introduction to domestic transfer pricing naveen nd gupta, ccm delhi 1

TRANSCRIPT

Introduction to Domestic Transfer Pricing

Naveen ND Gupta, CCM

Delhi1

What is Transfer Pricing?

2

Transfer Pricing : Demystified

3

Abuse of Tax Haven

1. Tax Haven may be DEFINED as a Country or Jurisdiction:

(i) which does not levy any tax / levies very small tax;

(ii) which has no controls on foreign exchange movements;

(iii) which has a legal system that ensures secrecy;

(iv) which permits foreigners to open companies & other entities; and

(v) which makes laws specifically designed to help “financial engineering”, “creative accounting” and “tax avoidance”.

(vi) Which signs DTA with several countries & facilitates Treaty Shopping.

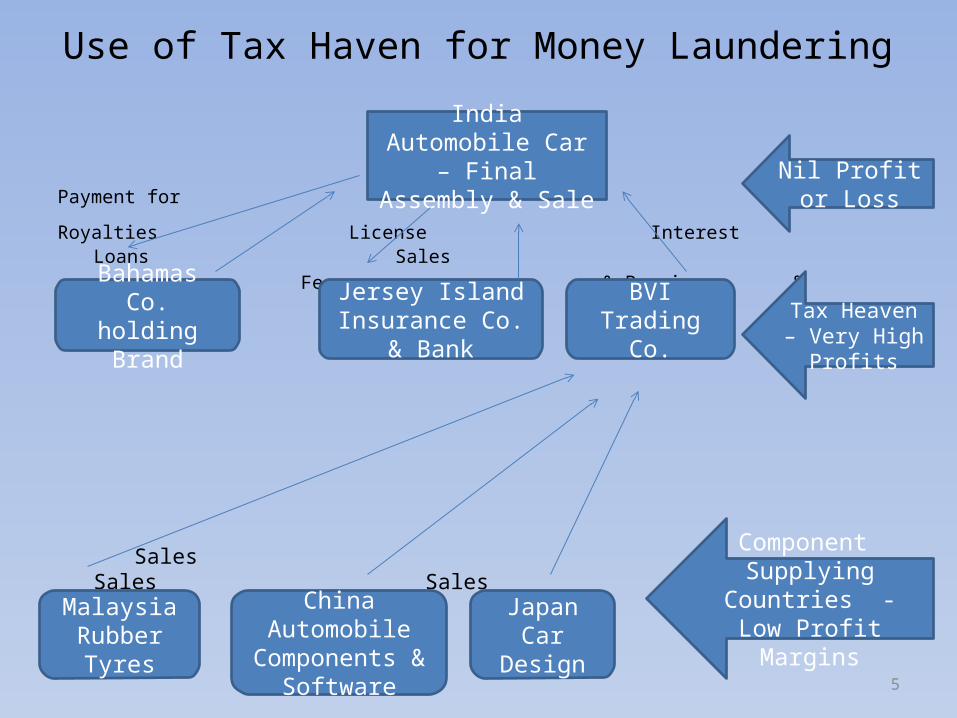

Use of Tax Haven for Money Laundering

4

Corrupt Politicians/ Bureaucracy

Bankers & Solicitors

Bearer Shares

Panama Companies – 1, 2 & 3

Netherlands Antilles Company

Swiss Bank Account Immovable Properties in U.S.A.

Use of Tax Haven for Money Laundering

5

Payment for

Royalties License Interest Loans Sales Fees & Premium & Advances

& Premium

Sales Sales Sales

India Automobile Car – Final Assembly &

Sale

Bahamas Co. holding Brand

Jersey Island Insurance Co. &

Bank

BVI Trading Co.

Nil Profit or Loss

Tax Heaven – Very High

Profits

Malaysia Rubber Tyres

China Automobile Components &

Software

Japan Car Design

Component Supplying Countries - Low Profit

Margins

Amnesty U/s 115BD ?

6

(1) Where the total income of an assessee, being an Indian company, for the previous year relevant to the assessment year beginning on the 1st day of April, 2012 28[or beginning on the 1st day of April, 2013] 28a[or beginning on the 1st day of April, 2014] includes any income by way of dividends declared, distributed or paid by a specified foreign company, the income-tax payable shall be the aggregate of— (a) the amount of income-tax calculated on the income by way of such dividends, at the rate of fifteen per cent; and (b) the amount of income-tax with which the assessee would have been chargeable had its total income been reduced by the aforesaid income by way of dividends.(3) In this section,— (i) "dividends" shall have the same meaning as is given to "dividend" in clause (22) of section 2 but shall not include sub-clause (e) thereof; (ii) "specified foreign company" means a foreign company in which the Indian company holds twenty-six per cent or more in nominal value of the equity share capital of the company.]

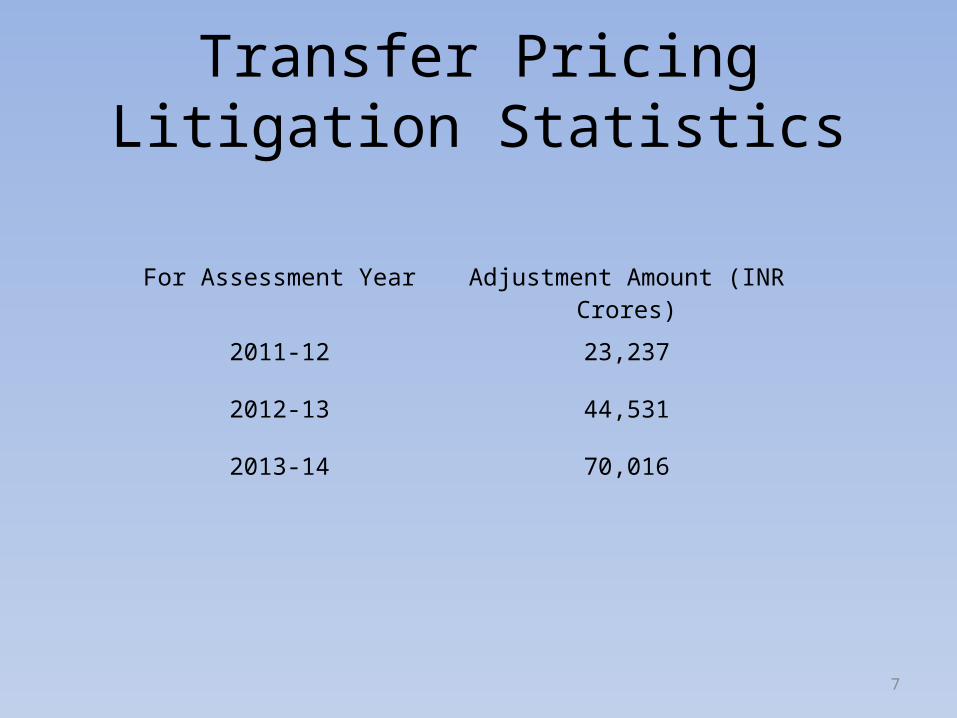

Transfer Pricing Litigation Statistics

For Assessment Year Adjustment Amount (INR Crores)

2011-12 23,237

2012-13 44,531

2013-14 70,016

7

(A) When one of entity is a loss making and other is profit making. In such a case the profit may be shifted to the loss making entity so that the total tax burden of the group is reduced as a whole; or

(B) Where Parties to a transactions are subjected to different tax rates under the scheme of the Act. In such a case, the profits may be shifted to an entity subjected to lower rate of tax from an entity subjected to comparatively higher rate of tax. The lower tax rate may be on account of different status (e.g. Individual, Hindu Undivided Family, Association of Persons, Body of Individuals, Partnership Firm, Company etc.), nature of activity, sectoral or location based tax incentives etc.

DOMESTIC TAX ARBITRAGE OPPORTUNITIES

8

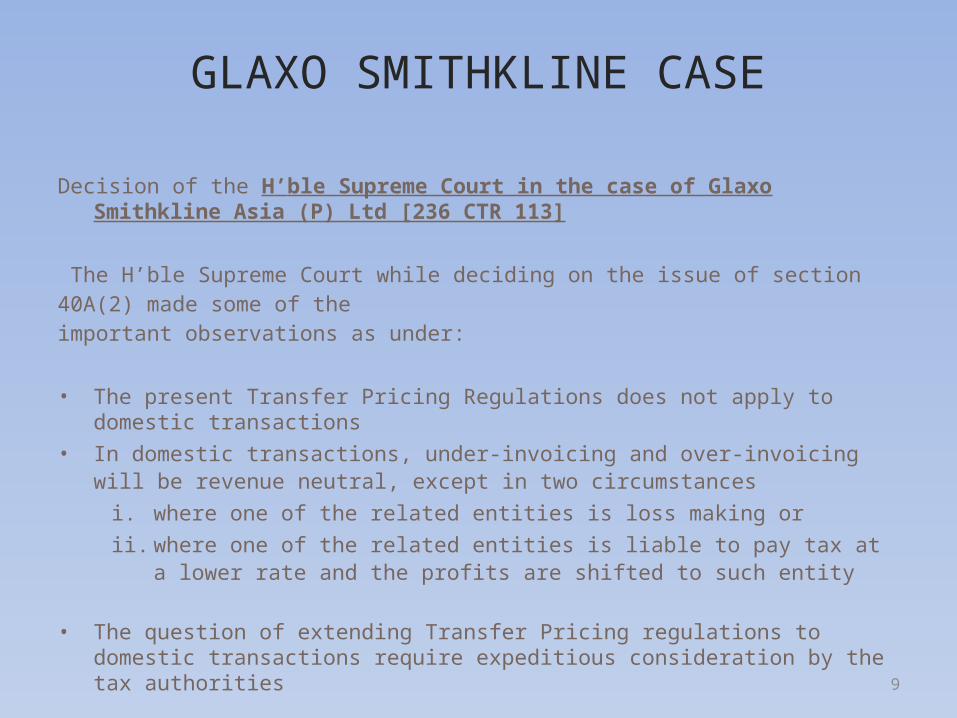

Decision of the H’ble Supreme Court in the case of Glaxo Smithkline Asia (P) Ltd [236 CTR 113]

The H’ble Supreme Court while deciding on the issue of section 40A(2) made some of theimportant observations as under:

• The present Transfer Pricing Regulations does not apply to domestic transactions

• In domestic transactions, under-invoicing and over-invoicing will be revenue neutral, except in two circumstances

i. where one of the related entities is loss making or

ii. where one of the related entities is liable to pay tax at a lower rate and the profits are shifted to such entity

• The question of extending Transfer Pricing regulations to domestic transactions require expeditious consideration by the tax authorities

GLAXO SMITHKLINE CASE

9

Section 40A• Expenditure paid or to be paid to related party as defined under section

40A(2)(b)

Section 80IA• Inter unit transfer of goods and services as referred to in section 80IA(8)

Section 80IA• Transaction between the tax payer and any other person owing to close

connection as referred to in section 80IA(10) where more than ordinary profits are earned by business unit claiming tax holiday/deduction

Section 10AA• Any transaction under Chapter VIA or Section 10AA to which the provisions

of 80IA apply, ie:

― inter-unit transfers― more than ordinary profits earned by tax holiday/ exemption unit

Where aggregate of above transactions by assessee in previous year exceeds Rs. 5 crore.

SPECIFIED DOMESTIC TRANSACTIONS (Sec. 92BA)

10

• Domestic Transfer Pricing is applicable only where value of Specified Domestic Transactions (other than International Transactions) crosses 5 Crs

• While computing the aggregate value of transactions: - Value of the International transactions to be excluded - Value of transactions between 2 units of the same company to be

covered (when undertaken with a tax holiday unit) - Inter-company transactions to be covered (when undertaken with a

company having a tax holiday unit) - Transactions with a person having a close connection as mentioned

in section 80IA(10) to be covered - Payment of expenses to related person defined under section 40A(2)

(b) to be covered

THRESHOLD LIMIT & COVERAGE

Aggregate Value oftransaction below INR 5

Cr

Aggregate Value of SDT above INR 5 Cr

Subject to existing tax laws

Subject to Domestic TransferPricing regulations

11

.

Types of Specified Domestic Transactions

12

Nature of Transaction Provision Applicable

Description of Transaction

Expenditure in respect of which payment has been made/ is to be made to specified persons

Sec. 40 A(2) Only expenditure incurred by assessee in respect of which payment has been made/to be made to persons specified in Sec 40A(2)(b) are covered.

Transaction concerning eligible business transaction enjoying profit linked deductions/exemptions

Sec 80A Transfer of goods or services from an eligible unit to any other business of the tax payer and vice versa

Sec 80 – IA (8) Transfer of goods or services from an eligible unit to business of the tax payer and vice versa

Sec 80 – IA (10) Any business transacted between a taxpayer carrying on an eligible business with any other person producing more than ordinary profits to taxpayers eligible business owing to close connection with such other person or for any other reason

.

