investment in turkey

DESCRIPTION

Turkey Investment, Automotive Sector turkey, Growing turkey,TRANSCRIPT

PROJECT International Marketing | Lalit Sharma ( Roll No 13)

Automotive Industry – Upcoming Opportunity in TURKEY

TURKEY IS ONE OF THE FASTEST GROWING ECONOMIES IN THE WORLD

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 2

TABLE OF CONTENTS

I. COUNTRY PROFILE: INTRODUCING TURKEY __________________________04

1.1 HISTORY, GEOGRAPHY, POPULATION __________________________________ 04

1.2 FUTURE PROSPECTS ___________________________________________________ 05

II. PESTLE ANALYSIS _____________________________________________________06

2.1 Political _________________________________________________________________06

2.2 Economic _______________________________________________________________07

2.3 Social___________________________________________________________________10

2.4 Technological ____________________________________________________________10

2.5 Legal___________________________________________________________________12

2.6 Environmental____________________________________________________________13

III. WHY INVEST IN TURKEY? _____________________________________________11

10 Reasons to Invest in Turkey ____________________________________________15

IV. TURKEY-INDIA. ECONOMIC RELATIONS_______________________________17

India, Turkey negotiating free trade accord___________________________________18

India-Turkey Relation ___________________________________________________18

India, Turkey can have economic strategic partnership__________________________18

India, Turkey set up study group for FTA____________________________________18

Indian Oil Corp Ltd Turkey plan put on backburner____________________________19

V. ENTERING INTO TURKEY MARKET ____________________________________19

VI. SELECTING AUTOMATIVE SECTOR FOR INVESTMENT IN TURKEY____22

6.1 Global Sector_____________________________________________________________23

6.2 The Domestic Sector _______________________________________________________25

VII. TARGET SEGMENT EXPORTING AUTOMOTIVE PARTS ________________29

Opportunities__________________________________________________________30

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 3

SWOT Analysis________________________________________________________34

V1II. BEFORE INVESTING IN TURKEY_____________________________________36

General Business Environment____________________________________________36

Macroeconomics________________________________________________________37

Taxation______________________________________________________________37

Legal System___________________________________________________________38

Workforce_____________________________________________________________38

References

Abbreviations

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 4

I. COUNTRY PROFILE: INTRODUCING TURKEY

1.1 History, geography, population

Turkey, strategically located in the Eurasia region, is a dynamic country with a robust economy

and a young population, often described as the “China of Europe.”

It is a nation steeped in rich history and cultural life; a realm of sprawling cities and vast rural

areas; of coastal towns and tiny fishing communities. It is a mountainous country with mist-

hidden plateaus, combined with enormous steppes and fertile river valleys.

Sixty percent of the country is located at altitudes of 3,300 feet above sea level or higher. Located

in eastern Turkey, Ağrı Dağı (Mount Ararat) at 16,976 feet is the nation’s highest peak and the

biblical resting grounds of Noah’s Ark.

More than 99% of Turkey’s population is Muslim, but the nation is a secular state with a definite

western perspective. Christian and Jewish communities also exist in the big cities like Istanbul,

İzmir and Adana.

Conservative Sunni Muslims make up the large majority of the country’s Muslim population. But

about a sixth of Turkey’s population is Alevi, an Anatolian offshoot of the Shiite branch of Islam.

Two continents

Located on two continents -- Europe and Asia -- Turkey has always served as a bridge between

the Occident and Orient. The Silk Road, the traditional trade passage connecting Europe to

China, began in the ancient cities of what is now western Turkey.

Eight countries border Turkey: Bulgaria in the northwest, Greece in the west, Georgia in the

northeast, Armenia, Azerbaijan and Iran in the east, Iraq and Syria in the southeast.

Turkey is the third biggest nation in Europe in terms of territory after Russia and Kazakhstan---

nearly twice the size of the state of California. Three percent of Turkey lies in Europe. Known as

Thrace, European Turkey forms the southeastern tip of the Balkans. Ninety-seven percent of

Turkey is located in Asia and is known as Anatolia. A bulging peninsula, shaped like a mare’s

head, Anatolia is surrounded by the Black Sea, the Bosphorus, the Sea of Marmara, the

Dardanelles, the Aegean and the Mediterranean and has been home to many civilizations,

including the Hittite, and the Carian, Lydian and Phrygian empires. Anatolia served as the

granary of the Roman and Byzantine Empires. Its loss to the Turks in the 11th

century deprived

the Byzantine Empire of its agricultural wealth and led to its eventual demise.

Turkey is a key member of NATO and has the second biggest standing army in Europe after

Russia with more than one million men under arms. It is a member of the United Nations, the

Organization for Economic Cooperation and Development and other international bodies.

Young people

Turkey is a nation of young people. More than half of its population is under the age 25. The

country’s population has grown from 13.6 million in 1927 to over 72.561 million in 2009. By the

end of 2020, Turkey is expected to have 81.650 million inhabitants. It already has the third

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 5

largest population in Europe after Russia and Germany and is expected to surpass Germany in the

next several years.

Atatürk’s reforms

Turkey was proclaimed a republic in 1923, emerging from the ruins of the Ottoman Empire

which ruled the Middle East, North Africa, the Balkans and parts of Eastern Europe for over 450

years. The Ottoman Empire crumbled after its disastrous World War One defeat as an ally of the

Central Powers.

From 1923 to 1938, Kemal Atatürk, the founder and first president of the Turkish Republic,

carried out sweeping reforms that transformed the country from a backward, feudal state to a

progressive nation with a western outlook. The Sultanate was abolished. Atatürk replaced the

Sharia, or Islamic holy law, with civilian, trade and criminal codes adopted from Switzerland,

Italy and Germany.

In 1925, the fez and the turban, symbols of Islamic backwardness, were banned, replaced by the

şapka, or western-style hat with a brim. Three years later, the Latin alphabet replaced the esoteric

Ottoman script, allowing masses of illiterate Turks to learn to read and write.

Atatürk established state economic enterprises, or state-owned industries, as a solution to

Turkey’s economic underdevelopment. Enormous government-owned textile mills, mines and

mineral processing plants, oil refineries and petrochemical complexes came into being. State

banks with huge branch networks were also set up to help finance industrial growth and

commerce.

Private Sector

Atatürk’s successors encouraged the creation of private industry. Until the 1980s, authorities

protected local industry from outside competition by imposing severe restrictions on imports,

including steep duties and customs barriers. The motor vehicle industry, synthetic fibers and

yarns manufacturing, ready-wear and apparel, home textiles, pharmaceutical products, military

aircraft and armored vehicles, household appliances, home electronics were some of the sectors

that thrived as a result of the liberalization of the economy.

In the past 22 years, the government has privatized many major industries that were originally

established during the early years of the Republic, including, steel plants, pulp and paper mills,

oil refineries, clothing and textile plants, and cement factories to make the economy more

responsive to market forces.

1.2 Future Prospects

Challenges and Expectations

Turkey is one of the fastest growing large economies of the world. It has had high growth rates

over the past four decades. But growth has come in spurts and stalls, resulting in high inflation,

budgetary and current account deficits and political instability. From 1960 through 1997, the

country had three military interventions and a post-modern military and civilian coup.

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 6

International Monetary Fund-backed programs have helped Prime Minister Recep Tayyip

Erdoğan’s government push down inflation to single digits from around 69.5% in 2001, revalue

the Turkish Lira against the dollar, introduce a new currency and achieve six years of strong

growth and help draw record foreign investment and capital. Year-to-year inflation in March

2009 stood at 7.89%, only to rise to 10.13% in February 2010.

In the past three decades, Turkish leaders have adopted free market policies designed to integrate

Turkey with the world economy. Under the late President Turgut Özal and his successors, the

government encouraged Turkish companies to do business abroad.

In 2009, Turkey exported motor vehicles and automotive parts and components to more than 187

countries and autonomous regions and 14 free zones on five continents.

Exports of textiles and apparel, iron and steel, chemical products, electrical appliances, color

television sets, textiles and textile raw materials, nonferrous metals, mineral products, grains,

pulses, oil seeds, cement, ceramic tiles and sanitary ware and jewelry, have also boomed.

Imports, chiefly in crude oil, natural gas, boilers and machinery, iron and steel, motor vehicles,

electrical machinery, plastics, valuable metals and stones, organic chemicals, pharmaceutical

products and optical equipment have also rocketed.

Turkey’s foreign trade increased 34-fold in the past 29 years from a mere $7 billion in 1979 to

$240.3 billion in 2009, according to the Turkish Statistical Institute. Exports have risen from

about $2 billion in 1979 to $102.1 billion in 2009. Imports have ballooned from $5 billion to

$140.7 billion in 2007.

Many imported items previously banned in Turkey, such as computers, foreign-made

automobiles and commercial vehicles, mobile phones, furniture, and food stuffs, are now

available on the market and compete with domestic products.

Turkish political and economic influence has grown in the Balkans and in the Turkic Republics

of the former Soviet Caucasus and Central Asia since the breakup of the USSR and Yugoslavia.

Turkish companies are among the biggest foreign investors in Romania, Bulgaria, Russia, Egypt,

Ukraine, Azerbaijan, Georgia, Kazakhstan, Kyrgyzstan, Moldova, Uzbekistan, Turkmenistan

Tunisia, Libya, Syria, Morocco and Iraq.

During the past three decades, the nation completed a key part of its infrastructural development.

New highways linking Europe with the Middle East, scores of new hydroelectric dams, power

plants, modern telecommunication networks were constructed. Phone lines were installed in

every village and hamlet in Anatolia.

II. PESTLE ANALYSIS

2.1 Political

Politics of Turkey takes place in a framework of a secular parliamentary representative

democratic republic, whereby the Prime Minister of Turkey is the head of government, and of a

pluriform multi-party system.Executive power is exercised by the government.Legislative power

is vested in both the government and the Grand National Assembly of Turkey. The Judiciary is

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 7

independent of the executive and the legislature. Its current constitution was adopted on

November 7, 1982 after a period of military rule, and enshrines the principle of secularism.

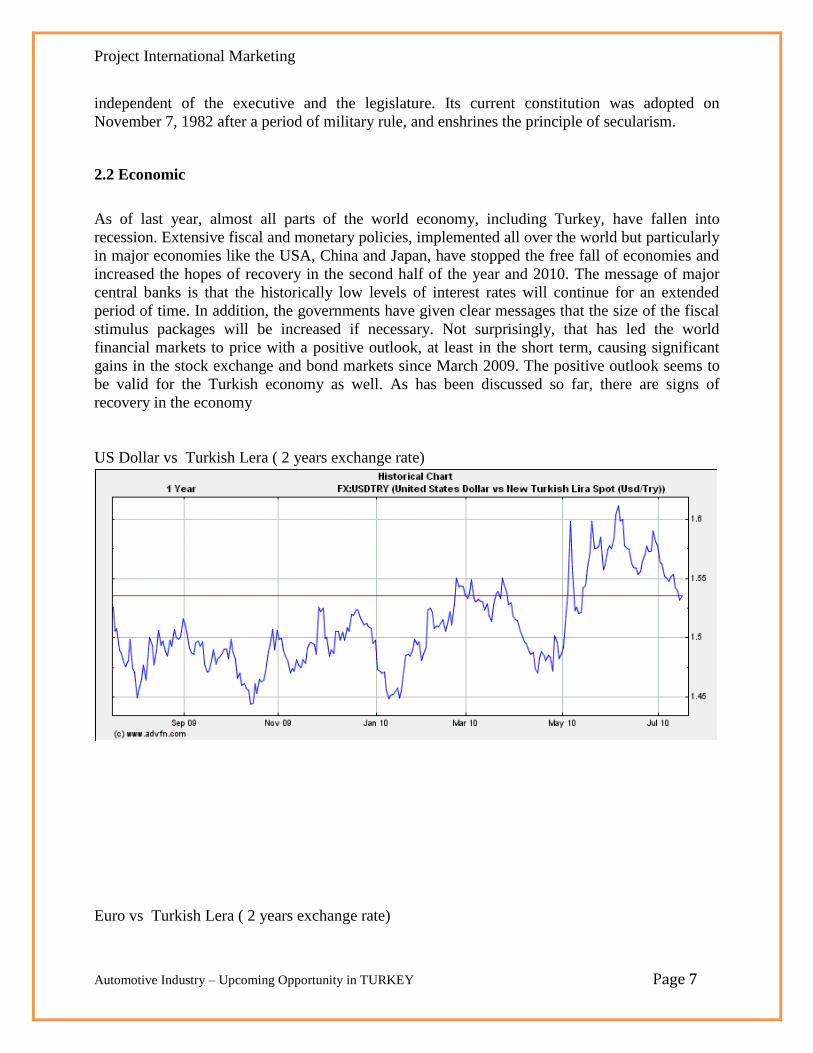

2.2 Economic

As of last year, almost all parts of the world economy, including Turkey, have fallen into

recession. Extensive fiscal and monetary policies, implemented all over the world but particularly

in major economies like the USA, China and Japan, have stopped the free fall of economies and

increased the hopes of recovery in the second half of the year and 2010. The message of major

central banks is that the historically low levels of interest rates will continue for an extended

period of time. In addition, the governments have given clear messages that the size of the fiscal

stimulus packages will be increased if necessary. Not surprisingly, that has led the world

financial markets to price with a positive outlook, at least in the short term, causing significant

gains in the stock exchange and bond markets since March 2009. The positive outlook seems to

be valid for the Turkish economy as well. As has been discussed so far, there are signs of

recovery in the economy

US Dollar vs Turkish Lera ( 2 years exchange rate)

Euro vs Turkish Lera ( 2 years exchange rate)

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 8

Project International Marketing

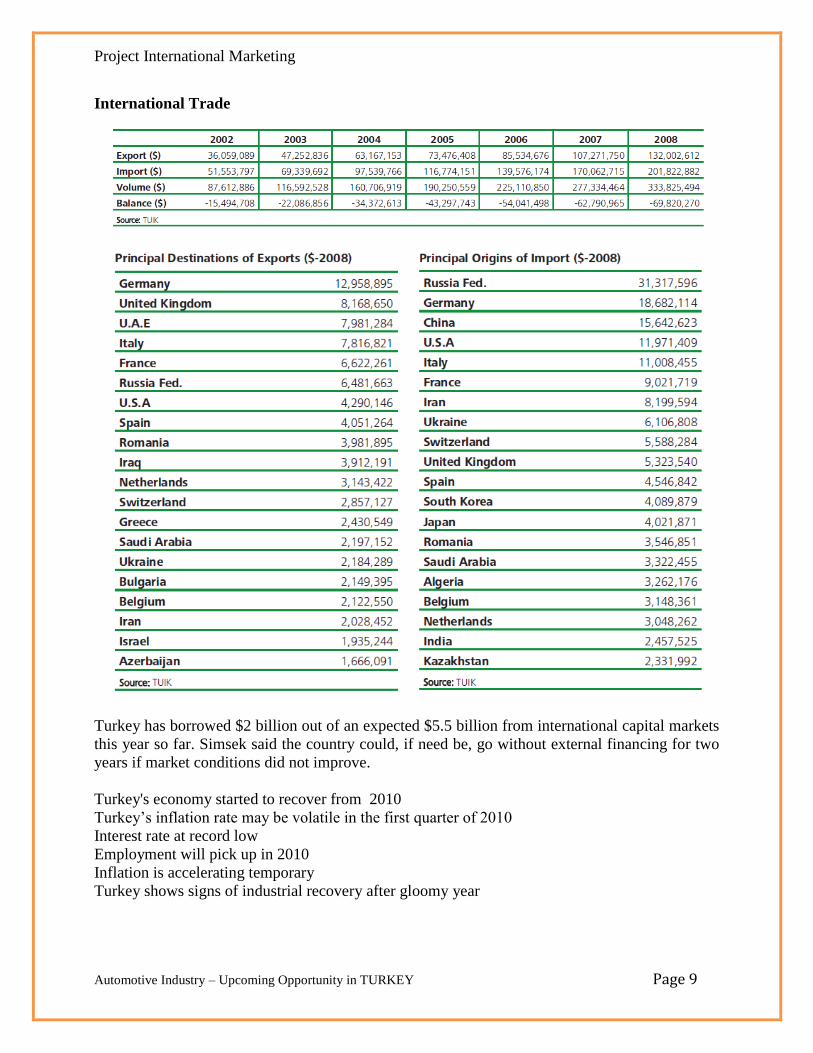

Automotive Industry – Upcoming Opportunity in TURKEY Page 9

International Trade

Turkey has borrowed $2 billion out of an expected $5.5 billion from international capital markets

this year so far. Simsek said the country could, if need be, go without external financing for two

years if market conditions did not improve.

Turkey's economy started to recover from 2010

Turkey’s inflation rate may be volatile in the first quarter of 2010

Interest rate at record low

Employment will pick up in 2010

Inflation is accelerating temporary

Turkey shows signs of industrial recovery after gloomy year

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 10

2.3 Social

The liveliness of the Turkish culture is so rich that it cannot be fit into a single definition. It is

influenced by the ancient history of Anatolia, the Mediterranean, the Middle East, the Caucasus,

Eastern Europe, and certainly by the Aegean culture.

Throughout history, Anatolia, like Istanbul, has hosted and produced many centers of culture and

the legacy of various civilizations attests to that fact. Today, this heritage also determines the

cultural life of Turkey. The culture of tolerance for all religions and languages living together in

peace, spread from Istanbul (which was the capital of empires) to Anatolia. This tradition of

tolerance is one of the most important inheritances that Turkey can share with the world.

Hospitality

In addition to the existing social values of families living in a big city, the Turkish people have

retained some distinctive values of their own. One is an immense courtesy towards guests and

visitors and a tendency to lavish hospitality upon them, no matter how costly. Another is an

abiding respect for their family and its senior members. Another Turkish value is a strong respect

for hard work and determination. And above all, there is a sense of humor and a love of life and

music. One 19th century English ambassador noticed that the people of Turkey loved to sing and

dance whenever they could. Many things have changed in Turkey since his time, but not that.

2.4 Technological

The Republic of Turkey has long been and continues to be an advocate of raising science and

technology to new heights, and has recently been engaged in a significant science, technology

and innovation (STI) impetus. Such an advocacy is rooted in the advancement of a dynamic ideal

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 11

based on continuous renewal and modernization under the guidance of science, technology, and

knowledge.

The Turkish model is all the more significant given that the low levels of public R&D funds,

industrial R&D, and demand for innovation alongside rising global competitive pressure on

sectors with high exports were overcome by the instigation of an STI impetus. With similar

conjectures still being valid in many developing countries, the Turkish model provides useful

insight to address these challenges.

This policy brief is organized into three main sections, namely long-term visions, strategies and

targets for STI driven growth, major instruments in the STI policy mix, and achievements. With

regards to the Turkish model, this paper emphasizes the conceptualization of the Turkish

Research Area (TARAL) in triggering a particular kind of mobilization, both in the sense of

resources and in guiding system actors towards socio-economic goals.

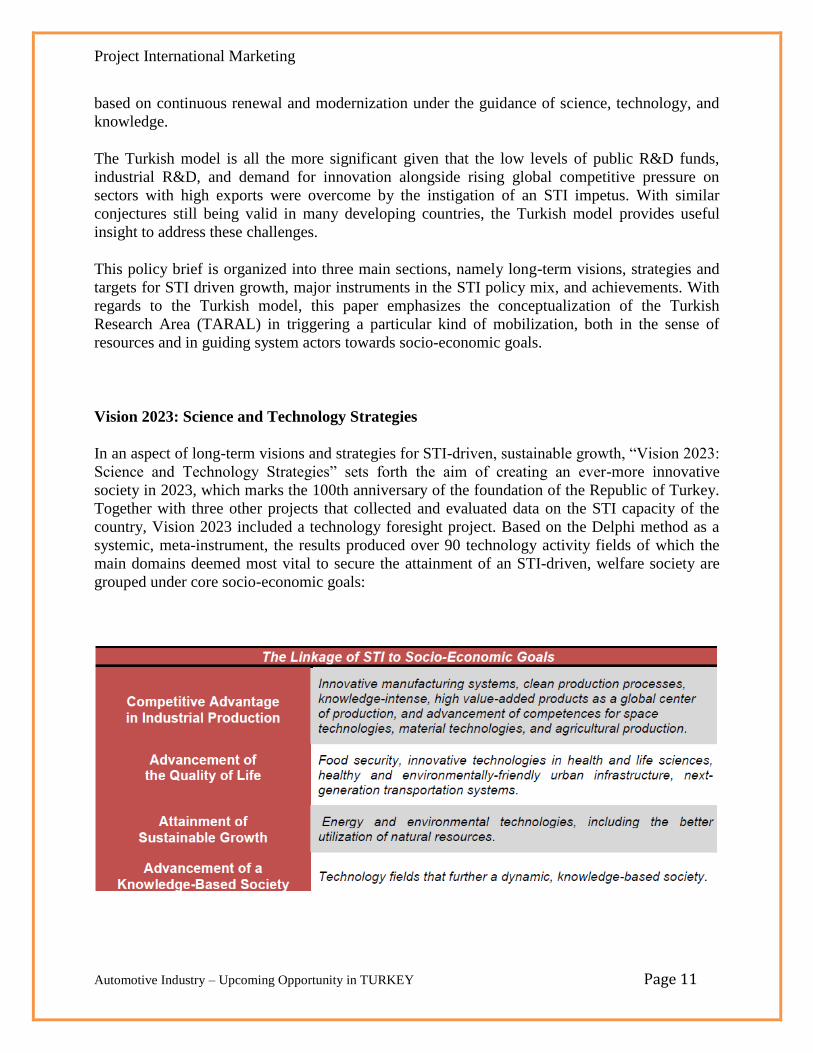

Vision 2023: Science and Technology Strategies

In an aspect of long-term visions and strategies for STI-driven, sustainable growth, ―Vision 2023:

Science and Technology Strategies‖ sets forth the aim of creating an ever-more innovative

society in 2023, which marks the 100th anniversary of the foundation of the Republic of Turkey.

Together with three other projects that collected and evaluated data on the STI capacity of the

country, Vision 2023 included a technology foresight project. Based on the Delphi method as a

systemic, meta-instrument, the results produced over 90 technology activity fields of which the

main domains deemed most vital to secure the attainment of an STI-driven, welfare society are

grouped under core socio-economic goals:

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 12

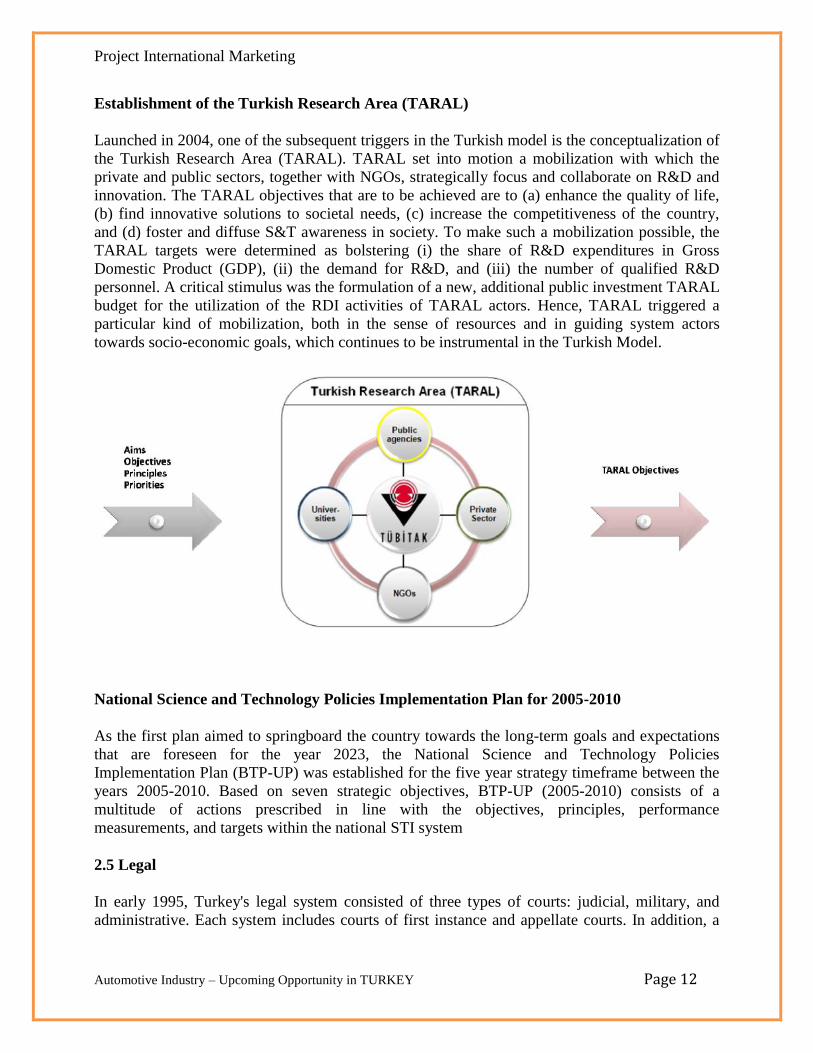

Establishment of the Turkish Research Area (TARAL)

Launched in 2004, one of the subsequent triggers in the Turkish model is the conceptualization of

the Turkish Research Area (TARAL). TARAL set into motion a mobilization with which the

private and public sectors, together with NGOs, strategically focus and collaborate on R&D and

innovation. The TARAL objectives that are to be achieved are to (a) enhance the quality of life,

(b) find innovative solutions to societal needs, (c) increase the competitiveness of the country,

and (d) foster and diffuse S&T awareness in society. To make such a mobilization possible, the

TARAL targets were determined as bolstering (i) the share of R&D expenditures in Gross

Domestic Product (GDP), (ii) the demand for R&D, and (iii) the number of qualified R&D

personnel. A critical stimulus was the formulation of a new, additional public investment TARAL

budget for the utilization of the RDI activities of TARAL actors. Hence, TARAL triggered a

particular kind of mobilization, both in the sense of resources and in guiding system actors

towards socio-economic goals, which continues to be instrumental in the Turkish Model.

National Science and Technology Policies Implementation Plan for 2005-2010

As the first plan aimed to springboard the country towards the long-term goals and expectations

that are foreseen for the year 2023, the National Science and Technology Policies

Implementation Plan (BTP-UP) was established for the five year strategy timeframe between the

years 2005-2010. Based on seven strategic objectives, BTP-UP (2005-2010) consists of a

multitude of actions prescribed in line with the objectives, principles, performance

measurements, and targets within the national STI system

2.5 Legal

In early 1995, Turkey's legal system consisted of three types of courts: judicial, military, and

administrative. Each system includes courts of first instance and appellate courts. In addition, a

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 13

Court of Jurisdictional Disputes rules on cases that cannot be classified readily as falling within

the purview of one court system.

The judicial courts form the largest part of the system; they handle most civil and criminal cases

involving ordinary citizens. The two supreme courts within the judicial system are the

Constitutional Court and the Court of Appeals.

The Constitutional Court reviews the constitutionality of laws and decrees at the request of the

president or of one-fifth of the members of the National Assembly. Its decisions on the

constitutionality of legislation and government decrees are final. The eleven members of the

Constitutional Court are appointed by the president from among candidates nominated by lower

courts and the High Council of Judges and Public Prosecutors. Challenges to the constitutionality

of a law must be made within sixty days of its promulgation. Decisions of the Constitutional

Court require the votes of an absolute majority of all its members, with the exception of decisions

to annul a constitutional amendment, which require a two-thirds majority

2.6 Environmental

With the establishment of the Environment Ministry in 1991, Turkey began to make significant

progress addressing its most pressing environmental problems. The most dramatic improvements

were significant reductions of air pollution in Istanbul and Ankara. However, progress has been

slow on the remaining--and serious--environmental challenges facing Turkey.

In 2003, the Ministry of Environment was merged with the Forestry Ministry. With its goal to

join the EU, Turkey has made commendable progress in updating and modernizing its

environmental legislation. However, environmental concerns are not fully integrated into public

decision-making and enforcement can be weak. Turkey faces a backlog of environmental

problems, requiring enormous outlays for infrastructure. The most pressing needs are for water

treatment plants, wastewater treatment facilities, solid waste management, and conservation of

biodiversity. The discovery of a number of chemical waste sites in 2006 has highlighted

weakness in environmental law and oversight.

