investment policy statement - home - state super … · · 2017-02-10the purpose of this...

TRANSCRIPT

1

Investment Policy Statement

Version 2

17 June 2015

Investment Policy Statement

2

Investment Policy Statement

1. Introduction ............................................................................................................. 4

2. Purpose and Objective of the Policy .......................................................................... 4

3. Applications ............................................................................................................ 4

4. Governing Legislation and Regulatory Requirements .................................................. 4

5. Formulating Investment Strategy ............................................................................... 5

6. Implementing Investment Strategy .......................................................................... 10

7. Investment Risk Management ................................................................................. 12

8. Monitoring and Reporting ....................................................................................... 13

9. Review .................................................................................................................. 14

10. Definitions ............................................................................................................. 15

Investment Policy Statement

3

Policy Control Information

Policy Name Investment Policy Statement

Policy Owner Chief Investment Officer

Current Version Version 2

Approval Date 2015

Version Prepared By Reviewed By Approved By

Version 1 STC Investment Team Investment Committee 2013

STC Board 2013

Version 2 STC Project Team STC Board

June 2015

STC Board 17 June 2015

Investment Policy Statement

4

1. Introduction

STC was continued on 1 July 1996 under the Superannuation Act 1996 (SA Act) as the Trustee of the following four closed NSW superannuation schemes (the STC schemes):

State Authorities Superannuation Scheme (SASS);

State Superannuation Scheme (SSS);

Police Superannuation Scheme (PSS); and

State Authorities Non-contributory Superannuation Scheme (SANCS).

The assets of the STC schemes are amalgamated into the Pooled Fund under the SA Act.

STC’s governing rules are contained in the SA Act which sets down the functions, duties, powers and obligations of STC. STC's principal functions are to:

administer the STC schemes;

invest and manage the STC Pooled Fund in which the STC schemes invest;

provide for the custody of the assets and securities of the STC Pooled Fund;

ensure STC scheme benefits are properly paid; and

determine disputes under the STC schemes.

In exercising these functions, STC must have regard to, amongst other things, the interests of its members entitled to receive benefits under the STC schemes and the future liabilities of the STC funds.

2. Purpose and Objective of the Policy

The Board is responsible for the sound and prudent management of STC’s investments,

including establishing investment strategies that are appropriate for the size and complexity

of the Pooled Fund.

The purpose of this Investment Policy Statement (IPS) is to document STC’s investment

approach to ensure investment decisions are in the best interests of persons entitled to

benefits under the STC schemes and is compliant with regulatory requirements. The IPS is

STC’s key investment policy document. The policy also addresses key requirements

outlined in APRA’s Prudential Standard SPS 530 Investment Governance.

It is integral that this document is read in conjunction with STC’s Investment Governance

Framework (the Framework).

3. Applications

This policy applies to all STC Board members, the CEO, all STC staff and those operating under delegated authority. This includes third party service providers involved in the management and monitoring of STC’s investments.

4. Governing Legislation and Regulatory Requirements

In developing this IPS, STC has considered the key legislative requirements with respect to investments as it applies to the STC schemes as outlined in the SA Act. Refer to Appendix 1

Investment Policy Statement

5

for the SA Act requirements. The SA Act requires STC to:

Determine and give effect to an investment strategy having regard to the circumstances of the STC schemes, including but not limited to the risks and likely returns from the investment, the composition of the investments as a whole, the liquidity of the investment, and the ability of STC to discharge its liabilities;

Any other matters required to be considered in determining an investment strategy under the Superannuation Industry (Supervision) Act 1993 (SIS Act), including to have regard to the availability of reliable valuation information, costs and tax consequences;

Exercise care, skill and diligence in relation to all matters affecting the STC schemes; and

Exercise its functions relating to the STC schemes in the best interests of persons entitled to receive benefits under the STC schemes.

In executing these requirements, STC must also comply with the limits on its investment powers under the SA Act, the NSW Government’s Public Authorities (Financial Arrangements) Act 1987 (PAFA) and the approvals granted to STC under PAFA.

In addition, the SA Act states that STC must also give regard to the Heads of Government Agreement (HOGA) entered into by the State and Commonwealth Governments relating to the exemption of certain State public sector superannuation schemes from the SIS Act and the Superannuation Industry (Supervision) Regulations 1994 (SIS Regs) of the Commonwealth.

HOGA undertakes to ensure that exempted schemes, such as the STC schemes, will conform to the best of their endeavours with the principles of the Commonwealth’s retirement income policy as reflected in HOGA, and those in Commonwealth legislation, such as SIS legislation and the Corporations Act 2001.

