at the end of the maturity.

Foreign currency interest rates swap (FCIRS)

FCIRSisdefinedasacombinationtransactionofamoneyswapandanIRS.

In this respect it should be taxed as explained in the money swap and IRS sections above.

Options According to the explanations made in the Communiqué, option premium is in the nature of money received in one’s favor in terms of the party who buys the buying or selling right, and BITT taxpayers must calculate BITT over the option premiums they receive in their own favor as of the agreement date.

The Communiqué also states that option premium in question shall be treated as cost in the calculation of the money received in one’s favor (BITT base) as a result of the option agreement.

Warrant As per article 29, clause (p) of the BITT Law, warrants quoted on the Istanbul Stock Exchange and the monies received in one’s favor as a result of these transactions are exempt from BITT.

Leveraged buying-selling

The Communiqué states that Leveraged Buying and selling transactions are subject to BITT at a rate of 5%.Also, according to the examples in the communiqué, hedging transactions of intermediary company should be treated as cost.

5International Tax Alert

For additional information with respect to this Alert, please contact the following:

Kuzey Yeminli Mali Müşavirlik A.Ş., International Tax Services, Istanbul• A. Feridun Gungor +90 212 368 5421 [email protected]• Müge Tan +90 212 368 5223 [email protected]• Levent Atakan +90 212 368 5263 [email protected]

6 International Tax Alert

www.ey.com

© 2012 EYGM Limited. All Rights Reserved.

EYG no. CM2704

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 152,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.Kuzey Yeminli Mali MüşavirlikA.Ş.isamemberfirmservingclients in Turkey.

International Tax ServicesAbout Ernst & Young’s International Tax services practices

Our dedicated international tax professionals assist our clients with their cross-border tax structuring, planning, reporting and risk management. We work with you to build proactive and truly integrated global tax strategies that address the tax risks of today’s businesses and achieve sustainable growth. It’s how Ernst & Young makes a difference.

Ernst & Young

Assurance | Tax | Transactions | Advisory

Ernst & Young International Tax Services• Global ITS, Jim Tobin

• Americas, Jeffrey Michalak

• Asia Pacific, Alice Chan

• Europe, Middle East, India and Africa, Alex Postma

• Japan, Kai Hielscher

• Argentina Carlos Casanovas Buenos Aires• Australia Daryn Moore Sydney• Austria Roland Rief Vienna• Belgium Herwig Joosten Brussels• Brazil Gil Mendes Sao Paulo• Canada George Guedikian Toronto• Central America Rafael Sayagues San José• Chile Osiel Gonzalez Santiago• China Becky Lai Beijing• Colombia Ximena Zuluaga Bogota• Czech Republic Libor Frýzek Prague• Denmark Niels Josephsen Soborg• Finland Katri Nygård Helsinki • France Claire Acard Paris• Germany Stefan Koehler Frankfurt• Hong Kong Christian Pellone Hong Kong• Hungary Botond Rencz Budapest

Balazs Szolgyemy Budapest• India Hitesh Sharma Mumbai• Ireland Joe Bollard Dublin• Israel Sharon Shulman Tel Aviv• Italy Marco Magenta Milan• Japan Kai Hielscher Tokyo• Korea Kyung-Tae Ko Seoul• Luxembourg Frank Muntendam Luxembourg• Malaysia Hock Khoon Lee Kuala Lumpur• Mexico Koen van ‘t Hek Mexico City• Middle East Tobias Lintvelt Abu Dhabi • Middle East Michelle Kotze Dubai• Netherlands Johan van den Bos Amsterdam• Norway Oyvind Hovland Oslo• Peru Roberto Cores Lima• Philippines Ma Fides Balili Makati City• Poland Andrzej Broda Warsaw• Portugal Antonio Neves Lisbon• Russia Vladimir Zheltonogov Moscow• Singapore Andy Baik Singapore• South Africa Justin Liebenberg Johannesburg• Spain Federico Linares Madrid• Sweden Erik Hultman Stockholm• Switzerland Daniel Gentsch Zurich• Taiwan Alice Chung Taipei• Thailand Anthony Loh Bangkok• Turkey Feridun Gungor Istanbul• United Kingdom Matthew Mealey London

Anna Anthony London• United States Jeffrey Michalak Detroit• Venezuela Jose Velazquez Caracas• Vietnam Vu Huong Hanoi

Ernst & Young Member Firm Contacts