investing in microfinance - university meets · pdf filesame results if conducting arima model...

TRANSCRIPT

University Meets Microfinance Workshop Microfinance in crisis? Impact and financial transparency

Frankfurt School of Finance & Management, July 19th - 20th

Ph.D Project Julia Meyer

Center for Microfinance

Investing in Microfinance Benchmarking Microfinance Investment Funds: Index Calculation

Outline

Research Questions

Background

Problem Outline

Empirical Approach

Index Calculation Methodologies

Results

Comparison to SMX and SRI / commercial Indices

2

Research Questions

How to benchmark MFIFs by one or more preferably homogeneous indices?

Might adding microfinance to a commercial portfolio lead to diversification effects?

3

Background: Investment in Microfinance - Growth

Increase in number of MIIs*

*Microfinance Investment Intermediaries (MIIs): MIVs, Holding Companies, Other MIIs, CGAP (2010)

MIV Asset Growth*

*US$ Mio.; Source: MicroRate 2011, 80 participating MIVs

*

4

4058

8090

23 25 29 34 40

61

35

35

31

32

0

20

40

60

80

100

120

140

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Survey Respondents All MIIs

1'195

1'964

3'864

4'931

6'0236'420

705

1'476

3'053

3'8144'246

4'749

0

1'000

2'000

3'000

4'000

5'000

6'000

7'000

2005 2006 2007 2008 2009 2010

Total MIV Assets (Mio. US$) Total MF Assets (Mio. US$)

Growth in MIIs and assets invested Increasing number of investors Transparency and disclosure

important

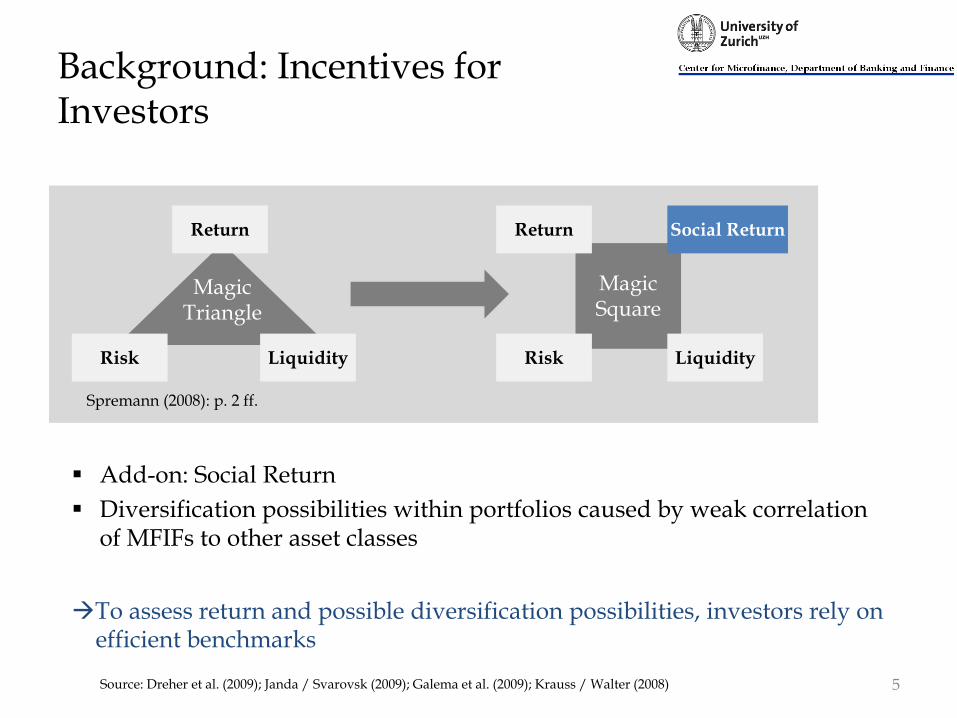

Add-on: Social Return

Diversification possibilities within portfolios caused by weak correlation of MFIFs to other asset classes

To assess return and possible diversification possibilities, investors rely on efficient benchmarks

Source: Dreher et al. (2009); Janda / Svarovsk (2009); Galema et al. (2009); Krauss / Walter (2008)

Background: Incentives for Investors

Return

Risk Liquidity

Magic Triangle

Magic Square

Liquidity Risk

Return Social Return

Spremann (2008): p. 2 ff.