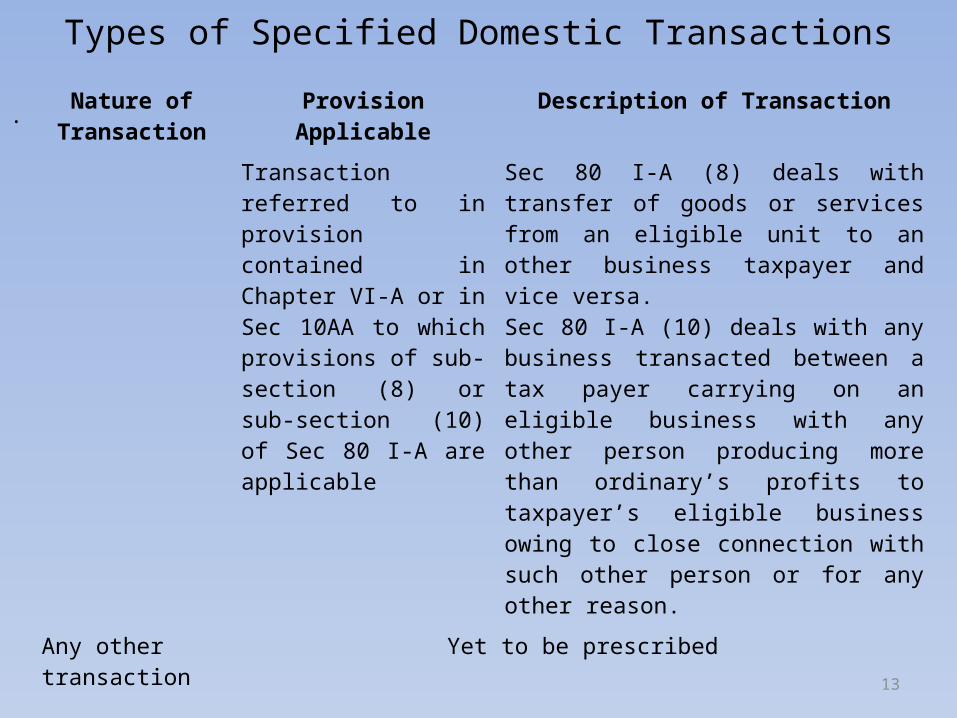

Types of Specified Domestic Transactions

13

Nature of Transaction

Provision Applicable Description of Transaction

Transaction referred to in provision contained in Chapter VI-A or in Sec 10AA to which provisions of sub-section (8) or sub-section (10) of Sec 80 I-A are applicable

Sec 80 I-A (8) deals with transfer of goods or services from an eligible unit to an other business taxpayer and vice versa. Sec 80 I-A (10) deals with any business transacted between a tax payer carrying on an eligible business with any other person producing more than ordinary’s profits to taxpayer’s eligible business owing to close connection with such other person or for any other reason.

Any other transaction

Yet to be prescribed

• EXPENDITURE U/S 40A(2)(b) INCLUDES CAPITAL EXPENDITURE ?

.

14

DTP provisions cover payments for expenditure. Expenditure means capital as well as revenue expenditure.

• Mahendra Mills 243 ITR 56 (SC), Plasmac Machine 201 ITR 650 : capital expenditure payments eligible for depreciation are not covered under section 40A(2) of the Act.

• Depreciation is not a deduction but an allowance

Hence, capital expenditures eligible for depreciation may be excluded by taxpayers from DTP.

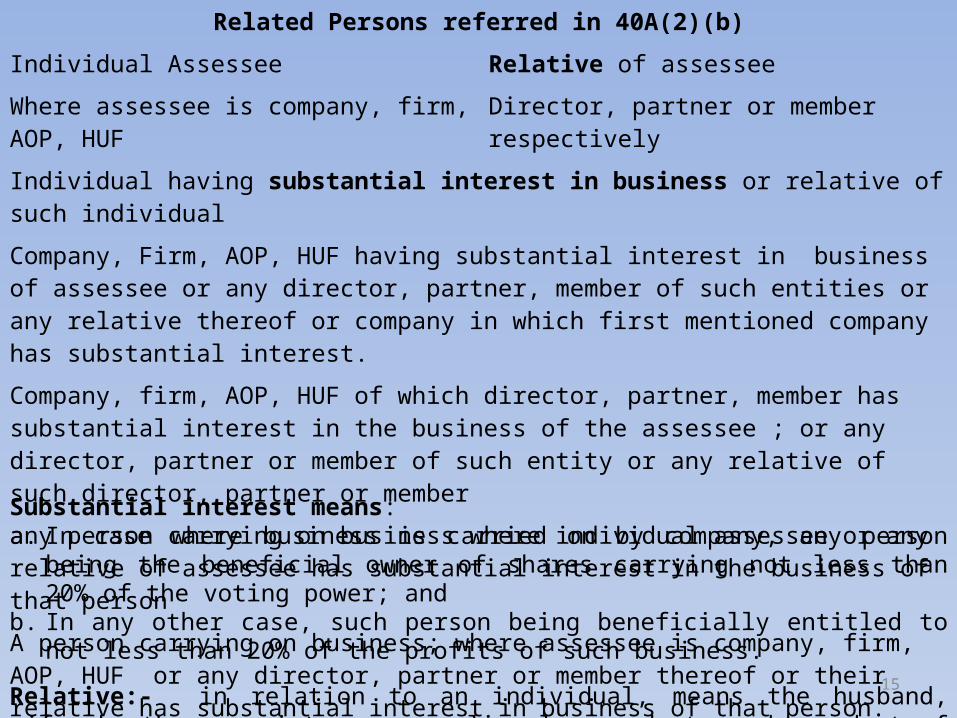

Related Persons referred in 40A(2)(b)

Individual Assessee Relative of assessee

Where assessee is company, firm, AOP, HUF Director, partner or member respectively

Individual having substantial interest in business or relative of such individual

Company, Firm, AOP, HUF having substantial interest in business of assessee or any director, partner, member of such entities or any relative thereof or company in which first mentioned company has substantial interest.Company, firm, AOP, HUF of which director, partner, member has substantial interest in the business of the assessee ; or any director, partner or member of such entity or any relative of such director, partner or member any person carrying on business where individual assessee or any relative of assessee has substantial interest in the business of that person A person carrying on business; where assessee is company, firm, AOP, HUF or any director, partner or member thereof or their relative has substantial interest in business of that person.

Substantial interest means: a. In case where business is carried on by company, any person being the beneficial owner of

shares carrying not less than 20% of the voting power; and b. In any other case, such person being beneficially entitled to not less than 20% of the profits

of such business.

Relative:- in relation to an individual, means the husband, wife, brother or sister or any lineal ascendant or descendant of that individual. 15

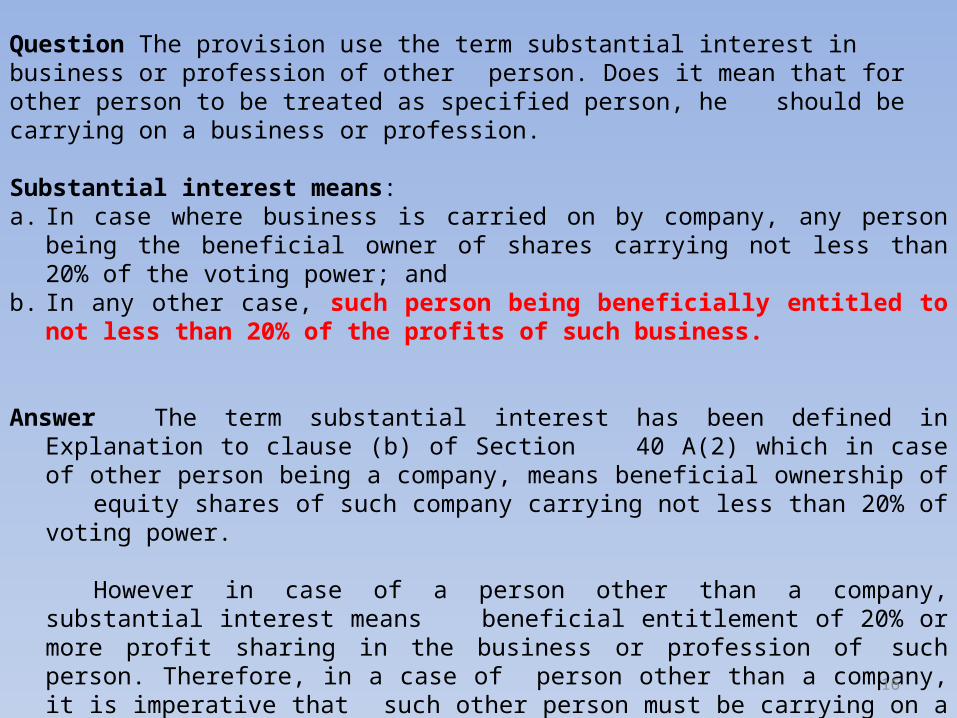

Question The provision use the term substantial interest in business or profession of other person. Does it mean that for other person to be treated as specified person, he should be carrying on a business or profession.

Substantial interest means: a. In case where business is carried on by company, any person being the beneficial owner of

shares carrying not less than 20% of the voting power; and b. In any other case, such person being beneficially entitled to not less than 20% of the profits

of such business.

Answer The term substantial interest has been defined in Explanation to clause (b) of Section 40 A(2) which in case of other person being a company, means beneficial ownership of equity shares of such company carrying not less than 20% of voting power.

However in case of a person other than a company, substantial interest means beneficial entitlement of 20% or more profit sharing in the business or profession of such person. Therefore, in a case of person other than a company, it is imperative that such other person must be carrying on a business or profession in which the taxpayer has profit sharing of less than 20%

16

DIRECT V INDIRECT OWNERSHIP

17

Whether ‘beneficial ownership’ includes direct as well as indirect shareholdings is debatable.

•NatWest Bank of UK 220 ITR 377 : beneficial owner is immediate shareholder.

• Revised ICAI Guidance Note (August 2013) on transfer pricing suggests that it may be appropriate to consider only direct shareholding and not indirect or derivative shareholding

Type of Persons When Covered

Investor Company Any Company (Say Company A) which has substantial interest in Company B (Assessee)

Sister Company Any Company in which Company A has substantial interest (i.e. Company C)

Investee Company Any company in which Company B has substantial interest (i.e. Company D)

Group Company • Any company of which a director has substantial interest in Company B • Any Company in which a director of Company B has substantial interest• Any relative of such director

Parties Covered ?A & B YesA & C YesB & C Yes

A & D No (Indirect ownership

not covered)

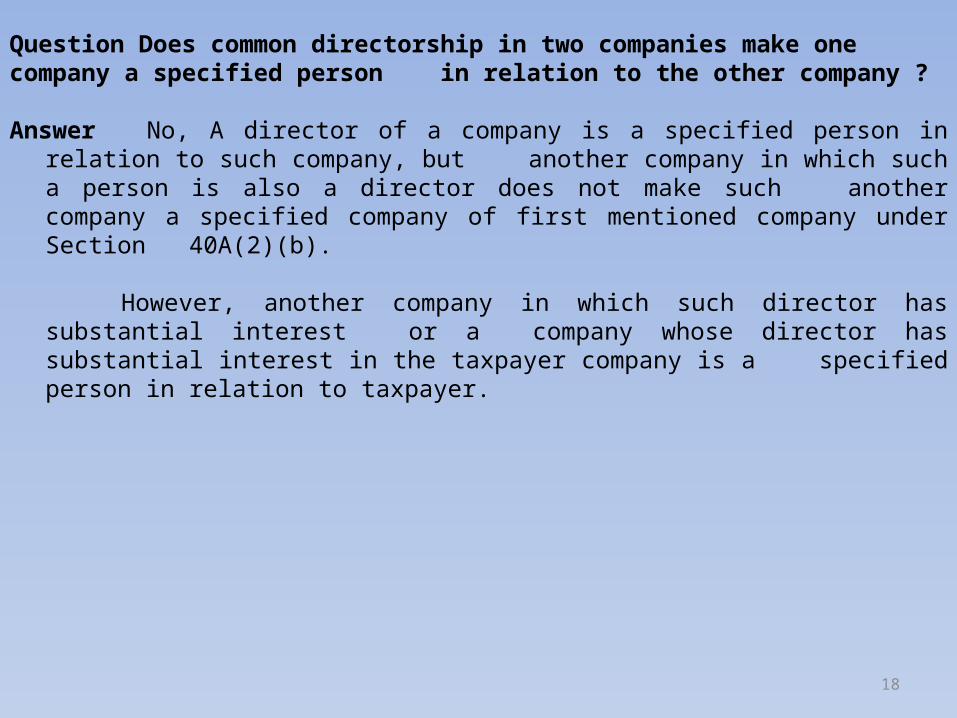

Question Does common directorship in two companies make one company a specified person in relation to the other company ?

Answer No, A director of a company is a specified person in relation to such company, but another company in which such a person is also a director does not make such another company a specified company of first mentioned company under Section 40A(2)(b).

However, another company in which such director has substantial interest or a company whose director has substantial interest in the taxpayer company is a

specified person in relation to taxpayer.

