investment analysis session 3: 10 th november 2009 duration 1 hour 30 min

TRANSCRIPT

Investment Analysis

Session 3: 10th November 2009

Duration 1 hour 30 min

Page 2

Topics to be covered

Equity Investment Analysis

Financial Distress

Types of Risk

Valuation Approaches

Page 3

EQUITY INVESTMENT ANALYSIS

Equity Investment Analysis

Page 4

Creative Accounting or Aggressive Accounting

Creative accounting and earnings management are:

Accounting practices that may follow the letter of the rules of standard accounting practices, but certainly deviate from the spirit of those rules

The term generally refers to, systematic misrepresentation of the true income and assets of corporations or other organizations for the purpose of pleasing investors and inflating stock prices

The main forms of earnings management are as follows: Unsuitable revenue recognition Inappropriate accruals and estimates of liabilities Excessive provisions and generous reserve accounting Intentional minor breaches of financial reporting requirements that

aggregate to a material breach

Page 5

Balance Sheet

• A documented report of your company's assets

and obligations, as well as the residual ownership

claims against your equity at any given point in

time.

Page 6

Balance Sheet

Assets Side:

Fixed assets: (plant, equipments, machinery)

Investment: (in other companies, in market)

Current assets(Stock, Debtors, prepaid expenses)

Intangible assets (Goodwill, patent, trademark)

Fictitious assets: (Preliminary expenses)

Page 7

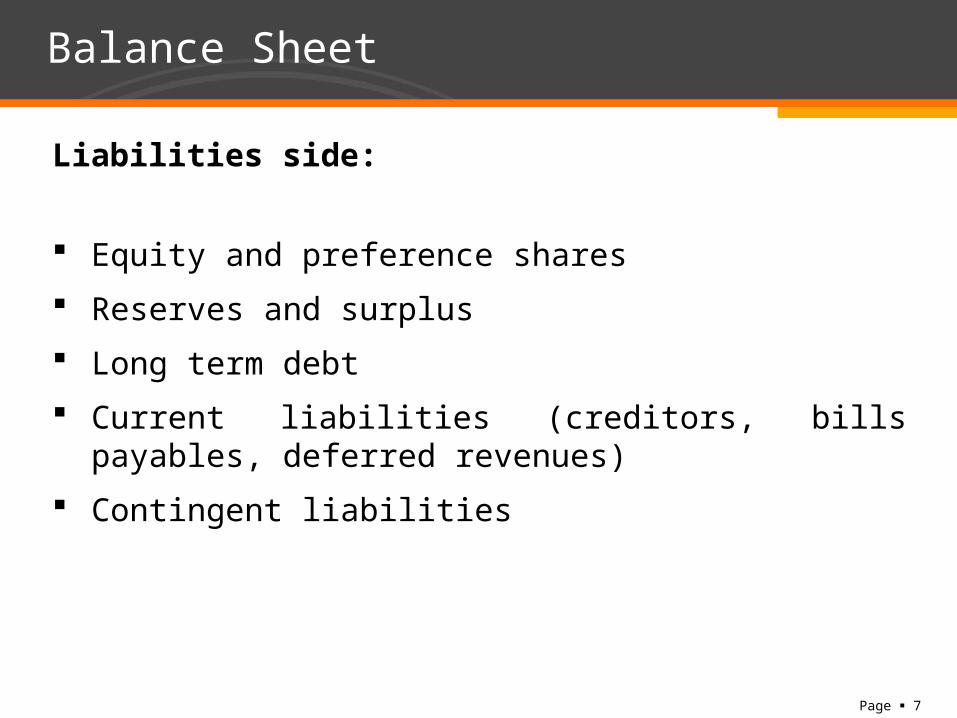

Balance Sheet

Liabilities side:

Equity and preference shares

Reserves and surplus

Long term debt

Current liabilities (creditors, bills payables, deferred revenues)

Contingent liabilities

Page 8

Major Earnings Indicators

EBITDA: (Earnings Before Interest, Taxes, Depreciation and Amortization)

EBIT: (Earnings before interest and tax)

PAT or net income

where p is plow back ratio

Page 9

Financial Distress

Page 10

What is Financial Distress?