5

Problem Outline

New market, not well established to date

No structured information available for investors

Missing benchmarks

Existing Index SMX: Symbiotics 2005

Index Debt (2-7 Funds)

Index Equity (5 MFIs)

SMX shows shortcomings

Only self-managed funds included

Limited picture of the market

Equal weighting of the funds

SMX might overestimate the performance of the microfinance universe

6

Empirical Approach – Data Situation

Current Situation:

Most MFIFs do not publicly disclose performance information

Data-bases and existing surveys include only few MFIFs and only provide yearly data

Even these yearly data are not easy to access

Elaboration of excel based survey and distribution to all MFIFs

7

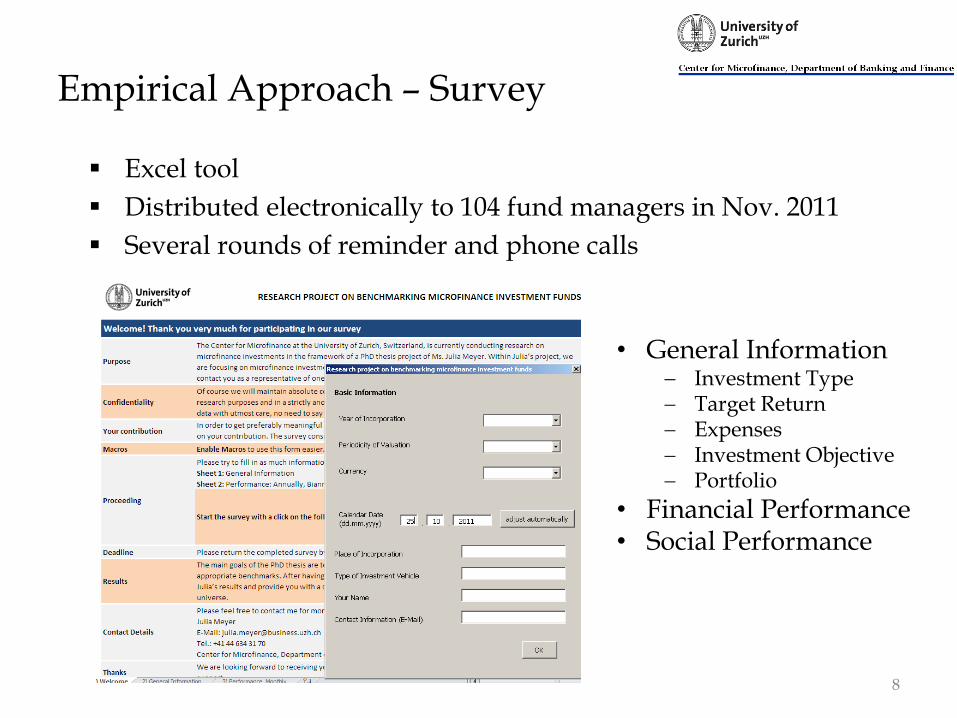

Empirical Approach – Survey

Excel tool

Distributed electronically to 104 fund managers in Nov. 2011

Several rounds of reminder and phone calls

• General Information Investment Type Target Return Expenses Investment Objective Portfolio

• Financial Performance • Social Performance

8

Empirical Approach – Feedback

9

Mostly comparable funds mainly invested in debt provide monthly performance data

Calculation of two debt indices: USD and EUR

Description Number of Funds

Surveys distributed 104

Responses 28 (27%)

