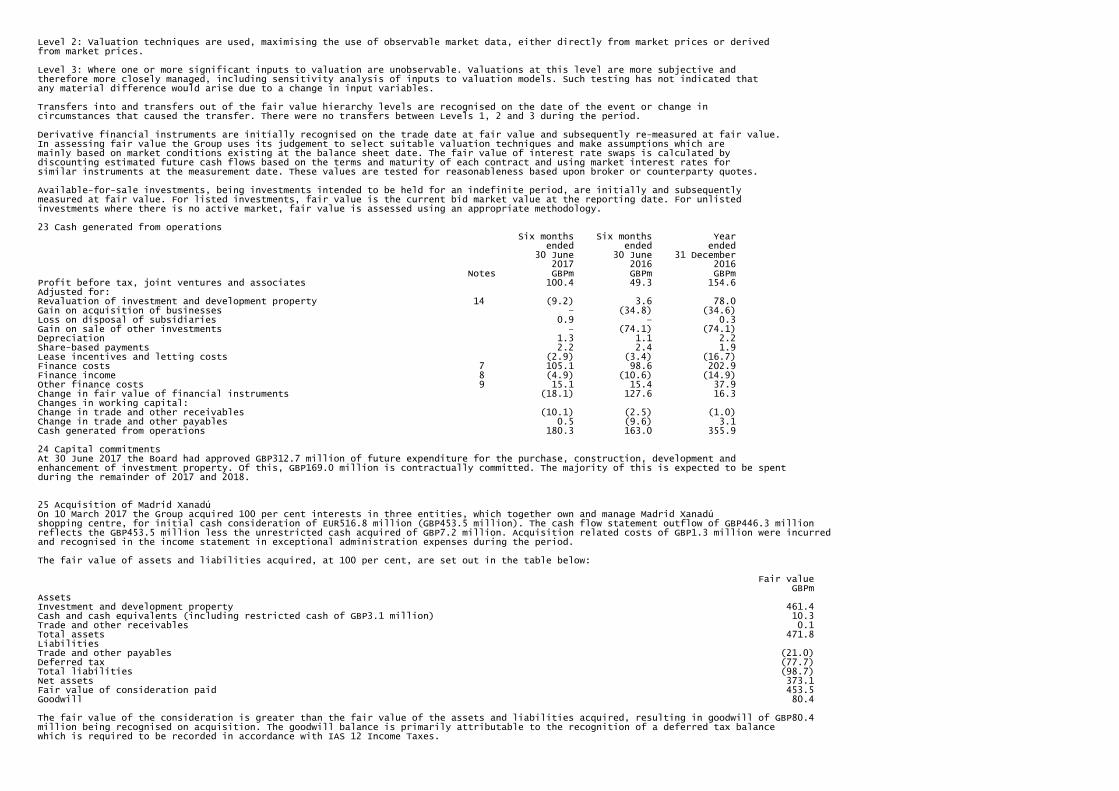

intu properties plc (registration number · pdf fileduring the period, we acquired madrid...

TRANSCRIPT

INTU PROPERTIES PLC (Registration number UK3685527)ISIN Code: GB0006834344 JSE Code: ITU

Press Release

INTERIM REPORT FOR THE SIX MONTHS ENDED 30 JUNE 2017

David Fischel, intu Chief Executive, commented:

"intu has performed robustly over the six month period in a UK retail environment which continues to be challenging.Retail brands are being selective in their expansion, looking at established locations such as our 17 prime shoppingcentres which are attracting high footfall through their differentiated offering and compelling customer experience.

The resilience of the tenant market in our centres is shown by our 103 lettings in the period at 7 per cent aboveprevious passing rents, including brands such as Next, River Island, Hugo Boss, Gant, Paul Smith, Victoria's Secretand Tesla. Also our tenants continue to invest in upsizing and upgrading their units which has resulted in maintainedhigh occupancy.

Our GBP679 million UK development programme is progressing on schedule with the GBP180 million intu Watford extensionon target to open in Autumn 2018. We expect to start shortly on the GBP71 million intu Lakeside leisure extension whichis over 90 per cent let to tenants including Nickelodeon, Hollywood Bowl and multiple restaurants.

Our Spanish business continues to perform well and intu now owns three of the country's top ten shopping centres.During the period, we acquired Madrid Xanadú for EUR530 million, a centre which has strong leisure attractions includingan indoor ski slope, with an aquarium and Nickelodeon theme park attraction under construction.

We have a clear strategy to deliver long-term value to shareholders and, with cash and available facilities amountingto GBP920 million, we have significant flexibility to pursue opportunities as they arise in the UK and Spain."

Investor presentation

A presentation to analysts and investors will take place at UBS, 5 Broadgate, London EC2 at 09.30BST on 27 July2017. The presentation will also be available to international analysts and investors through a live audio call andwebcast. The presentation and a copy of this announcement will be available on the Group's website intugroup.co.uk.

Enquiries

intu properties plcDavid Fischel Chief Executive +44 (0)20 7960 1207Matthew Roberts Chief Financial Officer +44 (0)20 7960 1353Adrian Croft Head of Investor Relations +44 (0)20 7960 1212Public relationsUK: Justin Griffiths, Powerscourt +44 (0)20 7250 1446SA: Frédéric Cornet, Instinctif Partners +27 (0)11 447 3030

About intu

intu is the UK's leading owner, manager and developer of prime regional shopping centres with a growing presence in Spain. We are passionate about creating uniquely compelling experiences, in centre and online, that attract customers, delivering enhancedfootfall, dwell time and loyalty. This helps our retailers flourish, driving occupancy and income growth.

We own many of the UK's largest and most popular retail destinations, with super-regional centres such as intu Trafford Centre andintu Lakeside and vibrant city centre locations from Newcastle to Watford.

We are focused on four strategic objectives: optimising the performance of our assets to deliver attractive long-term total propertyreturns, progressing our UK development pipeline to add value to our portfolio, leveraging the strength of our brand and seizing theopportunity in Spain to create a business of scale.

We are committed to our local communities, our centres support over 120,000 jobs representing about 4 per cent of the total UKretail workforce, and to operating with environmental responsibility.

Our success creates value for our retailers, investors and the communities we serve.

Presentation of information

We account for our interests in joint ventures using the equity method as required by IFRS 11 Joint Arrangements. This means thatthe income statement and the balance sheet include single lines for the Group's total share of post-tax profit and the netinvestment in joint ventures respectively.

Management review and monitor performance as well as determine the strategy of the business primarily on a proportionatelyconsolidated basis. This includes the Group's share of joint ventures on an individual line-by-line basis rather than a post-tax profitor net investment basis. The figures and commentary presented are consistent with our management approach as we believe thisprovides a more meaningful analysis of the Group's performance. The other information section provides reconciliations of theincome statement and balance sheet between the two bases.

See financial review for more details on the presentation of information and alternative performance measures used.

This press release contains "forward-looking statements" regarding the belief or current expectations of intu properties plc, its Directors and other members of its senior management about intu properties plc's businesses, financial performance and results of operations.

These forward-looking statements are not guarantees of future performance. Rather, they are based on current views and assumptions and involve known and unknown risks, uncertainties and other factors, many of which are outside the control of intu properties plc and are difficult to predict, that may cause actual results, performance or developments to differ materially from any future results, performance or developments expressed or implied by the forward-looking statements. These forward-looking statements speak only as at the date of this press release. Except as required by applicable law, intu properties plc makes no representation or warranty in relation to them and expressly disclaims any obligation to update or revise any forward-looking statements contained herein to reflect any change in intu properties plc's expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

Any information contained in this press release on the price at which shares or other securities in intu properties plc have been bought or sold in the past, or on the yield on such shares or other securities, should not be relied upon as a guide to future performance.

HIGHLIGHTS OF THE FIRST SIX MONTHS OF 2017Operating highlights

Optimising asset performanceWe aim to deliver attractive long-term total property returns from strong, stable income streams- after increases of 1.8 per cent in 2015 and 3.6 per cent in 2016, like-for-like net rental income decreased by 1.5 per cent in the period, against a strong comparative of 7.5 per cent increase for the first half of 2016; guidance of second half recovery to deliver unchanged outcome for 2017- signed 103 long-term leases (80 in the UK and 23 in Spain) delivering GBP18 million of annual rent at an average of 7 per cent above previous passing rent and in line with valuers' assumptions- occupancy stable at 95.9 per cent (December 2016: 96.0 per cent)- footfall decreased by 0.5 per cent (2016: +1.3 per cent) outperforming the national ShopperTrak retail average which fell by 2.7 per cent in the period- like-for-like property values improved slightly in the period, increasing by 0.2 per cent, broadly in line with the IPD monthly retail index of 0.6 per cent (2016: intu +0.0 per cent; IPD down 4.7 per cent)

Delivering UK developmentsBy extending and enhancing our existing locations we aim to deliver superior returns- capital expenditure of GBP99 million in the period including GBP40 million on the GBP180 million extension of intu Watford which is on target to open in Autumn 2018- intend to commence two further developments in 2017 – the GBP71 million Nickelodeon-anchored leisure scheme at intu Lakeside and the GBP74 million extension and enclosure of Barton Square at intu Trafford Centre- signed The Light cinema to anchor the intu Broadmarsh redevelopment and expect to commit to this GBP89 million project later in 2017- near-term committed and pipeline of projects through to the end of 2020 of GBP679 million

Making the brand countWe leverage the strength of our brand to create compelling experiences for our customers- net promoter score, our measure of customer service, running consistently high at around 70- intu Experiences, our dedicated promotions business, generated income of GBP8 million in the period, which is in line with the first half of 2016 (GBP21 million annually, equivalent to the rental income of our eighth largest centre)- intu.co.uk, our online shopping platform providing strong editorial content, has seen an 80 per cent year-on-year increase in visits to our shop pages offering products from 470 retailers- on target to deliver our 2020 environmental objectives ahead of time, including intensity reduction in carbon emissions of 47 per cent since 2010 against our 2020 target of 50 per cent

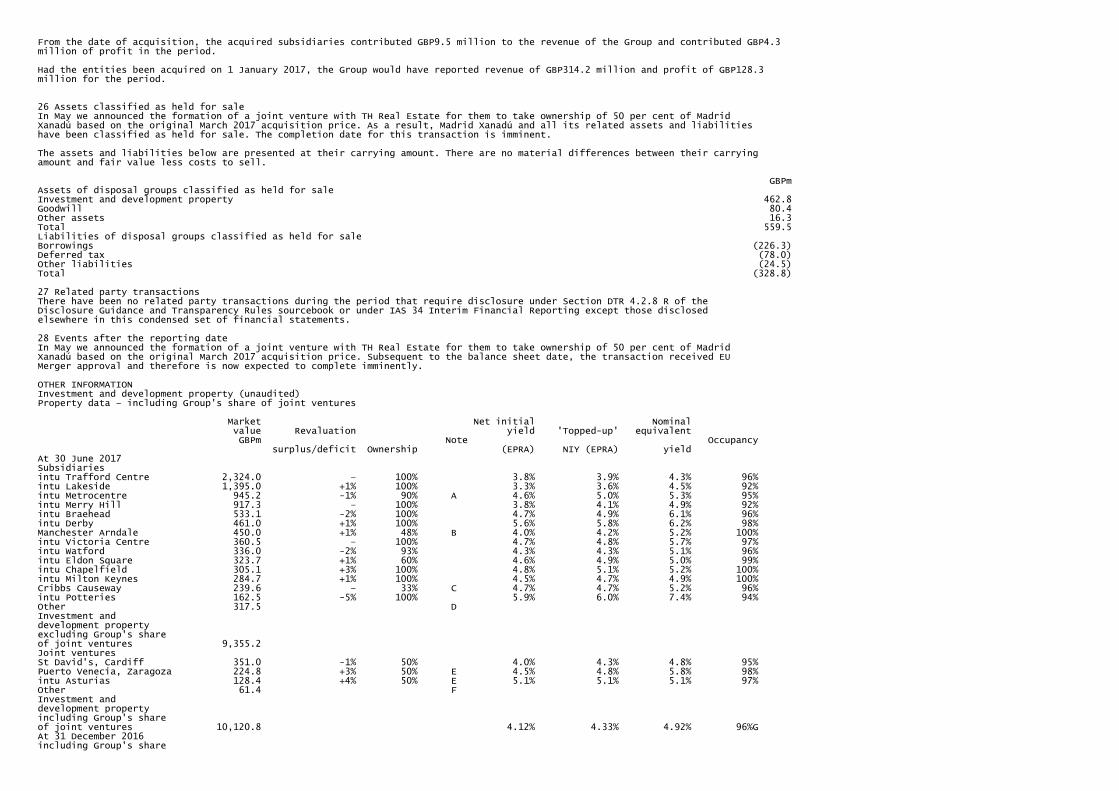

Seizing the growth opportunity in SpainOur strategy is to create a business of scale through acquisitions and development projects- acquired Madrid Xanadú, one of Spain's top 10 shopping centres in March 2017, for an agreed price of EUR530 million, and announced formation of a joint venture with TH Real Estate for them to take ownership of 50 per cent- completed a EUR8 million project at intu Asturias developing a previously under-utilised space. The redevelopment opened successfully in July 2017- signed 23 leases, including nine for the recently completed development at intu Asturias. New lettings of existing units were 14 per cent above the previous passing rent- occupancy remained strong in our three centres at 98 per cent, with footfall and retailer sales both up by 1 per cent- increases in the market value of existing centres with intu Asturias up 4 per cent and Puerto Venecia, Zaragoza up 3 per cent- strong interest from prospective tenants for the intu Costa del Sol development and progressing discussions with lenders for development finance for the project