As such, while STC is exempt from meeting the prudential requirements under the SIS Act, as administered by the Australian Prudential Regulation Authority (APRA), STC aspires to be compliant with the APRA’s Prudential Standards, specifically prudential standard SPS 530 Investment Governance (SPS 530) to the best of its endeavours. However, HOGA does require STC to supply APRA with statistical information as required under the SIS Act and the Financial Sector (Collection of Data) Act 2001.

Further, whilst STC is also exempt from investment disclosure requirements in relation to substantial shareholding and takeovers, contained in Chapters 6 and 7 of the Corporations Act (2001), STC discloses this information.

The Minister for Finance, Services and Property is responsible for the prudential oversight of

STC, while the NSW Treasurer is responsible for matters relating to STC’s financial

management of its liabilities.

5. Formulating Investment Strategy

5.1. Investment Beliefs and Guiding Principles

STC has established a set of investment beliefs and guiding principles to provide a basis for consistent decision making. Details of these are attached in Appendix 2.

5.2. Investment Options Structures

The assets in the Pooled Fund are notionally allocated into three asset pools to reflect the benefits provided by the STC schemes; defined benefit (DB), defined contributions (DC) and universities reserves (universities).

Investment Policy Statement

6

STC has appointed a Master Investment Manager to be responsible for managing the investments with respect to the DB asset pool. STC directly manages the underlying Investment Manager responsible for the DC and Universities asset pools.

The assets supporting these asset pools are split into the following seven investment options:

Trustee Selection (Defined Benefits – Growth);

Defined Contributions – Growth;

Defined Contributions – Balanced;

Defined Contributions – Diversified;

Defined Contributions – Cash;

University – Diversified; and

University – Cash.

Each of the investment options has been constructed through the development of:

(a) investment objectives (return and risk) for each investment option;

(b) an asset allocation designed to have a high probability of meeting the investment objective for each investment option, which includes target allocations for each asset class and ranges around those target allocations;

(c) a range of investment managers within each asset class to ensure appropriate diversification. In addition each asset class is diversified across, countries, sectors, assets and in the case of unlisted assets across vintages;

(d) a list of permissible investments for each investment manager ; and

(e) investment restrictions applying to each investment manager , including counterparty exposure limits and the use of derivatives.

5.3. Investment Strategy

The Board is responsible for the formulation, oversight and review of the investment strategies for each investment option within the Pooled Fund.

The formulation of investment strategies for each investment option is multi-layered and involves:

the establishment of investment objective;

incorporation of liquidity and cash flow requirements;

strategic asset allocation (SAA), dynamic asset allocation (DAA) tilts around the SAA and tilts around the DAA;

asset class configuration;

consideration of the reliability of valuation information;

consideration of tax consequences related to the investments;

the use of derivatives; and

consideration of costs (including investment management fees).

5.3.1. Investment Objectives

STC’s primary investment objective is to achieve target rate of returns within acceptable risk

Investment Policy Statement

7

parameters and to support the NSW Government meet its funding goal.

In respect of the accumulation components of the relevant STC schemes, STC’s objective is to provide members a range of investment options that broadly cover the risk-return spectrum. This provides members with flexibility to select an investment option that best suits their financial circumstances and risk appetites.

Each investment option has an investment objective which includes a return objective and a risk objective. The return objective is described as achieving a return in excess of inflation (measured by the Consumer Price Index (CPI)), with a relatively high probability over a stated investment time horizon. The risk objective is described in terms of the estimated number of negative annual returns in a 20 year period.

Refer to Appendix 3 for the investment objectives and asset allocations of the respective investment option.

5.3.2. Liquidity and cash flow requirements

STC has a Liquidity Policy designed to ensure that each investment option within the Pooled Fund is able at all times to meet its liabilities when they fall due. The policy sets minimum liquidity levels to be met.

The STC Investment Control team is responsible for monitoring liquidity levels.

If minimum liquidity levels are breached, the investment option is promptly restored to within the stated policy limits. A breach of minimum liquidity levels is reported by the Investment Control team to the STC Executive and the Audit, Risk and Compliance Manager. The breach is also report to the Investment Committee (IC), Risk, Audit and Compliance Committee (RACC) and Board as appropriate.

5.3.3. Asset Allocation Target and Ranges

STC sets asset allocation targets and ranges for each investment option. STC manages its asset allocation across different time horizons as follows:

(a) Strategic asset allocation (SAA), where the long-term asset allocation targets and ranges are determined, within which each diversified investment option operates to achieve its objectives.