Providing Performance Information 20

Performance on a monthly Basis 13

Data in USD 5

Data in EUR 8

Data from Bloomberg (USD) 1

Data from Bloomberg (EUR) 5

Total Funds for Index Calculation USD 6

Total Funds for Index Calculation EUR 13

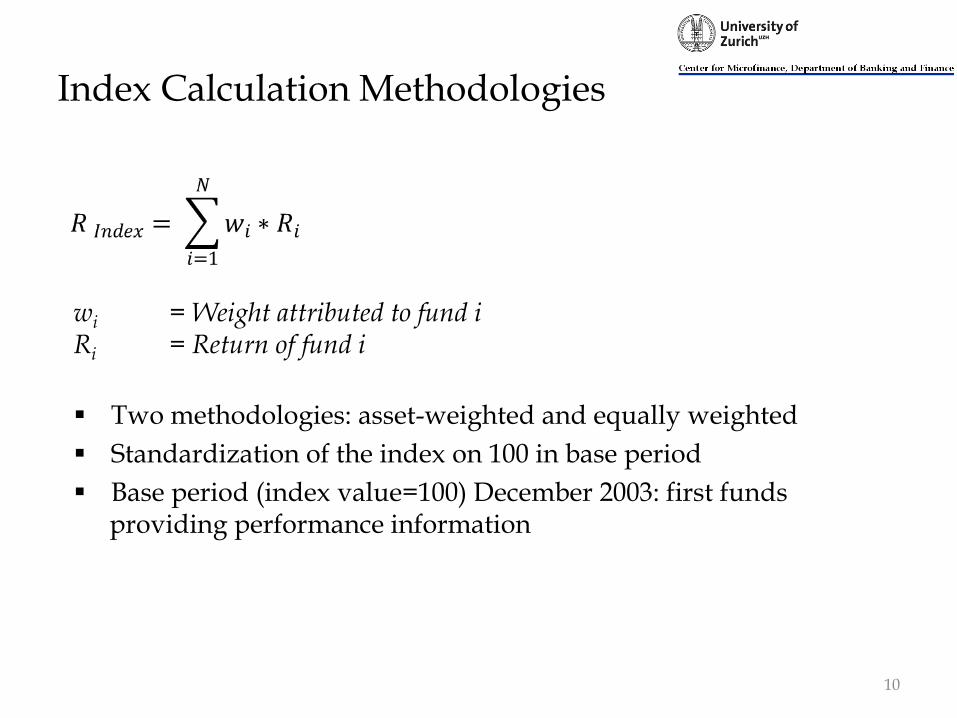

Index Calculation Methodologies

10

wi = Weight attributed to fund i Ri = Return of fund i

Two methodologies: asset-weighted and equally weighted

Standardization of the index on 100 in base period

Base period (index value=100) December 2003: first funds providing performance information

