introducing financial analysis

TRANSCRIPT

INTRODUCING FINANCIAL ANALYSIS

T.VENKATARAMANAN. FICWA.FCS.

Executive Overview

WHY?

Why bother with financial analysis ?what tools and techniques ?

How it helps decision making?A Practical Example.

The Three uses

1.Is the project going to make money?

2. Demonstrating Additionality

3.The choice: The structuring of the project

Profit & loss plan & revenue plans

Beware of little expenses ; a small leak will sink a great ship

Projects cost money- outflow

Projects generate inflows

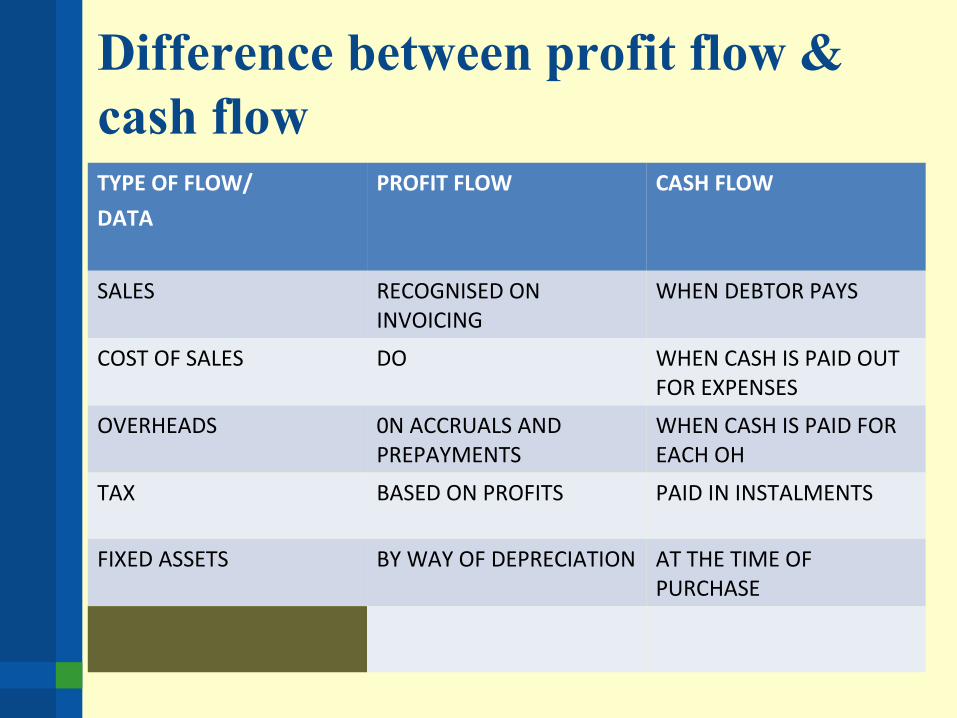

The differencebetween profit flow and cash flow.

Arrive at net cash flow

Difference between profit flow & cash flowTYPE OF FLOW/

DATA

PROFIT FLOW CASH FLOW

SALES RECOGNISED ON INVOICING

WHEN DEBTOR PAYS

COST OF SALES DO WHEN CASH IS PAID OUT FOR EXPENSES

OVERHEADS 0N ACCRUALS AND PREPAYMENTS

WHEN CASH IS PAID FOR EACH OH

TAX BASED ON PROFITS PAID IN INSTALMENTS

FIXED ASSETS BY WAY OF DEPRECIATION AT THE TIME OF PURCHASE

FREE CASH FLOW

OPERATING PROFIT

CHANGES IN WORKING CAPITAL

LESS TAX PAID

LESS CAPITAL EXPENDITURE

FREE CASH FLOW

FREE CASH FLOW THE INCLUSIONS & EXCLUSIONSTO INCLUDE TO EXCLUDE

SALES LOAN FINANCE/EQUITY

PAYMENT FOR PURCHASES - DIVIDENDS/INTERESTS

RUNNING COSTS - LEASE PAYMENTS

PAID/RECD ON ASSETS INTEREST ON SURPLUS DEPOSITS

PURCHASE COSTS OF ASSETS OTHERWISE WOULD HAVE BEEN LEASED

TAX PAYMENTS AND REFUNDS

The Next step :demonstrating /the best alternative

In the earlier stage we would have considered a myriad of alternatives which might have resulted in same or different net cash flows

therefore it becomes necessary to make comparative analysis of the various options available.

the appropriate indicators

choose an appropriate indicator to evaluate the alternatives.The generally selected indicators are IRR , NPV, CBA, etc.It may also be neccessary to calculate pay back periods and B.E.Pointsto make proper assessmentscompare the above results with bench mark values internally or externallyROI etc.

Pay back Period

It is the length of time taken by the inflows of cash, to match the original investment.