(b) Dynamic asset allocation (DAA), are active tilts away from the SAA, for example, in response to changes in specific market factors and/or conditions that change STC’s investment views. DAA is applied to all investment options with the exception of the two investment options which solely invest in cash.

(c) Tilts around the DAAs are used to take advantage of, or to protect the investment options, against short term market movements.

5.3.3.1. Annual Strategic Asset Allocation Review

STC conducts a comprehensive review of the investment strategy for each investment option annually.

The STC Asset and Liability team manages this extensive annual review of the SAA. The review consists of two parts; a report on the investment environment and the SAA review.

The report on the economic environment focuses on the investment risks and opportunities on a medium to long term perspective. It takes into account, fundamental factors and a range of valuation measures. In preparing the report, input is sourced from STC’s Master Investment Manager and STC’s Asset Consultant. This report informs the review and development of the SAA.

The SAA review component of the report takes into consideration, amongst other things,

Investment Policy Statement

8

the following:

the existing position of the investment option relative to the objectives;

review of each investment option, including any recommendations to vary the investment objectives;

estimated net cash-flows, which includes the NSW Government’s funding plan and the liquidity requirements within each investment option;

asset pool optimisations using both the Asset Consultant’s long term and short term capital market assumptions. The results are assessed relative to the identified risks and opportunities identified in the economic environment portion of the report;

review of the investment ranges around the SAA for each investment option, which are used for DAA and tilting purposes;

the sources of risk and return that are likely to contribute to the stated investment objectives. The risk and return characteristics are translated into a set of investment parameters with respect to asset classes and SAA ranges, which guide the configuration of each asset;

determination of the risk and overlay budgets for the year ahead taking into consideration the various investment risk exposures; and

stress testing the SAA using both historical events and the forward looking scenarios identified in the economic environment portion of the report.

The SAA review is presented to the Investment Committee for endorsement and the Board for approval.

The Master Investment Manager is notified of any changes arising from the SAA review to be subsequently implemented within the respective investment option with respect to the DB asset pool.

The Asset and Liability team implement any changes arising from the SAA review with respect to the investment options in the DC and Universities asset pools.

5.3.3.2. Quarterly Asset Allocation Review – (QAAR)

STC undertakes a quarterly asset allocation review (QAAR). The review considers the investment environment, the actual allocations for each investment option relative to the SAA for that investment option and allowable ranges.

Should the QAAR identify any changes to the parameters underpinning the SAA, warranting a DAA tilt, these changes are considered and approved by the IC within the SAA ranges approved at the prior annual SAA review.

The Master Investment Manager is notified of any changes arising from the QAAR to be subsequently implemented within the respective investment options.

The Asset and Liability team implement any changes from the QAAR with respect to the investment options in the DC and Universities asset pools.

5.3.3.3. Weekly Review

The Master Investment Manager and the Asset and Liability team review the actual investment option positions relative to the appropriate SAA and DAA targets on a weekly basis. Both parties are able to implement tilts around the DAA within the allowable ranges for Australian and international equities, Australian and international fixed income, listed property, and listed infrastructure with the aim of capturing opportunities and reducing downside risk.

Investment Policy Statement

9

5.3.3.4. Ad-hoc Review

Whilst a thorough review of the asset allocation is undertaken annually and are reviewed on a quarterly basis, the asset allocation ranges may also be considered outside of the review process in the event there are significant changes to the economic landscape or the investment market.

5.3.4. Asset Class Structures and Sector Configurations

The asset classes in which the investment options of the Pooled Fund invest, fall into three broad asset categories:

liquid growth assets;

alternative assets (infrastructure and direct property); and

liquid defensive assets.

An SSA target and a DAA range is applied to each asset category.

5.3.4.1. Liquid Growth Assets

STC expects assets in the liquid growth category to make a large contribution to long term returns of each diversified investment option, but returns are likely to be volatile.

An example of a liquid growth asset is listed equities. STC invests in both Australian listed equities and international listed equities.

5.3.4.2. Alternative Assets

Alternative assets, such as infrastructure and direct property, serve a dual purpose. Some of the asset classes are expected to generate returns in line with or higher than STC’s stated investment objective for the investment options, whilst other strategies within this category are expected to provide growth but with the ability to also provide downside protection when markets are turbulent.