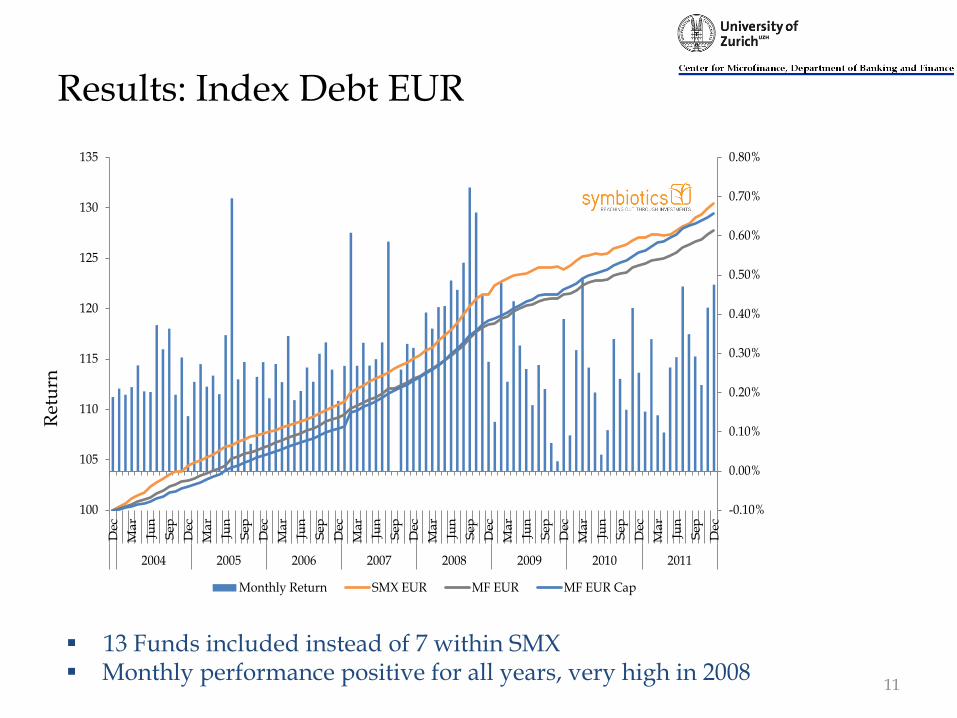

Results: Index Debt EUR

11

Ret

urn

13 Funds included instead of 7 within SMX Monthly performance positive for all years, very high in 2008

100

105

110

115

120

125

130

135

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

2004 2005 2006 2007 2008 2009 2010 2011

-0.10%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

Monthly Return SMX EUR MF EUR MF EUR Cap

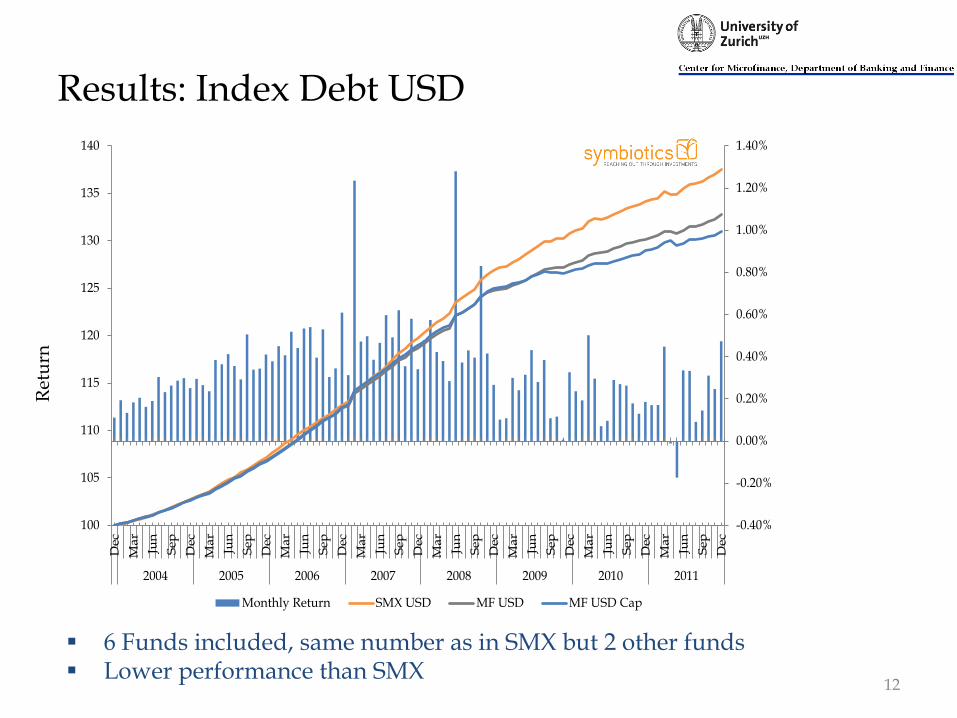

Results: Index Debt USD

12

Ret

urn

6 Funds included, same number as in SMX but 2 other funds Lower performance than SMX

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

100

105

110

115

120

125

130

135

140

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

Ma

r

Jun

Sep

Dec

2004 2005 2006 2007 2008 2009 2010 2011

Monthly Return SMX USD MF USD MF USD Cap

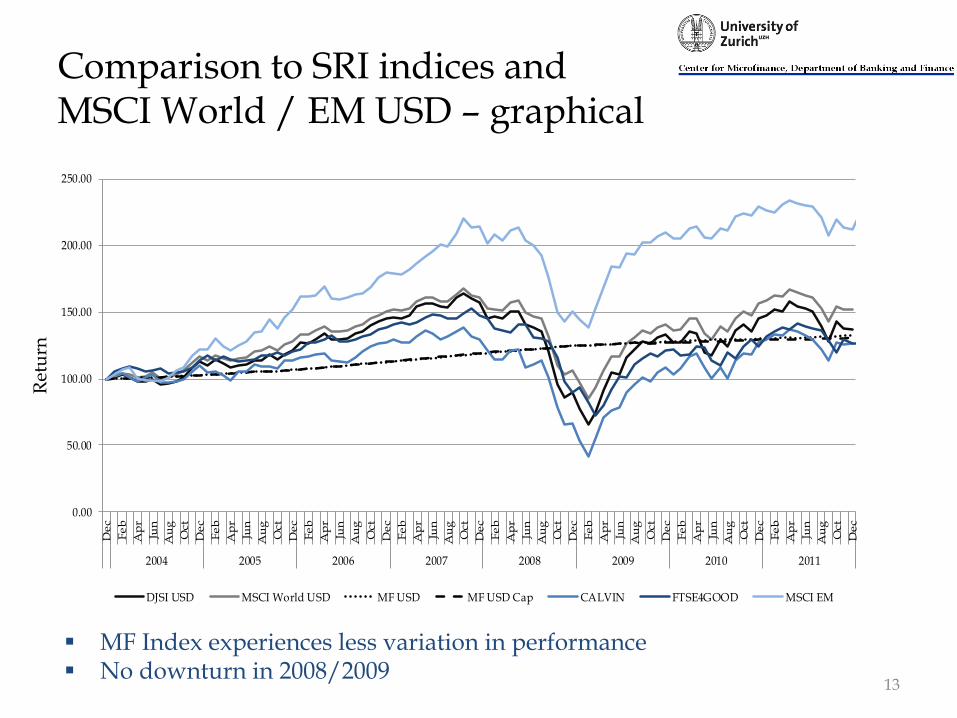

Comparison to SRI indices and MSCI World / EM USD – graphical

13

Ret

urn

0.00

50.00

100.00

150.00

200.00

250.00