After long years of silence, Turkey's becoming a signatory of the Kyoto Protocol was back on the

agenda in 2007, and a focus of Prime Minister Erdogan's speech at the UN General Assembly.

Despite the positive approach, Turkey would still like to keep its reservation to get developing

country treatment with regard to the emission levels set by the protocol.

Turkey's economic emergence has brought with it fears of increased environmental degradation.

As Turkey's economy experienced high levels of growth in the mid-1990s, the country's boom in

industrial production resulted in higher levels of pollution and greater risks to the country's

environment. With domestic energy consumption on the rise, Turkey has been forced to import

more oil and gas, and the resultant increase in oil tanker traffic in the Black Sea and Bosporus

Straits has increased environmental threats there.

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 14

With Turkey now a formal candidate for membership in the European Union, Turkey's

environmental record will come under heavy scrutiny. In 1983, Turkey promulgated the country's

overarching "Environmental Law," and a national Ministry of Environment was created in 1991.

Turkey is building an extensive network of hydroelectric energy sources in the southeast part of

the country, and cleaner-burning natural gas is moving to replace coal in power generation.

The importance of strong environmental protection measures, as well as the fragility of Turkey's

environment, was driven home recently by catastrophe that struck the Tisza and Danube rivers in

southeast Europe. After a reservoir wall at a gold mine in Romania collapsed, cyanide-tainted

water was dumped into the Tisza River, and the toxic spill killed thousands of fish in Hungary as

it flowed downstream into the Danube. Although the spill was supposed to be diluted by the time

it reached the Black Sea, and it was not expected to cause any damage there or in the Marmara

Sea, Turkey took no chances, taking water samples in the Bosporus Straits to measure any effects

from the toxic spill.

As Turkey steers itself towards meeting EU membership criteria, it should see increased energy

efficiency. The growth in energy consumption should wane as state subsidies are eliminated and

prices more accurately reflect costs. Yet, there will still be much room for improvement, and

Turkey's vigilance in safeguarding its environment will be key to the continuance of its economic

development.

To the extent that natural gas replaces more carbon-intensive fuels, the country's increased use of

natural gas will further diversify the Turkish energy supply and contribute to the mitigation of

urban pollution and CO2 emissions. By setting differentiated taxes to promote the use of cleaner

fuels (and, in particular, to promote the use of low-sulfur heavy fuel oil), Turkey can significantly

stem the rising tide of carbon emissions. Continuing to educate the public about the benefits of

saving energy, as well as involving large industries in energy efficiency programs, will lead to

long-term positive effects for Turkey's economy and environment.

Finally, Turkey's State Planning Organization, together with the World Bank, is coordinating a

project called the "Turkish National Environmental Strategy and Action Plan" to implement

activities in Turkey related to Agenda 21. By establishing basic environmental standards and

identifying environmental investment priorities, Turkey can integrate sustainable policies into its

overall economic development, thereby safeguarding its environment well into the futur

III. Why invest in Turkey?

The Turkish economy has registered superb improvement in competitiveness in recent years and

proven its potential as a magnet for international investors, world-renowned strategist Professor

Michael Porter has said. Addressing agroup of businessmen and reporters on Saturday at a

conference organized by İşTcell, a Turkcell brand directed at corporate customers, Porter,

director of Harvard Business School’s Institute for Strategy and Competitiveness, said that if

Turkey were traded on the stock market, he would definitely make an equity investment in the

country. During the first part of his speech, Porter described the major premises of creating

strategies and determining and developing a competitive approach and the role of leaders in the

competitiveness of a company. He also shared his views on possible strategies that may be

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 15

adopted during times of economic crisis. He devoted the second part of his speech to discussing

Turkey’s economic strategies, including an in-depth analysis of the business world’s role in these

strategies.

This is perhaps the best time to consider investing in Turkey for business, because Turkey has a

vibrant economy which is all set to take off when Turkey joins the EU. Joining the EU will imply

that the economy will take off in a big way with a lot of foreign investments coming in. Turkey

also has a fast growing manufacturing industry which will enable the economy to grow faster,

generating a greater demand for product consumption, which will in turn drive up profits for

industry, increasing its valuation.

The Republic of Turkey’s movement toward membership in the European Union is creating

momentum to adopt European business regulations and standards in Turkey, thereby ultimately

making it easier to sell and conduct business in this market. Similarly, reforms since 2001 have

created a strong and stable economy that attracts foreign investment, which in turn will be

followed by desperately needed capital improvements and demand for new products and services.

The Commercial Service in Turkey has identified a number of market opportunities for Indian

firms and continues to work with companies to either enter the Turkish market or expand market

share.

10 Reasons to Invest in Turkey

1. SUCCESSFUL ECONOMY

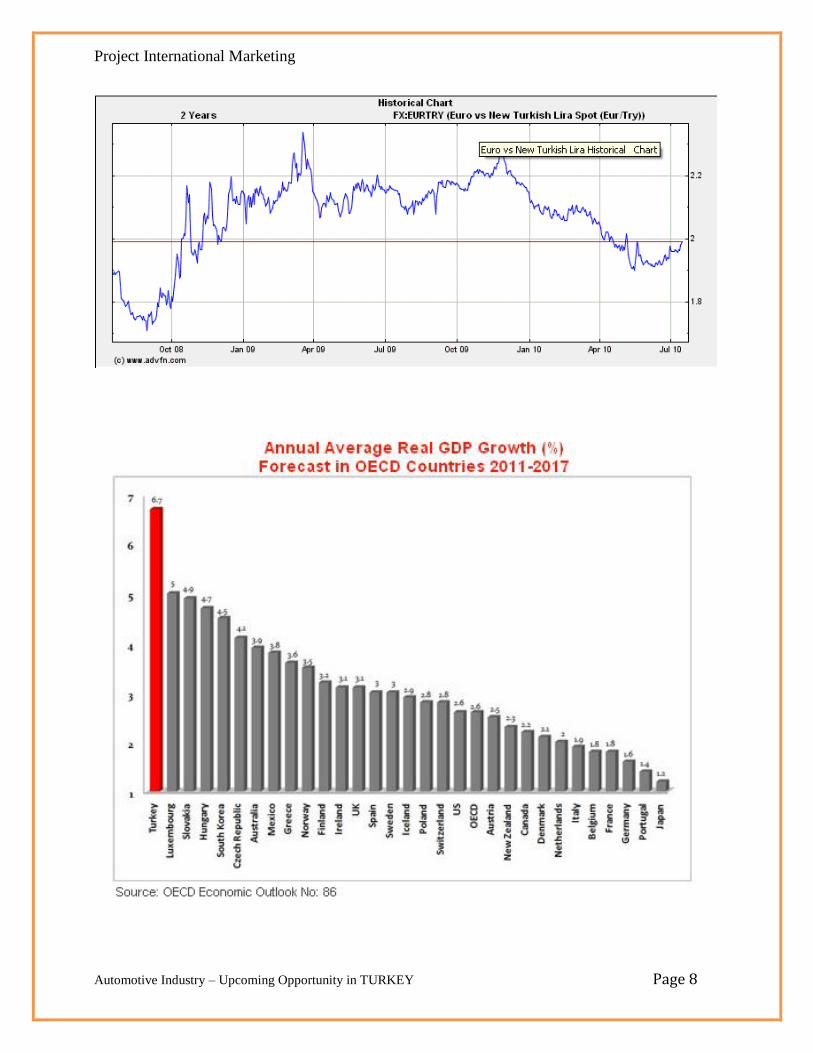

Booming economy (USD 230 billion to USD 618 billion GDP from 2002 to 2009)

Sustainable economic growth (4.3 percent annual average real GDP increase for the last 7 years)

Promising economy with a bright future as it is expected to be the fastest growing economy among the

OECD members during 2011-2017 with an annual average real GDP growth rate of 6.7 percent

16th largest economy in the world and 6th largest economy compared to the EU area in 2009

Institutionalized economy fueled by over USD 83 billion of FDI in the last 7 years and ranked as the 15th

most attractive FDI destination for 2008-2010 (UNCTAD)

2. POPULATION

A population of 73 million people

Largest youth population compared with the EU

Median age 28.8

60 percent of the population under the age of 35

Young, dynamic, well-educated and multi-cultural population

3. QUALIFIED LABOR FORCE

Over 24.7 million young, well-educated and motivated professionals

Labor productivity with an annual average growth of 4.4 percent between 2002 and 2009

5th largest labor force compared with the EU

Consumer base and motivated work force

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 16

Approximately 450,000 graduates from circa 150 universities

Around 550,000 high school graduates, including one third from vocational and technical high schools

4. LIBERAL AND REFORMIST INVESTMENT CLIMATE

A dynamic and mature private sector with USD 102 billion worth of exports and an increase of 183 percent

between 2002 and 2009

Highly competitive investment conditions

Strong industrial and service culture

Equal treatment for all investors

More than 23,000 companies with international capital

International arbitration

Guarantee of transfers

5. INFRASTRUCTURE

New and highly developed technological infrastructure in transportation, telecommunications and energy

Well-developed and low-cost sea transport facilities

Railway transport advantage to Central and Eastern Europe

6. CENTRALLY LOCATED

A natural bridge between both East-West and North-South axes, thus creating an efficient and cost

effective outlet to major markets

Easy access to 1.5 billion customers in Europe, Eurasia, the Middle East and North Africa

Access to multiple markets worth USD 22 trillion of GDP

7. ENERGY CORRIDOR AND TERMINAL OF EUROPE

An important energy terminal and corridor in Europe connecting the East and West

As an energy transit country, Turkey currently has the capacity to transport 121 million tons of oil to the

world markets per annum. Once the ongoing projects are completed, the annual transit capacity will

increase to 221 million tons of oil and 43 billion m³ of natural gas.

8. LOW TAXES & INCENTIVES

Corporate Income Tax reduced from 30 percent to 20 percent

Individual Income Tax varies from 15 percent to 35 percent

Tax benefits and incentives in Technology Development Zones, Industrial Zones and Free Zones could

include total or partial exemption from Corporate Income Tax, up to 80 percent grant on employer’s social

security share, as well as land allocation.

New R&D and Innovation Support Law

Region and sector-based incentive system

9. CUSTOMS UNION WITH THE EU SINCE 1996

Customs Union with the EU since 1996, and Free Trade Agreements (FTA) with 16 countries

More FTAs underway

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 17

Accession negotiations with the EU since 2005

10. LARGE DOMESTIC MARKET

30 million internet users in 2009, up from 4 million in 2002

63 million GSM users in 2009, up from 23 million in 2002

44.4 million credit card users in 2009, up from 16 million in 2002

Over 85 million airline passengers in 2009, up from 33 million in 2002

27.3 million international tourist arrivals in 2009, up from 13 million in 2002

IV. INDIA- TURKEY ECONOMIC RELATIONS

India–Turkey relations are foreign relations between India and Turkey. Diplomatic relations

between India and Turkey was established in 1948. India has an embassy in Ankara and a

consulate–general in Istanbul. Turkey has an embassy in New Delhi. Both countries are full

members of the World Trade Organization (WTO). Both countries are regarded as trustworthy

referees in the Israeli-Palestinian conflict. Due to the latter's key strategic support for India's

chronological enemy, Pakistan, relations between the two countries have sometimes been coldly

strained. In recent years nevertheless, India and Turkey have decided to put aside differences, and

seek closer political, economic, and military connections. India now characterizes the relations

between the two countries with warmth and cordiality. Also, the Indian real estate firm GMR

Group has decided to industrialize Ankara Airport. In 2007, trade between the two countries was

at $2,647 million

Bilateral Trade and Investments

2002 – 2003 – 2004 – 2005 – 2006 – 2007 – 2008

The major items of India’s exports to Turkey include cotton yarn, synthetic yarn, organic dyes,

organic chemicals, denim, steel (bars and rods), granite, antibiotics, carpets, unwrought zinc,

sesame seed, TV CRTs, mobile handsets, clothing and apparel.

Turkey’s exports to India includes poppy seed, auto components, marble, textile machinery,

denim, carpets, cumin seeds, minerals (vermiculite, perlite and chlorites) and fittings and steel

products.

Indai – Turkey Exports & Imports (Department of Commerce)

Exports

S.No. Country 2008-2009 %Share 2009-2010(Apr-Dec) %Share

1. TURKEY 637,029.19 0.7577 498,373.02 0.8317

India's Total Export 84,075,505.87 59,924,452.16

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 18

Imports

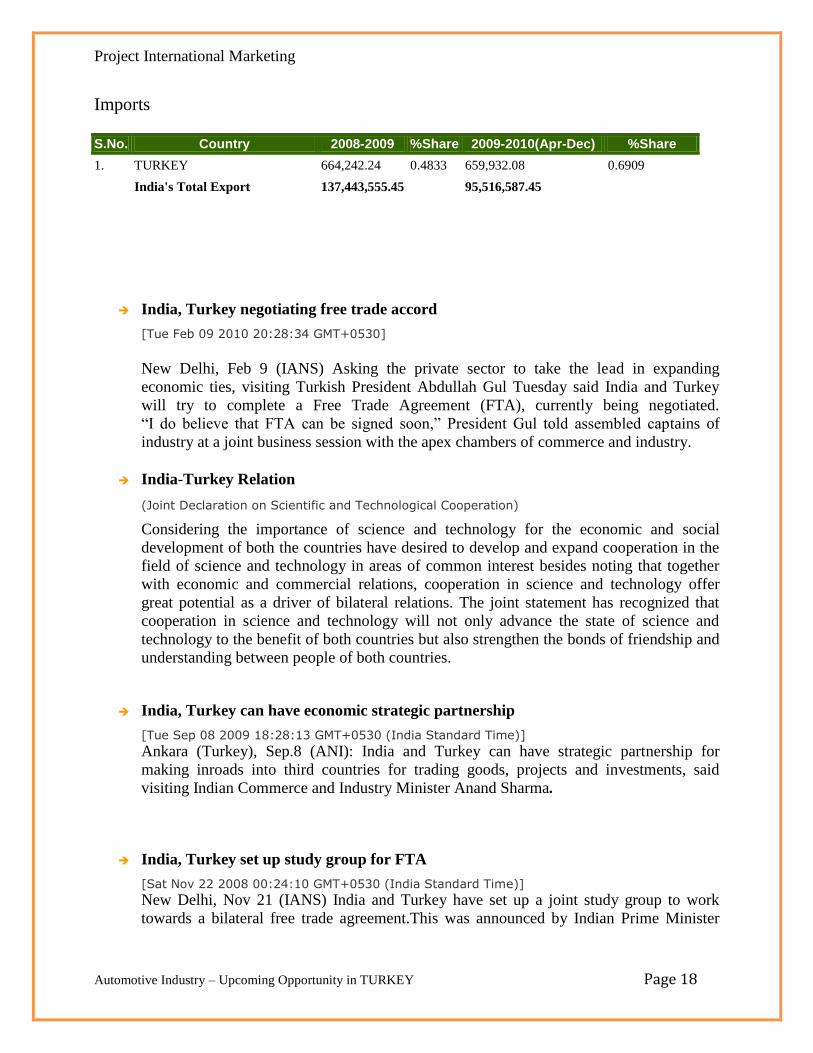

S.No. Country 2008-2009 %Share 2009-2010(Apr-Dec) %Share

1. TURKEY 664,242.24 0.4833 659,932.08 0.6909

India's Total Export 137,443,555.45 95,516,587.45

India, Turkey negotiating free trade accord

[Tue Feb 09 2010 20:28:34 GMT+0530]

New Delhi, Feb 9 (IANS) Asking the private sector to take the lead in expanding

economic ties, visiting Turkish President Abdullah Gul Tuesday said India and Turkey

will try to complete a Free Trade Agreement (FTA), currently being negotiated.

―I do believe that FTA can be signed soon,‖ President Gul told assembled captains of

industry at a joint business session with the apex chambers of commerce and industry.

India-Turkey Relation

(Joint Declaration on Scientific and Technological Cooperation)

Considering the importance of science and technology for the economic and social

development of both the countries have desired to develop and expand cooperation in the

field of science and technology in areas of common interest besides noting that together

with economic and commercial relations, cooperation in science and technology offer

great potential as a driver of bilateral relations. The joint statement has recognized that

cooperation in science and technology will not only advance the state of science and

technology to the benefit of both countries but also strengthen the bonds of friendship and

understanding between people of both countries.

India, Turkey can have economic strategic partnership

[Tue Sep 08 2009 18:28:13 GMT+0530 (India Standard Time)] Ankara (Turkey), Sep.8 (ANI): India and Turkey can have strategic partnership for

making inroads into third countries for trading goods, projects and investments, said

visiting Indian Commerce and Industry Minister Anand Sharma.

India, Turkey set up study group for FTA

[Sat Nov 22 2008 00:24:10 GMT+0530 (India Standard Time)] New Delhi, Nov 21 (IANS) India and Turkey have set up a joint study group to work

towards a bilateral free trade agreement.This was announced by Indian Prime Minister

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 19

Manmohan Singh after talks with visiting Turkish Prime Minister Recep Tayyip Erdogan

Friday evening at the stately Hyderabad House here.

Indian Oil Corp Ltd Turkey plan put on backburner

[Friday, June 18, 2010 2:48]

New Delhi: State-owned Indian Oil Corp Ltd has put its plans to set up an oil refinery in

Turkey on the backburner, and is currently focusing on acquiring a producing

hydrocarbon asset overseas along with Oil India Ltd.

V. ENTERING INTO TURKEY MARKET

To enter the Turkish market, most INDIAN companies first opt to have a local representative or

liaison office. As the business develops, companies open up subsidiaries. Companies rely on

local experience and knowledge as to how business is done in this market. Knowing the

regulatory and business framework is a difficult task without the support of a local business

partner. The Commercial Service in Turkey has a number of programs and services available to

assist the Indian. business community in establishing a presence in this market. In addition, the

Commercial Service in Turkey employs experienced Commercial Specialists with industry sector

expertise that can tailor your business approach to the right audience and advise and steer your

company through the often less than transparent bureaucratic procedures that are common in

Turkey.

Keeping in mind that Turkey is also the commercial hub of the region, companies should also

consider using Turkey or Turkish partners to access business opportunities throughout Central

Asia, the Caucasus, the Middle East and even Africa. Turkish partners know these neighboring

markets well, and are ready to take risks to make sales.

Using an Agent or Distributor

Unless a Indian firm's interests are large enough to warrant opening an office in the country, the

most effective means of selling in Turkey is through a reliable and qualified local representative.

Personal contact is extremely important in Turkish business in both private and public sectors.

When dealing with government tenders, an agent is an absolute necessity in view of complicated

bureaucratic procedures and the language barrier.

An Indian firm should carefully investigate the reputation and possible conflicting interests of

any prospective representative or agent before signing contractual agreements. Indian

Commercial Service Turkey can make background check on a selected company and prepare an

International Company Profile (ICP) report, which can be a useful tool in the elimination of an

agent or distributor candidate.

Agency agreements under Turkish law are private contracts between two parties and their

stipulations vary according to mutual consent. There are no fixed commission rates. It is

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 20

recommended that sole manufacturer representatives/distributors be appointed for the entire

country, which may include other countries in the region. Agency Agreements can be for a

period of a year to be renewed depending on the success of the agent. In cases where a large

volume of government business is expected, it is essential either to appoint an Ankara firm or an

Istanbul firm with a branch office in the capital.

Direct Marketing

Unless a Indian firm has established an office in Turkey, direct marketing from the India without

an agent or representative is not recommended. In fact, it is virtually impossible to surmount

complicated bureaucratic requirements, language obstacles, and purchasing transactions without a

competent local representative/agent. Especially for those firms with sales potential large enough

to warrant it, a local affiliate is the best possible way of selling to this market without an agent,

representative or distributor.

Distribution and Sales Channels

Marketing of most foreign products in Turkey is through foreign suppliers' representatives or

distributors. Depending on the location of consumers/end-users, most distributors have a dealer

network throughout the country or in areas where the product is most used—in the case of several

industrial sectors; a dealer/repair network may be required. Commission representatives/agents,

on the other hand, periodically visit their customers together with their foreign principals to

maintain strong personal contact, which is a very important marketing tool in Turkey.

Selling Factors/Techniques

Once an American firm appoints a manufacturers’ representative or agent, the agent or distributor

expects-and should receive-the principal's full support with regard to literature, technical

information, advertisement and promotional materials. Possible private-sector importers should

receive catalogs and other literature clearly indicating the name and address of the local

representatives/distributors. A common and very effective support practice by European

principals is to invite the representative/agent to the principal's country (India ) every year for an

annual sales meeting. Both agents and, if possible, their principals, should periodically visit

existing and potential customers since the importance of personal contact in Turkey cannot be

overemphasized.

Especially in larger Turkish cities, international trade promotional events, such as fairs,

exhibitions and seminars, are common methods of sales promotion. These fairs are also

opportunities for Indian companies to assess (and meet) existing competition, since all major

foreign and local suppliers participate in such events. The catalogs of the events serve as 'trade

lists' on specific product categories. Currently, there are about seventy international fair and

exhibit organizers in Turkey.

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 21

Electronic Commerce

The majority of E-commerce transactions in Turkey are in the field of Internet banking. Local

industry sources report that nearly 70 percent of all electronic commerce transactions are in on-

line banking and financial services. The concept of Internet banking in Turkey is popular given

the very high cost of maintain physical bank branches throughout the country. Apart from

increasing customer service, the commercial banks realized that charging substantially less

transaction cost for Internet banking than the traditional brick and mortar enterprise of the past,

made the Internet banking more attractive to the consumers.

Protecting Your Intellectual Property

Several general principles are important for effective management of intellectual property rights

in Turkey. First, it is important to have an overall strategy to protect IPR. Second, IPR is

protected differently in Turkey than in the India. Third, rights must be registered and enforced in

Turkey, under local laws. Companies may wish to seek 6/30/2009 advice from local attorneys or

IP consultants.

It is vital that companies understand that intellectual property is primarily a private right and that

the Indian government generally cannot enforce rights for private individuals in Turkey. It is the

responsibility of the rights' holders to register, protect, and enforce their rights where relevant,

retaining their own counsel and advisors. While the Indian Government is willing to assist, there

is little it can do if the rights holders have not taken these fundamental steps necessary to securing

and enforcing their IPR in a timely fashion. Moreover, in many countries, rights holders who

delay enforcing their rights on a mistaken belief that the USG can provide a political resolution to

a legal problem may find that their rights have been eroded or abrogated due to doctrines such as

statutes of limitations, laches, estoppel, or unreasonable delay in prosecuting a law suit. In no

instance should USG advice be seen as a substitute for the obligation of a rights holder

to promptly pursue its case.

It is always advisable to conduct due diligence on partners. Negotiate from the position of your

partner and give your partner clear incentives to honor the contract. A good partner is an

important ally in protecting IP rights. Keep an eye on your cost structure and reduce the margins

(and the incentive) of would-be bad actors. Projects and sales in Turkey require constant

attention. Work with legal counsel familiar with Turkey laws to create a solid contract that

includes non-compete clauses, and confidentiality/nondisclosure provisions. It is also

recommended that small and medium-size companies understand the importance of working

together with trade associations and organizations to support efforts to protect IPR and stop

counterfeiting. There are a number of these organizations, both Turkey or India based. These

include:

- National Association of Manufacturers (NAM)

- Board of Trade (BOT)

- Export Promotion Board (EPB)

- International Intellectual Property Alliance (IIPA)

- International Trademark Association (INTA)

- The Coalition Against Counterfeiting and Piracy

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 22

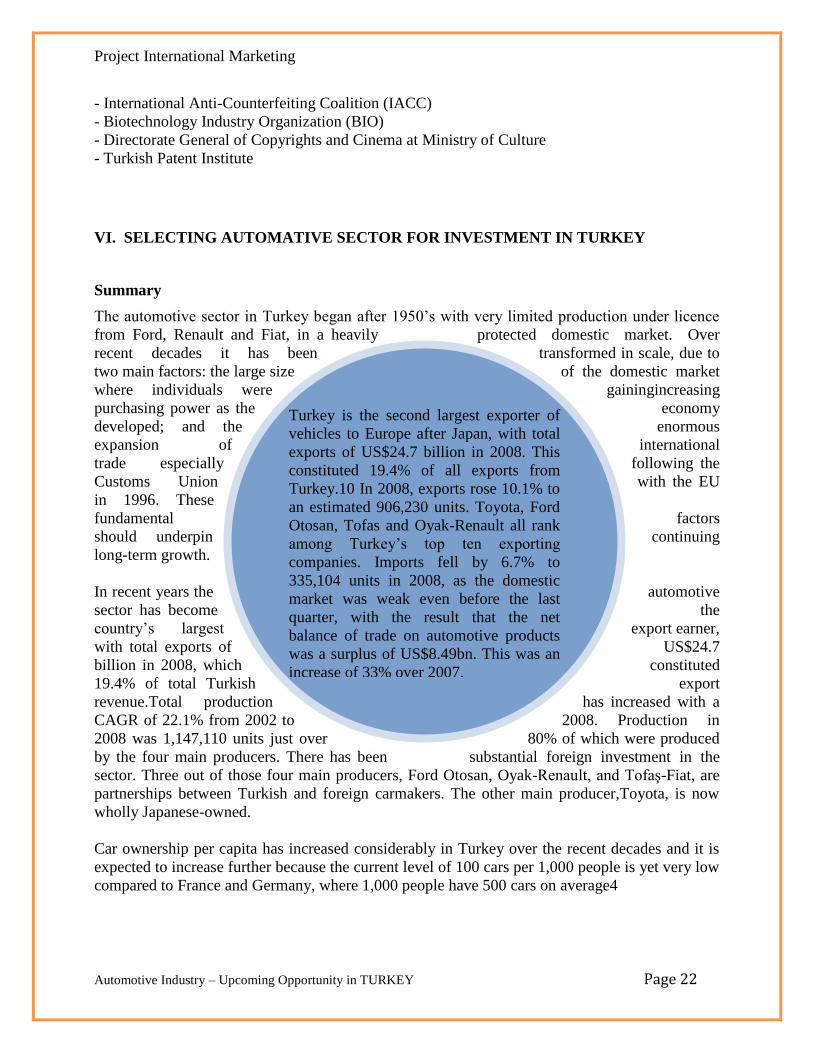

Turkey is the second largest exporter of

vehicles to Europe after Japan, with total

exports of US$24.7 billion in 2008. This

constituted 19.4% of all exports from

Turkey.10 In 2008, exports rose 10.1% to

an estimated 906,230 units. Toyota, Ford

Otosan, Tofas and Oyak-Renault all rank

among Turkey’s top ten exporting

companies. Imports fell by 6.7% to

335,104 units in 2008, as the domestic

market was weak even before the last

quarter, with the result that the net

balance of trade on automotive products

was a surplus of US$8.49bn. This was an

increase of 33% over 2007.

- International Anti-Counterfeiting Coalition (IACC)

- Biotechnology Industry Organization (BIO)

- Directorate General of Copyrights and Cinema at Ministry of Culture

- Turkish Patent Institute

VI. SELECTING AUTOMATIVE SECTOR FOR INVESTMENT IN TURKEY

Summary

The automotive sector in Turkey began after 1950’s with very limited production under licence

from Ford, Renault and Fiat, in a heavily protected domestic market. Over

recent decades it has been transformed in scale, due to

two main factors: the large size of the domestic market

where individuals were gainingincreasing

purchasing power as the economy

developed; and the enormous

expansion of international

trade especially following the

Customs Union with the EU

in 1996. These

fundamental factors

should underpin continuing

long-term growth.

In recent years the automotive

sector has become the

country’s largest export earner,

with total exports of US$24.7

billion in 2008, which constituted

19.4% of total Turkish export

revenue.Total production has increased with a

CAGR of 22.1% from 2002 to 2008. Production in

2008 was 1,147,110 units just over 80% of which were produced

by the four main producers. There has been substantial foreign investment in the

sector. Three out of those four main producers, Ford Otosan, Oyak-Renault, and Tofaş-Fiat, are

partnerships between Turkish and foreign carmakers. The other main producer,Toyota, is now

wholly Japanese-owned.

Car ownership per capita has increased considerably in Turkey over the recent decades and it is

expected to increase further because the current level of 100 cars per 1,000 people is yet very low

compared to France and Germany, where 1,000 people have 500 cars on average4

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 23

In 2010, demand patterns are likely to change for the Turkish automotive sector. Starting from

the second half of 2010, domestic demand patterns are likely to start normalising and monthly

sales are expected to be more stable. This would lead to more efficient production planning and

therefore to higher operating margins. Nevertheless, it is expected that the market for new

passenger cars will stagnate in 2010 full year. Once the effects of the global financial crisis start

to weaken, it is expected that the Turkish automotive sector will pick up to average annual

growth rates of 4.5-5% per year in 2011 and through to 2013.

The Turkish automotive parts industry has shown considerable growth between 2002 and 2007

and the first half of 2008, parallel to the increase in vehicle production. Exports of components

and parts, about 70% of which go to Europe, doubled in value between 2005 and 2008, reaching

US$7 billion, or 32% of total automotive exports4. Also affected by the global financial crisis in

2009, the automotive parts sector is expected to recover along with the automotive sector.

Key factors which attract foreign capital inflows to Turkey include;

Easy access to neighbouring (regional) emerging markets,

Friendly investment legislation,

Liberal banking system,

Highly skilled human resources in production and management,

Complementary level of technology and industrial experience on OEM and OES level

Competitive labour cost with high productivity

Extensive R&D support for projects.

Sector Overview

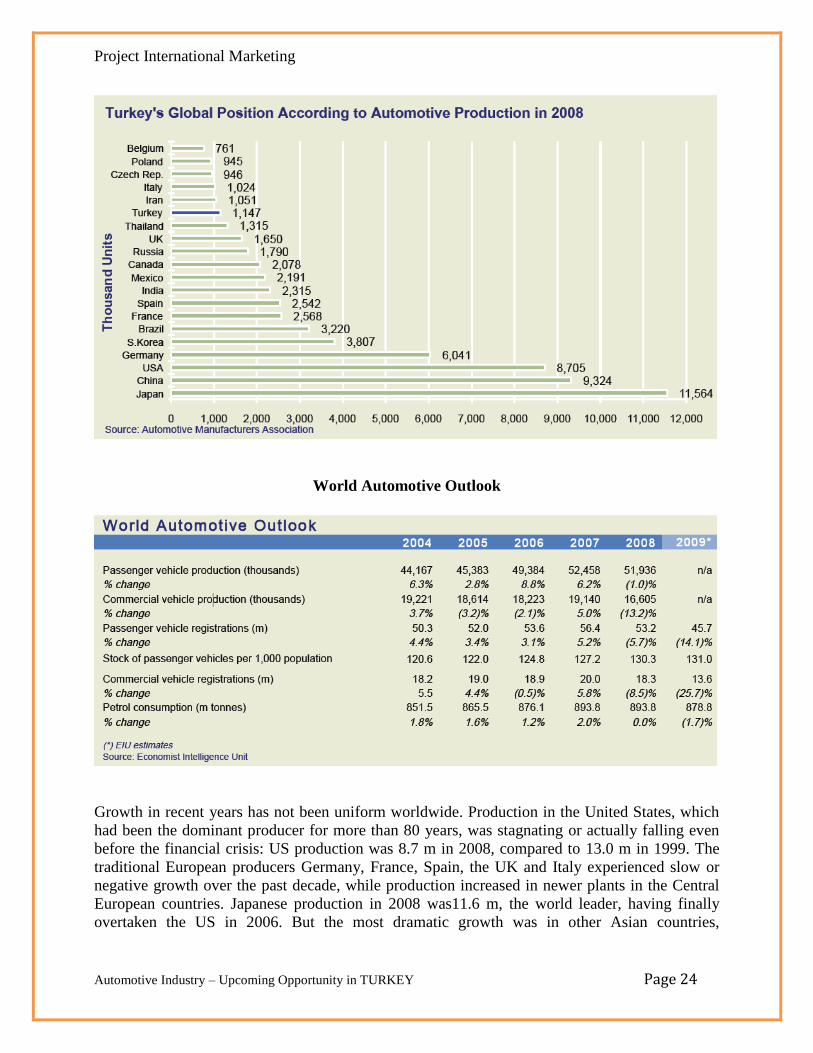

6.1 GLOBAL SECTOR

In 2008 global production of motor vehicles was 70.5 million, of which 52.6 million were

passenger cars and 17.9 million were commercial vehicles. Seventeen countries, including

Turkey, each produced more than one million vehicles in 2008. The industry had experienced

strong growth over the past five years, mostly in passenger cars, although this came to an abrupt

end in the last quarter of 2008. Turkey is 15th in global automotive production and 5th in Europe

Turkey's Global Position According to Automotive Production in 2008

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 24

World Automotive Outlook

Growth in recent years has not been uniform worldwide. Production in the United States, which

had been the dominant producer for more than 80 years, was stagnating or actually falling even

before the financial crisis: US production was 8.7 m in 2008, compared to 13.0 m in 1999. The

traditional European producers Germany, France, Spain, the UK and Italy experienced slow or

negative growth over the past decade, while production increased in newer plants in the Central

European countries. Japanese production in 2008 was11.6 m, the world leader, having finally

overtaken the US in 2006. But the most dramatic growth was in other Asian countries,

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 25

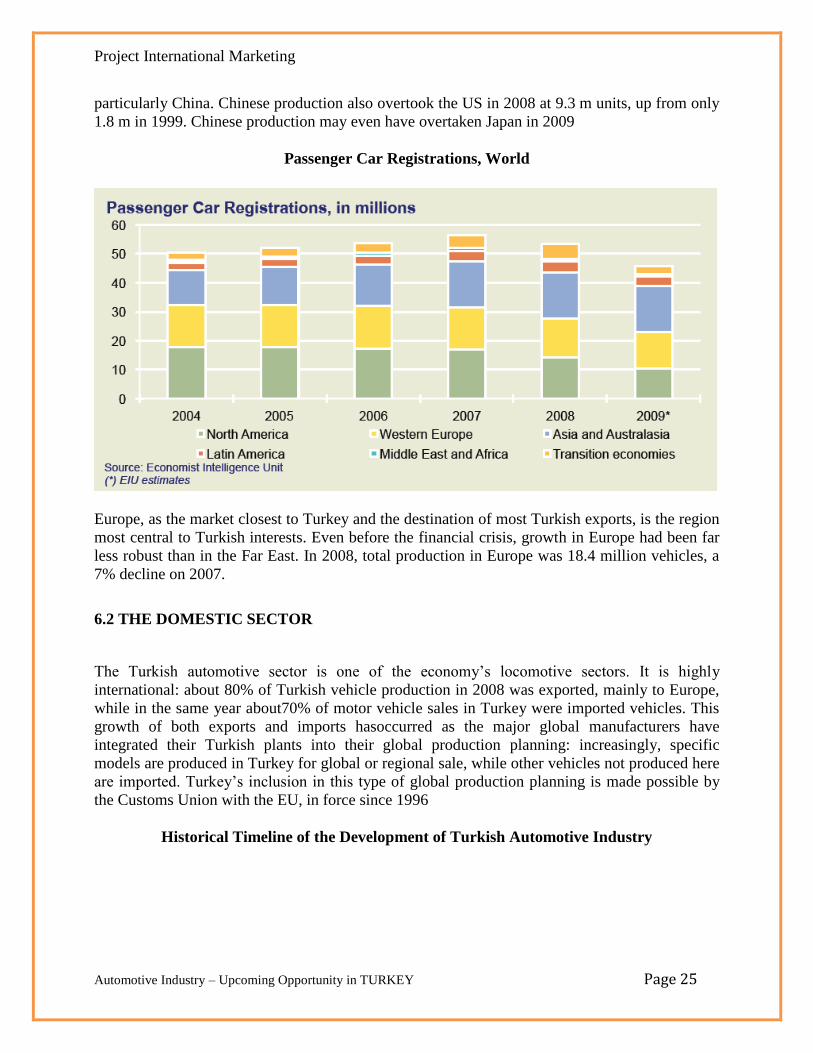

particularly China. Chinese production also overtook the US in 2008 at 9.3 m units, up from only

1.8 m in 1999. Chinese production may even have overtaken Japan in 2009

Passenger Car Registrations, World

Europe, as the market closest to Turkey and the destination of most Turkish exports, is the region

most central to Turkish interests. Even before the financial crisis, growth in Europe had been far

less robust than in the Far East. In 2008, total production in Europe was 18.4 million vehicles, a

7% decline on 2007.

6.2 THE DOMESTIC SECTOR

The Turkish automotive sector is one of the economy’s locomotive sectors. It is highly

international: about 80% of Turkish vehicle production in 2008 was exported, mainly to Europe,

while in the same year about70% of motor vehicle sales in Turkey were imported vehicles. This

growth of both exports and imports hasoccurred as the major global manufacturers have

integrated their Turkish plants into their global production planning: increasingly, specific

models are produced in Turkey for global or regional sale, while other vehicles not produced here

are imported. Turkey’s inclusion in this type of global production planning is made possible by

the Customs Union with the EU, in force since 1996

Historical Timeline of the Development of Turkish Automotive Industry

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 26

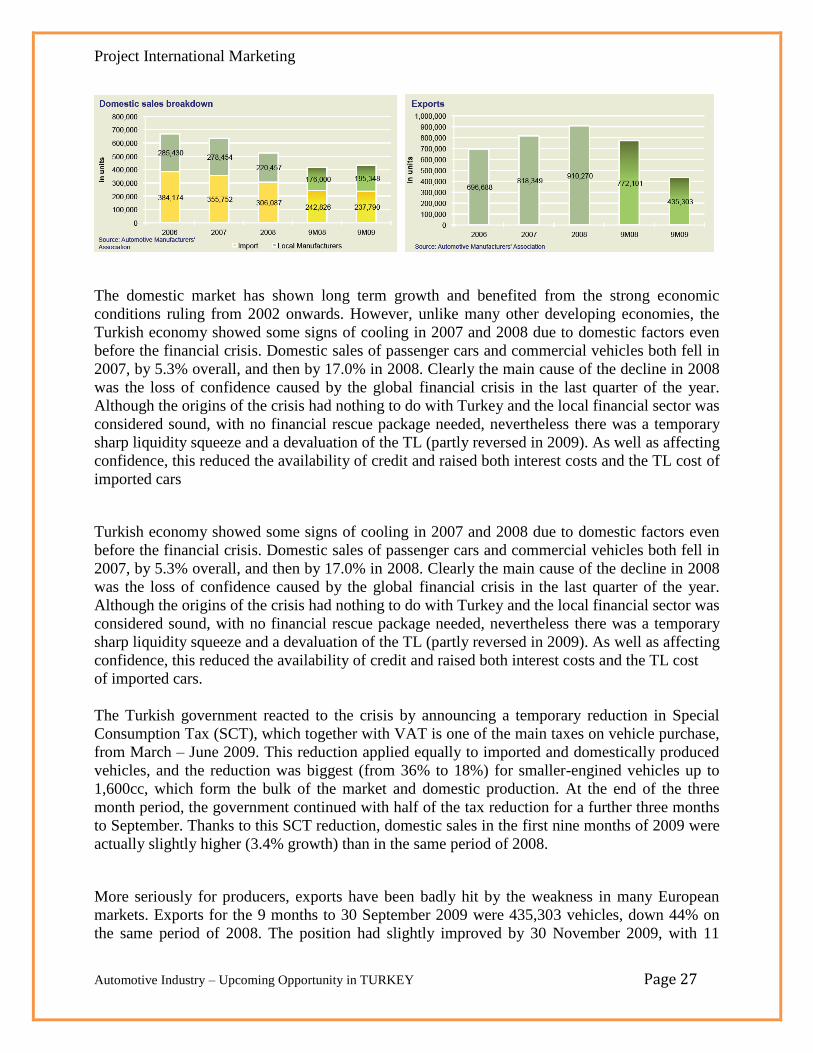

There are currently 15 passenger and commercial vehicle manufacturers in the country, in

addition to 6 tractor producers. The total capacity of the OSD members (15 manufacturers

including 2 tractor manufacturers) amounts to 1,562,405 vehicles as of 2009.8 These

manufacturers, together with the spare part producers, employ more than 230 thousand people,

ranking in the top 10 globally.9 Importers usually sell through regional distributors, who sell on

to consumers. The largest importers are Ford, GM (Opel),Volkswagen, Toyota, PSA Peugeot-

Citroën and Hyundai. There were approximately 231,000 employees in the sector as of 2007.

Turkey is the second largest exporter of vehicles to Europe after Japan, with total exports of

US$24.7 billion in 2008. This constituted 19.4% of all exports from Turkey.10 In 2008, exports

rose 10.1% to an estimated 906,230 units. Toyota, Ford Otosan, Tofas and Oyak-Renault all rank

among Turkey’s top ten exporting companies. Imports fell by 6.7% to 335,104 units in 2008, as

the domestic market was weak even before the last quarter, with the result that the net balance of

trade on automotive products was a surplus of US$8.49bn. This was an increase of 33% over

2007.

Sales and Production

Domestic Sales and Exports

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 27

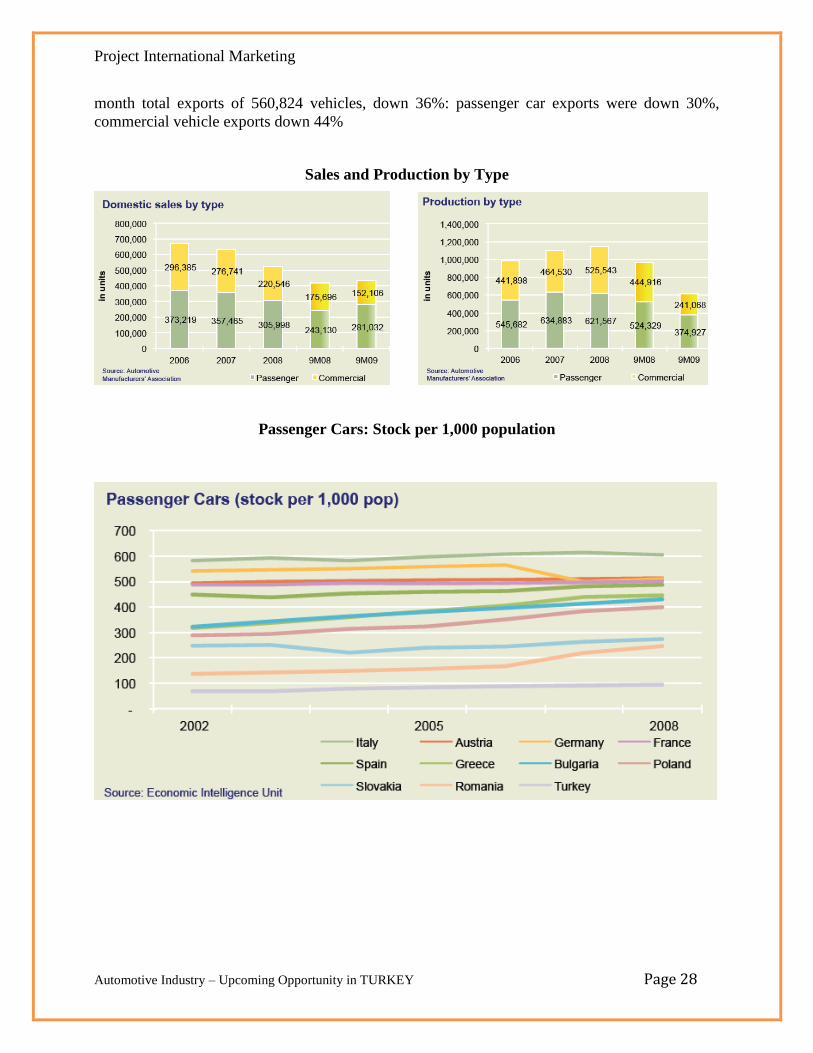

The domestic market has shown long term growth and benefited from the strong economic

conditions ruling from 2002 onwards. However, unlike many other developing economies, the

Turkish economy showed some signs of cooling in 2007 and 2008 due to domestic factors even

before the financial crisis. Domestic sales of passenger cars and commercial vehicles both fell in

2007, by 5.3% overall, and then by 17.0% in 2008. Clearly the main cause of the decline in 2008

was the loss of confidence caused by the global financial crisis in the last quarter of the year.

Although the origins of the crisis had nothing to do with Turkey and the local financial sector was

considered sound, with no financial rescue package needed, nevertheless there was a temporary

sharp liquidity squeeze and a devaluation of the TL (partly reversed in 2009). As well as affecting

confidence, this reduced the availability of credit and raised both interest costs and the TL cost of

imported cars

Turkish economy showed some signs of cooling in 2007 and 2008 due to domestic factors even

before the financial crisis. Domestic sales of passenger cars and commercial vehicles both fell in

2007, by 5.3% overall, and then by 17.0% in 2008. Clearly the main cause of the decline in 2008

was the loss of confidence caused by the global financial crisis in the last quarter of the year.

Although the origins of the crisis had nothing to do with Turkey and the local financial sector was

considered sound, with no financial rescue package needed, nevertheless there was a temporary

sharp liquidity squeeze and a devaluation of the TL (partly reversed in 2009). As well as affecting

confidence, this reduced the availability of credit and raised both interest costs and the TL cost

of imported cars.

The Turkish government reacted to the crisis by announcing a temporary reduction in Special

Consumption Tax (SCT), which together with VAT is one of the main taxes on vehicle purchase,

from March – June 2009. This reduction applied equally to imported and domestically produced

vehicles, and the reduction was biggest (from 36% to 18%) for smaller-engined vehicles up to

1,600cc, which form the bulk of the market and domestic production. At the end of the three

month period, the government continued with half of the tax reduction for a further three months

to September. Thanks to this SCT reduction, domestic sales in the first nine months of 2009 were

actually slightly higher (3.4% growth) than in the same period of 2008.

More seriously for producers, exports have been badly hit by the weakness in many European

markets. Exports for the 9 months to 30 September 2009 were 435,303 vehicles, down 44% on

the same period of 2008. The position had slightly improved by 30 November 2009, with 11

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 28

month total exports of 560,824 vehicles, down 36%: passenger car exports were down 30%,

commercial vehicle exports down 44%

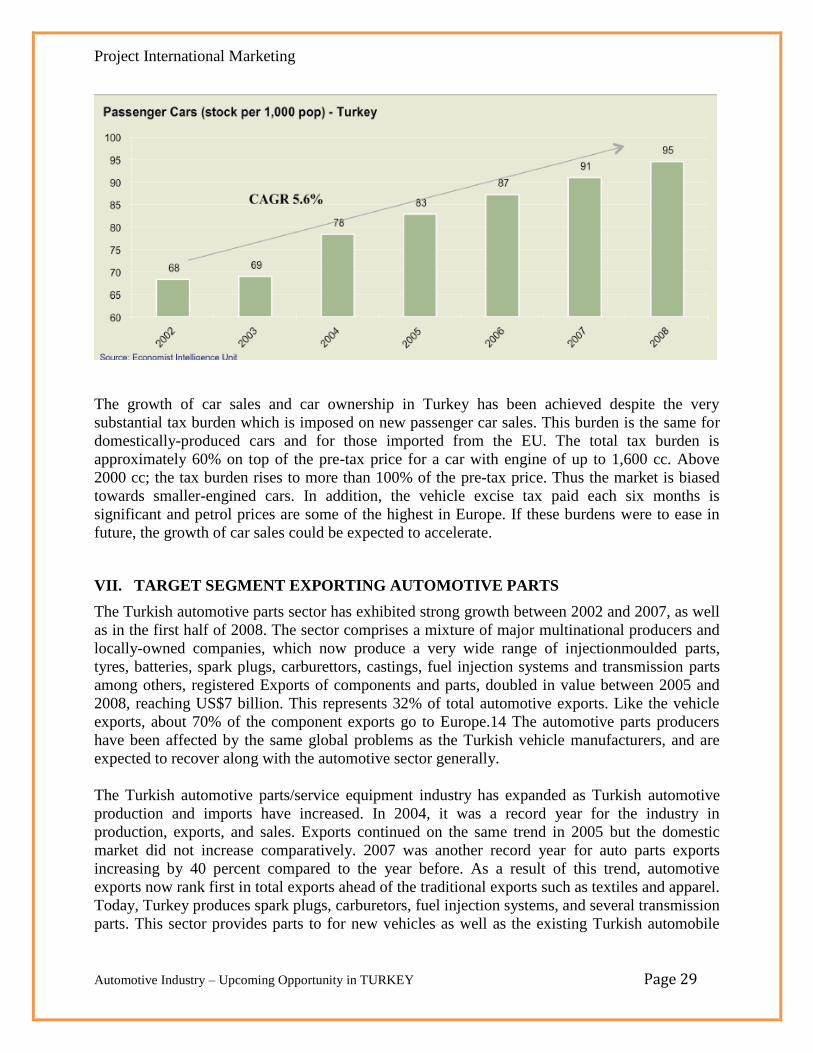

Sales and Production by Type

Passenger Cars: Stock per 1,000 population

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 29

The growth of car sales and car ownership in Turkey has been achieved despite the very

substantial tax burden which is imposed on new passenger car sales. This burden is the same for

domestically-produced cars and for those imported from the EU. The total tax burden is

approximately 60% on top of the pre-tax price for a car with engine of up to 1,600 cc. Above

2000 cc; the tax burden rises to more than 100% of the pre-tax price. Thus the market is biased

towards smaller-engined cars. In addition, the vehicle excise tax paid each six months is

significant and petrol prices are some of the highest in Europe. If these burdens were to ease in

future, the growth of car sales could be expected to accelerate.

VII. TARGET SEGMENT EXPORTING AUTOMOTIVE PARTS

The Turkish automotive parts sector has exhibited strong growth between 2002 and 2007, as well

as in the first half of 2008. The sector comprises a mixture of major multinational producers and

locally-owned companies, which now produce a very wide range of injectionmoulded parts,

tyres, batteries, spark plugs, carburettors, castings, fuel injection systems and transmission parts

among others, registered Exports of components and parts, doubled in value between 2005 and

2008, reaching US$7 billion. This represents 32% of total automotive exports. Like the vehicle

exports, about 70% of the component exports go to Europe.14 The automotive parts producers

have been affected by the same global problems as the Turkish vehicle manufacturers, and are

expected to recover along with the automotive sector generally.

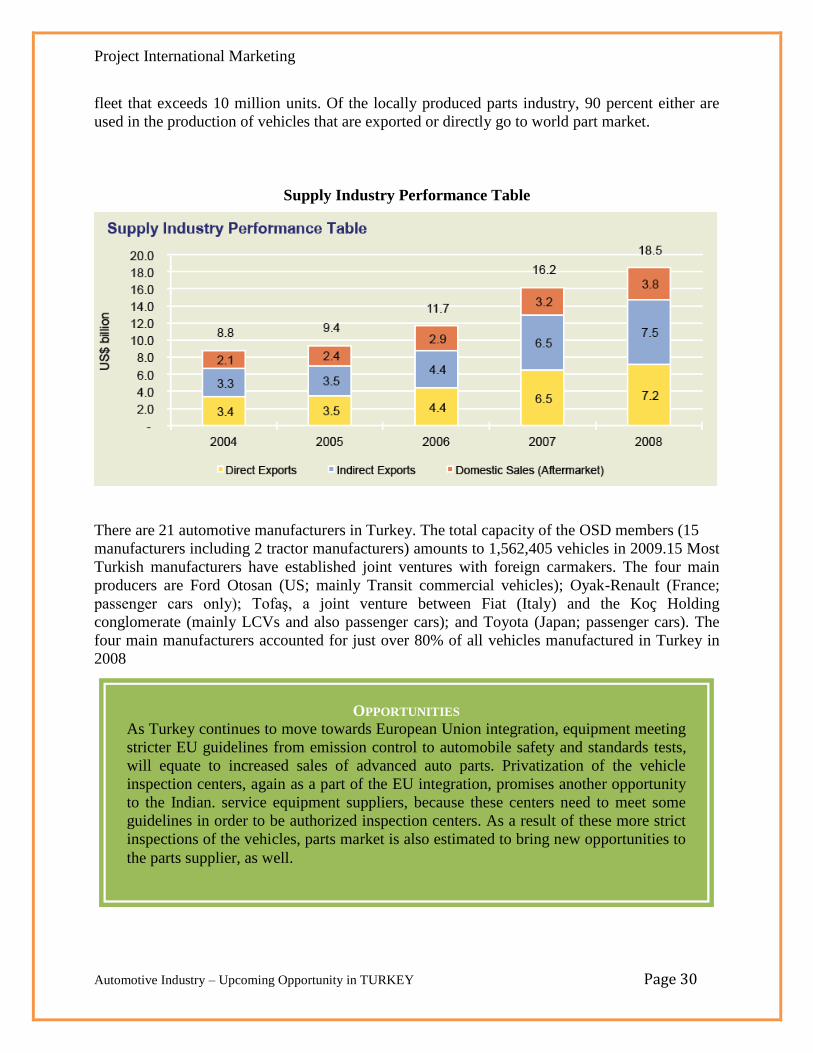

The Turkish automotive parts/service equipment industry has expanded as Turkish automotive

production and imports have increased. In 2004, it was a record year for the industry in

production, exports, and sales. Exports continued on the same trend in 2005 but the domestic

market did not increase comparatively. 2007 was another record year for auto parts exports

increasing by 40 percent compared to the year before. As a result of this trend, automotive

exports now rank first in total exports ahead of the traditional exports such as textiles and apparel.

Today, Turkey produces spark plugs, carburetors, fuel injection systems, and several transmission

parts. This sector provides parts to for new vehicles as well as the existing Turkish automobile

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 30

fleet that exceeds 10 million units. Of the locally produced parts industry, 90 percent either are

used in the production of vehicles that are exported or directly go to world part market.

Supply Industry Performance Table

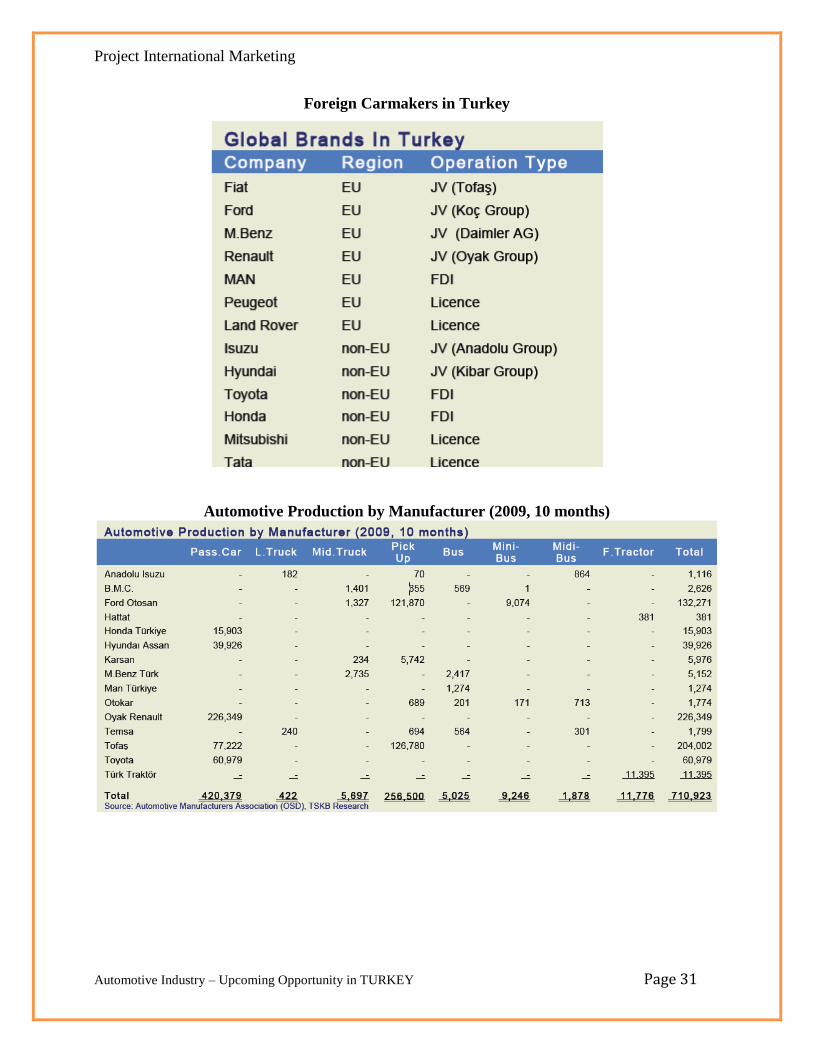

There are 21 automotive manufacturers in Turkey. The total capacity of the OSD members (15

manufacturers including 2 tractor manufacturers) amounts to 1,562,405 vehicles in 2009.15 Most

Turkish manufacturers have established joint ventures with foreign carmakers. The four main

producers are Ford Otosan (US; mainly Transit commercial vehicles); Oyak-Renault (France;

passenger cars only); Tofaş, a joint venture between Fiat (Italy) and the Koç Holding

conglomerate (mainly LCVs and also passenger cars); and Toyota (Japan; passenger cars). The

four main manufacturers accounted for just over 80% of all vehicles manufactured in Turkey in

2008

OPPORTUNITIES

As Turkey continues to move towards European Union integration, equipment meeting

stricter EU guidelines from emission control to automobile safety and standards tests,

will equate to increased sales of advanced auto parts. Privatization of the vehicle

inspection centers, again as a part of the EU integration, promises another opportunity

to the Indian. service equipment suppliers, because these centers need to meet some

guidelines in order to be authorized inspection centers. As a result of these more strict

inspections of the vehicles, parts market is also estimated to bring new opportunities to

the parts supplier, as well.

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 31

Foreign Carmakers in Turkey

Automotive Production by Manufacturer (2009, 10 months)

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 32

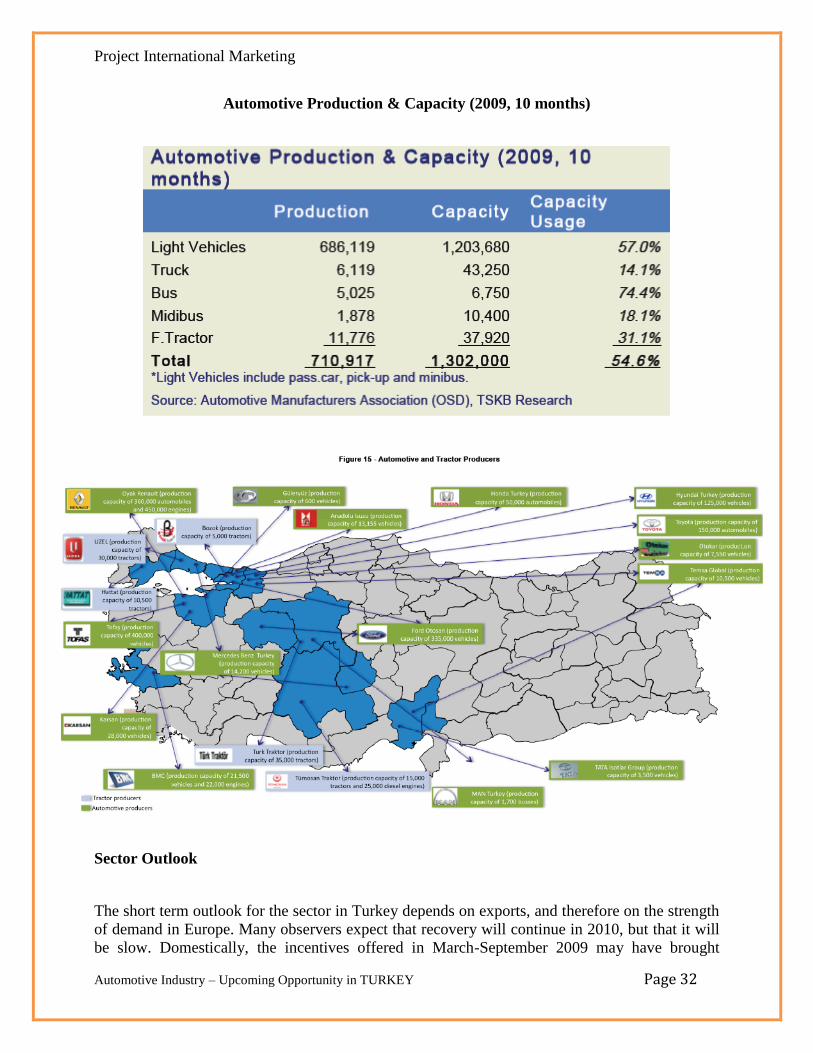

Automotive Production & Capacity (2009, 10 months)

Sector Outlook

The short term outlook for the sector in Turkey depends on exports, and therefore on the strength

of demand in Europe. Many observers expect that recovery will continue in 2010, but that it will

be slow. Domestically, the incentives offered in March-September 2009 may have brought

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 33

forward sales, but from the second half of 2010 domestic demand patterns are likely to resume

their former stability and then growth. Monthly sales should become more stable in 2010,

enabling more efficient and profitable production planning. Once the effects of the global

financial crisis start to weaken, it is expected that the Turkish automotive sector will pick up to

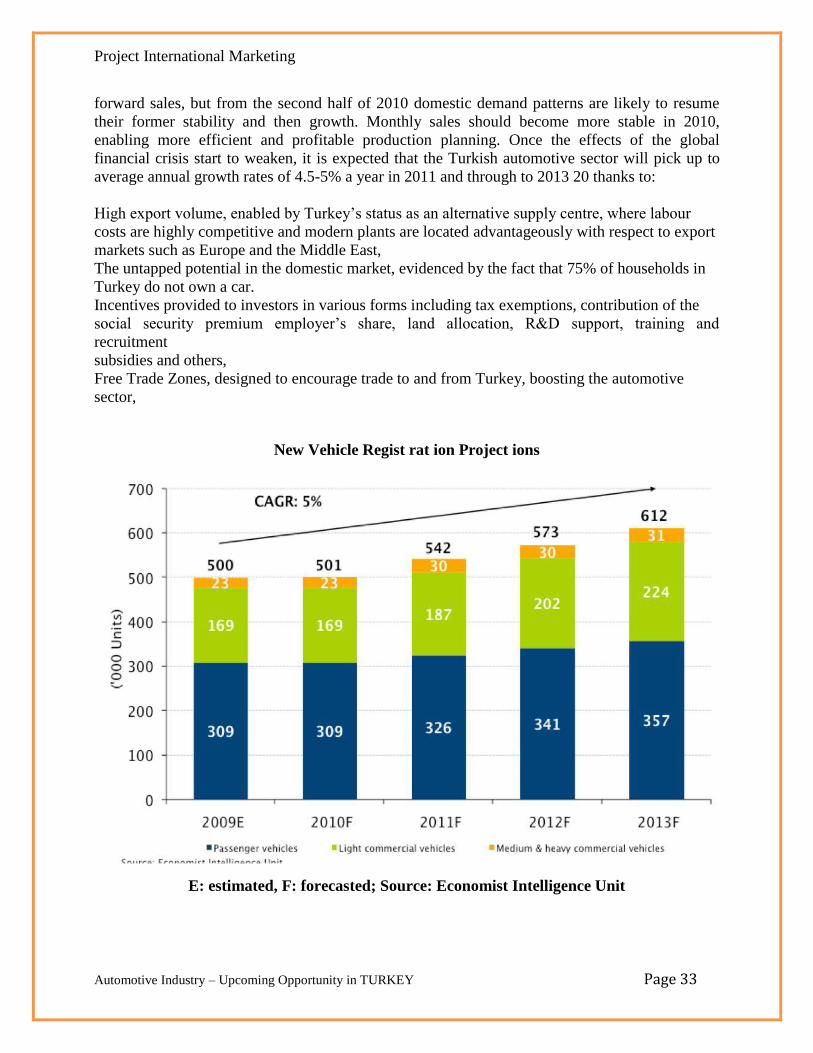

average annual growth rates of 4.5-5% a year in 2011 and through to 2013 20 thanks to:

High export volume, enabled by Turkey’s status as an alternative supply centre, where labour

costs are highly competitive and modern plants are located advantageously with respect to export

markets such as Europe and the Middle East,

The untapped potential in the domestic market, evidenced by the fact that 75% of households in

Turkey do not own a car.

Incentives provided to investors in various forms including tax exemptions, contribution of the

social security premium employer’s share, land allocation, R&D support, training and

recruitment

subsidies and others,

Free Trade Zones, designed to encourage trade to and from Turkey, boosting the automotive

sector,

New Vehicle Regist rat ion Project ions

E: estimated, F: forecasted; Source: Economist Intelligence Unit

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 34

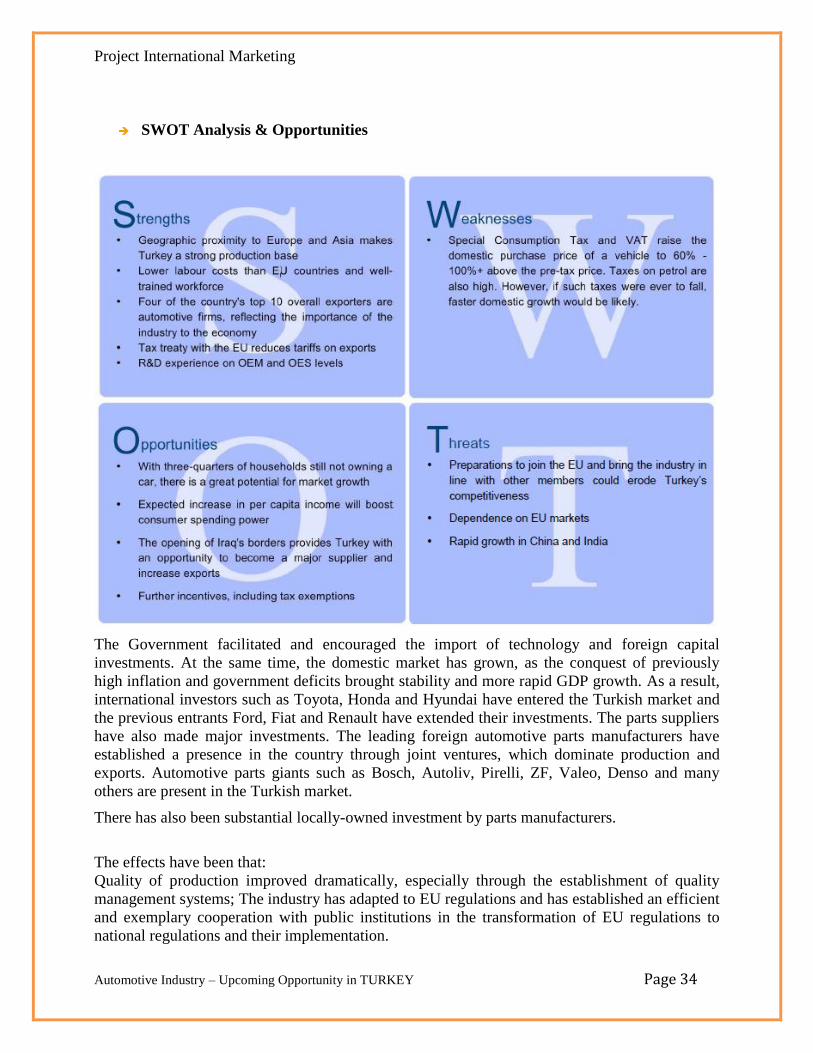

SWOT Analysis & Opportunities

The Government facilitated and encouraged the import of technology and foreign capital

investments. At the same time, the domestic market has grown, as the conquest of previously

high inflation and government deficits brought stability and more rapid GDP growth. As a result,

international investors such as Toyota, Honda and Hyundai have entered the Turkish market and

the previous entrants Ford, Fiat and Renault have extended their investments. The parts suppliers

have also made major investments. The leading foreign automotive parts manufacturers have

established a presence in the country through joint ventures, which dominate production and

exports. Automotive parts giants such as Bosch, Autoliv, Pirelli, ZF, Valeo, Denso and many

others are present in the Turkish market.

There has also been substantial locally-owned investment by parts manufacturers.

The effects have been that:

Quality of production improved dramatically, especially through the establishment of quality

management systems; The industry has adapted to EU regulations and has established an efficient

and exemplary cooperation with public institutions in the transformation of EU regulations to

national regulations and their implementation.

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 35

Exports have risen sharply, and Turkish production has been integrated into manufacturers’

global planning. The export potential of the automotive parts sector, coupled with the presence of

major international automotive manufacturers, has attracted an increasing number of foreign

investors.

The Turkish automotive market, comprised of

passenger cars, commercial vehicles, tractors, and

automotive components sub-segments, offers foreign

investors attractive investment opportunities, from

automotive and components manufacturing

(particularly viable for aftermarket and 1st tier

suppliers) to joint production development for global

car models, R&D and testing houses, technology

transfer, as well as in electronics – diagnostics,

safety (air bags, side protection systems), lighting

(HID - Xenon), security (theft protection devices),

comfort (smart seating), audio / navigation and larger

and sophisticated moulds.

Indian Manufaturer in Turkey Market

Indian Tractor Industry Leader Tafe Makes a

Greenfield Investment in Manisa Industrial Zone

Istanbul, October 13, 2008 - The Investment

Support and Promotion Agency of Turkey

(ISPAT) and India's leading tractor manufacturer Tractors and Farm Equipment Limited (TAFE),

today jointly announced TAFE's decision to invest in a tractor assembly/manufacturing facility in

Manisa Organized Industrial Zone, with plans to manufacture 15,000 tractors per year. While

investment plans are being finalized, in order to launch a full range of tractors (from 45 to 80 HP)

for the Turkish market at the earliest, production will start initially with the support of aggregates

from TAFE's plants in India, while production is expected to start in the first quarter of 2009.

TAFE, an Indian JV based at Chennai, is the world's second largest manufacturer of tractors in

the sub 100 HP range with an annual production and sales of 80,000 units in India, South Asia,

Africa and North America. With a history of designing, manufacturing and marketing tractors

around fifty years, and nearly a million satisfied tractor customers, TAFE has vast experience in

manufacturing tractors to suit every possible type of agro-climatic condition and operation in

the small and medium HP range.

TAFE is the first Indian manufacturer to set up a manufacturing base in Turkey. The company

has chosen to locate its new plant in Manisa, which in addition to its strategic location, has

Key factors which attract foreign

capital inflows to Turkey

mainly include; the market size,

consumer composition, friendly

investment legislation and liberal

banking system together with other

attractiveness arising from highly

skilled human resources in

production and management, the

unsaturated domestic market with

high potential, easy access to

neighbouring (regional) emerging

markets, and low labour cost..

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 36

excellent infrastructure. Commenting on the issue, Mallika Srinivasan, TAFE's Director and CEO

said, ―The tractor market in Turkey is of great significance to us as its composition is well within

our experience and manufacturing range. Turkey is an investor friendly country and we have

been welcomed and assisted in our investment proposals by the authorities at the Manisa

Organized Industrial Zone as well as directly by the Prime Minister's office at Ankara. With

ISPAT's support, we are confident in beginning manufacturing operations by the first quarter of

2009‖. Manisa is well located in terms of proximity to the well-developed automotive component

manufacturing base in Turkey and TAFE is expected to leverage this for its local as well as

global requirements. It is worth noting that over 2,000 TAFE tractors are already in operation in

Turkey and that negotiations for sales and distribution of tractors from the new plant are in

progress with a world leader in agricultural equipment, while final arrangements are expected to

be announced shortly.

India’s Wipro signs strategic cooperation deal with AS/Nexia Turkey

Turkiye - India’s IT solutions provider Wipro, has signed a strategic cooperation deal with

AS/Nexia Turkey, an auditing and consultancy firm. The cooperation between Turkish and

Indian companies first came about during Turkish President Abdullah Gul’s official visit to India,

where Gul invited the Indian company to invest in Turkey. Wipro and AS/Nexia Turkey will

cooperate in providing consultancy services in Turkey’s energy sector. Having a market value of

around USD 30 billion, Wipro is one of the largest IT companies in India, with stocks traded in

the Indian and New York stock markets.

V1II BEFORE INVESTING IN TURKEY

General Business Environment

DUE TO THE LACKS OF THE CERTAİNTY AND PREDİCTABİLİTY OF THE LAW AND

TRANSPARENCY CATCHİNG İNVESTORS DEPENDS ON PROVİDİNG HİGH YİELD AND

TAXİNCENTİVES.

SELECTIVE APPLICATION OF THE LAW. POOR BUSINESS ETHICS. THE CONCEPT OF

A WRITTEN "CONTRACT" IS NOT MAINSTREAMED. TURKEY WILL ALWAYS HAVE

GREAT POTENTIAL. I WONDER IF THEY WILL EVER REACH THAT POTENTIAL.

THE BUSINESS ENVIRONMENT IS UNPREDICTABLE DUE TO HEAVY GOVERNMENT

INVOLVEMENT IN EVERY ASPECT OF THE BUSINESS LIFE. PERMITS REQUIRED FOR

MANY BUSINESS DEVELOPMENT INITIATIVES ARE HINDERED BY UNCERTAINTIES

IN THE OFFICIAL PROCEDURES, SUB-STANDARD GOVERNMENT INSTUTION

CAPACITIES, CONSTANTLY REPEALED REGULATIONS/LAWS, TECHNICAL

INCOMPETENCE OF GOVERNMENTAL WORKERS, AND INAPTNESS OF COURTS IN

TECHNICAL MATTERS, LACK OF OBJECTIVE AND STANDARDIZED

APPROACHES/PROCEDURES. MOST OF THE DAY-TO-DAY WORK INVOLVING

GOVERNMENT (WHETHER LOCAL OR CENTRAL) REQUIRES KNOWING THE "RIGHT"

PEOPLE IN GOVERNMENTAL ORGANIZATIONS.

THE FACT THAT INTELLECTUAL PROPERTY IS NOT ADOPTED PREVENTS EVERY

KIND OF INTELLECTUAL CAPITAL INVESTMENT

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 37

PRIMAL INVESTMENT COSTS AND RISKS ARE HIGH. THAT GENERATES QUESTION

MARKS ABOUT THE RETURN OF THE INVESTMENT AND AGGRAVATES

CONVINCING THE INTERNATIONAL CENTER

Macroeconomics

TAXES ARE TOO HIGH. PUBLIC ENTITIES WITH STRONG MACROECONOMIC

FUNCTION SUCH AS SGK AND TEIAS DELAYING PAYMENTS. CONTINUING

POPULIST IMPLEMENTATIONS AT MUNICIPAL LEVELS DRAWING ON RESOURCES.

TRADE DEFICIT IS UNSUSTAINABLE.LINKAGES TO NEIGHBORING EMERGING

MARKETS WILL BRING THE BIGGESTS GAINS

DETERMINED AND DISCIPLINED APPLICATION OF FISCAL POLICY IN

COORDINATION WITH THE MONETARY POLICY WILL PAY OFF IN THE LONGER

TERM. IT SEEMS THAT THE FISCAL SIDE IS QUITE WEAK AND IS LACKING AN

ANCHOR.

STILL RISKS TO INFLATION/INTEREST RATES FROM GOVERNMENT SPENDING

POLICIES AND LACK OF IMF PROGRAM.

EXTERNAL DEMAND NARROWNESS AND THE DİFFİCULTİES LİVED BY EXPORTERS

ARE THE MOST PRİMAL ECONOMİC PROBLEMS. THE STRONGEST SİDE İS THE FACT

THAT BANKİNG SECTOR İS AFFECTED MİNİMUM FROM THE GLOBAL CRİSİS.

Taxation

TAX SYSTEM: THERE ARE HIDDEN TAXES. THERE IS ALWAYS AN ADDITIONAL FEE

ETC WHICH INCREASES THE OVERALL TAX BURDEN AND COMPLICATES THE

BUSINESS TRANSACTIONS. FOR EXAMPLE, STAMP TAX LEVIED ON BUSINESS

CONTRACTS. THE INDIRECT TAXES (SALES AND OTHER) SUCH AS THOSE APPLIED

TO TELECOMMUNICATION BILLS, ETC. ARE ALSO RATHER HIGH. FURTHER TO

GOVERNMENTAL AGENCIES TAXES THERE ARE SEMI-OFFICIAL INSTITUTIONS

THAT CHARGE FEES THAT ARE MANDATORY BY LAW. FOR EXAMPLE, TRADE

CHAMBERS CHARGE MANDATORY ANNUAL FEES AS PERCENTAGE OF COMPANY

REVENUE. SIMILARLY ENGINEERING CHAMBERS ALSO CHARGE CERTAIN

MANDATORY AMOUNTS. THE PROBLEM IS NOT THE FEES, BUT WE DO "NOT" GET

IN RETURN AS A SERVICE. THEN THERE IS MANDATORY NOTARY FEES WHICH ARE

VERY HIGH

INTERNATIONAL INVESTORS AND CORPORATIONS ARE PENALIZED BY HIGHER

RATES OF TAX THAT ARE NOT COMPETITIVE WITH LOWER TAX COUNTRIES LIKE

SINGAPORE OR IRELAND. THE REDUCTION IN CORPORATE TAXATION WAS A GOOD

START, BUT THE ORGANIZED, CORPORATE SECTOR IS SUBSIDIZING THE INFORMAL

SECTOR -- EFFORTS TO ADDRESS TAX EVASION IN THE INFORMAL SECTOR IS

WELCOMED, BUT WE SHOULD ALSO BE ASKING IF TAXING PRODUCTION, CAPITAL

AND INVESTMENT IS BETTER THAN TAXING CONSUMPTION, IN TERMS OF

ENCOURAGING ECONOMIC GROWTH

TURKEY İS NOT A DEVELOPED COUNTRY AND DO NOT HAVE A STRUCTURE WHİCH

CAN TOLERATE HEAVY TAXES. SİNCE TAXES ARE NOT COLLECTED FROM THE

REVENUES GENERALLY, CONSUMPTİON TAXES ARE VERY HİGH. BESİDES,

İNSTİTUTİONS WHO PAYS THE TAXES VİA REVENUES AND PEOPLE PAY TAXES

TWİCE

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 38

TAX AND EMPLOYMENT ARE İN DİRECT PROPORTİON. UNFORTUNATELY, PRESENT

TAX RATES CAUSES UNFAİR COMPETİTİON AND TAX EVASİON.

INCOME TAXES ARE AT PAR WITH MATURE MARKETS; HOWEVER, STATE BENEFITS

ARE VERY LOW COMPARED TO THE TAXES PAID.

Legal System

IT IS BETTER TO SETTLE DISPUTES OUTSIDE OF THE COURTS IF POSSIBLE. THE

COURTS ARE TOO SLOW TO REACT. IN MATTERS OF TECHNICAL ISSUES, THE

COURTS ARE INCOMPETENT. CERTAIN COURTS ARE BIASED IN THEIR DECISIONS

CULTURE OF TRADEMARK PROTECTION HAS TO BE STRENGTHEN

DELAYS IN THE JURIDICAL PROCESSES AND DISCRIMINATION OF LOCAL VS.

FOREIGN IN MINDS ARE IMPORTANT PROBLEMS

IMPLEMENTATİONS ABOUT THE COPRİGHTS AND PATENTS SHOULD BE

ELABORATED İN AN İNTERNATİONAL LEVEL

CASES TAKES A LONG TİME. THERE ARE NO EXPERT JUDGES ABOUT THE İSSUES

AND GENERALLY THE SYSTEM CONDUCTS İNCH ALONG. RESULTİNG OF THE

CASES TAKES YEARS. THAT ENFORCES THE TURKEY'S COMPETİTİON ADVANTAGE

Workforce

DO NOT FİND THE DİSPLACEMENT DECİSİON OF THE COURT FAİR. WORKERS ARE

PROTECTED MORE THAN ADEQUATE AND EMPLOYERS ARE MİSTREATED.

FİSCAL BURDENS ON THE EMPLOYMENT İS STİLL VERY HEAVY. LABOUR COURTS

ALWAYS DECİDE İN FAVOUR OF THE WORKERS

THE LAW AND COURTS ARE BIASED IN FAVOR OF DISMISSED EMPLOYEES, SO

INVESTORS AND EMPLOYERS ARE HESISTANT TO HIRE, BECAUSE DISMISSALS FOR

POOR PERFORMANCE OR UNETHICAL

BEHAVIOR CAN STILL END UP COSTING COMPANIES A LOT OF MONEY WHEN

COURTS SIDE WITH DISMISSED EMPLOYEES, WHICH IS THE RESULT IN THE

MAJORITY OF CASES.

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 39

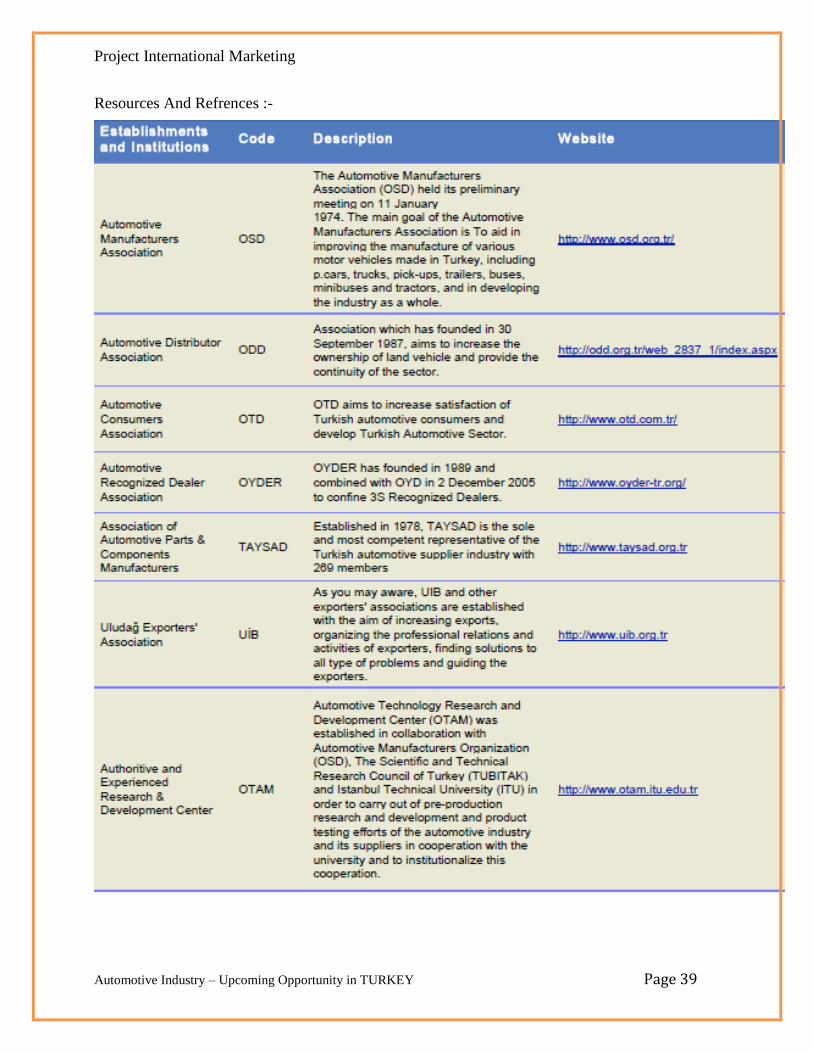

Resources And Refrences :-

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 40

Other Sources :-

w w w . e m p a d v i s e r s . c o m

http://www.buyusa.gov/turkey/en/doing_business_in_turkey.html

http://www.allaboutturkey.com/info.htm

http://www.invest.gov.tr

http://commerce.nic.in

http://www.usemb-ankara.org.trd

Project International Marketing

Automotive Industry – Upcoming Opportunity in TURKEY Page 41

Abbreviations

ACEA The European Automobile Manufacturers Association