18

Case-I: Director or any relative of Director – Section 40A(2)(b)(ii)

Relative: in relation to an individual, means the husband, wife, brother or sisteror any lineal ascendant or descendant of that individual

TRANSACTIONS COVERED UNDER SECTION 40A(2)(b)

Mr. A Mr. B Mr. C

XYZ

Directors/ Partners/ Member

Relative

Covered Transaction Under Domestic Transfer Pricing 19

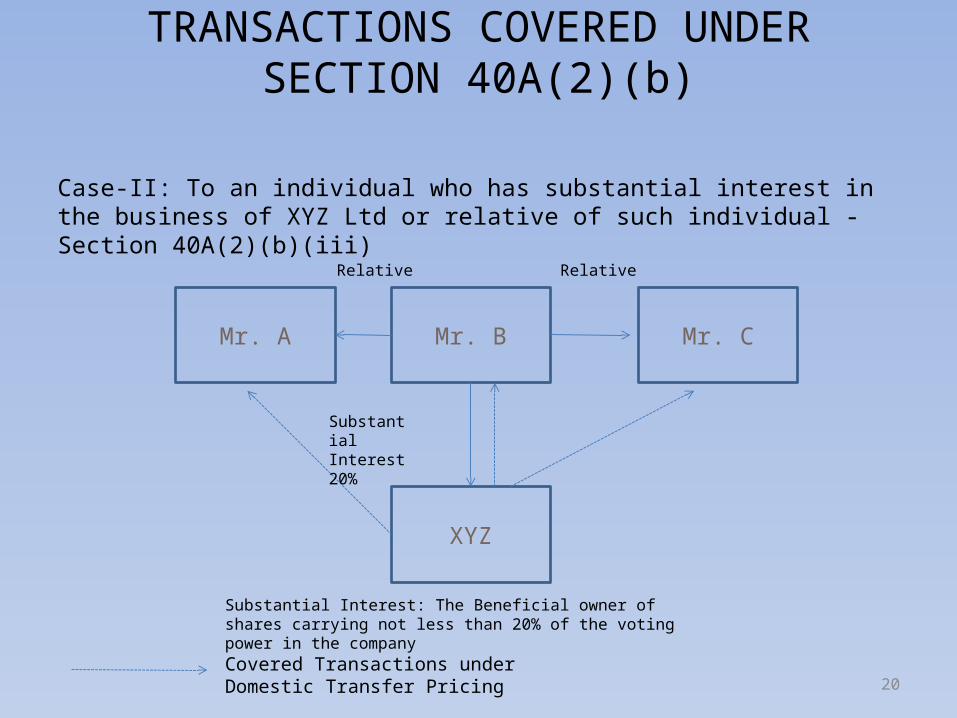

Case-II: To an individual who has substantial interest in the business of XYZ Ltd or relative of such individual - Section 40A(2)(b)(iii)

TRANSACTIONS COVERED UNDER SECTION 40A(2)(b)

Mr. A Mr. B Mr. C

XYZ

RelativeRelative

Substantial Interest 20%

Substantial Interest: The Beneficial owner of shares carrying not less than 20% of the voting power in the company

Covered Transactions under Domestic Transfer Pricing 20

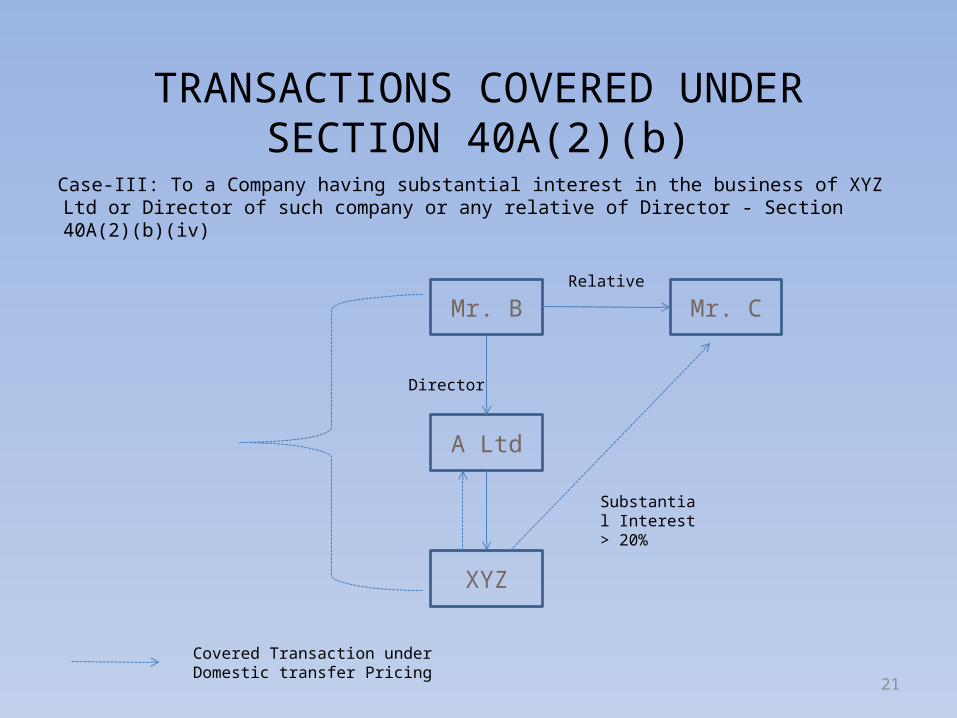

Case-III: To a Company having substantial interest in the business of XYZ Ltd or Director of such company or any relative of Director - Section 40A(2)(b)(iv)

TRANSACTIONS COVERED UNDER SECTION 40A(2)(b)

Mr. B Mr. C

A Ltd

XYZ

Relative

Director

Substantial Interest > 20%

Covered Transaction under Domestic transfer Pricing

21

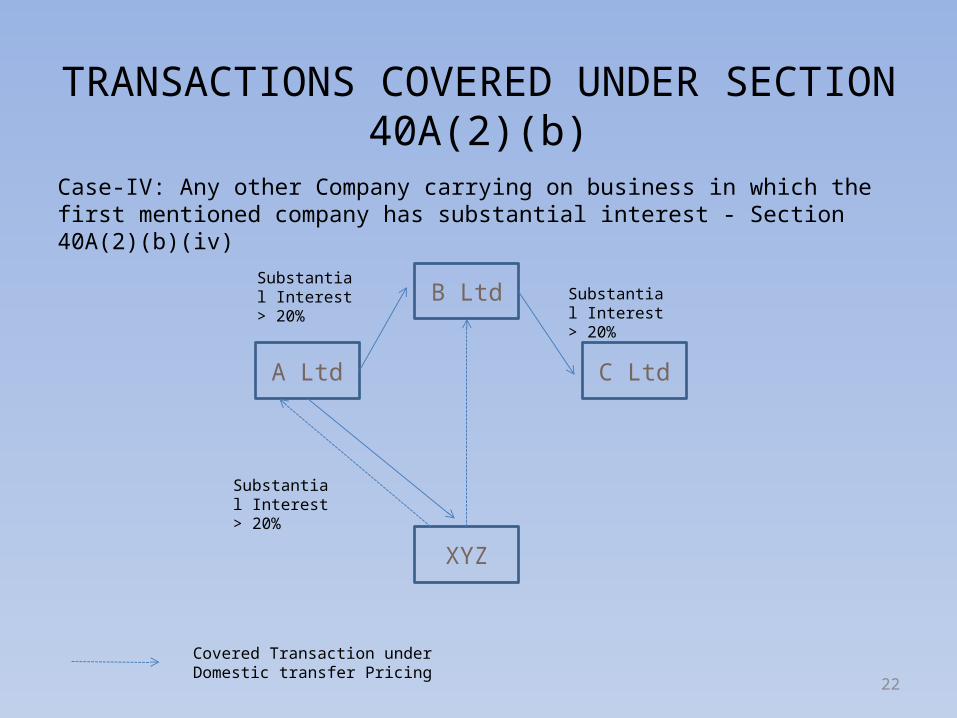

Case-IV: Any other Company carrying on business in which the first mentioned company has substantial interest - Section 40A(2)(b)(iv)

TRANSACTIONS COVERED UNDER SECTION 40A(2)(b)

B Ltd

C LtdA Ltd

XYZ

Substantial Interest > 20% Substantial

Interest > 20%

Substantial Interest > 20%

Covered Transaction under Domestic transfer Pricing

22

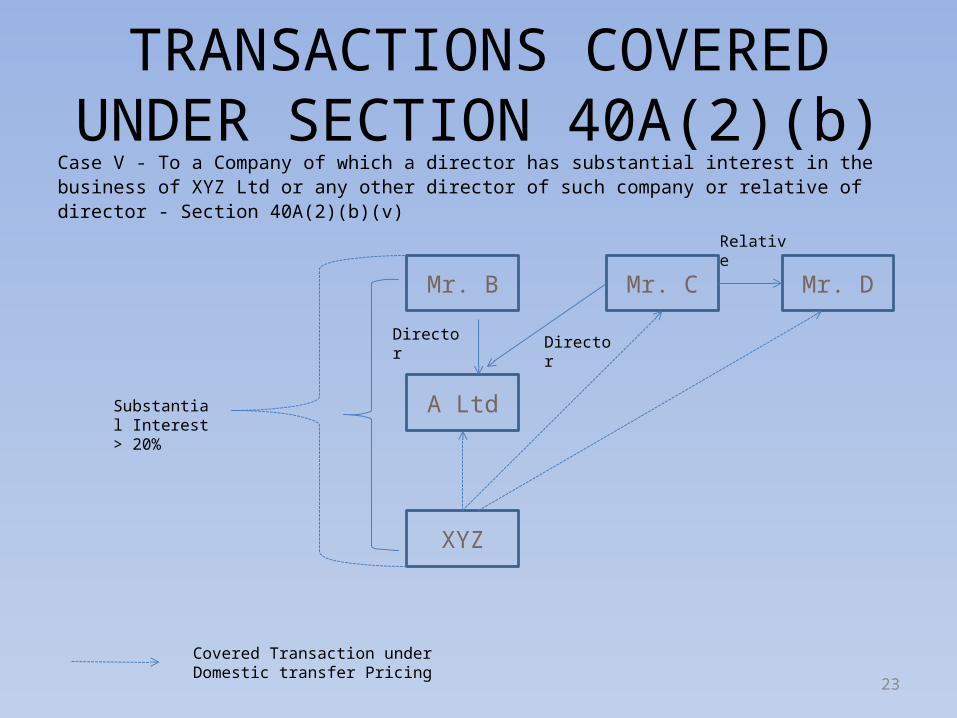

Case V - To a Company of which a director has substantial interest in the business of XYZ Ltd or any other director of such company or relative of director - Section 40A(2)(b)(v)

TRANSACTIONS COVERED UNDER SECTION 40A(2)(b)

Mr. B Mr. C Mr. D

A Ltd

XYZ

Substantial Interest > 20%

Director Director

Relative

Covered Transaction under Domestic transfer Pricing

23

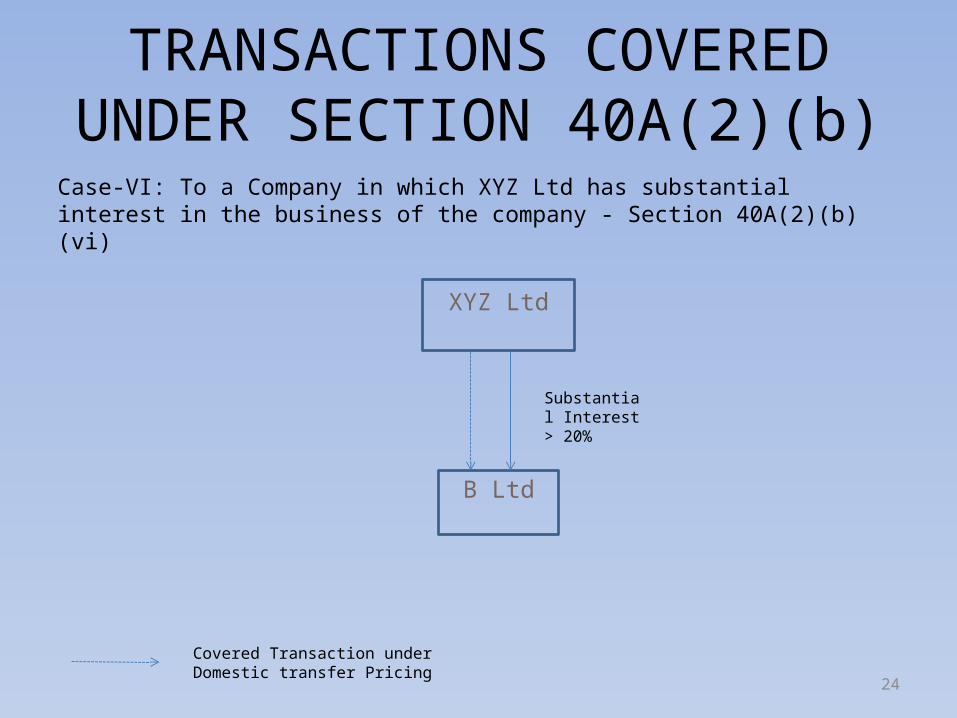

Case-VI: To a Company in which XYZ Ltd has substantial interest in the business of the company - Section 40A(2)(b)(vi)

TRANSACTIONS COVERED UNDER SECTION 40A(2)(b)