A situation where a firm’s operating cash flows are not

sufficient to satisfy current obligations and the firm is forced

to take corrective action

Financial distress may lead a firm to default on a contract,

and it may involve financial restructuring between the firm,

its creditors, and its equity investors

Page 11

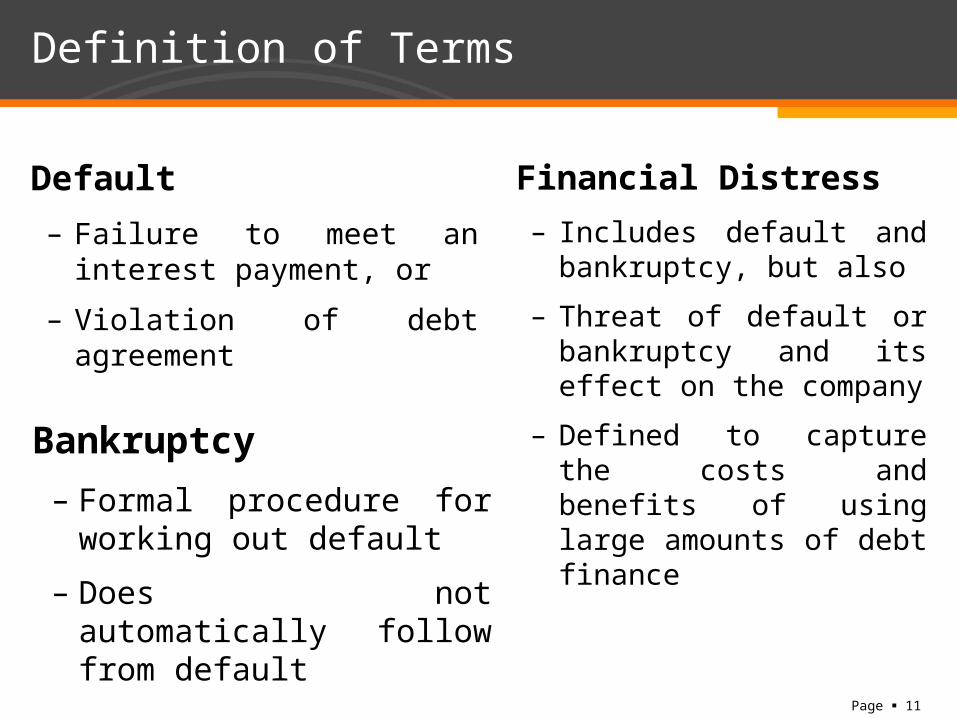

Definition of Terms

Default

– Failure to meet an interest payment, or

– Violation of debt agreement

Financial Distress

– Includes default and bankruptcy, but also

– Threat of default or bankruptcy and its effect on the company

– Defined to capture the costs and benefits of using large amounts of debt finance

Bankruptcy

– Formal procedure for working out default

– Does not automatically follow from default

Page 12

Insolvency

Stock - base insolvency: the value of the firm’s assets is

less than the value of the debt

AssetsAssets

DebtDebt

EquityEquity

Solvent firmSolvent firm

AssetsAssets

Insolvent firmInsolvent firm

DebtDebt

Note the negative equity

Page 13

Insolvency

Flow - base insolvency: It occurs when the firms’ cash flows are

insufficient to cover contractually required payments

Contractual obligations

Insolvency

$

Firm cash flow

Cash flow shortfall

time

Page 14

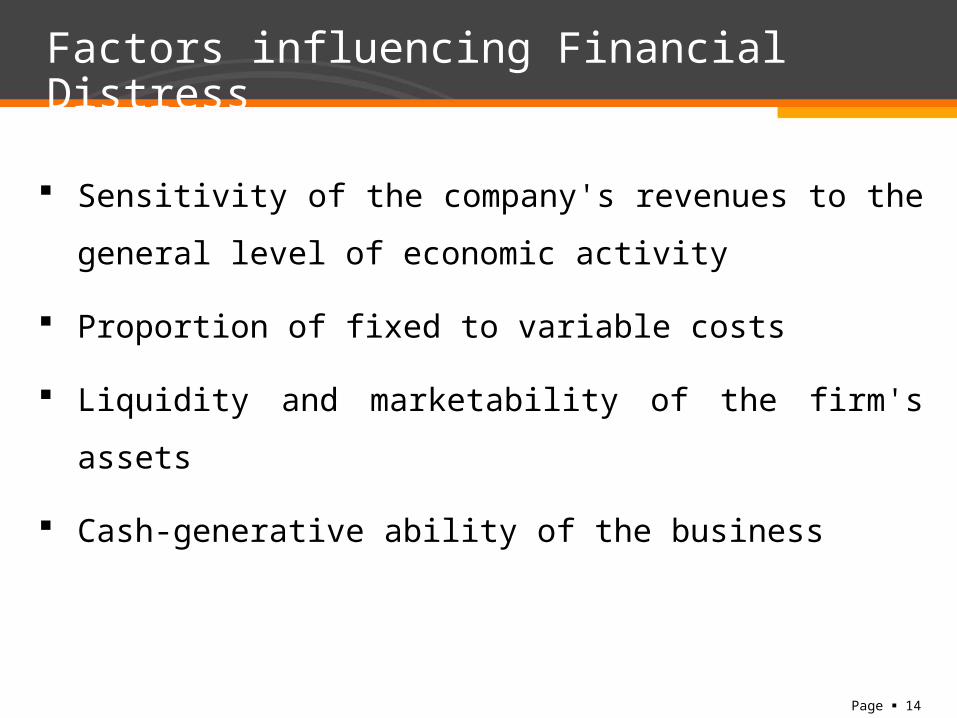

Factors influencing Financial Distress

Sensitivity of the company's revenues to the general level

of economic activity

Proportion of fixed to variable costs

Liquidity and marketability of the firm's assets

Cash-generative ability of the business

Page 15

Factors influencing Financial Distress

Operating leverage:

A measurement of the degree to which a firm or project incurs a combination of fixed and variable costs

A business that makes few sales, with each sale providing a very high gross margin, is said to be highly leveraged

A business that has a higher proportion of fixed costs and a lower proportion of variable costs is said to have used more operating leverage

Degree of Operating Leverage (DOL) = % Change in EBIT

% Change in sales

Page 16

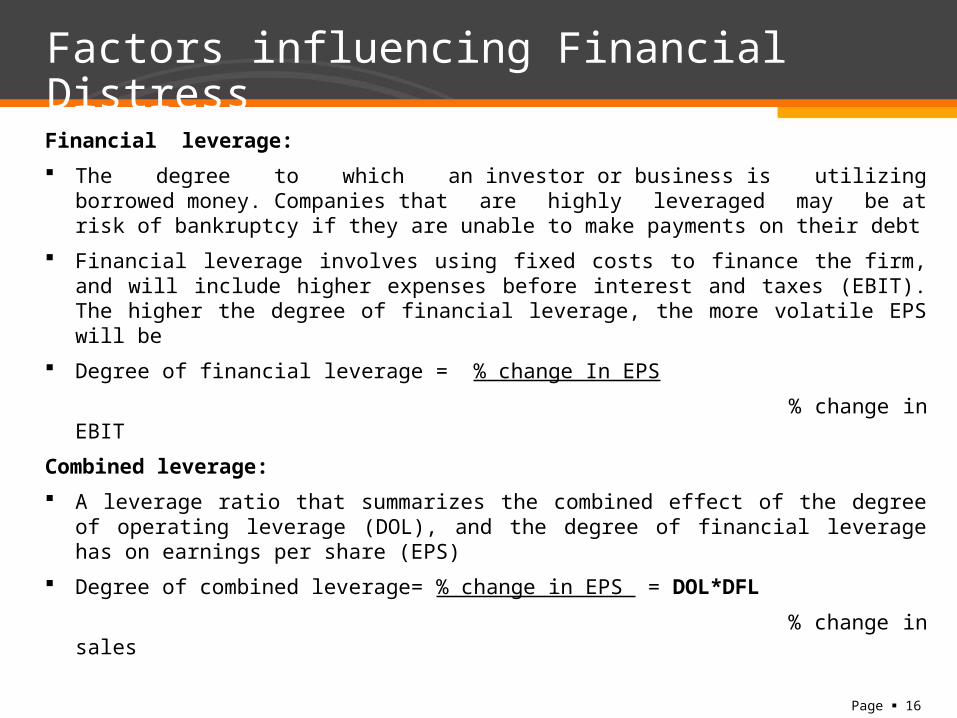

Factors influencing Financial Distress

Financial leverage:

The degree to which an investor or business is utilizing borrowed money. Companies that are highly leveraged may be at risk of bankruptcy if they are unable to make payments on their debt

Financial leverage involves using fixed costs to finance the firm, and will include higher expenses before interest and taxes (EBIT). The higher the degree of financial leverage, the more volatile EPS will be

Degree of financial leverage = % change In EPS

% change in EBIT

Combined leverage:

A leverage ratio that summarizes the combined effect of the degree of operating leverage (DOL), and the degree of financial leverage has on earnings per share (EPS)

