investing in spain a guide for chinese businesses -...

TRANSCRIPT

Investing in SpainA guide for Chinese BusinessesIn collaboration with the Chinese Embassy in Spain

A journey of ten thousand miles begins with just one step

Chinese proverb

Investing in Spain - A guide for Chinese Businesses 3

Contents

Letter of Endorsements 8

Chinese Embassy in Spain 8

ICBC 9

Foreword 10

1. Introduction to Spain 11

1.1. Location 11

1.2. Population and language 11

1.3. Government 12

1.4. Business environment 12

1.5. Financial centre 12

1.6. Benefits to business 13

1.7. Currency 13

1.8. Foreign investment 14

1.9. Operating costs 14

2. Spain – China economic and trade relations 16

2.1. Institutional framework 16

2.2. Commercial exchange 17

2.3. Trends and future development 19

3. Chinese investment into Spain 20

3.1. Chinese overview 20

3.2. The appeal of Spain 21

3.3. Deal rationale 22

Investing in Spain - A guide for Chinese Businesses 4

4. Main business structures 23

4.1. The incorporated company 23

4.2. Branch or representative office of an incorporated foreign company 31

4.3. Business regulation 36

4.3.1. Reorganisation process: national and international mergers and acquisitions 36

4.3.2. Foreign investments in Spain 41

5. Corporate Governance 44

5.1. Overview 44

5.2. Appliance and compliance 44

6. Accounting and auditing 46

6.1. Overview 46

6.2. Reporting requirements 46

6.3. Accounting principles and standards 48

6.4. Audit requirements and standards 48

6.5. Frequently asked questions 49

7. Taxation 51

7.1. Overview of Spanish taxation 52

7.2. Principal direct taxes 52

7.2.1. Corporate income tax 52

7.2.2. Personal income tax 63

7.2.3. Non-resident income tax 66

7.2.4. Inheritance and gift tax 68

Investing in Spain - A guide for Chinese Businesses 5

7.3. Principal indirect taxes 68

7.3.1. VAT 68

7.3.2. Transfer tax 69

7.3.3. Capital duty 70

7.3.4. Stamp tax 70

7.3.5. Property tax 70

7.3.6. Customs and excise duties 70

7.3.7. Tax on certain means of transport 71

7.3.8. Other taxes 72

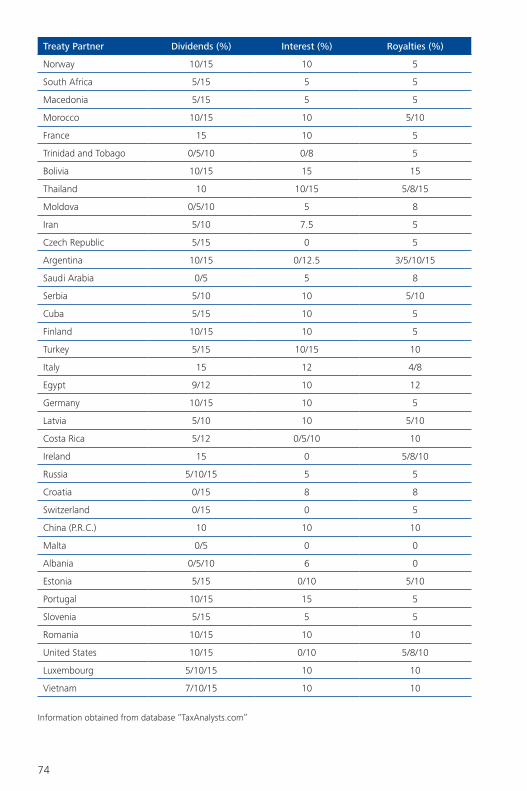

7.4. Avoidance of double taxation 72

7.4.1. Foreign tax credits/ Exempt income 72

7.4.2. Tax treaties 72

7.4.3. Republic of China – Spain tax treaty 75

7.4.4. Hong Kong – Spain tax treaty 76

8. Labour environment 76

8.1. Overview 76

8.2. Employment of foreigners 77

8.3. Employment and remuneration 77

8.4. Social Security and benefits 78

8.5. Termination of employment 78

9. Banking sector in Spain 79

9.1. Entering the Spanish banking market 79

9.1.1. Formalities for setting up a bank in Spain 79

Investing in Spain - A guide for Chinese Businesses 6

9.1.2. Branch of an EU bank in Spain 80

9.1.3. Branch of a foreign non EU bank in Spain 80

9.2. Regulation of the banking Business 80

9.2.1. Spanish supervisory authorities 80

9.2.2. Mergers and acquisitions of Spanish banks 80

9.3. Corporate income tax 81

9.3.1. Attribution of profits 81

9.3.2. Minimum amount of “free” capital for Spanish tax purposes 81

9.3.3. Specific tax computation considerations for branches of Chinese banks 82

9.4. VAT 84

9.4.1. Output VAT: the VAT exemption on financial services 84

9.4.2. Input VAT recovery 84

9.5. Withholding taxes 86

9.5.1. Withholding tax on interest income 86

9.5.2. Withholding tax on interest payments 86

9.6. Reporting obligations 87

9.7. Leasing and asset finance 87

9.7.1. Legal requirements 87

9.7.2. Types of leases recognised (by law) 88

9.7.3. Finance leases 88

9.7.4. Financial regulations / supervisory requirements 89

9.7.5. Regulatory requirements for lease transactions 89

Investing in Spain - A guide for Chinese Businesses 7

10. Institutional framework for attracting foreign investment to Spain 90

10.1. Spanish Government Institutions 90

10.2. Support framework in regions and relevant cities 91

10.3. Grants and subsidies to attract foreign investment 96

Appendix 101

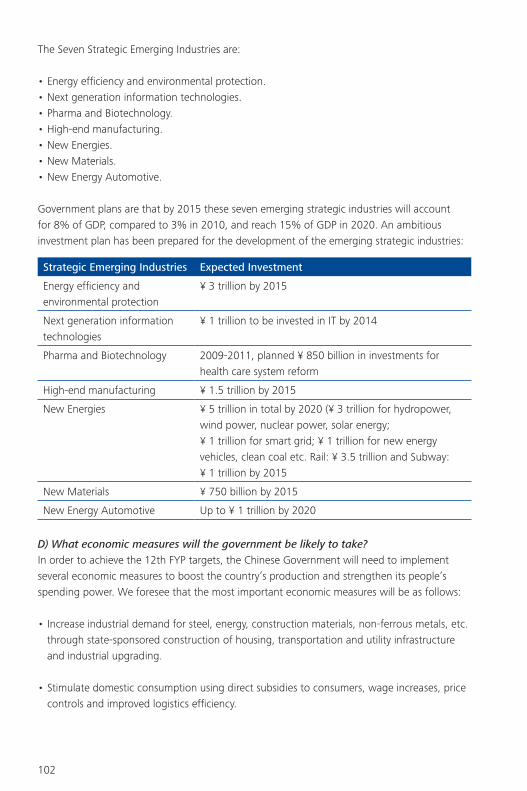

I. China’s 12th Five Year Plan 101

A) Introduction 101

B) Strategic Priorities of the 12th FYP 101

C) Strategic Emerging Industries Plan 101

D) What economic measures will the government be likely to take? 102

E) Major issues and implications 103

II. How Can ICBC Help? 105

III. How can Deloitte help? 109

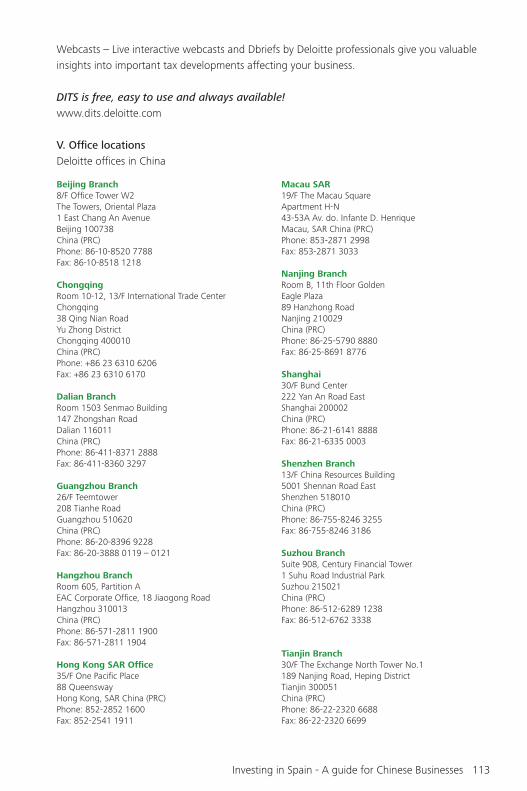

IV. Deloitte International Tax Source 114

V. Office locations 115

VI. Deloitte team involved in this edition 118

8

Letter of Endorsements

China established the diplomatic ties with Spain in 1973 and upgraded the relations to comprehensive strategic partnership in 2005. In recent years, both countries have joined hands together to meet the financial crisis, which helped increase political mutual trust, expand cooperation in fields like culture and education and bring economic & trade relations into a spotlight for both societies.

