investment community conference call … · hong kong dollar 7.80 7.77 ... indian rupee 43.53 44.09...

TRANSCRIPT

Baring Asset Management (Asia) Limited19th Floor, Edinburgh Tower

15 Queen’s Road Central, Hong KongTel: (852) 2841 1411Fax: (852) 2868 5296

Internet: www.baring-asset.com

THE ASIA PACIFIC FUND, INC.

Asia : Long-Term and Short-Term Market Review and Outlook

Investment Community Conference Call

www.asiapacificfund.com

September 20, 2005

1

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Table of Contents

Page

Section 1: Asian Markets Review 2 - 5

Section 2: Market Outlook

- Re-assessing The Secular Case for Asia 7 - 16

- Asia – The Short-Term View 17 - 33

Section 3: Portfolio Strategy 34 - 36

Section 1:

ASIAN MARKETS REVIEW

3

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

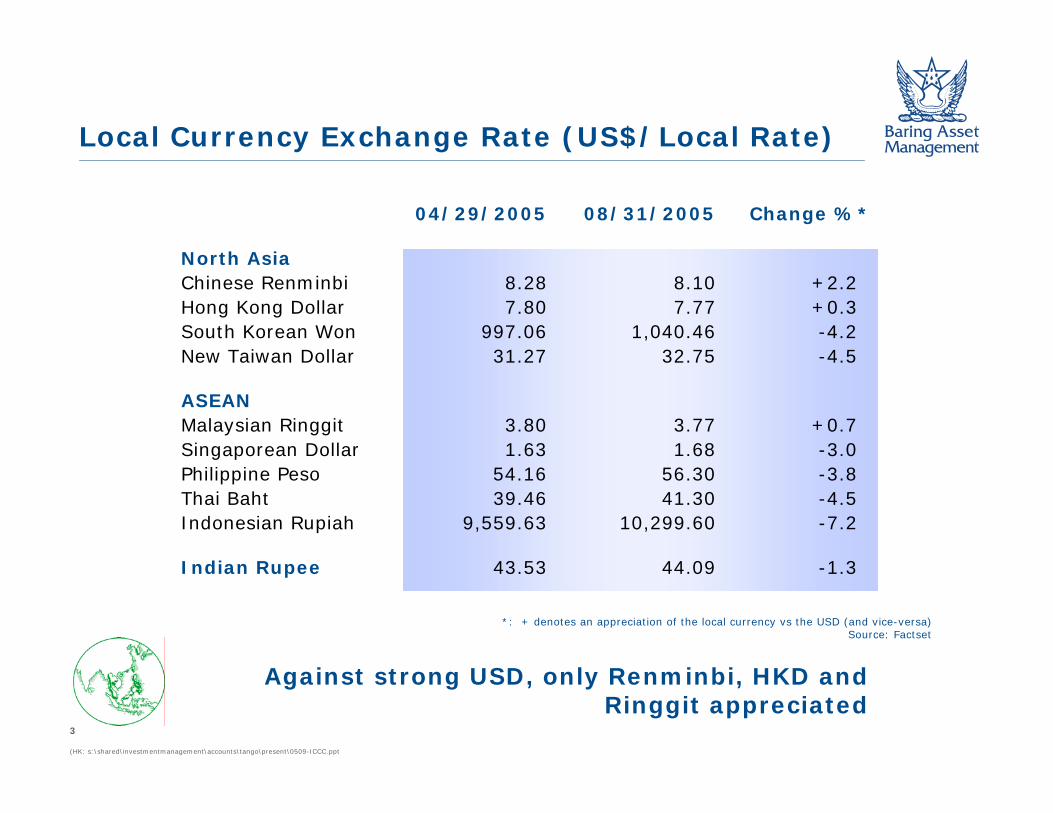

Local Currency Exchange Rate (US$/Local Rate)

04/29/2005 08/31/2005 Change %*

North AsiaChinese Renminbi 8.28 8.10 +2.2Hong Kong Dollar 7.80 7.77 +0.3South Korean Won 997.06 1,040.46 -4.2New Taiwan Dollar 31.27 32.75 -4.5

ASEANMalaysian Ringgit 3.80 3.77 +0.7Singaporean Dollar 1.63 1.68 -3.0Philippine Peso 54.16 56.30 -3.8Thai Baht 39.46 41.30 -4.5Indonesian Rupiah 9,559.63 10,299.60 -7.2

Indian Rupee 43.53 44.09 -1.3

*: + denotes an appreciation of the local currency vs the USD (and vice-versa)Source: Factset

Against strong USD, only Renminbi, HKD and Ringgit appreciated

4

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

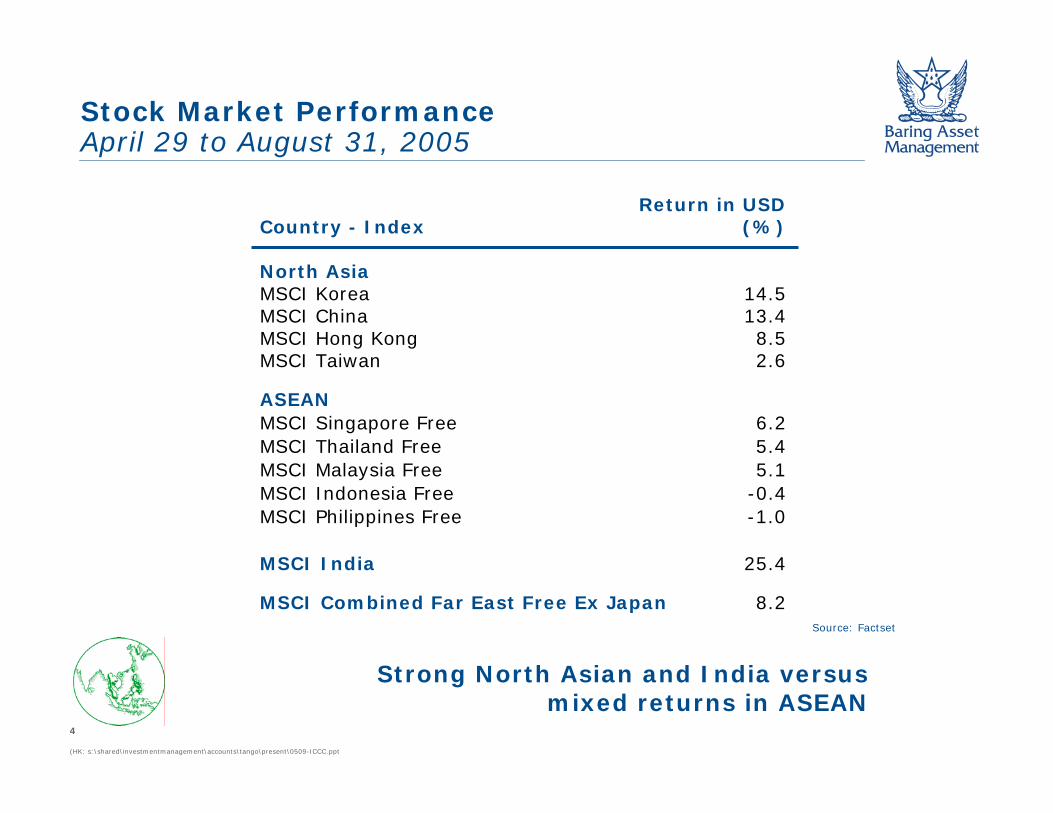

Stock Market PerformanceApril 29 to August 31, 2005

Return in USDCountry - Index (%)

North AsiaMSCI Korea 14.5MSCI China 13.4MSCI Hong Kong 8.5MSCI Taiwan 2.6

ASEANMSCI Singapore Free 6.2MSCI Thailand Free 5.4 MSCI Malaysia Free 5.1MSCI Indonesia Free -0.4MSCI Philippines Free -1.0