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

2004 2005 2006 2007 2008 2009 2010 2011

DJSI USD MSCI World USD MF USD MF USD Cap CALVIN FTSE4GOOD MSCI EM

MF Index experiences less variation in performance No downturn in 2008/2009

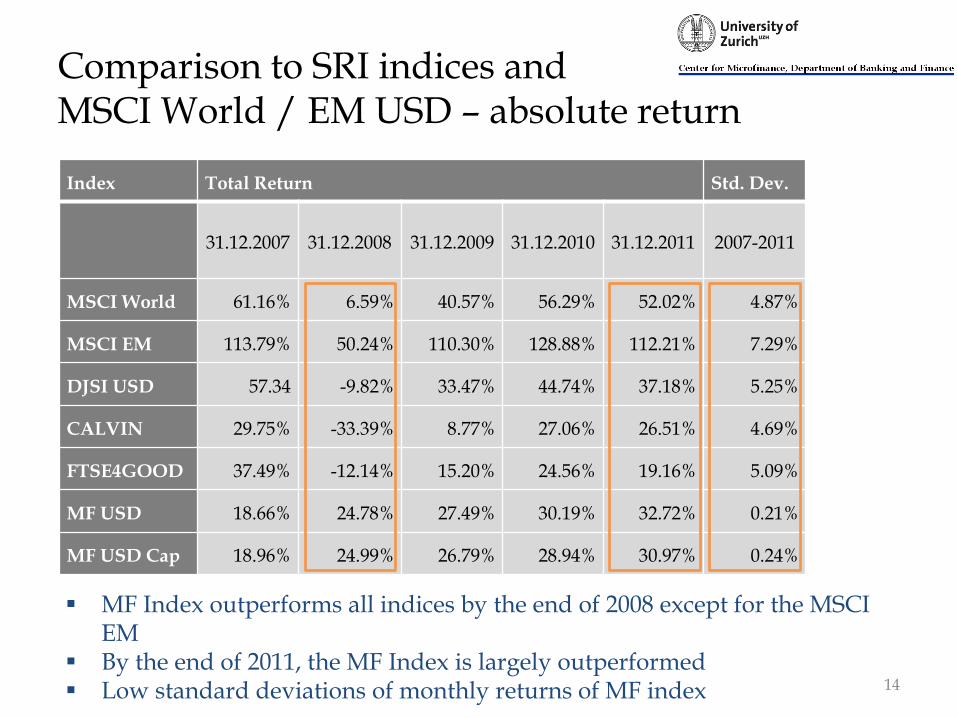

Comparison to SRI indices and MSCI World / EM USD – absolute return

Index Total Return Std. Dev.

31.12.2007 31.12.2008 31.12.2009 31.12.2010 31.12.2011 2007-2011

MSCI World 61.16% 6.59% 40.57% 56.29% 52.02% 4.87%

MSCI EM 113.79% 50.24% 110.30% 128.88% 112.21% 7.29%

DJSI USD 57.34 -9.82% 33.47% 44.74% 37.18% 5.25%

CALVIN 29.75% -33.39% 8.77% 27.06% 26.51% 4.69%

FTSE4GOOD 37.49% -12.14% 15.20% 24.56% 19.16% 5.09%

MF USD 18.66% 24.78% 27.49% 30.19% 32.72% 0.21%

MF USD Cap 18.96% 24.99% 26.79% 28.94% 30.97% 0.24%

14

MF Index outperforms all indices by the end of 2008 except for the MSCI EM

By the end of 2011, the MF Index is largely outperformed Low standard deviations of monthly returns of MF index

Equity index (SMX Equity)