In 2010, the growth in Spain’s exports to China surpassed that in its imports from China and the bilateral trade amounted to US$ 24.4 billion. Spain and China have become each other's most important trading partner, and the bilateral goods trade, in particular, has reached a relatively mature stage of development. The number of Chinese tourists to Spain is expected to total 300,000 in 2013.

As more and more commodities and people go global, the pace of international allocation of China’s capital speeds up as well. In 2010, China reported nearly US$ 60 billion of outward investment in non-financial sectors, one of the hugest among the developing countries. In the future, China’s inward investment and outward investment will tend to be more balanced and China will soon become a global investment giant.

Spain is among the most developed countries of the world. With close ties with EU and Latin America markets, it boasts a high degree of market openness, advanced infrastructures and complete investment promotion systems, thus being an investment destination which the Chinese businesses cannot ignore. China’s aggregate investment in Spain is not huge at present, but the operation is generally good and well on a stage featuring accelerated rise. Either investing in Spain or jointly carrying out global strategic cooperation with Spanish businesses is of great significance to the sustainable development of both economies.

The Chinese government encourages businesses to earnestly study and actively adapt to local investment environment, observe laws and rules, follow local customs and merge into local society. Mutual understanding is the first step for future cooperation. Therefore, we hope the cooperative publishing of the guide for investing in Spain can play a positive role in promoting the investment by Chinese businesses in Spain.

Zhu Bangzao Ambassador of the People´s Republic of China in Spain

Investing in Spain - A guide for Chinese Businesses 9

‘Going Global’ has become a strategically important policy for China to deepen its opening up and proactively participate to international economic cooperation. With greater exposure to the world economy, China has built up enormous overseas economic interest with vast of enterprises and overseas Chinese around the globe. The huge needs for financial service of overseas Chinese enterprises and individuals have laid a solid foundation for Chinese banks to follow their globalized customers to provide support worldwide.

ICBC has been playing an active role in support of Chinese enterprises going globalization in recent years. By the end of 2010, ICBC had 203 overseas branches and subsidiaries in 28 countries and regions, thus the global financial service network covering Asia, Europe, Africa, America and Australia has been basically established. ICBC has contributed to so many aspects of overseas Chinese enterprises daily operations such as financing, merge and acquisition, capital raising and wealth management, that has greatly propelled our clients´ business booming.

Spain is one of the major destination countries for foreign direct investment. The recent years have seen a remarkable increase of Chinese investment flow into Spain. The establishment of ICBC´s new branch in Madrid is the most recent highlight of the achievement of Sino-Spanish economic cooperation and development. ICBC becomes the first Chinese bank to set its footprint in Spain, a meaningful move for the Chinese enterprises exploring the Spanish market. We strive to provide excellent financial services to Chinese and Spanish customers and aim to be a financial bridge between China and Spain to boost bilateral economic and trade relationship.

As such, we feel really honored to have the chance of being part of the editor team of this Investment Guide in Spain. I hope this book will be a useful tool for Chinese enterprises to better understand the investment environment of Spain. ICBC Spanish Branch will always be ready to partner our customers to make contribution to the enhancement of economic relationship between China and Spain.

Liu GangGeneral Manager of ICBC Spain Branch

10

It is an honour for me to introduce the first edition of the Investing in Spain guide. This guide couldn’t come at a better time, at a moment when Spain has been declared as China’s best friend in Europe; Spain - China economic relations are getting stronger by the day, and Chinese investment into Spain is growing faster than ever.

China is already Spain’s principal commercial partner from outside the European Union. Spain’s imports from China have more than quadrupled in the last ten years and our exports are also growing at healthy rates. Furthermore, all signs point to the fact that this relationship will continue to grow in the future. The number of Chinese companies in Spain is steadily increasing, and the setting up of the first Chinese financial institutions will make Spain an even more attractive destination for them.

As we can see in the 12th Five Year Plan approved in March 2011, it is clear that China’s Government will continue to push for a rapid development of the country. Economic growth targets are set to continue at high single digits during the 2011-2015 period. The main driver of this outstanding growth will be an increase in private consumption. According to the 12th FYP, China’s development model will undergo major change from an exports driven economy to a consumption driven one. Domestic demand will grow faster than the economy, and its contribution to China’s GDP will also increase significantly.

In order to achieve these targets, China’s consumption of natural resources from abroad will continue to increase, and the import to China of western brands and technologies will rise dramatically, as Chinese companies use them to satisfy their customers’ needs. In this context, Spain will strengthen its position as a benchmark destination for Chinese investors.

Deloitte and its Chinese Services Group (CSG) are committed to developing long-term partnerships with the Chinese business community and to support the entrance of Chinese companies in Spain. We are convinced there are considerable opportunities to strengthen our mutual trade and investment relationships, and will do our utmost to promote them. Our professionals, with extensive experience and knowledge of the Spanish market, are in a unique position to help any Chinese investors understand the Spanish market and bridge any cultural gap that would otherwise pose a major challenge for them. The CSG, at all times in cooperation with the China firm, serves as the unifying force to market, facilitate and deliver Deloitte professional services to our Chinese clients in Spain.

Both China and Spain have much to offer each other. I hope this guide, coordinated and tailored for Chinese investors, with the full support of the Chinese Embassy in Spain and ICBC, will become the tool of reference when targeting Spain. I am confident it will help you make the right choices when deciding whether to invest in Spain and it will be a pleasure for me to offer you all our help when doing business in Spain.

Fernando RuizCEO of Deloitte Spain

Foreword

Investing in Spain - A guide for Chinese Businesses 11

1. Introduction to Spain1.1. LocationSpain is one of the fifty largest countries in the world, with an area of 505,955 square kilometres.

Most of its territory is the Iberian Peninsula, while the rest is composed of the Balearics and the Canary Islands plus the cities of Ceuta and Melilla -situated on the coast of Africa.

Because of its privileged geographical situation -the Iberian Peninsula is located in the extreme south west of Europe and only 14 kilometres away from Africa- Spain has great strategic value: it acts as a bridge between the Mediterranean on one side and Africa and America on the other. The Spanish coastline runs along the Mediterranean Sea and the Atlantic Ocean.

The climate in the different parts of Spain can vary greatly:

•In the North, the weather is temperate. Often with little change from summer to winter, and rain is common year round.

•The Centre is characterised by hot summers and cold winters. In this area it does not rain very often, but when it does, it rains heavily.

•In southern Spain, the summers are hot and winters range from cool to cold.

1.2. Population and languageIn 2011 the Spanish population is estimated to stand at around 47 million, some 5.7 million of whom are foreign residents.

The population of Spain is concentrated mainly in large cities.

Madrid, the capital city of Spain, has more than 3 million inhabitants -more than 6 million if we take into account the outlying area. Barcelona, with an official population of 1.6 million, is the second largest city in Spain. They are followed by Valencia (809,267 inhabitants), Seville (704,198 inhabitants), Zaragoza (675,121 inhabitants), Malaga (568,507 inhabitants) and Bilbao (353,187 inhabitants).

The official language of Spain is Castilian Spanish. However, Spanish is not the only language spoken in Spain. There are many other officially-recognised languages in the following Autonomous Communities: Catalonia, Galicia, the Basque Country, Valencia and the Balearic Islands.

12

1.3. GovernmentSpain’s political regime is a constitutional monarchy, with a hereditary monarch and a parliament based on a two-House system. The maximum institution is the Spanish Crown. Juan Carlos I is both the King and the Head of State. He is in charge of moderating the regular functioning of the institutions, as well as being the highest representative of the Spanish state in international relations.

The Spanish Constitution is the legal framework of the political organisation of the Spanish nation. According to the Constitution, the powers of the state are separated into three branches: legislative, executive and judicial. Legislative power is held by parliament, while executive power is represented by the government. The head of the government is proposed by the King and elected after the renewal of parliament.

Spain is divided into provinces and into other larger units –the Autonomous Communities. There are 17 Autonomous Communities: Andalusia, Aragon, Asturias, the Balearic Islands, the Canary Islands, Cantabria, Castilla-León, Castilla-La Mancha, Catalonia, Extremadura, Galicia, Madrid, Murcia, Navarre, Basque Country, La Rioja and Valencia. There are also two cities –Ceuta and Melilla– each with a Statute of Autonomy. Each Autonomous Community has its own parliament and regional government.