Financial strength

Robust capital structure provides capacity to deliver our objectives from a range of funding sources. Since the half year, we haverefinanced a GBP488 million loan on intu Merry Hill, raised additional finance of GBP250 million on intu Trafford Centre and imminentlyexpect to complete the disposal of 50 per cent of Madrid Xanadú. On a pro forma basis, taking into account the above transactions:- cash and available facilities of GBP920 million (31 December 2016: GBP922 million)- weighted average debt maturity of 7.1 years, with minimal refinancing until 2021- substantial headroom on our debt covenants. By way of example, a 25 per cent fall in capital values and 10 per cent fall in income would only require an equity cure of GBP10 million

With 100 per cent ownership of assets valued at GBP6.7 billion and high quality income streams, we intend to continue the process of

recycling capital from existing assets to help finance our investment programme.

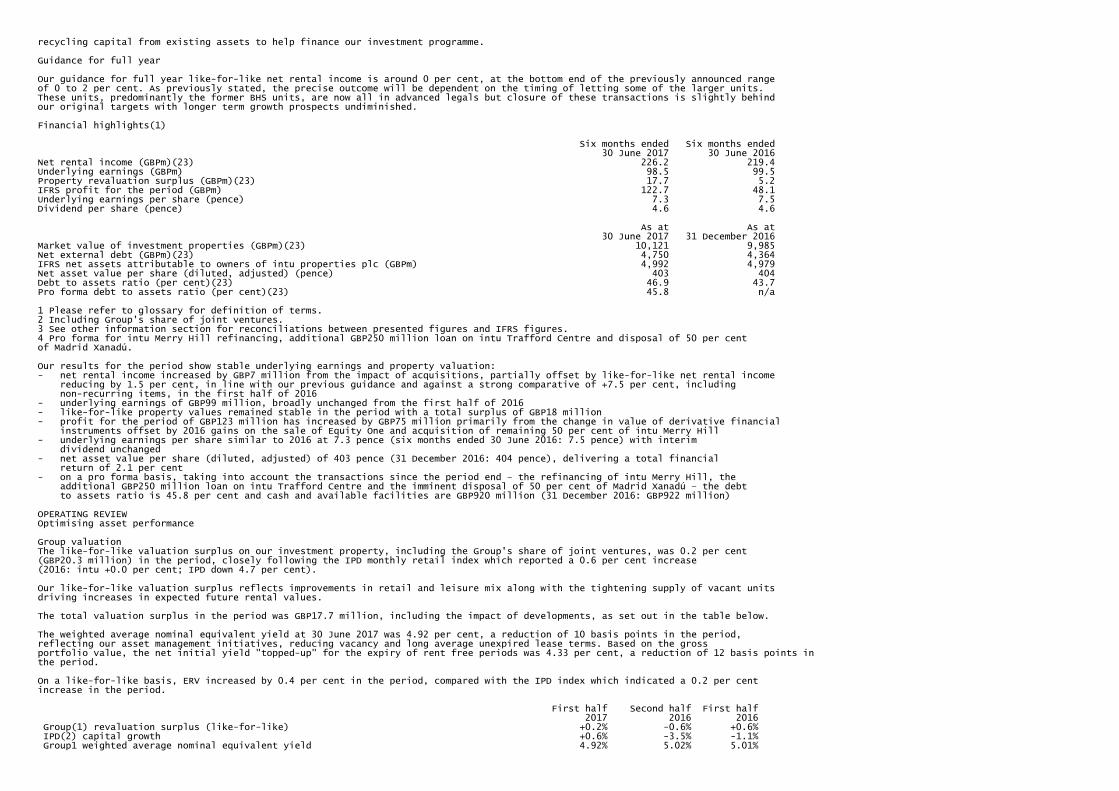

Guidance for full year

Our guidance for full year like-for-like net rental income is around 0 per cent, at the bottom end of the previously announced rangeof 0 to 2 per cent. As previously stated, the precise outcome will be dependent on the timing of letting some of the larger units.These units, predominantly the former BHS units, are now all in advanced legals but closure of these transactions is slightly behindour original targets with longer term growth prospects undiminished.

Financial highlights(1)

Six months ended Six months ended 30 June 2017 30 June 2016Net rental income (GBPm)(23) 226.2 219.4Underlying earnings (GBPm) 98.5 99.5Property revaluation surplus (GBPm)(23) 17.7 5.2IFRS profit for the period (GBPm) 122.7 48.1Underlying earnings per share (pence) 7.3 7.5Dividend per share (pence) 4.6 4.6 As at As at 30 June 2017 31 December 2016Market value of investment properties (GBPm)(23) 10,121 9,985Net external debt (GBPm)(23) 4,750 4,364IFRS net assets attributable to owners of intu properties plc (GBPm) 4,992 4,979Net asset value per share (diluted, adjusted) (pence) 403 404Debt to assets ratio (per cent)(23) 46.9 43.7Pro forma debt to assets ratio (per cent)(23) 45.8 n/a

1 Please refer to glossary for definition of terms.2 Including Group's share of joint ventures.3 See other information section for reconciliations between presented figures and IFRS figures.4 Pro forma for intu Merry Hill refinancing, additional GBP250 million loan on intu Trafford Centre and disposal of 50 per cent of Madrid Xanadú.

Our results for the period show stable underlying earnings and property valuation:- net rental income increased by GBP7 million from the impact of acquisitions, partially offset by like-for-like net rental income reducing by 1.5 per cent, in line with our previous guidance and against a strong comparative of +7.5 per cent, including non-recurring items, in the first half of 2016- underlying earnings of GBP99 million, broadly unchanged from the first half of 2016- like-for-like property values remained stable in the period with a total surplus of GBP18 million- profit for the period of GBP123 million has increased by GBP75 million primarily from the change in value of derivative financial instruments offset by 2016 gains on the sale of Equity One and acquisition of remaining 50 per cent of intu Merry Hill- underlying earnings per share similar to 2016 at 7.3 pence (six months ended 30 June 2016: 7.5 pence) with interim dividend unchanged- net asset value per share (diluted, adjusted) of 403 pence (31 December 2016: 404 pence), delivering a total financial return of 2.1 per cent- on a pro forma basis, taking into account the transactions since the period end – the refinancing of intu Merry Hill, the additional GBP250 million loan on intu Trafford Centre and the imminent disposal of 50 per cent of Madrid Xanadú – the debt to assets ratio is 45.8 per cent and cash and available facilities are GBP920 million (31 December 2016: GBP922 million)

OPERATING REVIEWOptimising asset performance

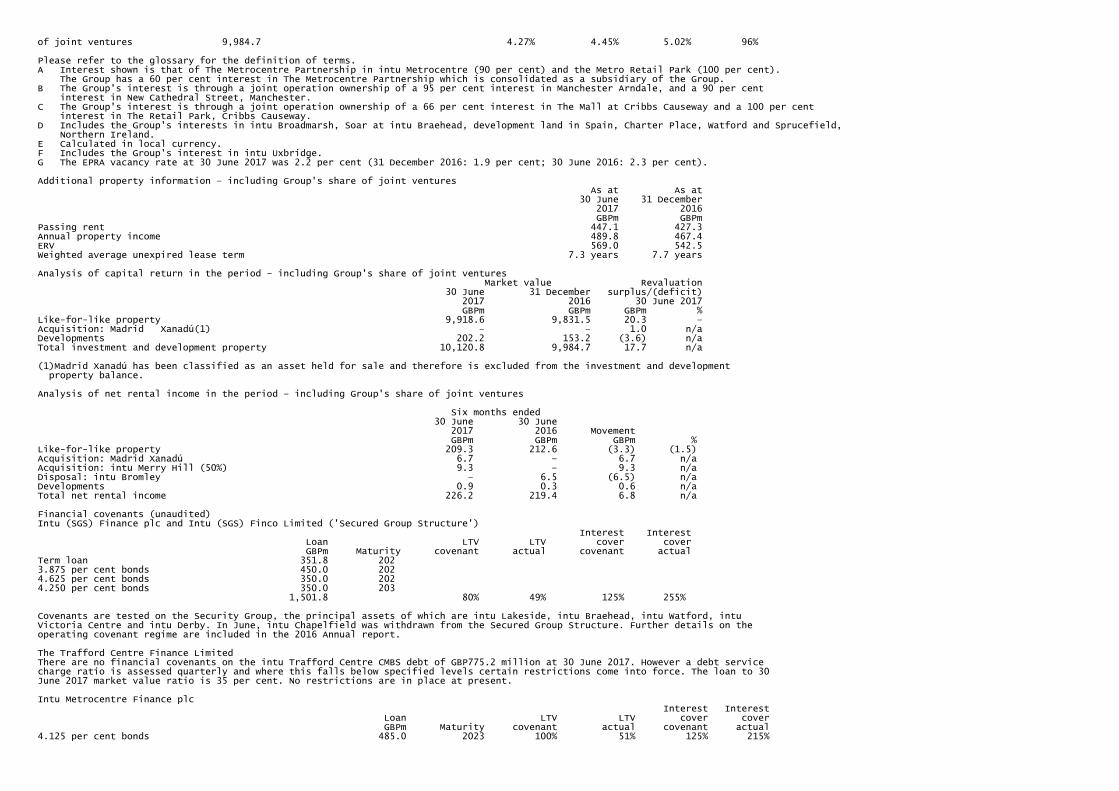

Group valuationThe like-for-like valuation surplus on our investment property, including the Group's share of joint ventures, was 0.2 per cent(GBP20.3 million) in the period, closely following the IPD monthly retail index which reported a 0.6 per cent increase(2016: intu +0.0 per cent; IPD down 4.7 per cent).

Our like-for-like valuation surplus reflects improvements in retail and leisure mix along with the tightening supply of vacant unitsdriving increases in expected future rental values.

The total valuation surplus in the period was GBP17.7 million, including the impact of developments, as set out in the table below.

The weighted average nominal equivalent yield at 30 June 2017 was 4.92 per cent, a reduction of 10 basis points in the period,reflecting our asset management initiatives, reducing vacancy and long average unexpired lease terms. Based on the grossportfolio value, the net initial yield "topped-up" for the expiry of rent free periods was 4.33 per cent, a reduction of 12 basis points inthe period.