15

0

50

100

150

200

250

De

c

Jan

Fe

b

Mar

Ap

r

May Jun

Jul

Au

g

Sep Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r

May Jun

Jul

Au

g

Sep Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r

May Jun

Jul

Au

g

Sep Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r

May Jun

Jul

Au

g

Sep Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r

May Jun

Jul

Au

g

Sep Oct

No

v

De

c

2007 2008 2009 2010 2011

USD Equity SMX DJSI USD MSCI World USD CALVIN FTSE4GOOD MSCI EM

Ret

urn

Different picture for equity index Seems to perform similar to other indices but clearly outperforms all of them Most probably overstates the performance of MF equity funds by only

accounting for five publicly listed MFIs (Brière/Szafarz, 2011)

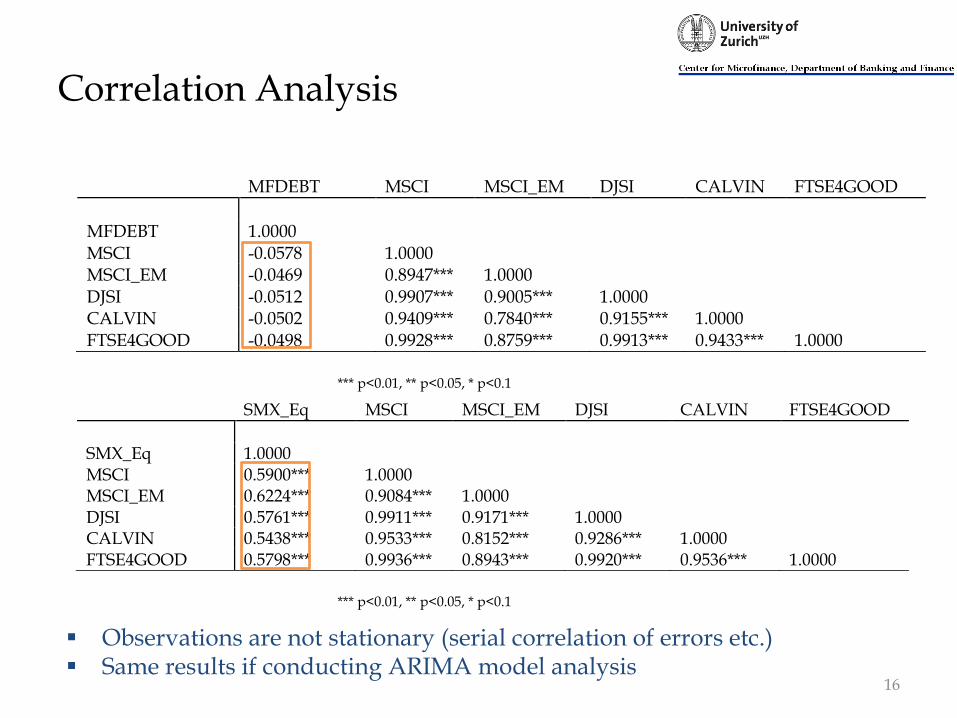

Correlation Analysis

16

SMX_Eq MSCI MSCI_EM DJSI CALVIN FTSE4GOOD

SMX_Eq 1.0000 MSCI 0.5900*** 1.0000 MSCI_EM 0.6224*** 0.9084*** 1.0000 DJSI 0.5761*** 0.9911*** 0.9171*** 1.0000 CALVIN 0.5438*** 0.9533*** 0.8152*** 0.9286*** 1.0000 FTSE4GOOD 0.5798*** 0.9936*** 0.8943*** 0.9920*** 0.9536*** 1.0000

MFDEBT MSCI MSCI_EM DJSI CALVIN FTSE4GOOD

MFDEBT 1.0000 MSCI -0.0578 1.0000 MSCI_EM -0.0469 0.8947*** 1.0000 DJSI -0.0512 0.9907*** 0.9005*** 1.0000 CALVIN -0.0502 0.9409*** 0.7840*** 0.9155*** 1.0000 FTSE4GOOD -0.0498 0.9928*** 0.8759*** 0.9913*** 0.9433*** 1.0000

*** p<0.01, ** p<0.05, * p<0.1

*** p<0.01, ** p<0.05, * p<0.1

Observations are not stationary (serial correlation of errors etc.) Same results if conducting ARIMA model analysis