The Constitutional Court must safeguard the constitutionality of the laws and resolves any conflict arising between the Autonomous Communities and the state.

Spain is a democracy based on the supreme values of its legal system which are the concepts of freedom, justice, equality and political pluralism.

1.4. Business environmentSpain is an EU member state and a member of the OECD.

Spain is a large economy and a popular destination for foreign investment. The services sector dominates the economy, with retail, tourism, banking and telecommunications accounting for a significant proportion of economic activity. The tourism industry is particularly important and Spain is one of the most popular tourist destinations in the world. The most prominent manufacturing industry is vehicle production. The bulk of Spanish trade is with the EU, although trade with Latin America and Asia has grown in recent years.

1.5. Financial centreThe city of Madrid is considered to be the financial centre of Spain. In this regard, the two largest banks in Spain –Santander and BBVA- have established their headquarters in Madrid.

The prestigious business schools Instituto de Empresa and IESE are also located in Madrid.

Investing in Spain - A guide for Chinese Businesses 13

The regulation and supervision of the Bank of Spain safeguards the soundness of the Spanish banking system. This system has been acknowledged by news agencies such as the Dow Jones International News, multilateral institutions such as the European Central Bank and other central banks like the Bank of England.

The Spanish stock index is a leader in contracted fixed-income products and has been growing at a rate far above the international average.

1.6. Benefits to businessCurrently, Spain is one of the most internationally-oriented countries in the world. With regard to the trading of goods, Spain is ranked 16th in the world as an exporter and 13th as an importer; while in the trading of services it occupies 7th place as an exporter and 9th place as an importer (WTO “International Trade Statistics 2010” report.)

Spain’s human and technological resources make it a very attractive country for the international business community. Spain has a highly developed infrastructure network and it is very well communicated by road, train –highly developed network of high-speed trains: AVE-, air - two of the biggest airports in Europe- and sea.

The Spanish market is one of the biggest in Europe with 47 million consumers and spending power above the European average.

As a member of the EU, Spain is directly connected to the members of the European Union.

Spain has the highest number of double taxation and investment protection agreements signed with Latin America. Moreover, many Spanish companies are leaders in the Latin American markets.

Because of its geographical proximity to North Africa, Spain is an important connection point between Europe and the African market.

The Spanish language is also a key factor as there are currently more than 450 million Spanish speakers and it is the official language of 22 countries.

1.7. CurrencyAs Spain is a member of the European Union, its official currency has been the euro since 2002.

14

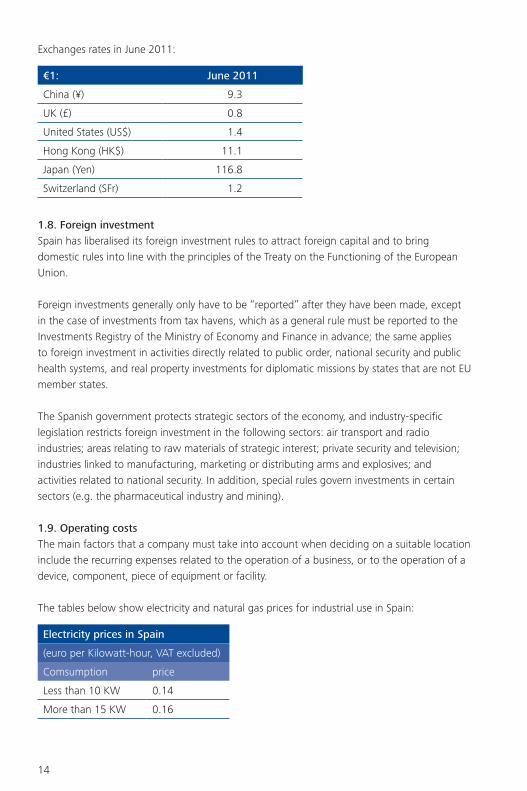

Exchanges rates in June 2011:

€1: June 2011

China (¥) 9.3

UK (£) 0.8

United States (US$) 1.4

Hong Kong (HK$) 11.1

Japan (Yen) 116.8

Switzerland (SFr) 1.2

1.8. Foreign investmentSpain has liberalised its foreign investment rules to attract foreign capital and to bring domestic rules into line with the principles of the Treaty on the Functioning of the European Union.

Foreign investments generally only have to be “reported” after they have been made, except in the case of investments from tax havens, which as a general rule must be reported to the Investments Registry of the Ministry of Economy and Finance in advance; the same applies to foreign investment in activities directly related to public order, national security and public health systems, and real property investments for diplomatic missions by states that are not EU member states.

The Spanish government protects strategic sectors of the economy, and industry-specific legislation restricts foreign investment in the following sectors: air transport and radio industries; areas relating to raw materials of strategic interest; private security and television; industries linked to manufacturing, marketing or distributing arms and explosives; and activities related to national security. In addition, special rules govern investments in certain sectors (e.g. the pharmaceutical industry and mining).

1.9. Operating costsThe main factors that a company must take into account when deciding on a suitable location include the recurring expenses related to the operation of a business, or to the operation of a device, component, piece of equipment or facility.

The tables below show electricity and natural gas prices for industrial use in Spain:

Electricity prices in Spain

(euro per Kilowatt-hour, VAT excluded)

Comsumption price

Less than 10 KW 0.14

More than 15 KW 0.16

Investing in Spain - A guide for Chinese Businesses 15

On the other hand, the price of water depends on variables such as the consumption or the season. In this regard, the price in Madrid for 2011 varies between €0.38 /m3 and €1.39 /m3.

Another major cost that must be analysed is that relating to the rental of office space that a business occupies. It is important to stress that rentals in Spain vary notably depending on the region. In this regard, the following figure shows the average price for 2010 depending on the area of Madrid (as a reference of a first tier city):

Natural gas prices in Spain

(euro per Kilowatt-year, VAT excluded)

Comsumption price

5,000 KWh or less 0.14

5,000 KWh-50,000 KWh 0.16

50,000 KWh-100,000 KWh 0.39

More than 100,000 KWh 0.36

70

370

270

170

€/m2/YearMax Avg Min

CBDCity centrer

Periphery

No city centrer

Source: BNP Paribas Real Estate Research

16

2. Spain – China economic and trade relations2.1. Institutional frameworkIn the modern era, diplomatic relations were established by both the Chinese and Spanish Governments in 1973.

Furthermore, a few years ago –in 2005-, the two economies decided to embark on a new project in which they would become strategic partners and provide mutual aid through the signing of the Strategic Association Agreement. For the purpose of clarification, said agreement recognised the ongoing commercial relationship established between China and Spain under the same conditions that others, such as France, the UK and Germany, also enjoyed at that time.

Institutional relations have been notably strengthened in recent years. To mark the recent opening ceremony of Expo Shanghai 2010, numerous dignitaries such as the Minister of Industry, Tourism and Trade, the Director General of the Public Treasury, the Prime Minister and others had the opportunity to visit China. In addition, Spain was visited by the Deputy Minister of the Chinese National Committee for Development and Reforms (NDRC), the main economic advisor to the Prime Minister, Zhu Zhixin, the deputy minister for trade, Zhong Shan, the Deputy Minister of the Ministry for Railways, An Limin, and the Deputy Chairman of the CCPIT, Zhang Wei (in a ceremony with the Spanish Employers Confederation -CEOE-, its Spanish counterpart).

Recently, in 2011 the Spanish Prime Minister along with the Ministry of Industry, Tourism and Trade and the State Secretary for the Economy visited China. Furthermore, in January 2011 the deputy Prime Minister Li Keqiang visited Spain.

Among the most significant projects and agreements recently signed between both nations, the following should be mentioned:•Economic and industrial cooperation treaty (1984).•Scientific and technical cooperation agreement (signed 1985).•Double tax treaty (in force since 1992).•Mutual investment protection and promotion agreement (in force since 2008).

Investing in Spain - A guide for Chinese Businesses 17

2.2. Commercial exchangeSpanish exportsThe total volume of Spanish exports to China in 2009 amounted to nearly €2,000 M whereas those registered in 2010, amounted to €2,650 M –a rate of growth of 33.13%.

