investment , insurance and you - fpam · bancassurance the purpose of this presentation is to...

TRANSCRIPT

Bancassurance

INVESTMENT , INSURANCE

and YOU

October 14, 2010

Bancassurance

The purpose of this presentation is to enhance investor awareness of

ILP.

INVESTMENT LINKED PRODUCTS

2

Bancassurance

The Need of a Retiree

What are the risks?

1.Death / Disabilities / Critical Illnesses

2.Hospitalization and other routine medical

expense.

3.Large dependency on debt

4.Unavailability of income is disastrous for

families

5.Accumulation of small amounts in large sums

for future needs i.e. saving

What is needed is risk mitigation

Bancassurance

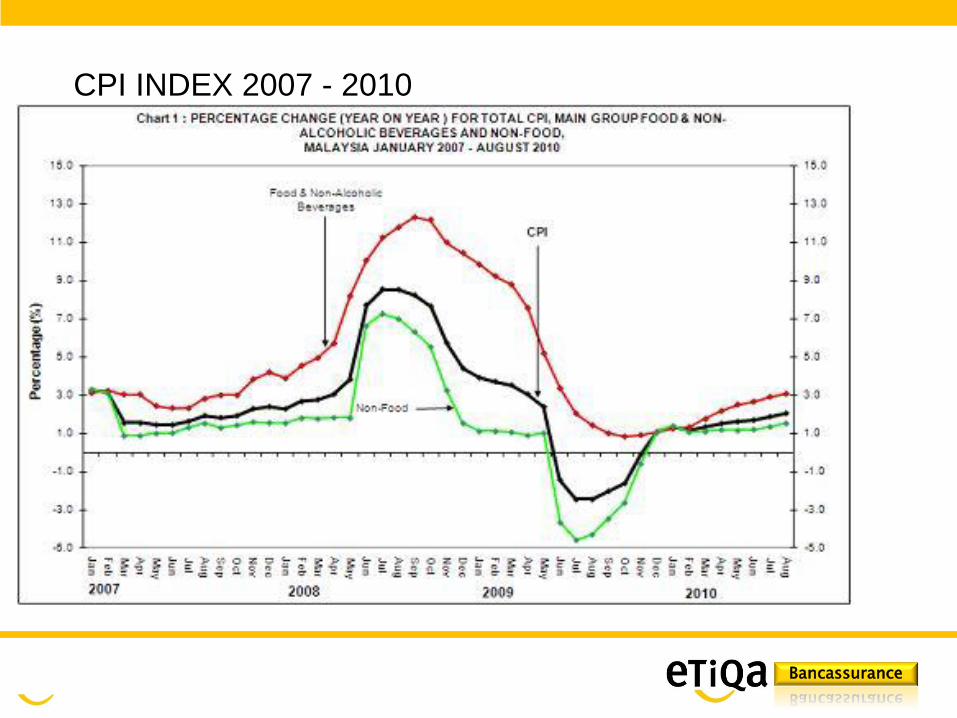

Cost of living is increasing every year!

Petrol price up 5 cents Sugar price up

25 cents / kg

AUGUST

2010

CPI UP 2.1%

Agt AUG

2009

Bancassurance

CPI INDEX 2007 - 2010

Bancassurance

Cost of a pack of Cigarettes 20 sticks wef 4 Oct 2010

RM 10.00

Bancassurance

Comparison between 12-month FD rate against Malaysia’s

Inflation Rate (%)

Sources: Alliance Research

CP

I

FD

Current FD rates are still relatively low (3.20% pa. for 12 months tenure)

Bancassurance

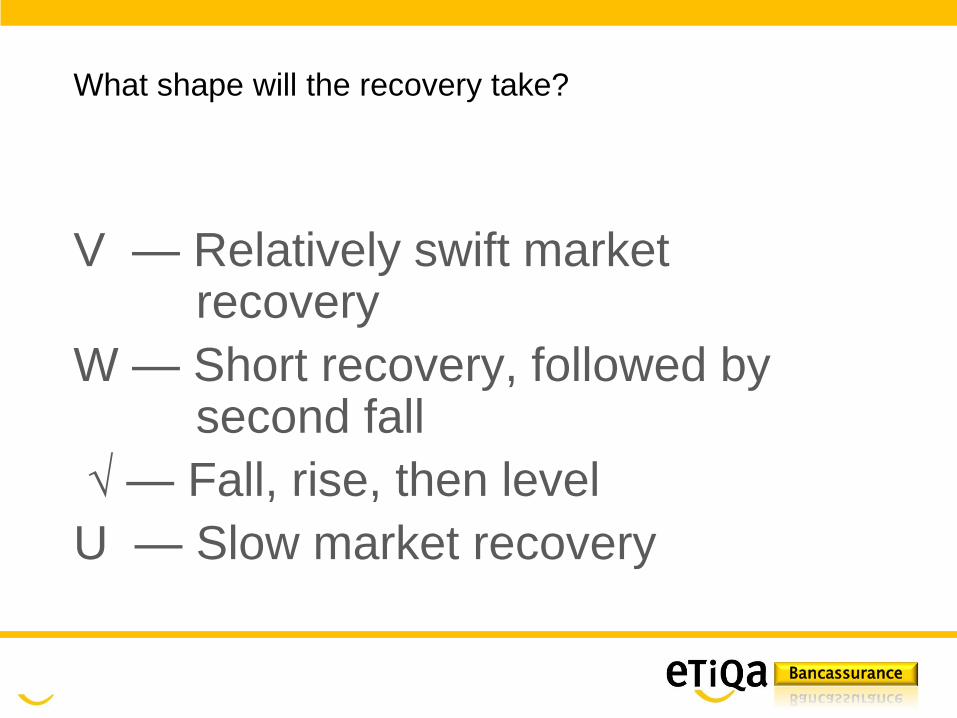

What shape will the recovery take?

V — Relatively swift market recovery

W — Short recovery, followed by second fall

√ — Fall, rise, then level

U — Slow market recovery

Bancassurance

CURRENT ISSUES

PRICES OF HOUSES

MEDIAN PRICE OF TWO TO THREE

STOREY TERRACED HOUSES*

Location 2006 2007 2008 2009 2010 %

Penang 198,000 221,000 253,000 236,500 250,000 26.26

Kuala

Lumpur

340,000

355,000 350,000 342,000 410,000 20.58

Petaling

Jaya

315,000 340,000 350,000 338,000 400,000 26.98

Johor

Bharu

168,050 180,000 195,000 187,000 190,000 13.06

SOURCE : Data for 2010 NATIONAL PROPERTY INFORMATION CENTRE FINANCE MINISTRY

Bancassurance

Life Expectancy

As scientists identify new remedies for life-shortening ailments we can expect to see life expectancy continuing to lengthen year after year. Since 1945 life expectancy of citizens living in the wealthier countries around the world has increased by one year in every five. The American Life Extension Institute believes that average life expectancy in the U.S. will reach 100 by 2029,in just 21 years. Some scientists hold strong views that ageing is a curable disease and that in our own lifetimes it may be curable and life expectancy of even mature adults extend to 500 or even 1,000 years of age 40. Even a fraction of this life expectancy increase challenges any idea that we should retire in our 60’s. But of course there are always pandemics, which we are warned to be alert for, which could wipe out millions of people in a few months. The last major worldwide pandemic was the influenza outbreak of 1918, when around 40 million people died. The other current challenger to an older workforce is obesity, a by-product of our wealthier and more sedentary lifestyles.

MALAYSIA LIFE EXPECTANCY is 75

Bancassurance

Structure of ILP

Bancassurance

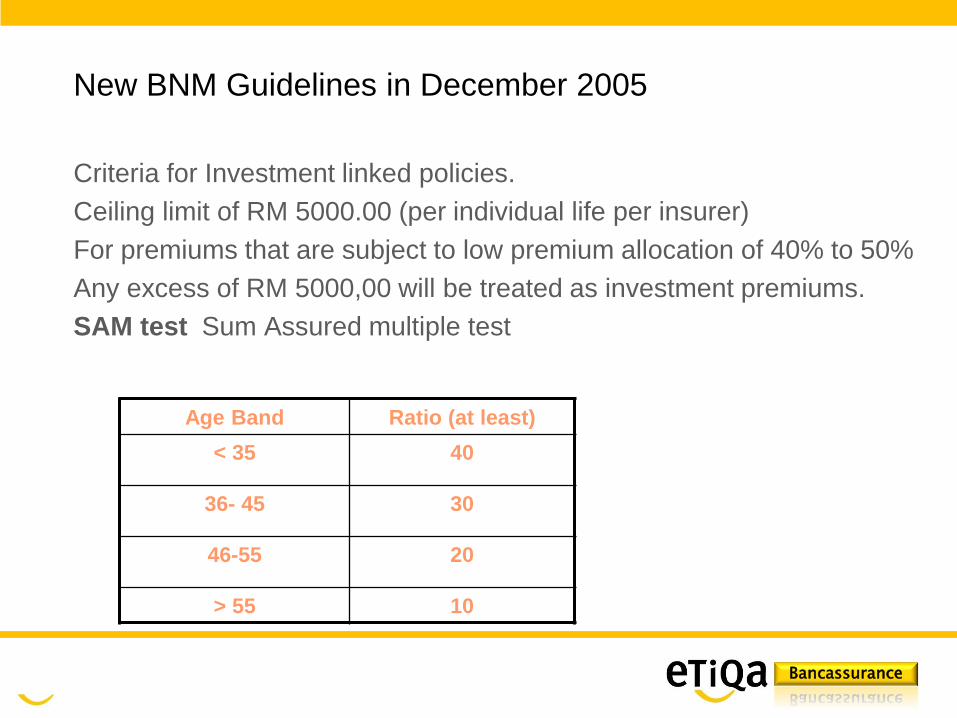

New BNM Guidelines in December 2005

Criteria for Investment linked policies.

Ceiling limit of RM 5000.00 (per individual life per insurer)

For premiums that are subject to low premium allocation of 40% to 50%

Any excess of RM 5000,00 will be treated as investment premiums.

SAM test Sum Assured multiple test

Age Band Ratio (at least)

< 35 40

36- 45 30

46-55 20

> 55 10

Bancassurance

What IF ?

BEST LOCKED IN FD RETURN ?

BEST INVESTMENT RETURN FROM

EQUITY MARKET

Bancassurance

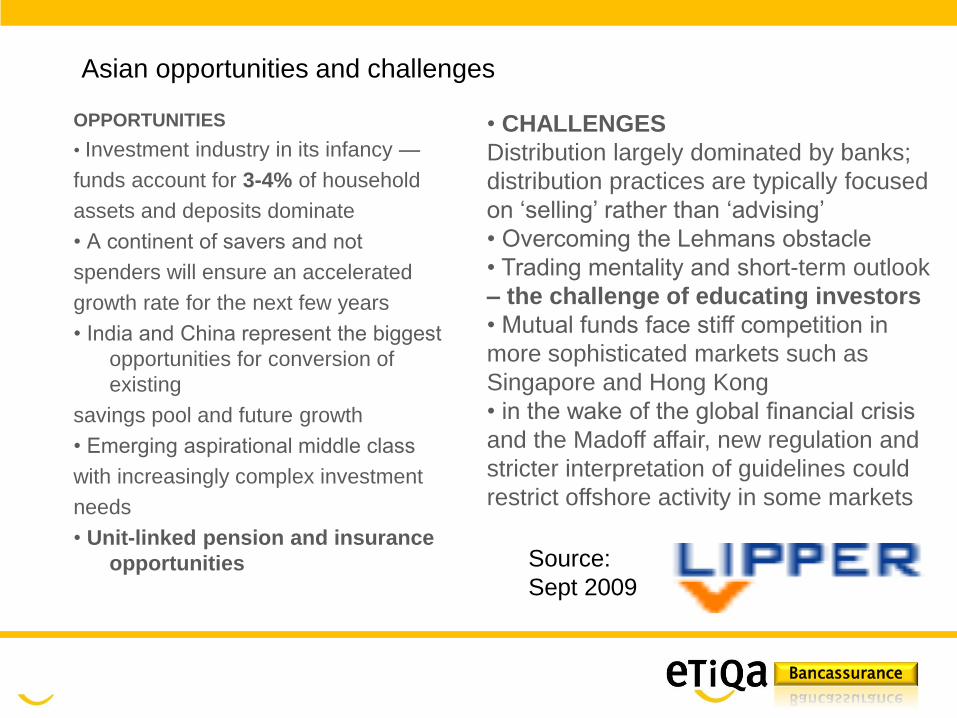

Asian opportunities and challenges

OPPORTUNITIES

• Investment industry in its infancy —

funds account for 3-4% of household

assets and deposits dominate

• A continent of savers and not

spenders will ensure an accelerated

growth rate for the next few years

• India and China represent the biggest

opportunities for conversion of

existing

savings pool and future growth

• Emerging aspirational middle class

with increasingly complex investment

needs

• Unit-linked pension and insurance

opportunities

• CHALLENGES

Distribution largely dominated by banks;

distribution practices are typically focused

on ‘selling’ rather than ‘advising’

• Overcoming the Lehmans obstacle

• Trading mentality and short-term outlook

– the challenge of educating investors

• Mutual funds face stiff competition in

more sophisticated markets such as

Singapore and Hong Kong

• in the wake of the global financial crisis

and the Madoff affair, new regulation and

stricter interpretation of guidelines could

restrict offshore activity in some markets

Source:

Sept 2009

Bancassurance

IN NEWS

Bancassurance

RINGGIT VS US

Bancassurance

FBM KLCI

Bancassurance

V50, The VIP investment

Which diamonds can you pick for the flexible investments in

V50?

The “hand picked” funds:

For Professional Investors Only

GROWTH

STABLE

BALANCE

Bancassurance

V50, The VIP investment

FLEXIBLE INVESTMENT

For Professional Investors Only

Bancassurance

Etiqa experience

BANCASSURANCE and BANCATAKAFUL

20

Bancassurance 21

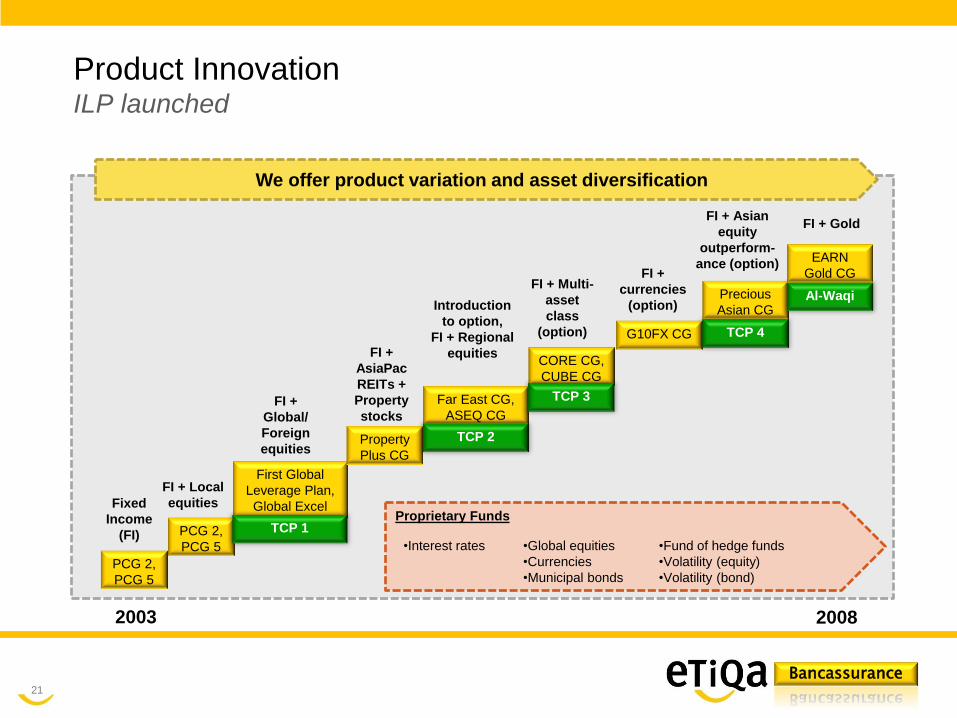

Product Innovation ILP launched

2003 2008

We offer product variation and asset diversification

Proprietary Funds

•Interest rates •Global equities

•Currencies

•Municipal bonds

•Fund of hedge funds

•Volatility (equity)

•Volatility (bond)

FI + Local

equities

PCG 2,

PCG 5

PCG 2,

PCG 5

Fixed

Income

(FI)

FI +

Global/

Foreign

equities

First Global

Leverage Plan,

Global Excel

FI +

AsiaPac

REITs +

Property

stocks

Property

Plus CG

Introduction

to option,

FI + Regional

equities

Far East CG,

ASEQ CG

FI + Multi-

asset

class

(option)

CORE CG,

CUBE CG

FI +

currencies

(option)

G10FX CG

FI + Asian

equity

outperform-

ance (option)

Precious

Asian CG

TCP 1

TCP 3

TCP 2

TCP 4

FI + Gold

EARN

Gold CG

Al-Waqi

Bancassurance

Takaful Investment-linked fund size of RM mil

22

3-year CAGR of 9.4%

Growth 21.1% 34.7% -19.8% 45.2%

Bancassurance

About Takaful Investment-linked

23

Bancassurance 24

Local Policymaker Set the Direction – Regulated Business BNM addresses basic requirements and customer protection

Fees / Charges

and Expenses Disclosures

Investment

Guidelines on

Investment-

linked Takaful

Business

Bancassurance 25

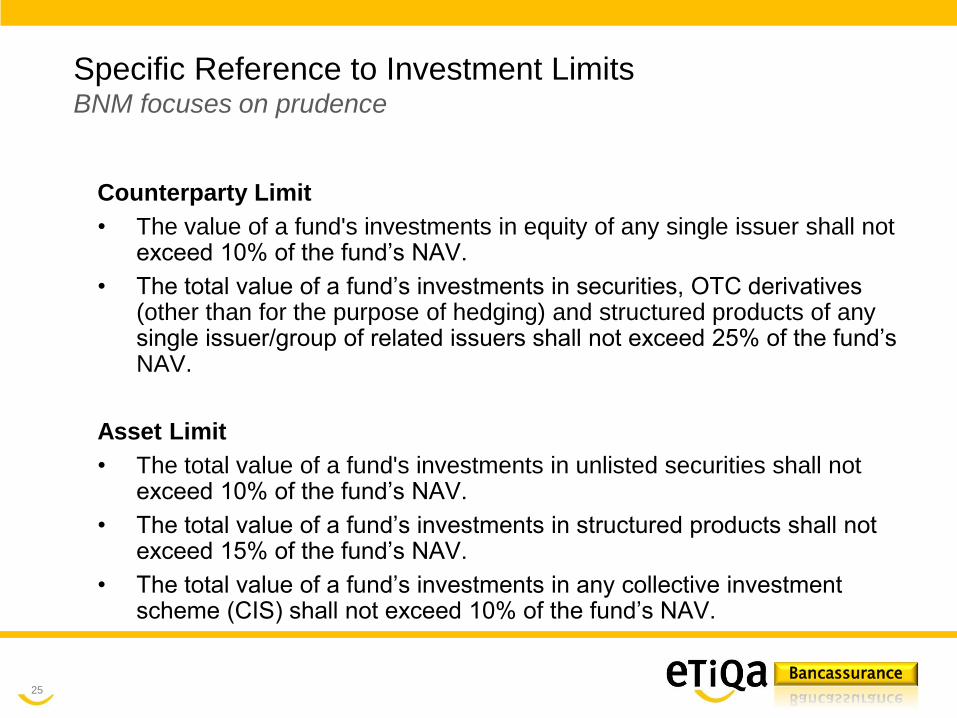

Specific Reference to Investment Limits BNM focuses on prudence

Counterparty Limit

• The value of a fund's investments in equity of any single issuer shall not exceed 10% of the fund’s NAV.

• The total value of a fund’s investments in securities, OTC derivatives (other than for the purpose of hedging) and structured products of any single issuer/group of related issuers shall not exceed 25% of the fund’s NAV.

Asset Limit

• The total value of a fund's investments in unlisted securities shall not exceed 10% of the fund’s NAV.

• The total value of a fund’s investments in structured products shall not exceed 15% of the fund’s NAV.

• The total value of a fund’s investments in any collective investment scheme (CIS) shall not exceed 10% of the fund’s NAV.

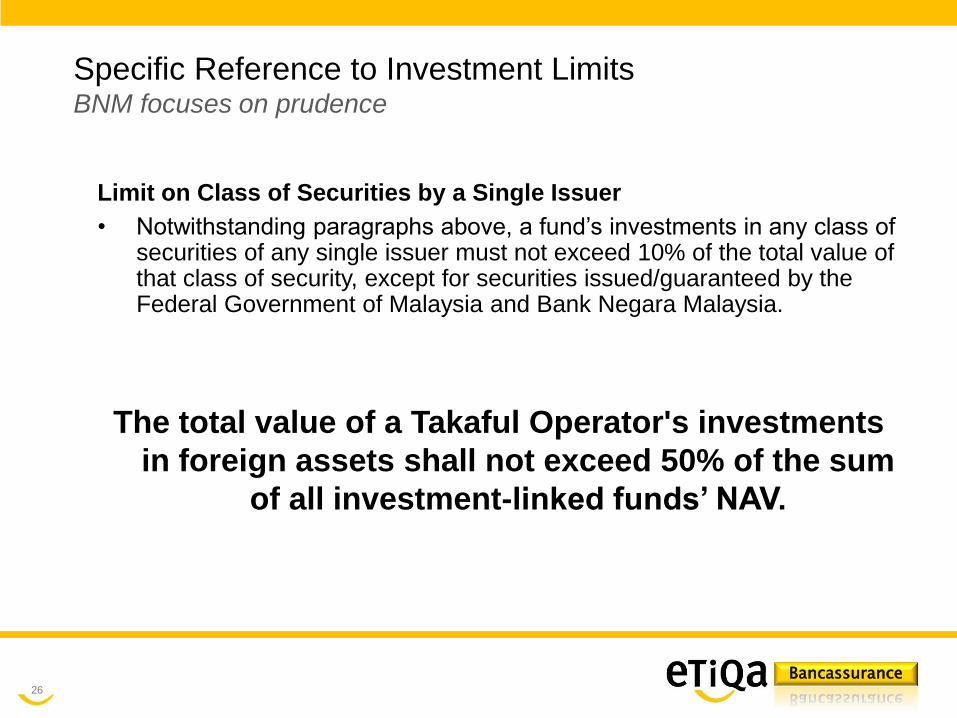

Bancassurance 26

Specific Reference to Investment Limits BNM focuses on prudence

Limit on Class of Securities by a Single Issuer

• Notwithstanding paragraphs above, a fund’s investments in any class of securities of any single issuer must not exceed 10% of the total value of that class of security, except for securities issued/guaranteed by the Federal Government of Malaysia and Bank Negara Malaysia.

The total value of a Takaful Operator's investments

in foreign assets shall not exceed 50% of the sum

of all investment-linked funds’ NAV.

Bancassurance 27

• Portfolio diversification, improve asset allocation.

• NOT meant to replace conventional asset classes.

• Helps to lower overall portfolio risk, volatility.

• Helps to increase overall portfolio return.

• Helps in asset planning via naming of beneficiary.

• Tax advantage – may vary in different jurisdictions.

The Case for Takaful ILP Complements existing portfolio

Bancassurance 28

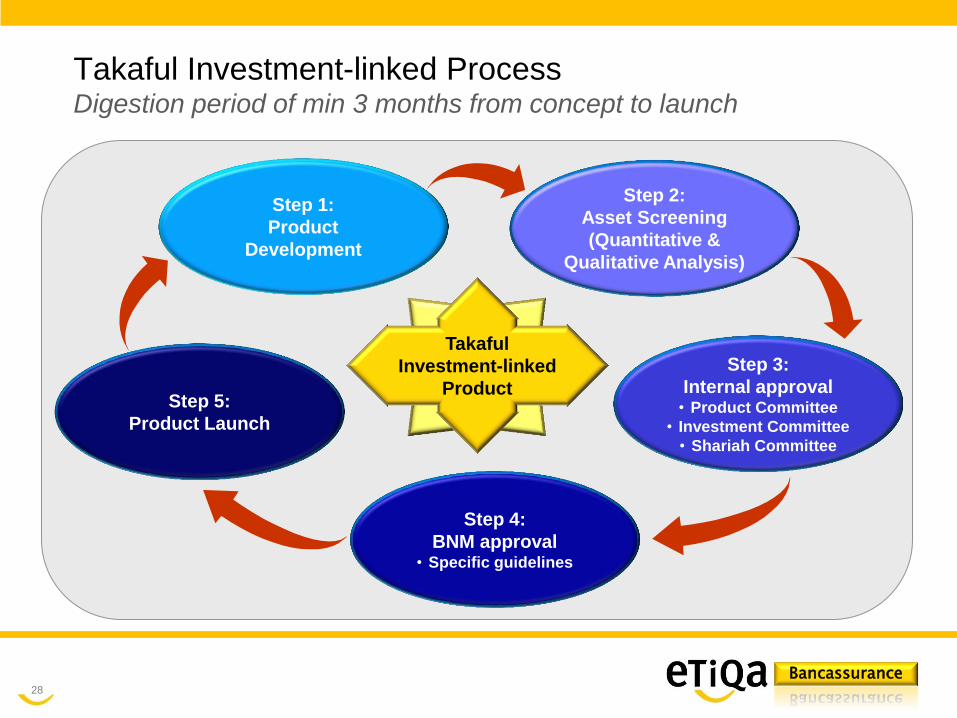

Takaful Investment-linked Process Digestion period of min 3 months from concept to launch

Step 1:

Product

Development

Step 2:

Asset Screening

(Quantitative &

Qualitative Analysis)

Step 3:

Internal approval • Product Committee

• Investment Committee

• Shariah Committee

Step 4:

BNM approval • Specific guidelines

Step 5:

Product Launch

Takaful

Investment-linked

Product

Bancassurance

• Investment strategy is decided by the

Takaful provider.

• Profit earned is divided on

Mudharabah basis (profit sharing).

• FLEXIBILITY!

1.Participants have full control over

their investments - Which fund ?

When to invest? When to sell

back?

2.Participants can choose

coverage level.

• Profits earned fully belong to

Participants.

• The Takaful provider charges nominal

fee for selling of units and

management of the fund.

29

What is Takaful Investment-Linked Product? vs. an Ordinary Family Takaful plan

Ordinary Family Takaful Investment-Linked Takaful

Bancassurance 30

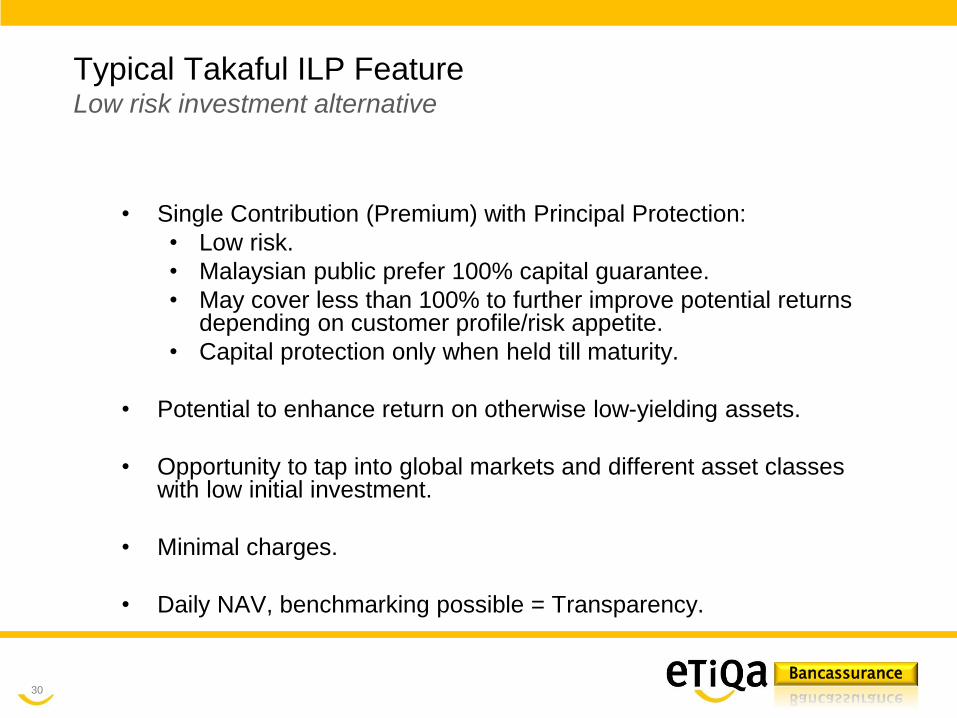

• Single Contribution (Premium) with Principal Protection:

• Low risk.

• Malaysian public prefer 100% capital guarantee.

• May cover less than 100% to further improve potential returns depending on customer profile/risk appetite.

• Capital protection only when held till maturity.

• Potential to enhance return on otherwise low-yielding assets.

• Opportunity to tap into global markets and different asset classes with low initial investment.

• Minimal charges.

• Daily NAV, benchmarking possible = Transparency.

Typical Takaful ILP Feature Low risk investment alternative

Bancassurance

Takaful Protection Wrap

31

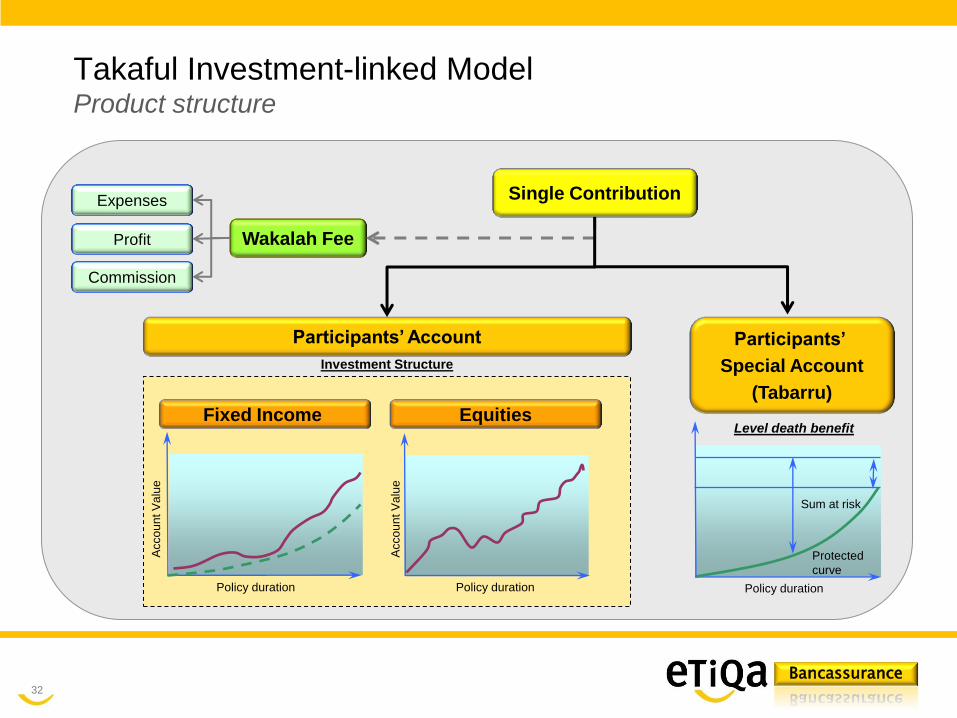

Takaful Investment-linked Model Takaful protection + investment strategy

Investment

Strategy Participants’ Account (Investment Structure)

Participants’ Special Account

(Tabarru / Risk charge)

Bancassurance 32

Single Contribution

Wakalah Fee

Expenses

Profit

Commission

Participants’ Account Participants’

Special Account

(Tabarru)

Fixed Income Equities

Policy duration

Acco

un

t V

alu

e

Protected

curve

Sum at risk

Level death benefit

Policy duration

Acco

un

t V

alu

e

Policy duration

Investment Structure

Takaful Investment-linked Model Product structure

Bancassurance 33

Evolution of Islamic Investment Strategy Options allows access to greater asset choice, enhance returns

Co

mp

lex

ity / R

an

ge

of A

ss

ets

R

etu

rn

Risk

NOTE: Shariah investments naturally bear less risk by virtue of not invest in conventional finance,

alcohol, tobacco, pornography, armaments and gambling related businesses.

Islamic

Financing

(Bonds)

Direct

Investment

(Unit Trust)

Leveraging

(Option)

Bancassurance 34

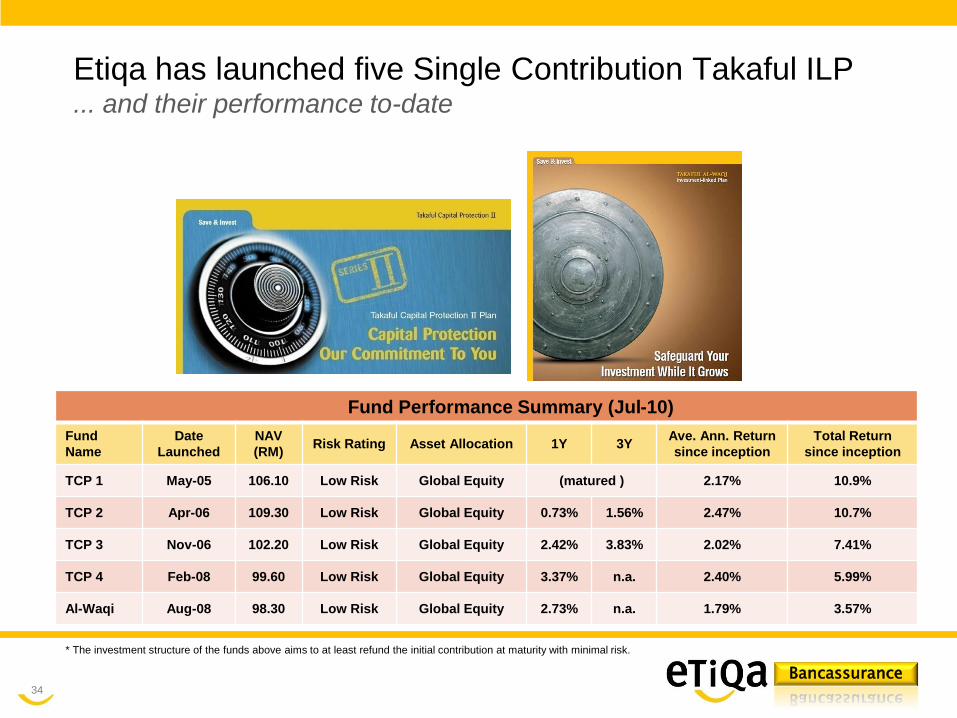

Etiqa has launched five Single Contribution Takaful ILP ... and their performance to-date

* The investment structure of the funds above aims to at least refund the initial contribution at maturity with minimal risk.

Fund Performance Summary (Jul-10)

Fund

Name

Date

Launched

NAV

(RM) Risk Rating Asset Allocation 1Y 3Y

Ave. Ann. Return

since inception

Total Return

since inception

TCP 1 May-05 106.10 Low Risk Global Equity (matured ) 2.17% 10.9%

TCP 2 Apr-06 109.30 Low Risk Global Equity 0.73% 1.56% 2.47% 10.7%

TCP 3 Nov-06 102.20 Low Risk Global Equity 2.42% 3.83% 2.02% 7.41%

TCP 4 Feb-08 99.60 Low Risk Global Equity 3.37% n.a. 2.40% 5.99%

Al-Waqi Aug-08 98.30 Low Risk Global Equity 2.73% n.a. 1.79% 3.57%

Bancassurance 35

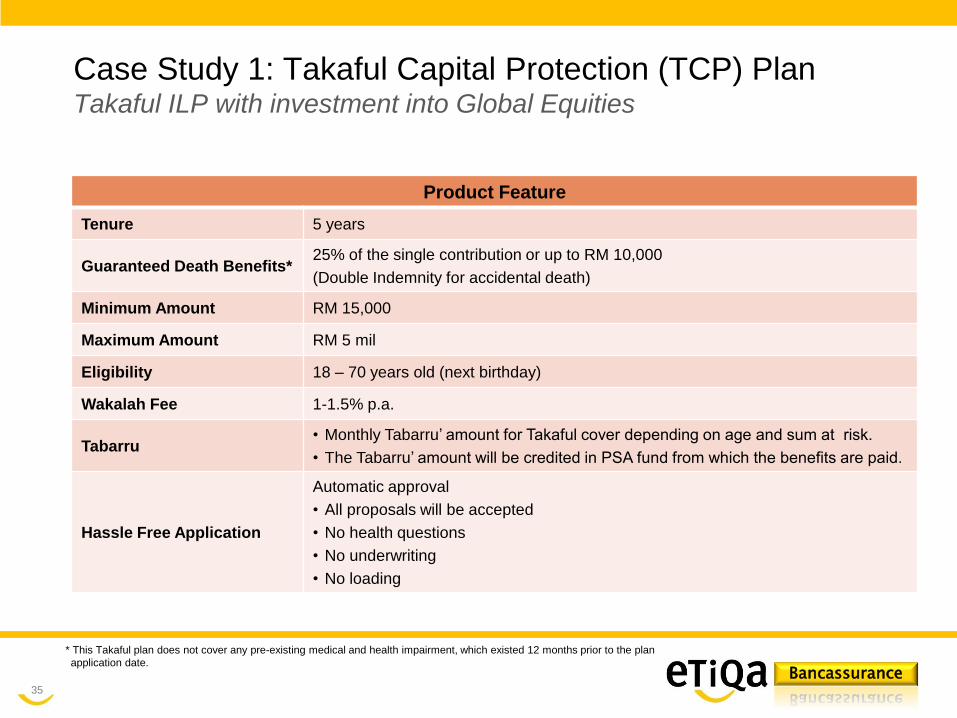

Case Study 1: Takaful Capital Protection (TCP) Plan Takaful ILP with investment into Global Equities

Product Feature

Tenure 5 years

Guaranteed Death Benefits* 25% of the single contribution or up to RM 10,000

(Double Indemnity for accidental death)

Minimum Amount RM 15,000

Maximum Amount RM 5 mil

Eligibility 18 – 70 years old (next birthday)

Wakalah Fee 1-1.5% p.a.

Tabarru • Monthly Tabarru’ amount for Takaful cover depending on age and sum at risk.

• The Tabarru’ amount will be credited in PSA fund from which the benefits are paid.

Hassle Free Application

Automatic approval

• All proposals will be accepted

• No health questions

• No underwriting

• No loading

* This Takaful plan does not cover any pre-existing medical and health impairment, which existed 12 months prior to the plan

application date.

Bancassurance 36

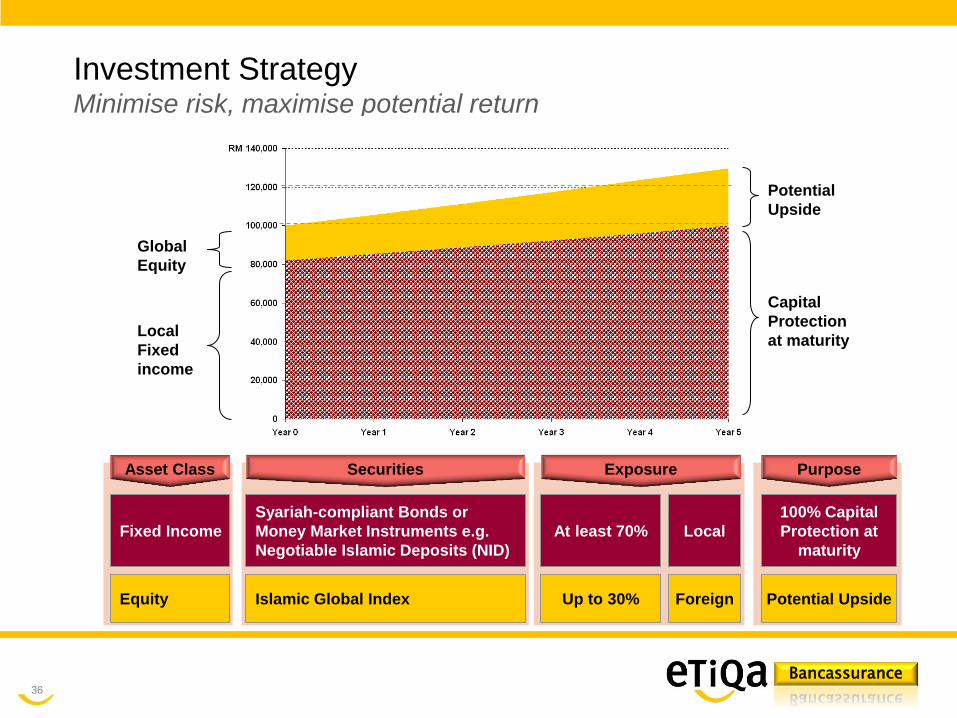

Investment Strategy Minimise risk, maximise potential return

Fixed Income

Equity

Syariah-compliant Bonds or

Money Market Instruments e.g.

Negotiable Islamic Deposits (NID)

Islamic Global Index

At least 70%

Up to 30%

Asset Class Securities Exposure

Local

Foreign

100% Capital

Protection at

maturity

Potential Upside

Purpose

Capital

Protection

at maturity

Potential

Upside

Local

Fixed

income

Global

Equity

Bancassurance 37

Case Study 2: Takaful Al-Waqi Plan Takaful ILP with investment into Commodities

Product Feature

Tenure 2 years

Guaranteed Death Benefits* 25% of the Single Contribution or up to RM 10,000

(Double Indemnity for accidental death)

Minimum Amount RM 20,000

Maximum Amount Unlimited

Eligibility 18 – 70 years old (next birthday)

Bid-Offer Spread

(Initial Charge) 2% of Single Contribution

Wakalah Fee 0.5% p.a.

Tabarru • Monthly Tabarru’ amount for Takaful cover depending on age and sum at risk.

• The Tabarru’ amount will be credited in PSA fund from which the benefits are paid.

Hassle Free Application

Automatic approval

• All proposals will be accepted

• No health questions

• No underwriting

• No loading

* This Takaful plan does not cover any pre-existing medical and health impairment, which existed 12 months prior to the plan

application date.

Bancassurance 38

Wakalah

• Wakalah is a contract whereby one party nominates another (as ‘Wakil’) to act on his/her behalf.

• In the context of a Investment-linked Takaful product, the participant nominates Etiqa Takaful Berhad to manage the Takaful Fund on their behalf.

• Participants will be charged an Annual Wakalah Fee, akin to Annual Management Fee in conventional insurance, of the total Fund Value.

Tabarru

• Participants will contribute (Tabarru’) a fixed amount of the initial capital/contribution, upfront, and placed in the Participants’ Special Account. It is akin to the risk charge in conventional insurance, where in this case it is for the Takaful cover e.g. 0.275% of the Single Contribution.

Wakalah and Tabarru’ (Annual Management Fee and Risk Charge)

Bancassurance 39

Keeping Up with Conventional Finance Shariah capital market is still far behind its conventional counterpart

• Investment strategies which aim to deliver absolute return or the quest of positive return under all market condition have risen in popularity and appeal.

• Nonetheless, there is limited supply of such Takaful offering.

• As a result, the increasing demand still depends largely on conventional strategies.

• The universe of Islamic financial instruments is very limited. Plenty of work needs to be done to engineer new Islamic instruments to satisfy the diverse risk/return needs and profiles of Islamic investors.

• The possibilities seems to be virtually limitless in the world of Islamic finance.

Bancassurance

BANCASSURANCE

CONVENTIONAL

PRODUCTS

Bancassurance

VIP 50 VIP 50 PCI & VIP 50 INVEST

An exclusive single premium plan brought to you by

Bancassurance

VIP 50 PLAN

A packaged plan of Guaranteed

Savings (VIP 50 PCI) plus Flexible

Investment (VIP 50 INVEST) for

potential upside – all in one great

plan.

Bancassurance

How does VIP 50 Plan work ?

(50%)

VIP 50 INVEST

- Flexible Investment to suit your life style

- Choice of 3 investment funds:

Stable, Balanced & Growth

- Excellent track record of fund performance

- Long term insurance coverage up to age 85 years old

(50%)

VIP 50 PCI

- Guaranteed Annual Cash payout of 3.80%. Total 19.0% Guaranteed Cash Payout over 5 Years

- 100% Capital Guarantee at maturity

- Insurance protection up to 125% of Single Premium for 5 years

- No market risks

VIP 50 PLAN

(100%)

Bancassurance

What is the Unique Value Proposition of VIP 50? Capitalize on 1Malaysia positive outlook

44

• POSITIVE economic GROWTH of Malaysia @ 6% p.a.* for next 5 years.

• 100% of funds shall be invested in MALAYSIA.

• FLEXIBLE investment structure to suit customers’ risk appetite – everybody can participate.

• GUARANTEED SAVINGS and ANNUAL CASH PAYOUT elements.

• PROTECTION up to 125% of SINGLE PREMIUM in case of unexpected circumstances.

*10th Malaysia Plan

Bancassurance

Single Premium Open-Ended Investment-linked Plan

Provide Protection and investment Benefits

Maturity following Life Insured’s age of 85 (Age Next

Birthday) at Policy Anniversary date

NO Capital Guaranteed

NO Annual Cash Payout

What is VIP 50 - Invest

Bancassurance

100% CAPITAL GUARANTEED when held till maturity

GUARANTEED 3.80% Annual Cash Payouts for 5 years

Absolutely NO Market Risk

Insurance Coverage at No Additional Costs

Tax-Relief On Annual Cash Payouts & Maturity Value

Speedy Benefit Distribution

Why VIP 50 PCI

Bancassurance

This plan is suitable for those who want to :

Diversify the returns on their savings

Contribute towards their retirement plan

Be assured of their investment returns in advance

Save and receive a regular stream of income

Who should buy a VIP 50 PCI?

Bancassurance

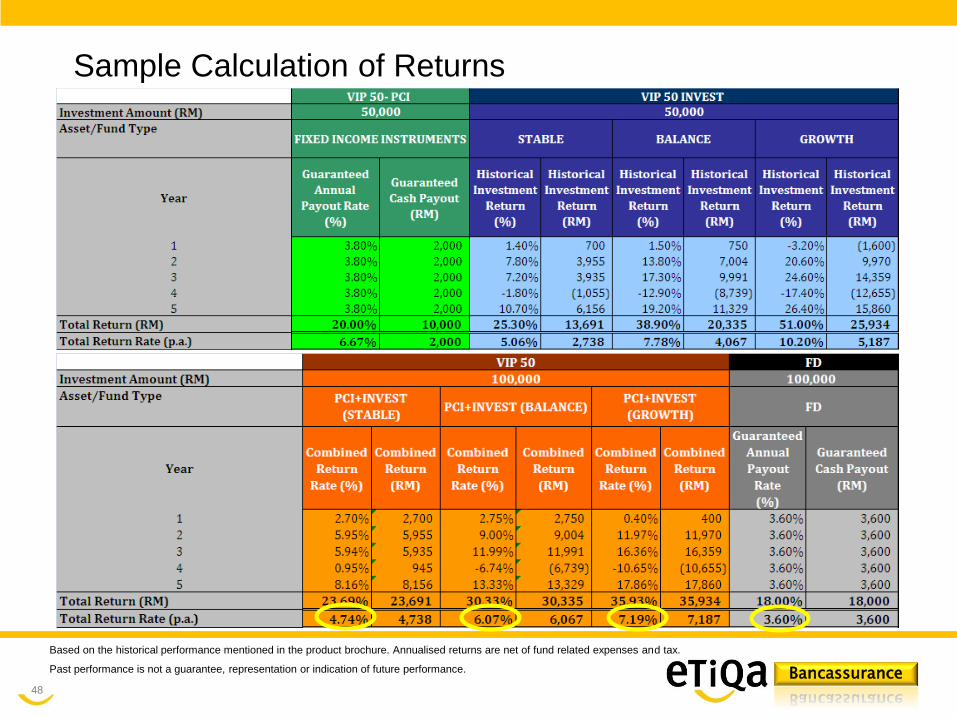

Sample Calculation of Returns

48

Based on the historical performance mentioned in the product brochure. Annualised returns are net of fund related expenses and tax.

Past performance is not a guarantee, representation or indication of future performance.

Bancassurance

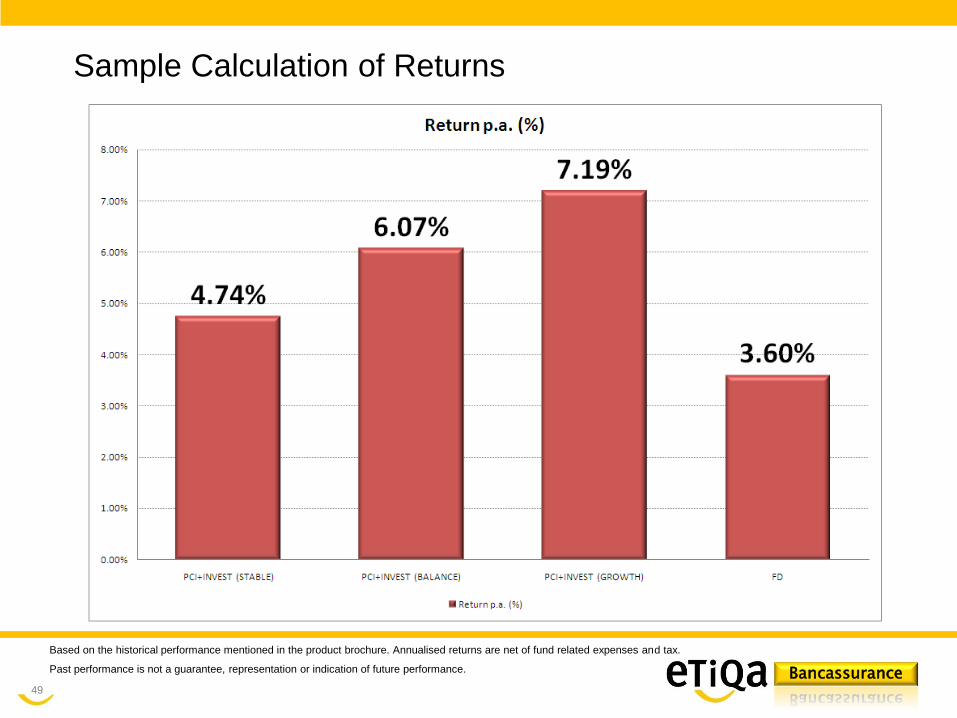

Sample Calculation of Returns

49

Based on the historical performance mentioned in the product brochure. Annualised returns are net of fund related expenses and tax.

Past performance is not a guarantee, representation or indication of future performance.

Bancassurance

4. -

To create public awareness of VIP 50

50

Exclusive gifts for customers – 4 GB diamond

thumbdrive

Bancassurance

Investment-related explanations

51

RETURN

PROTECTION

What are the main 4 features of VIP 50 to remember?

VIP 50, Investment

Flexible investment

Guaranteed Savings

Protection up to 125%

Protection up to 85 years

VIP 50 PCI

VIP 50 INVEST

VIP 50, Investment

guaranteed savings & flexible investment

VIP 50 PCI VIP 50 Invest

•Capital guaranteed at maturity

•Fixed yearly cash payout

• Additional potential higher returns

• Investments to match your profile

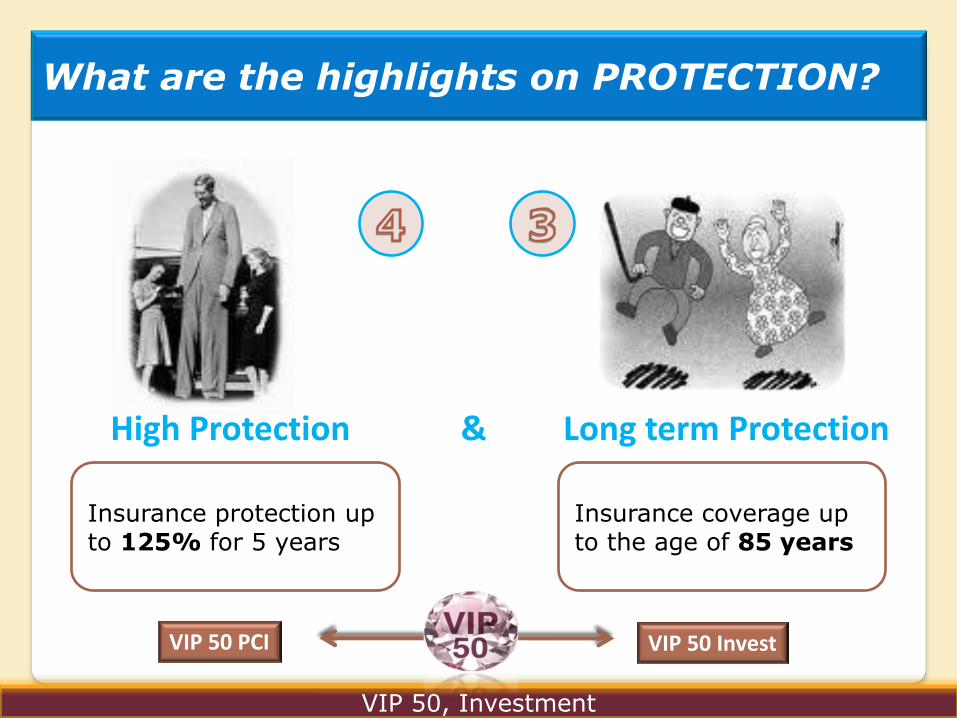

What are the highlights on RETURN?

VIP 50, Investment

VIP 50 PCI VIP 50 Invest

Insurance protection up to 125% for 5 years

Insurance coverage up to the age of 85 years

High Protection & Long term Protection

What are the highlights on PROTECTION?

• Guaranteed 3.8% per year

• Total 19% guaranteed cash Payout over 5 years

• 100% capital guarantee at maturity

• Insurance protection up to 125% for 5 years

VIP 50 PCI

• 3 choices of investment funds:

Stable, Balanced, Growth

• Excellent track record

• Long term insurance coverage up to age of 85 years old.

VIP 50 Invest

How are these 4 ingredients combined?

guaranteed & high flexible & long

VIP 50, Investment

VIP 50, Investment

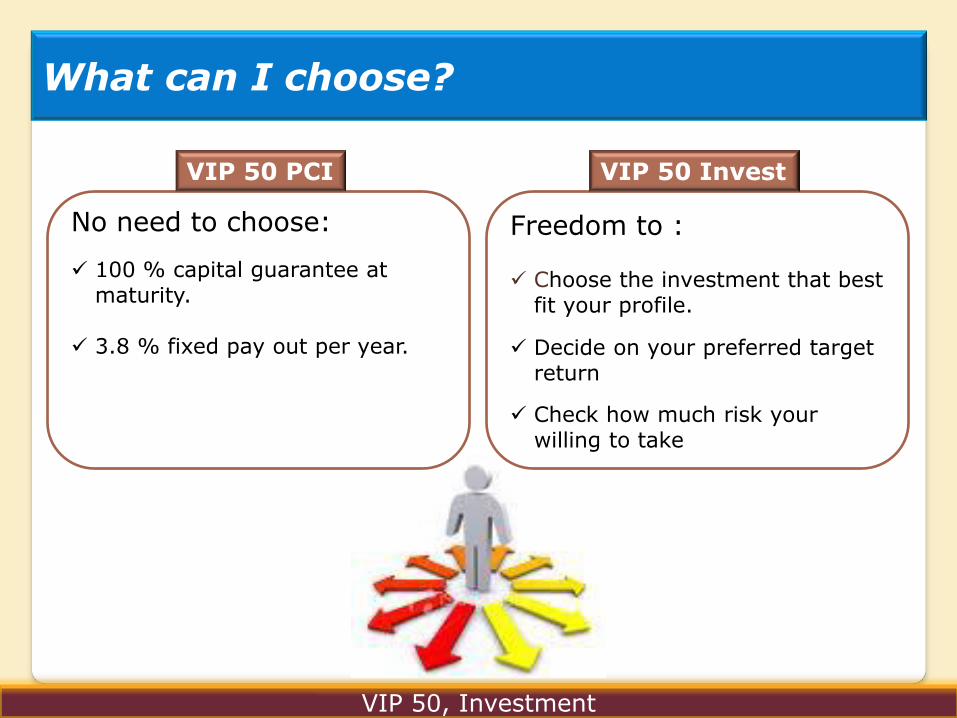

What can I choose?

No need to choose:

100 % capital guarantee at maturity.

3.8 % fixed pay out per year.

Freedom to : Choose the investment that best

fit your profile.

Decide on your preferred target return

Check how much risk your willing to take

VIP 50 PCI VIP 50 Invest

What is my profile?

Growth

Stable

Balance

“The more risk your willing to take, the higher the potential returns “

VIP 50 Invest

VIP 50, Investment

VIP 50, Investment

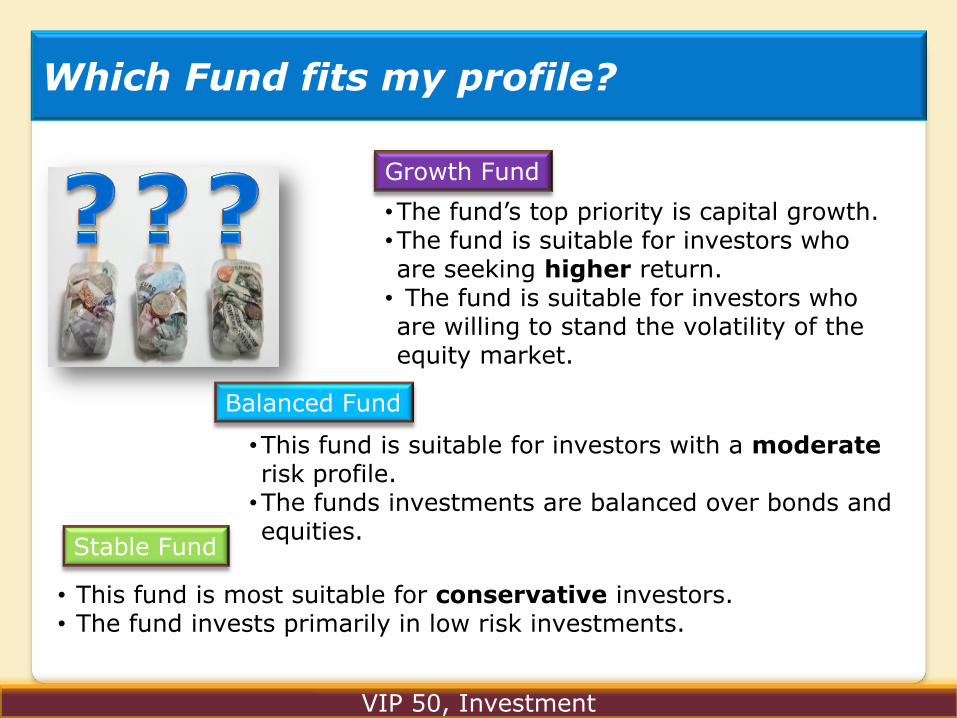

Stable Fund

Which Fund fits my profile?

• This fund is most suitable for conservative investors. • The fund invests primarily in low risk investments.

Balanced Fund

•This fund is suitable for investors with a moderate risk profile.

•The funds investments are balanced over bonds and equities.

Growth Fund

•The fund’s top priority is capital growth. •The fund is suitable for investors who are seeking higher return.

• The fund is suitable for investors who are willing to stand the volatility of the equity market.

, You can switch; • Two times per year

for FREE. • After that, at the

flat rate of 25 RM per switch.

VIP 50, Investment

Stable Fund

Can I switch, should I switch??

Balanced Fund

Growth Fund

, normally there is no need to switch: • You’ve selected the fund that matches your

profile, the fund managers will react on economical changes within the funds.

• But if your profile changes, you may want to switch between funds.

VIP 50, Investment

Stable Fund

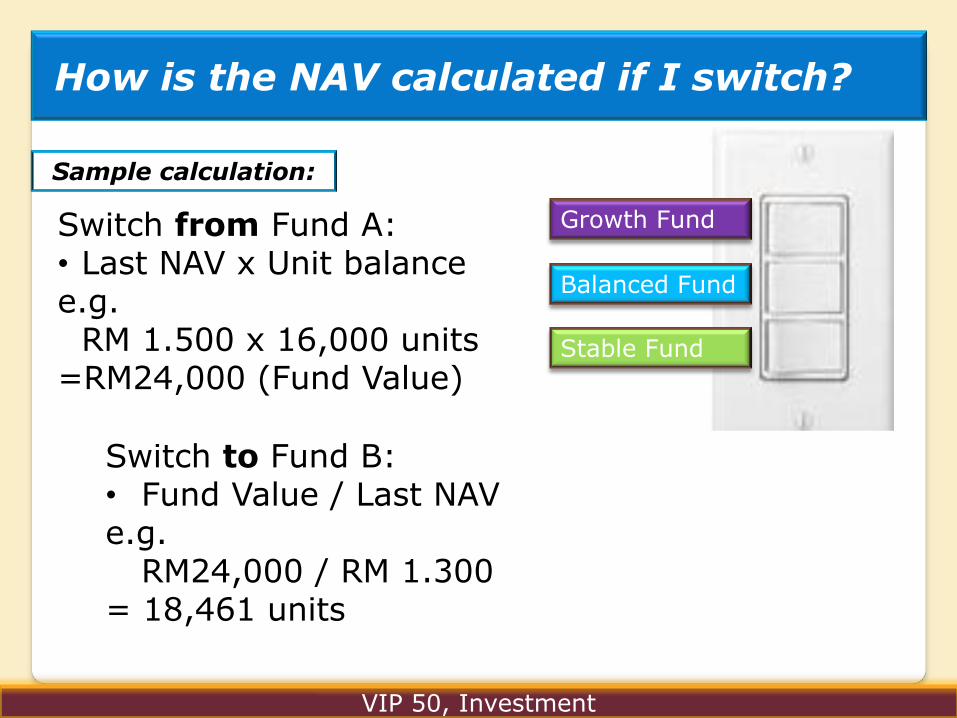

How is the NAV calculated if I switch?

Balanced Fund

Growth Fund

Sample calculation:

Switch from Fund A: • Last NAV x Unit balance e.g. RM 1.500 x 16,000 units =RM24,000 (Fund Value)

Switch to Fund B: • Fund Value / Last NAV e.g. RM24,000 / RM 1.300 = 18,461 units

VIP 50, Investment

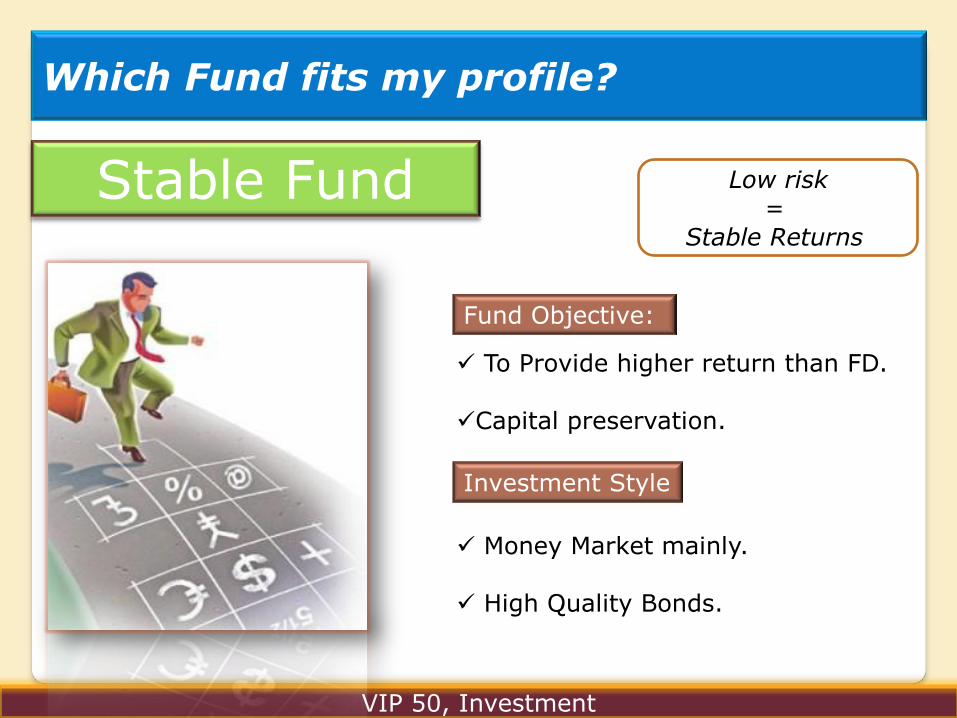

STABLE

Fund Objective:

Investment Style

To Provide higher return than FD.

Capital preservation.

Money Market mainly.

High Quality Bonds.

Low risk =

Stable Returns

Stable Fund

Which Fund fits my profile?

VIP 50, Investment

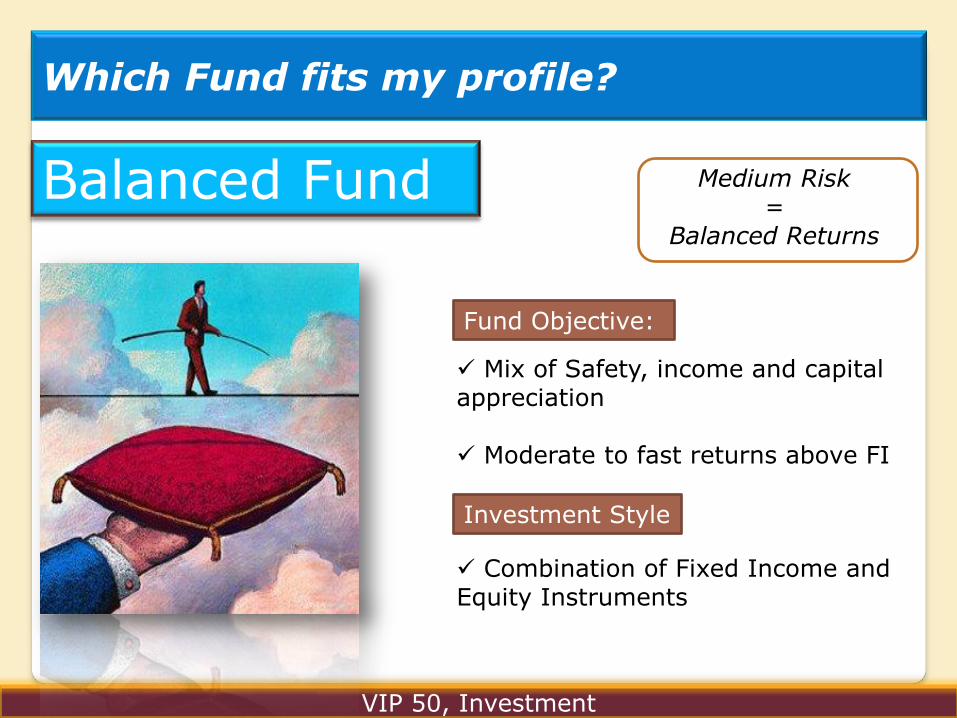

Fund Objective:

Investment Style

Mix of Safety, income and capital appreciation

Moderate to fast returns above FI

Combination of Fixed Income and Equity Instruments

Medium Risk =

Balanced Returns

Balanced Fund

Which Fund fits my profile?

VIP 50, Investment

Fund Objective:

Investment Style

Capital appreciation

Invests in primarily in equities that show high potential for growth

Investing 85% into Equity and the remaining into FI and MM

Higher Risk =

High Returns

Growth Fund

Which Fund fits my profile?

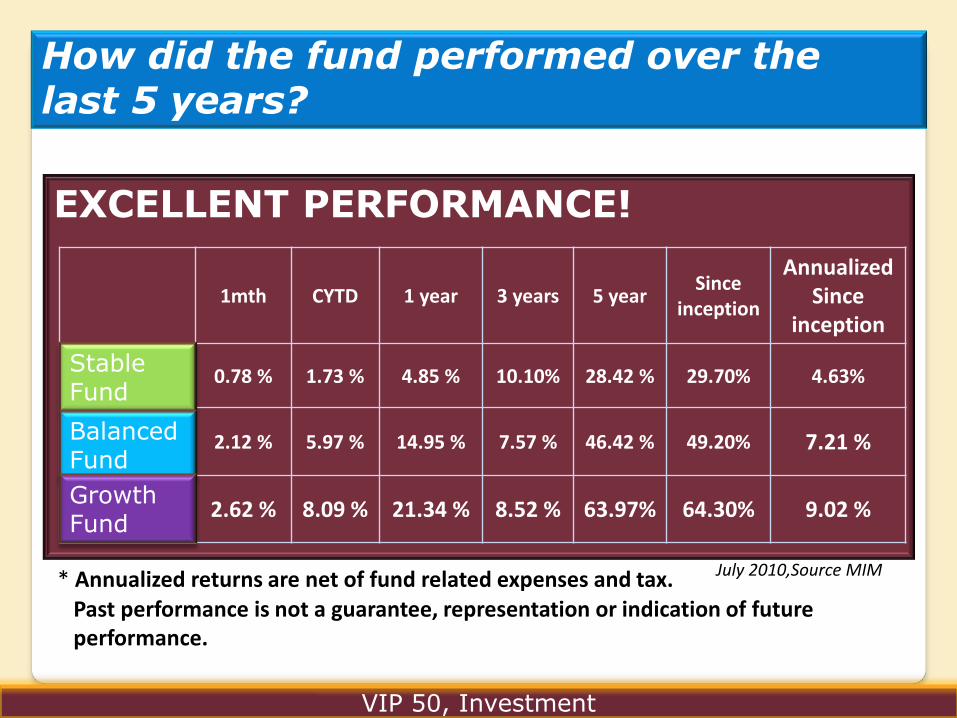

EXCELLENT PERFORMANCE!

VIP 50, Investment

1mth CYTD 1 year 3 years 5 year Since

inception

Annualized Since

inception

Stable 0.78 % 1.73 % 4.85 % 10.10% 28.42 % 29.70% 4.63%

Balance 2.12 % 5.97 % 14.95 % 7.57 % 46.42 % 49.20% 7.21 %

Growth 2.62 % 8.09 % 21.34 % 8.52 % 63.97% 64.30% 9.02 %

July 2010,Source MIM * Annualized returns are net of fund related expenses and tax.

How did the fund performed over the last 5 years?

Stable Fund

Balanced Fund

Growth Fund

Past performance is not a guarantee, representation or indication of future performance.

Where does the outperformance come from?

There or two main sources of additional return in the funds. 1. Asset Allocation 2. Bond/Stock selection

The Asset Allocation decision is the decision how much to invest in which asset class. In these funds there are three asset classes: Money Market, Fixed Income, Equities

The Bond/Stock Selection is the decision in which specific Money Market Instrument, Bond or Stock to invest.

1st source of return

2nd source of return

VIP 50, Investment

Top-Down Approach

What is Asset Allocation?

The Fund Manager allocates the funds between the three Asset Classes based on the economic outlook on short- to medium-term.

The Manager will shift to lower risk assets in times of uncertainty and will allocate more to riskier assets when the outlook is

positive.

The Asset Allocation is monitored at all times and will depend on the strategic allocation in the three funds.

1st source of return

VIP 50, Investment

What is the Asset Allocation in my Fund?

• The three funds have three different risk/return profiles

• Every fund has a different allocation over the asset classes depending on the risk/return profile.

• For every asset class there is a strategic weight for every asset class.

• The STRATEGIC WEIGHT is allocation in a neutral situation (the fund manager is has no preference for one of the asset classes.

• Depending on the economic outlook the fund manager can decide to invest more or less into specific asset classes.

• The funds are always in line with their profile, therefore there is a minimum and maximum weight for every asset class in every fund.

VIP 50, Investment

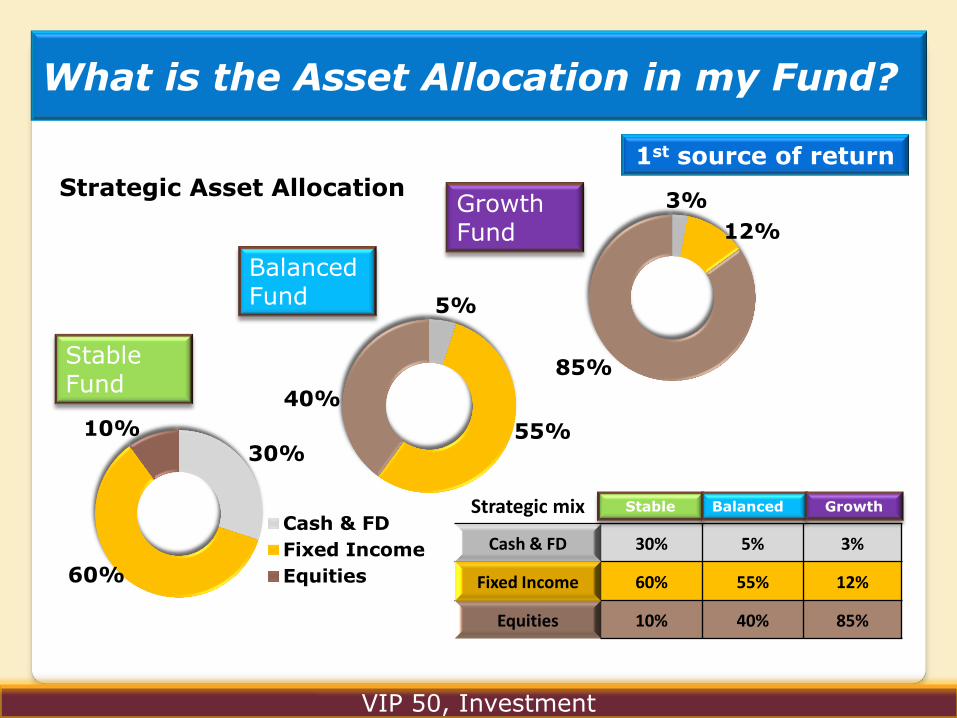

VIP 50, Investment

30%

60%

10%

Cash & FD

Fixed Income

Equities

5%

55%

40%

3%

12%

85%

Strategic mix Stable Balance Growth

Cash & FD 30% 5% 3%

Fixed Income 60% 55% 12%

Equities 10% 40% 85%

1st source of return

Strategic Asset Allocation

Stable Fund

Balanced Fund

Growth Fund

Stable Balanced Growth

What is the Asset Allocation in my Fund?

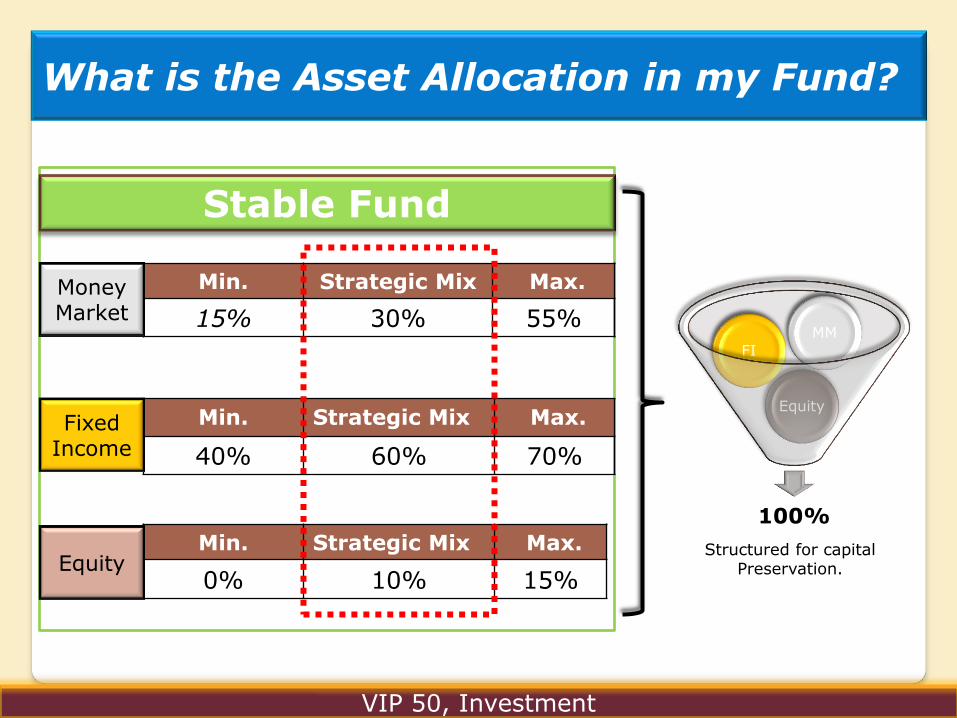

VIP 50, Investment

100%

Equity

FI

MM

Min. Strategic Mix Max.

15% 30% 55%

Min. Strategic Mix Max.

40% 60% 70%

Min. Strategic Mix Max.

0% 10% 15% Equity

Fixed Income

Money Market

Structured for capital Preservation.

Stable Fund

What is the Asset Allocation in my Fund?

VIP 50, Investment

100%

Equity

FI

MM

Min. Strategic Mix Max.

0% 5% 40 %

Min. Strategic Mix Max.

25% 55% 60%

Min. Strategic Mix Max.

15% 40% 50% Equity

Fixed Income

Money Market

Balanced Fund

To provide a balanced mixture of safety, income, and capital appreciation.

What is the Asset Allocation in my Fund?

VIP 50, Investment

100%

Equity

FI

MM

Min. Strategic Mix Max.

0% 3% 30%

Min. Strategic Mix Max.

0% 12% 40%

Min. Strategic Mix Max.

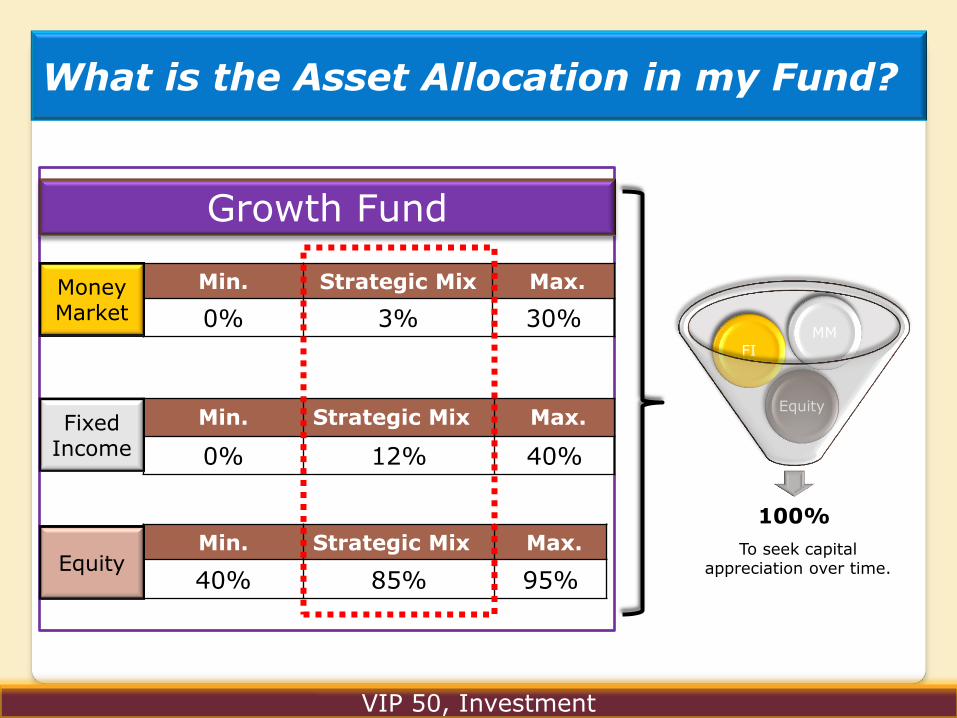

40% 85% 95% Equity

Fixed Income

Money Market

To seek capital appreciation over time.

Growth Fund

What is the Asset Allocation in my Fund?

VIP 50, Investment

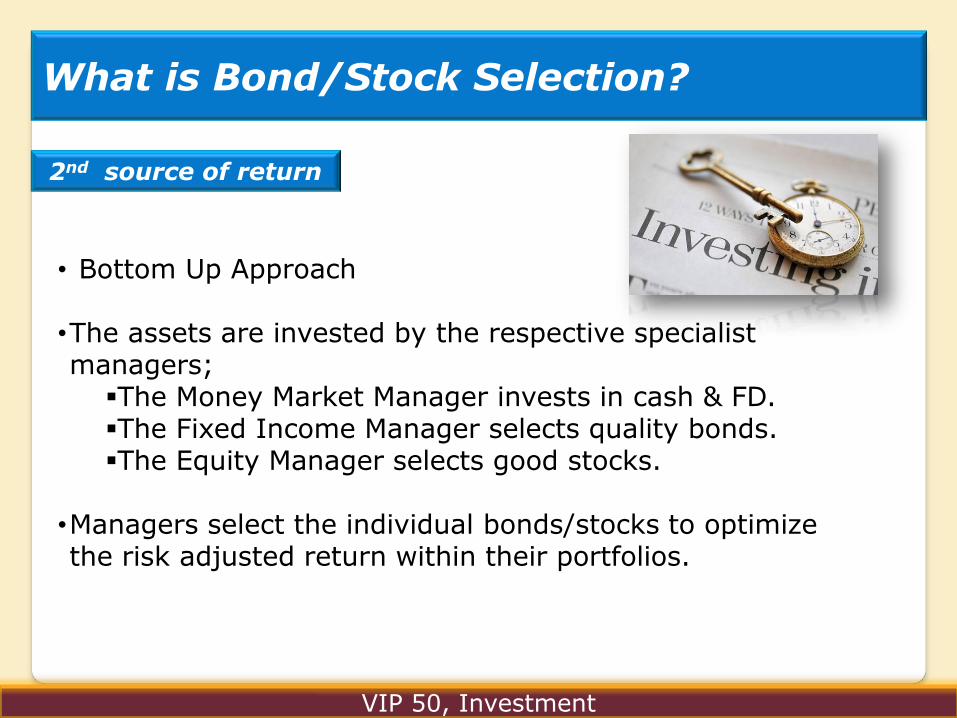

• Bottom Up Approach

•The assets are invested by the respective specialist managers;

The Money Market Manager invests in cash & FD. The Fixed Income Manager selects quality bonds. The Equity Manager selects good stocks.

•Managers select the individual bonds/stocks to optimize the risk adjusted return within their portfolios.

2nd source of return

What is Bond/Stock Selection?

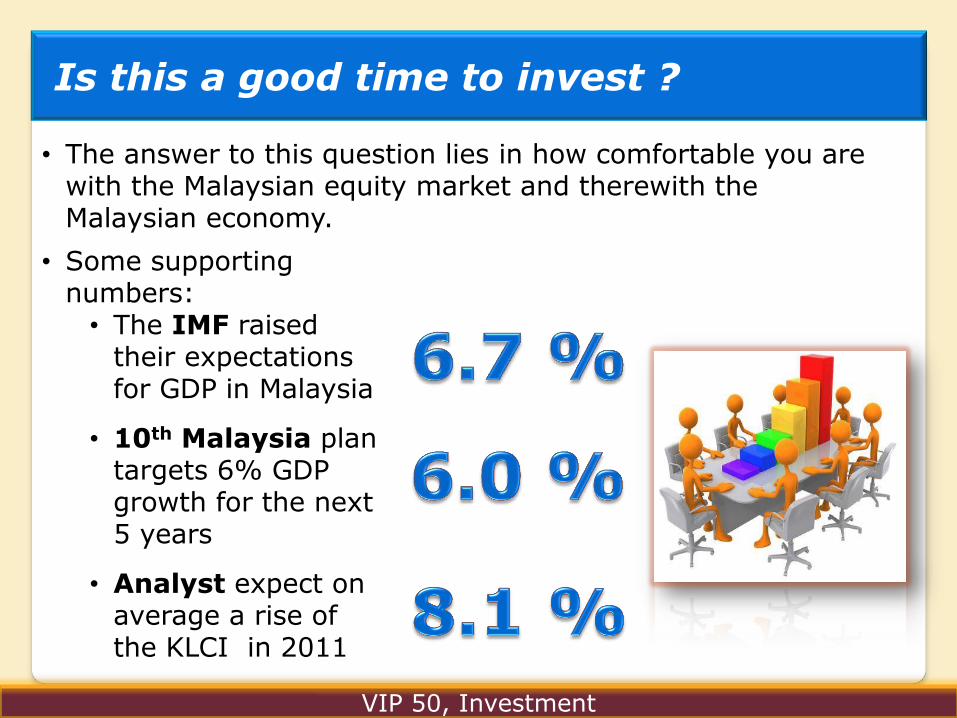

Is this a good time to invest ?

• The answer to this question lies in how comfortable you are with the Malaysian equity market and therewith the Malaysian economy.

• Some supporting

numbers: • The IMF raised

their expectations for GDP in Malaysia

• 10th Malaysia plan targets 6% GDP growth for the next 5 years

• Analyst expect on average a rise of the KLCI in 2011

VIP 50, Investment

Why now in Malaysia?

VIP 50, Investment

• IMF raised the 2010 GDP growth expectations for Malaysia to

• IMF expectations for GDP growth in Malaysia for 2011

IMF Forecast 2009 2010E 2011E

Malaysia -1.7% 6.7% 5.3%

Why now in Malaysia?

VIP 50, Investment

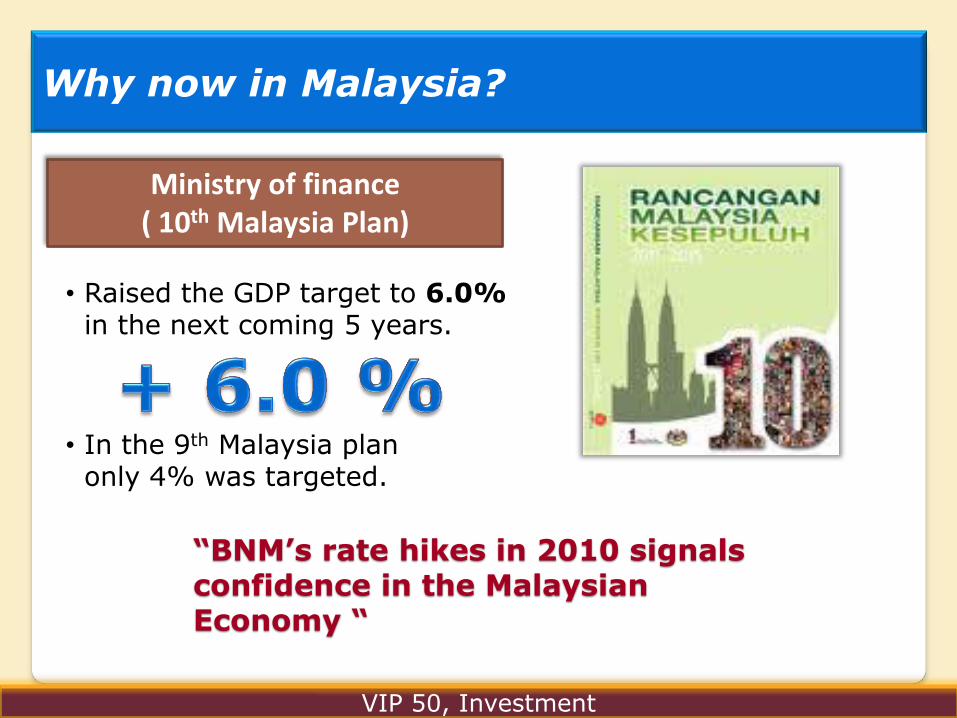

• Raised the GDP target to 6.0% in the next coming 5 years.

Ministry of finance ( 10th Malaysia Plan)

• In the 9th Malaysia plan only 4% was targeted.

“BNM’s rate hikes in 2010 signals confidence in the Malaysian Economy “

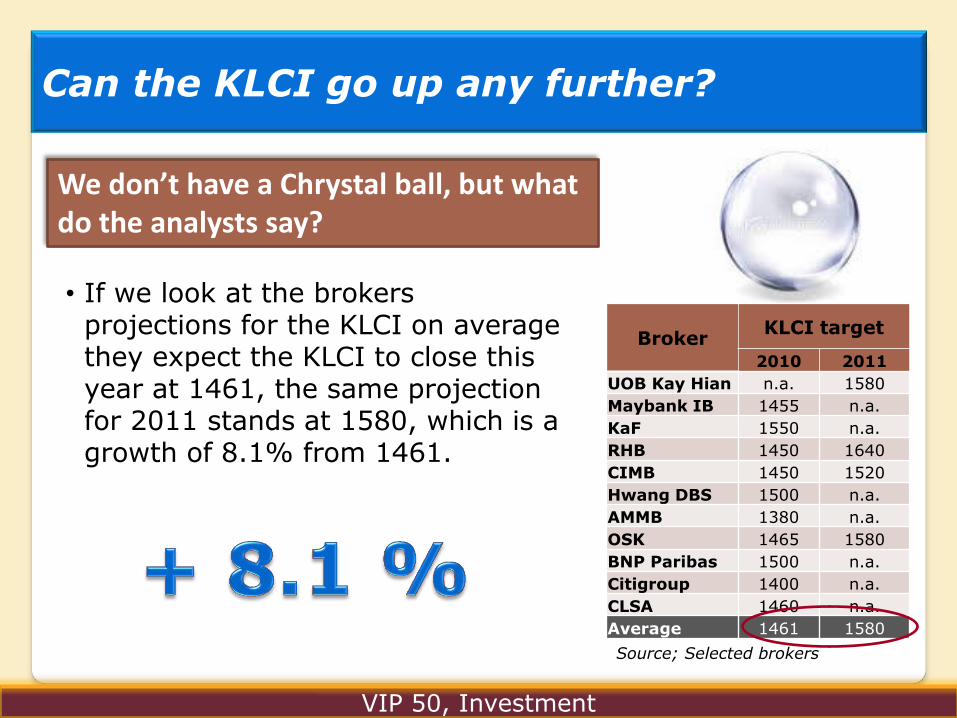

Can the KLCI go up any further?

• If we look at the brokers projections for the KLCI on average they expect the KLCI to close this year at 1461, the same projection for 2011 stands at 1580, which is a growth of 8.1% from 1461.

We don’t have a Chrystal ball, but what do the analysts say?

Broker KLCI target

2010 2011

UOB Kay Hian n.a. 1580

Maybank IB 1455 n.a.

KaF 1550 n.a.

RHB 1450 1640

CIMB 1450 1520

Hwang DBS 1500 n.a.

AMMB 1380 n.a.

OSK 1465 1580

BNP Paribas 1500 n.a.

Citigroup 1400 n.a.

CLSA 1460 n.a.

Average 1461 1580

Source; Selected brokers

VIP 50, Investment

What about the “double dip” scenario?

Is the US

going for a

second dip?

• Investing is never without risk. • There are always insecurities in the market.

• Today's wondering is “is there going to be a second dip on the global market?”

• This question cannot be answered by Yes or No, but there a few things to remember:

The global recovery after the financial crises is led by Asia! Not by Europe or the US.

The prospects for the Asian Economy are VERY POSITIVE.

The funds invests 100% in Malaysia.

VIP 50, Investment

When investing via funds, the Unit Price does not matter. No matter how high or low the Unit Price, the same amount will be invested in the market. What does matters is the market outlook of the market to invest in!

Is the Unit Price too high?

Question:

You have RM 10 to invest and you have two choices: 1. Buy 10 units of 1 RM each, or 2. Buy 5 units of 2 RM each

Which of the two is the smarter buy?

Answer:

It does not make any difference! in the end you still have 10 RM to invest either way. Suppose the market goes up by 10 %, your investment will grow to 11 RM. No difference if you hold 10 units of 1.1 RM or 5 units of 2.2 RM.

Does size matter?

VIP 50, Investment

What if BNM decides to raise the OPR?

“BNM’s rate hikes signals confidence in the Malaysian Economy “

• The market expects a rate hike either end of this year or early next year.

• First of all that shows BNM’s confidence in the Malaysian economy.

• A rate hike doesn’t necessarily mean that product like VIP 50 PCI can offer better fixed returns.

• We have seen the opposite in 2010; while BNM raised the OPR, market yields came down.

• Supply and demand for Fixed Income Instruments determined the market yields.

VIP 50, Investment

How strong is MIM?

MIM is one of the largest Asset Management companies in

Malaysia. Consistently in the top 3 position.

MIM manages the largest fixed income portfolio in the

industry.

MIM manages the largest Takaful portfolio in Malaysia

But I had products managed by MIM before that didn’t deliver any return! • These were structured products, where the manager has little or no influence

on the performance. • The three offered funds in VIP 50 Invest are ACTIVELY MANAGED funds. To

really look at the quality of the fund manager we should look at the long-term performance on these funds.

• The annualized performance since October 2004:

July 2010,Source MIM

Stable Fund

Balanced Fund

Growth Fund

4.63 % 7.21 % 9.02 %

VIP 50, Investment

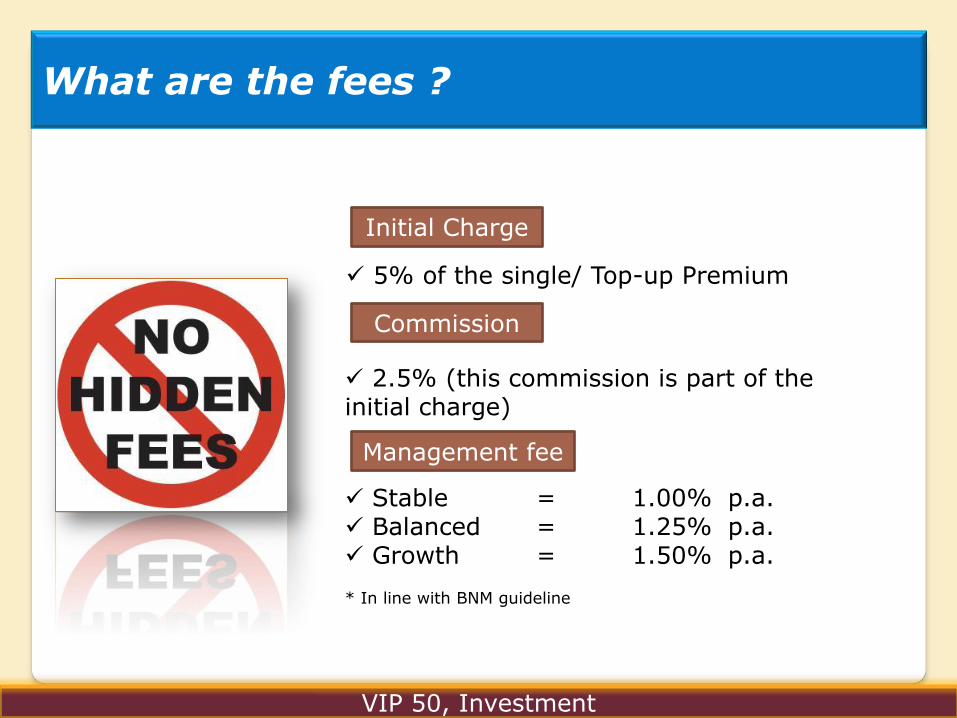

Initial Charge

5% of the single/ Top-up Premium Commission

2.5% (this commission is part of the initial charge)

Management fee

Stable = 1.00% p.a. Balanced = 1.25% p.a. Growth = 1.50% p.a. * In line with BNM guideline

What are the fees ?

VIP 50, Investment

The initial fee is lower than what most unit trust funds charge, which ranges between 6% and 7%. The initial fee applies on VIP 50 Invest only hence the effective fee for VIP 50 is 2.50%. The initial fee is also in line with the latest BNM guideline, which specified that fee must be taken upfront instead of taken during partial withdrawal or surrender, which was the practice previously.

Is the Initial Fee high?

VIP 50, Investment

• All investments have a certain level of risk.

• In the three funds there are three levels of risk linked to the target return to match the customer’s profile:

What are the risks of the investment part?

“Risk and opportunity are just different sides of the same coin“

• The fund that allocates the most to low risk assets i.e.

money market like Stable Fund has the lowest risk.

• With its mixture of Fixed income and equity, the Balanced Fund carries moderate risk.

• With the highest portion allocated to equity. The risk of the Growth Fund is the highest.

VIP 50, Investment

June 2010,Source MIM All numbers are based on NAV development and are after fees and costs of the fund.

VIP 50, Investment

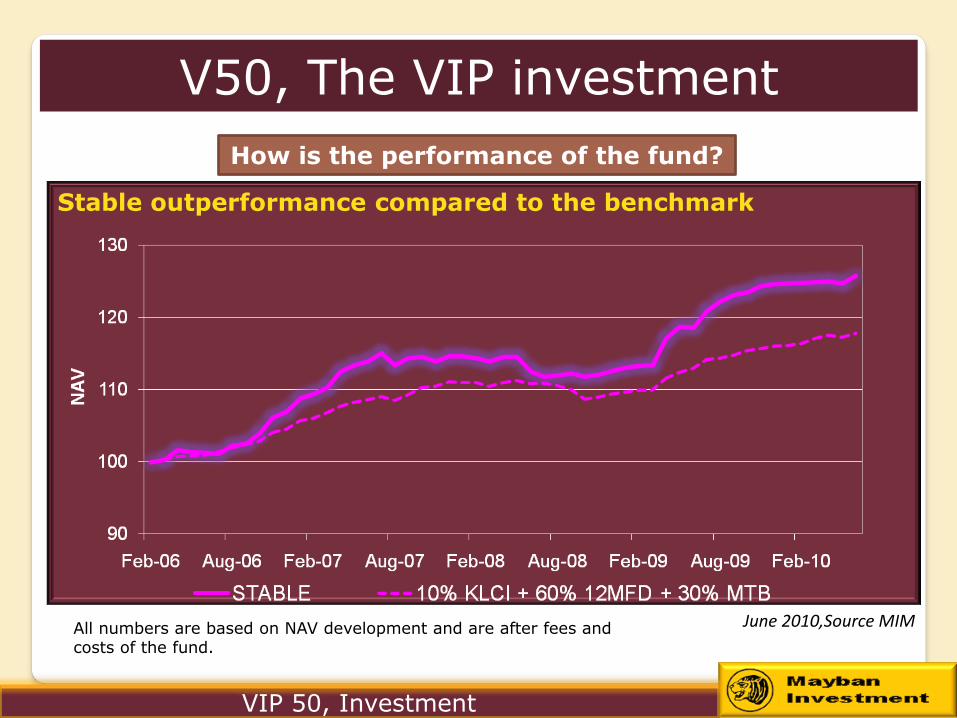

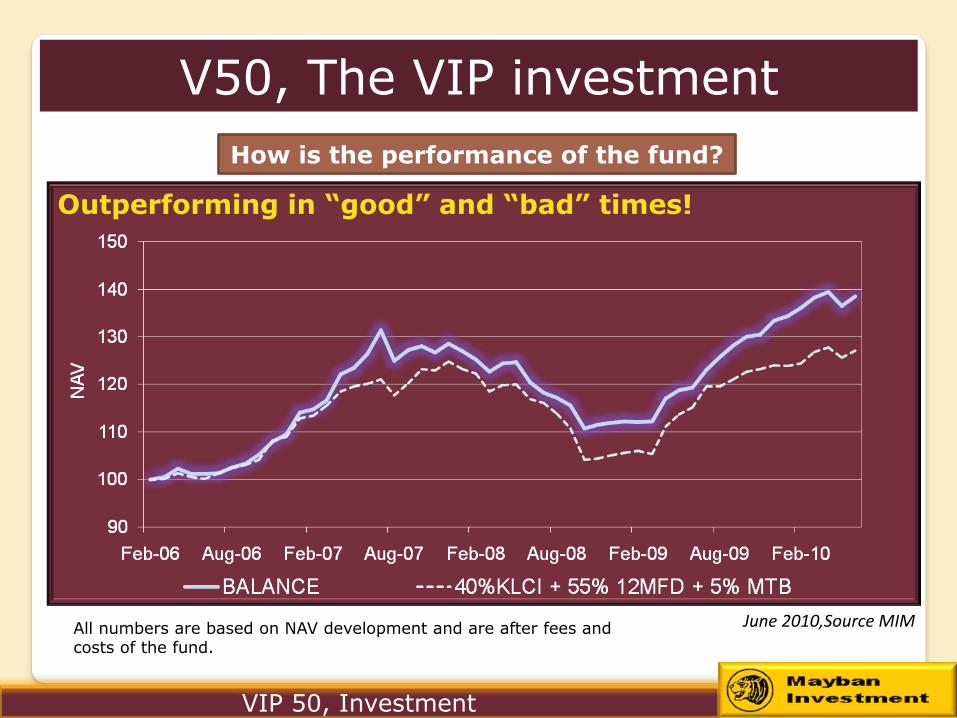

V50, The VIP investment

How is the performance of the fund?

Stable outperformance compared to the benchmark

Outperforming in “good” and “bad” times!

VIP 50, Investment

V50, The VIP investment

How is the performance of the fund?

June 2010,Source MIM All numbers are based on NAV development and are after fees and costs of the fund.

VIP 50, Investment

V50, The VIP investment

Cautious during crisis, accelerating during recovery

How is the performance of the fund?

June 2010,Source MIM All numbers are based on NAV development and are after fees and costs of the fund.

This document has been prepared solely for informational purposes and does not constitute 1) an offer to buy or sell or a solicitation of an offer to buy or sell any security or financial instrument mentioned in this document or 2) any investment advice. Any decision to invest in the securities described herein should be made after reviewing the most recent version of the prospectus/info memo. Moreover, prospective investors should conduct such investigations as the investor deems necessary and should seek their own legal, accounting and tax advice in order to make an independent determination of the suitability and consequences of an investment in the securities. The opinions contained herein are subject to change without notice.

Investors should ensure themselves that they read the last available version of this document.

Past performance or achievements are not indicative of current or future performance. The performance data do not take account of the commissions and costs incurred on the issue and redemption of units.

Please read…

VIP 50, Investment

HAPPY INVESTING

THANK YOU

Knowing is not enough; we must apply. Willing is not enough; we must do.“

-BRUCE LEE

QUESTIONS ?