XYZ Ltd

B Ltd

Substantial Interest > 20%

Covered Transaction under Domestic transfer Pricing

24

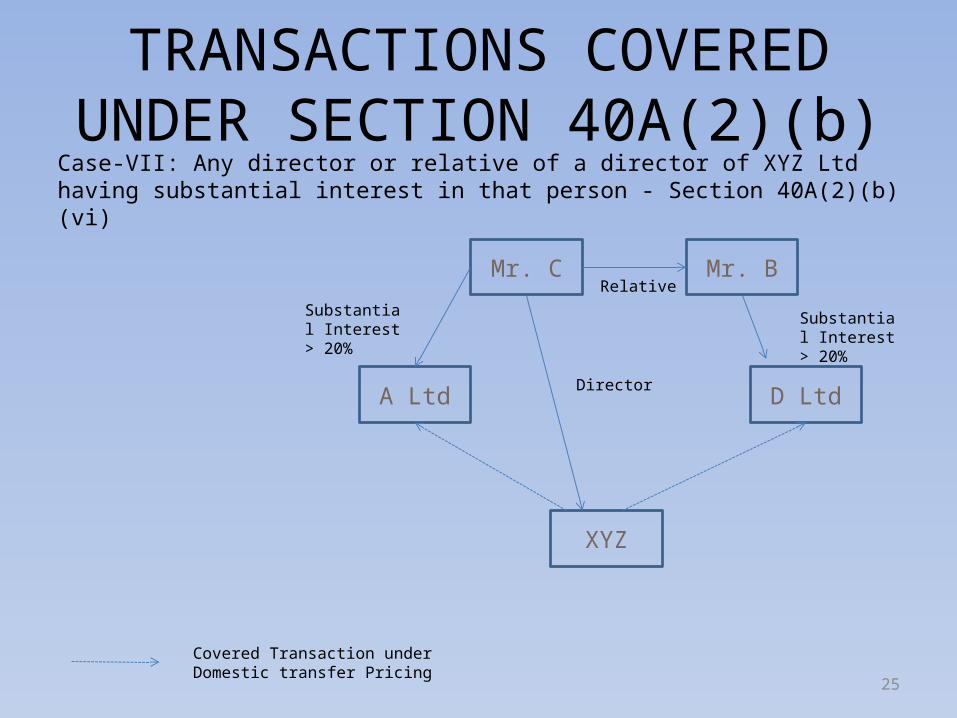

Case-VII: Any director or relative of a director of XYZ Ltd having substantial interest in that person - Section 40A(2)(b)(vi)

TRANSACTIONS COVERED UNDER SECTION 40A(2)(b)

Mr. C Mr. B

D LtdA Ltd

XYZ

Covered Transaction under Domestic transfer Pricing

Substantial Interest > 20%

Substantial Interest > 20%

Relative

Director

25

Goods & Services

Transfer at Rs 120Market Value of above goods/ services is Rs 100

Thus, the ALP of the above transaction would be Rs 100

TRANSACTIONS COVERED UNDER SECTION 80IA(8)

A Ltd.

Unit A Telecom Business

Unit B Manufacturing Business

80IA - Eligible Unit Taxable Unit

26

Goods and Services

Close Connection

80IA - Eligible Unit Taxable Unit

Operating Margin: 40% (Extraordinary Profits) Industry Average: 10%

Thus, Arm’s length profit margin would be taken as 10%

TRANSACTIONS COVERED UNDER SECTION 80IA(10)

A LtdInfrastructure Business

B LtdTrading Business

27

• For A Co– Domestic TP not applicable

transaction is of income receipt, 40A(2) not triggered

• For B Co– Covered by S. 40A(2)(b)

and hence SDT. But, payment is at < FMV, no TP adjustments required.

– S. 80-IA(10) may still be invoked on the ground that arrangement leads to more than ordinary profits?

Coverage of SDT

28

A Co B Co(WOS)

Related Parties

Tax Holiday

Unit

Sale of goods at cost < FMV

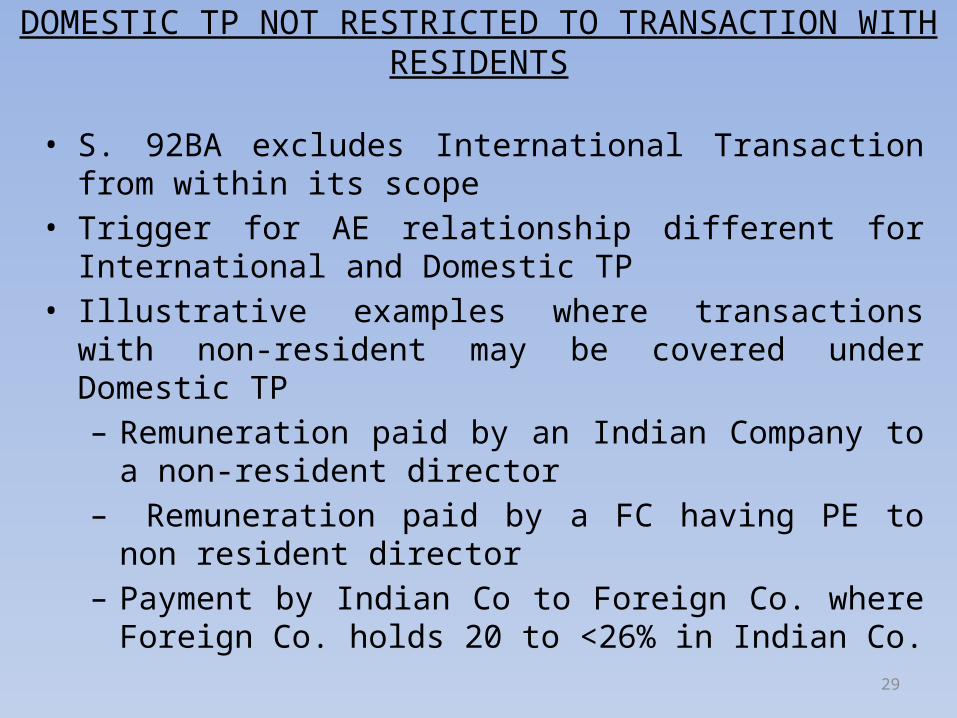

• S. 92BA excludes International Transaction from within its scope• Trigger for AE relationship different for International and

Domestic TP• Illustrative examples where transactions with non-resident may

be covered under Domestic TP– Remuneration paid by an Indian Company to a non-resident

director– Remuneration paid by a FC having PE to non resident director– Payment by Indian Co to Foreign Co. where Foreign Co. holds

20 to <26% in Indian Co.

DOMESTIC TP NOT RESTRICTED TO TRANSACTION WITH RESIDENTS

29

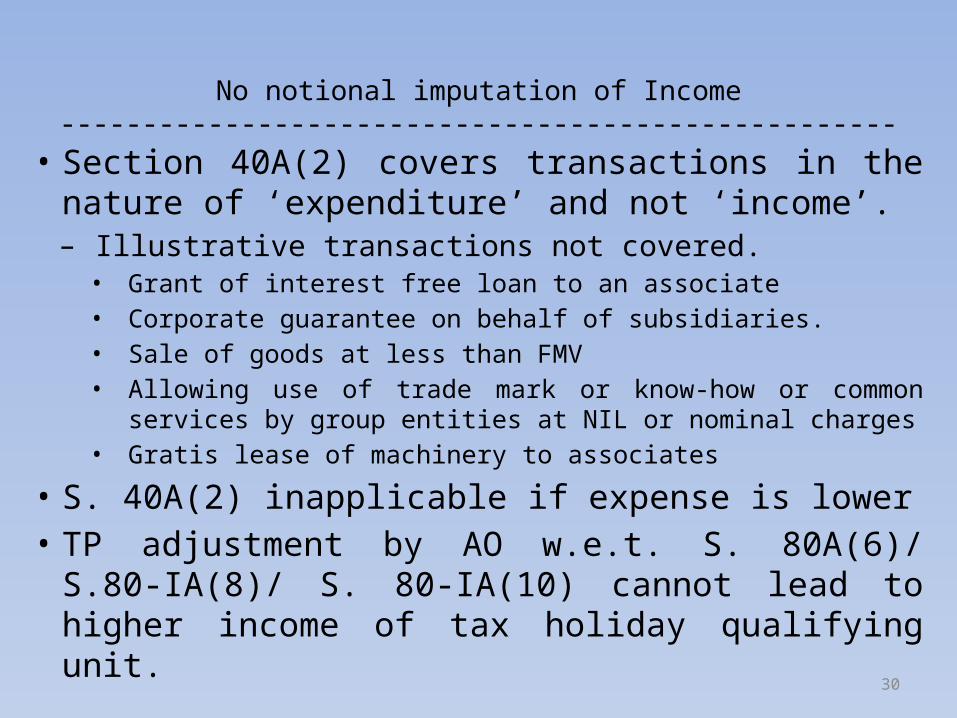

• Section 40A(2) covers transactions in the nature of ‘expenditure’ and not ‘income’.– Illustrative transactions not covered.

• Grant of interest free loan to an associate• Corporate guarantee on behalf of subsidiaries.• Sale of goods at less than FMV• Allowing use of trade mark or know-how or common

services by group entities at NIL or nominal charges• Gratis lease of machinery to associates

• S. 40A(2) inapplicable if expense is lower• TP adjustment by AO w.e.t. S. 80A(6)/ S.80-IA(8)/

S. 80-IA(10) cannot lead to higher income of tax holiday qualifying unit.

No notional imputation of Income---------------------------------------------------

30

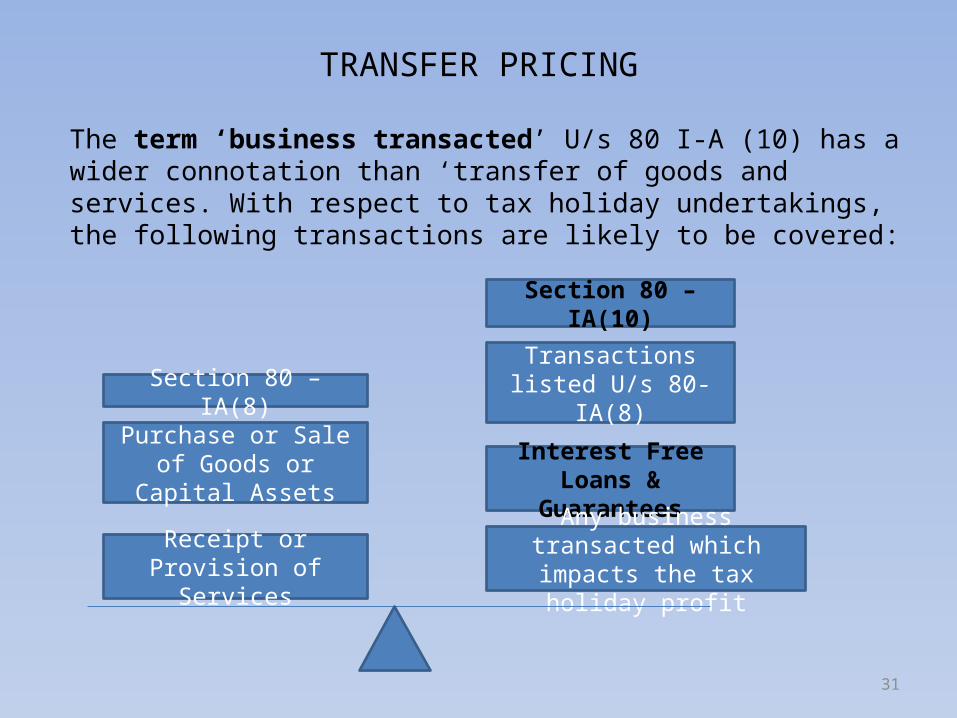

The term ‘business transacted’ U/s 80 I-A (10) has a wider connotation than ‘transfer of goods and services. With respect to tax holiday undertakings, the following transactions are likely to be covered:

TRANSFER PRICING

31

Section 80 – IA(8)

Purchase or Sale of Goods or Capital Assets

Receipt or Provision of Services

Transactions listed U/s 80-IA(8)

Section 80 – IA(10)

Interest Free Loans & Guarantees

Any business transacted which impacts the tax holiday profit

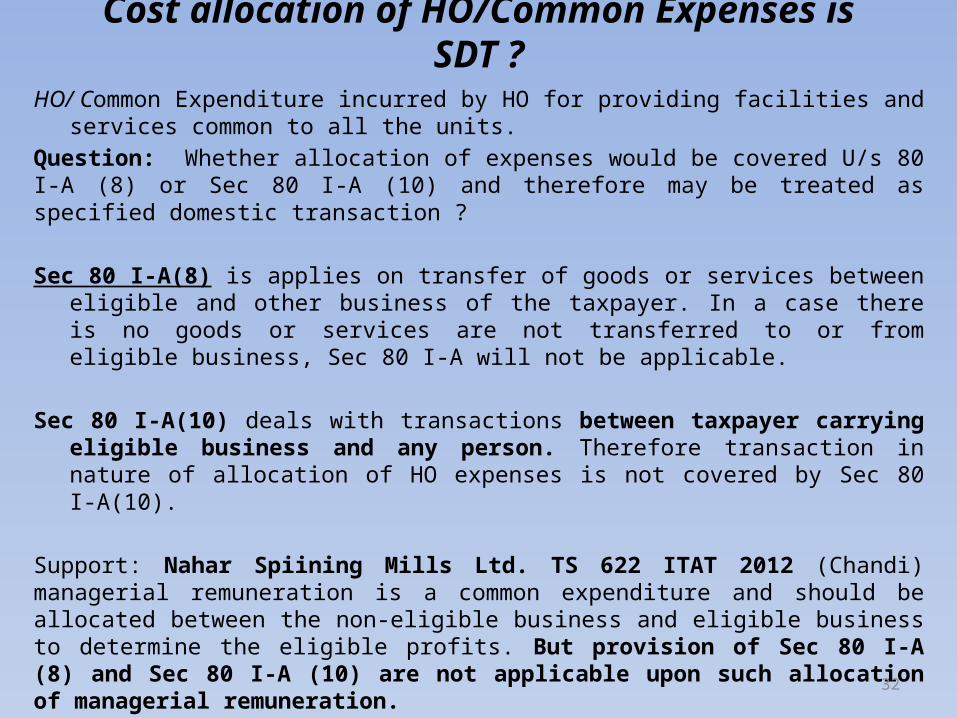

HO/ Common Expenditure incurred by HO for providing facilities and services common to all the units.

Question: Whether allocation of expenses would be covered U/s 80 I-A (8) or Sec 80 I-A (10) and therefore may be treated as specified domestic transaction ?

Sec 80 I-A(8) is applies on transfer of goods or services between eligible and other business of the taxpayer. In a case there is no goods or services are not transferred to or from eligible business, Sec 80 I-A will not be applicable.

Sec 80 I-A(10) deals with transactions between taxpayer carrying eligible business and any person. Therefore transaction in nature of allocation of HO expenses is not covered by Sec 80 I-A(10).

Support: Nahar Spiining Mills Ltd. TS 622 ITAT 2012 (Chandi) managerial remuneration is a common expenditure and should be allocated between the non-eligible business and eligible business to determine the eligible profits. But provision of Sec 80 I-A (8) and Sec 80 I-A (10) are not applicable upon such allocation of managerial remuneration.

Cost allocation of HO/Common Expenses is SDT ?

32

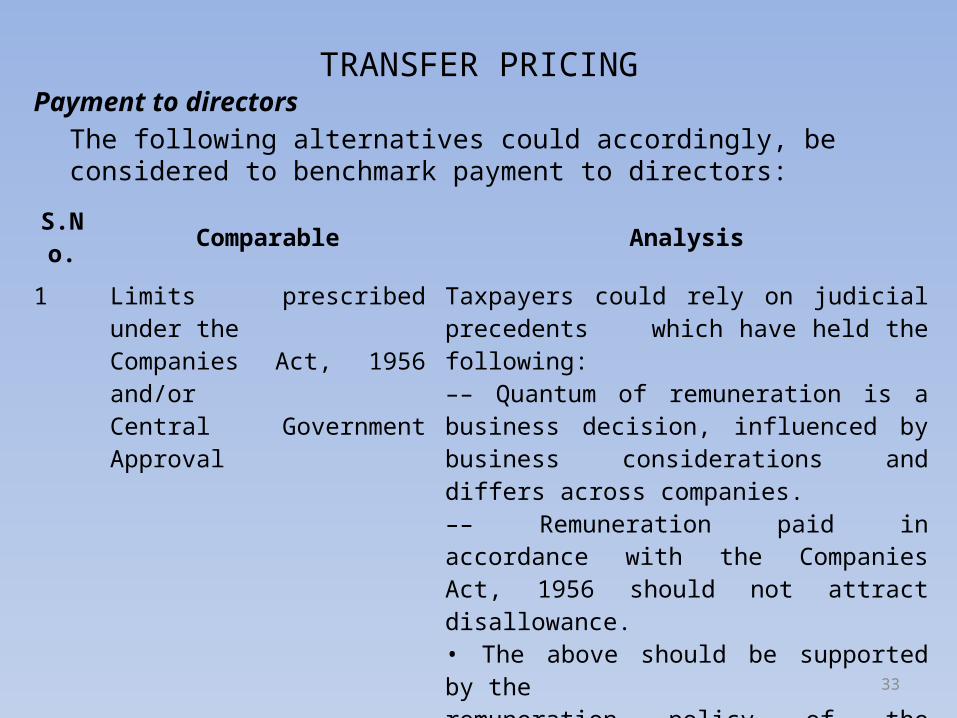

Payment to directorsThe following alternatives could accordingly, be considered to benchmark payment to directors:

TRANSFER PRICING

33

S.No. Comparable Analysis1 Limits prescribed under the

Companies Act, 1956 and/orCentral Government Approval

Taxpayers could rely on judicial precedents which have held the following:–– Quantum of remuneration is a business decision, influenced by business considerations and differs across companies.–– Remuneration paid in accordance with the Companies Act, 1956 should not attract disallowance.• The above should be supported by theremuneration policy of the company.

2 Benchmarking from external Agency

Determining the cost involved in recruitment of another personnel with similar qualifications, experience levels, skill sets and operational capabilities.

Loss-making undertakingsA tax holiday undertaking may incur a loss during the current year and have transactions covered under section 80-IA(8) or 80-IA(10). Applicability of DTP provisions to such transactions will depend upon whether such loss is required to be set off against the tax holiday profits in future years, as depicted below:

Taxpayers may argue that in the event of loss, the ‘motive’ of shifting tax holiday profits is absent and the DTP provisions should not apply. However, the treatment of the losses in future years needs to be considered in determining the approach.

TRANSFER PRICING

34

Yes

DTP provision should apply in Current Year

No

Whether Current Year losses required to be set off against future tax holiday profit

DTP provision should not apply in Current Year

Case StudyA group business development company (D Co) sets up a 100% owned special purpose vehicle (SPV) to bid for each infrastructure project, eligible for tax holidays. The construction activity is outsourced to a construction company (C Co). • D Co, SPV and C Co are related parties. Their respective functions are as under.• D Co is responsible for engaging with government agencies, Developing and

placing bids apart from undertaking routine administrative functions. • SPV enters into contract directly with the relevant government agency

awarding the project.• C Co undertakes the construction work.• The transactions subject to domestic transfer pricing are as follows:• Payment of construction charges by SPV to C Co• Debt funding of SPV by D Co• Performance guarantees provided by D Co, on behalf of SPV• Administrative costs incurred by D Co

TRANSFER PRICING

35

Q & A

Q.1 Are construction charges (typically treated as ‘capital work in progress ’) covered under SDT?

Ans. Yes. Construction charges are ‘business transacted’ between closely connected entities (i.e. C Co and SPV, a tax holiday undertaking) under section 80-IA(10). Accordingly, these must be reported in Form 3CEB applying the arm’s length test.

Q.2 Does depreciation in future years constitute SDT?Ans.No. Since construction charges are considered as SDT in earlier years, the

depreciation claim in future years should not constitute SDT.

Q.3 If the answer to #1 is yes, once it’s reported in the year of construction, is there any reporting requirement in the years when depreciation is claimed?

Ans. Ideally, no. However, one may consider disclosing as a note in Form 3CEB to that effect.

TRANSFER PRICING

36

Q & A

Q.4 Does depreciation relating to construction completed prior to FY 2012-13 (the first year of SDT applicability) constitute SDT?

Ans. No. If the construction was completed before 1 April 2012, there should not be any other implications of SDT. However, one may consider disclosing a note in Form 3CEB to that effect.

Q.5 If FY 2012-13 is the second or third year of construction that begun prior to

FY 2012-13, are construction charges incurred during FY 2012-13 covered under SDT?

Ans. Yes. However, the part of construction charges incurred prior to FY 2012-13 for the same project would not be covered under SDT requirements. That said, for arm’s length testing, one may need to take into consideration the entire transaction, which will depend on the facts of the case

TRANSFER PRICING

37

Q & A

Q.6 Debt funding and performance guarantees by D CoAns. The scope of section 80-IA(10) is wide enough to cover transactions such as

debt funding and performance guarantees provided by D Co. These would need to be transacted at arm’s length to ensure that the profits of the SPV are arrived at after considering an arm’s length charge for these transactions.

Q.7 Administrative costs incurred by D CoAns. Various costs incurred by D Co for the benefit of SPV will need to be

appropriately allocated to the SPV to ensure reasonableness of the profits of the SPV eligible for tax holiday. Whether the allocation of costs should be with or without an appropriate mark-up is not free from doubt. While the tax authorities may seek to treat the same as a service being provided by D Co, taxpayers may argue that D Co is incurring these costs on behalf of the SPV supported by cost-sharing agreements

TRANSFER PRICING

38

DOMESTIC TRANSFER PRICING COMPLIANCES

39

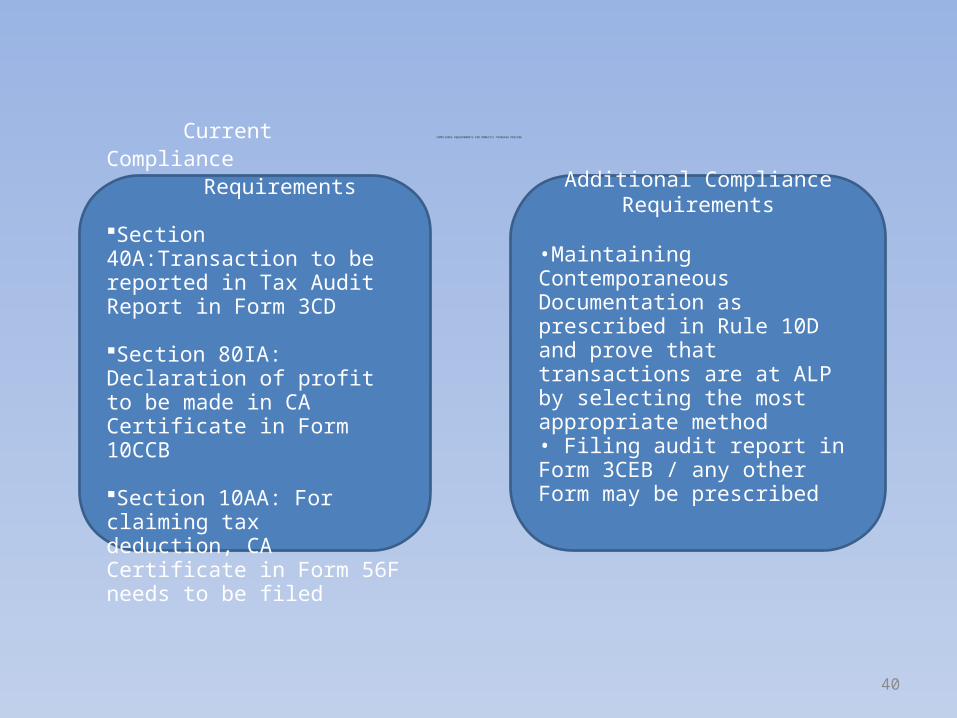

COMPLIANCE REQUIREMENTS FOR DOMESTIC TRANSFER PRICING

Current Compliance Requirements

Section 40A:Transaction to be reported in Tax Audit Report in Form 3CD

Section 80IA: Declaration of profit to be made in CA Certificate in Form 10CCB

Section 10AA: For claiming tax deduction, CA Certificate in Form 56F needs to be filed

Additional ComplianceRequirements

•Maintaining ContemporaneousDocumentation as prescribed in Rule 10D and prove thattransactions are at ALP by selecting the most appropriate method • Filing audit report in Form 3CEB / any other Form may be prescribed

40

ALPDOMESTIC TRANSFER PRICING - PROCESS FLOW

Identification ofSpecified Domestic Transactions

Determination of ALP

VoluntaryAdjustments inReturn (if any)

FAR AnalysisSelection of Most

Appropriate Method

Documentation,Return Filing andForm 3CEB Filing

Identification of comparable transactions

EstablishingComparability,adjustment for

differences

Assessment and Appellate Proceedings

41

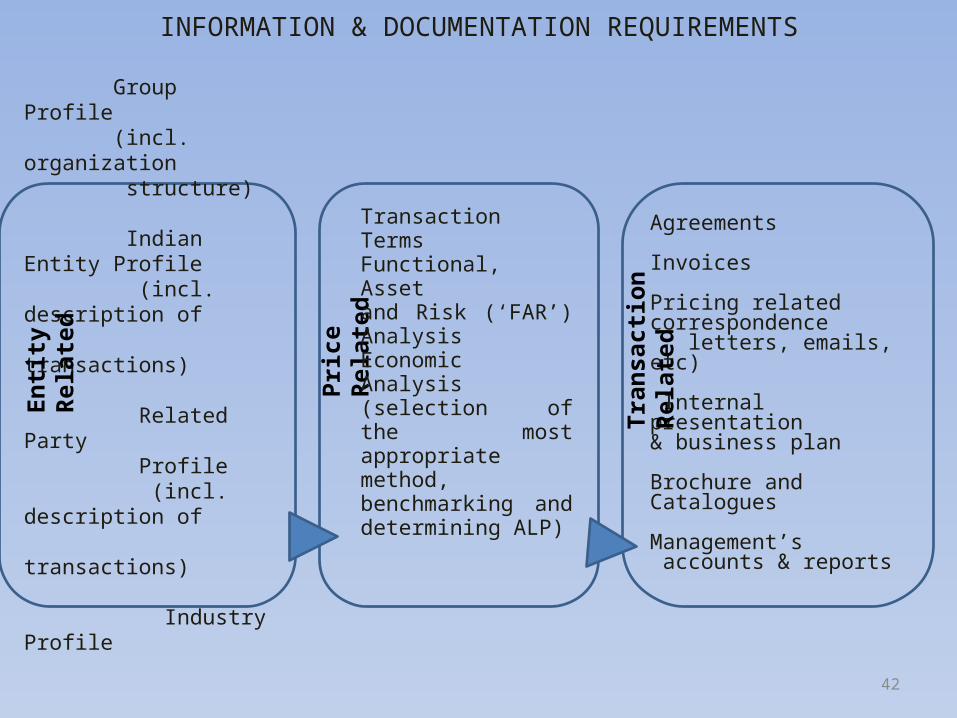

INFORMATION & DOCUMENTATION REQUIREMENTS

Group Profile (incl. organization structure)

Indian Entity Profile (incl. description of transactions)

Related Party Profile (incl. description of transactions)

Industry Profile

Agreements

Invoices

Pricing relatedcorrespondence letters, emails, etc) Internal presentation & business plan

Brochure andCatalogues Management’s accounts & reports

Entit

y Re

late

d

Tran

sacti

on R

elat

ed

Pric

e R

elat

ed

Transaction Terms Functional, Asset and Risk (‘FAR’) Analysis Economic Analysis (selection of the most appropriate method, benchmarking and determining ALP)

42

COMMON TRANSACTIONS DOCUMENTATION

Transaction entered Documents to be maintained

Purchase/ Sale of raw material

-Invoices- purchase/ Sale order- product details- Sale Details if sold to 3rd Party

-Pricing strategy- proof of price negotiation- Quotes from competitors- Terms of payment

Remuneration to Directors

-Qualification- Work experience & profile- Minutes of Meeting authorizing- the Director’s remuneration

- Data from HR firms for Directors in the same line of Business

Corporate Cost sharing -Nature of expenses- Auditor’s certificate allocating the expenses

-Basis of allocation between the companies- proof of usage (rendering) of services- Cost Benefit analysis

43

COMMON TRANSACTIONS DOCUMENTATION

Transaction entered Documents to be maintained

Rent paid toward use of premises

- rent receipts- Documents suggesting the rent of the surrounding area

-Rental agreement- Fair market Value of the property (municipal Valuation, only if higher than actual rent paid)

Reimbursement of expenses

-Nature of expenses with detailed break up- reason of expense incurred for

-Employee Details-Actual invoice of the expense

Interest on loan (non financial service company)

- Basis of determination of Interest rate - Interest rate card for the period of loan

-Loan agreement- Basis on which the interest rate is pegged above standard rate

44

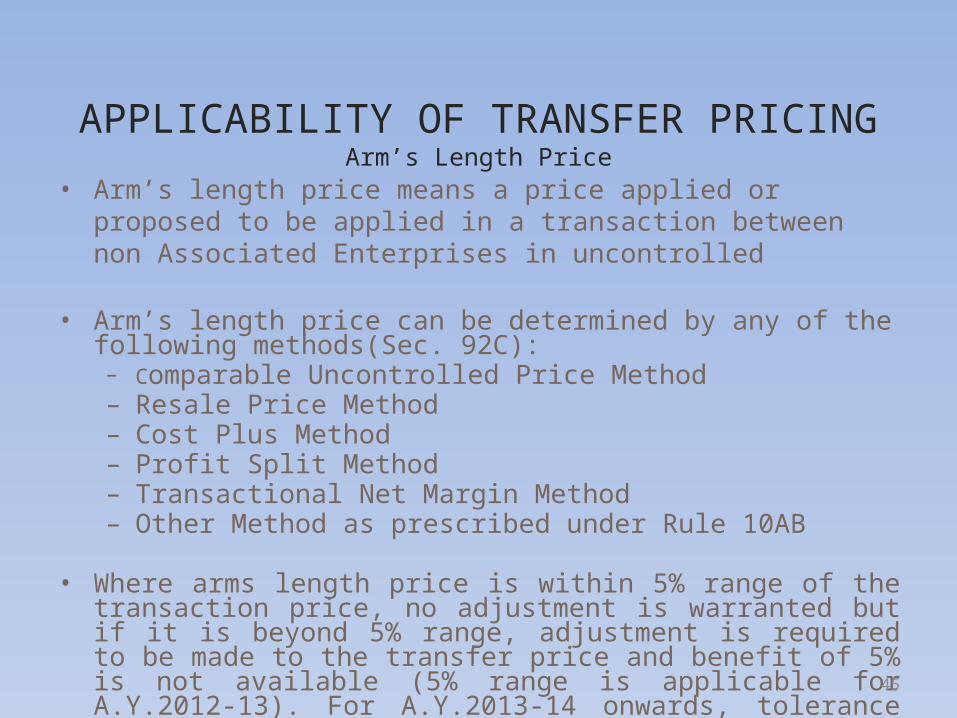

• Arm’s length price means a price applied or proposed to be applied in a transaction between non Associated Enterprises in uncontrolled

• Arm’s length price can be determined by any of the following methods(Sec. 92C):– Comparable Uncontrolled Price Method– Resale Price Method– Cost Plus Method– Profit Split Method– Transactional Net Margin Method– Other Method as prescribed under Rule 10AB

• Where arms length price is within 5% range of the transaction price, no adjustment is warranted but if it is beyond 5% range, adjustment is required to be made to the transfer price and benefit of 5% is not available (5% range is applicable for A.Y.2012-13). For A.Y.2013-14 onwards, tolerance range would be notified by the central government subject to maximum 3%.

APPLICABILITY OF TRANSFER PRICINGArm’s Length Price

45

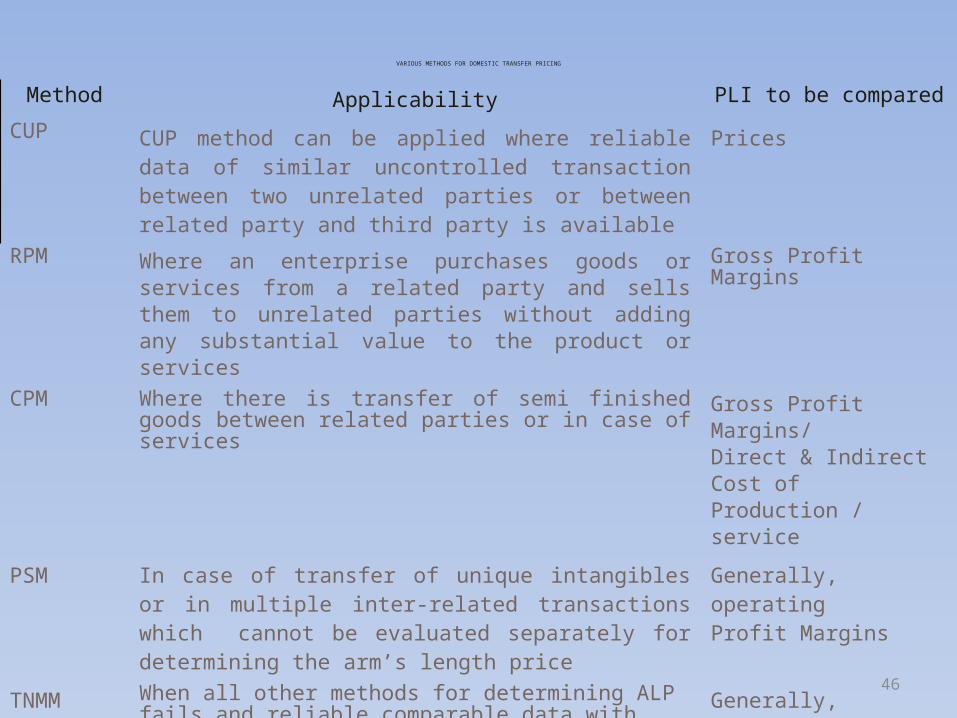

VARIOUS METHODS FOR DOMESTIC TRANSFER PRICING

Method Applicability PLI to be compared

CUP CUP method can be applied where reliable data of similar uncontrolled transaction between two unrelated parties or between related party and third party is available

Prices

RPM Where an enterprise purchases goods or services from a related party and sells them to unrelated parties without adding any substantial value to the product or services

Gross Profit Margins

CPM Where there is transfer of semi finished goods between related parties or in case of services

Gross Profit Margins/Direct & Indirect Cost of Production / service

PSM In case of transfer of unique intangibles or in multiple inter-related transactions which cannot be evaluated separately for determining the arm’s length price

Generally, operatingProfit Margins

TNMM When all other methods for determining ALP fails and reliable comparable data with broad functional similarity is available

Generally, operatingProfit Margins

Other Method as per Rule 10AB

Where the price which would be charged for similar transaction between unrelated parties is available (based on the valuation reports, genuine quotes available from independent parties, etc)

Such "would be Price“46

• Internal CUP

Comparable Uncontrolled Price Method----------------------------------------------------

47

Manufacturer A

Sale to related party B

Sale to non-related party C

• External CUP (Unrelated Parties)

Non-related party P Non-related party Q

Adjustments permitted for volume discount, geographical differences, etc.

• Compares the resale gross margin earned by AE, with gross margin of comparable independent distributors

Resale Price Method (RPM)---------------------------------------------------

48

Group Manufacturer (Eligible Unit)

Related Distributor (India)

Unrelated Wholesalers

INR 75 INR 100

• Comparable need not be in very same product• Software distributor compared with FMCG distributor

• Used predominantly when AE works for another AE as contract manufactures.

Cost Plus Method (CPM) (C+)---------------------------------------------------

49

ALP =Direct & Indirect Cost of Production / service

+ Comparable Margin

• Typically applied to a contract manufacturer who:• Does not bear risk of marketing• Does not “normally” undertake high skill work

• May apply to contract manufacture, BPO, call centre, software developers, etc.

• Generally applicable in case of transaction involving– Transfer of unique intangibles

OR– Multiple transactions which are interrelated not

permitting separate evaluation• Split global profit according to contribution of

each AE.

Profit Split Method (PSM)---------------------------------------------------

50

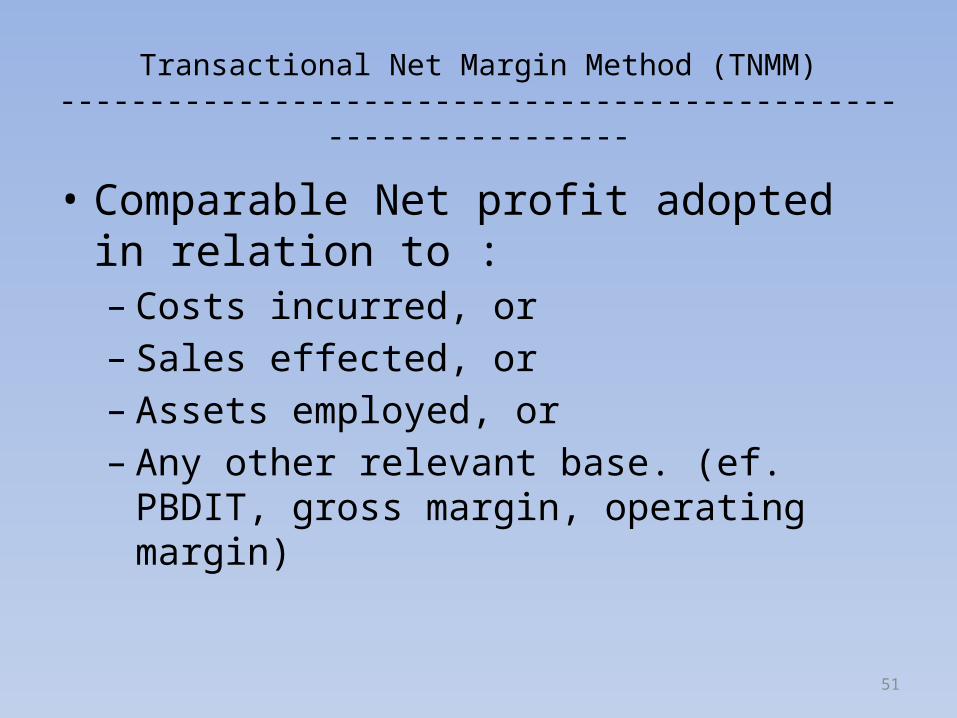

• Comparable Net profit adopted in relation to :– Costs incurred, or– Sales effected, or– Assets employed, or– Any other relevant base. (ef. PBDIT, gross margin,

operating margin)

Transactional Net Margin Method (TNMM)----------------------------------------------------------------

51

Rule 10AB of the I.T Rules’1962, the arm’s length price under the any other method is determined in the following manner

“For the purposes of clause (f) of sub-section (1) of section 92C, the other method for determination of the arms' length price in relation to an international transaction [or a specified domestic transaction] shall be any method which takes into account the price which has been charged or paid, or would have been charged or paid, for the same or similar uncontrolled transaction, with or between non-associated enterprises, under similar circumstances, considering all the relevant facts”

Examples: A. Valuation Report prepared on discounted cash flow method (DCF)B. Quotations from Third PartyC. LIBOR used for Inter Company BorrowingsD. Stock ExchangesE. Cost Allocation/ApportionmentF. Tender/Bid Document

Any Other Method (Rule 10AB)----------------------------------------------------------------

52

Selection of Most Appropriate Method (MAM)

Rule 10C of I.T Rules’1962 requires the satisfaction of two primary conditions for the selection of any method as the MAM:

(a). It should be best suited on the facts and circumstances of an international transaction

(b). The method should provide the most reliable measure of an Arm’s Length Price in relation to the International Transaction.

EXAMPLEWhere an enterprise A ltd. who is a manufacturer of lamps engages in an international transaction to sell 500 lamps to its Associated Enterprise B ltd. & Associated Enterprise C Ltd. in Canada. B ltd has sold 1000 similar lamps to an unrelated enterprise D ltd. in Canada at a discount of 1%. Having regard to the provisions of Rule the selection of MAM may be made in the following manner: 53

.

54

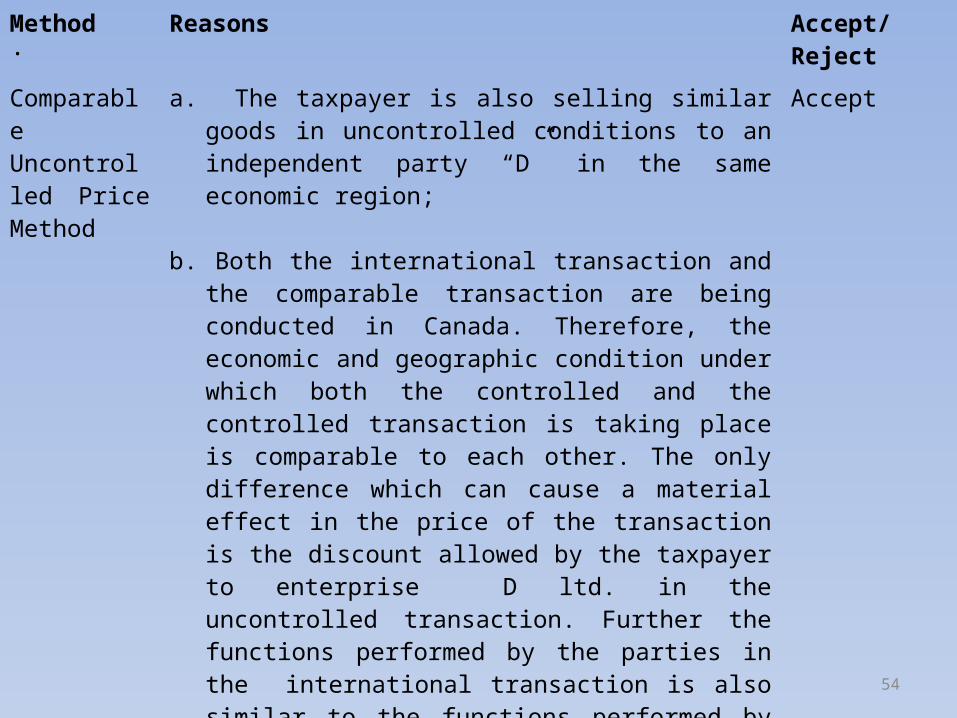

Method Reasons Accept/Reject

Comparable Uncontrolled Price Method

a. The taxpayer is also selling similar goods in uncontrolled conditions to an independent party “D” in the same economic region;

b. Both the international transaction and the comparable transaction are being conducted in Canada. Therefore, the economic and geographic condition under which both the controlled and the controlled transaction is taking place is comparable to each other. The only difference which can cause a material effect in the price of the transaction is the discount allowed by the taxpayer to enterprise D ltd. in the uncontrolled transaction. Further the functions performed by the parties in the international transaction is also similar to the functions performed by the parties to the uncontrolled transaction;

c. Accurate adjustments can be made for the differences arising in the two transactions on account of discount allowed by the taxpayer in the uncontrolled transactions;

Accept

.

55

Method Reasons Accept/Reject

Resale Price Method

The International transaction is a transaction of sale of goods. Resale price method is used to determine the Arm’s Length Price in case of Purchase Transaction where the tested party is only conducting distribution activities. Hence the nature of the transaction does not support the use of Resale Price Method. Hence Resale Price Method may not be selected as the MAM as it does not fulfill the conditions specified in clause (a) of Rule 10C

Reject

Cost Plus Method

Although the nature of the international transaction supports the use of Cost Plus Method, the details of direct and indirect costs incurred in the international transaction is not available. Therefore this method cannot be selected as the MAM due to the lack of the information required to apply this method. Hence cost plus method may not be selected as the MAM as it does not fulfill the conditions specified in clause (c) of Rule 10C

Reject

.

56

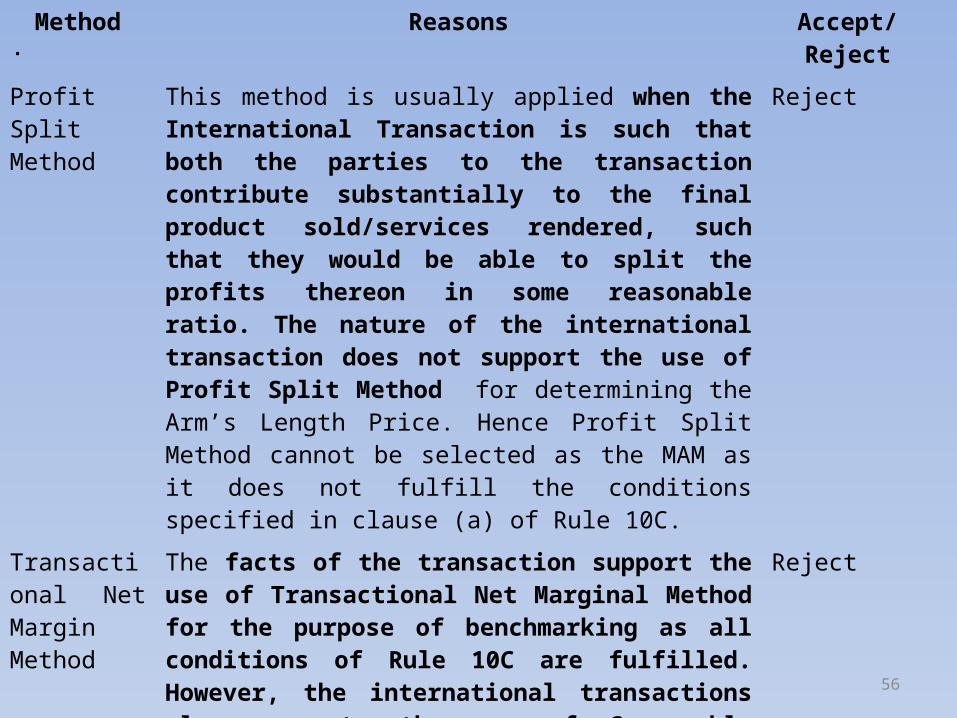

Method Reasons Accept/Reject

Profit Split Method

This method is usually applied when the International Transaction is such that both the parties to the transaction contribute substantially to the final product sold/services rendered, such that they would be able to split the profits thereon in some reasonable ratio. The nature of the international transaction does not support the use of Profit Split Method for determining the Arm’s Length Price. Hence Profit Split Method cannot be selected as the MAM as it does not fulfill the conditions specified in clause (a) of Rule 10C.

Reject

Transactional Net Margin Method

The facts of the transaction support the use of Transactional Net Marginal Method for the purpose of benchmarking as all conditions of Rule 10C are fulfilled. However, the international transactions also supports the use of Comparable Uncontrolled Price method for determining its ALP . Keeping in mind the fact that the Comparable Uncontrolled Price Method may provide more appropriate results with regard to the ALP in comparison to the Transactional Net Margin Method, this method may not be selected as the MAM to determine the ALP of the international transaction.

Reject

.

57

Method Reasons Accept/Reject

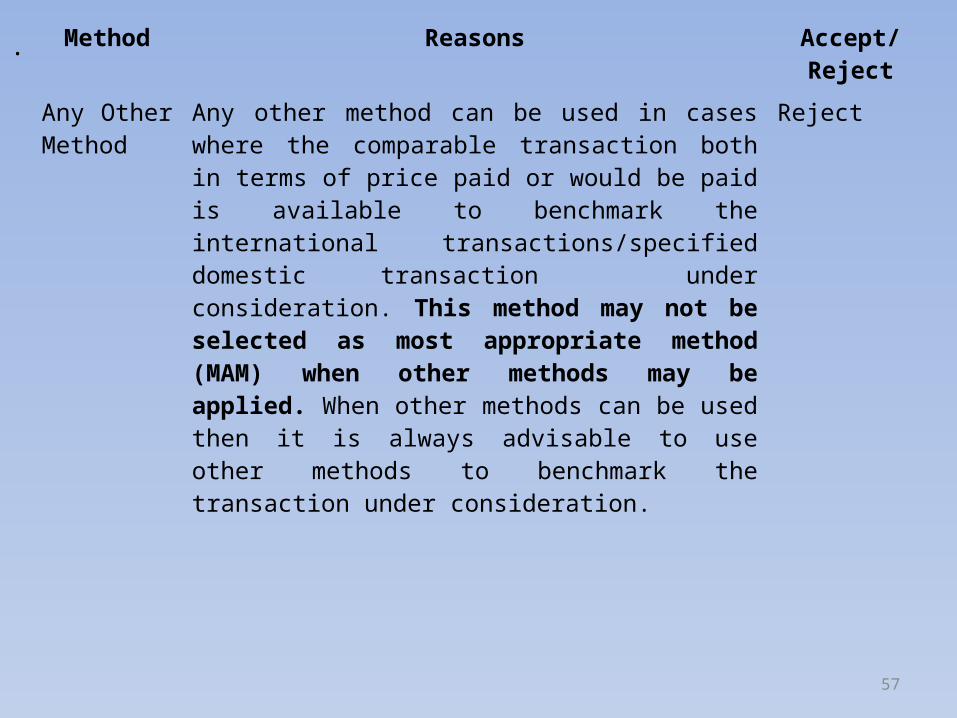

Any Other Method

Any other method can be used in cases where the comparable transaction both in terms of price paid or would be paid is available to benchmark the international transactions/specified domestic transaction under consideration. This method may not be selected as most appropriate method (MAM) when other methods may be applied. When other methods can be used then it is always advisable to use other methods to benchmark the transaction under consideration.

Reject

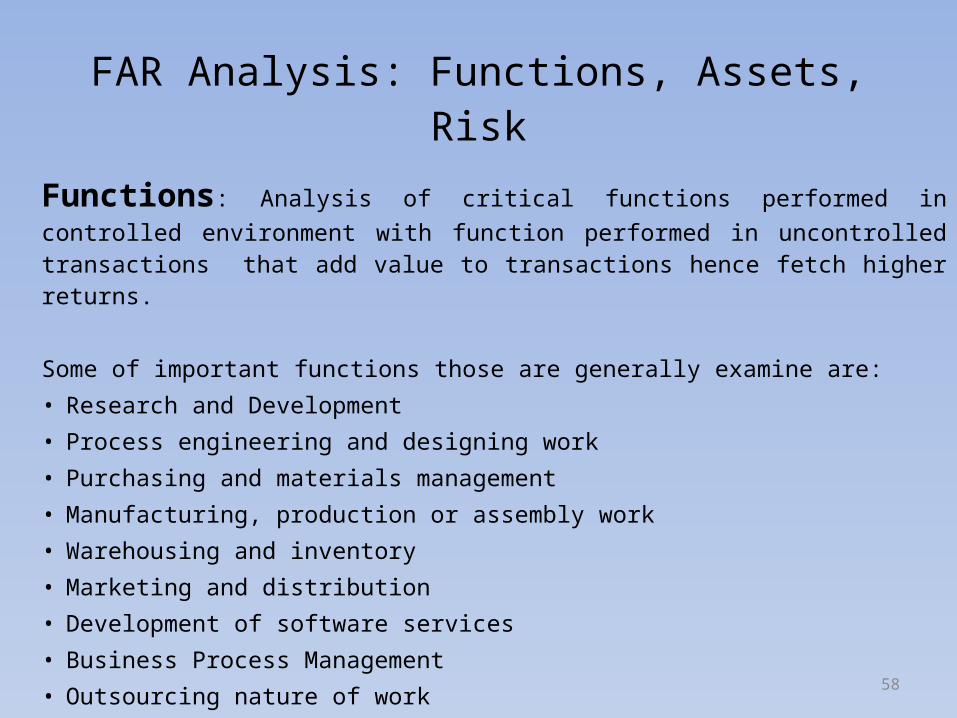

Functions: Analysis of critical functions performed in controlled environment with function performed in uncontrolled transactions that add value to transactions hence fetch higher returns.

Some of important functions those are generally examine are:• Research and Development • Process engineering and designing work• Purchasing and materials management• Manufacturing, production or assembly work• Warehousing and inventory• Marketing and distribution• Development of software services• Business Process Management• Outsourcing nature of work

FAR Analysis: Functions, Assets, Risk

58

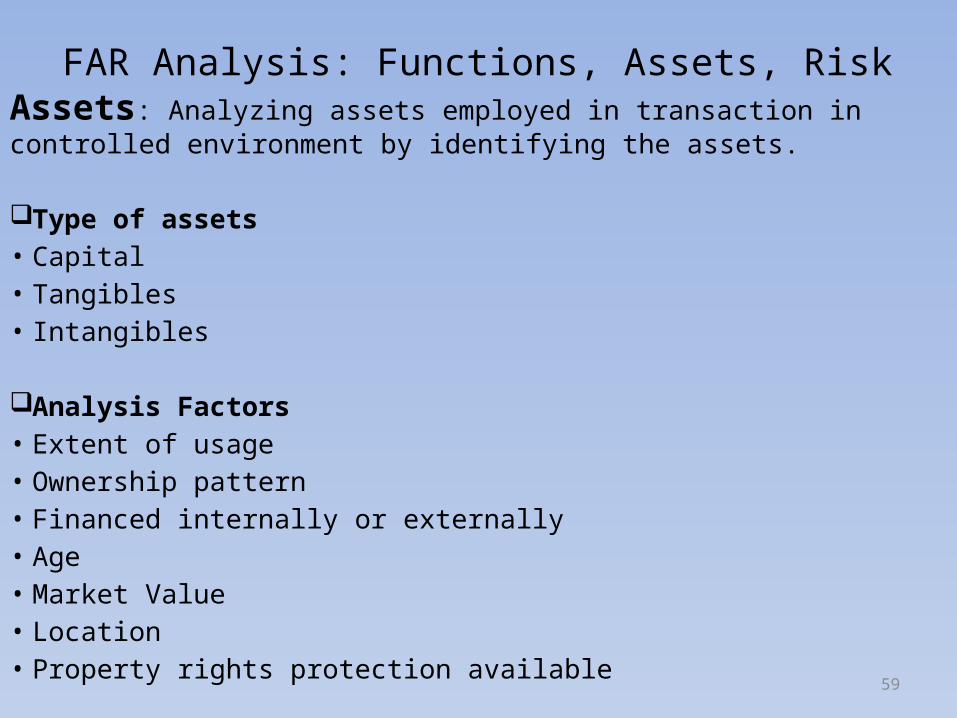

Assets: Analyzing assets employed in transaction in controlled environment by identifying the assets.

Type of assets• Capital • Tangibles• Intangibles

Analysis Factors • Extent of usage • Ownership pattern• Financed internally or externally • Age• Market Value• Location• Property rights protection available

FAR Analysis: Functions, Assets, Risk

59

Risk: Analysis involve identification of various risk assumed by each party in controlled transaction.

FAR Analysis: Functions, Assets, Risk

Financial Risk Product Risk Market Risk Collection Risk

Entrepreneurial Risk

Method of Funding

Design & Development of product

Development of market

Bad Debt Risk

Risk of loss of capital investment

Funding of losses

Up gradation / obsolescence of product

Product Promotion and Advertisement

Foreign Exchange Risk

After sales Service

Fluctuation in demand & prices

Product Liability Risk

Business cycle risk

Intellectual Property Risk

60

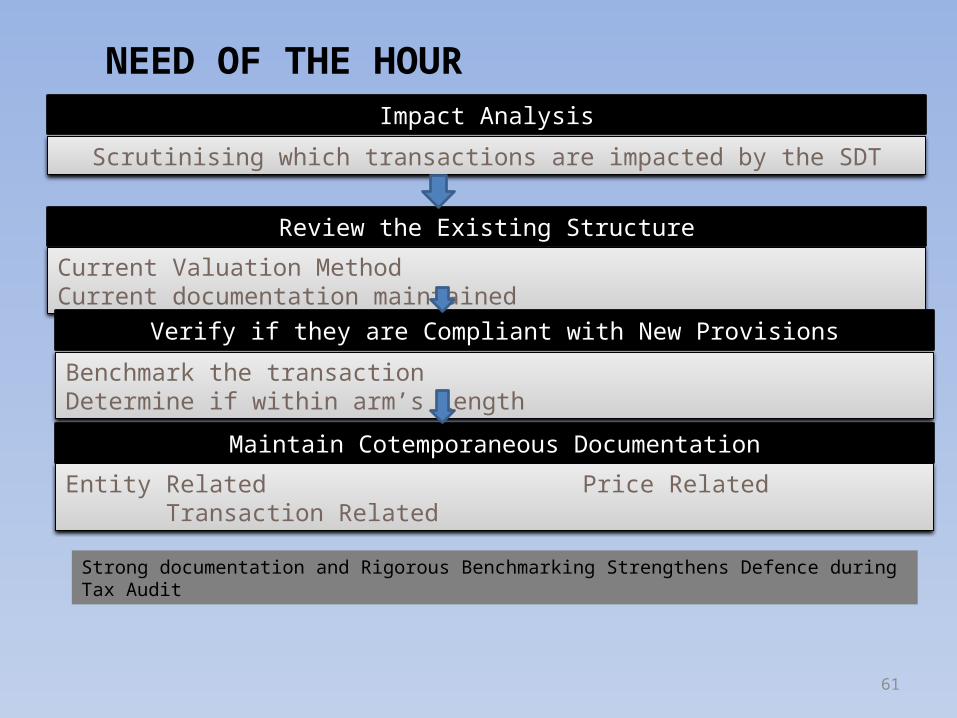

NEED OF THE HOURImpact Analysis

Scrutinising which transactions are impacted by the SDT

Strong documentation and Rigorous Benchmarking Strengthens Defence during Tax Audit

Review the Existing Structure

Current Valuation Method Current documentation maintained

Verify if they are Compliant with New Provisions

Benchmark the transaction Determine if within arm’s length

Maintain Cotemporaneous Documentation

Entity Related Price Related Transaction Related

61

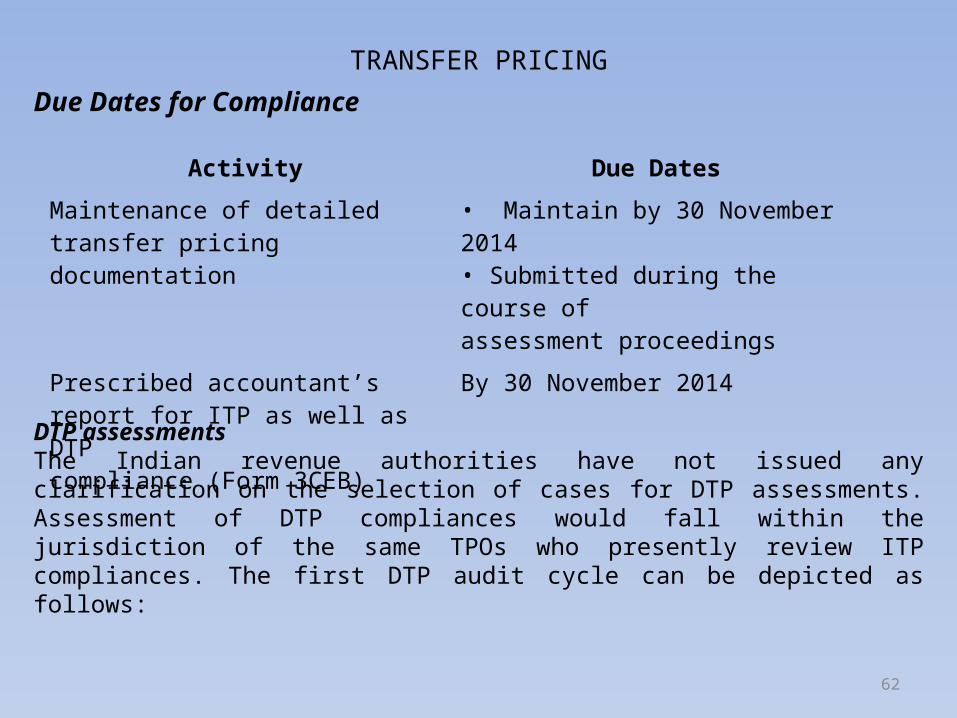

Due Dates for Compliance

TRANSFER PRICING

62

Activity Due Dates

Maintenance of detailedtransfer pricing documentation

• Maintain by 30 November 2014• Submitted during the course ofassessment proceedings

Prescribed accountant’sreport for ITP as well as DTPcompliance (Form 3CEB)

By 30 November 2014

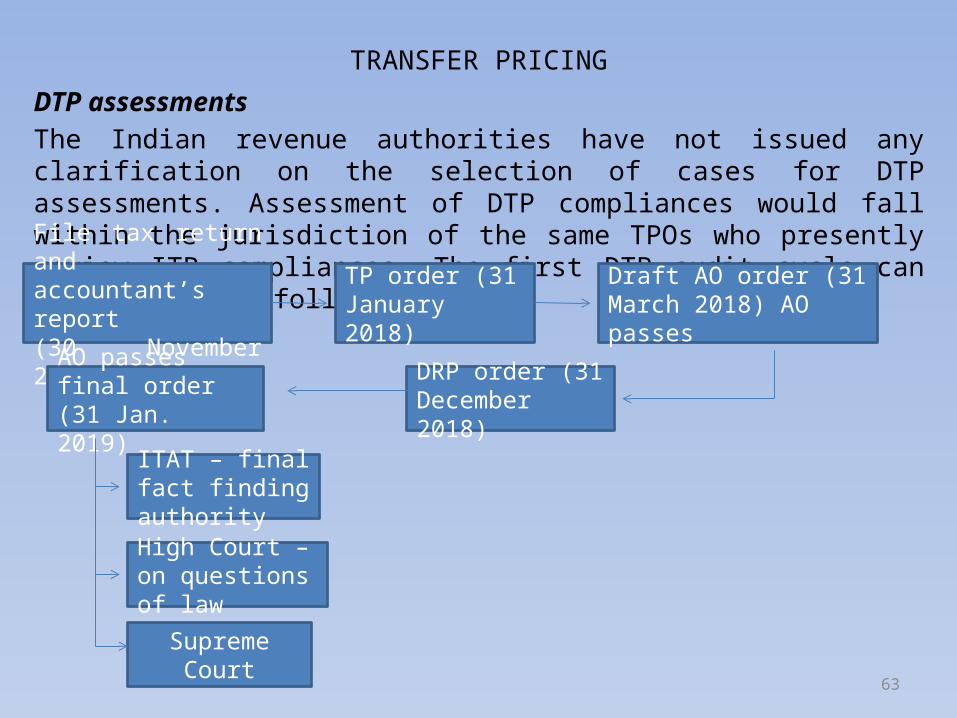

DTP assessmentsThe Indian revenue authorities have not issued any clarification on the selection of cases for DTP assessments. Assessment of DTP compliances would fall within the jurisdiction of the same TPOs who presently review ITP compliances. The first DTP audit cycle can be depicted as follows:

DTP assessmentsThe Indian revenue authorities have not issued any clarification on the selection of cases for DTP assessments. Assessment of DTP compliances would fall within the jurisdiction of the same TPOs who presently review ITP compliances. The first DTP audit cycle can be depicted as follows:

TRANSFER PRICING

63

File tax return and accountant’s report(30 November 2014)

TP order (31 January 2018)

ITAT – final fact finding authority

Draft AO order (31 March 2018) AO passes

AO passes final order (31 Jan. 2019)

Supreme Court

High Court – on questions of law

DRP order (31 December 2018)

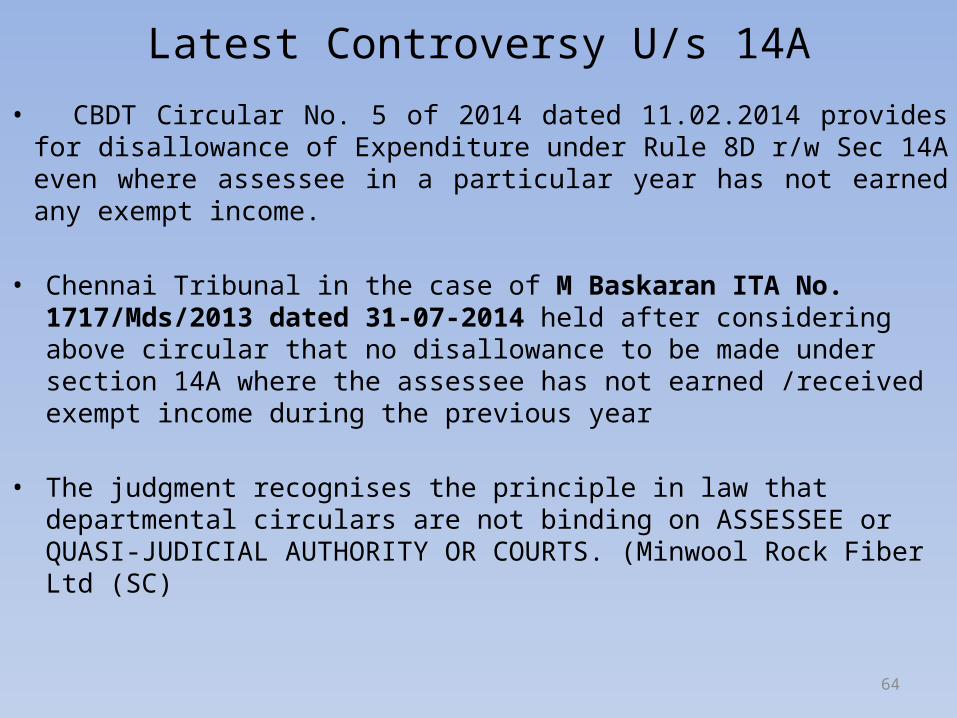

• CBDT Circular No. 5 of 2014 dated 11.02.2014 provides for disallowance of Expenditure under Rule 8D r/w Sec 14A even where assessee in a particular year has not earned any exempt income.

• Chennai Tribunal in the case of M Baskaran ITA No. 1717/Mds/2013 dated 31-07-2014 held after considering above circular that no disallowance to be made under section 14A where the assessee has not earned /received exempt income during the previous year

• The judgment recognises the principle in law that departmental circulars are not binding on ASSESSEE or QUASI-JUDICIAL AUTHORITY OR COURTS. (Minwool Rock Fiber Ltd (SC)

Latest Controversy U/s 14A

64

THANK YOU

65