MSCI India 25.4

MSCI Combined Far East Free Ex Japan 8.2Source: Factset

Strong North Asian and India versusmixed returns in ASEAN

5

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

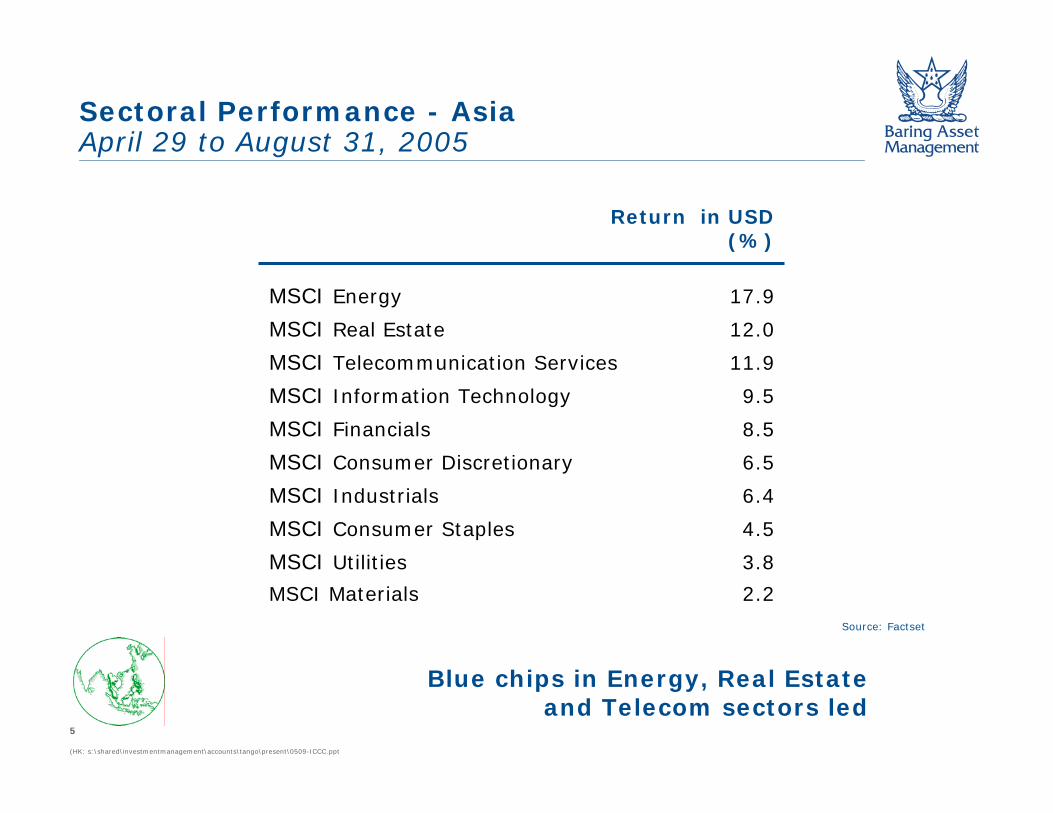

Sectoral Performance - AsiaApril 29 to August 31, 2005

Source: Factset

Return in USD(%)

MSCI Energy 17.9

MSCI Real Estate 12.0

MSCI Telecommunication Services 11.9

MSCI Information Technology 9.5

MSCI Financials 8.5

MSCI Consumer Discretionary 6.5

MSCI Industrials 6.4

MSCI Consumer Staples 4.5

MSCI Utilities 3.8

MSCI Materials 2.2

Blue chips in Energy, Real Estateand Telecom sectors led

Section 2:

MARKET OUTLOOK

Re-assessing The Secular Casefor Asia

8

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Asia - The Secular Case remains intact

Re-rating of Asian equities is set to continue on superior economic growth and higher corporate returns

Favorable demographics and rising credit culture lead to stronger domestic consumption

Corporate ROE has improved thanks to better supply side discipline and deleveraging

Asian currencies remain undervalued and Asian equities are under-owned

A more sustainable earnings growth with less cyclicality will bethe major driver for re-rating

Source: Baring Asset Management, Sept 2005

Asia remains an attractive strategic investment

9

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

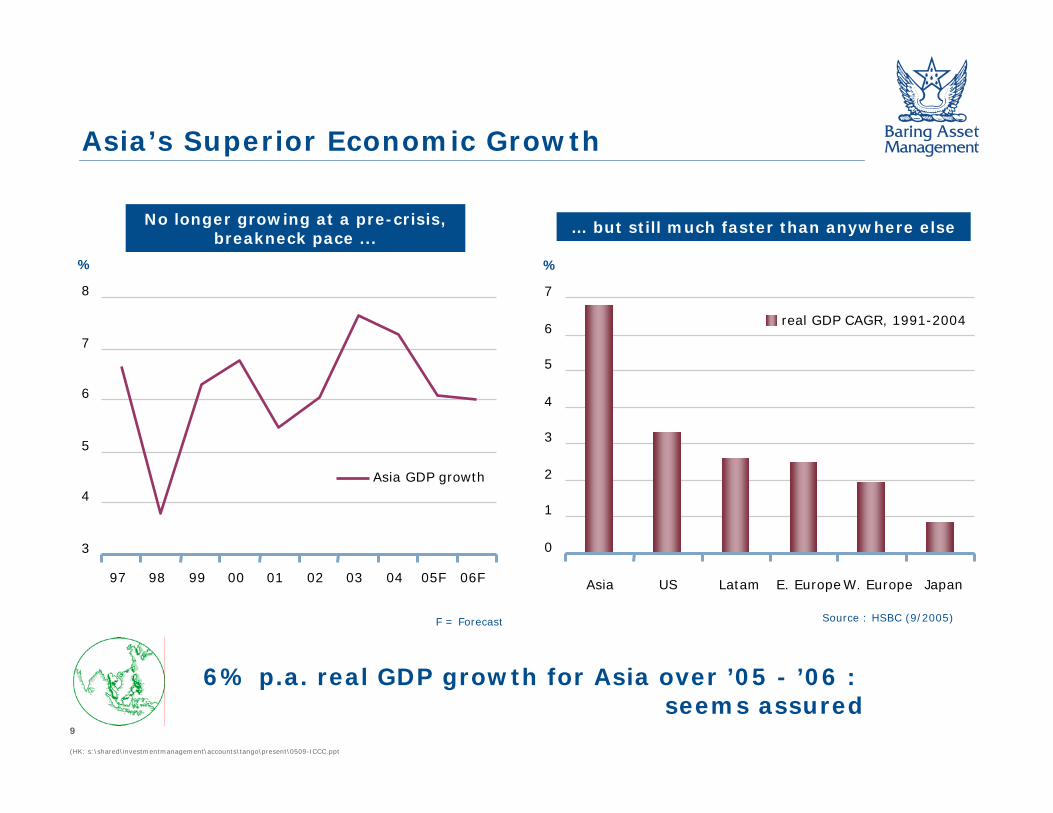

No longer growing at a pre-crisis, breakneck pace ...

Source : HSBC (9/2005)

… but still much faster than anywhere else

6% p.a. real GDP growth for Asia over ’05 - ’06 : seems assured

Asia’s Superior Economic Growth

F = Forecast

3

4

5

6

7

8

97 98 99 00 01 02 03 04 05F 06F

Asia GDP growth

%

0

1

2

3

4

5

6

7

Asia US Latam E. EuropeW. Europe Japan

real GDP CAGR, 1991-2004

%

10

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

A high proportion of economically active citizens ...

… can fund much higher levels of borrowing

Domestic consumption : solid long-term trend

Consumption - Supported by Demographics and a Rising Credit Culture

% of population aged 15-39 Household loans as % of GDP

Source : HSBC (9/2005)

20

25

30

35

40

45

Chin

a

India

Indones

ia

Kore

a

Mal

aysi

a

Thai

land

US

UK

Japan

2005 2015

0

10

20

30

40

50

60

70

80

90

100

SG US JP KR HK MY TW TH ID PH

11

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

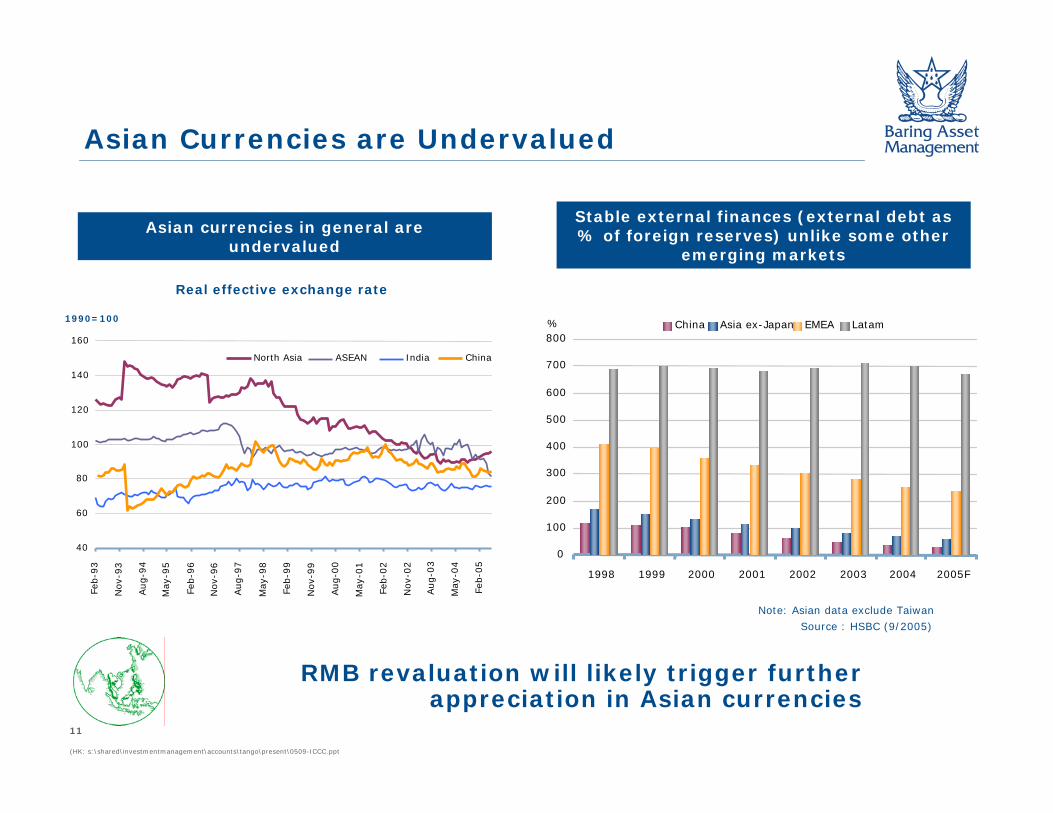

Asian currencies in general are undervalued

Stable external finances (external debt as % of foreign reserves) unlike some other

emerging markets

Note: Asian data exclude Taiwan

Real effective exchange rate

Asian Currencies are Undervalued

Source : HSBC (9/2005)

RMB revaluation will likely trigger further appreciation in Asian currencies

40

60

80

100

120

140

160

Feb-9

3

Nov-

93

Aug-9

4

May

-95

Feb-9

6

Nov-

96

Aug-9

7

May

-98

Feb-9

9

Nov-

99

Aug-0

0

May

-01

Feb-0

2

Nov-

02

Aug-0

3

May

-04

Feb-0

5

North Asia ASEAN India China

1990=100

0

100

200

300

400

500

600

700

800

1998 1999 2000 2001 2002 2003 2004 2005F

China Asia ex-Japan EMEA Latam%

12

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Credit upgrades as % of all changes -only Asia is collecting net credit upgrades

Asia’s average ROE vs COE - finally,a value-creating Asia

Clear improvement in recent two years: a sign of secular change?

