investec final 1 citywire nma conference jan 12

DESCRIPTION

TRANSCRIPT

Citywire New Model Adviser Conference Diversification and the importance of avoiding value traps

Alastair Mundy – Portfolio Manager

Investec Cautious Managed Fund

12-13 January 2012

Page 2 | CONFIDENTIAL

07717

Target audience

This document is only for professional investors, professional financial advisors and, at

their exclusive discretion, their clients. No other person should rely on the information

contained in this document.

If you plan to show this to your clients, please ensure that you comply with any applicable

local marketing regulations.

This document is not to be generally distributed to the public.

Page 3 | CONFIDENTIAL

07717

Four routes to Cautious Managed Funds

Unfettered Fund of Funds

Fund of Passives Directly Invested

Fettered Fund of Funds

Cautious

Managed

Funds

ETFs

ETCs

Trackers UK Equities

Overseas Equities

Fixed Income

Cash

Page 4 | CONFIDENTIAL

07717

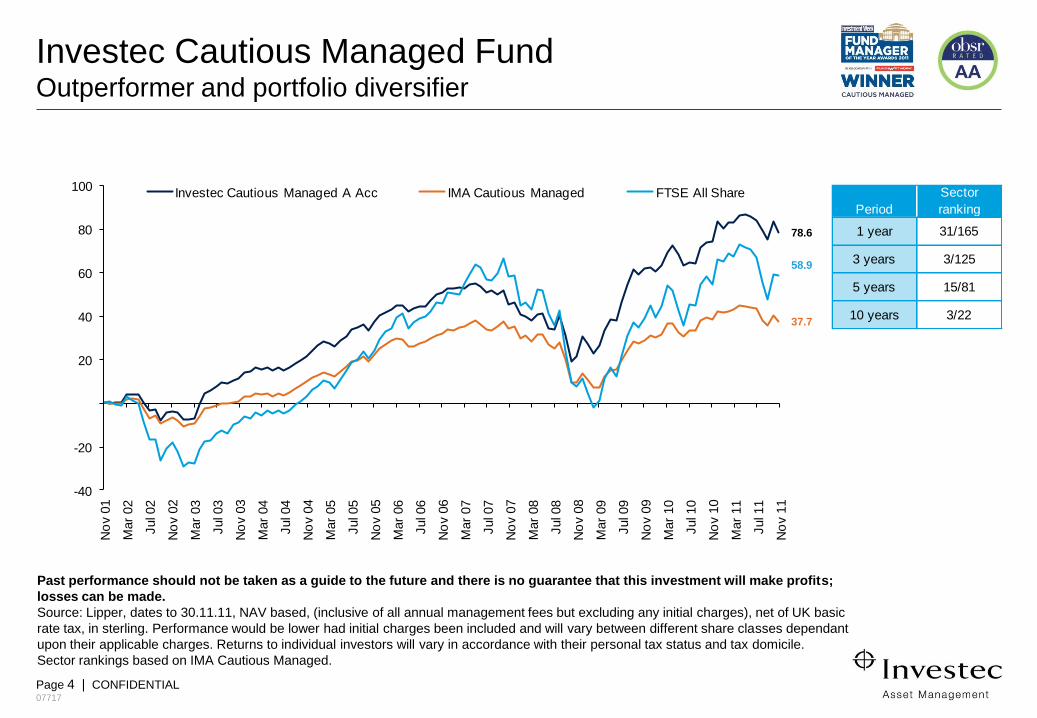

Investec Cautious Managed Fund Outperformer and portfolio diversifier

Past performance should not be taken as a guide to the future and there is no guarantee that this investment will make profits;

losses can be made.

Source: Lipper, dates to 30.11.11, NAV based, (inclusive of all annual management fees but excluding any initial charges), net of UK basic

rate tax, in sterling. Performance would be lower had initial charges been included and will vary between different share classes dependant

upon their applicable charges. Returns to individual investors will vary in accordance with their personal tax status and tax domicile.

Sector rankings based on IMA Cautious Managed.

G:\Depts\Marketing\Presentations\Hamilton Brown Graphics\¬MASTER

OEIC\MASTER Cautious Managed (Alastair Mundy)\Evidence\Master

_UK Cautious Managed Fund.xlsx\Cautious_10

Period

Sector

ranking

1 year 31/165

3 years 3/125

5 years 15/81

10 years 3/22

G:\Depts\Marketing\Presentations\Hamilton Brown Graphics\¬MASTER

OEIC\MASTER Cautious Managed (Alastair Mundy)\Evidence\Master

_UK Cautious Managed Fund.xlsx\Ranking

78.6

37.7

58.9

-40

-20

20

40

60

80

100

No

v 0

1

Mar

02

Jul 0

2

No

v 0

2

Mar

03

Jul 0

3

No

v 0

3

Mar

04

Jul 0

4

No

v 0

4

Mar

05

Jul 0

5

No

v 0

5

Mar

06

Jul 0

6

No

v 0

6

Mar

07

Jul 0

7

No

v 0

7

Mar

08

Jul 0

8

No

v 0

8

Mar

09

Jul 0

9

No

v 0

9

Mar

10

Jul 1

0

No

v 1

0

Mar

11

Jul 1

1

No

v 1

1

Investec Cautious Managed A Acc IMA Cautious Managed FTSE All Share

Page 5 | CONFIDENTIAL

07717

Do calendar year returns provide a good measure of risk?

I would like to point out to people that a year is the amount

of time it takes the earth to go around the sun. It is nothing

to do with the investment or business cycle. You should

really measure a fund manager over a full business cycle.

“ ” Terry Smith

Page 6 | CONFIDENTIAL

07717

Are all Cautious Funds too risky?

● No, but you’re only as good as your

clients....

● ALL investors need to be willing to accept

volatility (i.e. temporary medium-term

loss) to achieve returns

● Investors need to be willing to invest for

AT LEAST 5 years (and probably 10

years)

● Investors must be in a position where

they are NEVER forced sellers

Page 7 | CONFIDENTIAL

07717

Some methods of risk management

● Diversification (Diworsification?) - let’s all be like Yale

● Remain heavily invested in cash at all times

● Short stocks, Pairs trades etc.

● None are foolproof, BUT, EVEN WORSE, some

provide false comfort and encourage overbetting

Page 8 | CONFIDENTIAL

07717

How do we define risk?

● Risk is understanding what you have bought

● It is the potential for PERMANENT capital loss

● You cannot sensibly control risk, markets do

Page 9 | CONFIDENTIAL

07717

Our approach to risk management

● Don’t pretend to yourself you know all the answers. Neuroses and schizophrenia are

the best bedfellows

● Don’t wish for all your investments to rise simultaneously ...if they do, they will probably

fall simultaneously

● Search for complementary assets...but don’t expect too much of them

● Pay a great deal of attention to valuations –

buying something which is cheap is a great

way to reduce risk

● Make sure you understand the worst-case

scenario for each investment. If you can’t

think of one, then you don’t understand

what you are buying

Page 10 | CONFIDENTIAL

07717

The Dinner Party Approach to risk management

● Invite a good mix

● But don’t include too many revellers

● Make sure you leave early and while you

are still enjoying yourself

● Focus on creating a series of good dinner

parties and not about creating the best

dinner party ever

Page 11 | CONFIDENTIAL

07717

Investec Cautious Managed Fund Rolling 5 year total return

Past performance should not be taken as a guide to the future and there is no guarantee that this investment will make

profits; losses can be made.

Source: Lipper, 30.11.06 to 30.11.11, NAV based, (inclusive of all annual management fees but excluding any initial charges), net of

UK basic rate tax, in sterling.

Performance would be lower had initial charges been included and will vary between different share classes dependant upon their

applicable charges. Returns to individual investors will vary in accordance with their personal tax status and tax domicile.

0%

10%

20%

30%

40%

50%

60%

70%

No

v-0

6

Dec-0

6

Jan-0

7

Mar-

07

Ap

r-07

May-0

7

Jun-0

7

Aug

-07

Sep

-07

Oct-

07

Dec-0

7

Jan-0

8

Feb

-08

Ap

r-08

May-0

8

Jun-0

8

Aug

-08

Sep

-08

Oct-

08

No

v-0

8

Jan-0

9

Feb

-09

Mar-

09

May-0

9

Jun-0

9

Jul-09

Sep

-09

Oct-

09

No

v-0

9

Jan-1

0

Feb

-10

Mar-

10

May-1

0

Jun-1

0

Jul-10

Sep

-10

Oct-

10

No

v-1

0

Dec-1

0

Feb

-11

Mar-

11

Ap

r-11

Jun-1

1

Jul-11

Aug

-11

Oct-

11

No

v-1

1

Page 12 | CONFIDENTIAL

07717

How is our investment approach different?

Patience Long waiting periods and long holding periods

Value Committed value investors….we will not chase new paradigms

Contrarian A focus solely on out of favour companies for our buy ideas

Bottom-up We are stock pickers with strong risk controls

Market agnostic Our portfolio is constructed without reference to equity market levels

Downside aware We spend as much time worrying about what might go wrong as about what

might go right

Focus on long term performance We are comfortable to struggle in the short-term and explain ourselves in the

search for superior long term performance

Evolution and improvement A continual programme of navel-gazing

Avoiding Value Traps

Page 14 | CONFIDENTIAL

07717

Bad things do happen

● History supports investing in out of favour shares

● However, there are many examples of falling knives not recovering

● What strategies do we employ to reduce our chances of catching these falling knives?

Page 15 | CONFIDENTIAL

07717

1. Play the averages

● We are not trying to get everything right. Bad things do happen

● Too much fear can result in paralysis

Page 16 | CONFIDENTIAL

07717

2. Patience

● Allow shares to fall significantly before purchase

● Benefits:

− This typically allows us to avoid buying in favour momentum stocks before they

collapse...

− ...and also ensures that we can be more aware of the negatives when we are

analysing the stocks

Page 17 | CONFIDENTIAL

07717

3. Make sure they are cheap

● Buying fallen knives alone is not sufficient – valuation is a key requirement

Page 18 | CONFIDENTIAL

07717

4. Scenario testing

● Make sure that a number of different outcomes are tested to ensure the company’s

balance sheet is appropriate

Page 19 | CONFIDENTIAL

07717

5. Establish your circles of competence

● We cannot hope to be experts on everything

● Some subjects are harder than others

Page 20 | CONFIDENTIAL

07717

6. Watch market share moves

● Industries which exhibit large moves in market shares of its competitors suggest that

companies are more likely to implode

Page 21 | CONFIDENTIAL

07717

7. Consider capacity

● Is it easy for capacity to exit the industry? Are incumbents involved in a race to the

bottom?

● Can capacity enter the industry easily and put a lid on returns?

Page 22 | CONFIDENTIAL

07717

8. Look for early warning signs

● Analysts continue to focus on the P & L, but sometimes the greatest clues are in the

balance sheet

Page 23 | CONFIDENTIAL

07717

What doesn’t work for us in spotting value traps

1. Meeting management

● They stretch the truth well and are typically very plausible

● They cannot provide inside information

● They really do believe conditions will improve...but belief is not always enough

2. Forecasting the future

● Forecasting the future is very difficult and can lead to the risk of over-confidence and the

refusal to consider other alternatives

3. Buy all falling knives

● Might work...but will provide many sleepless nights

Current Thoughts

Page 25 | CONFIDENTIAL

07717

5

10

15

20

25

Jan-8

5A

ug

-85

Mar-

86

Oct-

86

May-8

7D

ec-8

7Jul-88

Feb

-89

Sep

-89

Ap

r-90

No

v-9

0Jun-9

1Jan-9

2A

ug

-92

Mar-

93

Oct-

93

May-9

4D

ec-9

4Jul-95

Feb

-96

Sep

-96

Ap

r-97

No

v-9

7Jun-9

8Jan-9

9A

ug

-99

Mar-

00

Oct-

00

May-0

1D

ec-0

1Jul-02

Feb

-03

Sep

-03

Ap

r-04

No

v-0

4Jun-0

5Jan-0

6A

ug

-06

Mar-

07

Oct-

07

May-0

8D

ec-0

8Jul-09

Feb

-10

Sep

-10

Ap

r-11

No

v-1

1

FTSE350 ex-Investment Trusts Index

Median FTSE 350 ex IT Index Price Earnings ratio suggests

that stocks are fair value

Source: Morgan Stanley, 30.11.11

The median stock

looks far less

attractive...

Equities

cheap

Equities

expensive

...and assumes

the current level

of profitability is

sustainable

Trailing PE Ratio – Median Stock

Page 26 | CONFIDENTIAL

07717

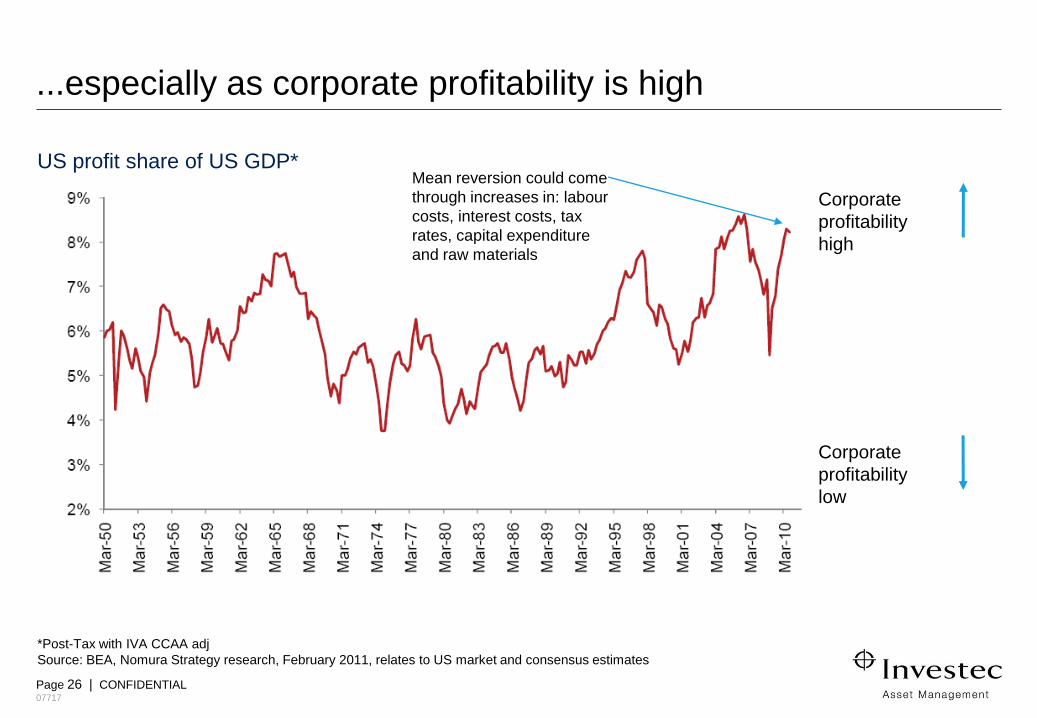

...especially as corporate profitability is high

*Post-Tax with IVA CCAA adj

Source: BEA, Nomura Strategy research, February 2011, relates to US market and consensus estimates

US profit share of US GDP*

Corporate

profitability

low

Corporate

profitability

high

Mean reversion could come

through increases in: labour

costs, interest costs, tax

rates, capital expenditure

and raw materials

Page 27 | CONFIDENTIAL

07717

Investec Cautious Managed Fund Rolling 10 year total return since inception

Past performance should not be taken as a guide to the future and there is no guarantee that this investment will make

profits; losses can be made.

Source: Lipper, 07.06.93 to 30.11.11, NAV based, (inclusive of all annual management fees but excluding any initial charges), net of

UK basic rate tax, in sterling. Performance would be lower had initial charges been included and will vary between different share

classes dependant upon their applicable charges. Returns to individual investors will vary in accordance with their personal tax

status and tax domicile.

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Jun-0

3

Aug

-03

Oct-

03

Jan-0

4

Mar-

04

May-0

4

Aug

-04

Oct-

04

Dec-0

4

Feb

-05

May-0

5

Jul-05

Sep

-05

Dec-0

5

Feb

-06

Ap

r-06

Jul-06

Sep

-06

No

v-0

6

Jan-0

7

Ap

r-07

Jun-0

7

Aug

-07

No

v-0

7

Jan-0

8

Mar-

08

Jun-0

8

Aug

-08

Oct-

08

Dec-0

8

Mar-

09

May-0

9

Jul-09

Oct-

09

Dec-0

9

Feb

-10

May-1

0

Jul-10

Sep

-10

No

v-1

0

Feb

-11

Ap

r-11

Jun-1

1

Sep

-11

No

v-1

1

Page 28 | CONFIDENTIAL

07717

Gold Shares7.2%

Cash and short dated

Government

Bonds12.5%

UK Index-Linked Government

bonds

3.9%

US Index-Linked Government

bonds

9.6%

Corporate Bonds7.8%

Norwegian Government

Bonds

10.7%

UK Equities34.6%

US Equities2.9%

European Equities

1.5%Japanese Equities

9.3%

Investec Cautious Managed Fund Asset allocation and holdings as at 30.11.11

Asset allocation

The portfolio may change significantly over a short period of time. This is not a buy or sell recommendation for any particular stock.

Data to 30.11.11. Source: Investec Asset Management

*Index is FTSE All Share.

\\mercury\gdrive\Depts\Marketing\Presentations\Hamilton Brown

Graphics\¬MASTER OEIC\MASTER Cautious Managed (Alastair

Mundy)\Evidence\Master_UK Cautious Managed

Top 10 equity holdings

(excl. gold shares)% of fund

GlaxoSmithKline 3.4

Signet Jewelers 3.2

Royal Dutch Shell 3.2

HSBC Holdings 2.7

Unilever 1.9

Kingspan 1.8

Travis Perkins 1.6

Grafton Group 1.4

UK Commercial Property Trust 1.4

AstraZeneca 1.3

Bond type Modified

Duration

Corporate 3.92

Index-Linked 7.73

Supporting Advisers

Page 30 | CONFIDENTIAL

07717

Adviser support & resources

Customise our website to suit you

Video and webcast updates

Adviser and end-investor sales aids,

manager updates and factsheets

Online Fund pages

Page 31 | CONFIDENTIAL

07717

Investec’s funds are available via leading platforms and life

companies

Page 32 | CONFIDENTIAL

07717

David Aird Managing Director,

UK Client Group

Investec Sales Team

Charles Wilson Sales Director

Page 33 | CONFIDENTIAL

07717

Important information

This communication is not for general public distribution. If you are a private investor and receive it as part of a general circulation, please

contact us at +44 (0)20 7597 1900.

The value of this investment, and any income generated from it, will be affected by changes in interest rates, general market conditions

and other political, social and economic developments, as well as by specific matters relating to the assets in which it invests. The Fund’s

investment objective will not necessarily be achieved and investors are not certain to make profits; losses may be made. All the

information contained in this communication is believed to be reliable but may be inaccurate or incomplete. Any opinions stated are

honestly held but are not guaranteed and should not be relied upon.

This is not a buy, sell or hold recommendation for any particular security. The portfolio may change significantly over a short period of

time.

This communication is provided for general information only. It is not an invitation to make an investment nor does it constitute an offer

for sale. The full documentation that should be considered before making an investment, including the prospectus and simplified

prospectus or offering memorandum, which set out the fund specific risks, is available from Investec Asset Management.

This communication should not be distributed to private customers who are resident in countries where the Fund is not registered for sale

or in any other circumstances where its distribution is not authorised or is unlawful. Please visit

www.investecassetmanagement.com/registrations to check registrations by country.

In the USA, this communication should only be read by institutional investors, professional financial advisers and, at their exclusive

discretion, their eligible clients, but must not be distributed to US Persons. THIS INVESTMENT IS NOT FOR SALE TO US PERSONS.

Telephone calls may be recorded for training and quality assurance purposes. Issued by Investec Asset Management Ltd (IAM),

January 2012. IAM is authorised and regulated by the Financial Services Authority.