Degree of combined leverage= % change in EPS = DOL*DFL

% change in sales

Page 17

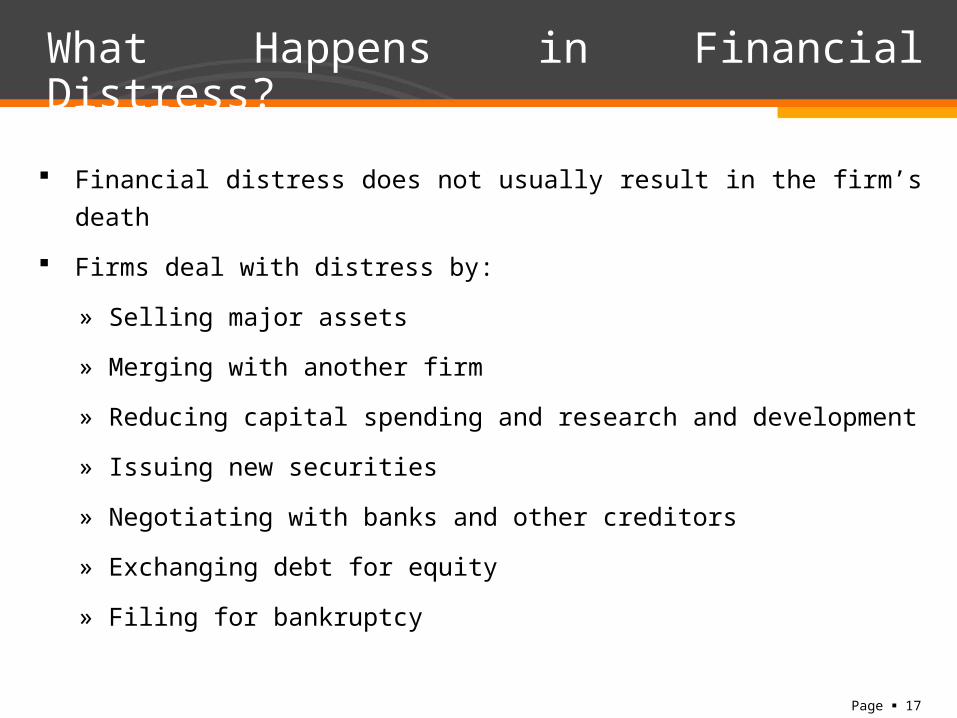

What Happens in Financial Distress?

Financial distress does not usually result in the firm’s death

Firms deal with distress by:

» Selling major assets

» Merging with another firm

» Reducing capital spending and research and development

» Issuing new securities

» Negotiating with banks and other creditors

» Exchanging debt for equity

» Filing for bankruptcy

Page 18

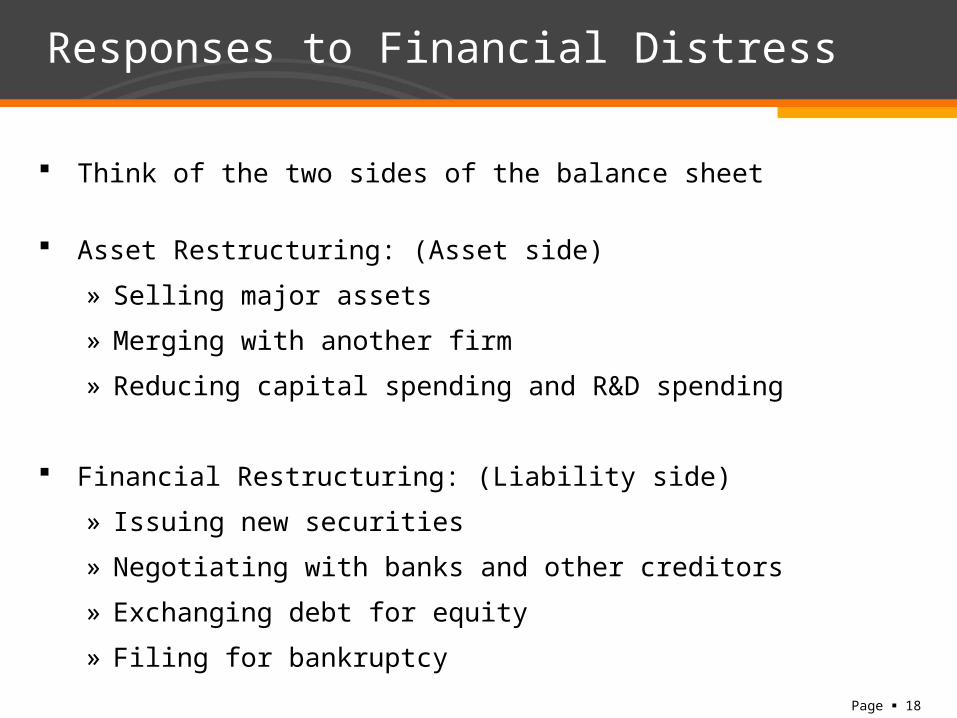

Responses to Financial Distress

Think of the two sides of the balance sheet

Asset Restructuring: (Asset side)

» Selling major assets

» Merging with another firm

» Reducing capital spending and R&D spending

Financial Restructuring: (Liability side)

» Issuing new securities

» Negotiating with banks and other creditors

» Exchanging debt for equity

» Filing for bankruptcy

Page 19

TYPES OF RISKS

Types of Risks

Page 20

Type of Risks

Capital Risk:

The risk an investor faces that he or she may lose all or part of the principal amount invested

The risk a company faces that it may lose value on its capital. The capital of a company can include equipment, factories and liquid securities

Liquidity Risk:

The risk stemming from the lack of marketability of an investment that cannot be bought or sold quickly enough to prevent or minimize a loss

Business Risk:

The risk that a company will not have adequate cash flow to meet its operating expenses

Financial Risk:

The risk that arises from use of debt in capital structure

Page 21

Type of Risks

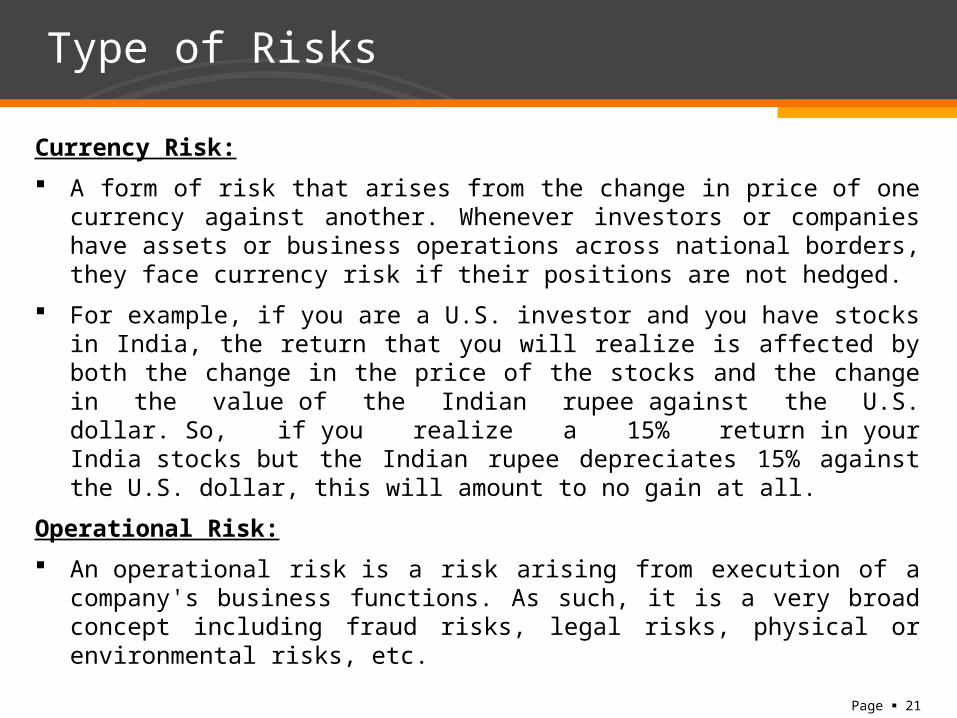

Currency Risk:

A form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

For example, if you are a U.S. investor and you have stocks in India, the return that you will realize is affected by both the change in the price of the stocks and the change in the value of the Indian rupee against the U.S. dollar. So, if you realize a 15% return in your India stocks but the Indian rupee depreciates 15% against the U.S. dollar, this will amount to no gain at all.

Operational Risk:

An operational risk is a risk arising from execution of a company's business functions. As such, it is a very broad concept including fraud risks, legal risks, physical or environmental risks, etc.

Page 22

Valuation Methods

Page 23

Definition of Valuation

In finance, valuation is the process of estimating the potential market value of a financial and real asset or liability

The value found by such method is also called “Fair value” or “intrinsic value”

Fair value, also called fair price is a concept used in finance and economics, defined as a rational and unbiased estimate of the potential market price of a good, service, or asset, taking into account two factors

Objective factors:

Acquisition/ production/ distribution costs, replacement costs, or costs of close substitutes