The total volume of exports in 2010 related mainly to the sale of:•Raw materials and semi-finished plastic products (10.46%)•Automotive accessories (9.49%)•Steel products (4.48%)

The data for 2009 and 2010 is as follows:

Main Spanish Export Products(millon Euros)

2009 2010 Growth

Amount % Amount % %

Raw materials and semi-finished plastic products 231.87 11.67% 277.11 10.46% 19.51%

Automotive equipment, components and accesories 102.33 5.15% 251.25 9.49% 145.53%

Iron and steel products 114.00 5.74% 118.72 4.48% 4.14%

Pharmachemicals products 80.27 4.04% 102.62 3.88% 27.85%

Organic chemicals 115.60 5.82% 102.41 3.87% -11.41%

Marble and related goods for construction 59.99 3.02% 87.60 3.31% 46.01%

Copper and its alloys 60.00 3.02% 86.51 3.27% 44.19%

Semi-finished copper products and the related alloys 33.98 1.71% 84.53 3.19% 148.78%

Metal and non-metal ores (except copper and zinc) 63.86 3.22% 71.59 2.70% 12.11%

Raw and tanned hide and leather 43.15 2.17% 71.47 2.70% 65.63%

Source: Spanish Customs Authorities

Spanish ImportsThe total volume of Spanish imports from China in 2009 amounted to nearly €14,500 M whereas those registered in 2010, amounted to €18,870 M –a rate of growth of 33.13%.

The total volume of imports in 2010 related mainly to the purchase of:•Women’sclothing(10.22%)•Computerhardware(8.25%)•Telecomparts&equipment(5.88%)•Electronicdevices(4.51%)

18

The data for 2009 and 2010 are as follows:

Main Spanish Export Products(millon Euros)

2009 2010 Growth

Amount % Amount % %

Women´s clothing 1,688.16 11.68% 1,927.48 10.22% 14.18%

Computer hardware 964.99 6.67% 1,557.14 8.25% 61.36%

Telecomunications equipment 926.87 6.41% 1,108.45 5.88% 19.59%

Electronic parts 484.93 3.35% 851.76 4.51% 75.65%

Footwear 569.98 3.94% 764.40 4.05% 34.11%

Organic chemicals 430.01 2.97% 556.54 2.95% 29.42%

Men´s clothing 506.74 3.51% 553.53 2.93% 9.23%

Iron and steel products 357.00 2.47% 537.14 2.85% 50.46%

Toys 402.26 2.78% 505.23 2.68% 25.60%

Leathers goods 381.41 2.64% 492.36 2.61% 29.09%

Source: Spanish Customs Authorities

Evolution of Spain’s balance of trade Spain’s balance of trade is usually marked by severe deficits due to the low volume of Spanish exports entering the Chinese market. However, it has been observed that Spanish sales have begun to increase slightly over the last two years.

In fact, in 2010 the Spanish trade deficit reached €16,219 M. Also, the foreign trade coverage rate has improved to the extent that in 2010 it reached 14% pointing to greater growth in the volume of exports than in imports.

Foreign capital companies represent half of Chinese imports, with approximately one third of the imports relating to the manufacturing trade. Foreign direct investment (FDI) in China constitutes the main source of Chinese imports.

In principal, it could be argued that the current weak level of industrial placement and positioning of Spanish companies in the Chinese economy could have a significant impact on the access of Spanish exports, together with other factors such as access barriers and the profile of the Spanish export companies.

Investing in Spain - A guide for Chinese Businesses 19

The data for 2008, 2009 and 2010 are as follows:

Main Spanish Export Products(millon Euros)

2008 2009 2010

Amount % Amount % Amount %

Spanish Exports 2,152.60 1.2% 1,989.40 -7.6% 2,648.09 33.1%

Spanish Imports 20,492.60 10.8% 14,454.20 29.5% 18,867.09 30.5%

Trade Balance 18,339.80 12.1% 12,464.90 32.0% 16,219.02 30.1%

Trade Coverage Rate 10.5% - 13.8% - 14.0%

Source: Compiled by Deloitte Spain based on previous charts.

Chinese investment in Spain may appear to be still relatively low and although certain Chinese corporations, such as ICBC bank (since January 2011), HNA (which acquired 20% of NH Hoteles in May of this year), CITIC, ZTE, Huawei and Air China all have a presence in Spain, it has yet to become a significant destination for outward Foreign Direct Investment ("FDI") in comparison with other large economies located in the European Union.

In 2007, Chinese investment in Spain surpassed €2.15 M but in 2008 it dropped significantly to €1.05 M. Although the highest level of investment (€2.76 M) was recorded in 2009, it subsequently fell to €2.2 M in 2010.

2.3. Trends and future developmentSeveral wealthy Chinese territories have recently been faced with a decrease in their competitive advantage based on low salaries. Rich areas have witnessed a significant degree of relocation of labour-intensive and consumer-goods industries (toys, clothing, footwear. etc.) to other Asian economies. As a consequence, the former competitive pressure exerted by these territories on the European Union market has tended to become less price-orientated and based more on the range, quality and innovation of the products.

Furthermore, the population of these territories is acquiring a pattern of consumption and investment which is increasingly similar to that of Europe, a factor that indirectly allows for an increase in the volume of EU products to be traded. Previously, exports were based mainly on the sale of high-quality equipment and luxury goods, which would tend to become less limited as new more basic products gained access to the Chinese economy. Accordingly, those competitors that focused their main competitive advantage on the price-factor should gradually adjust to their new scenario.

In this light, the indicators for 2010 and this current year 2011 so far show an increase in the bilateral trade flows between both economies. It must therefore be emphasized that the Chinese development priorities could give rise to opportunities for Spanish companies, in two different ways:

20

•As an advantage for technological-intensive sectors (e.g. renewable energies, water treatment and biomed) before Chinese companies operating in these sectors develop the subsequent technologies in their own right.

•As a more stable form for medium and high-range consumer goods (fashion, food and beverages).

Nevertheless, in the medium and long term horizon, the development and growth of bilateral relations would be determined by factors such as the growth of current modest Spanish production investment in China.

Most importantly, the future of Spain’s bilateral relations with China would significantly depend on (i) the capacity of China to continue to open up and the growth of its economy (ii) growth of household disposable income above the actual GDP and promotion of personal consumption, as the main element to drive demand, (iii) an in-depth analysis of the intervention procedures adopted by the public sector in the economy through public enterprises and highly active financial and industrial policies.

3. Chinese investment into Spain3.1. Chinese overviewThe strengthening of the Chinese economy, growing at 11.9% and 10.3% during the first two quarters of 2010, is behind the rise in outbound investment that we are seeing from China. Such a rapid rate of development has resulted in further M&As, as Chinese investors are becoming victims of their own success. China’s economy is rapidly moving up the value chain, as Chinese consumers are seeing their purchasing power increase. Therefore, Chinese manufacturers are being pushed to seek more cost effective centres of production and are facing increasing challenges to meet the demands of their customers for higher quality and design. Chinese investors are now looking to diversify their operations away from the mainland and are looking for reputed brands, technology and resources. Spain is a good target that meets their requirements.

In the near future, Chinese banks will play a very important role in facilitating Chinese outbound investments. Over the past few years Chinese financial institutions have opened a large number of branches around the world, including Spain, and we expect this trend to continue as Chinese companies and investors will continue to focus on overseas markets to diversify their investments.

Spain offers a number of benefits to a potential investor, which is why many Chinese companies chose to establish their operations here, and many others are considering Spain as their target country for investments. Benefits such as incentives for foreign investors, the broadest network of double taxation and investment protection agreements, and strong government commitment to attracting foreign investment are oriented towards helping foreign companies to set up in Spain and take advantage of the market for their individual needs.

Investing in Spain - A guide for Chinese Businesses 21

Spain is the third largest recipient of Chinese FDI in Europe, and according to official data, Chinese FDI into Spain grew at a Compound Annual Growth Rate (CAGR) of 44.3% between 2003 and 2009. The overall stock of Chinese FDI in Spain is already over €8 million. Although the figure might not seem too big, the underlying trend is outstanding, meaning that Spain is becoming an increasingly attractive destination for Chinese investment. As proof of this affirmation, and according to several reports, the number of Chinese companies in Spain is forecast to double by 2013.

Since Spain started receiving FDI from China, the sector pattern of Chinese investment appeared to be in intermediate commercial goods, real estate and textiles; nowadays the investment focus is changing and the Spanish renewables and electronic components sectors are gaining appeal as investment targets. Spain is becoming a very attractive location for Chinese investors looking to start their European and Mediterranean operations. The fact that Spanish multinationals have a strong position and experience in Latin American markets is also an attractive point for Chinese companies seeking to profit from their experience.