5.3.4.3. Liquid Defensive Assets

Liquid defensive assets such as, sovereign bonds and cash, represent asset classes that tend to do well when markets are turbulent. These asset classes provide capital protection when most other strategies are not performing well, but they are not expected to generate returns in excess of the stated investment objective for the investment options over the long term.

5.3.5. Valuations

Accurate and timely asset valuations are important to ensure equity is maintained across continuing and exiting members. As such, STC considers the availability and reliability of valuation information an important aspect of setting and reviewing investment strategies.

STC maintains a separate Asset Valuation Policy to ensure the methodologies and assumptions for the valuations of assets held in the investment options are reasonable to address any potential adverse impacts between members as a result of valuation practices.

STC is responsible for determining the frequency at which assets are valued and is committed to regular (at least annual) independent valuations of the assets.

5.3.6. Use of Derivatives

Investment Policy Statement

10

Derivatives, such as futures, forwards, swaps, options and options on futures, are financial assets or liabilities whose value depends on, or is derived from, other assets, liabilities or indices.

Derivatives play a major role in STC’s investment strategy and are consistent with STC’s overall objectives of the investment strategy. The detail on the use of derivatives to hedge existing positions including currency exposures, improve implementation efficiency and to manage asset allocation, and the related controls is contained in STC’s Derivative Risk Statement and STC’s Large Exposure and Counterparty Policy.

5.3.7. Costs and Fees

When considering a potential investment, STC examines the fees and costs associated with buying, holding and realizing the investment. These costs and fees are reflected in the Management Expense Ratio (MER) calculations and/or ducted from investment returns as appropriate.

5.3.8. Taxation

STC retains the responsibility for the overall tax strategy. As such, STC considers the impacts of taxation as an important factor when developing investment strategies.

6. Implementing Investment Strategy

6.1. Investment Manager Selection

Under the SA Act, STC is not permitted to undertake superannuation investment management services and instead it is required to appoint external underlying Investment Managers. For these purposes, an underlying Investment Manager may be an investment manager appointed under an agreement of the trustee or investment manager of a unit trust in which STC invests.

The Master Investment Manager, together with the STC Asset and Liability team, identify and examine suitable underlying Investment Managers.

STC’s Master Investment Manager undertakes the due diligence process for the proposed underlying Investment Manager for the DB asset pool, whilst the Asset and Liability team undertakes the due diligence process for proposed underlying Investment Managers for the DC and Universities asset pools. The due diligence process addresses regulatory requirements including assessing the management of market and investment risk factors, as well as, operational risk exposures.

The outcomes of the due diligence process for the DB asset pool are documented in a recommendation report produced by the Master Investment Manager in conjunction with the STC Asset and Liability team.

The STC Asset and Liability team will also produce a recommendation report documenting the outcomes from the due diligence process for the DC and Universities asset pools.

Recommendation reports are submitted to the CEO for approval prior to seeking consent from the Minister as required by the SA Act.

Once the Minister has granted consent, the underlying Investment Manager is then engaged under an Investment Management Agreement (IMA), or letter of agreement that contains a scope or mandate delineating the authorised investments, investment constraints such as counterparty exposure limits, hedging, use of derivatives etc. as well as investment objectives and performance benchmarks, performance reporting requirements and risk management standards that are required.

Investment Policy Statement

11

The underlying Investment Manager receives a fee for its role. The fee may include a base fee and a performance based fee to incentivise performance above the benchmark.

6.2. Direct Investments

STC looks to use its scale to access opportunities to invest directly into assets. Typically these direct investments are in infrastructure and/or direct property.

As with underlying Investment Managers, the Master Investment Manager, together with the STC Asset and Liability team, identify and examine suitable direct investments.

STC’s Master Investment Manager undertakes the due diligence process for the proposed infrastructure and/or direct property investments with respect to DB asset pool, whilst the STC Asset and Liability team undertake the due diligence with respect to the DC and Universities asset pools.

The outcomes of the due diligence with respect to the DB asset pool are documented in a recommendation report produced by the Master Investment Manager in conjunction with the STC Asset and Liability team.

The STC Asset and Liability team will also produce a recommendation report documenting the outcomes from the due diligence process for the DC and Universities asset pools.

The recommendation reports are submitted to the IC for approval.

6.3. Rebalancing Program

STC has a formal rebalancing program in place which is implemented by an underlying Investment Manager. The rebalancing program aims to execute asset allocation changes of listed asset classes (i.e. equities and fixed income) in an efficient and cost effective manner. The STC Asset and Liability team uses the QAAR process to determine the mid-point around which the rebalancing program will be undertaken.