On a like-for-like basis, ERV increased by 0.4 per cent in the period, compared with the IPD index which indicated a 0.2 per centincrease in the period.

First half Second half First half 2017 2016 2016 Group(1) revaluation surplus (like-for-like) +0.2% -0.6% +0.6% IPD(2) capital growth +0.6% -3.5% -1.1% Group1 weighted average nominal equivalent yield 4.92% 5.02% 5.01%

Change in Group nominal equivalent yield -10bp +1bp -13bp IPD(2) equivalent yield shift -7bp +25bp +4bp Group(1) "topped-up" net initial yield (EPRA) 4.33% 4.45% 4.49% Group(1) change in like-for-like ERV +0.4% +0.1% -0.1% IPD(2) change in rental value index +0.2% +0.3% +0.5%

1 Including Group's share of joint ventures.2 IPD monthly index, retail.

The table below shows the main components of the Group's GBP17.7 million overall valuation surplus:

Market value Like-for-like 30 June 31 December Surplus/ Surplus/ 2017 2016 (deficit) (deficit) GBPm GBPm GBPm %intu Lakeside 1,395.0 1,375.0 10.4 1Intu Chapelfield 305.1 296.3 9.5 3intu Trafford Centre 2,324.0 2,312.0 9.4 –intu Potteries 162.5 169.0 (8.0) (5)intu Braehead 533.1 546.2 (12.0) (2)Other UK like-for-like 4,845.7 4,802.0 0.5 –Total UK like-for-like 9,565.4 9,500.5 9.8 –Spain like-for-like 353.2 331.0 10.5 3Redevelopments 202.2 153.2 (3.6) n/aInvestment and development property including Group's share of joint ventures 10,120.8 9,984.7 16.7 n/aAcquisition: Madrid Xanadú (asset held for sale) 462.8 – 1.0 n/aTotal 10,583.6 9,984.7 17.7 n/a

- intu Lakeside: completion of new leases and renewals on expiry adds certainty to the income streams going forward as well as providing evidence for growth in future rental levels- intu Chapelfield: strong investment demand for prime centres with limited vacant units and strong tenant mix- intu Trafford Centre: new lettings continue to drive forward rental tone- intu Potteries: pressure on long-term rental values has impacted the centre's value- intu Braehead: continuation of the less buoyant occupier and investment market in Scotland has resulted in a reduction in value of this centre- Spain: limited vacant space and strong operating metrics increase the rental value potential of intu Asturias and Puerto Venecia, Zaragoza (see below – seizing the growth opportunity in Spain – for further details)

Group like-for-like net rental income

Like-for-like net rental income was 1.5 per cent lower than the same period in 2016 due to non-recurring rental items in the first halfof 2016 not repeating and the impact of the closure of BHS which was fully income producing in the first half of 2016, partially offsetby rental growth from new lettings and rent reviews, analysed as follows:

First half First half 2017 2016 % %Rent reviews, improved letting and turnover income +2.5% +2.3%Capital investment +0.5% +0.9%Vacancy impact -0.2% +1.9%Units closed for redevelopment -2.1% –Other letting activity (e.g. bad debt; surrender premiums) -2.2% +2.4%Total like-for-like net rental income -1.5% +7.5%

Our guidance for full year like-for-like net rental income is around 0 per cent, at the bottom end of the previously announced rangeof 0 to 2 per cent. As previously stated, the precise outcome will be dependent on the timing of letting some of the larger units.These units, predominantly the former BHS units, are now in advanced legals but closure of these transactions is slightly behindour original targets with longer term growth prospects undiminished. We expect the reletting of the former BHS units to increasethe rents on these units by around 15 per cent in aggregate.

UK operating metrics First half Full year First half 2017 2016 2016Occupancy 95.9% 96.0% 96.1%- of which, occupied by tenants trading in administration 0.3% 0.5% 1.3%Leasing activity - number, new rent 80, GBP17m 187, GBP35m 82, GBP16m- new rent relative to previous passing 7% above 4% above 7% aboveFootfall -0.5% +1.3% +1.3%Retailer sales (like-for-like centres) -2.1% +0.2% +0.2%Rent to estimated sales (exc. anchors and major space users) 12.4% 12.2% 12.5%

Occupancy is 95.9 per cent, in line with 31 December 2016 and 30 June 2016. Five UK centres now have occupancy of 98 percent or above.

We agreed 80 new long-term leases in the period, amounting to GBP17 million new annual rent, at an average of 7 per cent above

previous passing rent (like-for-like units) and in line with valuers' assumptions. Retailers continue to focus on increasing their spacein prime, high footfall retail destinations. Significant activity in the period includes:- key fashion retailers upsizing to optimise their offering and configuration, including Next and River Island at intu Merry Hill- aspirational and international brands continuing to recognise the attraction of destination shopping centres, with Hugo Boss and Guess joining the line up at intu Metrocentre, Tesla and Victoria's Secret at intu Milton Keynes, Tag Heuer opening its first store in the West Midlands at intu Merry Hill and Paul Smith opening its first Manchester store at Manchester Arndale- traditional retail park tenants introducing smaller format stores in our prime high footfall locations. This includes Decathlon at intu Uxbridge, taking part of the former BHS unit, and Sharps Bedrooms at intu Lakeside, intu Eldon Square and intu Broadmarsh

84 new shops opened or refitted in our UK centres in the first half of 2017, around 3 per cent of our 2,800 units. Tenants haveinvested around GBP41 million in these stores, a significant demonstration of their commitment to our centres.

We settled 117 rent reviews in the period for new rents totalling GBP27 million, an average uplift of 8 per cent on the previous rents.

Footfall was 0.5 per cent lower than the same period in 2016. The closure of the Sainsbury's unit for redevelopment at intu MerryHill and the short-term impact on our Manchester centres following the terrorist attack in the city have impacted the period.Excluding these, other centres were 0.4 per cent ahead of 2016. This is ahead of the ShopperTrak measure of UK national retailfootfall which is down by 2.7 per cent for the same period.

Estimated retailer sales in our centres were down 2.1 per cent in the period. The ratio of rents to estimated sales for standard unitsremained stable in the period at 12.4 per cent.

The difference between annual property income (see glossary) of GBP490 million and ERV of GBP569 million represents GBP38 million fromvacant units and reversion of GBP41 million, 8 per cent, from rent reviews and lease expiry. Of the 8 per cent reversion, 1 per cent isonly realisable on expiry of leases with over 10 years remaining (e.g. anchor units), leaving 7 per cent realisable from other leaseexpiries and rent reviews.

The weighted average unexpired lease term is 7.3 years (31 December 2016: 7.7 years). 89 per cent of our top 40 tenants, over 50per cent of the rent roll, have a below average risk profile according to Experian Delphi bands, illustrating the quality and longevityof our income streams.

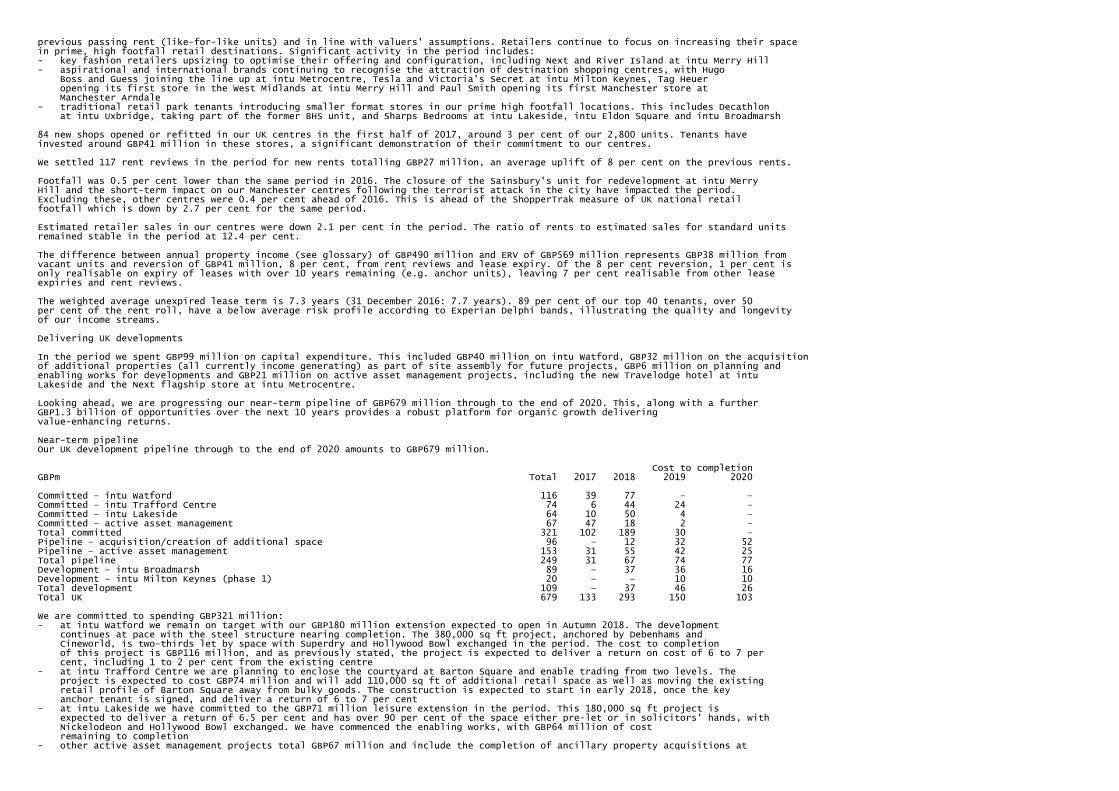

Delivering UK developments

In the period we spent GBP99 million on capital expenditure. This included GBP40 million on intu Watford, GBP32 million on the acquisitionof additional properties (all currently income generating) as part of site assembly for future projects, GBP6 million on planning andenabling works for developments and GBP21 million on active asset management projects, including the new Travelodge hotel at intuLakeside and the Next flagship store at intu Metrocentre.

Looking ahead, we are progressing our near-term pipeline of GBP679 million through to the end of 2020. This, along with a furtherGBP1.3 billion of opportunities over the next 10 years provides a robust platform for organic growth delivering value-enhancing returns.

Near-term pipelineOur UK development pipeline through to the end of 2020 amounts to GBP679 million.

Cost to completionGBPm Total 2017 2018 2019 2020 Committed – intu Watford 116 39 77 – –Committed – intu Trafford Centre 74 6 44 24 –Committed – intu Lakeside 64 10 50 4 –Committed – active asset management 67 47 18 2 –Total committed 321 102 189 30 –Pipeline – acquisition/creation of additional space 96 – 12 32 52Pipeline – active asset management 153 31 55 42 25Total pipeline 249 31 67 74 77Development – intu Broadmarsh 89 – 37 36 16Development – intu Milton Keynes (phase 1) 20 – – 10 10Total development 109 – 37 46 26Total UK 679 133 293 150 103

We are committed to spending GBP321 million:- at intu Watford we remain on target with our GBP180 million extension expected to open in Autumn 2018. The development continues at pace with the steel structure nearing completion. The 380,000 sq ft project, anchored by Debenhams and Cineworld, is two-thirds let by space with Superdry and Hollywood Bowl exchanged in the period. The cost to completion of this project is GBP116 million, and as previously stated, the project is expected to deliver a return on cost of 6 to 7 per cent, including 1 to 2 per cent from the existing centre- at intu Trafford Centre we are planning to enclose the courtyard at Barton Square and enable trading from two levels. The project is expected to cost GBP74 million and will add 110,000 sq ft of additional retail space as well as moving the existing retail profile of Barton Square away from bulky goods. The construction is expected to start in early 2018, once the key anchor tenant is signed, and deliver a return of 6 to 7 per cent- at intu Lakeside we have committed to the GBP71 million leisure extension in the period. This 180,000 sq ft project is expected to deliver a return of 6.5 per cent and has over 90 per cent of the space either pre-let or in solicitors' hands, with Nickelodeon and Hollywood Bowl exchanged. We have commenced the enabling works, with GBP64 million of cost remaining to completion- other active asset management projects total GBP67 million and include the completion of ancillary property acquisitions at

intu Merry Hill, the Halle Place restaurant redevelopment at Manchester Arndale and the creation of flagship stores for Next at intu Metrocentre and intu Merry Hill. These projects are expected to deliver returns of between 6 and 10 per cent

Our pipeline of planned projects amounts to GBP249 million:- extending the space of existing centres by developing non-income producing areas and acquiring certain adjacent properties is expected to cost GBP96 million. This includes the leisure extension at intu Merry Hill which forms part of our strategy for repositioning the centre. This project is expected to have similar returns to the leisure extension at intu Lakeside- other active asset management projects at the feasibility stage amount to GBP153 million and are across all centres. We have the flexibility to start these projects when we have the required level of pre-lets and expect them to deliver similar returns to those that we have committed to

Extensions and redevelopments to which we have not yet committed are expected to cost GBP109 million. The majority of this relatesto the redevelopment of intu Broadmarsh which is expected to cost GBP89 million and deliver a stabilised initial yield of around 7 percent. In the period, we have signed The Light cinema to anchor the scheme and we would expect to have the required level of pre-lets and completed detailed design to enable us to commit to this by the end of the year. The remaining GBP20 million is thecommencement of phase one of the redevelopment of space at intu Milton Keynes, the planning approval of which has now beenreinstated after the successful outcome of a public inquiry.