Following the implementation of the 12th Five-Year Plan, we expect a surge in Chinese investment entering Spain, not only with the aim of entering the Spanish or European markets, but also as a way of acquiring renowned brand and world-class technologies to import them back to their home markets. Foreign brands acquisition and importing to their domestic markets by Chinese investors have become the new way for Chinese companies to gain a competitive advantage over their counterparts, especially in those sectors where Chinese domestic markets are already saturated such as retail, food and beverage or aviation spaces.

3.2. The appeal of SpainAs China develops and its domestic consumption markets start to gain speed, Chinese companies are starting to feel increasing pressure from both foreign and Chinese competitors. This trend will not only continue in the coming years, but will become even stronger, putting pressure on companies’ margins and market share. Therefore, Chinese companies have had to look at foreign markets in search of the competitive advantages that they are losing at home. Furthermore, Chinese companies wish to become the leaders in their home markets and to achieve this objective it will not be enough to try to outpace their domestic competitors, they will also need to beat multinational competition from abroad to become global leaders.

In their search for competitiveness and new markets Spain has much to offer Chinese investors. According to the World Bank, Spain is the 49th country in the world, and 10th in Europe, in terms of ease of doing business in the country. The country is the fifth biggest economy in Europe with a GDP per capita of US$ 31.946, and historically it has been among the biggest consumer markets of the European Union, with average per capita spending above the EU average. Additionally, Spain was ranked as the most popular and friendly destination for expatriates in Europe.

22

When targeting European and Latin American markets, Spanish companies can be the perfect partner for Chinese companies. Our companies already have vast experience, deep knowledge and a good reputation in both markets. Therefore, cooperating with a Spanish company would place any Chinese company in a much better position when entering these markets, and would enable them to benefit from our companies’ reputation and knowledge of the target market.

In terms of the country’s resources and infrastructures, Spain offers a pool of highly qualified workers at a very competitive cost, lower than their European peers; some of the best infrastructures in Europe, including the best high-speed train network; two of Europe’s biggest airports and the busiest ports in southern Europe. Spain’s extensive logistics network has direct connections with Europe, Latin America and the entire Mediterranean area.

As an investment opportunity for Chinese investors, Spain offers a range of high potential brands and companies with European level standards of design, technology and management. Spanish brands and technologies are acknowledged around the world for their top quality and high level of design, placing them in an unbeatable position to be exported abroad. The country’s strategic geographical location, with access to North Africa, Europe and Latin America, together with its economic openness and competitiveness, makes it a very attractive location for foreign investors.

Spain is not only a big consumer market with a high degree of purchasing power, but also offers a range of domestic high quality brands easily exportable to and marketable on the Chinese market. Spain’s renewable energies such as wind and solar power generators are amongst the most advanced technologies in the world. Brand acquisitions, as well as the purchase of advanced technologies are also crucial for Chinese outbound appeal and in this sense, Spain has a lot to offer Chinese corporate investors looking to strengthen their position and expand market shares not only in the international, but also in their domestic markets.

3.3. Deal rationaleAre earliest matches the best matches? This is a good question that should be raised before any overseas investment.

Indeed, one of the main risks that Chinese acquirers have traditionally faced was their inexperience in the field of cross-border purchases.

Ensuring that the reasons for acquiring any foreign target are duly checked from a professional perspective is a key driver for a successful investment strategy.

Being surrounded by good quality advice, especially by teams with solid international background, is the best guarantee to avoid succumbing to the so-called “window shopper mentality” where the inexperience of Chinese acquirers can lead them to take wrong decisions based on unreal synergies.

Investing in Spain - A guide for Chinese Businesses 23

The process of searching for outbound investment goes from target origination through to post-merger integration, including detailed valuation exercises or tax structuring support in order to close the acquisition under a complete long-term strategic vision.

Fluent communication with the counterparts and the development of soft skills at the time of running the deal process are excellent ingredients to reach a win-win situation for all.

Lastly, understanding the importance of cultural barriers when transacting is a paramount concern in the outbound investment process.

Chinese investors need to realise that their international growth should be based on in-depth knowledge of the cultural framework of each jurisdiction involved.

Involving a professional team with extensive experience at international and local level is an excellent approach to be able to bridge any cultural gaps.

Although it is true that over the years Chinese investors have improved their ability in the art of deal-making when buying foreign assets, addressing all of these concerns remains a “must” in any potential foreign acquisition.

4. Main business structures.4.1. The incorporated company.The incorporation of companies in Spain is mainly governed by the Consolidated Spanish Limited Liability Companies Law 1/2010 of July 2nd (Texto Refundido de la Ley de Sociedades de Capital). It recently adapted Spanish legislation to incorporate European Community company law directives and substantially amends the former Companies Law of 1989 and Limited Liability Companies Law of 1995.

Chinese companies setting up a company in Spain may do so by creating a wholly-owned subsidiary (a company whose shares are 100% owned by the Chinese parent company, or may join others in establishing a company that is jointly owned by various shareholders).

This chapter explains the most common types of companies / joint ventures that can be registered in Spain as well as their differences and advantages/ disadvantages.

Accordingly, set out below is a brief explanation of the principal forms of Company in Spain: the Public Limited Liability Company (Sociedad Anónima – S.A.), Private Limited Liability Company (Sociedad de Responsabilidad Limitada – S.L.), New Enterprise Limited Company (Sociedad Limitada Nueva Empresa- S.L.N.E.), General and Limited Partnerships (Sociedad Colectiva and Sociedad Comanditaria), Joint Ventures, and European Public Limited-Liability Company (Societas Europaea – SE).

24

A. Public Limited Liability Company (Sociedad Anónima - S.A.)As in other countries, an S.A. in Spain is distinct from its members. It provides limited liability for its members and the possibility of unrestricted transfer of shares without its own continuity being affected. Nevertheless, in certain circumstances, a sole shareholder and / or the directors may become liable in respect of the company’s debts.

1. ShareholdersAn S.A. may be listed on a stock exchange or it may be owned by only a few shareholders; it may also be a wholly owned subsidiary of another entity (sole shareholder entity). If the company has only one shareholder, the following further requirements must be met to comply with Spanish regulation:

i. The identity of the sole shareholder must be filed at the Mercantile Registry ("Registro Mercantil").

ii. A Register of Agreements entered into between the sole shareholder and the company must be legalised at the Mercantile Registry in a similar way to the Register of Minutes. These agreements must be transcribed into this Register.

iii. The fact that the company has one shareholder must be stated on all documentation, correspondence, orders, invoices and in all publications which must be made in accordance with the law or the of the company by-laws.

iv. The Notes to the financial statements ("Memoria") should make express and individual reference to agreements between the sole shareholder and the company indicating their nature and terms and conditions.

The founder-shareholders may be Spanish nationals or foreigners, individuals or legal entities. There are no residence or nationality requirements. However, the foreign legal entity shareholders must obtain a taxpayer identification number, for statistical purposes only. If the shareholders are foreign individuals, they must obtain a resident alien identification number (NIE) in order to register the company with the Spanish tax authorities. The procedure to obtain a NIE may take over one month. The NIE must be applied for at a Spanish consulate or by someone (i.e. Deloitte lawyers) in Spain with a power of attorney.

2. Share capitalAn S.A.'s share capital must be at least €60,000. There is no maximum share capital established by law for an S.A. All shares must have a par value and shares may not be issued for less than that par value, although they may be issued at a premium (paid-in surplus). Shares must be “nominative” (registered) until they are fully paid in; thereafter, they may be “bearer” shares.

Investing in Spain - A guide for Chinese Businesses 25

In order to establish the par value of the shares representing the share capital correctly, it is advisable to set an exact amount of euros as share capital which can be divided into the entire number of shares (i.e. €60,000 of share capital divided into 6,000 shares of a par value of €10).

The initial share capital with which the S.A. proposes to be incorporated (its authorised capital) must be stated in the by-laws and, therefore, in the public deed of incorporation and registered at the Mercantile Registry. Any change to the capital involves an amendment to the by-laws and must be registered at the Mercantile Registry.

An S.A. cannot be set up unless its share capital is fully subscribed and at least 25% of the par value of each share is paid. As for the remaining 75%, any disbursement of that percentage to be made in the form of non-cash assets must be paid in within five years following the initial subscription; if the disbursement is in cash, the maximum term during which the 75% balance must be paid in is established by the by-laws.

Cash contributions must be made in euros; if made in a foreign currency, the euro equivalent must be determined in accordance with the law. Cash contributions must be evidenced by bank deposit receipts issued by the bank, in which the cash contribution has been made, delivered to the Notary Public concerned when the deed of incorporation is executed.

Contributions may also be made in a form other than in cash, as long as certain conditions are met (i.e. report of an independent expert).