Note: Data compiled using credit changes made by all the major global agencies. Note: Average Asia-wide ROEs and COEs are calculated using year-end neutral weights.

Post-Crisis TransformationA Value-Creating Asia

Source : HSBC (9/2005)

0

2

4

6

8

10

12

14

16

18

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

ROE COE

%

0

10

20

30

40

50

60

70

80

90

01/96 01/98 01/00 01/02 01/04

Asia ex-Japan World excluding Asia

13

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

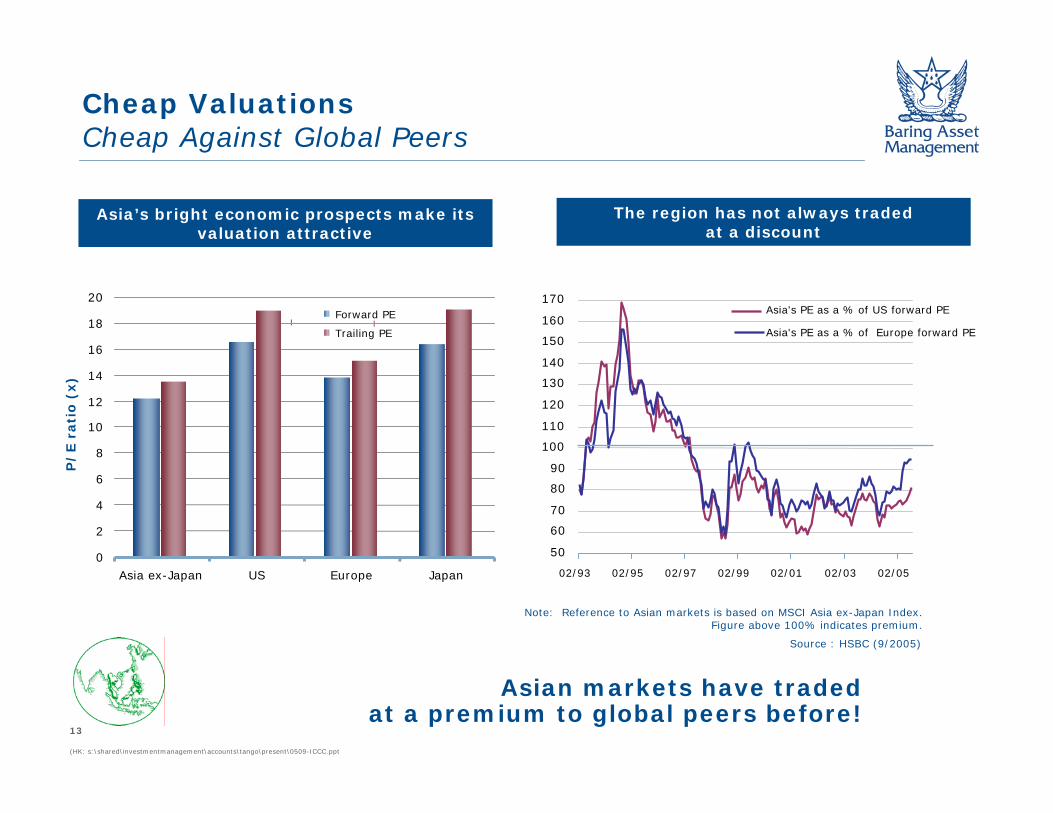

Asia’s bright economic prospects make its valuation attractive

The region has not always traded at a discount

Asian markets have tradedat a premium to global peers before!

Note: Reference to Asian markets is based on MSCI Asia ex-Japan Index.Figure above 100% indicates premium.

Cheap Valuations Cheap Against Global Peers

Source : HSBC (9/2005)

50

60

70

80

90

100

110

120

130

140

150

160

170

02/93 02/95 02/97 02/99 02/01 02/03 02/05

Asia's PE as a % of US forward PE

Asia's PE as a % of Europe forward PE

0

2

4

6

8

10

12

14

16

18

20

Asia ex-Japan US Europe Japan

P/

E r

ati

o (

x)

Forward PE

Trailing PE

14

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

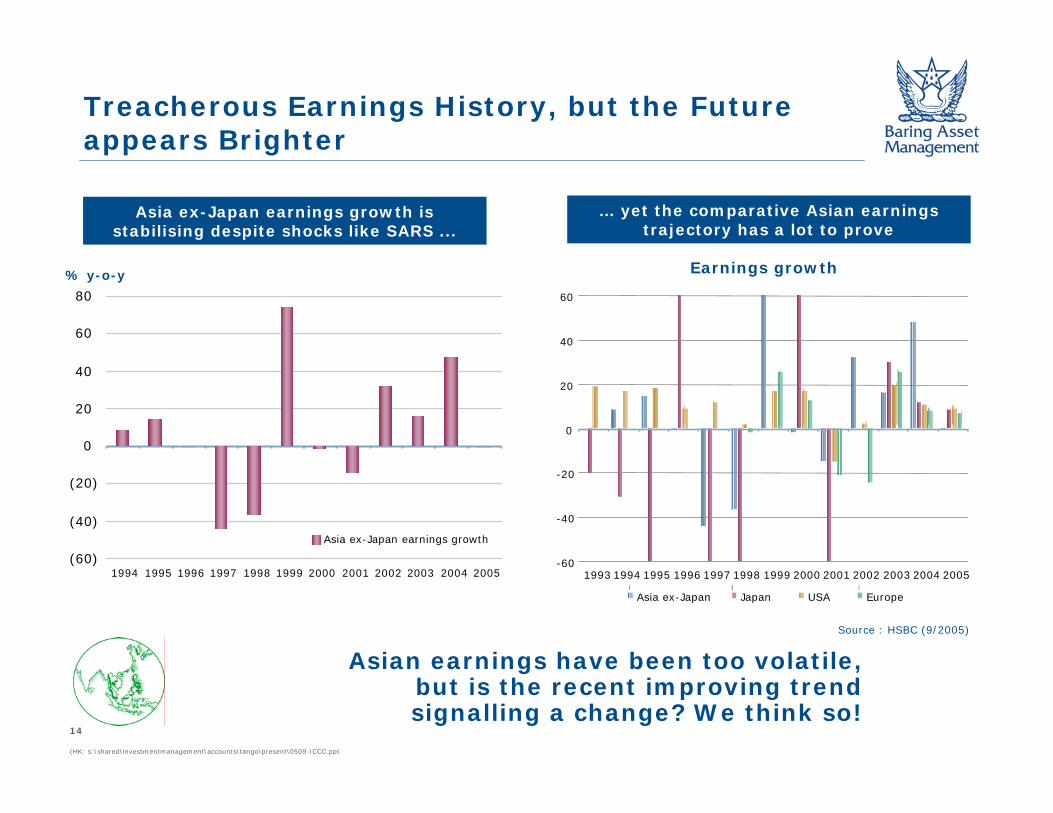

Asia ex-Japan earnings growth is stabilising despite shocks like SARS ...

… yet the comparative Asian earnings trajectory has a lot to prove

Asian earnings have been too volatile,but is the recent improving trendsignalling a change? We think so!

