introduction to bank reconciliation

TRANSCRIPT

Md. Hasan Basri(Software Consultant)

What is a bank reconciliation? A bank reconciliation is a process performed by a

company to ensure that the company's records (check register, general ledger account, balance sheet, etc.) are correct and that the bank's records are also correct.

Reason of Difference

Cheque issued but not presented for payment.

Cheque deposited but not cleared.

Charges debited by bank.

Interest credited by bank.

Error made either by bank or the company.

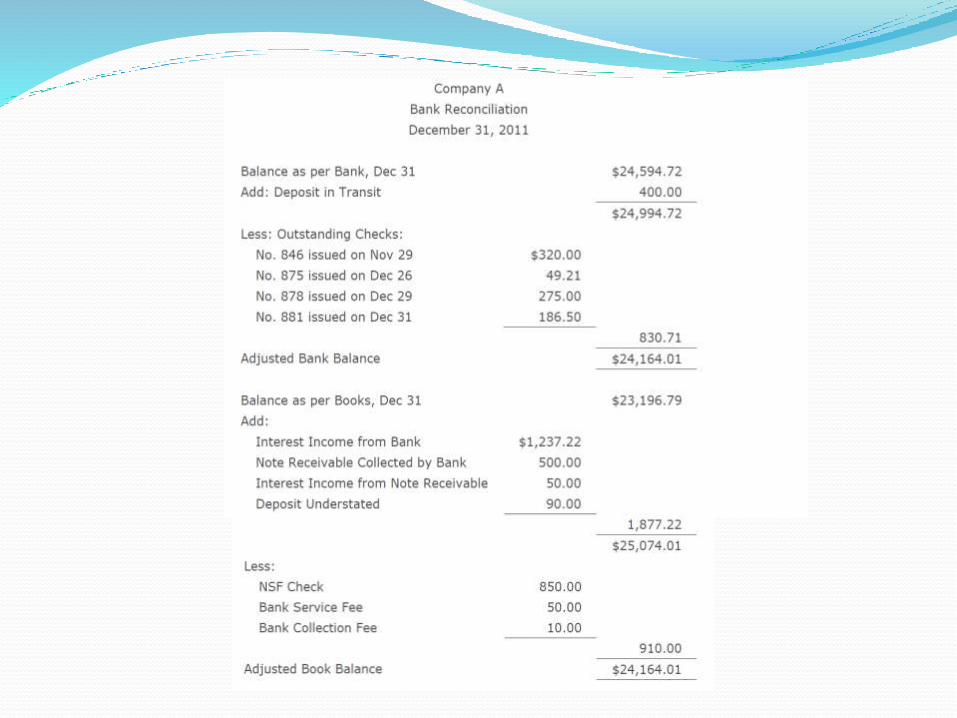

Bank Reconciliation Process Step 1. Adjusting the Balance per Bank

Step 2. Adjusting the Balance per Books

Step 3. Comparing the Adjusted Balances

Step 4. Preparing Journal Entries

Step 1. Adjusting the Balance per Bank

Step 2. Adjusting the Balance per Books

Step 3. Comparing the Adjusted Balances

After adjusting the balance per bank (Step 1) and afteradjusting the balance per books (Step 2), the two adjustedamounts should be equal. If they are not equal, you mustrepeat the process until the balances are identical. Thebalances should be the true, correct amount of cash as of thedate of the bank reconciliation.

Step 4. Preparing Journal Entries

Journal entries must be prepared for the adjustmentsto the balance per books (Step 2). Adjustments toincrease the cash balance will require a journal entrythat debits Cash and credits another account.

All items on the book side of the bank reconciliationrequire journal entries.

If the item is added to book side: Debit Cash

If the item is subtracted from the book side: Credit Cash

Adjustment at Journal Sample

Sample Exercise: