introduction to insurance rating and reserving.pdf

TRANSCRIPT

Introduction to insurance rating and claims reserving

Presented to The Lloyd’s Marine U35 Group

by

Ana Mata, PhD, ACAS

Managing Director and Actuary

London, June 2014

Matβlas Underwriting and Actuarial Consulting, Training and Research

Introduction to insurance rating and claims reserving

Copyright © 2014 by MatBlas Limited. All rights reserved

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means,

electronic, mechanical, photocopying, recording, scanning or otherwise, without prior written permission by MatBlas

Limited.

Disclaimer: This presentation has been prepared for educational purpose only. It should only be used for reference

purposes for those attending or that have attended the presentation. The content of this note is theoretical in nature and

exclusively prepared for training purposes. No part of the content of this course material constitutes actuarial advice for

any company or organization. All worked examples shown in this note were derived from hypothetical assumptions only

and do not reflect any company’s rates, rating factors, benchmark factors, loss experience or reporting processes. Any

similarity between these examples and any insurance company is coincidental only.

Copyright © by Matβlas. All rights reserved 3

Agenda

What is insurance rating?

Technical pricing with UMS

Pricing considerations for some marine lines

Basics of claims reserving

WHY ME?

WHY THIS?

WHY NOW?

WHAT NOW?

Traditional underwriting

Look at the

policy, rate it and

agree to write it

or not.

Agreed price

only record.

Common workflow today

“Modelling” each risk

Technical pricing

Lloyd’s benchmark

Loss ratios by policy

Rate monitoring (PMD)

Business planning

Extremely competitive

market!

4

Challenges faced by underwriters

Copyright © by Matβlas. All rights reserved 5

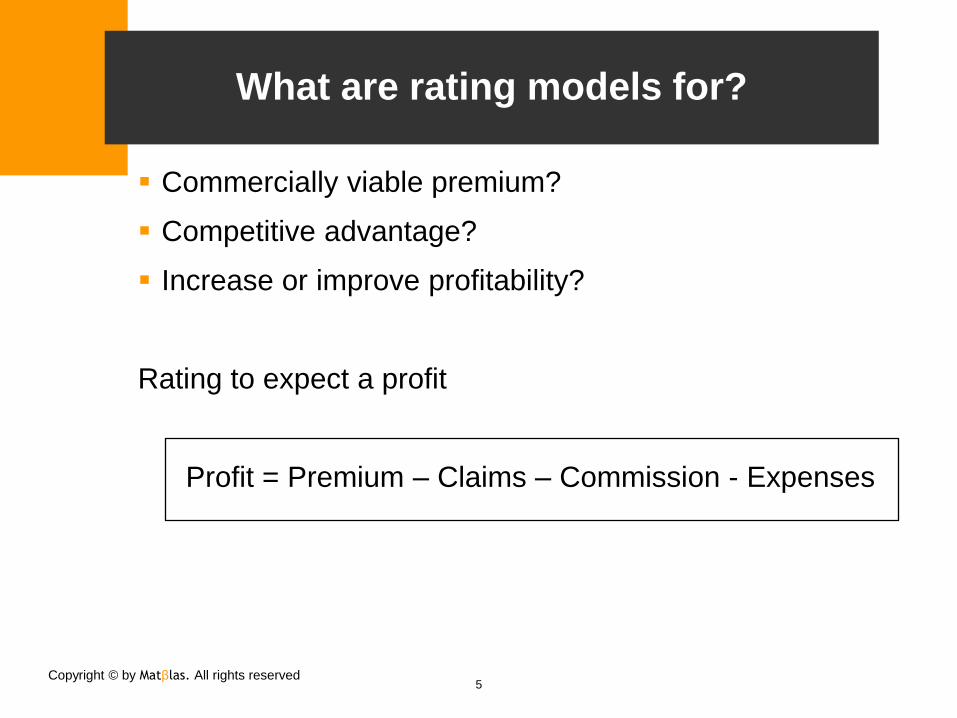

What are rating models for?

Commercially viable premium?

Competitive advantage?

Increase or improve profitability?

Rating to expect a profit

Profit = Premium – Claims – Commission - Expenses

Copyright © by Matβlas. All rights reserved 6

Rating is about forecasting claims costs

Product: promise to indemnify the policyholder if

An insured event happens

Policyholder incurs damages as a result

Production cost = cost of actual claims paid

Final cost per policy not known in advance

Years before known

Expected claim costs can be estimated

Copyright © by Matβlas. All rights reserved 7

What is the expected claim cost?

The expected claim cost of a policy is the

average claim cost across all possible future

claims and across policyholders

Expected claim cost = frequency x severity

Copyright © by Matβlas. All rights reserved 8

The expected claim cost: hypothetical example

Each vessel 1% chance of a loss

Each vessel worth £10M (Insured Value)

Assume each loss is total

Frequency = 1%

Severity = £10M

Expected claim cost = 1% x £10M = £100k

9

From claim cost to premium

1. Start by calculating the expected loss cost or risk

premium (frequency and severity)

This is the amount needed to cover average

claims costs

2. Other costs (usually a % of premium):

Contingency factor or risk load

Operating costs

Distribution costs

Underwriting profit or ROE

3. Derive the premium rate per unit of exposure

Copyright © by Matβlas. All rights reserved 10

Key relationship between premium and claim cost

Expected loss ratio (ELR) = loss ratio before

claims reported

Ultimate loss ratio (ULR) = loss ratio when

claims are settled and paid

Premium

Cost Claim ExpectedELR

Premium

Paid Claims ActualULR

Copyright © by Matβlas. All rights reserved 11

Technical pricing

Technical or Benchmark premium

Premium that is expected to generate a certain pre-selected

expected loss ratio (and thus profits)

Premium Technical

Cost Claim ExpectedELR

ELR

Cost Claim ExpectedPremium Technical

Copyright © by Matβlas. All rights reserved 12

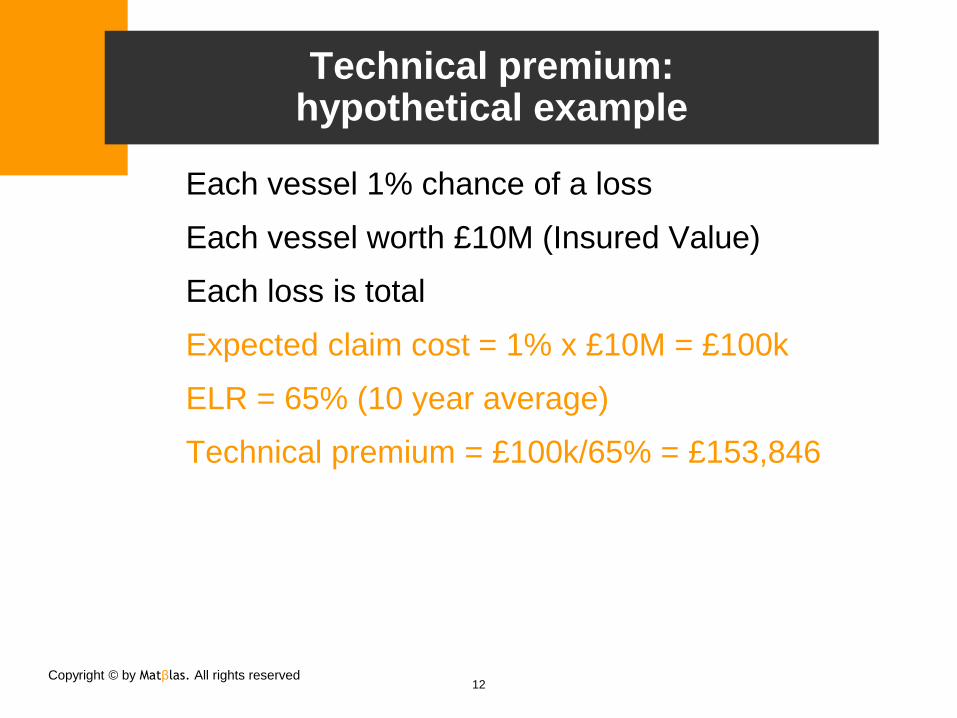

Technical premium: hypothetical example

Each vessel 1% chance of a loss

Each vessel worth £10M (Insured Value)

Each loss is total

Expected claim cost = 1% x £10M = £100k

ELR = 65% (10 year average)

Technical premium = £100k/65% = £153,846

Copyright © by Matβlas. All rights reserved 13

Common approach to comply with underwriting minimum standards (UMS)

Technical premium

Premium that is expected to support a selected long term ELR

Benchmark premium for Lloyd’s

Premium that is expected to support the business plan (short

term) ELR

“Walk-away” or break even premium

Premium that covers expected claim costs and expenses

without profits (100% combined ratio)

Charged premium

Premium actually charged for the policy and that appears on

the slip

Copyright © by Matβlas. All rights reserved 14

Premiums and loss ratios: hypothetical example

Expected claim cost = £100k; expenses = 10% of premium

Long term ELR = 65%

2014 BP ELR = 80%

“Break even” ELR = 90%

Agreed premium = £140k

TP = £100k/65% = £153.8k

Lloyd’s BP = £100k/80% = £125k

“Walk-away” prem. = £100/90%

= £111k

IELR = 100k/140k = 71.4%

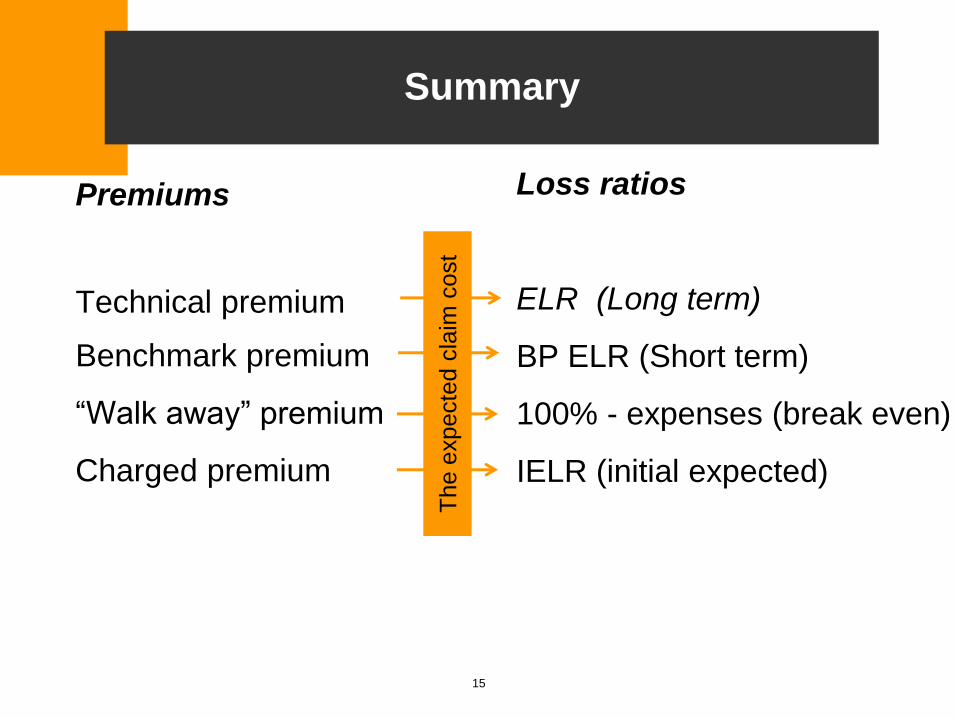

Summary

Premiums

Technical premium

Benchmark premium

“Walk away” premium

Charged premium

Loss ratios

ELR (Long term)

BP ELR (Short term)

100% - expenses (break even)

IELR (initial expected)

15

The e

xpecte

d c

laim

cost

Copyright © by Matβlas. All rights reserved

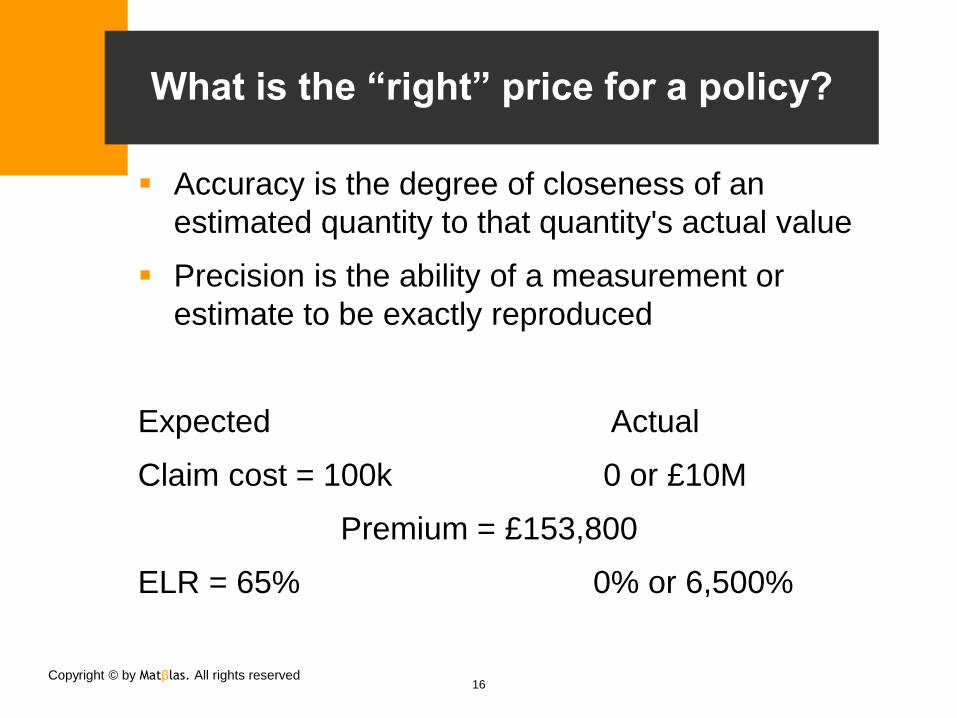

What is the “right” price for a policy?

Accuracy is the degree of closeness of an

estimated quantity to that quantity's actual value

Precision is the ability of a measurement or

estimate to be exactly reproduced

Expected Actual

Claim cost = 100k 0 or £10M

Premium = £153,800

ELR = 65% 0% or 6,500%

16

Copyright © by Matβlas. All rights reserved

What is the “right” price for each year?

100 policies same risk profile, same premium

collected

Expect 1 claim per year

17

Year

Tech. Premium

(£M) No. losses Losses (£M) ULR

1 15.38 1 10 65.00%

2 15.38 0 0 0.00%

3 15.38 0 0 0.00%

4 15.38 2 20 130.00%

5 15.38 0 0 0.00%

6 15.38 0 0 0.00%

7 15.38 4 40 260.00%

8 15.38 0 0 0.00%

9 15.38 1 10 65.00%

10 15.38 2 20 130.00%

65.00%10 year average loss ratio

The law of

large numbers

is about long

term averages

18

The expected claim cost in practice

Experience rate or burning cost

Base on insured own claims experience

Rating tables with risk drivers and premium

factors

Premium factors

Origin of tables?

Licensed software

CAT models

19

Rating tables and risk classification

Insurance rating is estimating expected

future average claims cost and allocating it

to each policy in proportion to its exposure

The average claim cost is adjusted up or

down to reflect the specific risk profile and

potential for claims

Copyright © by Matβlas. All rights reserved

In an ideal but no utopian world

Rating tables should be derived from claim

experience

Very few are!

Rating factors must reflect differences in

expected claim costs - risk

It can be and has been done

Market data can be bought for some lines, e.g.

Marine Hull

20

Copyright © by Matβlas. All rights reserved

Legal matters

Disclaimer: while we (MatBlas) have licensed a database

of vessels trading for the last 15+ years together with all

casualties and losses recorded, the results presented in

the next few slides are for illustration only and are not

meant to provide benchmarks to be used for pricing or

underwriting purposes.

The year of loss has been changed, frequency by type of

vessel, age and flag has been randomly re-distributed and

the insured loss has been completely changed for this

example. The results, as presented, are not real and are

inaccurate.

While the methodology presented here is overly

simplified, it does show typical actuarial methodology

used in statistical analysis to derive loss cost rates.

21

Copyright © by Matβlas. All rights reserved

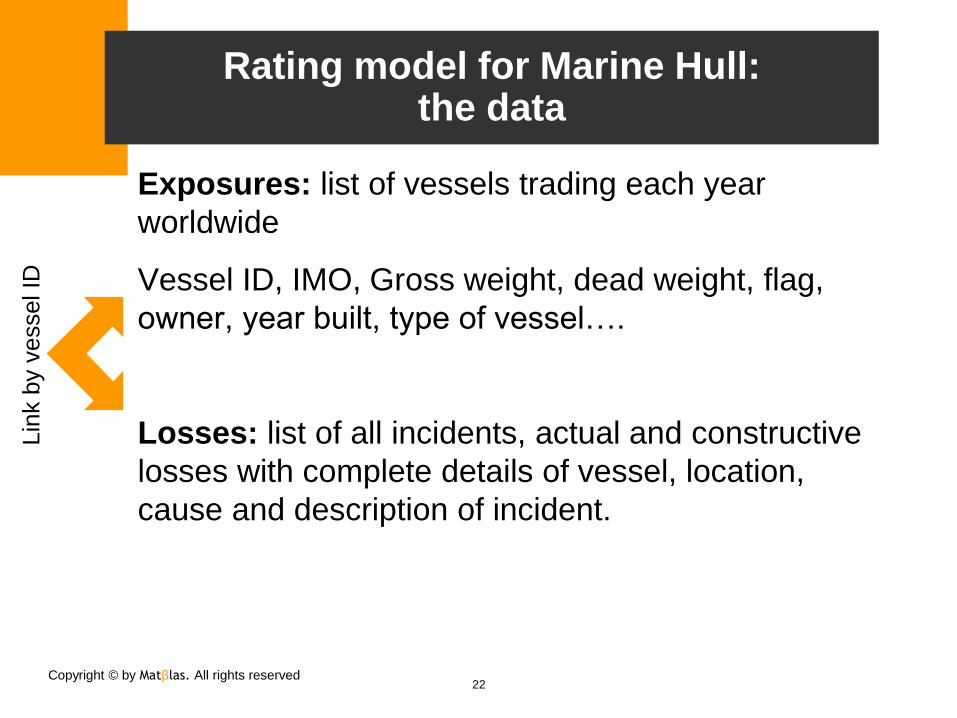

Rating model for Marine Hull: the data

Exposures: list of vessels trading each year

worldwide

Vessel ID, IMO, Gross weight, dead weight, flag,

owner, year built, type of vessel….

Losses: list of all incidents, actual and constructive

losses with complete details of vessel, location,

cause and description of incident.

22

Lin

k b

y v

essel ID

Copyright © by Matβlas. All rights reserved

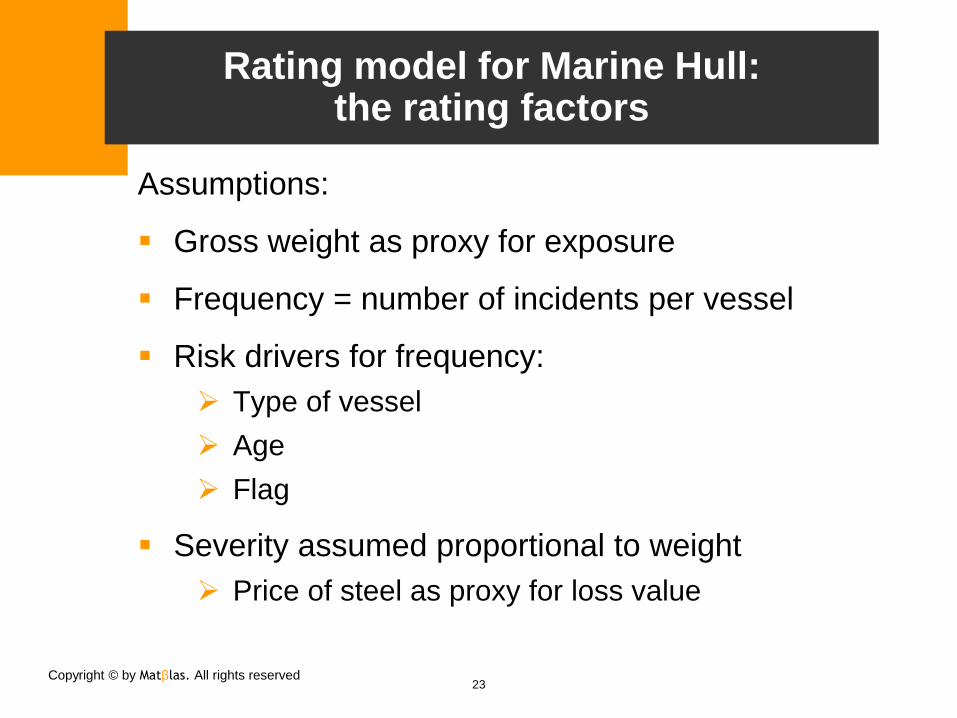

Rating model for Marine Hull: the rating factors

Assumptions:

Gross weight as proxy for exposure

Frequency = number of incidents per vessel

Risk drivers for frequency:

Type of vessel

Age

Flag

Severity assumed proportional to weight

Price of steel as proxy for loss value

23

Copyright © by Matβlas. All rights reserved

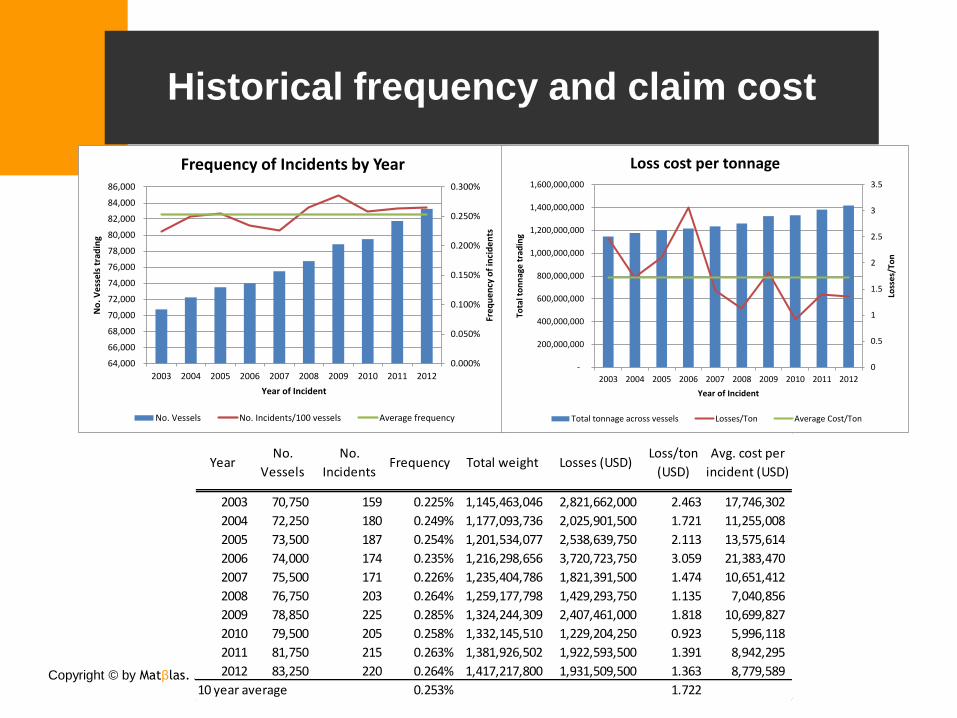

Historical frequency and claim cost

24

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

64,000

66,000

68,000

70,000

72,000

74,000

76,000

78,000

80,000

82,000

84,000

86,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Fre

qu

en

cy o

f in

cid

en

ts

No

. Ve

sse

ls t

rad

ing

Year of Incident

Frequency of Incidents by Year

No. Vessels No. Incidents/100 vessels Average frequency

0

0.5

1

1.5

2

2.5

3

3.5

-

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Loss

es/

Ton

Tota

l to

nn

age

tra

din

g

Year of Incident

Loss cost per tonnage

Total tonnage across vessels Losses/Ton Average Cost/Ton

YearNo.

Vessels

No.

IncidentsFrequency Total weight Losses (USD)

Loss/ton

(USD)

Avg. cost per

incident (USD)

2003 70,750 159 0.225% 1,145,463,046 2,821,662,000 2.463 17,746,302

2004 72,250 180 0.249% 1,177,093,736 2,025,901,500 1.721 11,255,008

2005 73,500 187 0.254% 1,201,534,077 2,538,639,750 2.113 13,575,614

2006 74,000 174 0.235% 1,216,298,656 3,720,723,750 3.059 21,383,470

2007 75,500 171 0.226% 1,235,404,786 1,821,391,500 1.474 10,651,412

2008 76,750 203 0.264% 1,259,177,798 1,429,293,750 1.135 7,040,856

2009 78,850 225 0.285% 1,324,244,309 2,407,461,000 1.818 10,699,827

2010 79,500 205 0.258% 1,332,145,510 1,229,204,250 0.923 5,996,118

2011 81,750 215 0.263% 1,381,926,502 1,922,593,500 1.391 8,942,295

2012 83,250 220 0.264% 1,417,217,800 1,931,509,500 1.363 8,779,589

10 year average 0.253% 1.722

Copyright © by Matβlas. All rights reserved

Historical frequency by age of vessel

25

Age range No. Vessels No. Incidents Frequency

0-1 40,933 16 0.039%

2-3 39,803 21 0.053%

4-5 39,529 26 0.066%

6-7 41,000 37 0.090%

8-9 44,621 46 0.103%

10-14 127,744 178 0.139%

15-19 139,293 397 0.285%

20-24 115,594 460 0.398%

22-29 73,955 328 0.444%

30+ 103,628 430 0.415%

Total 766,100 1,939 0.253%0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

0.350%

0.400%

0.450%

0.500%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

0-1 2-3 4-5 6-7 8-9 10-14 15-19 20-24 22-29 30+

Fre

qu

en

cy o

f in

cid

en

ts

No

. Ve

sse

ls t

rad

ing

Age of vessel

Frequency of Incidents by Age

No. Vessels Frequency by age Average frequency

Copyright © by Matβlas. All rights reserved

Historical frequency by type of vessel

26

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

0.350%

0.400%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Fre

qu

en

cy o

f in

cid

en

ts

No

. Ve

sse

ls t

rad

ing

Type of vessel

Frequency of Incidents by Type

No. Vessels Frequency by type Average frequency

Type No. Vessels No. Incidents Frequency

Bulk 59,394 162 0.273%

Dredger 9,571 9 0.094%

Fishing 115,672 397 0.343%

Gas 11,344 20 0.176%

General Cargo 288,967 975 0.337%

Passenger 40,215 73 0.182%

Research 9,604 7 0.073%

Tanker 84,226 138 0.164%

Tug 103,676 92 0.089%

Vehicle 43,431 66 0.152%

Total 766,100 1,939 0.253%

Copyright © by Matβlas. All rights reserved

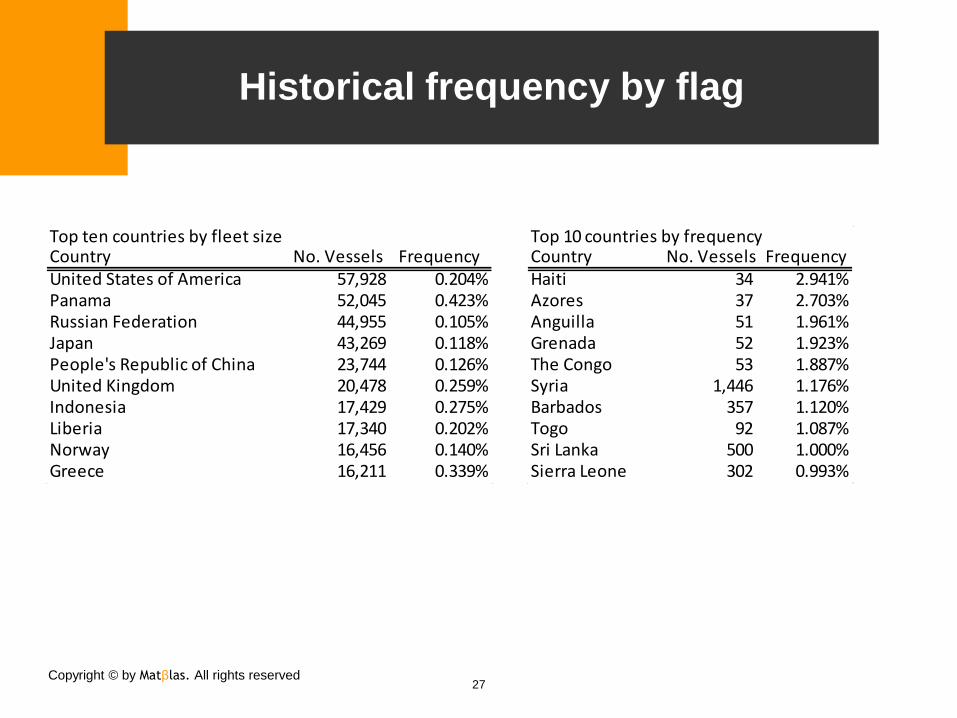

Historical frequency by flag

27

Top ten countries by fleet sizeCountry No. Vessels FrequencyUnited States of America 57,928 0.204%Panama 52,045 0.423%Russian Federation 44,955 0.105%Japan 43,269 0.118%People's Republic of China 23,744 0.126%United Kingdom 20,478 0.259%Indonesia 17,429 0.275%Liberia 17,340 0.202%Norway 16,456 0.140%Greece 16,211 0.339%

Top 10 countries by frequencyCountry No. Vessels FrequencyHaiti 34 2.941%Azores 37 2.703%Anguilla 51 1.961%Grenada 52 1.923%The Congo 53 1.887%Syria 1,446 1.176%Barbados 357 1.120%Togo 92 1.087%Sri Lanka 500 1.000%Sierra Leone 302 0.993%

Copyright © by Matβlas. All rights reserved

A simple marine hull model

Average cost/ton = $1.72, Long term ELR = 70%

Rate/ton = $2.45 (technical rate)

Rate for newly built passenger cruise in Greece

$0.364/ton 28

Type Load/Discount

Bulk 7.77%

Dredger -62.85%

Fishing 35.60%

Gas -30.34%

General Cargo 33.31%

Passenger -28.28%

Research -71.20%

Tanker -35.26%

Tug -64.94%

Vehicle -39.96%

Country Load/discountUnited States of America -19.52%Panama 67.01%Russian Federation -58.69%Japan -53.43%People's Republic of China -50.08%United Kingdom 2.26%Indonesia 8.81%Liberia -20.25%Norway -44.78%Greece 34.05%. .. .

. .

Age range Load/discount

0-1 -84.56%

2-3 -79.15%

4-5 -74.01%

6-7 -64.34%

8-9 -59.27%

10-14 -44.95%

15-19 12.61%

20-24 57.23%

22-29 75.23%

30+ 63.95%

Copyright © by Matβlas. All rights reserved

Why is not everyone doing this? Commonly heard excuses

I am happy with my model rates

Back tested?

Downloading from websites to cut and paste

too much work

Websites can transfer data to Excel

Data in pdf

Tools can convert to Excel

Large fleets too much work

Pre-rate and search by insured name (owner)

29

Copyright © by Matβlas. All rights reserved

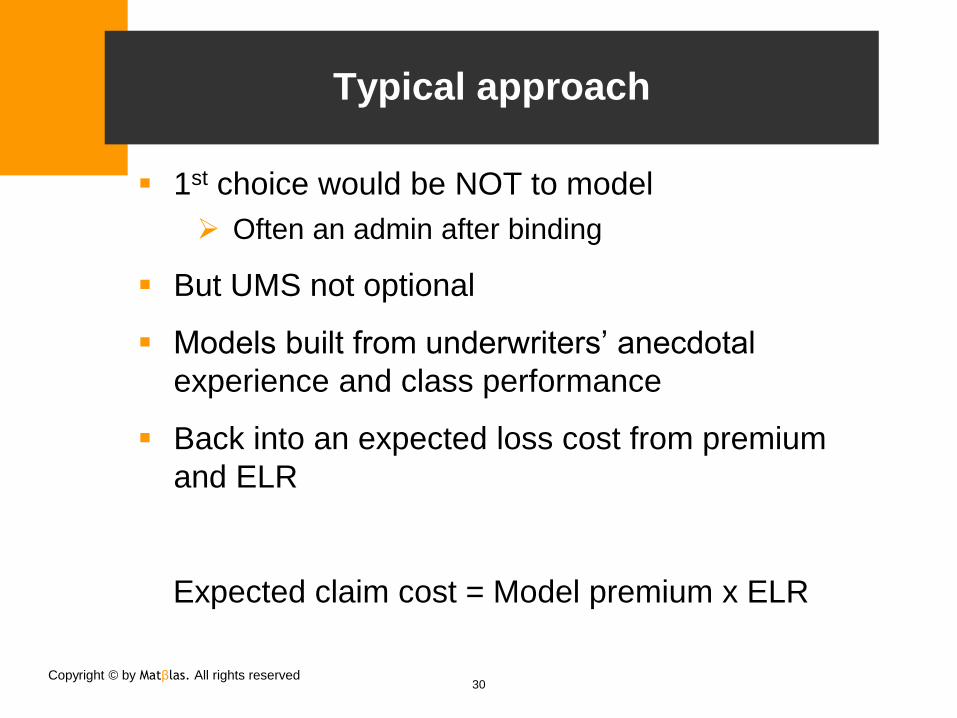

Typical approach

1st choice would be NOT to model

Often an admin after binding

But UMS not optional

Models built from underwriters’ anecdotal

experience and class performance

Back into an expected loss cost from premium

and ELR

Expected claim cost = Model premium x ELR

30

Copyright © by Matβlas. All rights reserved

Is not that simple!

True!

Models are tools not decision makers

Some classes difficult or impossible to rate

War and terrorism

Consistent models can streamline inefficient

workflows

31

Basics of claims reserving

Copyright © by Matβlas. All rights reserved 33

Pricing and reserving

Start YOA with business plan ELR for class

For each unit of premium set aside ELR% as

reserve

Each individual policy priced with IELR

Aggregate IELR across policies

Allows to validate business plan

Copyright © by Matβlas. All rights reserved 34

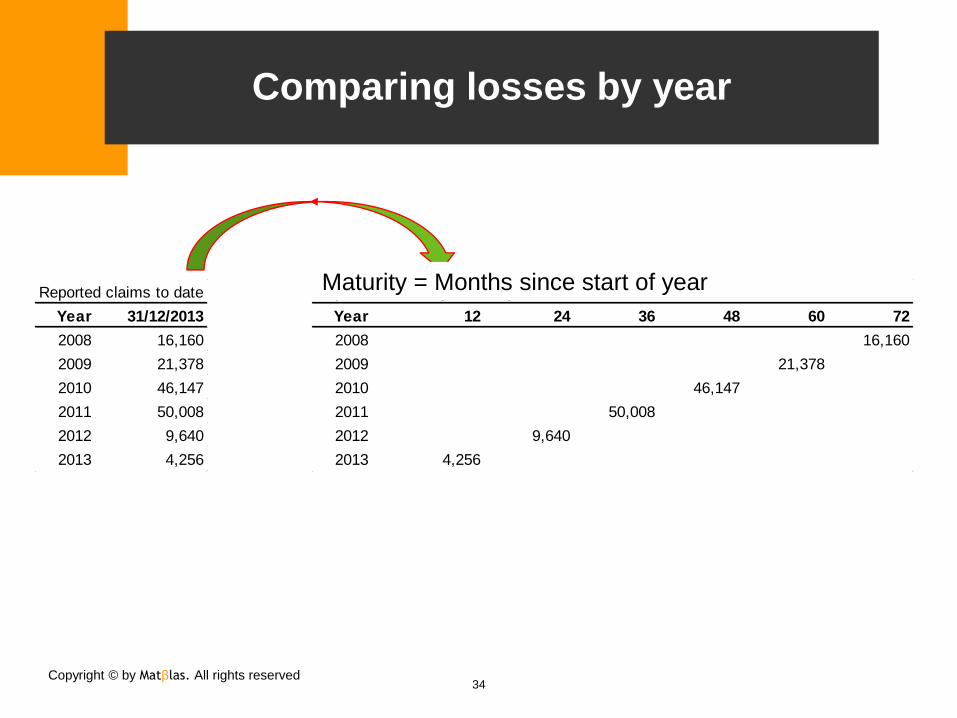

Comparing losses by year

Reported claims to date

Year 31/12/2013

2008 16,160

2009 21,378

2010 46,147

2011 50,008

2012 9,640

2013 4,256

Reported claims by "maturity"

Year 12 24 36 48 60 72

2008 16,160

2009 21,378

2010 46,147

2011 50,008

2012 9,640

2013 4,256

Maturity = Months since start of year

Copyright © by Matβlas. All rights reserved 35

Basic definitions

Paid = amount paid to or on behalf of policy holder

Outstanding or case reserve = amount allocated to

specific claim and held as reserve (not yet paid)

Incurred = paid + case reserve

IBNR = Incurred but not reported (held as reserve)

IBNER = incurred but not enough reported (held

as reserve)

Copyright © by Matβlas. All rights reserved 36

Actuarial estimates of future claims movements

Reported claims to date

Year 31/12/2013

2008 16,160

2009 21,378

2010 46,147

2011 50,008

2012 9,640

2013 4,256

Reported claims by "maturity"

Year 12 24 36 48 60 72

2008 1,688 6,340 13,472 13,203 15,117 16,160

2009 1,165 7,527 15,038 21,926 21,378

2010 2,549 8,814 27,816 46,147

2011 3,565 16,747 50,008

2012 3,760 9,640

2013 4,256

Copyright © by Matβlas. All rights reserved 37

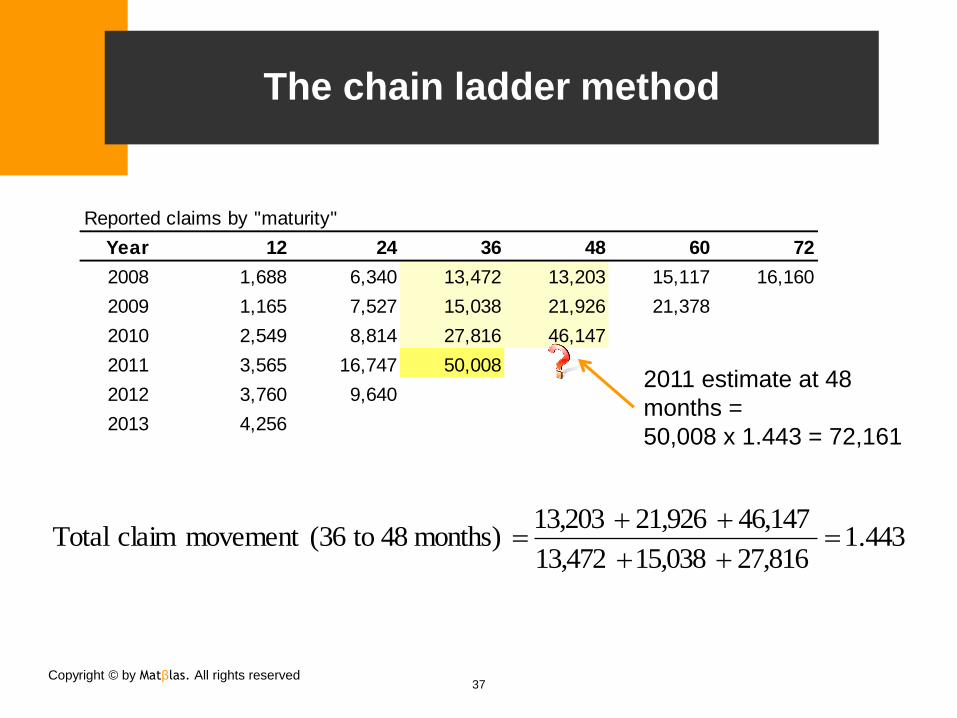

The chain ladder method

Reported claims by "maturity"

Year 12 24 36 48 60 72

2008 1,688 6,340 13,472 13,203 15,117 16,160

2009 1,165 7,527 15,038 21,926 21,378

2010 2,549 8,814 27,816 46,147

2011 3,565 16,747 50,008

2012 3,760 9,640

2013 4,256

443.127,81615,03813,472

46,14721,92613,203 months) 48 to(36movement claim Total

2011 estimate at 48

months =

50,008 x 1.443 = 72,161

Copyright © by Matβlas. All rights reserved 38

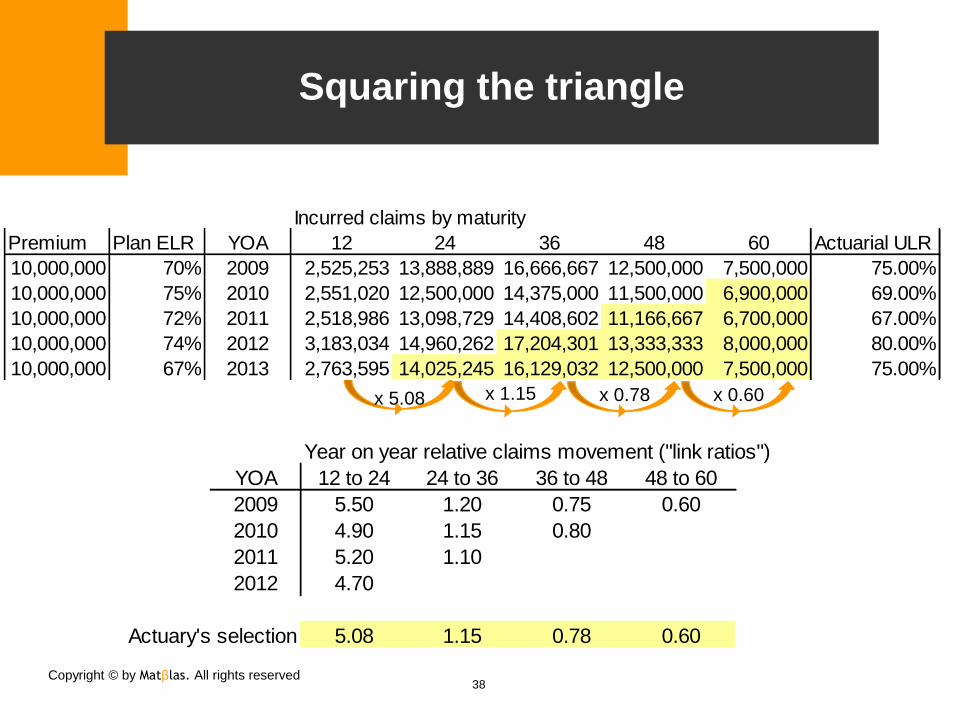

Squaring the triangle

Year on year relative claims movement ("link ratios")

YOA 12 to 24 24 to 36 36 to 48 48 to 60

2009 5.50 1.20 0.75 0.60

2010 4.90 1.15 0.80

2011 5.20 1.10

2012 4.70

Actuary's selection 5.08 1.15 0.78 0.60

Incurred claims by maturity

Premium Plan ELR YOA 12 24 36 48 60 Actuarial ULR

10,000,000 70% 2009 2,525,253 13,888,889 16,666,667 12,500,000 7,500,000 75.00%

10,000,000 75% 2010 2,551,020 12,500,000 14,375,000 11,500,000 6,900,000 69.00%

10,000,000 72% 2011 2,518,986 13,098,729 14,408,602 11,166,667 6,700,000 67.00%

10,000,000 74% 2012 3,183,034 14,960,262 17,204,301 13,333,333 8,000,000 80.00%

10,000,000 67% 2013 2,763,595 14,025,245 16,129,032 12,500,000 7,500,000 75.00%

Incurred claims by maturity

Premium Plan ELR YOA 12 24 36 48 60 Actuarial ULR

10,000,000 70% 2009 2,525,253 13,888,889 16,666,667 12,500,000 7,500,000 75.00%

10,000,000 75% 2010 2,551,020 12,500,000 14,375,000 11,500,000 6,900,000 69.00%

10,000,000 72% 2011 2,518,986 13,098,729 14,408,602 11,166,667 6,700,000 67.00%

10,000,000 74% 2012 3,183,034 14,960,262 17,204,301 13,333,333 8,000,000 80.00%

10,000,000 67% 2013 2,763,595 14,025,245 16,129,032 12,500,000 7,500,000 75.00%

Incurred claims by maturity

Premium Plan ELR YOA 12 24 36 48 60 Actuarial ULR

10,000,000 70% 2009 2,525,253 13,888,889 16,666,667 12,500,000 7,500,000 75.00%

10,000,000 75% 2010 2,551,020 12,500,000 14,375,000 11,500,000 6,900,000 69.00%

10,000,000 72% 2011 2,518,986 13,098,729 14,408,602 11,166,667 6,700,000 67.00%

10,000,000 74% 2012 3,183,034 14,960,262 17,204,301 13,333,333 8,000,000 80.00%

10,000,000 67% 2013 2,763,595 14,025,245 16,129,032 12,500,000 7,500,000 75.00%

Incurred claims by maturity

Premium Plan ELR YOA 12 24 36 48 60 Actuarial ULR

10,000,000 70% 2009 2,525,253 13,888,889 16,666,667 12,500,000 7,500,000 75.00%

10,000,000 75% 2010 2,551,020 12,500,000 14,375,000 11,500,000 6,900,000 69.00%

10,000,000 72% 2011 2,518,986 13,098,729 14,408,602 11,166,667 6,700,000 67.00%

10,000,000 74% 2012 3,183,034 14,960,262 17,204,301 13,333,333 8,000,000 80.00%

10,000,000 67% 2013 2,763,595 14,025,245 16,129,032 12,500,000 7,500,000 75.00%

Incurred claims by maturity

Premium Plan ELR YOA 12 24 36 48 60 Actuarial ULR

10,000,000 70% 2009 2,525,253 13,888,889 16,666,667 12,500,000 7,500,000 75.00%

10,000,000 75% 2010 2,551,020 12,500,000 14,375,000 11,500,000 6,900,000 69.00%

10,000,000 72% 2011 2,518,986 13,098,729 14,408,602 11,166,667 6,700,000 67.00%

10,000,000 74% 2012 3,183,034 14,960,262 17,204,301 13,333,333 8,000,000 80.00%

10,000,000 67% 2013 2,763,595 14,025,245 16,129,032 12,500,000 7,500,000 75.00%

x 5.08 x 1.15 x 0.78 x 0.60

Copyright © by Matβlas. All rights reserved 39

Practical issues with claims reserving

Historic claims emerging patterns

Consistent case reserve setting

Changes in patterns may cause distortion

Large or CAT losses separate treatment

Some classes ULR is “pegged”

Long tail lines: what happens after 60 months?

ULRs starting point of plan loss ratio

Reserving Pricing

Copyright © by Matβlas. All rights reserved 40

Wrap Up

Underwriting minimum standards does not mean

minimum effort

Consistent rating helps achieve efficiency

Rating models are tools and should not replace

Underwriting

Portfolio management

Risk selection

Diversification

Common sense!