An S.A. may acquire its own fully paid-in shares, amounting to up to 20% of its authorised capital, provided that various formalities are complied with, but (i) such an acquisition cannot entail that the net equity be reduced to less than the amount resulting from the sum of share capital plus legal or by-law restricted reserves; and (ii) it must then constitute a restricted reserve of an amount equal to the value of the controlling company‘s shares recognised on the asset side of the balance sheet. If the S.A. is listed on the stock exchange, this 20% limit is reduced to 10%.

The shareholders' liability to third parties is limited to the par value of the shares that they have subscribed.

3. Shareholders' rights:Shareholders' rights include a share in profit distribution, preferential right of subscription in capital increases (except for contributions in kind) and participation in the allocated share capital in the event that the company is wound up.

Shareholders' general rights include attendance at the Annual General Meetings and the exercise of the right to vote as per capital participations rather than as per person.

26

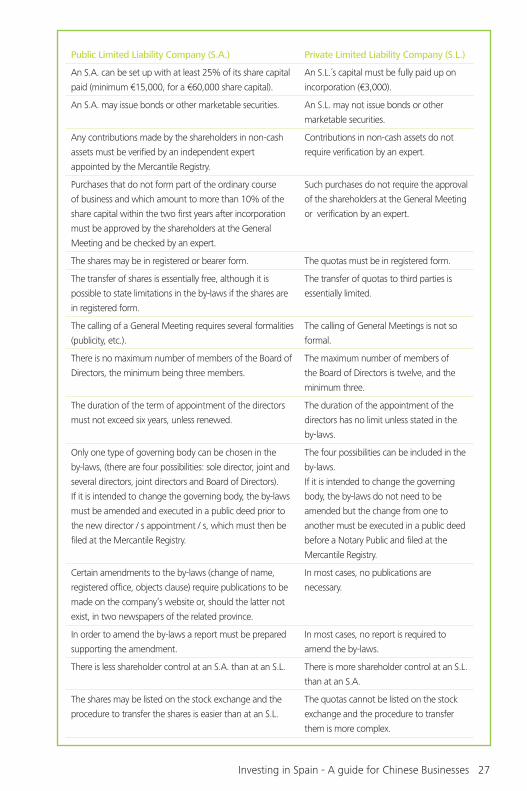

Main differences between an S.L. and an S.A.:

4. Directors liability:The provisions in respect of directors’ liability have become much more stringent under Spanish law in recent years. Directors of both S.A.s and S.L.s may incur civil liability when the company, shareholders or creditors have suffered damage due to an unlawful act or omission of the Directors or one carried out without due diligence. Under company legislation, directors may also become jointly and severally liable for all the company’s debts where, in circumstances in which the company ought to be wound-up (in practice, particularly when losses reduce the net worth to below half the value of the share capital), they do not take the necessary steps. However, in such cases the directors shall only be held jointly and severally liable for the debts incurred after the legal grounds for dissolution have arisen.

Directors may also be held liable in relation to the taxes. They may be held criminally liable and failure to comply with Labour Law and Social Security obligations may also lead to directors being held liable when their conduct has been unlawful or negligent.

Directors’ liability may extend not only to directors who have been legally appointed as such, but also to “de facto” directors.

B. Private limited liability company (Sociedad De Responsabilidad Limitada - S.L.)An S.L., like an S.A., may be founded by only one shareholder. The additional requirements in this case are the same as detailed above (point A. Shareholders. points i - iv) in respect of sole shareholder status.

As with an S.A., the shareholders' liability is limited to their contribution to the share capital.

Minimum initial capital of €3,000 is required, which must be paid in full on the company’s incorporation. The capital is divided not into shares but into equal “quotas” ("participaciones sociales"). Each quota carries one vote and must be fully paid before the company can commence trading. There is no minimum size for a quota and there is no maximum share capital established by law for an S.L. Quotas must be in registered form.

In order to establish the par value of the quotas representing the share capital, it is advisable to set an exact amount of euros as share capital which can be divided into the entire number of quotas, (i.e. €3,000 of share capital divided into 300 quotas of par value of 10 Euros).

Public Limited Liability Company (S.A.) Private Limited Liability Company (S.L.)

An S.A.´s capital is divided into shares. An S.L.´s capital is divided not into shares

but into equal quotas.

An S.A.´s share capital may not be less than €60,000. An S.L.´s capital may not be less than

€3,000.

Investing in Spain - A guide for Chinese Businesses 27

Public Limited Liability Company (S.A.) Private Limited Liability Company (S.L.)

An S.A. can be set up with at least 25% of its share capital

paid (minimum €15,000, for a €60,000 share capital).

An S.L.´s capital must be fully paid up on

incorporation (€3,000).

An S.A. may issue bonds or other marketable securities. An S.L. may not issue bonds or other

marketable securities.

Any contributions made by the shareholders in non-cash

assets must be verified by an independent expert

appointed by the Mercantile Registry.

Contributions in non-cash assets do not

require verification by an expert.

Purchases that do not form part of the ordinary course

of business and which amount to more than 10% of the

share capital within the two first years after incorporation

must be approved by the shareholders at the General

Meeting and be checked by an expert.

Such purchases do not require the approval

of the shareholders at the General Meeting

or verification by an expert.

The shares may be in registered or bearer form. The quotas must be in registered form.

The transfer of shares is essentially free, although it is

possible to state limitations in the by-laws if the shares are

in registered form.

The transfer of quotas to third parties is

essentially limited.

The calling of a General Meeting requires several formalities

(publicity, etc.).

The calling of General Meetings is not so

formal.

There is no maximum number of members of the Board of

Directors, the minimum being three members.

The maximum number of members of

the Board of Directors is twelve, and the

minimum three.

The duration of the term of appointment of the directors

must not exceed six years, unless renewed.

The duration of the appointment of the

directors has no limit unless stated in the

by-laws.

Only one type of governing body can be chosen in the

by-laws, (there are four possibilities: sole director, joint and

several directors, joint directors and Board of Directors).

If it is intended to change the governing body, the by-laws

must be amended and executed in a public deed prior to

the new director / s appointment / s, which must then be

filed at the Mercantile Registry.

The four possibilities can be included in the

by-laws.

If it is intended to change the governing

body, the by-laws do not need to be

amended but the change from one to

another must be executed in a public deed

before a Notary Public and filed at the

Mercantile Registry.

Certain amendments to the by-laws (change of name,

registered office, objects clause) require publications to be

made on the company’s website or, should the latter not

exist, in two newspapers of the related province.

In most cases, no publications are

necessary.

In order to amend the by-laws a report must be prepared

supporting the amendment.

In most cases, no report is required to

amend the by-laws.

There is less shareholder control at an S.A. than at an S.L. There is more shareholder control at an S.L.

than at an S.A.

The shares may be listed on the stock exchange and the

procedure to transfer the shares is easier than at an S.L.

The quotas cannot be listed on the stock

exchange and the procedure to transfer

them is more complex.

28

C. New Enterprise Limited Company (Sociedad Limitada Nueva Empresa- S.L.N.E.)This corporate entity is a special type of limited liability company.

As with an S.A. and an S.L., the S.L.N.E. must be set up by public deed, which must be registered at the corresponding Mercantile Registry. However, the procedure is simplified and the use of new technologies is permitted with the aim of expediting the process of setting up companies of this type.

There are, however, a number of characteristics of the S.L.N.E. which make it unlikely to be of interest, in principle, to foreign investors; for example, the founder shareholders must be individuals and on incorporation they may not exceed five. Subsequent transfers may only be to individuals (although after incorporation, transfers of shares may result in there being more than five shareholders).

The name of the S.L.N.E. must be the name and surnames of one of the founders, followed by an alphanumerical code and the indication Sociedad Limitada Nueva Empresa or its abbreviation SLNE. The share capital may not be less than €3,012, or more than €120,202. The S.L.N.E. cannot have a Board of Directors and it is necessary to be a shareholder to be a director.

Legal steps to set up a company (S.A./S.L.)

i. In general terms, the legal steps in order to set up a company are very similar for an S.A. and an S.L.:

ii. Make a prior declaration to the Directorate-General of Commerce and Investments, should the shareholder of the Spanish company be a company from a tax haven country.

iii. Obtain a certificate on behalf of one of the shareholders from the Central Mercantile Registry to the effect that the proposed name of the company has not already been entered in the Register.

iv. Draft the company's by-laws (“Estatutos Sociales”).v. Draft powers of attorney appointing any person in Spain, who will appear before

a Notary Public in Spain to incorporate the company acting for and on behalf of the shareholder(s). Such power of attorney must bear the Apostille of The Hague Convention of 5 October 1961, abolishing the requirement for legalisation for foreign public documents, in order to have legal effects in Spain.

vi. Liaise with the chosen Bank regarding the preparation of the bank certificate evidencing that the funds have been remitted from overseas and credited in the company's account.

vii. Prepare the company’s public deed of incorporation, which must be signed in the presence of a Notary Public by the shareholder(s) or by their attorneys, as the case may be.