Future opportunitiesBeyond 2020, we continue to work on securing the required planning approvals and tenant demand to start GBP1.3 billion of projectswhich we would expect to deliver stabilised initial yields of around 7 per cent. We have the required planning approvals forextensions to intu Lakeside, intu Victoria Centre, intu Braehead and intu Milton Keynes and are at earlier stages of the approvalprocess for the extension at Cribbs Causeway.

FundingWe will fund our near-term pipeline from cash and available facilities and from recycling capital to deliver superior returns. Proforma cash and available facilities at 30 June 2017 were GBP920 million. Further recycling potential lies in the introduction of partnersinto some of our centres, although this would have a short-term impact on earnings through the development phase.

In addition, we expect to raise finance on near-term projects, such as the intu Watford extension, as they complete to fund futureopportunities.

Making the brand count

As the role of a shopping centre operator becomes ever more specialised, the steps we have taken following the rebranding havepositioned us well to ensure our centres remain relevant for both customers and retailers. To ensure the highest quality and theability to deliver initiatives quickly, it is important that we control and manage all our space directly.

The first step of this was to bring all staff in-house and ensure we deliver the best customer service. In addition, we took control ofall our commercialisation within the malls, through intu Experiences, to control the quality and quantity of our mall, promotional andmedia activity. Finally, we embraced the multichannel world of retail introducing a transactional website through intu Digital.

Overall, our scale, expertise and insight along with our in-house teams ensure we offer the best customer service and experiencein an ever evolving multichannel world.

Customer serviceOur focus on putting the customer first is embedded in our culture, with our net promoter score, a measure of customer service,running consistently high at around 70. Pleasingly, the range of scores across centres is narrowing as we are able to roll-out bestpractices across the portfolio.

intu ExperiencesCuration of the customer experience is a key element of our role in managing shopping centres. Having an in-house teamdelivering nationwide immersive brand partnerships, mall commercialisation and advertising is crucial in ensuring everything meetsour quality standards and is complementary to the asset strategy for each centre.

An example of this end to end control is through the large format digital screens we are introducing to centres, providing newincome streams. We own all these screens and in many instances produce the content in an area of growth for us.

Similarly, choosing the brands we work with promotionally is important in delivering the right messages. Through the Easterholidays we furthered our collaboration with Nick Jr., Nickelodeon's pre-school television channel, adding augmented realityfunctionality to our in-centre app to deliver a new family experience to our customers.

We can also focus on innovations and are working with Virgin StartUp on 'Foodpreneur', a competition to find aspiring foodentrepreneurs, and we have launched intu Accelerate, looking for innovative ideas in the retail and leisure market through a 10week incubation programme.

intu DigitalThe attraction of our digital offering through our premium content publisher and shopping platform, intu.co.uk, saw an increase ofover 50 per cent in online sales for retailers in the first six months of 2017.

We recorded an increase in website visits in the period of 2 per cent on the previous year. Visits to centre specific pages showingthe likes of opening times are reducing as search engines provide more of this basic information. However, we are seeing year-on-year growth of over 80 per cent in visits to our shopping platform which offers product comparison from 470 retailers. Key to thisgrowth is our online marketing to the 2.5 million individuals on our active marketing database and over one million social mediaaudience.

Commitment to the communityWe are performing strongly against our 2020 environmental targets, set against a 2010 base line, with a 47 per cent intensityreduction in carbon emissions (target 50 per cent), 100 per cent of waste diverted from landfill of which 74 per cent is recycled(targets 99 per cent and 75 per cent respectively) and a 14 per cent water intensity reduction (target 10 per cent).

Our people are crucial to what we do and in 2017 we have achieved the internationally recognised accreditation Investors inPeople gold standard across all intu branded centres. This highly regarded achievement defines what it takes to lead, support andmanage people well for sustainable results.

Seizing the growth opportunity in Spain

Our Spanish strategy is to create a business of scale through acquisitions and our pipeline of development projects. Concentratingon the top 10 key catchments, we aim to establish a market leading position in the country through ownership and management ofprime shopping resorts. We own and manage three of Spain's top 10 shopping centres and have four development sites with themost advanced project being intu Costa del Sol, near Málaga.

AcquisitionIn March 2017, we acquired Madrid Xanadú, one of Spain's top 10 shopping centres, for an agreed price of EUR530 million. Thecentre has many of the key retailers, including El Corte Ingles, all of the Inditex fascias, Primark and Apple, along with a strongleisure offering of Spain's only indoor ski slope, cinema, bowling and soon to open aquarium and Nickelodeon theme park. Footfallis 13 million, with a potential catchment of four million people living within a 30 minute drive time. There is good reversionarypotential over the medium term, with further growth opportunity from key asset management initiatives which will enhance thecentre's status as a truly regional retail and leisure resort, drawing visitors from a wider catchment.

Further, in May 2017, we announced the formation of a joint venture with TH Real Estate for them to take ownership of 50 per centof Madrid Xanadú based on the original acquisition price. This is expected to complete imminently.

Operational performanceThe occupancy of our Spanish centres is 98 per cent, with Puerto Venecia and Madrid Xanadú both 98 per cent and intu Asturias97 per cent.

We agreed 23 new long-term lettings in the period, amounting to over EUR1 million new annual rent, at an average of 14 per centabove previous passing rent (like-for-like units) and ahead of valuers' assumptions. New names to our centres included Quiz, Levisand Pandora.

In the period we have completed a redevelopment of a previously underutilised area at intu Asturias to introduce a supermarketand new retail units which has opened with one unit remaining to be let. The development has impacted footfall and sales for thecentre in the first six months of the year as the work continued, but this has picked up strongly since opening. Excluding thisimpact, footfall and sales increased in aggregate by around 1 per cent at the other two centres.

We have increased the value of the centres owned throughout the period with our share of Puerto Venecia, Zaragoza, valued atEUR256 million, an increase of 3 per cent, and our share of intu Asturias increased by 4 per cent, to EUR146 million. The investment market in Spain remains strong with continued demand for quality shopping centres.

Near-term pipeline

Cost to completionGBPm Total 2017 2018 2019 2020Committed 4 3 – 1 –Pipeline 40 5 5 15 15intu Costa del Sol 470 – 98 186 186Total 514 8 103 202 201

We are committed to spend GBP4 million, mainly at intu Asturias, and have a pipeline of proposed projects of GBP40 million through tothe end of 2020. These are across all three centres and focus on enhancing the resort content of each centre.

Our plan for intu Costa del Sol, near Málaga, is to develop a shopping resort of around 230,000 sq. m. to target the three millionresidents and 10 million annual tourists to the region. We have received the required planning approval from the local(Torremolinos) town hall and the final approval from the regional government could be received by the end of the year. We havestrong interest from potential tenants and would anticipate being on site in the second half of 2018.

The total cost of the development is expected to be around EUR750 million, including the EUR82 million already incurred by intu, anddeliver a stabilised initial yield of around 7 per cent. We have previously included this project on the basis of introducing a partnerto the project at an early stage, however our current plan is to develop alone and fund through bank and other finance, introducinga partner at a later stage.

Future opportunitiesWe continue to develop plans at the three other sites in Valencia, Palma and Vigo, with intu Valencia being the most likely to followintu Costa del Sol.

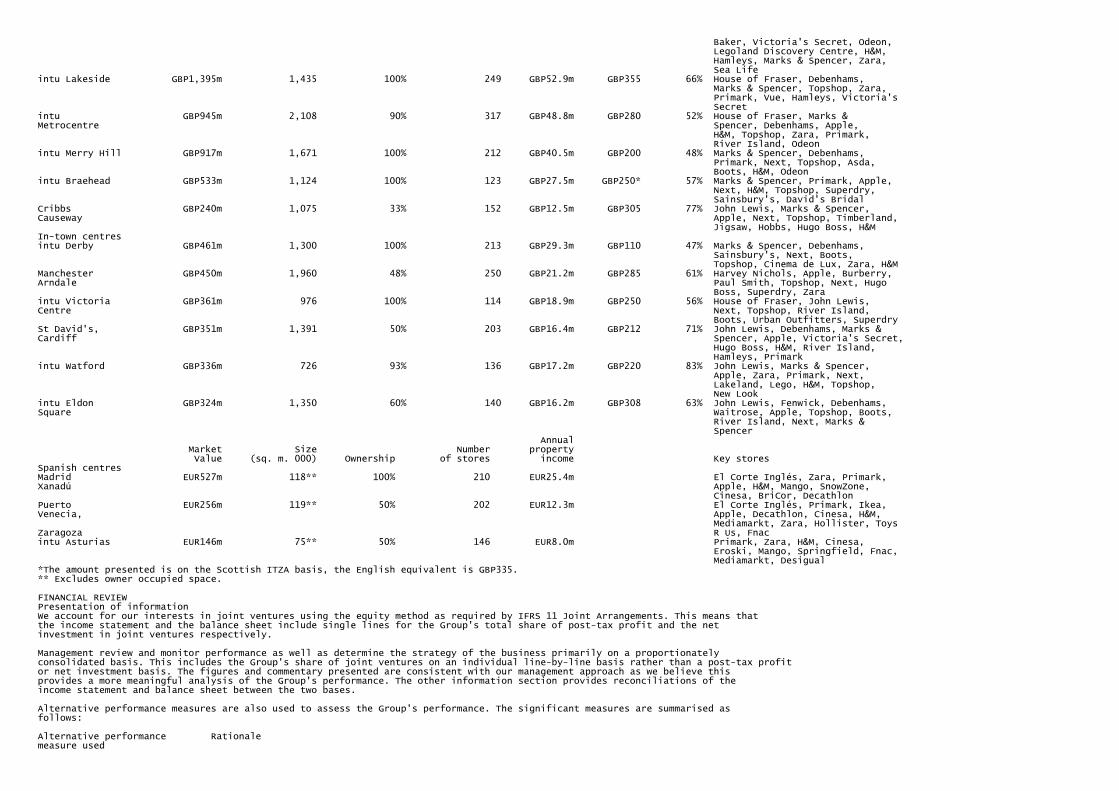

TOP PROPERTIES Annual Headline Market Size Number property rent ABC value (sq. ft. 000) Ownership of stores income ITZA customers Key storesSuper-regional centresintu Trafford GBP2,324m 1,973 100% 228 GBP94.6m GBP435 66% Debenhams, Topshop, Selfridges,Centre John Lewis, Next, Apple, Ted