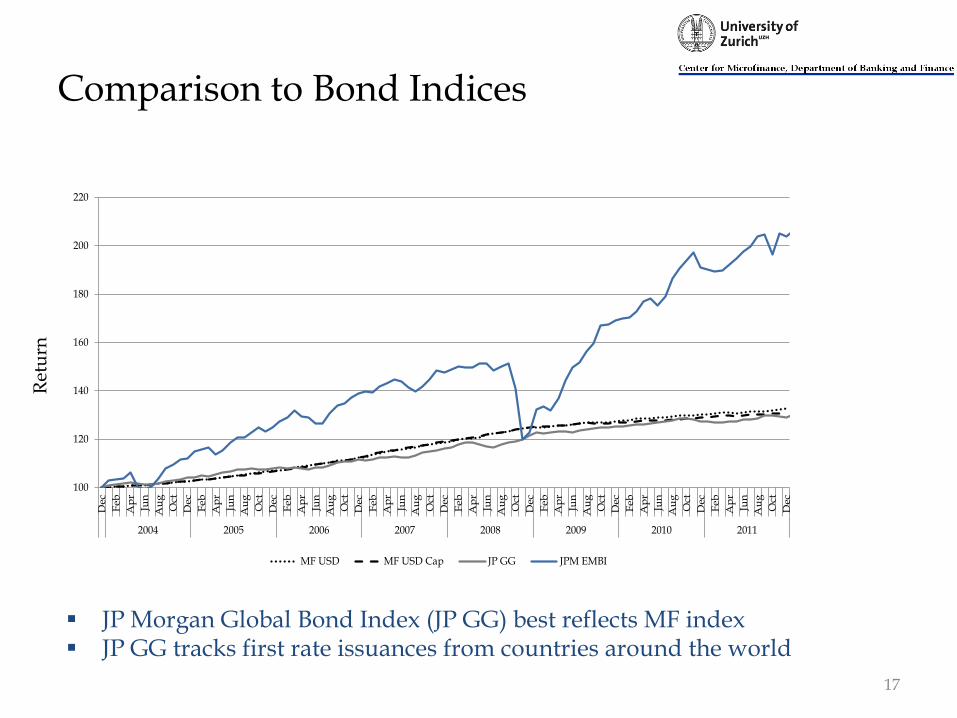

Comparison to Bond Indices

17

100

120

140

160

180

200

220

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

Feb

Ap

r

Jun

Au

g

Oct

Dec

2004 2005 2006 2007 2008 2009 2010 2011

MF USD MF USD Cap JP GG JPM EMBI

Ret

urn

JP Morgan Global Bond Index (JP GG) best reflects MF index JP GG tracks first rate issuances from countries around the world

Conclusions

• Funds providing performance information are all rather comparable debt funds

• Index shows lower performance than SMX, especially USD

• SMX seems to overestimate microfinance return with only analyzing own managed funds

• Asset weighted or equally weighted: no big difference between large and small funds regarding performance

• Large differences between debt MF index and SRI / commercial indices indication for diversification possibilities