Treacherous Earnings History, but the Future appears Brighter

Source : HSBC (9/2005)

Earnings growth

-60

-40

-20

0

20

40

60

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Asia ex-Japan Japan USA Europe

(60)

(40)

(20)

0

20

40

60

80

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Asia ex-Japan earnings growth

% y-o-y

15

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

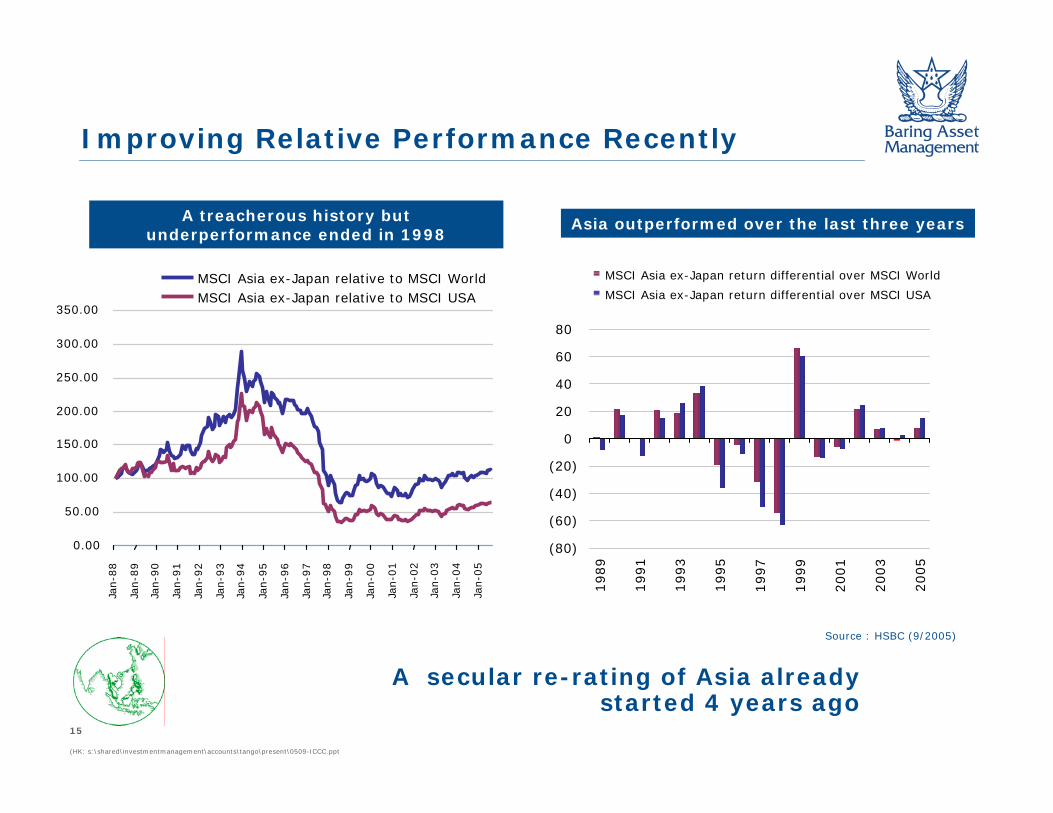

A treacherous history but underperformance ended in 1998

Asia outperformed over the last three years

A secular re-rating of Asia alreadystarted 4 years ago

Improving Relative Performance Recently

Source : HSBC (9/2005)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Jan-8

8

Jan-8

9

Jan-9

0

Jan-9

1

Jan-9

2

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

MSCI Asia ex-Japan relative to MSCI WorldMSCI Asia ex-Japan relative to MSCI USA

MSCI Asia ex-Japan return differential over MSCI World

MSCI Asia ex-Japan return differential over MSCI USA

(80)

(60)

(40)

(20)

0

20

40

60

80

1989

1991

1993

1995

1997

1999

2001

2003

2005

16

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Global investors remain massively under-invested in the region -

as evidenced by neutral weights

Domestic investors still hold a lot in low-yielding deposits

Ample room for re-rating if local and global investorsthink that earnings growth is sustainable

Under-ownedCompared to Its Economic Size

Source : HSBC (9/2005)

Share of world GDP (in PPP)

Share of world GDP (in USD bn)

Weight in MSCI AC World index

0

50

100

150

200

250

CN TW ID KR IN MY PH HK SG TH

%Market capitalisation to deposits

05

101520253035404550

Asia ex-Japan United States European Union Japan Others

Asia – The Short-Term View

18

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

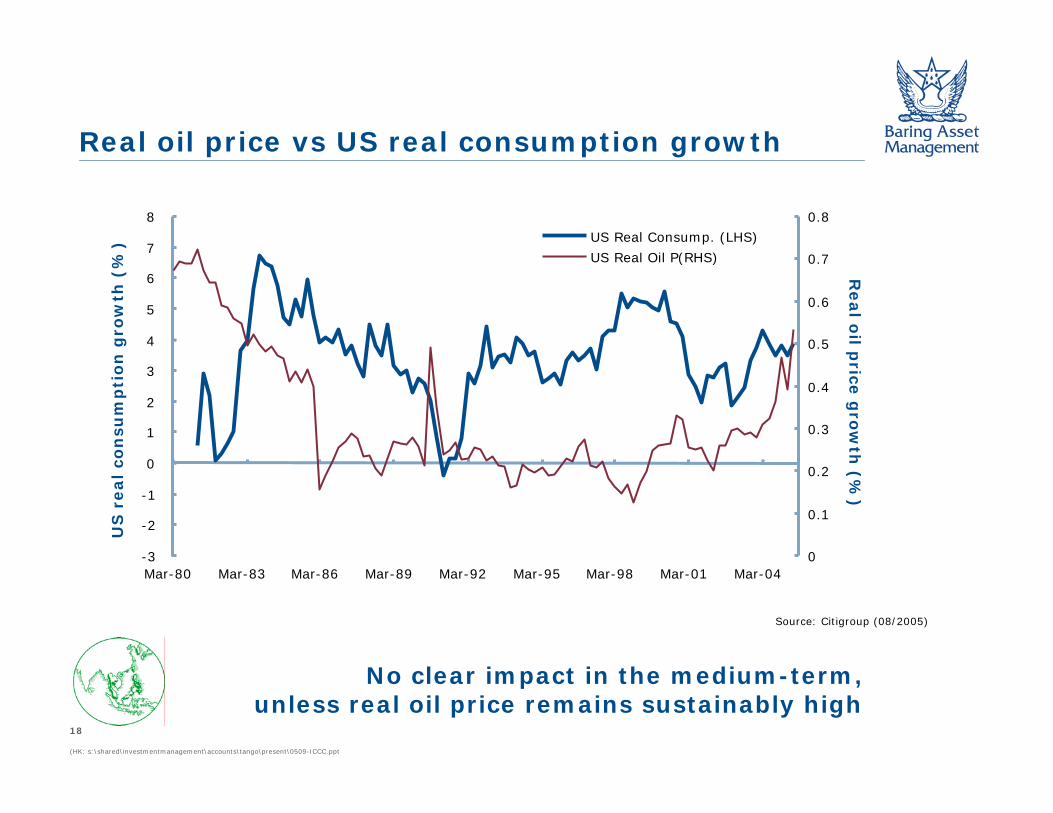

Real oil price vs US real consumption growth

No clear impact in the medium-term,unless real oil price remains sustainably high

Source: Citigroup (08/2005)

-3

-2

-1

0

1

2

3

4

5

6

7

8

Mar-80 Mar-83 Mar-86 Mar-89 Mar-92 Mar-95 Mar-98 Mar-01 Mar-040

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

US Real Consump. (LHS)

US Real Oil P(RHS)

US

real

con

sum

pti

on

gro

wth

(%

)

Real o

il price

gro

wth

(%)

19

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

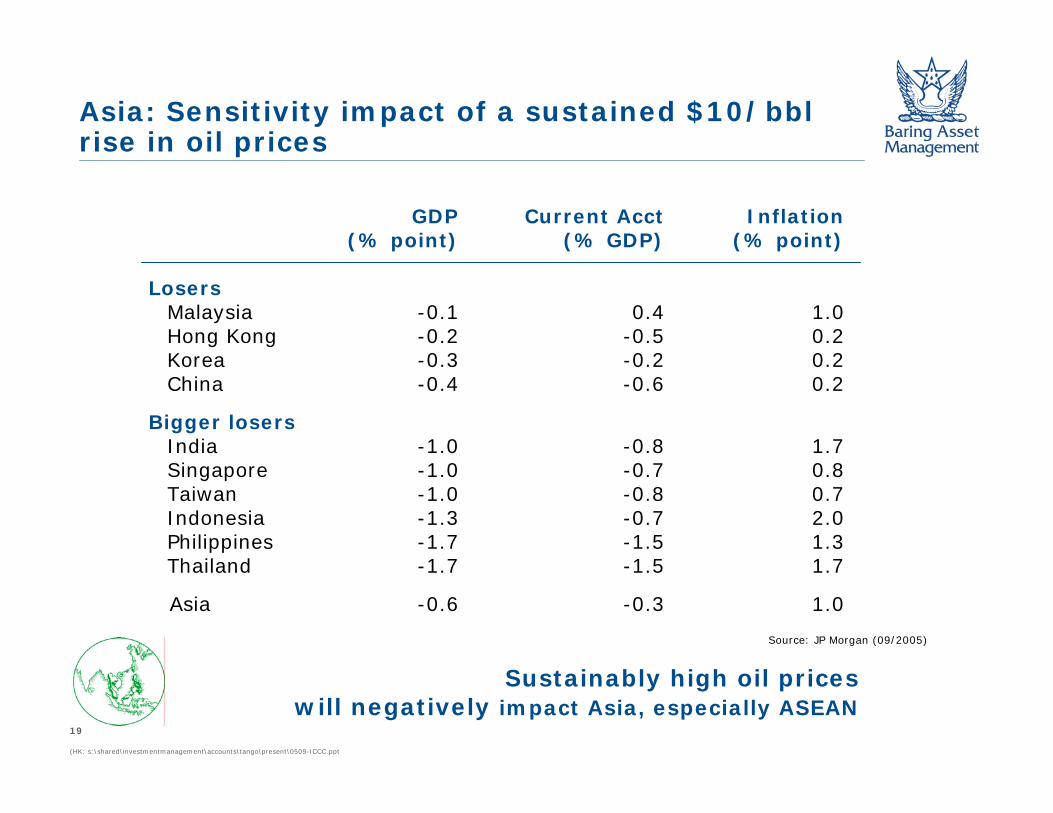

Asia: Sensitivity impact of a sustained $10/bbl rise in oil prices

GDP Current Acct Inflation(% point) (% GDP) (% point)

LosersMalaysia -0.1 0.4 1.0Hong Kong -0.2 -0.5 0.2Korea -0.3 -0.2 0.2China -0.4 -0.6 0.2

Bigger losersIndia -1.0 -0.8 1.7Singapore -1.0 -0.7 0.8Taiwan -1.0 -0.8 0.7Indonesia -1.3 -0.7 2.0Philippines -1.7 -1.5 1.3Thailand -1.7 -1.5 1.7

Asia -0.6 -0.3 1.0

Sustainably high oil priceswill negatively impact Asia, especially ASEAN

Source: JP Morgan (09/2005)

20

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

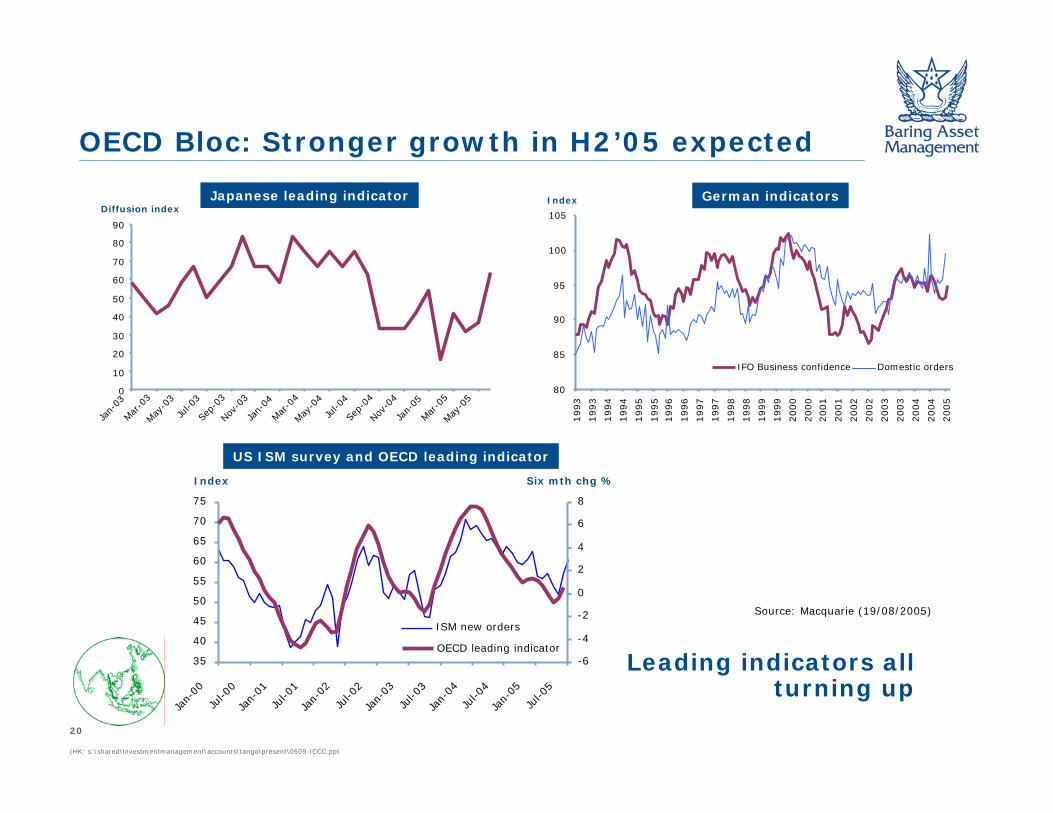

OECD Bloc: Stronger growth in H2’05 expected

German indicators

US ISM survey and OECD leading indicator

Japanese leading indicator

Source: Macquarie (19/08/2005)

Leading indicators all turning up

0

10

20

30

40

50

60

70

80

90

Jan-

03Mar

-03

May-0

3Ju

l-03

Sep-

03Nov

-03

Jan-

04Mar

-04

May-0

4Ju

l-04

Sep-

04Nov

-04

Jan-

05Mar

-05

May-0

5

Diffusion index

80

85

90

95

100

105

1993

1993

1994

1994

1995

1995

1996

1996

1997

1997

1998

1998

1999

1999

2000

2000

2001

2001

2002

2002

2003

2003

2004

2004

2005

IFO Business confidence Domestic orders

Index

35

40

45

50

55

60

65

70

75

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

-6

-4

-2

0

2

4

6

8

ISM new orders

OECD leading indicator

Index Six mth chg %

21

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

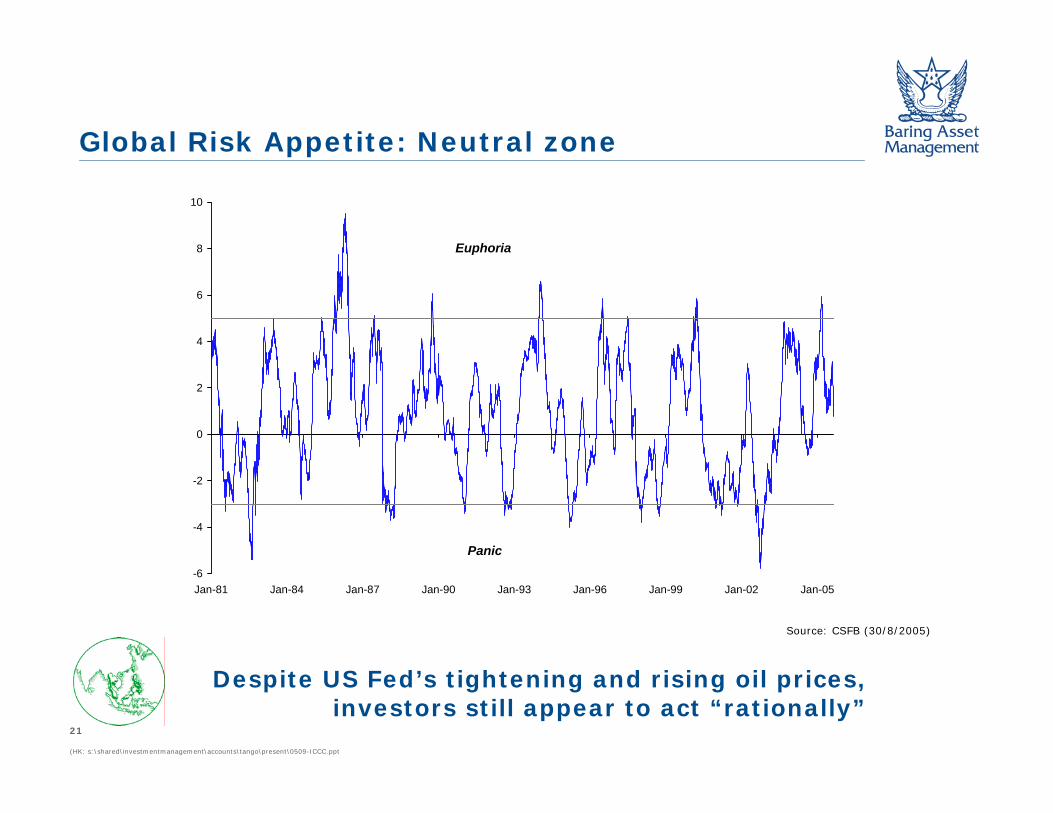

Global Risk Appetite: Neutral zone

Despite US Fed’s tightening and rising oil prices, investors still appear to act “rationally”

Source: CSFB (30/8/2005)