Investing in Spain - A guide for Chinese Businesses 29

viii. Declare the foreign investment at the Directorate-General of Commerce and Investments so that it may be recorded for statistical purposes.

ix. Obtain a taxpayer identification number for each of the shareholders in the company (Número de Identificación Fiscal - NIF) for statistical purposes only.

x. Obtain the provisional taxpayer identification number card for the company (Tarjeta Provisional de Número de Identificación Fiscal - NIF).

xi. File a capital duty return (1% on the share capital). Said tax is currently exempt.xii. File the public deed of incorporation of the company at the provincial Mercantile

Registry.xiii. Legalisation of the Register of Shareholders, Register of Minutes and Register of

Agreements entered into between the Company and its sole shareholder (the latter only if it is a sole-shareholder company).

It usually takes approximately one week to set up the S.A. / S.L. once all the information and documents are gathered plus a further three to four weeks to register it at the Mercantile Registry.

Lastly, it must be noted that the Spanish tax authorities currently require that the non-Spanish resident directors or individual shareholders of Spanish companies obtain a resident alien identification number (NIE) in order to register the company with the tax authorities.

D. General And Limited Partnerships (Sociedad Colectiva and Sociedad Comanditaria)Spanish commercial law allows for both general and limited partnerships. In a general partnership, the members are normally jointly and severally liable for all the debts and obligations of the partnership, whereas a limited partnership is created by one or more general partners (socios colectivos), who are jointly and severally liable without limit for the partnership’s debts and one or more limited partners (socios comanditarios), who are liable only up to the amount of their respective capital contributions.

Limited partnerships in which the limited partners’ interests are in the form of transferable shares are called share partnerships (Sociedad Comanditaria por acciones).

E. Joint VenturesSpanish legislation envisages several types of co-operation companies:

•Unincorporated Temporary Joint Ventures (Uniones Temporales de Empresas): entity created by several companies when setting up a sort of temporary association which is to exist only for a limited period of time and to undertake a specific project. These types of associations do not have separate legal personality and are not corporations.

30

•Economic interest grouping (EIG) (Agrupación de Interés Económico – AIE): is a vehicle for a joint venture between Spanish participants. It is similar in concept to a partnership, its participants having joint and several liability for its debts.

To form an AIE, the participants must execute a public deed, incorporating the by-laws. This deed must be filed at the Mercantile Registry. The internal operation of an AIE is similar to that of an S.A.

•European economic interest grouping (Agrupación Europea de Interés Económico- AEIE): is a cross-border version of the AIE. A Spanish AEIE is a separate legal entity and must have its registered office in Spain. It must be registered at the Mercantile Registry, and in almost all respects it is similar in constitution and operation to an AIE.

However, S.A. and / or S.L. companies may also form joint-ventures.

F. European Public Limited Liability Company (Societas Europaea – SE)The introduction of the SE is an important company law development in the EU and may provide easier cross-border mergers and changes of registered office and cost savings. However, as many issues affecting the SE are subject to national law, it is not an entirely uniform new entity. Although this type of company has been included in Spanish law since 2005, very few entities have opted for this type of corporation.

Some of the basic characteristics of the SE are: the minimum share capital is €120,000; the registered office of the SE must be located in the same Member State as its head office; there is no central registration and an SE shall be registered in the Member State in which it has its registered office at the registry designated by its law.

The formation of an SE requires involvement of entities of at least two different Member States. There are four ways in which an SE may be formed: merger; formation of a holding SE; incorporation of a subsidiary SE and conversion of an existing company into an SE. An SE may itself set up one or more subsidiaries in the form of SEs.

The Regulation also provides for the possibility of an SE transferring its registered office from one Member State to another.

Investing in Spain - A guide for Chinese Businesses 31

As regards the structure and management of the SE, the Regulation provides that the SE shall comprise:

i. A general meeting of shareholders; and

ii. Either a supervisory body and a management body (two-tier system) or a governing body (one-tier system).

Directive 2001/86/EC is designed to ensure that employees have a right of involvement in issues and decisions affecting the life of their SE.

4.2. Branch or representative office of an incorporated foreign companyChinese companies wishing to expand their business activities into new territories will often consider establishing a branch or even a representative office instead of incorporating a new company.

A. Branches Of Foreign Companies (Sucursal Extranjera)From a tax point of view, branches are permanent establishments of non-resident entities.

It is important to take into account that a branch in Spain is not a separate legal entity from its parent company. Nevertheless, the branch has certain autonomy of operation. As with an S.A. and an S.L., any type of activity can be performed by a branch although the parent company is fully liable for the debts of the branch.

The branch must have the same name as the parent company plus the words "Sucursal en España" ("Branch in Spain").

It is important to note that for fiscal and foreign transactions, the arm’s length principle applies to operations between the parent company and the branch. Separate accounts must be kept.

A branch of a non-resident company must appoint a resident individual or legal entity to represent it. The representative appointed will be the person who deals with the tax authorities before the expiry of the deadline for filing the declaration of income earned in Spain. The appointment of a representative to act as tax representative must be reported to the local tax administration office within 2 months of the date of the appointment. This representative is normally one of the branch’s legal representatives, as registered in the Mercantile Register, but if those legal representatives are themselves non-resident, a resident individual or legal entity must be appointed instead.

32

The representatives may be held jointly and severally liable for the tax debts of the permanent establishments of the non-resident entities they represent.

If the parent company's financial statements are not filed at the Mercantile Registry of its country of origin (or if they are so filed but do not comply with the requirements of Spanish law, the financial statements of the branch itself must be filed at the Mercantile Registry in Spain. When filed in Spain, the financial statements of the branch are open to public inspection.

1. Main advantages and disadvantages:

Advantages Disadvantages

There is no minimum working capital requirement.

More risk, because branches are liable to third parties up to the full amount of the parent company's equity (in the case of a Spanish company, only the equity in that company is at risk).

It is an inexpensive way to break into an unknown market.

It is not the ideal vehicle for substantial projects, because the parent company runs the entire risk and there is no division between the activities of the parent company and those of the branch.

It is an appropriate vehicle for low cost projects and those with a low turnover.

The fact that it is a foreign company could make some clients or creditors less willing to do business with it, thus making it difficult to obtain loans, contracts, etc.

Possibility for the parent company of offsetting the branch's losses for tax purposes in the same financial year in which they are incurred.

Corporate income tax payable by the branch is normally deductible by the parent company, as well as the transfer of working capital.

The branch is more solvent, because the parent company is liable to third parties up to the full amount of its equity.

Spanish law does not allow the simple conversion of a branch into a subsidiary company.

Investing in Spain - A guide for Chinese Businesses 33

2. Main differences between a branch and a public limited liability company (S.A.) and a private limited liability company (S.L.):

i. Public and private limited liability companies must be wound up if their accumulated losses reduce their net worth to less than the 50% of their share capital, unless that capital is reduced or increased, or if the capital is reduced below the legal minimum. Moreover, the share capital of public limited liability companies must be formally reduced when losses have reduced net assets to less than two-thirds of the share capital and equilibrium is not restored in the following financial year.

ii. Public and private limited liability companies must transfer 10% of net profit for each year to the legal reserve until the balance of this reserve reaches at least 20% of the share capital. Until the legal reserve exceeds 20% of share capital, it can only be used to offset losses, provided that sufficient other reserves are not available for this purpose.

iii.S.A and S.L. companies are taxed in the same way. Branches are considered to be Permanent Establishments (PE) and, in general terms, they are taxed in Spain applying the same rules as those applicable to subsidiaries, with certain exceptions.

The main difference between subsidiaries and branches is that, in order to determine taxable income, the payments which the PE makes to its Head Office (or any other PE the Head Office may have) for royalties, interest, commissions, or in exchange for technical assistance or for the use or assignment of other assets or rights, are not deductible in the calculation of non-resident income tax.

On the other hand, management and general administrative expenses incurred by the Head Office are deductible to the extent that they are allocated to the branch, they are provided for in the accounts of the PE, that the amounts, criteria and method of distributing the costs are set out in a document filed with the tax return, and the costs are allocated on a rational and continuous basis.

A Spanish subsidiary, on the other hand, may claim as deductible expenses any payments made to the parent company in respect of management fees, technical assistance, interest and royalties, the cost of which must be fixed on an arm's length basis since the companies are related. Specific formal requirements have to be met for certain expenses.