It measures the length of time it takes for the project to pay back the original investment or capital cost

If the cost of a m/c is Rs 20,000/= and the annual net cash flow per annum is Rs 10,000/= the pay back period is 2 years .

the pay back period acts as a proxy for Risk.The lesser the pay back period the lesser is the Risk

Informal thresholds are typically employed 3-5 years for Britain. For countries like Iraq it is 6 months

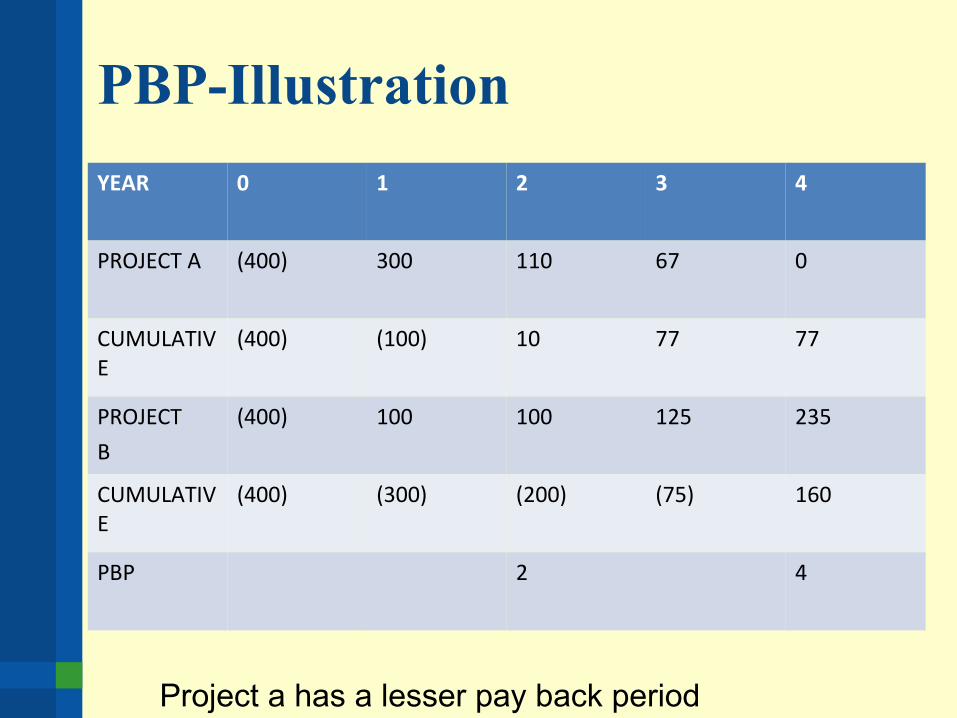

PBP-Illustration

YEAR 0 1 2 3 4

PROJECT A (400) 300 110 67 0

CUMULATIVE

(400) (100) 10 77 77

PROJECT

B

(400) 100 100 125 235

CUMULATIVE

(400) (300) (200) (75) 160

PBP 2 4

Project a has a lesser pay back period

NPV -METHOD

P.B.Period does not consider the time value of money.

A Bird in hand is worth two in the bush.

The money in hand today is more valuable than the distant cash flow on a/c of two reasons.1) Interest it will earn 2)the impact of inflation

Rs 1000/= deposited in bank today @ 5% interest will be equal to 1050.

But Rs 1050/= today if idle, after a year is equal to Rs 1000/= if rate of inflation is 5%

This is the oppurtunity cost of investing money in bank .

NPV ILLUSTRATION

YEAR 0 1 2 3 4 5

A (400) 300 110 67 0 0

CUMULATIVE

(400) (100) 10 77 77 77

D.F @10% 1 .909 .826 .751 .683

NPV (400) 272.2 90.9 50.3

B (400) 100 100 125 235

CUMU (400) (300) (200) (75) 160

D.F 1 .909 .826 .751 .683

NPV (400) 90.9 82.6 93.9 160.5

NNPV A=13.4 B=27.9

AS NNPV PROJECT B IS BETTER

IRR.

IRR is the discount rate that produces a net present value of zero.It can be considered as the breakeven discount rate .It represents the maximum cost of finance at which the project remains VIABLEThe procedure for calculating is thro trial and error method or use computers.irr is determined thro an iteration process using different discount rates until ZERO NPV is produced.

Hurdle rate

Once IRR is calculated it is compared with the companys'preset threshold investment rate,which is called hurdle rate.Hurdle rate is company's oppurtunity cost of capital.Alternatively the WACCIRR Decision rule : IRR > HR ACCEPT IRR < HR REJECTIRR Provides the simplest tool for decision making by managers

BCR

When confronted with 2 or more NPV positive projects and capital rationing is there BCR provides a means to identify the better ones.BCR = PV of Future cash flows//value of Initial capital invested The project with the highiest BCR represents the most attractive The typical BCR bench mark is 1.3

WACC - illustration

A cost of equity current year

16

previous year

17

B interest 275 280

C average borrowings

2348 2533

D pretax borrowing cost

11.71 11.06

E post tax cost of debt

8.20 7.76

F average invested capital

3983 3858

G average equity 1635 1325

H wacc 11.40 10.92

WACC = (E X C/F + A *G/F )

Company Objectives

List your company objectivesDefine these objectives in detail

Defining Terms

Define any terms or vocabulary you need to discuss in your presentation while your audience may be unfamiliar with.

First item•Definition

Second item•Definition

Third item•Definition

Current Situation

Explain the current situation and issues that face your company, and explain their implications.

Background to Recommend a Strategy

The original strategy fails to catch up with the current changes

New problems/needs/issues

Available SolutionsList available solutions with pros, cons, and costs for each. If necessary, insert a chart below.

0

20

40

60

80

100

120

Solution 1 Solution 2 Solution 3 Solution 4

CostConPro

Solution 1Solution 2Solution 3Solution 4

Recommend a Strategy

Recommend one solution that you think is best suited to the situation.

Benefits of My Recommendation

Benefit 1

Benefit 2

Benefit 3

Benefit 4

Costs of Rejecting this Solution

List the costs of not using this solution

Questions and Answers

Prepared questions

Questions from the audience

Thank You for Coming!