Actual utility at a given level of development of social productive capability

Supply vs. demand

Subjective Factors

Risk characteristics

Cost of and return on capital

Individually perceived utility

Page 24

Valuation Approaches

Assets value approach

Liquidation approach

Market comparable approach

Discounted cash flow approach

Page 25

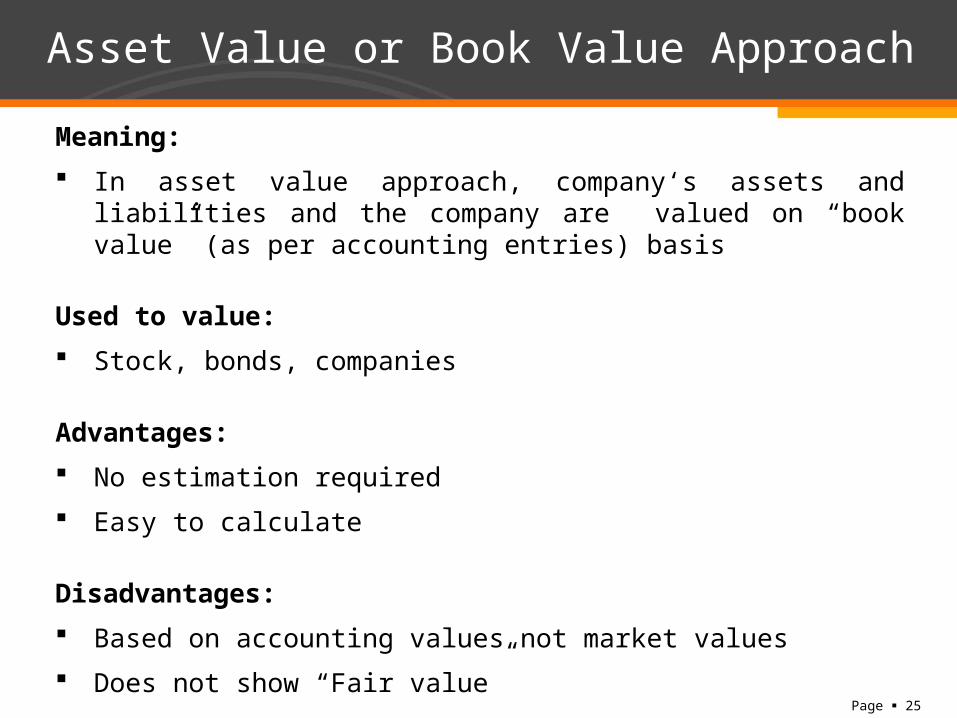

Asset Value or Book Value Approach

Meaning:

In asset value approach, company‘s assets and liabilities and the company are valued on “book value” (as per accounting entries) basis

Used to value:

Stock, bonds, companies

Advantages:

No estimation required

Easy to calculate

Disadvantages:

Based on accounting values not market values

Does not show “Fair value”

Page 26

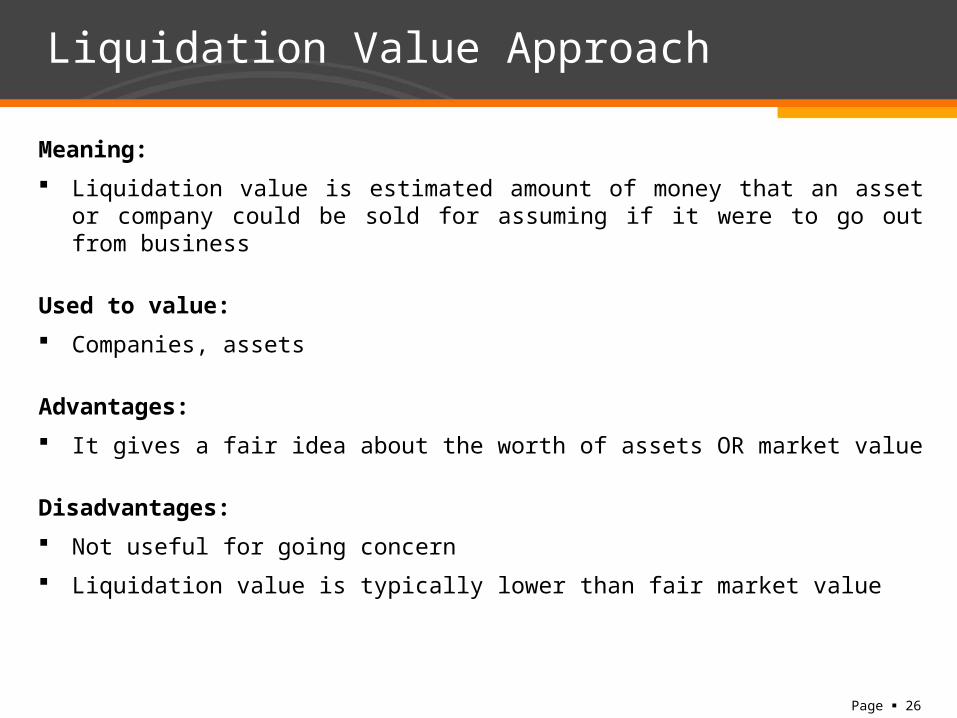

Liquidation Value Approach

Meaning:

Liquidation value is estimated amount of money that an asset or company could be sold for assuming if it were to go out from business

Used to value:

Companies, assets

Advantages:

It gives a fair idea about the worth of assets OR market value

Disadvantages:

Not useful for going concern

Liquidation value is typically lower than fair market value

Page 27

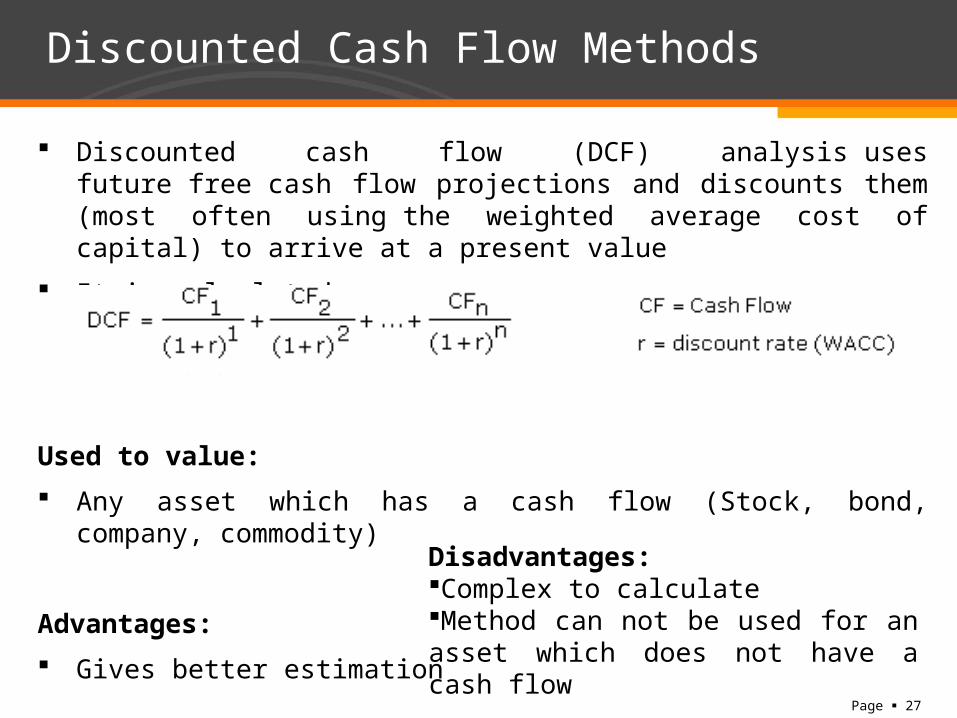

Discounted Cash Flow Methods

Discounted cash flow (DCF) analysis uses future free cash flow projections and discounts them (most often using the weighted average cost of capital) to arrive at a present value

It is calculated as:

Used to value:

Any asset which has a cash flow (Stock, bond, company, commodity)

Advantages:

Gives better estimation

Disadvantages:Complex to calculateMethod can not be used for an asset which does not have a cash flow

Page 28

Market Comparable Approach

In market comparable approach the fair value of asset is derived by using comparable multiples

For example: P/E multiple, EV/EBITDA, EV/EBIT, EV/NOPAT

Important point is to use the right multiples for valuation

Firm having same business type, capital structure, same sales volume etc.)

Used to value:

Stock, Firm

Advantages:

Ready references are available

Can be used when cash flows are not available

Disadvantages:

Difficult to find right benchmark

Page 29

In Class Exercises

If a company's current year dividend is $ 2 and it is going to increase by 20% for two years and then 10% and then will grow forever by 5%. If cost of equity is 10%, find the price of the stock?