Nonetheless, please bear in mind that the tax deductibility of expenses on transactions carried out between related entities (applicable to certain types of entity, i.e., subsidiaries, branches, representative offices, etc) would depend on whether these transactions represent a real advantage or use for their recipient.

34

Moreover, it should be highlighted that Royal Decree 1793/2008, of 3 November amending the Corporate Income Tax Regulations, was published on 18 November 2008. Mainly Articles 18 to 20 of that Royal Decree regulate the documentation obligations affecting (i) transactions between related entities; (ii) the group to which the tax payer belongs; and (iii) the tax payer itself. In accordance with Transitional Provision Three of the Royal Decree, these obligations have had to be complied with since 19 November, 2008, three months after the entry into force of the Royal Decree. Please note that pursuant to Article 18.3 of Royal Decree 1793/2008, transactions between entities in the same tax consolidation group are exempt from the above-mentioned documentation obligations.

3. Legal steps to set up a branch

A branch must be set up in the presence of a Spanish notary public who will require the following documents:

i. A certificate from a bank in Spain to the effect that the working capital, if any, of the branch has been transferred and credited to a current account opened in the branch's name.

ii. A certificate issued by a notary public stating that the parent company has been duly incorporated, that the Memorandum and By-laws have been duly approved and that the directors have been duly appointed.

iii. A certificate of the minutes of the General Meeting or Board Meeting of the parent company at which it is resolved to set up the branch, detailing the allocated capital, if any, the objects, registered office and financial year of the branch. Representatives of the branch should be appointed and their powers defined and an individual must be empowered to appear before a notary public in Spain to execute the public deed setting up the branch. A tax representative should also be appointed.

iv. A sworn translation into Spanish of the parent company's Memorandum and By-laws.

It will also be necessary to:

a. Make a prior declaration to the Directorate-General of Commerce and Investments should the parent company be resident in a tax haven.

b. Record the foreign investment at the Directorate-General of Commerce and Investments so that it may be recorded for statistical purposes only.

Investing in Spain - A guide for Chinese Businesses 35

c. Obtain a non-resident taxpayer identification number (Número de Identificación Fiscal - N.I.F.) for the foreign company

d. Obtain a provisional taxpayer identification number (Número de Identificación Fiscal provisional - N.I.F.) for the branch.

e. File the public deed setting up the branch at the corresponding Mercantile Registry.

f. File a capital transfer tax return.

4. Main disbursements:

i. Fees of the notary public (the amount will depend on the working capital, if any);ii. Mercantile Registry fees (the amount will depend on the working capital, if any); iii. Translation costs for obtaining a sworn translation of the parent company’s Memorandum

and By-laws.

It usually takes approximately 1 week to set up the branch plus a further 3 to 4 weeks to register it at the Mercantile Registry.

B. Representative Office (Oficina De Representación)A representative office is one that, unlike a branch or a company, has no power to conclude contracts with customers of any type in Spain.

It is very important to stress that if the idea is to conduct business activities in Spain, the representative office would not be the most appropriate vehicle. Therefore, since the final purpose of these entities is very different, it is crucial to determine the exact type of structure required in Spain. Although representative offices are very “simple” in principle, they should only be used for certain activities.

1. Legal steps to set up a representative officeAs with a branch, a representative office must be set up in the presence of a Spanish notary public who will require the following documents:

i. A certificate from a bank in Spain to the effect that the capital of the representative office, if any, has been transferred and credited to a current account opened in the representative office's name.

ii. A certificate issued by a notary public stating that the parent company has been duly incorporated, that the Memorandum and By-laws have been duly approved and that the directors have been duly appointed.

36

iii. A certificate of the minutes of the General Meeting or Board Meeting of the parent company at which it is resolved to set up the representative office, detailing the allocated capital, if any, the objects and the registered office of the representative office. Representatives should be appointed and their powers defined and someone must be empowered to appear before a notary public in Spain to execute the public deed setting up the representative office. A tax representative should also be appointed.

iv. A sworn translation into Spanish of the parent company's Memorandum and By-laws.

It will also be necessary to:

a. Sign the public deed opening the representative office in the presence of a notary public.b. Obtain a non-resident taxpayer identification number (Número de Identificación Fiscal -

N.I.F.) for the foreign company.c. Obtain a provisional taxpayer identification number (Número de Identificación Fiscal

provisional - N.I.F.) for the representative office.d. Appoint a tax representative for non-resident income tax purposes.e. File a capital transfer tax return.

2. The main disbursements will include:i. Fees of the notary public.

ii. Translation costs for obtaining a sworn translation of the parent company’s Memorandum and By-laws.

It is not necessary to file the public deed opening the registered office at the Mercantile Registry.

It usually takes approximately 1 week to open the representative office once all the information and documents have been gathered.

4.3 Business regulation 4.3.1 Reorganisation process: national and international mergers and acquisitionsA. OverviewMergers and acquisitions are partnering strategies used by businesses to meet current challenges and to take advantage of the opportunities afforded by the new European framework.

The Law on structural changes to companies (March 2009) unifies Spanish law on the subject of mergers and, in certain aspects, it differs from European Union regulations, since the Spanish law envisages new methods and simplifies certain procedures.

Investing in Spain - A guide for Chinese Businesses 37

It introduces a new regulatory framework for structural changes to companies (alterations of a company’s legal form, mergers and spin-offs; transfers en bloc of assets and liabilities; the transfer of the registered office abroad), and establishes a common legal framework for all companies in Spain.

Likewise, it regulates cross-border mergers for the first time, by transposing Directive 2005/56/EC into Spanish law and, specifically, regulates mergers between Spanish and non-EU companies.

B. National and international mergers and other structural changes to companiesStructural changes are those alterations of a company that go beyond the basic amendments of the company’s by-laws and affect the equity structure or corporate form of the company.

These structural changes which Spanish companies are able to undertake are, mainly, the alteration of a company’s legal form, mergers and spin-offs; transfers en bloc of assets and liabilities and the transfer of the registered office abroad.

1. Alteration of a company’s legal form.The alteration of a company’s legal form is a structural modification whereby a company adopts a different legal structure while preserving its legal status.

In addition to further legal requirements, the alteration of a company’s legal form requires a resolution of the General Meeting. This resolution has to be published in the Official Gazette of the Mercantile Registry and in an important newspaper (however, the resolution does not have to be published if an individual notification of the resolution is sent to all the shareholders and creditors).

Afterwards, the resolution is executed as a public deed and must be recorded at the appropriate Mercantile Registry.

2. Mergers.There are a number of ways to acquire a company, other than simply purchasing it, one of which is a merger with another company.

There are two main types of merger: merger by absorption, and merger by setting up a new company. The merger by absorption entails the acquisition of one company by another. In this case, the company that is taken over is wound up and its assets become the property of the company that takes it over.

38

On the other hand, two or more companies may join forces to establish a new company. The original companies are wound up and their assets become the property of the newly-created company.

Mergers between companies quoted on the stock market are sometimes carried out by means of a public takeover bid, whereby a company publicly announces its intention to acquire a number of shares in another company, allowing it to take control of that company.

Depending on the industry or activity in which the companies are involved, mergers may be horizontal (between companies competing in the same industry), vertical (a company merges with the company which supplies its raw materials, for example, or with the company that distributes its final products) or conglomerates (merger between companies which do not have any connection with each other, with the aim of sharing services such as management, accounting, etc.).

In order for a merger to take place, the boards of directors of all the companies involved must approve the corresponding draft terms of merger . After the required time has elapsed to allow creditors to express their right of objection (one month), only two procedures need be carried out to make the merger official:

– formalising the merger resolutions in a public deed before a notary public, and – registering the said public deed at the corresponding Mercantile Registry.

Finally, it should be highlighted that not only intra-EU cross-border mergers but also international cross-border mergers are regulated for the first time in the Spanish Law on structural changes to companies.

3. Spin-offs.The spin-off of a company is a structural change by means of which a part of a company (or the whole company) is divided into two or more parts and these parts are transferred to a new company or to an existing company. The shareholders of the company carrying out the spin-off would receive a number of shares of the beneficiary company in proportion to the number of shares they own in the original company.

4. Transfers en bloc of assets and liabilities.Through a transfer en bloc of assets and liabilities, a company may transfer all of its assets to a partner or to a third party, for a fee which must not include stocks, shares or membership fees of the assignee.

5. Transfer of the registered office abroad.The transfer of the registered office of a Spanish company abroad is possible and, likewise, a foreign company may transfer its registered office to Spain.

Investing in Spain - A guide for Chinese Businesses 39