-6

-4

-2

0

2

4

6

8

10

Jan-81 Jan-84 Jan-87 Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05

Euphoria

Panic

22

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

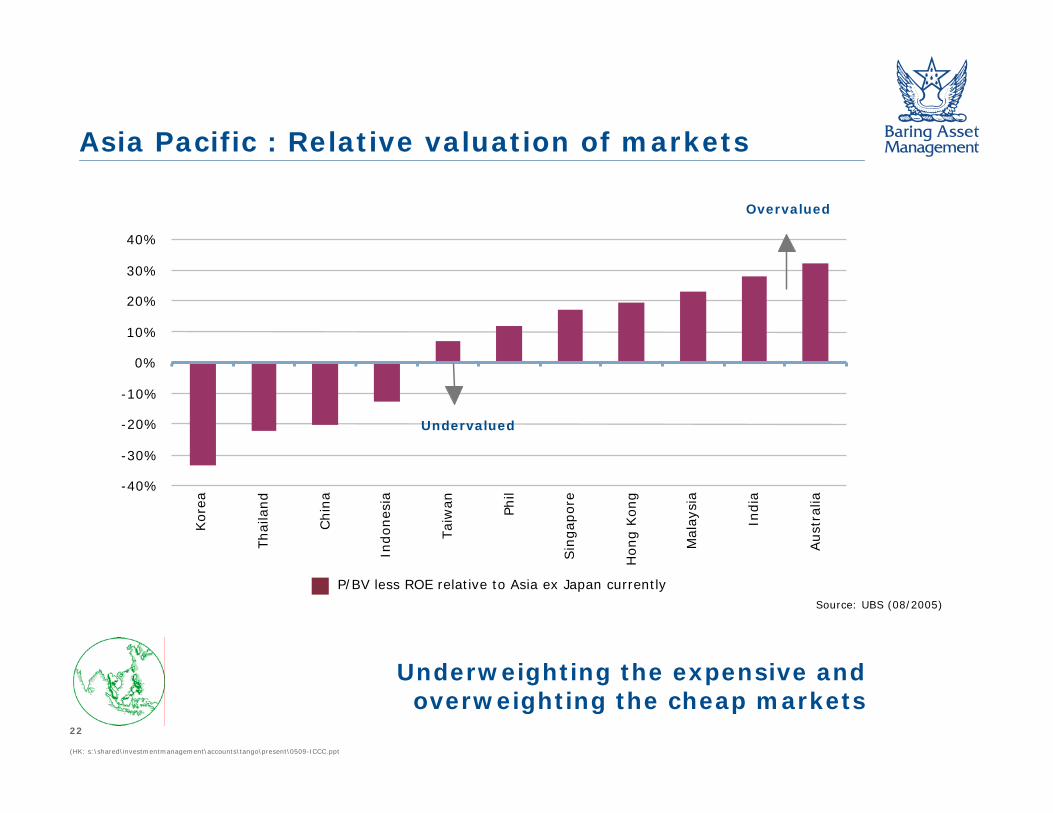

Asia Pacific : Relative valuation of markets

Underweighting the expensive and overweighting the cheap markets

Source: UBS (08/2005)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Kore

a

Thai

land

Chin

a

Indones

ia

Tai

wan Phil

Sin

gap

ore

Hong K

ong

Mal

aysi

a

India

Aust

ralia

Undervalued

Overvalued

P/BV less ROE relative to Asia ex Japan currently

23

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

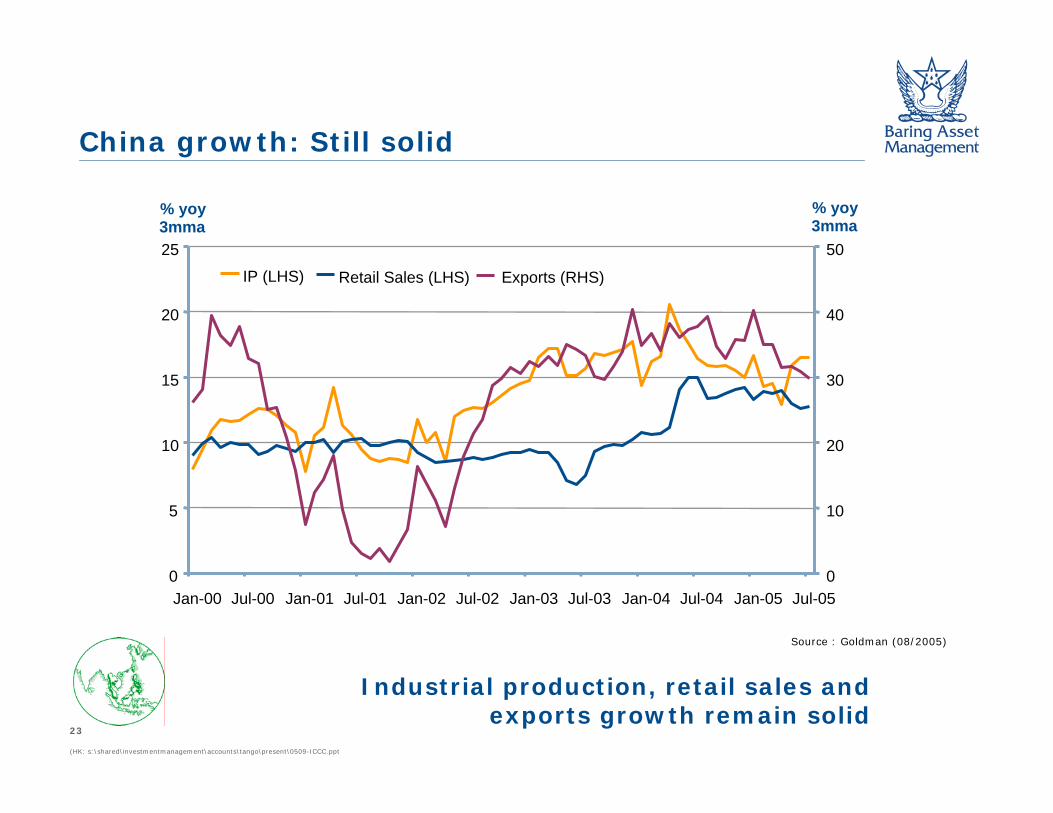

China growth: Still solid

Source : Goldman (08/2005)

Industrial production, retail sales and exports growth remain solid

0

5

10

15

20

25

Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-050

10

20

30

40

50

IP (LHS) Retail Sales (LHS) Exports (RHS)

% yoy3mma

% yoy3mma

24

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

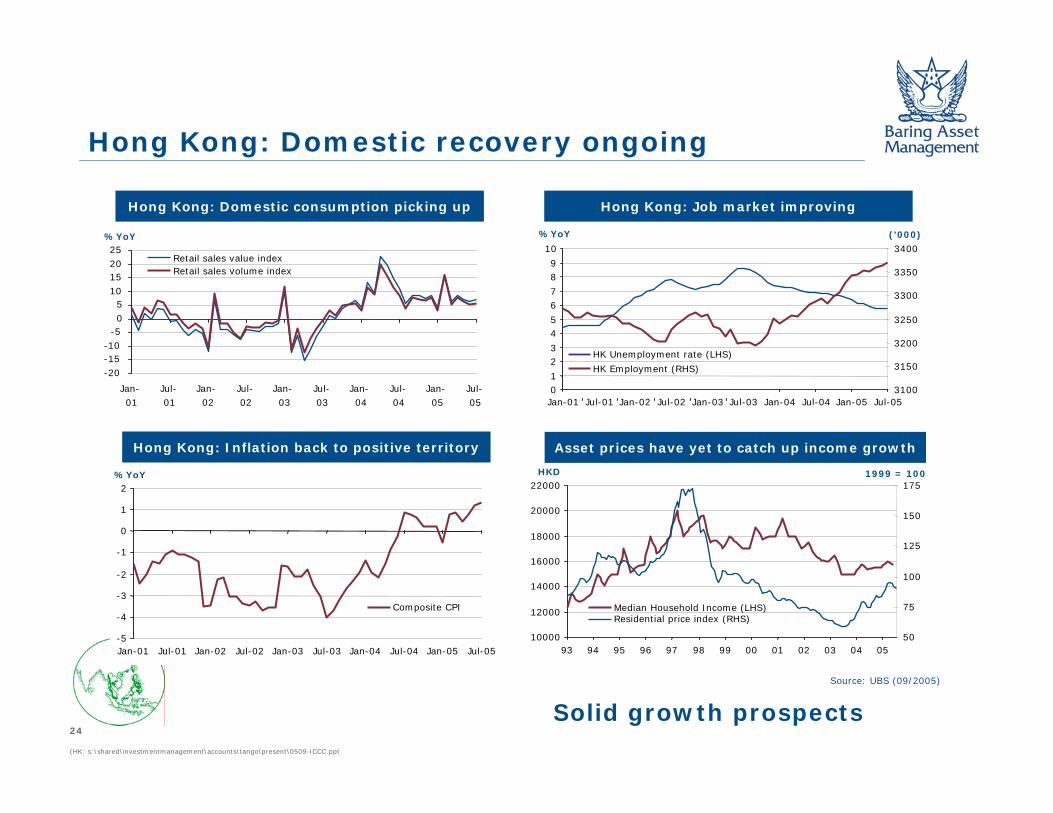

Hong Kong: Domestic recovery ongoing

Hong Kong: Domestic consumption picking up Hong Kong: Job market improving

Hong Kong: Inflation back to positive territory Asset prices have yet to catch up income growth

Source: UBS (09/2005)

-20-15-10

-505

10152025

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Retail sales value indexRetail sales volume index

%YoY

01

23

45

67

89

10

Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-053100

3150

3200

3250

3300

3350

3400

HK Unemployment rate (LHS)

HK Employment (RHS)

%YoY ('000)

10000

12000

14000

16000

18000

20000

22000

93 94 95 96 97 98 99 00 01 02 03 04 0550

75

100

125

150

175

Median Household Income (LHS)Residential price index (RHS)

HKD 1999 = 100

-5

-4

-3

-2

-1

0

1

2

Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05

Composite CPI

%YoY

Solid growth prospects

25

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Hong Kong: Property stocks to benefit from Reflation

Source: MSDW (9/2005)

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

0591 92 93 94 95 96 97 98 99 00 01 02 03 04

Property Investors Property Developers

Discount

Premium

Sep 11Asian

Financial Crisis

Maximum bullish 1993

Peak of bull market

Fed massive interest rate

easing

SARS

Mexican Crisis

China's austerity

NAV expansion

Premium/Discount to Net Asset Value

More upside in property stocks

26

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

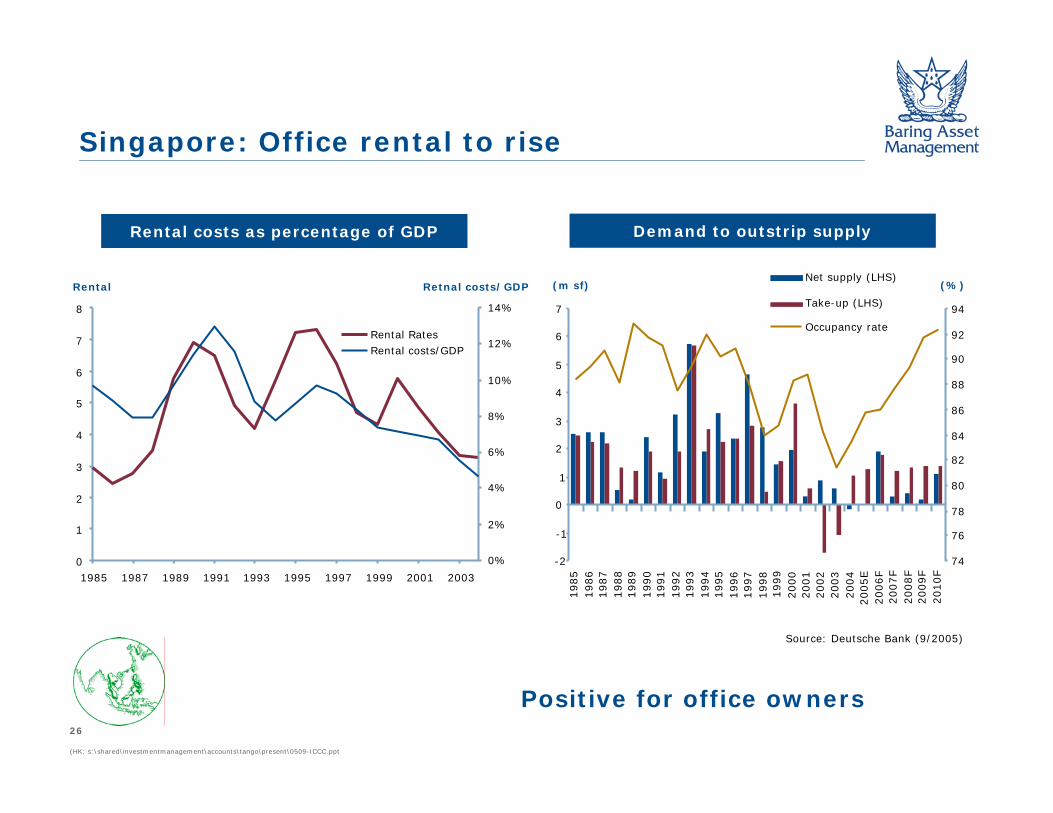

Singapore: Office rental to rise

Positive for office owners

Source: Deutsche Bank (9/2005)

0

1

2

3

4

5

6

7

8

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

0%

2%

4%

6%

8%

10%

12%

14%

Rental RatesRental costs/GDP

Rental Retnal costs/GDP

-2

-1

1

0

2

3

4

5

6

7

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005E

2006F

2007F

2008F

2009F

2010F

74

76

78

80

82

84

86

88

90

92

94

Net supply (LHS)

Take-up (LHS)

Occupancy rate

(m sf) (%)

Rental costs as percentage of GDP Demand to outstrip supply

27

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Taiwan: Undiscounted reflation story

Sinyi Housing Price index Transaction volume index- Taiwan

Cross-strait relation improvements provide trigger for Taiwan re-rating

Source: J P Morgan (9/2005)

60

70

80

90

100

110

120

130

140

3Q91

2Q92

1Q93

4Q93

3Q94

2Q95

1Q96

4Q96

3Q97

2Q98

1Q99

4Q99

3Q00

2Q01

1Q02

4Q02

3Q03

2Q04

1Q05

Taipei City Taichung Kaoshiung Taiwan

0

200

400

600

800

1000

1200

1400

1Q96

3Q96

1Q97

3Q97

1Q98

3Q98

1Q99

3Q99

1Q00

3Q00

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

80

85

90

95

100

105

110

115

120Cathay 30-day Transaction Volume Index- LHS

Cathay Housing Price Index- RHS

28

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Asian Technology: Still offering value

Source: UBS (9/2005)

A forecast upturn in Asian Tech earningsin H2 ’05 will further boost the rally in Tech;

Taiwan is the major beneficiary

1.93X Oct 2.08XSep

1.9 Apr 03 2.2X

0

1

2

3

4

5

6

7

8

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05

PB

V (

x)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

RO

E (%

)

PB (RHS) ROE (LHS)

29

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

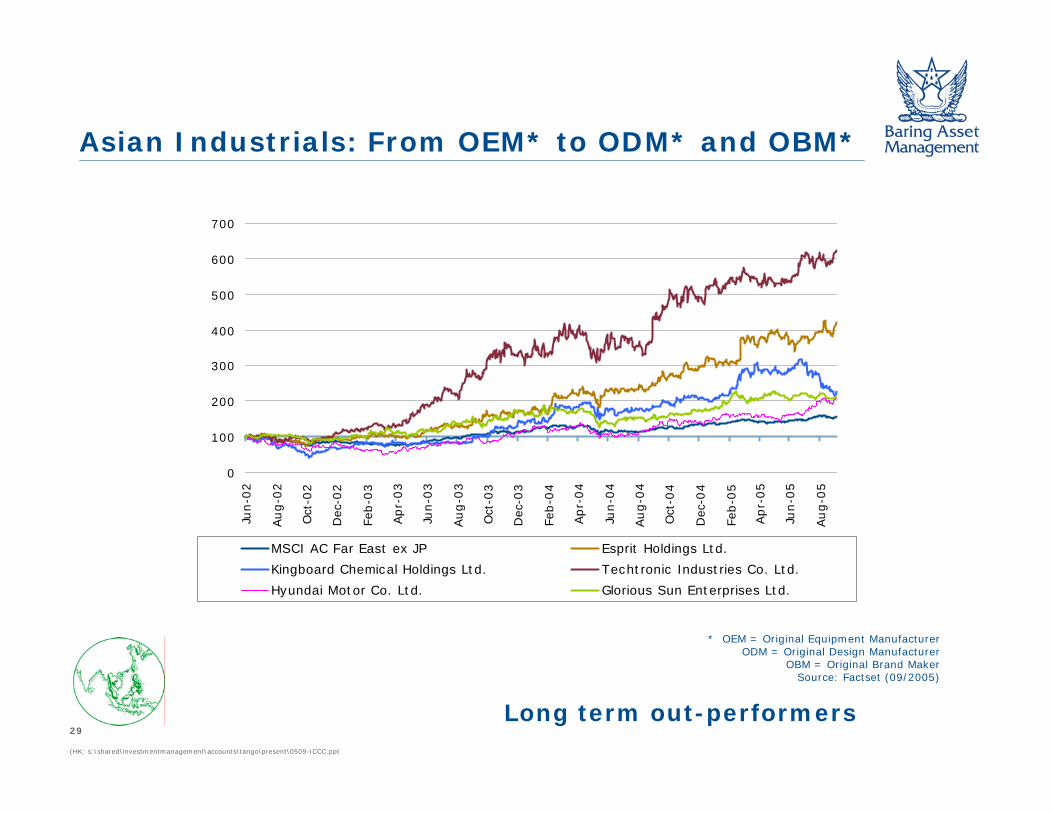

Asian Industrials: From OEM* to ODM* and OBM*

Long term out-performers

* OEM = Original Equipment ManufacturerODM = Original Design Manufacturer

OBM = Original Brand MakerSource: Factset (09/2005)

0

100

200

300

400

500

600

700

Jun-0

2

Aug-0

2

Oct

-02

Dec

-02

Feb-0

3

Apr-

03

Jun-0

3

Aug-0

3

Oct

-03

Dec

-03

Feb-0

4

Apr-

04

Jun-0

4

Aug-0

4

Oct

-04

Dec

-04

Feb-0

5

Apr-

05

Jun-0

5

Aug-0

5

MSCI AC Far East ex JP Esprit Holdings Ltd.

Kingboard Chemical Holdings Ltd. Techtronic Industries Co. Ltd.

Hyundai Motor Co. Ltd. Glorious Sun Enterprises Ltd.