Baker, Victoria's Secret, Odeon, Legoland Discovery Centre, H&M, Hamleys, Marks & Spencer, Zara, Sea Lifeintu Lakeside GBP1,395m 1,435 100% 249 GBP52.9m GBP355 66% House of Fraser, Debenhams, Marks & Spencer, Topshop, Zara, Primark, Vue, Hamleys, Victoria's Secretintu GBP945m 2,108 90% 317 GBP48.8m GBP280 52% House of Fraser, Marks &Metrocentre Spencer, Debenhams, Apple, H&M, Topshop, Zara, Primark, River Island, Odeonintu Merry Hill GBP917m 1,671 100% 212 GBP40.5m GBP200 48% Marks & Spencer, Debenhams, Primark, Next, Topshop, Asda, Boots, H&M, Odeonintu Braehead GBP533m 1,124 100% 123 GBP27.5m GBP250* 57% Marks & Spencer, Primark, Apple, Next, H&M, Topshop, Superdry, Sainsbury's, David's BridalCribbs GBP240m 1,075 33% 152 GBP12.5m GBP305 77% John Lewis, Marks & Spencer,Causeway Apple, Next, Topshop, Timberland, Jigsaw, Hobbs, Hugo Boss, H&MIn-town centresintu Derby GBP461m 1,300 100% 213 GBP29.3m GBP110 47% Marks & Spencer, Debenhams, Sainsbury's, Next, Boots, Topshop, Cinema de Lux, Zara, H&MManchester GBP450m 1,960 48% 250 GBP21.2m GBP285 61% Harvey Nichols, Apple, Burberry,Arndale Paul Smith, Topshop, Next, Hugo Boss, Superdry, Zaraintu Victoria GBP361m 976 100% 114 GBP18.9m GBP250 56% House of Fraser, John Lewis,Centre Next, Topshop, River Island, Boots, Urban Outfitters, SuperdrySt David's, GBP351m 1,391 50% 203 GBP16.4m GBP212 71% John Lewis, Debenhams, Marks &Cardiff Spencer, Apple, Victoria's Secret, Hugo Boss, H&M, River Island, Hamleys, Primarkintu Watford GBP336m 726 93% 136 GBP17.2m GBP220 83% John Lewis, Marks & Spencer, Apple, Zara, Primark, Next, Lakeland, Lego, H&M, Topshop, New Lookintu Eldon GBP324m 1,350 60% 140 GBP16.2m GBP308 63% John Lewis, Fenwick, Debenhams,Square Waitrose, Apple, Topshop, Boots, River Island, Next, Marks & Spencer Annual Market Size Number property Value (sq. m. 000) Ownership of stores income Key storesSpanish centresMadrid EUR527m 118** 100% 210 EUR25.4m El Corte Inglés, Zara, Primark,Xanadú Apple, H&M, Mango, SnowZone, Cinesa, BriCor, DecathlonPuerto EUR256m 119** 50% 202 EUR12.3m El Corte Inglés, Primark, Ikea,Venecia, Apple, Decathlon, Cinesa, H&M, Mediamarkt, Zara, Hollister, ToysZaragoza R Us, Fnacintu Asturias EUR146m 75** 50% 146 EUR8.0m Primark, Zara, H&M, Cinesa, Eroski, Mango, Springfield, Fnac, Mediamarkt, Desigual*The amount presented is on the Scottish ITZA basis, the English equivalent is GBP335.** Excludes owner occupied space.

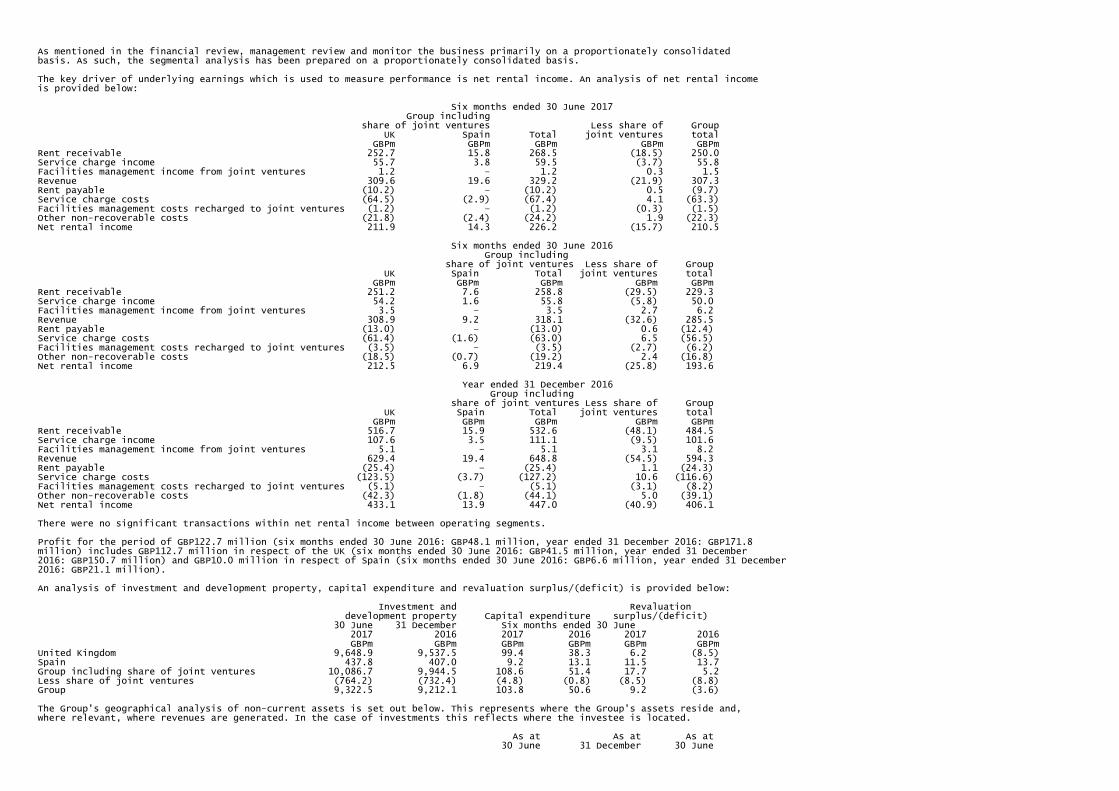

FINANCIAL REVIEWPresentation of informationWe account for our interests in joint ventures using the equity method as required by IFRS 11 Joint Arrangements. This means thatthe income statement and the balance sheet include single lines for the Group's total share of post-tax profit and the netinvestment in joint ventures respectively.

Management review and monitor performance as well as determine the strategy of the business primarily on a proportionatelyconsolidated basis. This includes the Group's share of joint ventures on an individual line-by-line basis rather than a post-tax profitor net investment basis. The figures and commentary presented are consistent with our management approach as we believe thisprovides a more meaningful analysis of the Group's performance. The other information section provides reconciliations of theincome statement and balance sheet between the two bases.

Alternative performance measures are also used to assess the Group's performance. The significant measures are summarised asfollows:

Alternative performance Rationalemeasure used

Like-for-like amounts Like-for-like amounts are presented as they indicate operating performance as distinct from the impact of acquisitions or disposals. In respect of property, the like-for-like measure relates to property which has been owned throughout both periods without significant capital expenditure in either period, so that income can be compared on a like-for-like basis. For the purposes of comparison of capital values, this will also include assets owned at the previous reporting period end but not throughout the prior period. Further analysis is presented in the other information section and in the operating review.

Net asset value ('NAV') NAV (diluted, adjusted) is presented as it is considered to be a key measure of the Group's(diluted, adjusted) performance. The key difference from EPRA NAV, an industry standard comparable measure, is the exclusion of interest rate swaps not currently used for economic hedges of debt as, in our view, this better allows management to review and monitor the Group's performance. A reconciliation of NAV (diluted, adjusted) to NAV attributable to owners of intu properties plc as well as EPRA NAV is provided in note 13(a).

Underlying earnings Underlying earnings is presented as it is considered to be a key measure of the Group's recurring income performance and an indication of the extent to which dividend payments are supported by underlying operations. It excludes property and derivative valuation movements, exceptional items and related tax. The key difference from EPRA earnings, an industry standard comparable measure, relates to adjustments in respect of exceptional items where EPRA is prescriptive about the adjustments that can be made. A reconciliation of underlying earnings to profit for the period attributable to owners of intu properties plc as well as EPRA earnings is provided in note 12(c). The underlying profit statement is also presented in full in the other information section.

Overview

Underlying earnings of GBP98.5 million is marginally down from GBP99.5 million in the first half of 2016. This reflects the reduction in like-for-like net rental income in the period, partially offset by the net impact of recent acquisitions and disposals. Underlying earnings per share of 7.3 pence, a decrease of 3 per cent on the same period in 2016.

Profit for the period attributable to owners of intu properties plc of GBP127.1 million has increased by GBP75.6 million, impacted by thechange in fair value of financial instruments, a surplus of GBP18.7 million (six months ended 30 June 2016: a charge of GBP130.6million), as well as a surplus on property valuations of GBP17.7 million (six months ended 30 June 2016: surplus of GBP5.2 million),partially offset by 2016 gains of GBP74.1 million on the sale of Equity One and GBP34.8 million on the acquisition of the remaining 50 percent of intu Merry Hill.

Net asset value per share of 403 pence is broadly unchanged from 31 December 2016, which when taking account of the dividendpaid in the period of 9.4 pence delivers a total financial return for the six months ended 30 June 2017 of 2.1 per cent.

In March we continued to increase our presence in Spain and strengthen our super prime portfolio, acquiring 100 per cent ofMadrid Xanadú for GBP453.5 million (EUR516.8 million). As part of this we arranged a EUR265 million loan facility, with a 2022 maturity. In May we announced the formation of a joint venture with TH Real Estate for them to take ownership of 50 per cent of MadridXanadú based on the original acquisition price. This transaction is expected to complete imminently. As a result, in accordancewith IFRS, the net assets of Madrid Xanadú have been classified as held for sale in the balance sheet.

Our financing metrics remain strong mainly due to our continued refinancing activity. In the period, we issued and refinanced GBP366million of debt, including the refinancing of intu Milton Keynes in February and financing of the acquisition of Madrid Xanadú inMarch. Our debt to assets ratio of 46.9 per cent (31 December 2016: 43.7 per cent) remains below our target maximum level of 50per cent. Our interest cover ratio of 1.93x has decreased slightly in the year (31 December 2016: 1.97x) with satisfactory headroomabove our target minimum level of 1.60x. At 30 June 2017 we had cash and available facilities of GBP566.9 million which havereduced in the period due to the acquisition of Madrid Xanadú (31 December 2016: GBP922.3 million).

Since the period end we have completed the refinancing of intu Merry Hill with a GBP488 million loan, have secured an additionalGBP250 million facility on intu Trafford Centre and imminently expect to complete the disposal of 50 per cent of Madrid Xanadú. On a pro forma basis, we have a debt to assets ratio of 45.8 per cent and cash and available facilities of GBP920 million.

Income statement Six months ended 30 June 2017 2016 Group Group Share of including including joint share of joint share of joint Group ventures ventures ventures GBPm GBPm GBPm GBPmUnderlying earnings 98.5 – 98.5 99.5Adjusted for:Revaluation of investment and development property 9.2 8.5 17.7 5.2Gain on acquisition of businesses – – – 34.8Loss on disposal of subsidiaries (0.9) – (0.9) –(Loss)/gain on sale of other investments – (0.3) (0.3) 74.1Administration expenses – exceptional (1.7) – (1.7) (1.3)Exceptional finance costs (12.2) – (12.2) (12.4)Change in fair value of financial instruments 18.1 0.6 18.7 (130.6)Tax on the above (0.3) 1.5 1.2 (16.7)Share of joint ventures' items 9.9 (9.9) – –Share of associates' items 4.0 – 4.0 (2.4)Non-controlling interests in respect of the above 2.5 (0.4) 2.1 1.3

Profit for the period attributable to owners ofintu properties plc 127.1 – 127.1 51.5Underlying earnings per share (pence) 7.3p n/a 7.3p 7.5p

Underlying earnings of GBP98.5 million is broadly unchanged from GBP99.5 million in the first half of 2016, the key movements of whichare shown in the chart below. Underlying earnings per share of 7.3 pence, a decrease of 3 per cent on the same period in 2016.