• Equity investments more correlated to SRI / commercial indices

• JP GG best reflecting MF index

18

Appendix

19

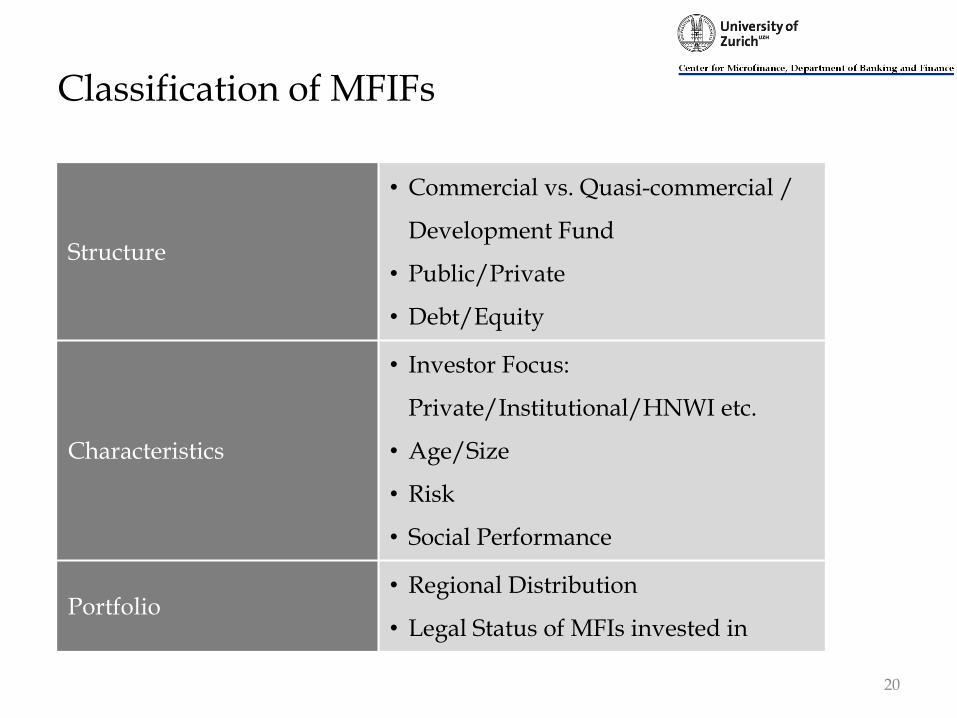

Classification of MFIFs

Structure

• Commercial vs. Quasi-commercial /

Development Fund

• Public/Private

• Debt/Equity

Characteristics

• Investor Focus:

Private/Institutional/HNWI etc.

• Age/Size

• Risk

• Social Performance

Portfolio • Regional Distribution

• Legal Status of MFIs invested in

20

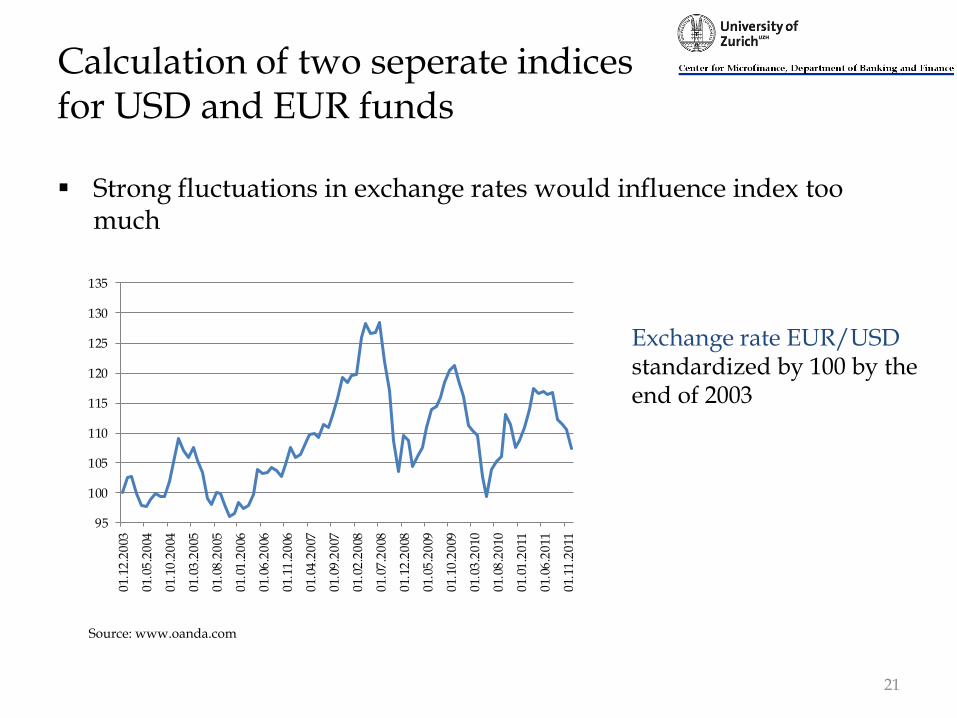

Calculation of two seperate indices for USD and EUR funds

Strong fluctuations in exchange rates would influence index too much

21

95

100

105

110

115

120

125

130

135

01.

12.2

003

01.

05.2

004

01.

10.2

004

01.

03.2

005

01.

08.2

005

01.

01.2

006

01.

06.2

006

01.

11.2

006

01.

04.2

007

01.

09.2

007

01.

02.2

008

01.

07.2

008

01.

12.2

008

01.

05.2

009

01.

10.2

009

01.

03.2

010

01.

08.2

010

01.

01.2

011

01.

06.2

011

01.

11.2

011

Exchange rate EUR/USD standardized by 100 by the end of 2003

Source: www.oanda.com

Comparison to SRI indices and MSCI World / EM EUR

22

0

20

40

60

80

100

120

140

160

180

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

Fe

b

Ap

r

Jun

Au

g

Oct

De

c

2004 2005 2006 2007 2008 2009 2010 2011

DJSI EUR MSCI World EUR MF EUR MF EUR Cap ING Socially Responsible