Step 1 : Decide which model to use

Dividend discount model

Step 2: Find out the present value of all dividends

Step 3: Find out the present value of terminal value

Step 4 : Add all of them two find value of stock

Page 30

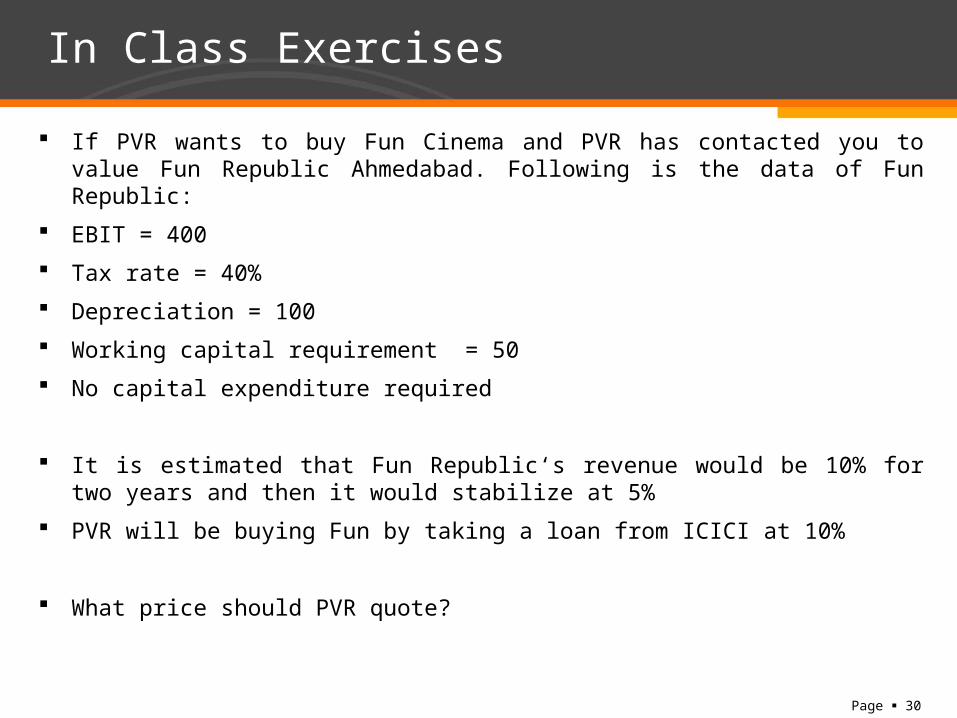

In Class Exercises

If PVR wants to buy Fun Cinema and PVR has contacted you to value Fun Republic Ahmedabad. Following is the data of Fun Republic:

EBIT = 400

Tax rate = 40%

Depreciation = 100

Working capital requirement = 50

No capital expenditure required

It is estimated that Fun Republic‘s revenue would be 10% for two years and then it would stabilize at 5%

PVR will be buying Fun by taking a loan from ICICI at 10%

What price should PVR quote?

Page 31

Example: Fun republic

Step 1: Find out FCFF for Fun Republic

FCFF = EBIT(1 - tc) + NCC - ∆WK - Capex

Step 2: Find out the discount rate

How PVR is going to finance the purchase?

Step 3: Find out FCFF1, FCFF2, FCFF3 and terminal value

Use growth rates given in the example

Step 4: Find out discounted FCFF

Step 5: Find the price PVR should quote

Page 32

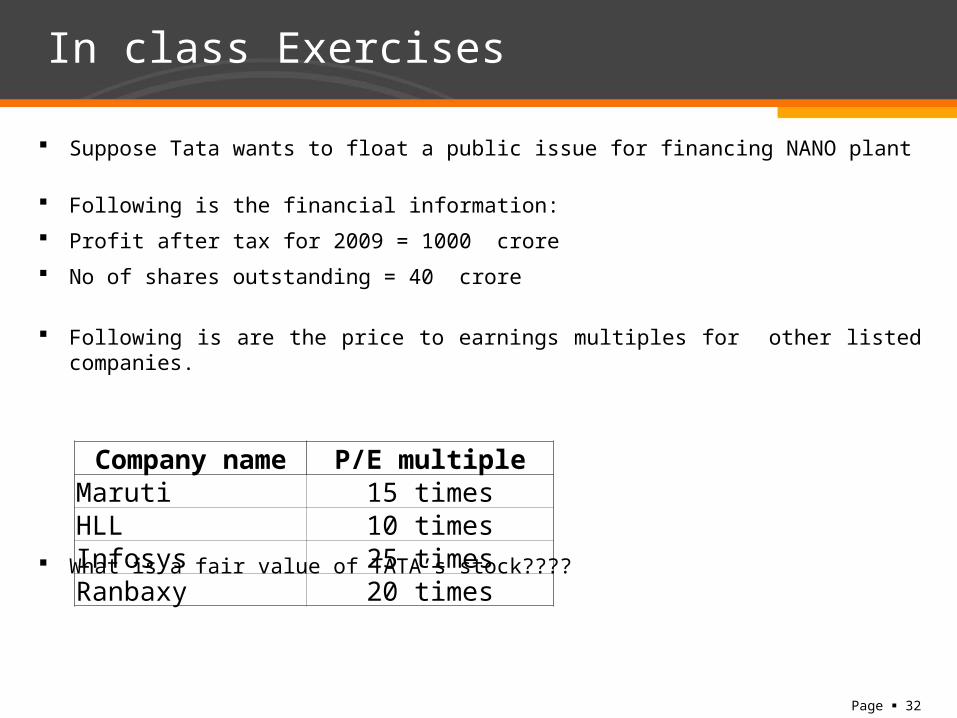

In class Exercises

Suppose Tata wants to float a public issue for financing NANO plant

Following is the financial information:

Profit after tax for 2009 = 1000 crore

No of shares outstanding = 40 crore

Following is are the price to earnings multiples for other listed companies.

What is a fair value of TATA’s stock????

Company name P/E multipleMaruti 15 timesHLL 10 timesInfosys 25 timesRanbaxy 20 times

Page 33

Example TATA

Step 1:Decide the valuation method –

Market comparables

Step 2: Decide the multiple for comparison

Price earning multiple

Step 3: Find out earning per share

Step 4: Find out comparable company

Step 5: Based on that find out the fair value

Page 34

Thank you !