Underlying earnings (GBPm)H1 2016 99.5Net rental income: like-for-like -3.3Net rental income: acquisitions/disposal + 10.1Net finance costs -5.7Administration costs -2.3Other +0.2H1 2017 98.5

Net rental income increased GBP6.8 million primarily due to the acquisition of Madrid Xanadú in March 2017 and the acquisition of theremaining 50 per cent of intu Merry Hill in June 2016, partially offset by the impact of the disposal of intu Bromley in December2016 and the slight reduction in like-for-like net rental income in the period.

Like-for-like net rental income decreased by GBP3.3 million, 1.5 per cent, driven by non-recurring rental items in the first half of 2016and the impact of the closure of BHS which was fully income producing in the first half of 2016, partially offset by rental growth fromnew lettings and rent reviews (see operating review).

Net finance costs have increased by GBP5.7 million primarily due to debt relating to the acquisition of Madrid Xanadú in March 2017,the acquisition of the remaining 50 per cent of intu Merry Hill in June 2016 and the GBP375 million convertible bonds issued inNovember 2016.

The profit for the period attributable to owners of intu properties plc is GBP127.1 million, an increase on the GBP51.5 million reported for the six months ended 30 June 2016. This was primarily due to the change in fair value of financial instruments, a surplus of GBP18.7 million (six months ended 30 June 2016: a charge of GBP130.6 million), as well as a surplus on property valuations of GBP17.7 million (six months ended 30 June 2016: surplus of GBP5.2 million), partially offset by 2016 gains of GBP74.1 million on the sale of Equity One and GBP34.8 million on the acquisition of the remaining 50 per cent of intu Merry Hill.

Our investment in joint ventures contributed GBP18.4 million to the profit of the Group (six months ended 30 June 2016: GBP17.6 million)including GBP8.5 million to underlying earnings (six months ended 30 June 2016: GBP12.1 million) and a gain on property valuations ofGBP8.5 million (six months ended 30 June 2016: GBP8.8 million).

As detailed in the table below, our net rental income margin has reduced to 88 per cent primarily due to higher void costs from theclosure of the former BHS units. Property operating expenses largely comprise car park operating costs and the Group'scontribution to shopping centre marketing programmes. Our ratio of total costs to income, as calculated in accordance with EPRAguidelines, remains low at 15.0 per cent (see other information section).

Six months Six months ended ended 30 June 30 June 2017 2016 GBPm GBPmGross rental income 268.5 258.8Head rent payable (10.2) (13.0) 258.3 245.8Net service charge expense and void rates (14.5) (11.0)Bad debt and lease incentive write-offs (1.4) (1.0)Property operating expense (16.2) (14.4)Net rental income 226.2 219.4Net rental income margin 87.6% 89.3%EPRA cost ratio (excluding direct vacancy costs) 15.0% 14.1%

Balance sheet

30 June 31 December 2017 2016 Group Group Group Share of including including balance joint share of joint share of joint sheet ventures ventures ventures GBPm GBPm GBPm GBPmInvestment and development property 9,322.5 746.2 10,068.7 9,944.5Investment in joint ventures 603.1 (603.1) – –Investment in associates and other investments 86.6 – 86.6 80.7Net external debt (4,605.7) (144.4) (4,750.1) (4,364.1)Derivative financial instruments (351.8) (1.9) (353.7) (380.0)Assets and associated liabilities classified as held for sale 230.7 – 230.7 –Other assets and liabilities (230.2) 6.1 (224.1) (234.7)

Net assets 5,055.2 2.9 5,058.1 5,046.4Non-controlling interest (63.2) (2.9) (66.1) (67.6)Attributable to shareholders 4,992.0 – 4,992.0 4,978.8Fair value of derivative financial instruments 351.8 1.9 353.7 380.0Other adjustments 79.2 (1.9) 77.3 76.3Effect of dilution 2.6 – 2.6 2.6Net assets (diluted, adjusted) 5,425.6 – 5,425.6 5,437.7NAV per share (diluted, adjusted) (pence) 403p – 403p 404p

The Group's net assets attributable to shareholders are GBP4,992.0 million, an increase from GBP4,978.8 million at 31 December 2016,while net assets (diluted, adjusted) are GBP5,425.6 million, a decrease from GBP5,437.7 million at 31 December 2016.

Net asset value per share (pence)31 Dec 2016 404Underlying earnings +7Dividend paid -9Exceptional costs -1Valuation surplus +1Foreign exchange movement +130 Jun 2017 403

NAV per share (diluted, adjusted) at 30 June 2017 decreased from 31 December 2016 to 403 pence with the key movementsshown in the chart above. This was driven principally by underlying earnings in the period of 7.3 pence, offset by the final dividendfor 2016 of 9.4 pence paid in the period.

Investment and development property has increased by GBP124.2 million primarily due to capital expenditure of GBP108.6 million, and asurplus on revaluation of GBP17.7 million. The acquisition of Madrid Xanadú in March has been subsequently classified as an assetheld for sale and therefore does not impact this movement.

Our net investment in joint ventures is GBP603.1 million at 30 June 2017 (31 December 2016: GBP587.6 million), which includes theGroup's share of net assets, on an equity accounted basis, of GBP375.1 million (31 December 2016: GBP355.4 million) and loans to jointventures of GBP228.0 million (31 December 2016: GBP232.2 million). The increase in net investment in joint ventures primarily reflectsthe Group's share of their profit in the period.

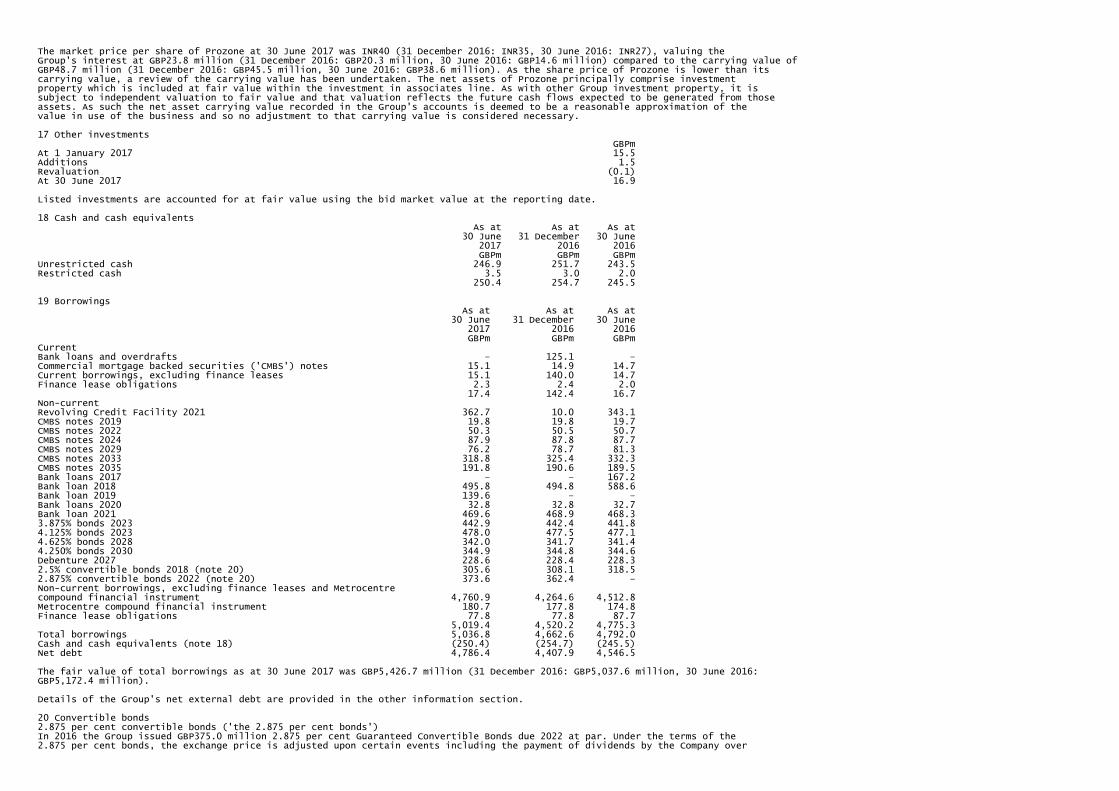

Investments in associates and other investments of GBP86.6 million primarily represent our interests in India, which comprises a 32per cent interest in Prozone (GBP48.7 million), a shopping centre developer listed on the Indian stock market, and a direct interest inEmpire (GBP21.0 million), owner and operator of a shopping centre in Aurangabad. See notes 16 and 17 for further details.

Net external debt of GBP4,750.1 million has increased by GBP386.0 million primarily from funding our acquisition of Madrid Xanadú andcapital expenditure in the period. Cash including the Group's share of joint ventures has reduced by GBP2.7 million to GBP288.9 millionand gross debt has increased by GBP383.3 million to GBP5,039.0 million.

Derivative financial instruments comprise the fair value of the Group's interest rate swaps. The net liability at 30 June 2017 isGBP353.7 million, a decrease of GBP26.3 million in the period, with the UK 10-year bond yield increasing marginally from 1.24 per cent to1.26 per cent. Cash payments in the year totalled GBP21 million, GBP12 million of which has been classified as an exceptional financecost as it relates to payments in respect of unallocated interest rate swaps. The balance of the payments has been included asunderlying finance costs as it relates to ongoing interest rate swaps used to hedge debt.

As previously detailed, we have a number of interest rate swaps, entered into some years ago, which are unallocated due to achange in lenders' practice. At 30 June 2017 these interest rate swaps have a market value liability of GBP239.6 million (31 December2016: GBP253.2 million). It is estimated that we will be required to make cash payments on these interest rate swaps of GBP13 million inthe second half of 2017, GBP28 million in 2018, reducing to below GBP18 million per annum in 2021.

Assets and associated liabilities classified as held for sale of GBP230.7 million relate to Madrid Xanadú. In May we announced theformation of a joint venture with TH Real Estate for them to take ownership of 50 per cent of Madrid Xanadú based on the originalacquisition price. This transaction is expected to complete imminently. As a result, in accordance with IFRS, the net assets ofMadrid Xanadú have been classified as held for sale in the balance sheet.

The non-controlling interest at 30 June 2017 relates primarily to our partner's 40 per cent stake in intu Metrocentre.

We are exposed to foreign exchange movements on our overseas investments and our policy is to ensure that the net exposure toforeign currency is less than 10 per cent of the Group's net assets attributable to shareholders. At 30 June 2017 the exposure, proforma for the 50 per cent disposal of Madrid Xanadú, is 8 per cent, higher than the 7 per cent at 31 December 2016 due to ourincreased exposure in Spain from the acquisition of Madrid Xanadú.

Cash flow

Six months ended Six months ended 30 June 2017 30 June 2016 GBPm GBPmGroup cash flow as reported Cash flows from operating activities 67.9 73.0Cash flows from investing activities (539.7) (244.8)Cash flows from financing activities 466.9 140.6Foreign currency movements 0.1 1.1Net decrease in Group cash and cash equivalents (4.8) (30.1)

During the six months ended 30 June 2017 cash and cash equivalents decreased by GBP4.8 million.

Cash flows from operating activities of GBP67.9 million are GBP5.1 million lower than 2016, primarily due to the timing of payments.Cash flows from investing activities reflect cash outflows for our acquisition of Madrid Xanadú of GBP446.3 million and capitalexpenditure paid during the period of GBP91.3 million.

Cash flows from financing activities include net debt drawdowns of GBP586.4 million primarily to fund our acquisition of MadridXanadú, partially offset by dividends paid in cash during the period of GBP117.8 million.

Financing

Debt structureWe have carried out significant refinancing activity in recent years which has resulted in diversified sources of funding, includingsecured bonds plus syndicated bank debt secured on individual or pools of assets, with limited or no recourse from the borrowingentities to other Group companies outside of these arrangements. Our corporate-level debt remains limited to the Revolving CreditFacility ('RCF') as well as the GBP375 million and GBP300 million convertible bonds.

During the period we undertook the following financing activities: - agreed a new GBP140 million facility secured against intu Milton Keynes, replacing the previous GBP125 million loan, maturing in 2019 - agreed a EUR265 million facility in connection with the acquisition of Madrid Xanadú, maturing in 2022

Since the period end, we have completed the refinancing of intu Merry Hill with a GBP488 million secured facility, now maturing in2024, and have secured an additional GBP250 million loan on intu Trafford Centre, maturing in 2022. Based on the current shareprice, it is likely the GBP300 million convertible bonds, maturing in 2018, will be repaid in cash. The chart below illustrates that wehave no major refinancing requirement due until 2021.

Debt maturity (GBPm) 2017 82018 3232019 2862020 882021 9212022 7732023 9582024 6022025 272026 282027-2031 1.0752032-2036 261

Debt measures 30 June 31 December 2017 2016Debt to assets 45.8%1 43.7%Interest cover 1.93x 1.97xWeighted average debt maturity 7.1 years(1) 7.1 years2Weighted average cost of gross debt 4.3%(1) 4.3%Proportion of gross debt with interest rate protection 99%(1) 88%Cash and available facilities GBP919.6m(1) GBP922.3m

1 Pro forma for intu Merry Hill refinancing, additional GBP250 million loan on intu Trafford Centre and disposal of 50 per cent of Madrid Xanadú.2 Pro forma for intu Milton Keynes refinancing, completed February 2017.

On a pro forma basis, our debt to assets ratio has increased to 45.8 per cent since 31 December 2016 due to the acquisition ofMadrid Xanadú and remains below our target maximum level of 50 per cent. Our weighted average debt maturity is unchanged at7.1 years and the weighted average cost of gross debt is unchanged at 4.3 per cent (excluding the RCF).

Interest cover of 1.93x has decreased slightly during the period and remains above our target minimum level of 1.60x.

We use interest rate swaps to fix interest obligations, reducing any cash flow volatility caused by changes in interest rates. Theproportion of debt with interest rate protection on a pro forma basis has increased in the period to 99 per cent within our policyrange of between 75 per cent and 100 per cent.

CovenantsFull details of the debt financial covenants are included in the other information section of this report. We are in compliance with allof our covenants and regularly stress test them for changes in capital values and income. A 25 per cent fall in property values anda 10 per cent reduction in income would only require a GBP10 million equity cure.

Capital commitmentsWe have an aggregate commitment to capital projects of GBP325.0 million at 30 June 2017 (31 December 2016: GBP257.0 million).In addition to the committed expenditure, we have an identified uncommitted pipeline of active management projects, majorextensions and developments that may become committed over the next three years (see operating review).

Other information

Tax policy positionLike all Real Estate Investment Trusts ('REIT's), tax on property operating profits is paid at shareholder level to the UKGovernment rather than by the Group. REIT status brings with it the requirement to operate within the rules of the REIT regime(see glossary for further information).

The Group's principle of good governance extends to our responsible approach to tax. We look to minimise the level of taxrisk and at all times seek to comply fully with our regulatory and other tax obligations and to act in a way which upholds intu'sreputation as a responsible corporate citizen by regularly carrying out risk reviews, seeking pre-clearance from HMRC in complexareas and actively engaging in discussions regarding proposed changes in the taxation system that might affect the Group. Itremains important to our stakeholders that our approach to tax is aligned to the long-term values and strategy of the Group. TheChief Financial Officer is the Executive Committee member with executive responsibility for tax matters, with close involvement ofexecutive and senior management.

We pay tax directly on overseas earnings, any UK non-property income under the REIT rules, business rates and transaction taxessuch as stamp duty land tax. In the six months ended 30 June 2017 the total of such payments to tax authorities was GBP13.1 million,of which GBP11.6 million was in the UK and GBP1.5 million in Spain. In addition, we also collect VAT, employment taxes and withholdingtax on dividends for HMRC and the Spanish tax authorities.

DividendsThe Directors are recommending an interim dividend of 4.6 pence per share in line with the 2016 interim dividend. A scrip dividendalternative may be offered. Details of the apportionment between the PID and non-PID elements per share will be confirmed indue course.

MARKET REVIEWUK investment market

Low interest rates and a weakened value of sterling mean that prime shopping centres continue to attract interest from internationalinvestors. Whilst activity was limited in the first half of 2017 as the UK general election took centre stage, good levels of demandremain for quality assets in the UK's liquid and transparent market for large shopping centres.

However, a flight to quality has ensured prime yields remain stable as investors look at the quality and longevity of income streamscoupled with rental growth potential in a market where new supply, by way of development, remains low. Against this, yields onsecondary assets are drifting outwards due to investors perceiving a relatively poor outlook for such assets.

UK consumer market

Uncertainty from the early stages of discussions of the UK's exit from the EU is creating a mixed picture on the state of the UKconsumer. Unemployment continues at record low levels which should in turn drive earnings growth. However, the increase ininflation from the weakening of sterling after the EU referendum vote is causing prices to rise faster than wages at the momentwhich impacts consumers' disposable income. This is reflected in the Asda benchmark index of household income which hasshown a reduction of 2 per cent since December 2016.

Looking further ahead, the Bank of England's forecasts suggest that wage growth will overtake inflation as we go into 2018.

Consumer confidence, as measured by GfK, had remained broadly stable over the majority of the first half of 2017, but hasdropped following the UK general election in June 2017, reflecting negative sentiment about consumers' personal finances andexpectations for the wider economy.

These mixed messages have not had a material effect on non-food retail spending, which remains unchanged against 2016 (BritishRetail Consortium like-for-like non-food retail index).

Occupier market

Retail is one of the UK's most dynamic and flexible industries which has always been able to adapt quickly in fast-changingenvironments. Retailers are facing both economic and structural challenges and the winners will be those with the right stores inthe right places, who align their online and instore strategies and who give customers an experience they cannot get elsewhere.

Economic pressures include the impact on retailers' cost bases from the weakness of sterling, business rates revaluations andincreases in the national living wage. The current squeeze on disposable income from higher inflation may add more pressure.

Structurally, retailers are still evolving in relation to the opportunities and costs of online shopping with those possessing a strongstore network benefitting from click and collect. This enables them to use their existing efficient distribution networks to reducedelivery costs and convert additional sales when the customer is instore.

Considering the challenges that face them, many retailers are looking at fewer stores, but in the best locations offering high footfallfrom a compelling mix of retail, catering and leisure. This demand is spread across all unit sizes with the powerhouse fashionbrands taking larger flagships and introducing their sub-brands, traditional big box retailers refining their offer to smaller shoppingcentre size stores, new international and aspirational lifestyle brands successfully entering the shopping centre market and thecontinued growth in new leisure concepts. Whilst the rapid expansion of food and beverage operators in the last few years isslowing, leisure operators are increasingly looking at shopping centres for their expansion plans.

With our prime portfolio of shopping centres, offering compelling customer experiences and a sophisticated online offer, we arewell positioned to meet the demands of this changing world, including the trend of online retailers taking physical stores, althoughthis is still at an early stage.

Retailer administrations in the period remained at relatively low levels. Jones the Bootmaker (three units), 99p Stores (one unit)and Handmade Burger Co. (four units) entered administration in the period and amount in total to 0.4 per cent of intu's rent roll.

Spanish market

In recent years, the Spanish economy has had significant growth making it one of Europe's fastest growing economies. Forecastssuggest that this is expected to continue in 2017 with its GDP growth expected to be one of the highest of the major Europeaneconomies. For the consumer, unemployment is at its lowest level for several years and consumer confidence at its highest. This inturn benefits retail sales which are further enhanced by record levels of tourists.

The investment market remains strong with continuing investor confidence in Spanish real estate supported by an economy that isgrowing. With the return of bank financing, the weight of money in the market looking to invest in quality assets has continued tostrengthen the market. Due to lack of development in recent years, prime regional shopping centres are a scarce asset class whichis reflected in good demand.

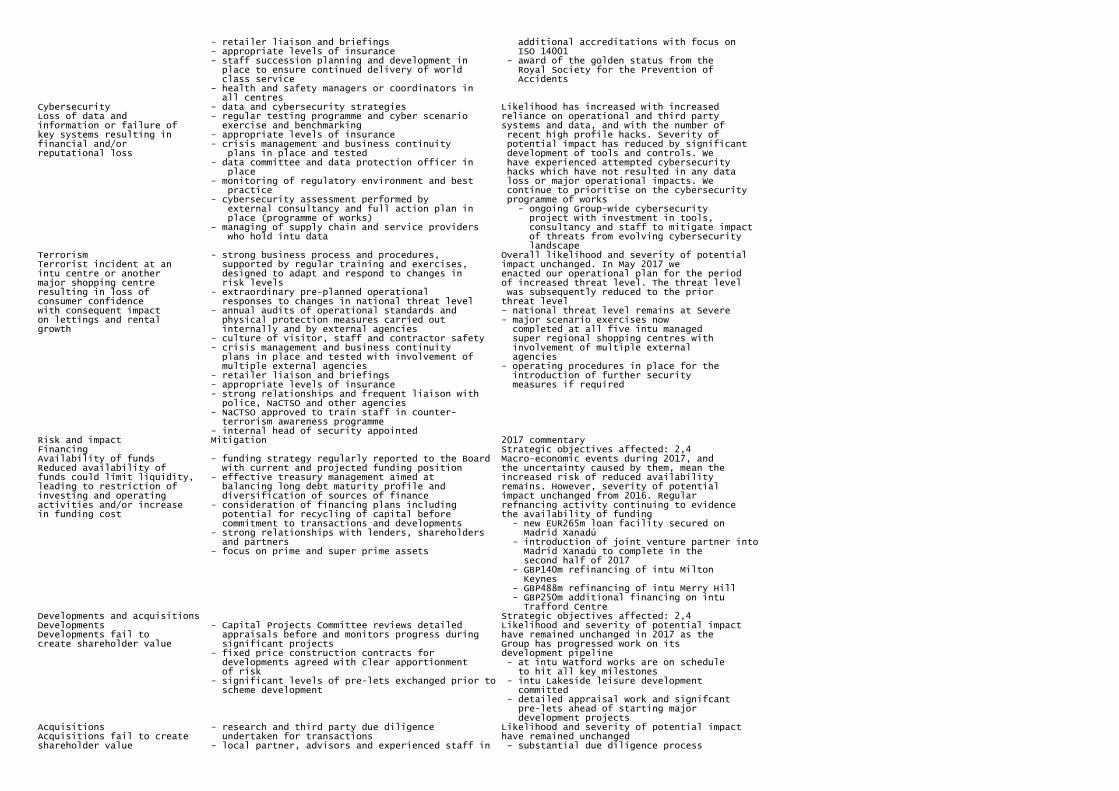

PRINCIPAL RISKS AND UNCERTAINTIESintu's Board has responsibility for establishing the Group's appetite for risk on the balance of potential risks and returns, and hasoverall responsibility for identifying and managing risks. The Board has updated its assessment of the principal risks facing theGroup, including those that would impact the business model, future performance, solvency or liquidity.

Principal risks and uncertainties are identified under five key headings: property market; operations; financing; developments andacquisitions; and brand. These are discussed in detail below. A principal risk is one which has the potential to significantly affectthe Group's strategic objectives, financial position or future performance and includes both internal and external factors. Wemonitor movements in likelihood and severity such that the risks are appropriately mitigated in line with the Group's risk appetite.

The risk profile for the six months ended 30 June 2017 has remained broadly in line with the year ended 31 December 2016 withno significant new risks identified nor substantial changes in existing risks. Uncertainty in the UK economy and real estate marketsfollowing the EU referendum vote last year ('Brexit') has not resulted in any material adverse impacts, although recent UK generalelection results may create some further uncertainty. Following recent events we remain focused on our approach to terrorism andcybersecurity.

Key to strategic objectives: Change in level of risk:1) Optimising asset performance Remained the same 2) Delivering UK developments3) Making the brand count4) Seizing the growth opportunity in Spain

Risk and impact Mitigation 2017 commentaryProperty market Strategic objectives affected: 1,2,3,4Macro-economic - focus on prime and super prime assets together Likelihood of macro-economic weaknessWeakness in the macro- with their upgrading continues to be a risk with politicaleconomic environment - covenant headroom monitored and stress- uncertainty in the UK and Brexitcould undermine rental tested arrangements not yet detailedincome levels and - make representation on key policies, for - like-for-like property values remainingproperty values, reducing example business rates stable in the periodreturn on investment and - large-scale national marketing events across - substantial covenant headroomcovenant headroom centres to attract footfall - no significant near-term debt maturities - leveraging the strength of the intu brand to and average unexpired term attract and retain aspirational retailers unchanged at 7.1 years - continued geographic diversification by - long-term lease structures with average increasing Spanish presence unexpired term of 7.3 years - Purchase of Madrid Xanadú for EUR516.8mRetail environment - active management of tenant mix including Likelihood and severity of potential impactFailure to react to letting of former BHS units was monitored closely in the first half ofchanges in the retail - regular monitoring of tenant strength and 2017 with intu's strategy continuing toenvironment could diversity deliver solid footfall numbers andundermine intu's ability to - upgrading assets to meet demand, for example, occupancyattract customers and increased leisure offering - signifcant progress on planning andtenants - Tell intu customer feedback programme helps pre-letting of near-term pipeline with a identify changes in customer preferences focus on leisure - work closely with retailers - continuing digital investment to improve - digital strategy that embraces technology and relevance as shopping habits change digital customer engagement. This enables intu - occupancy unchanged at 95.9 per cent to engage in and support multichannel retailing, - footfall continues to be ahead of and to take the opportunities offered by benchmark ecommerce - committed to the GBP71m intu Lakeside leisure extension

Risk and impact Mitigation 2017 commentaryOperations Strategic objectives affected: 1,3Health and safety - strong business process and procedures, Likelihood of potential impact has notAccidents or system including compliance with OHSAS 18001, changed signifcantly during the first half offailure leading to financial supported by regular training and exercises 2017, however severity impacted by newand/or reputational loss - annual audits of operational standards and enforcement structure equipment carried out internally and by external - maintenance of OHSAS 18001 consultants certifcation, demonstrating consistent - culture of visitor, staff and contractor safety health and safety management process - crisis management and business continuity and procedures across the portfolio plans in place and tested - work continuing towards achieving

- retailer liaison and briefings additional accreditations with focus on - appropriate levels of insurance ISO 14001 - staff succession planning and development in - award of the golden status from the place to ensure continued delivery of world Royal Society for the Prevention of class service Accidents - health and safety managers or coordinators in all centresCybersecurity - data and cybersecurity strategies Likelihood has increased with increasedLoss of data and - regular testing programme and cyber scenario reliance on operational and third partyinformation or failure of exercise and benchmarking systems and data, and with the number ofkey systems resulting in - appropriate levels of insurance recent high profile hacks. Severity offinancial and/or - crisis management and business continuity potential impact has reduced by significantreputational loss plans in place and tested development of tools and controls. We - data committee and data protection officer in have experienced attempted cybersecurity place hacks which have not resulted in any data - monitoring of regulatory environment and best loss or major operational impacts. We practice continue to prioritise on the cybersecurity - cybersecurity assessment performed by programme of works external consultancy and full action plan in - ongoing Group-wide cybersecurity place (programme of works) project with investment in tools, - managing of supply chain and service providers consultancy and staff to mitigate impact who hold intu data of threats from evolving cybersecurity landscapeTerrorism - strong business process and procedures, Overall likelihood and severity of potentialTerrorist incident at an supported by regular training and exercises, impact unchanged. In May 2017 weintu centre or another designed to adapt and respond to changes in enacted our operational plan for the periodmajor shopping centre risk levels of increased threat level. The threat levelresulting in loss of - extraordinary pre-planned operational was subsequently reduced to the priorconsumer confidence responses to changes in national threat level threat levelwith consequent impact - annual audits of operational standards and - national threat level remains at Severeon lettings and rental physical protection measures carried out - major scenario exercises nowgrowth internally and by external agencies completed at all five intu managed - culture of visitor, staff and contractor safety super regional shopping centres with - crisis management and business continuity involvement of multiple external plans in place and tested with involvement of agencies multiple external agencies - operating procedures in place for the - retailer liaison and briefings introduction of further security - appropriate levels of insurance measures if required - strong relationships and frequent liaison with police, NaCTSO and other agencies - NaCTSO approved to train staff in counter- terrorism awareness programme - internal head of security appointedRisk and impact Mitigation 2017 commentaryFinancing Strategic objectives affected: 2,4Availability of funds - funding strategy regularly reported to the Board Macro-economic events during 2017, andReduced availability of with current and projected funding position the uncertainty caused by them, mean thefunds could limit liquidity, - effective treasury management aimed at increased risk of reduced availabilityleading to restriction of balancing long debt maturity profile and remains. However, severity of potentialinvesting and operating diversification of sources of finance impact unchanged from 2016. Regularactivities and/or increase - consideration of financing plans including refnancing activity continuing to evidencein funding cost potential for recycling of capital before the availability of funding commitment to transactions and developments - new EUR265m loan facility secured on - strong relationships with lenders, shareholders Madrid Xanadú and partners - introduction of joint venture partner into - focus on prime and super prime assets Madrid Xanadú to complete in the second half of 2017 - GBP140m refinancing of intu Milton Keynes - GBP488m refinancing of intu Merry Hill - GBP250m additional financing on intu Trafford CentreDevelopments and acquisitions Strategic objectives affected: 2,4Developments - Capital Projects Committee reviews detailed Likelihood and severity of potential impactDevelopments fail to appraisals before and monitors progress during have remained unchanged in 2017 as thecreate shareholder value significant projects Group has progressed work on its - fixed price construction contracts for development pipeline developments agreed with clear apportionment - at intu Watford works are on schedule of risk to hit all key milestones - significant levels of pre-lets exchanged prior to - intu Lakeside leisure development scheme development committed - detailed appraisal work and signifcant pre-lets ahead of starting major development projectsAcquisitions - research and third party due diligence Likelihood and severity of potential impactAcquisitions fail to create undertaken for transactions have remained unchangedshareholder value - local partner, advisors and experienced staff in - substantial due diligence process

Spain with specialist market knowledge undertaken before acquisition of - where appropriate, investment risk reduced Madrid Xanadú through financing and joint venture investmentsBrand Strategic objectives affected: 1,2,3,4Integrity of the brand - intellectual property protection Likelihood and severity of potential impactThe integrity of the brand - strong guidelines for use of brand unchanged in the first half of 2017is damaged leading to - strong underlying operational controls and crisis - continuing media interest in intu andfinancial and/or management procedures our commentaries and opinions on thereputational loss - ongoing training programme and reward and business and wider landscape recognition schemes designed to embed brand - ongoing development of brand in Spain values and culture throughout the organisation - net promoter score consistently high at - traditional and digital media monitoring and around 70 for the period analysis - Tell intu and shopper view customer feedback programmes

DIRECTORS' RESPONSIBILITY STATEMENTThe Directors are responsible for preparing the interim report and condensed consolidated set of interim financial statements('interim financial statements'), in accordance with applicable law and regulations. The Directors confirm that, to the best of their knowledge:- the interim financial statements have been prepared in accordance with IAS 34 Interim Financial Reporting, as adopted by the European Union; and- the interim report includes a fair review of the information required by Sections DTR 4.2.7R and DTR 4.2.8R of the Disclosure Guidance and Transparency Rules sourcebook of the United Kingdom's Financial Services Authority.

The operating and financial reviews refer to important events which have taken place in the period.

The principal risks and uncertainties facing the business are referred to in the operating and financial reviews.Related party transactions are set out in note 27 of the interim financial statements.

Details, including biographies, of all current Directors are maintained on the intu properties plc website: intugroup.co.uk.

On behalf of the Board

David FischelChief Executive

Matthew RobertsChief Financial Officer27 July 2017

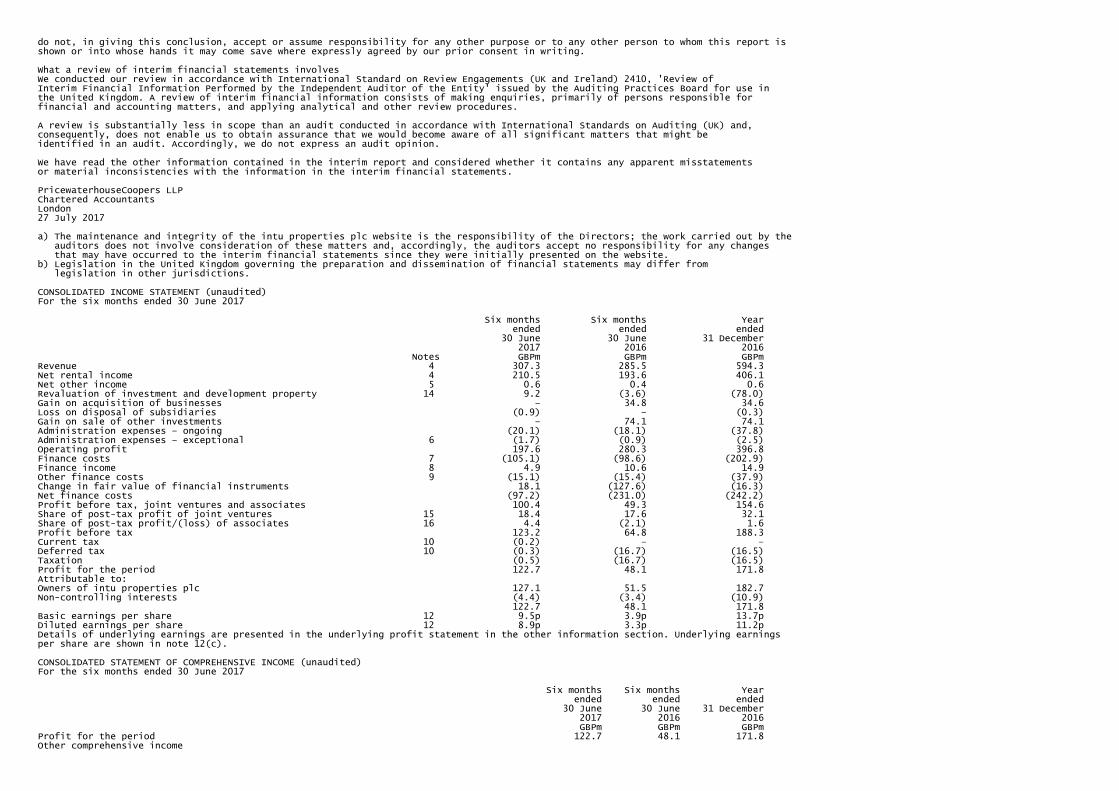

Independent review report to intu properties plcReport on the condensed consolidated interim financial statements

Our conclusionWe have reviewed intu properties plc's condensed consolidated interim financial statements (the "interim financial statements") inthe interim report of intu properties plc for the 6 month period ended 30 June 2017. Based on our review, nothing has come to ourattention that causes us to believe that the interim financial statements are not prepared, in all material respects, in accordancewith International Accounting Standard 34, 'Interim Financial Reporting', as adopted by the European Union and the DisclosureGuidance and Transparency Rules sourcebook of the United Kingdom's Financial Conduct Authority.

What we have reviewedThe interim financial statements comprise:- the consolidated balance sheet as at 30 June 2017;- the consolidated income statement and consolidated statement of comprehensive income for the period then ended;- the consolidated statement of changes in equity for the period then ended;- the consolidated statement of cash flows for the period then ended; and- the explanatory notes to the interim financial statements.