30

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

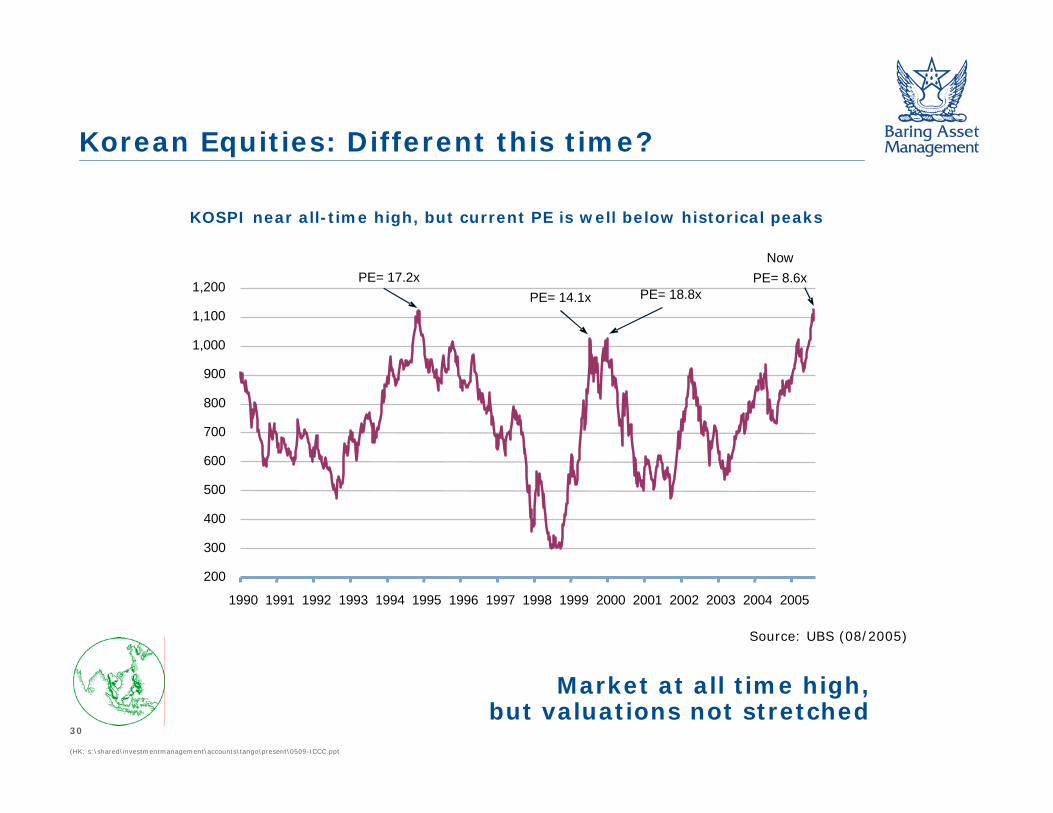

Korean Equities: Different this time?

KOSPI near all-time high, but current PE is well below historical peaks

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

PE= 17.2xPE= 14.1x PE= 18.8x

NowPE= 8.6x

Source: UBS (08/2005)

Market at all time high,but valuations not stretched

31

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

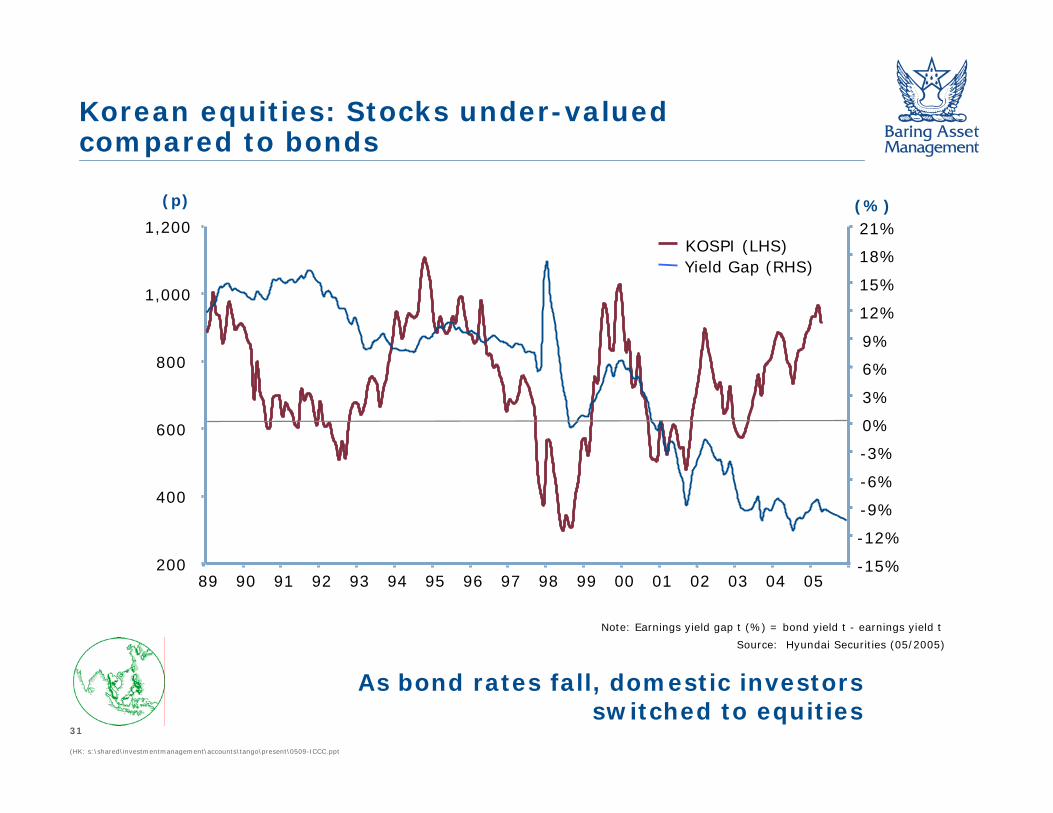

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

KOSPI (LHS)Yield Gap (RHS)

200

400

600

800

1,000

1,200

(p)

-15%

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

21%(%)

Source: Hyundai Securities (05/2005)

Note: Earnings yield gap t (%) = bond yield t - earnings yield t

Korean equities: Stocks under-valued compared to bonds

As bond rates fall, domestic investorsswitched to equities

32

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Korean Liquidity surprise: Strong domestic fund flows

Monthly net inflow into equity fund Monthly net inflow into equity fund

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

Jan-0

4

Feb-0

4

Apr-

04

May

-04

Jun-0

4

Aug-0

4

Sep

t-04

Nov-

04

Dec

-04

Jan-0

5

Mar

-05

May

-05

(Won Bn)

Balance of Equity Funds

Source : UBS (08/2005)

Domestic participation isa necessary condition for market re-rating

-1,000-800-600

-400-200

0200

400600

8001,000

Jan-

04

Feb -

04

Mar

-04

Apr-04

May

-04

Jun -

04

Jul -0

4

Aug -

04

Sep

-04

Oct

-04

Nov-

04

Dec

- 04

Jan-

05

Feb-

05

Mar

- 05

Apr-05

May

- 05

Jun-

05

Jul -0

5

Aug -

05

Monthly Net inflow of Equity fund

(Won bn)

10 days Aug MTD

33

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Conclusions

Macro

Strong economic growth

Favourable demographics

Recovering domestic consumption

Undervalued currencies

Micro

Cheap stock market valuations

Re-rating

Asia is attractive from both a short-term andlong-term perspectives

Section 3:

Portfolio Strategy

35

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Risks

Markets’ volatility likely to remain

Oil prices: will they rise to and stay sustainably above US$70/bbl?

Will the US Federal Reserve continue to tighten past the 4% rate?

How severe is the lagged impact of high oil prices and Fed tightening on US and global growth in 2006?

36

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Concluding Remarks

Expect trend growth in the key economies of the US and China

Asian equities remain attractive

Strategy to focus on domestic reflation and selective industrials and technology names

Planning for a more defensive market environment in 2006

37

(HK: s:\shared\investmentmanagement\accounts\tango\present\0509-ICCC.ppt

Regulatory Disclosure

This document is provided as a service to professional investors/advisers. It is issued in the United Kingdom by Baring Asset Management Limited and/or by its investment adviser affiliates in other jurisdictions. The affiliate serving as the Asia Pacific Fund’s investment adviser is Baring Asset Management (Asia) Limited. In the United Kingdom this document is issued only to persons falling within a permitted category under (i) the FSA’s rules made under section 238(5) of the Financial Services and Markets Act 2000 and (ii) the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001.

This is not an offer nor a solicitation to buy or sell any investment referred to in this document. Baring Asset Management group companies, their affiliates and/or their directors, officers and employees may own or have positions in any investment mentioned herein or any investment related thereto and from time to time add to or dispose of any such investment. The contents of this document are based upon sources of information believed to be reliable but no guarantee, warranty or representation, express or implied, is given as to their accuracy or completeness. This document may include forward-looking statements, which are based upon our current opinions, expectations and projections as of the date on the cover hereof. We undertake no obligation to update or revise any forward-looking statements. Actual results could differ materially from those anticipated in the forward-looking statements. The value of any investments and any income generated may go down as well as up and is not guaranteed. Past performance will not necessarily be repeated. Changes in rates of exchange may have an adverse effect on the value, price or income of an investment. There are additional risks associated with investments (made directly or through investment vehicles which invest) in emerging or developing markets. Compensation arrangements under the Financial Services and Markets Act 2000 of the United Kingdom will not be available.

Private investors in the Company referred to herein should obtain their own independent financial advice before making investments. This document must not be relied on for purposes of any investment decisions. Before investing in the Company, we recommend that all relevant documents, such as reports and accounts and prospectus should be read, which specify the particular risks associated with investment in the Company, together with any specific restrictions applying and the basis of dealing. The Company may not be available for investment in all jurisdictions. There may also be prohibitions or restrictions on distribution of this document and other material relating to the Company and accordingly recipients of any such documents are advised to inform themselves about and to observe any such restrictions.

Complied (Boston): September 15, 2005