investment oriented study on minerals and mineral based...

TRANSCRIPT

INVESTMENT ORIENTED STUDY on

MINERALS AND MINERAL BASED INDUSTRIES

Experts Advisory Cell Ministry of Industries & Production Government of Pakistan

April, 2004

“Do ye not see That God has subjected To your (use) all things In the heaven and in earth And has made His bounties Flow to you in exceeding Measures (both) seen and hidden”

Luqman XXXI - 20

PREFACE The Ministry of Industries & Production through Experts Advisory Cell assigned a

study “Investment Oriented Study on Minerals and Mineral Based Industries” to a

Mineral Consultant in June 2003. The objective of the study was to understand

and gauge the geological endowment and mineral potential of the country

alongwith allied matters for the identification and formulation of profiles of high

mineral potential deposits for their utilization in various sectors of economy.

Accordingly, the geological, minerals, policy and institutional situation obtaining in

the country has been reviewed, the scope of mineral potential for their fast track

development has been examined and capacities of their utilization have been

weighed. To this effect, various available sectoral and project specific studies

and reports, and comments/suggestions from pertinent bodies representing

broadly public, semi public and private sector have been scrutinized. As a result

of these toils and deliberations, viable and implementable recommendations

have been made under each heading/chapter of the study. EAC gratefully

acknowledges the valuable comments/suggestions received from the

stakeholders.

As the mineral sector is vast and complex, full of risks and uncertainties and host

of indigenous problems, it has been suggested that a Plan of Action may be

designed for translating these recommendations into action as desired both by

the Minister of Petroleum and N.R and Minister of Industries and Production

during their speeches in the Mineral Sector Development Consultation Workshop

with Stakeholders on 15-16 December, 2003 at Islamabad.

God Almighty has blessed us with abundant mineral resources and we pray to

Him to give us courage, commitment and talent for their scientific development

and productive utilization in the best interest of the country.

Experts Advisory Cell Islamabad

April, 2004

MESSAGE FROM MINISTER FOR

INDUSTRIES AND PRODUCTION The mineral resources of a country are valuable means and measures of its economic and industrial growth. These are still more important for Pakistan because of its favourable geological environment and a large number of mineral resources in the country. Considering that substantial scope exists for the development of mineral sector and their uses in industries, Ministry of Industries & Production through Experts Advisory Cell conducted “Investment Oriented Study on Minerals and Mineral Based Industries”. The objective of the study was to cover geoscientific and mineral development matters for identifying metallogenic regions and developing project portfolios of viable mineral deposits from their development and utilization. As the mineral sector is vast and complex & loaded with risks and

uncertainties, it requires Govt. support at various stages of its development. In this context, Ministry of Industries and Production has been and still is playing its role by declaring mineral rich parts of the country as Export Processing Zone particularly in Balochistan and Sindh. These zones, needless to say, would get the benefits of the package announced by the Prime Minister for encouraging investment in EPZ’s. All along your Government has been attaching high priority to Mineral Sector. This is evident from

the discovery and development of world class copper-gold deposits in Chagai; Balochistan by Australian Firms that would fetch $ 500 million to $ 600 million per year during the lives of these mines. Successful upgradation studies being carried out by German Consultants on Dilband Iron Ores Balochistan would, to large extent, minimize importation of Iron Ores 1.7 million tons iron ores costing about Rs. 3.2 billion per year. Development of Thar coal field, one of the largest good quality lignite deposits in the world, on completion, would provide additional source of energy. Moreover development of abundantly available high quality industrial minerals and natural stones have bright prospects for exports, import substitution and local consumption. The confidence of foreign investors, developers and consultants repose in Pakistan, clearly demonstrate the successful April, 2004

implementation of investment oriented policies initiated by the present regime. In order to consider the recommendations made in the study and to translate them into Action Plan, is necessary that modalities should be worked out for taking full advantage of our mineral potential. In the end, I quote an extract of the speech made by Quaid-e-Azam Mohammad Ali Jinnah on the occasion of laying of foundation – stone of the building of the Valika Textile Mills Ltd: on September 26, 1947, that shows his ability to see far ahead of his times, and whatever he prescribed proved to be correct and true. “Nature has blessed us with a good many raw materials of industry and it is upto us to utilize them to the best of the state and its people”

Liaquat Ali Jatoi Minister for Industries & Production

iv

MESSAGE FROM SECRETARY

INDUSTRIES & PRODUCTION

The mineral potential of Pakistan

is widely recognized to be

excellent but the sector is

inadequately developed. This is

evident from the fact that its

contribution to Gross National

Product (GNP) remained 0.5% to

1.0%, unchanged over the last

many decades despite

substantial growth in the

economy of Pakistan. Taking the

mineral potential into account, it

is clear that a more substantial

mining industry could be

developed to feed other sectors

of economy particularly the

industrial sector.

Minerals are very important for

the growth of mineral based

industries. The minerals described

below are under various phases

of exploration, development and

utilization in Pakistan.

Energy Minerals (coal), Agriculture

Minerals (rock phosphate,

gypsum), Metallic Minerals (iron

ores, copper, gold, zinc-lead,

chromite, antimony), Refractory

Minerals (refractory clays,

magnesite, chromite, silica sand,

dolomite) and Glass & Ceramic

Minerals (kaolin-china clay,

nephyeline syenite, silica sand).

Thus sustainable availability and requisite suitability of minerals is a requirement for rapid industrialization. In order to put the

v

minerals used in various industries

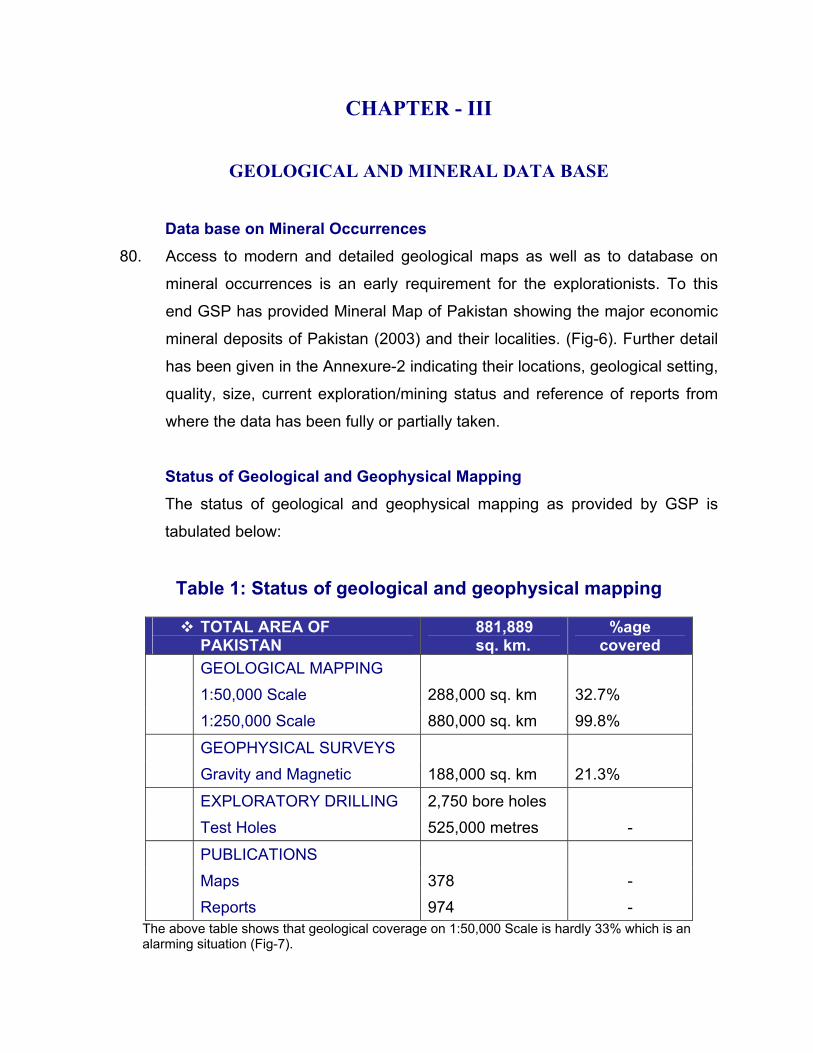

in proper perspective, M/o

Industries and Production

assigned the task to Experts

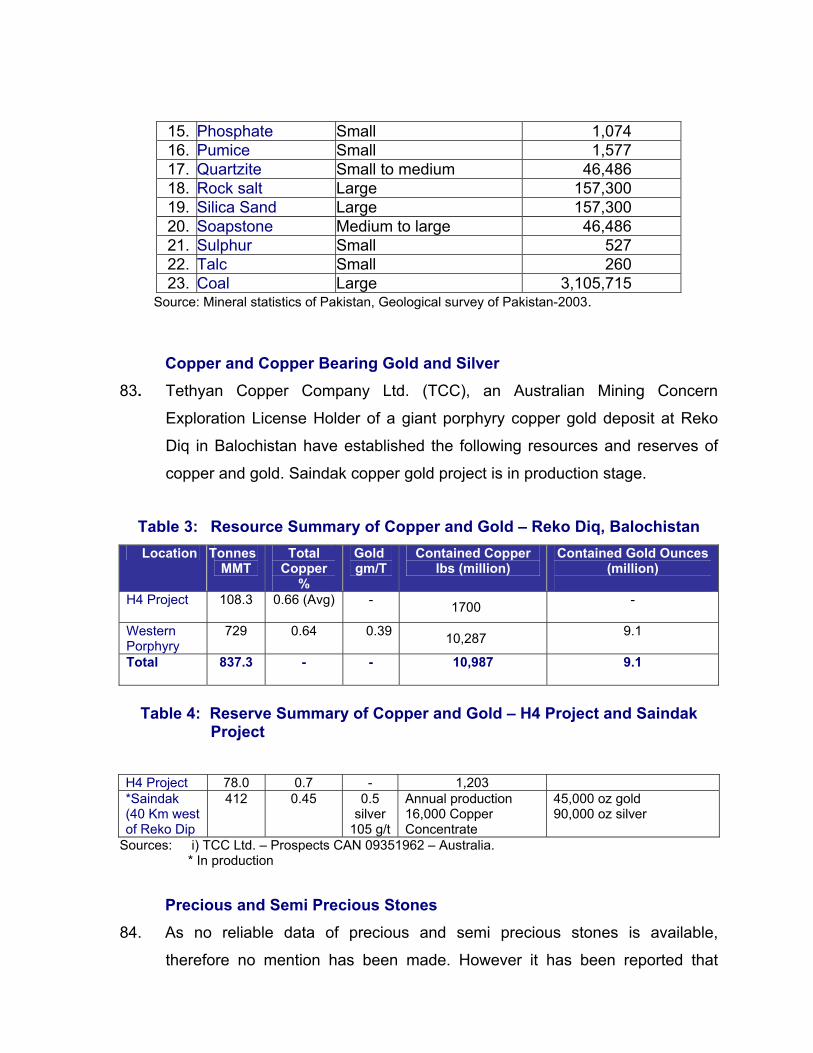

Advisory Cell to undertake a

study on the subject matter.

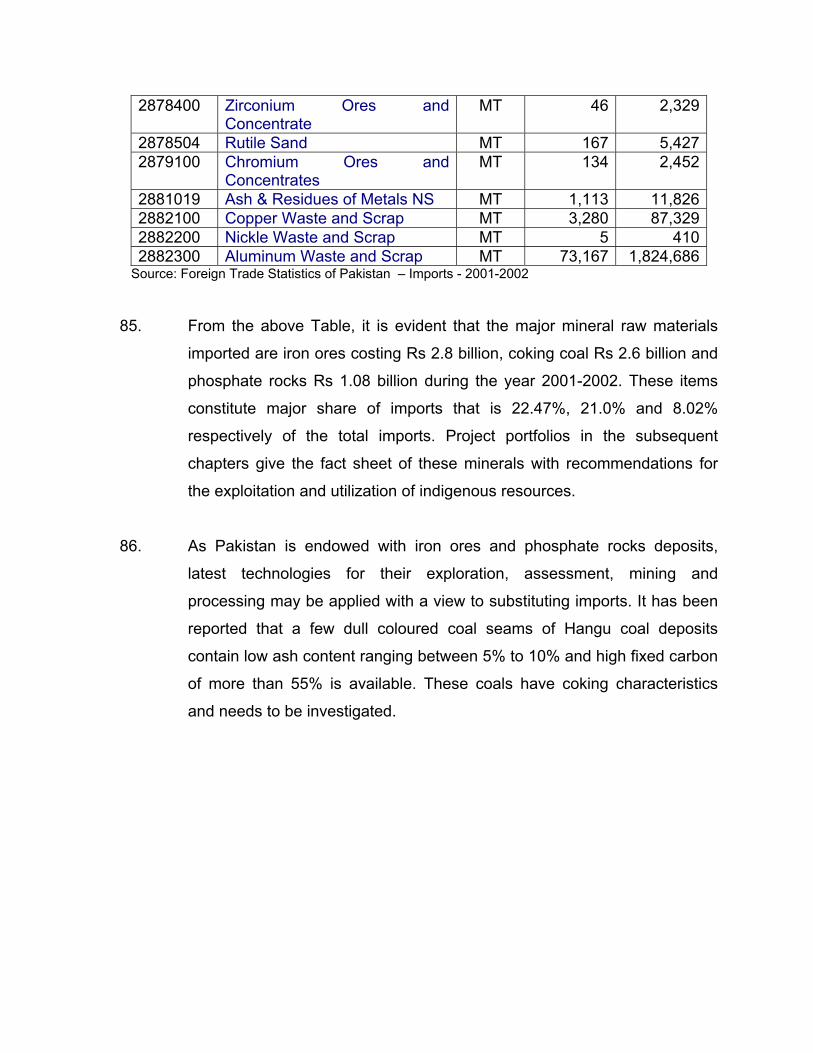

Accordingly, the study has been

completed that contains

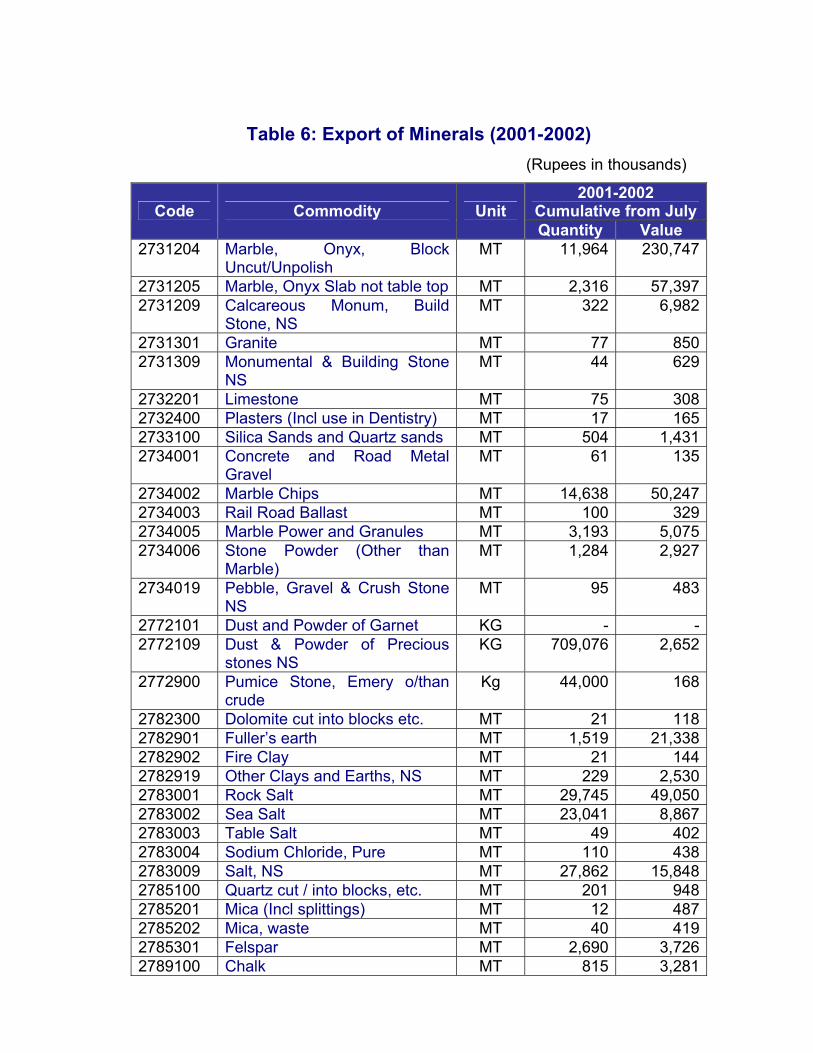

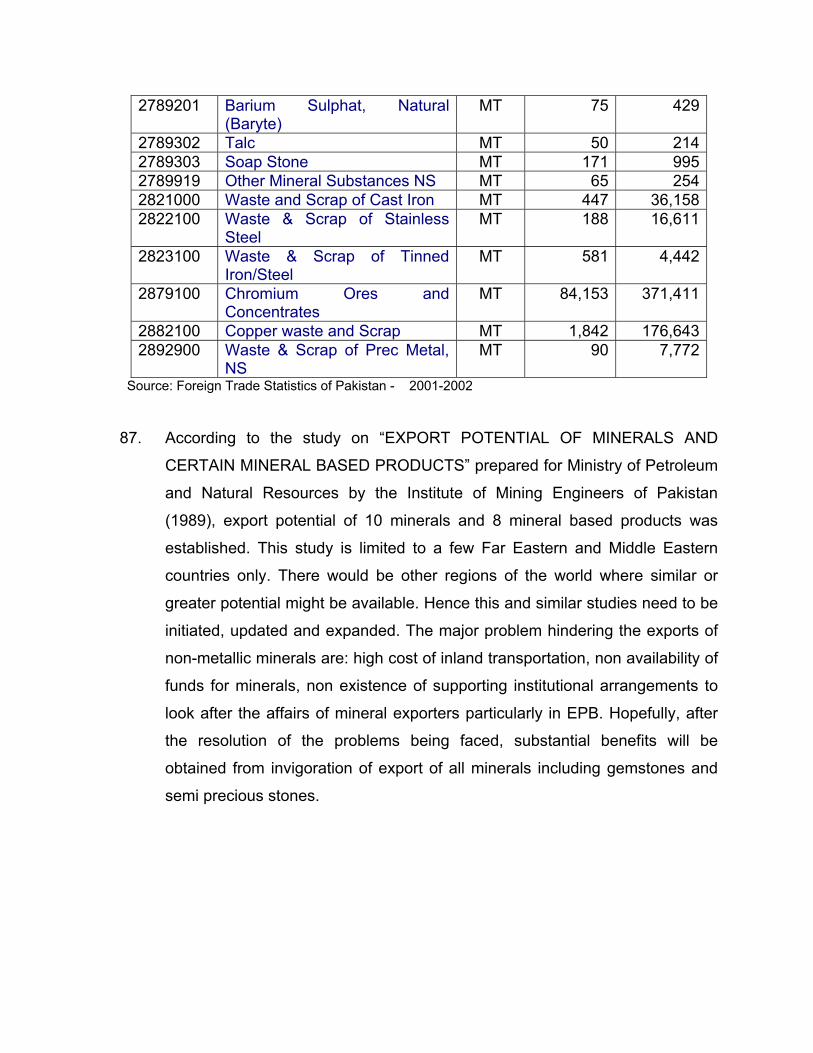

amongst others geo-scientific,

technological, policy matters,

availability of physical and

human infrastructure and

describes portfolios of 15 top

minerals that have potential of

development for export purposes,

import substitution and local

consumption on immediate and

short term basis.

In the end, I am grateful to the

Mineral Sector stakeholders

representing public and private

sectors, experts and professionals

who have provided valuable

comments/suggestions for the

finalization of viable and

implementable recommendations

for the consideration and approval

of the Government.

Muhammad Javed Ashraf Hussain Secretary

April, 2004

ACKNOWLEDGEMENT

Experts Advisory Cell gratefully acknowledges the concerted efforts made by Engr.

Tajammal Hussain, Consultant on Minerals in the preparation of this document. The

main theme of this effort was to provide dynamic tool for the development of

minerals and mineral based industries in Pakistan through integrated concept

involving multitude of geo-scientific and technological disciplines.

The consultant gathered, compiled, documented and analysed the available

geological and technological data, with a view to identifying the metallogenic regions

and high mineral potential areas. This resulted in preparation of portfolios of top 15

mineral deposits that have good potential to replace imports/ exports & thus attract

investment. Further, to facilitate the potential investors, geological and mineral data,

R&D infrastructure, policy and fiscal matters have been documented.

It is hoped that the recommendations made in the report, as generally agreed by more then 85% of the stakeholders who responded to EAC letter of January 15, 2004, would be realized by the public and private sector.

Experts Advisory Cell

Islamabad April, 2004

Table of Contents

Preface ............................................................................................................................... i

Message from Minister for Industries & Production, Govt. of Pakistan........................ ii Message from Secretary, Ministry of Industries & Production, Govt. of Pakistan ...... iv Contents ............................................................................................................................. vi EXECUTIVE SUMMARY.................................................................................................. 1 CHAPTER – I INTRODUCTION ................................................................................................................ 7 CHAPTER – II GEOLOGICAL AND MINERAL POTENTIAL OF PAKISTAN A. GEOLOGICAL FRAMEWORK ................................................................................. 9 Tectonic and Structural Features ................................................................................. 9 General Geological Division and Mineralization ...................................................... 14 a. The Plain Area .......................................................................................... 16 i) Platform Area ........................................................................................ 16 ii) Fore-deep Area ..................................................................................... 16 iii) Shield Rocks ......................................................................................... 18 b. The Folded Belt......................................................................................... 18 i) Potwar Area .......................................................................................... 18 ii) Suleman Range ................................................................................... 19 iii) Kirthar Range........................................................................................ 19 c. Melange Zone ........................................................................................... 19 d. Himalayan Crystalline Belt ...................................................................... 20 e. Kohistan - Island Arc................................................................................ 21 f. Karakoram Block ...................................................................................... 21 g. Chagai Arc ................................................................................................ 22 h. Makran Trench Zone ................................................................................ 22 PRIORITY REGIONS ...................................................................................... 23 Selection Criteria i) Lasbela Khuzdar Belt ............................................................................ 23 ii) Chagai Volcanic Arc.............................................................................. 24 iii) Kohistan – Island Arc ............................................................................ 24 iv) Indus Basin – (Sedimentary Basin) ...................................................... 25 v) Shield Rocks ......................................................................................... 25 vi) Makran Trench ...................................................................................... 25

B. ECONOMIC GEOLOGY OF PAKISTAN High Mineral Potential Zones As Identified by German Consultants Area 1: Chilas- Chilas Ultramafic–mafic Rock Complex, Northern Areas.................... 28 Area 2: Jijal- Jijal Ultramafic–mafic Rock Complex, Northern Areas........................... 29 Area 3: Sakhakot, Qila Sakhakot, Qila Ultramafic-mafic Rock Complex, N.W.F.P ..... 29 Area 4: Hunza - Suture Associated Gemstone Zone. Hunza, Northern Areas ............... 29 Area 5: Swat - Suture Associated Gemstones Zone, NWFP. ........................................ 30 Area 6: Awerith - Polymetallic Mineralization Chitral, NWFP ..................................... 30

Area 7: Drosh - Polymetallic Mineralization Chitral, NWFP......................................... 30 Area 8: Abbottabad - Precambrain – Paleozoic Tertiary, Abbottabad - Mansehra-

Muzafarabad, NWFP & AJK ............................................................................. 30 Area 9: Chiniot - Igeneous – Contact Metasomatic gold-bearing iron ore, Chiniot Bangla, Punjab ...................................................................................... 31 Area 10: Muslim Bagh - Ultramafic – mafic- basalt, Rock Com, Muslimbagh – Zhob valley, Balochistan. ........................................................................................... 31

Area 11: Khuzdar - Jurassic Mineralized Carbontes, Khuzdar – Balochistan.................. 31 Area 12: Lasbela - Ophiolite Belt, Jurassic Mineralized Carbonates and Tertiary Sediments, Bela- Duddar- Kundi – Balochistan. .............................................. 31

Area 13: Chagai Raskoh - Chagai Magmatic Arc, Chagai – Dalbindin, Khuzdar – Balochistan ....................................................................................... 32 Area 14: Saindak - Saindak Porphyry Copper Area, Saindak –Mashi chah – Nokkundi, Balochistan ....................................................................................... 32 Sequence of Steps for Carrying Out Exploration Projects as Suggested by German Consultants. i) Database ............................................................................................................ 32 ii) Geology .............................................................................................................. 33 iii) Geochemistry ..................................................................................................... 33 iv) Geophysics ......................................................................................................... 33 v) Drilling ............................................................................................................... 33 vi) Technological Testing and Planning .................................................................. 33

CHAPTER – III GEOLOGICAL AND MINERAL DATABASE i) Database on Mineral Occurrence ............................................................................ 34 ii) Status of Geological and Geophysical Mapping ...................................................... 34 iii) Mineral Deposits and Production............................................................................. 36 CHAPTER – IV EXPLORATION AND EVALUATION OF MINERAL DEPOSITS (Guidelines) a) Phase I - Technical Studies and Planning ............................................ 46 b) Phase II - Exploration Phase ................................................................... 47 i) Geological Mapping........................................................................................... 47 ii) Geophysical Studies ........................................................................................... 47 iii) Geochemical Studies .......................................................................................... 47

iv) Mineralogical, Pegtrological, Petrographic, Stratigraphic and Sedimentological Studies ................................................................................... 47

v) Drilling ............................................................................................................... 48 vi) Technological Testing. ....................................................................................... 48

CHAPTER – V GEOSCIENCE ORGANIZATIONS A. Federal a. Geological Survey of Pakistan (GSP) i) GSP HQ, Quetta ................................................................................................ 49 ii) Analytical Chemistry Division, Quetta .............................................................. 49 iii) Sedimentary Geology, Quetta ............................................................................ 50 iv) Geophysical Division, Quetta ............................................................................ 50 v) Services Division, Quetta................................................................................... 50 vi) Petrography Branch, Quetta ............................................................................... 50 vii) Photogeology and photogrammetry Branch, Quetta .......................................... 50 viii) Publication Directorate, Quetta .......................................................................... 51 ix) Geo-Science Research Centre, Islamabad.......................................................... 51

x) Seven Divisions/Directorates/Centre of GSP established in Quetta, Karachi, Lahore, Islamabad, Peshawar and Muzzafarabad. ............................................. 51

b. Pakistan Mineral Development Corporation, Islamabad. ................................. 51 c. Federally Administered Tribal Area Development Corporation ...................... 52 d. Pakistan Council of Scientific &Industrial Research Laboratories (PCSIR) .. 52 i) Mineral and Metallurgy Centre, Lahore............................................................. 52 ii) Glass and Ceramic Research Centre, Lahore ..................................................... 52 iii) Fuel Research Centre, Karachi........................................................................... 52 iv) Mineral Technology Division, Peshwar ................................................. 53

B. PROVINCIAL a. Punjab Mineral Development Corporation. ........................................................ 53 b. Balochistan Development Authority..................................................................... 53 c. Azad Kashmir Mineral and Industrial Development Corporation................... 54

CHAPTER – VI NATIONAL MINERAL POLICY - 1995

a.BRIEF FEATURES OF NATIONAL MINERAL POLICY (1995)- INCENTIVES FOR INVESTORS

i) Objectives........................................................................................................... 55 ii) Constitutional Position – 1973 ........................................................................... 55 iii) Background........................................................................................... 55 iv) Institutional Arrangements .................................................................... 57 v) Regulatory Regime ............................................................................... 57

Reconnaissance License (RL) ..................................................... 57 Exploration License (EL).............................................................. 58 Mineral Deposit Retention License (MDRL)................................ 58 Mining License (ML) .................................................................... 58

vi) Fiscal Regime..................................................................................................... 59 vii) Arbitration.............................................................................................. 61 CHAPTER – VII PROFILE OF THE TOP 15 MINERAL PROJECTS (documenting overview, status and scope, conclusions and recommendations)

1. COAL ........................................................................................................................... 63 2. COPPER AND COPPER BEARING GOLD AND SILVER .................................. 79 3. IRON ORES ................................................................................................................. 89 4. LEAD-ZINC ORES ..................................................................................................... 96 5. GOLD – PLACER AND MINERALIZED ................................................................ 99 6. CHROMITE ............................................................................................................... 101 7. GYPSUM/ ANHYDRITE ......................................................................................... 104 8. PHOSPHATES ........................................................................................................... 113 9. ROCK SALT ............................................................................................................. 118 10. SOLAR SALT............................................................................................................. 125 11. MAGNESITE ............................................................................................................ 127 12. LIMESTONE FOR LIME......................................................................................... 130 13. KAOLIN (CHINA CLAY) ........................................................................................ 133 14. NATURAL STONES ................................................................................................ 137 15. GEMSTONES ............................................................................................................ 144

GEO-TOURISM - THE SALT RANGE, A Treasure of Tourism .............................. 154 CHAPTER – VIII LOOKING AHEAD – Minerals and Mining: Vision and Strategy............................. 159 CHAPTER – IX CONCLUSIONS AND RECOMMENDATIONS ......................................................... 181 CHAPTER – X OBSERVATIONS AND PROPOSALS ON (EXECUTIVE SUMMARY AND CONCLUSIONS AND RECOMMENDATIONS) OF INVESTMENT ORIENTED STUDY ON MINERALS AND MINERAL BASED INDUSTRIES. Summary .......................................................................................................................... 208 Letter addressed to mineral sector Stakeholders group (Specimen) ................................. 209 List of targeted mineral sector Stakeholders group............................................................ 210 Table showing extracts of the observations/recommendation of the Stakeholders and Consultant response............................................................................................................ 219 FEDERAL A. M/o Petroleum and Natural Resources

1. Director General (Mineral Wing) Islamabad. ........................................................ 232 2. Director General, Geological Survey of Pakistan, Quetta ..................................... 234 3. Managing Director, Pakistan Mineral Development Corporation, Islamabad....... 238

B. M/o Science and Technology

4. Pakistan Council of Scientific and Industrial Research, Islamabad....................... 240

5. National Science Foundation, Islamabad ............................................................... 241 C. Planning and Development Division

6. Chief, Industries, Minerals and Commerce Section. ............................................. 242

D. M/o Industries & Production

7. SMEDA, Peshawar................................................................................................. 243

E. Privatization Division

8. Board of Investment ............................................................................................... 247 F. M/o Kashmir Affairs & Northern Areas and States and Frontier Regions Division.

9. Azad Kashmir Minerals and Industrial Development Corporation. ...................... 248

G. Northern Areas Administration Planning and Development Division

10. Secretary, Planning, Northern Areas...................................................................... 251 H. Atomic Energy Minerals Centre, Lahore.

11. Director General – PAEC....................................................................................... 255

I. Pakistan Atomic Energy Commission, Islamabad.

12. Directorate of Nuclear Fuel Cycle ......................................................................... 258 J. PROVINCIAL

13. Director General (Mines and Minerals), Govt. of the Punjab, Lahore................... 260

14. Director General (Mines and Minerals), Govt. of Balochistan, Quetta. ............... 261

15. Director General, Sindh Coal Authority, Karachi. ................................................ 262 16. Director General (Mines & Minerals), Govt. of NWFP, Peshawar. ..................... 263

K. ACADEMIA

17. Director, National Centre of Excellence in Geology- University of the Peshawar. 264 18. Chairman, Mining and Geological Engineering Department, University of

Engineering and Technology, Lahore. .................................................................. 267

L. EXPERTS 19. Dr. Naseeruddin Sheikh (Retd) Member (Tech) PCSIR.................................. 268 20. Ex-Senator, Mr. Saifullah Khan Paracha, Quetta. ........................................... 276

M. INTERNATIONAL ORGANIZATIONS

21. Country Director, Asian Development Bank, Resident Mission, Islamabad. ....... 279 22. Manager, Mining Department WB – Mining Department Washington USA....... 281 23. Dr. Ludwig Hofmann, RE UND, WASSER, GMBH, Germany ................ 288

N. PROFESSIONAL BODIES 24. Pakistan Gelological Society.................................................................................. 289 25. Institute of Mining Engineers, Pakistan ................................................................. 292

O. ENGINEERING DEVELOPMENT BOARD

26. Co-ordinator – Engineering Development Board .................................................. 294

P. FRONTIER MINE OWNERS ASSOCIATION NWFP

27. Chairman, Frontier Mine Owners Association ..................................................... 295

CHAPTER – XI REFERENCES................................................................................................................... 299

TABLES

Table Nos.

Page

1. Status of Geological and Geophysical Mapping…………………….. 34 2. Summary of Mineral Production (Average)…………………………. 36 3. Resource Summary of Copper and Gold-Rekodiq; Balochistan…. 38 4. Reserve Summary of Copper – Gold H4-Rekodiq, Project and

Saindak Project………………………………………………………....

38 5. Imports of Minerals & Metal Scraps (2001-02)……………………... 39 6. Export of Minerals (2001-02)…………………………………………. 42 7. Export Potential of Minerals and Gemstones……………………….. 44 8. Export Potential of Mineral Products………………………………… 45 9. Summary of Fiscal Regime…………………………………………… 62

10. World Wide Share of Coal in Electric Power Generation – Dec, 2002……………………………………………………………….

64

11. Characteristics of Major Coal Fields ………………………………… 74 12. Pakistan Coal Reserves/ Rsources as on June 30, 2002…………. 76 13. Thar Coal Reserves / Resources…………………………………….. 77 14. Thar Coal – field (investigated Blocks)………………………………. 78 15. Table showing Regional Copper+Gold Deposits of the Tethyan

Magmatic Arc……………………………………………………………

82 16. Location, Reserves, Quality and Accessibility of Iron Ore

Deposits…………………………………………………………………

89 17. Type of Phosphate Rocks, Reserves and Grades…………………. 115 18. Locality wise Ore Reserves of Rock Phosphate in Hazara;

NWFP……………………………………………………………………

115 19. Chemical Composition of Raw and Washed Clay of ShahDheri;

NWFP and Nagar Parkar; Sindh……………………………………...

134 20. Chemical Analysis of Islamkot China Clay………………………….. 135 21. Major Color and Shades of Natural Stones…………………………. 139 22. Color and Shades of Marble and Onyx……………………………… 140 23. Gems, Precious and Semi-Precious Stones reported to be

occurring in Pakistan…………………………………………………..

146 24. Mineral Production - Perspective Plan (vision 2010) by GSP

andExpected Growth Pattern of Some Key Indicators of Mineral Sector in Pakistan (from year 2000 to year 2025) by GSP………..

173 25. Proposed Projects with Additional year wise Financial Allocation,

for Reflection over 7 years period (2004-2011) in the perspective Development Plan (2001-2011) by Ministry of Science and Technology……………………………………………………………...

175

ILLUSTRATIONS

Figure Nos.

Page No.

1. Tectonic Plates…………………………………………………………. 11 2. Tectonic Zones of Pakistan…………………………………………… 13 3. Geological Map of Pakistan…………………………………………... 15

4. Geological Sketch Map of Pakistan………………………………….. 17 5. Principal Mineral Zones of Pakistan…………………………………. 27 6. Major Economic Mineral Deposits of Pakistan (2003)……………... 35 7. Status of Geological Mapping by GSP………………………………. 37 8. Map showing Major Coal Fields of Pakistan………………………... 66 9. Investigated Blocks at Thar Coal field……………………………….. 75

10. Location Map of Saindak Copper operations and Reko Diq Copper–Gold Deposits – Regional Infrastructure…………………..

81

11. Map showing Tethyan Porphyry Copper Belt ……………………… 83 12. Location Map of Iron Ore Deposits………………………………….. 91 13. Location Map of Lead-Zinc Deposits; Duddar; Balochistan………. 97

14. Location Map of Northern Pakistan – AIDAB-PAK Gold

Exploration Project……………………………………………………..

100

15. Location Map of Pakistan’s Main Gypsum Deposits………………. 106

16. Location and distribution of Hazara Phosphate deposits, NWFP, Pakistan………………………………………………………………….

114

17. Location map of Rock Salt Mines and Quarries operating under Pakistan Mineral Development Corporation…………………………

119

18. Flow Sheet line-diagram of Rock Salt Crushing and Grinding Iodated Salt Plant; Hattar; NWFP…………………………………….

124

19. Location map of Kumhar Magnesite Deposits Abbottabad; NWFP. 128

20. Map of Pakistan showing location of the Main Granite Areas…….. 138

21. Location Map showing Gilgit’s Main Granite Deposits…………….. 142 22. Major Tectonic Features of Northern Pakistan and Location of

Gemstone Deposits…………………………………………………….

145 23. Location Map of the Salt Range and Kohat Showing Salt

Exposures………………………………………………………………

155

EXECUTIVE SUMMARY

This Executive Summary presents review of mineral industry, geological

aspects, mineral data base, R&D infrastructure in geo-science organizations, policy

matters and fiscal measure, metallogenic regions, high mineral potential areas,

exploration and evaluations frame work, portfolios of TOP 15 mineral deposits,

proposed mineral based projects, mineral sector vision and strategy and suggested

Plan for Action for the fast track development of the sector.

Review Pakistan has a widely varied geological frame work, ranging from pre-Cambrian

to the Present, that includes a number of zones hosting several metallic minerals,

industrial minerals, precious and semi-precious stones. Although many efforts have

been made in developing geological products, institutional, academic and R&D

infrastructure, enough remains to be done to enable this sector to take full

advantage of its endowment. As a result of various toils devoted for the development

of mineral sector, resources of several minerals have been discovered over the last

many decades, including world class resources of lignite coal deposits at Thar,

Sindh, porphyry copper-gold deposits in Chagai, Balochistan, Iron ore deposits at

Dilband, Balochistan, lead-zinc deposits at Duddar, Balochistan, gypsum, rock salt,

limestone, dolomite, china clays etc. in the Indus Basin, ornamental and construction

stones in the various parts of the country; and about 30 different gems and precious

stone deposits in northern Pakistan. These and many other mineral projects are in

various stages of implementation from grass root through exploration, evaluation to

development stages.

However, mineral industry in Pakistan shows that over the last decades the

sector has been allocated very small amount, which has ranged between 0.45% to

2.46% of the total public sector expenditure since first five year plan reflecting its

contribution to Gross National Product (GNP) of just around 0.5%.

Executive Summary

Considering that substantial scope exists for the development of mineral

sector that can drive the economy and enhance industrial growth, Ministry of

Industries & Production through Experts Advisory Cell initiated a study in June, 2003

titled “Investment Oriented Study On Minerals And Mineral Based Industry” covering

geological aspects, policy and fiscal matters, identification of metallogenic zones,

individualizing high mineral potential areas, availability of human and physical

infrastructure with geo-science organizations, preparation of project portfolios of top

mineral deposits that have good chances of being exported, replacing imports and

have potential for local consumption. Further it was also required to collect, compile,

document and analyse mineral related data and to prepare predictable and viable

visionary approach and strategy for the minerals and mining sector.

Pursuant to the task assigned, relevant and latest geo-scientific, technological

and mineral database available with various government and semi-govt.

departments of federal and provincial govts. was collected and analysed. It was

known that some excellent reviews of potential metallogenic zones, sectoral and

project specific studies, feasibility studies, techno-economic reviews and thorough

exploration reports are available. Thar and Lakhra coal studies, techno-economic

reports on phosphates, gypsum, rock salt and magnesite deposits, UNDP/PMDC

feasibility work on Duddar zinc-lead deposits followed by work done on the same

deposit by Australian mining company pasminco, extensive work done by foreign

consultants and copper mining companies in the copper-gold mineralized regions of

Balochistan, Iron ore deposits study in Chagai and Kalat areas of Balochistan, geo-

chemical surveys for gold in northern Pakistan by Australian company and on

several industrial minerals as well as natural stones evaluation work has been done.

Undoubtedly much more work has been carried out in the geological departments of

various universities, geo-sciences labs of GSP and by the geo-scientists Museum of

Natural History, Islamabad. Efforts has been made to hold discussion with the key

persons to obtain their expert views and comments during the scrutiny of various

reports with a view to meeting the requirements of the Term of Reference of the

study.

Executive Summary

Brief description of the conclusions drawn and recommendations framed are

given below. Detailed description is documented in the report.

Geological Aspects Availability of thorough knowledge of geology and mineral potential is a

requirement for mineral investors who are risk takers and determined explorationists.

It is an alarming situation that only 33% of the total area of Pakistan is geologically

mapped to the scale of 1:50,000. For the speedier and accurate geologic mapping it

is recommended that:

i) a Remote Sensing Centre may be set up in GSP as application of this technology would save time and money through better programming of field trips in the promising areas.

ii) The geological maps and products prepared by various public sector mining departments and geological departments of universities may be checked and added in the inventory of GSP wherever considered necessary.

Data Base GSP may ensure access to the following: i) open file data (records of

geological maps, technical reports and borehole logs); ii) mineral locality data base

(synoptic information on all mineral showings; iii) mining database (plans of

abandoned mines) ; iv) national core library (library of drill holes); and v) Import-

export material.

R&D Aspects-Geoscience Organizaitons Availability of highly trained manpower, sophisticated equipment, testing

instruments and pilot plant facilities with various geo-science organizations has been

documented in the report. To facilitate in developing awareness and workable

linkages between the mining industry and geo-science organizations, it is

recommended that R&D infrastructure may continue to be updated and

disseminated.

Executive Summary

Policy Matters and Fiscal Measures National Mineral Policy (1995) being adequate and, as such, should remain

intact though necessary improvement may be made with a view to making it more

investment friendly. Metallogenic Regions Geo-scientific studies and surveys have identified following regions containing

world class mineral deposits.

i) Lasbella Khuzdar Belts, Balochistan: This belt extending hundred of kilometers from north of Karachi (Labela) to south of Quetta containing lead-zinc deposits and ultramafic rocks hosting chromite and platinum group elements (PGE).

ii) Chagai Island Arc, Chagai, Balochistan: This metallogenic province hosts world class porphyry copper+gold and molybdenium deposits. These deposits are being investigated and operated by foreign investors. Iron ore deposits near Dilband are also being evaluated from beneficiation stand point.

iii) Kohistan – Laddakh Island Arc: This region consisting of northern Pakistan hosts, gold, precious stones, platinum group elements and rare earths.

iv) Indus Basin: This basin contains large quantities of industrial minerals while the shield rocks consists of granite and iron ores.

High Mineral Potential Areas German Consultants Grundstofftechnik Gmbh, in association with preussag AG,

Metall, Mine Consultant hired by Asian Development Bank formulated a 10 years

National Mineral Exploration Programe (NMEP), which concentrated on the high

mineral potential Areas (1993). Fourteen Areas were individualized along with

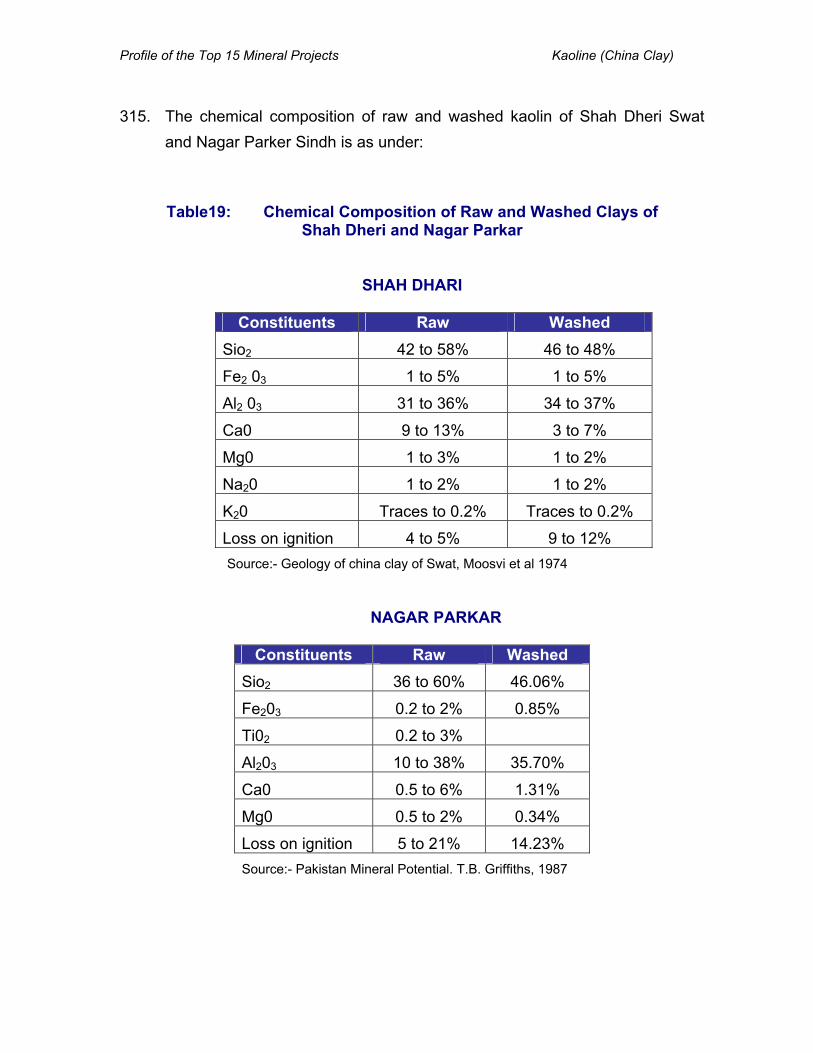

definite action plan. GSP worked with the consultants and designated as the

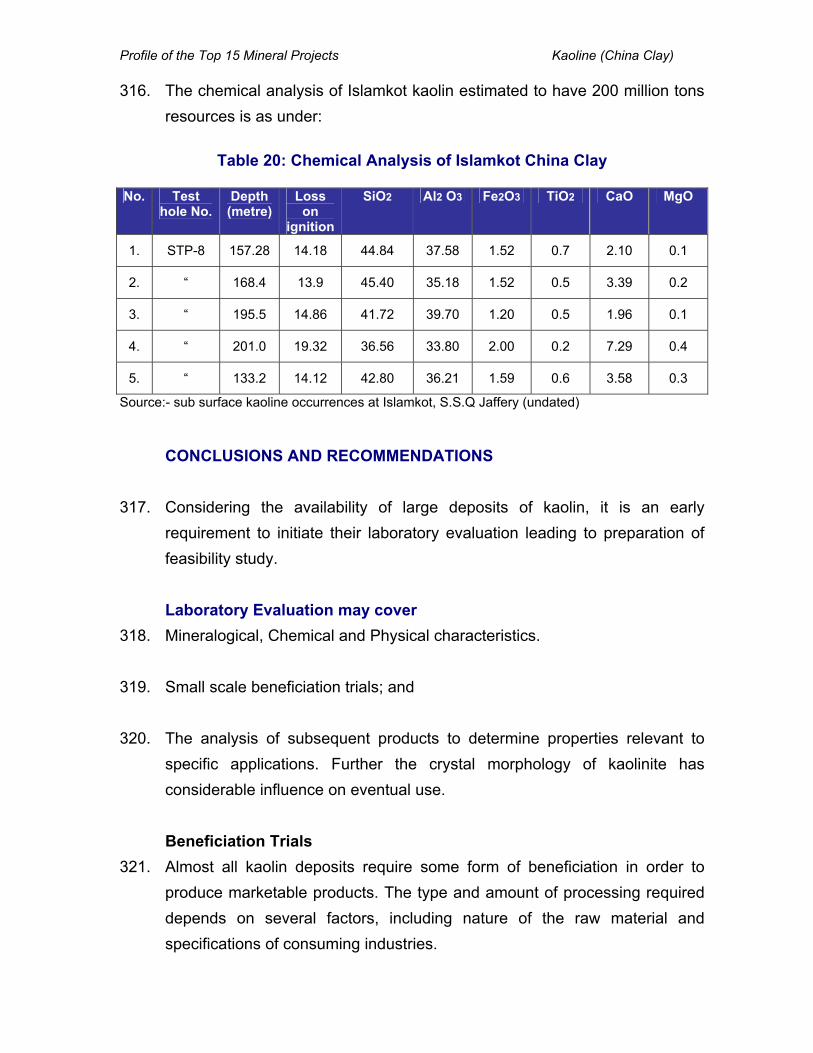

institution to implement this National Mineral Exploration Program (NMEP). Details

of the same are given in the main report while capsule description is documented in

the chapter on Conclusions and Recommendations. Similarly details of proposed

mineral projects are also given in the same chapter.

Executive Summary

Evaluation and Exploration of Mineral Deposits Mineral exploration and evaluation require high technology, high risk and expensive

exploration programe, This programe should be well focused and well defined and

its feasibility study may cover: i) Technical Studies and Planning (literature studies,

selection of target areas, mode of mineralizaition etc), and ii) Exploration Phase

(geo-scientific mapping, laboratory evaluation, drilling and test mining operations

and technological testing). It is vital that exploration be conducted in stages in order

to encourage regular decision making with respect to abandonment, suspension or

proceeding with exploration of specific areas and mineral deposits.

Project Portfolios of Top 15 Mineral Deposits Description of all mineral occurrences/deposits is an encyclopaedic task – far

beyond the scope of this study. Only Top 15 mineral deposits/areas have been

included that have good chances of being exported, replacing imports, have

potential for local consumption and attract investment. They include coal, copper

and copper bearing gold and silver, iron ores, lead-zinc ores, gold-placer and

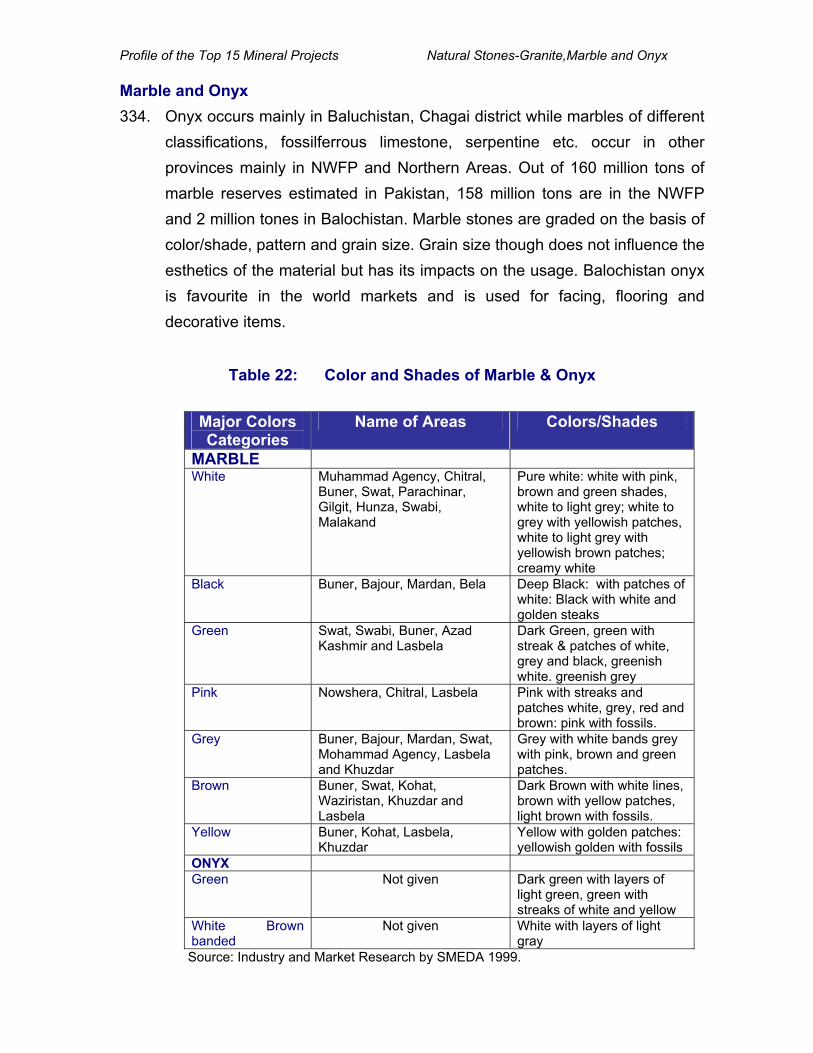

mineralized, chromite, gypsum/anhydrite, phosphates, rock salt, solar salt,

magnesite, limestone for lime, kaolin, natural stones and gemstones. Detail of the

same is given in the body of the report while summarized version may be seen

under the chapter of Conclusions & Recommendations.

Looking Ahead Based on the current mining situation, effort has been made to predict and

project a few viable and implementable propositions. This is a difficult task

particularly in the mineral sector as it is vast, complex sector and difficult to see twist

and turns that future may bring.

Executive Summary

Plan for Action Under the headings of various chapters, Conclusions have been drawn and

viable Recommendations made. In view of National urgencies and for obtaining

optimum benefits within the shortest possible time, it is necessary that the suggested

recommendations may be translated into Action Plan, wherever considered

necessary. This may be done by the Ministry of Petroleum & Natural Resources in

consultation with Ministry of Industries & Production, other concerned Federal

Ministries and Provincial Govt. departments, professional bodies and associations

alongwith domestic and foreign mineral experts and consultants.

CHAPTER - I

INTRODUCTION 1. The mineral potential of Pakistan is widely recognized to be excellent but its

development is inadequate and slow because of technical, financial and

organizational problems. This is evident from the fact that the sector has been

allocated very small amount which has ranged between 0.45% to 2.46% of

the total public sector expenditure since FIRST FIVE YEAR PLAN, reflecting

its contribution to Gross National Produce (GNP) of just around 0.5%.

2. However, in spite of all these indigenous and external problems, vigorous

efforts have been and are still being made to built the mineral sector as a

significant factor in the national economy. In this context, announcement of

National Mineral Policy (1995), organizational set up, enhancement of training

facilities, R&D infrastructure, availability of professional and skilled manpower

in geoscientific and technological disciplines, activation of private sector and

availability of some excellent reviews of potential metallogenic zones, sectoral

and project specific studies, techno-economic reviews etc. are a few strides

taken for its systematic enhancement.

3. Realizing the importance and need of gauging the availability and suitability of

indigenous mineral recources to meet the present and ever increasing

demand of various industrial sub-sectors i.e, energy (coal), metallurgical (iron

ores, chromite, lead-zinc, copper and associated minerals etc.) refractory and

ceramics (magnesite, clays, soapstone, feldspar etc.) chemical (rock salt,

barite, sulphur, limestone etc), construction (marble, natural stones, gypsum

etc) and agriculture (phosphates, potash, gypsum etc) and numerous other

industries wherein minerals and rocks are required, Experts Advisory Cell of

Ministry of Industries and Production initiated and awarded the study titled “

INVESTMENT ORIENTED STUDY-MINERALS AND MINERAL BASED

Introduction

INDUSTRIES” to Engr. Tajammal Hussain, consultant on minerals on June

20, 2003 required to be completed on or before Feb 20, 2004.

Terms of Reference of the Study 4. ‘To attract investor’s interest in Minerals and Mineral Based Industries in

various sectors of economy, the selected consultant would undertake interalia

the following assignments:

i) To review the existing available geo-scientific and other related data and include existing policies, regulations and fiscal matters;

ii) To inventorize and tabulate the mandate, manpower, sophisticated equipment etc. of geo-sciences R&D centres and other related institutions.

iii) To contact through e-mail, fax, phone, correspondence and/or through personnel discussion with Government functionaries, experts, associations, professional bodies, UNDP, UNESCAP etc for the recommendations to boost Mineral sector.

iv) Based on above, identifying and to prepare project portfolios on: a) Exploration Target Area (s) b) Economic Mineral Prospect (s)

v) To suggest future course of action’.

5. ‘The above TOR are only notional. They shall be adjusted/modified to prepare an exhaustive, comprehensive, and meaningful and practically implementable report’.

6. Pursuant to the task assigned, the Consultant gathered, compiled, documented and analysed the available geological and technological data, with a view to identifying the metallogenic regions and high mineral potential areas for the preparation of portfolios of top mineral deposits that have good chances of being exported, replace imports and have potential for local consumption and in turn attract investment. Further, to facilities the potential investors, geological and mineral data, R&D infrastructure, policy and fiscal matters have also been documented in the report.

CHAPTER - II

GEOLOGY AND MINERAL POTENTIAL OF PAKISTAN GEOLOGICAL FRAME WORK 7. In as much as Pakistan lies along the contact between the Indo-Pakistan and

the Eurasian Plates, it has had an exceptionally complex geologic history.

Summarized details of geological evolution, tectonic and structural features,

general geological division and mineralization are presented in the following

paragraphs.

Tectonic and Structural Features 8. The crust of the earth has never been static and the region of Karakoram,

Hindukush and the Himalayas is one of the most active geological areas in

the world. Much of the region is the geological filling in a huge sandwich

formed where two great continental crust meet. Pakistan lies on the

northwestern corner of the Indian plate, which represents part of the Tertiary

convergence zone between the Indian and Asian plates. To its south lies the

Indo-Pakistan continental plate and to the north the Asian/Karakoram

continental plate. In between the two continental plates lies an ancient

Kohistan island arc, and on which lies mostly the north and northeastern parts

of the NWFP and the Northern Areas of Pakistan. The deformation style and

structures on the edges of these plates mimic their past and present inter-

relationships.

9. If one looks into the plate tectonic concept, then the Indo-Pak continental

plate, Asian/Karakoram continental plate and the Kohistan island arc

represent three distinct tectonic segments. Research shows that Indo-Pak

continental plate was at the equator or south of the equator about 120 million

years ago. The early rifting of micro-continents away from the northern margin

of the Gondwanaland can be discussed with the development of Paleo-

Neththys with a spreading ridge in between. These microplates gradually

drifted towards north and welded to the Asian plate during Creataceous to

Paleogene times. The Gondwanic continent composed of South Africa,

Pakistan, India, Sri Lanka, Madagascar, Australia, and Antarctica etc. From

80 to 53 million years, Indo-Pak continental plate moved northward rapidly

relative to Antarctica/Australia. With the closure of the back-arc basin, the

Kohistan-Ladakh arc collided with the Eurasian plate between 102-85 million

years. The northward moving India Plate eventually collided with Kohistan –

Ladakh margin about 55 million years ago. The continued underthrusting of

the Indian plate since Cretaceous produced the spectacular mountain ranges

of the Himalaya and a chain of fold-and-thrust belts as thick sheets of

sediments thrusted over the Indian craton (Fig.-1&2). The boundary of the two

continental plates or continents is traceable in the southern Tibet. The

boundary extends to the west and in Pakistan, it bifurcates into two collisional

boundaries, (i) in the north, the boundary between the Asian/Karakoram

continental plate and the Kohistan island arc (Northern suture or Main

Karakoram Thrust; MKT), and (ii) in the south, the southern boundary of the

Kohistan island arc with the Indo-Pak continental plate (Indus suture or Main

Mantle Thrust; MMT). These sutures or the contact boundaries are very

unique where closure of the oceans are reflected by the presence of oceanic

crustal parts similar to the present day oceans.

10. The Indo-Pak continental plate is made up of Pre-Cambrian to Cambrian

basement, and Paleozoic to Mesozoic and Tertiary cover. Several episodes

of plutonic activity ranging from Pre-Cambrian to Permo-Triassic and even

Himalayan age have been recorded in the Indo-Pak continental margin. To

the south lies the Himalayan fold belt, it mostly comprises sedimentary rocks

of fore-deep and pre-cratonic shelf and consists of tightly folded and faulted

sediments of the outer Himalayan belt. Pre-Cambrian Basement rocks are

exposed along the Sargodha High about 80 km south of Salt Range thrust. To

the north the Himalayan crystalline schuppen zone follows the belt: the

precollisional crystalline rocks along the entire Himalayan belt represent this

zone. Further towards north lies the Nanga Parbat Haramosh massif. The rocks

in the massif are mainly remobilized granitic augen gneiss, slate, quartzite,

schist, paragneiss and amphibolite.

11. The Asian/Karakoram continental plate forms a part of the Karakoram-

Himalayan Fold and Thrust Zone. The rocks are predominantly pelitic and

comprise phyllites, schists, gneisses, marbles and amphibolites. These rocks

follow the arcuate trend of the major mega shears in the area and show an

increase in grade of metamorphism from south to north.

12. The collision in the west is oblique along a transgressional fault zone. The

discontinuous belt of ophiolites which runs through the Bela and Zhob valleys

represents the suture. Presently the Chaman / Ornach-Nal Transform Fault

Zone (COTFZ) marks the western plate boundary. The Indian plate is

separated from the Carlsberg Ridge while the Owen Fracture Zone marks the

boundary between the Indian and Arabian plates.

13. The mid Tertiary collision zone east of the COFTEZ can be subdivided into

stratigraphically and tectonically distinct regions viz., Northern Mountain Area,

Axial Belt and Indus Basin. The vast Indus Basin is located west of the Indian

Shield and extends from the Main Boundary Thrust in the north to the

offshore area south of Karachi, east of the Murray Ridge. The Indus Basin is

further subdivided into Upper, Middle and Lower Indus sub-basins. The Indus

Basin covers an area more than 25,000 sq. km in southeastern Pakistan and

includes the Indus Plain Thar-Cholistan Deserts. The Basin contains

sediments ranging from Pre-Cambrian to Tertiary with a well developed

plateform deposits of Jurassic. The area west and northwest of the Axial Belt

represents the Balochistan Basin, which includes the Makran Subduction

Complex and Kakar Jhurasan Flysch Trough. The rocks exposed in the

Balochistan Basin are mainly Cenozoic with a few isolated outcrops of

Cretaceous age. The evolution of the Balochistan and Makran areas persued

a different fashion from that of the Indus Basin. The northwest drift of the

Central Iran, Lut and Afghan microcontinents from the Gondawanaland, most

probably started as early as Permian. The presence of arc associated

volcanics in the Chagai and Raskoh Magmatic Belts of the Campanian age

suggests that a subduction complex had developed along the southern margin

of these microplates, probably during the Cenomanian. The accreted

Paleogene Flysch gradually gets younger from north to south.

General Geological Division and Mineralization 14. Pakistan is country where its geologically evolutionary history can be traced

back up to 1.8 billion years. During this long period one can imagine how

many times the area remained under sea for the formation of sedimentary

rocks and how many times igneous lavas have invaded this territory along

with creating metamorphic rocks and a host of complex geometry of the lofty

ranges which look so majestic now. Creation of mineral deposits is a side-by-

side mechanism that is only understandable with a broad geological

framework in mind.

15. Broadly hilly and mountain areas constitute about 60% of the country leaving

40% area as plain that merges into Arabian sea towards south. Plain areas in

fact belong to ‘concealed’ geology as hard rocks are lying beneath the entire

very thick cover of soil whereas mountains and hills are ‘exposed’ part of the

geology. Mineral resources, including oil and gas, are scattered both in

concealed as well as exposed part of the geology. Regional configuration of

the important ranges like Karakoram, Himalaya, Salt Range, Koh-i-Suleiman,

Kirthar, Chagai hills and Makran coastal area are result of an evolutionary

process where advance and retreat of sea, settling of sedimentation, eruption

of lavas and movements of earth crust in different directions due to regional

tectonic forces has played their respective vital roles in making the present

shape of our mighty ranges and plain areas (Fig-3).

16. For understanding general geological features the country can be

conveniently divided into eight parts as marked on Fig-4, which are:

1. The Plain Area

2. The Folded Belt

3. The Melange Zone

4. The Himalayan Crystalline Belt

5. The Kohistan Island Arc

6. The Karakoram Block

7. The Chagai Arc

8. The Makran Trench Zone

Brief description of each part is given here:

The Plain Area

17. The plain area comprises those parts where the Indus river along with its

tributaries settle their sediments and cover major part of the Punjab and the

Sindh provinces. This vast territory is geologically divided into:

Platform Area 18. Platform Area occupying all along the Indian borders. Thickness of soil

increases from east to west. This part is well known for its oil and gas

resources in Sindh. Quite recently huge coal resources have been discovered

in the Thar area. The same types of resources are expected to be discovered

in the Fort Abbas area of the Punjab as well.

Fore-deep Area 19. It is a stretch of land where rocks are deeply buried under the soil. It spreads

from Kashmore, Sibi, to D.G. Khan.

Shield Rocks 20. The above two areas have been pierced at Chiniot and Sangla hills in the

upper Punjab by one of the oldest rocks of Pre Cambrian age known as

Shield rocks. In Sindh such rocks are exposed in the Tharparker area. Chiniot

iron ores are being evaluated while pink granite and china clays are being

mined at Tharparker. The shield rocks, world over host precious and semi-

precious metallic mineral deposits.

The Folded Belt 21. These northern and western peripheral parts of the plain areas are occupied

by a sequence of sedimentary rocks which distinctly form three units as:

Potwar Area 22. It is bounded by Margalla and Kala Chitta hills towards north and Salt Range

in the south. These ranges are roughly east west in their direction. Both these

ranges seem abruptly emerging out at the surface by virtue of deep rooted

thrust faults traced all along their feet. Thrust line along which Margalla and

Kala Chitta Hills slipped upward is known as Main Boundary Thrust whereas

such a thrust at the base line of Salt Range has been named as Main Frontal

Thrust. Movements along these thrusts cause earthquake. Sedimentary rocks

comprising Salt Range are as old as Pre-Cambrian, just more than 500 million

year ago. Whereas Jurassic rocks (about 150 million years) are quite known

in the Margalla rocks. Highest age across the Indus river of such rocks is

Ordovician (about 350 million years) where Nowshera reef is a typical

example. Both these ranges were formed under shallow to deep-sea

environment in their early times succeeded by river conditions. World-Class

rock salt resources are confined in the Salt Range. Other important well

established mineral resources include limestone, dolomite, coal; iron ore,

bauxite, gypsum, and silica sand. Black limestone around Taxila is historically

used as a decorative building stone and kitchen wares while phyllitic rocks (a

mild metamorphosed shale rock) have been used in statue making. Other

minerals include fire clay, bentonite and ochre which are used in sanitary

wares, drilling mud and paint industry respectively. Buried sequence of rocks

in the Potwar plateau is a rich potential for oil and gas.

Suleiman Range 23. Area falling in between Quetta, Sibi, D.G. Khan and D.I. Khan, up to the

confluence point of Kurram river with the Indus form a separate garland-like

structure of rocks known as Koh-I-Suleiman ranges. These rocks have been

originated in a shallow to deep sea environments with younger rocks

comprising river deposits. Here too, Jurassic rocks are the oldest one. There

is a variety of industrial minerals identified in these rocks besides oil and gas

being extracted in this zone. limestone, dolomite, gypsum, fullers’ earth, silica

sand and iron ore near Sakhi Sarwar are quite well known. Uranium ore of

commercial quantity was first established as a river-type deposit at Baghal

Chur, west of D.G. Khan. Small quantity of coal has also been reported west

of Kot Addu.

Kirthar Range 24. It occupies much part of the District Dadu and Larkana of the Sindh province

where rocks are extremely low lying. There are some exposures of Jurassic

rocks as the oldest rocks in the area. Primarily rocks are of younger age

comprising river type deposits. The area is well known for its coal resources.

Besides oil and gas, silica sand, limestone, dolomite fuller’s earth and gypsum

are mined at different localities. The area is also known for its variety of clay

minerals. Celestite is also reported from this area.

Melange Zone 25. The plain area and the rocks of folded belt are generally put together under a

big single unit named as the Indus Basin. Further peripheral extension

towards west of the Indus Basin comprises a highly specific zone geologically

known as Melange Zone. It is a zone created by the collision of Indus Basin

rocks with the Balochistan Basin rocks in the west and with the Afghanistan

Basin rocks in the north-west. These three independent basins are largely

referred as Indo-Pak plate (Indus Basin); Afghan micro plate and Lut mirco

plate. It is due to the collision and interaction of these three plates which has

generated this special zone known as Melange Zone. On the basis of its

lithological varieties this zone is also known as Ophiolitic Zone. This block of

rocks starts emerging at Las Bela, continues towards Khuzdar, Zhob and

Waziristan. This collision occurred about 30 km down beneath the surface of

earth generating igneous activity during the Cretaceous time. Technically the

Indo-Pak plate simply brushed with the Balochistan plate creating one of the

largest fault in the sub-continent. There was great uplift and intrusion of

magma into the sedimentary sequence of rocks resulting a mix of crumbling

rocks. The sub-surface magma brought upward minerals like Muslim Bagh

and Waziristan chromite and lead and zinc at Duddar near Bela and Gunga

valley near Khuzdar. Malakand chromite is a part of mélange zone. Lead zinc

occurrences are reported at more than a dozen place. Dilband iron ore and

fluorite deposit, barite at Khuzdar, copper and manganese at Waziristan,

asbestos and titanium at Zhob are quite known mineral occurrences of this

belt. Some gemstones have also been discovered in the Mohmand Agency of

FATA. Swat emerald is yet another example of mineralization along the

mélange zone. There are very large deposits of marble besides quartzite and

soapstone.

Himalayan Crystalline Belt 26. The fourth zone has been identified as the Himalayan Crystalline Belt. It is a

very complex zone lying in between the Margalla – Cherat Hills towards south

to Pir Punjal and Basham area towards north. It covers areas such as Azad

Kashmir, Hazara, lower part of Kohistan, Abbotabad, Mardan and Charsada

etc. The oldest sedimentary rocks (Pre-Cambrian age of about 600 million

years) of the country are exposed in the Hazara area. It is here that age of a

granite rock located south of Basham has been calculated as 1.8 billion years.

The sedimentary sequence has been intruded several times with different

magmas at different places thus generating pure igneous to pure

metamorphic rocks. The belt is limited in the north by a yet another deep

rooted thrust fault which is geologically known as Main Mantle Thrust (MMT).

The Himalayan Crystalline belt is part of the Indo-Pak plate.

27. There is a variety of minerals in these rocks due to their complex nature of

evolution. There are large deposits of granites and marble and other building

stones. Soapstone at Sherawan, Langrial iron ores, Mohriwali graphite, Kakul

phosphate and quartzite, Oghi feldspar, nephline syenite, phyllite and slate

are common. Workers have also reported manganese, ochre and serpentine

rocks.

Kohistan – Island Arc 28. Further to the north of the Himalayan Crystalline Belt there is an area

developed in between the Indo-Pak plate and the Eurasian plate in the

extreme north. This area is geologically labeled as Kohistan Island Arc. This

covers upper parts of the Hazara, Swat and upper part of the Nilum valley.

Chilas, Gilgit, Astor, Skardu, lower parts of Hunza and Yasin valleys, Shindor

Pass and Dir etc. are part of this Arc zone. The Arc has been developed as a

result of the collision between the Indo-Pak plate in the south and Eurasian

plate (Karakoram Block in Pakistan) in the north.

The thrust zone developed towards north is known as the Main Karakoram

Thrust (MKT). The island started building chromite, granites, serpentinites,

feldspar, marble during Cretaceous, some 150 million years ago. Mostly rocks

are huge sheet-like structures. There are high temperature igneous and

metamorphic rocks. Important minerals include placer and host rock gold,

nickel, platinum and garnet. Marble and granite are available as building

stones. Suture zone between Kohistan Island Arc & Indian plate contains

chromite, soapstone/talc, emerald, manganese, quartz, peridote etc.

Karakoram Block 29. Rocks occurring beyond Main Karakoram Thrust (MKT) of the Island Arc up to

the northern borders, Wakhan area of Afghanistan and the China border of Pakistan are part of the Karakoram Block which in fact is the sourthern

continuity of the Eurasian plate. Sheet like east – west trend of the rocks is quite profound. The entire Block is extremely rugged and with very high altitude. About 30% of the area is covered by ice sheets and glaciers. Right from K2 peak, Hushe, Baltistan, Hunza, Ishkoman, upper part of Yasin valley, Tirich Mir and Chitral district is mainly covered by this Block. The oldest rocks are of Ordovician age, some 400 million years ago. Karakoram batholith (mostly granite) is centrally placed creating metamorphic rocks on both of its side. Regionally metamorphosed rocks show huge marble deposits. Dolomitic limestone is quite common. There are well developed slates and schists. Although no significant mining is going on but still the local population is busy in collecting nugget gold, precious stones like ruby, aquamarine, topaz, tourmaline and quartz crystals. Serpentine rock is used both as a building stone as well as decorative kitchen wares. Some arsenic from Chupurson valley and antimony from Awerith near Chitral has been mined in the past. Regional exploratory work has indicated presence of gold, copper, lead, zinc, antimony, cobalt and nickel. Geologists have equally reported pegmatites containing rare earths, barite, mica, garnet and mica flakes. Further precious minerals include Hunza ruby, tourmaline and emerald. Quartz crystals and feldspars are also common.

Chagai Arc 30. Chagai Arc is a body of volcanic rocks mainly developed during Cretaceous

time with some sedimentary sequence of younger age around Saindak copper deposit. It is one of the richest mineral-bearing areas of Pakistan. There are large iron ores deposits located at Pachin Koh, onyx marble north of Dalbandin, Koh-i-Sultan sulphur, pumice stone and one of the largest World Class copper + gold and silver deposits discovered at Reko Diq and are being evaluated.

Makran Trench Zone 31. Area falling all along Makran and Turbat has been termed as Makran Trench

Zone. It is an active zone where the entire area is rising upward due to the

Arabian Plate moving towards north beneath this zone. Very little exposure of

rocks are seen which include mudstone, sandstone and siltstone. Rather it is

a desert where younger rocks are covered by sandy material known as

accretionary deposit. Zircon and titanium have been reported from a few

places along the coastal areas.

PRIORITY REGIONS 32. The Priority Areas have been identified on the basis of known Metallic and

Non-metallic minerals resources. The criteria for their selection includes but

not limited to the following:

i. Easy and Safe Accessibility.

ii. Availability of geological infrastructure comprising topo graphic maps,

aerial photographs and satellite images along with basic geodata, geo-

chemical, geo-physical surveys and preliminary technological and

economic information.

iii. Areas of increased potential that warrant detailed investigations.

iv. Bearing minerals having bright future for their exploration and setting up

Mineral based industries both for local consumption and export.

v. Attractive for prospective investors.

Lasbela Khuzdar Belt 33. In Khuzdar District, several Lead-zinc prospects were reported. They appear

within a zone of mineralized Jurassic sequences in the generally south-north

striking Kirthar-Sulaiman ranges, from Las Bela area in the south to the Kalat

area in the north. They are of the Mississipi valley or Sedimentary – exhalative

(SEDEX) type origin, and are always associated with barite and often with

fluorite. This Belt extends for hundreds of kilometer north of Karachi (Lasbela)

and upto the south of Quetta (Kalat). According to the reports of Baluchistan

Development Authority (1990), the content of combined lead-zinc vary from

5% to 8% and estimated reserves are 10 million tons in Gunga area.

34. This Belt, therefore, deserves a major geo-chemical survey to compare with

the results of the air-borne electro-magnetic survey done by GSP in late

1980’s. Duddar (200 kms NNW from Karachi) has been thoroughly

investigated by PMDC –UNDP and PASMINCO of Australia establishing 14

million tons of 11% to 12% Pb+Zn deposits at 7% cut off grade. The other

prospects as Gunga and Surmai warrant further evaluation. In addition to

sulphur occurrences of which economic value seems marginal, the belt hosts

ultra-mafic rocks with chromite and platinum group element, manganese,

magnesite, iron ores, vermiculite and barite.

Chagai Volcanic Belt 35. This Belt is principally known for the Saindak porphyry Copper deposits, the

only World Class mining project developed and being operated by Chinese

Company. However, occurrences of gold, iron, silver, copper and

molybdenum have been reported that are being investigated by local public

sector agencies and International Mining Concerns. This metallogenic zone

that extends over an area of about 30,000 sq. km from West (Saindak) to East

(Raskoh) has the potential for other and possibly richer prorphyry copper

deposits than Saindak. Further more, there are several showings of gold and

base metal sulphur mineralization in out cropping volcanic rocks. The

magnetite rich skarn formation which are well developed in the region have a

known potential for base metals and skarn specific silicate minerals. Needless

to say, the infrastructure established for the Saindak Mine is a bonus feature.

Kohistan – Island Arc 36. This area is developed in between the Indo-Pak Plate and the Eurasian Plate

in the extreme north. This area lays in between the Main Mantle Thrust

towards south and the Main Karakoram Thrust towards north. The area

covers upper parts of the Hazara and Swat areas and upper part of the Nelum

Valley, Chilas, Gilgit, Skurdu, Hunza, etc. It contains high temperature

igneous and metamorphic rocks. Important minerals include placer and host

rock gold, nickle, platinum, lead, zinc and garnet. Precious minerals include

ruby, tourmaline and emerald.

Indus Basin (Sedimentary Basin) 37. The Indus basin is the largest and more thoroughly studied basin of Pakistan.

It trends NE-SW for over 1600 Kms along its Axis while its width varies with

an average of 300 Kms. The basin contains sediments ranging from Pre-

Cambrian to Tertiary with a well developed platform deposits of Jurassic

throughout. Low lying sedimentary folded bed of rocks have been geologically

subdivided into three recognizable strategraphic province; (i) The Kohat –

Potwar Area; (ii) Koh-i-Suleman Range; (iii) Kirthar Range.

38. The important minerals available in Potwar area include rock salt, limestone, dolomite, coal, bauxite, iron ores, gypsum, clay, silica sand, radio-active minerals and sandstones.

39. The Suleman Range covers most of D.G. Khan. The important minerals occur

are limestone, fuller’s earth, gypsum, iron ore, dolomite, radio-active minerals. 40. Kirthar Range is the most southern extension of this whole unit of folded rocks

that is mostly exposed in Sindh. Important minerals are coal, limestone, silica sand, dolomite and different clays.

Shield Rocks

41. The oldest assemblage in the Indus basin constitute a part of Indian shield

exposed near Nagar Parkar and Sargodha in the Lower Indus Basin and

Upper Indus Basin respectively. Pink granite and china clay are being mined

in Nagar Parkar while Iron ores are being explored in Chiniot near Sargodha.

Makran Trench 42. Area falling all along Makran and Turbat has been termed as Makran Trench.

It is a desert area where younger rocks are covered by sandy material. Zircon and titanium has been reported along the coastal areas.

ECONOMIC GEOLOGY OF PAKISTAN 43. As substantiated by research and exploration work carried out by various

government agencies and geology departments of universities, Pakistan is blessed with rich and diversified mineral potential. In 1979, (Khan, S.N; Tahirkheli, R.A.K.) tentatively identified mineral zones, which envelop most important mineral occurrences and potential of the country (Fig-5). The folded belts of Permian to mid-Miocene age occupy the western and northern margins of the country. They are generally referred to as Mountainous Areas, and are resulting from the dynamic process associated with Hamalyan Orogeny. Their formation is very complex and the rocks exposed in these areas relate to Island arc sequences, thrusted oceanic crust segments, deep seated metamorphic, mafic and felsic intrusions. These environments are very attractive for metallic mineral exploration. They host majority of the 14 IDNETIFIED METALLOGENIC provinces of Pakistan, which warrant increased exploration efforts.

44. Regarding INDUSTRIAL MINERALS, sedimentary formation of the Indus

Plain covers almost half of the Pakistani territory. Further unfolded or gently folded, their age ranges from Pre-Cambrian to Recent in the north, and from Eocene to Recent in the southern part, also referred to as the Lower Indus Basin. The Lower Indus Basin host large Tertiary coal field of Thar. The showings of the older formations are limited in surface extension. They are mostly buried under the recent alluvial sediments. The oldest assemblage in the Indus Basin constitute a part of Indian shield exposed in lower Indus Basin as “Nagar Parkar Granite” while the exposure of Upper Indus Basin as “Kirana Group”. Overlying the Pre-Cambrian rocks in the Indus Basin is the “Salt Range”. The youngest rocks, “Siwalik Group” contains the best vertebrate faunal succession in the world and have yielded fauna consisting of nearly all types of mamals together with varieties of reptiles, fishes and birds.

HIGH MINERAL POTENTIAL ZONES AS IDENTIFIED BY GERMAN CONSULTANTS.

45. In order to identify and demarcate the high mineral potential areas, Asian Development Bank through its Technical Assistance Programme hired M/S. GRUNDSTOFFTECHNIK GMBH and PREUSSAGAGMETALL – MINE CONSULTANTS of Germany for the execution of task assigned. In this context, the consultants were required to assist Geological Survey of Pakistan (GSP) in formulating a 10 years National Mineral Exploration Programme (NMEP) which concentrate on high mineral potential areas, and advising on required expertise, combination of exploration and mineral evaluation methods to be used and type of equipment required for carrying out mineral exploration related activities. The contract was made in October, 1991 between the Bank and the consultant. The NMEP remained a basic investigation programme – the first step for mineral development. Accordingly, the consultant hired eight qualified professionals, experienced in economic geology, geological mapping, chemistry / geochemistry, geophysics, engineering geology, mineralogy / petrography, cartography and mineral data management. The duration of the study was 18 man-months, including 13 field months and 5 office months. Based on reviewing of available field data and application of modern geological concepts and models, the consultants selected 14 Areas of known metallic and non-metallic mineral resources of high mineral potential. Description of these 14 Areas covering their geological, development potential, accessibility and size of the area to be geologically mapped is given below. According to the consultant the areas are worth to be mapped, prospected and explored in detail.

Area 1: Chilas- Chilas Ultramafic-mafic Rock Complex, Northern Areas 45. The Chilas rock body with indications of Pt, Pt-group elements and chromite

occurrences belongs to the largest basic intrusions in the world, which are continuously exposed. It is approximately 300 km long between Nanga Parbat in the east and Dir district in the west. It is considered as the root zone of the Kohistan Island Arc with its deepest part in the Chilas area.

47. The selected area (100 sq. Km) is accessible by the Karakoram Highway.

Away from the Chilas area, accessibility is difficult.

Area 2: Jijal- Jijal Ultramafic-mafic Rock Complex, Northern Areas 48. The Jijal rock complex with also indications of Pt, Pt-group elements and

chromite occurrences is well exposed between Jijal, Patan and Allai Kohistan.

It covers about 200 sq. km. It represents an upthrusted rock complex against

rocks of the Indo-Pakistan plate to the south.

49. The selected area is about 150 sq. km. Accessibility is difficult.

Area 3: Sakhakot-Qila- Sakhakot-Qila Ultramafic-mafic Rock Complex, NWFP 50. This rock complex is situated in Malakand Agency, west of Dargai. It is about

26 km long and 3 km to 6 km wide. It bears chromite, Pt and Pt-group

elements.

51. The area for detailed investigations covers approximately 200 sq. km.

Accessibility is moderate to difficult.

Area 4: Hunza - Suture Associated Gemstone Zone, Hunza, Northern Areas 52. The zone is marked by the Main Karakoram Thrust and extends for more than

100 km from the Hunza valley to Ish-ko-man. About 350 sq. km are selected

for detailed investigations along the ruby-bearing marble zone.

53. Except for the Hunza valley area, the accessibility is very difficult.

Area 5: Swat - Suture Associated Gemstone Zone, Swat, NWFP 54. The area is associated with the Indus suture zone, marked by the Main Mantle

Thrust (MMT) in Swat district. The area covers 250 sq. km for detailed

investigation along the emerald-bearing belt of talc-chlorite schists.

55. Accessibility is good in the Mingora area, and moderate to difficult in other

parts of the belt.

Area 6: Awerith - Polymetallic Mineralization Chitral, Awerith, NWFP 56. The center of this area is located about 25 km north of Chitral, within a cluster

of Au, Ag, Cu, Pb, Sb, Sn and W occurrences or deposits. Approximately 160

sq. km are selected for detailed investigation.

57. Accessibility is moderate where antimony mining was or is carried out, and

difficult otherwise.

Area 7: Drosh - Polymetallic Mineralization Chitral, Drosh, NWFP 58. The center of the Drosh area lies ca. 25 km SSW of Chitral, within a cluster of

Cu, Pb, and Sb mineral occurrences. The area for detailed investigations

covers approximately 160 sq. km and is difficult to access.

Area 8: Abbottabad - Precambrian-Paleozoic Tertiary, Abbottabad- Mansehra-Mazafarabad, NWFP and AJK

59. Within this Area, occurrences of Au, Ag, Cu, Pb, Mn and Fe mineralizations

and deposits of phosphate, magnesite, talc, glass sand and bauxite are

known. The area, for detailed investigation, covers about 400 sq. km.

60. Accessibility is moderate, in parts difficult.