If the QAAR determines a change to the SAA or DAA for listed asset classes is required, the underlying Investment Manager is instructed to change the relevant mid-points identified during the review.

For the Trustee Selection and DC Growth investment options, if any asset class is outside the relevant rebalancing ranges, the underlying Investment Manager has authority to buy or sell futures to bring the asset classes back to within the range or 1 percentage point deviation from the limit. This trade is funded by a matching trade to either sell or buy another asset class.

The DC Balanced and DC Conservative investment options are rebalanced back to their respective SAAs or, if applicable, DAAs at the end of each month. The DC Growth investment option is the liquidity provider for these trades.

The rebalancing program does not apply to unlisted asset classes (i.e. infrastructure and property) as they are typically only valued annually. The SAA is adjusted in respect of these unlisted asset classes on an annual basis.

6.4. Performance Based Fees

The principle return objective for each investment option is to produce a return above an inflation target, net of all investment fees and taxes.

STC understands that underlying investment managers should be properly rewarded for the services they provide and that active management fees are justified where there is a high probability of net outperformance over time. However, STC acknowledges that it is not in the members’ interests to overpay for a service. Therefore, the due diligence process performed by the Master Investment Manager explicitly considers the fee structure so that, wherever

Investment Policy Statement

12

possible, reward structures are aligned with the interests of members. Fee structures are also reviewed on an ongoing basis as part of the annual review.

6.5. Environmental, Social and Governance (ESG)

STC believes Environmental, Social and Governance (ESG) issues are material investment matters and as such should be incorporated into investment processes.

STC expects the approach of incorporating ESG issue in the investment processes will lead to better risk adjusted return to members. STC also believes organisations managing the risks and opportunities arising from ESG issues effectively are likely to be more successful than those that do not over the longer-term.

Further details of how STC implements ESG principles into its investment strategy are outlined in the ESG Policy.

7. Investment Risk Management

7.1. Risk Management

STC has a strong risk focus and maintains a number of specific policies for managing key investment risks, such as, but not limited to:

Liquidity Policy;

Large Exposure and Counterparty Policy;

Asset Valuation Policy;

Derivative Risk Statement; and

Risk Management Framework.

The asset allocation of an investment option is the primary determinant of its risk characteristics and, therefore, STC focuses most of its risk management resources on managing the asset allocation decisions. This includes adequate diversification across and within asset classes, adequate stress testing of investment options, appropriate asset allocation ranges and rebalancing processes.

As part of STC’s due diligence process undertaken by the Master Investment Managers, a formal risk assessment must be undertaken which includes:

(a) identification of risk factors;

(b) assessment and measurement of the identified risk factors, including the potential impact on the sources of investment return;

(c) the risk mitigation strategies in place; and

(d) how the identified risks would be monitored and reported.

7.2. Downside Protection

Given the rapidly changing profile of STC scheme members, with a greater proportion of members retiring and/or moving to a pension phase of their benefit, downside protection is an important aspect of investment risk management.

Downside protection strategies aim to reduce the frequency and/or magnitude of capital losses, resulting from significant investment market declines. Downside protection strategies involve adjusting an investment options’ market exposure to limit the impact of potential

Investment Policy Statement

13

losses from market downturns. These strategies can be applied to different types of asset market exposures, but are most commonly focused on equity. These strategies are implemented by STC’s Master Investment Managers for DB and DC assets respectively.

7.3. Stress Testing

STC has a comprehensive stress testing program in place. On an annual basis, the STC Asset and Liability team, together with its third party service provider and, where necessary Asset Consultant, undertake a series of stress tests for each of the investment options that cover a range of factors that can create extraordinary losses to make control of risk difficult.

The results of the stress testing are evaluated to determine whether a change to the investment strategies and/or risk mitigation strategies is required. The results of the stress test and any recommendations are presented to the IC and the Board for review and approval.

STC’s stress-testing program consists of three types of tests:

Historical event tests;

Forward looking scenario tests; and

Forward looking factor tests

7.4. Risk Monitoring

Every quarter the IC assesses the performance of the investment options through a Risk Report.

The Risk Report encompasses an analysis of the risk factors and diversification embedded in the relevant asset allocations and benchmarks.

The report provides STC with detail regarding the type and magnitude of risk exposures.

8. Monitoring and Reporting

8.1. Investment Strategy Monitoring

The STC Asset and Liability team and IC reviews the investment performance of investment options and each underlying Investment Manager each month via reporting provided by the Master Investment Manager and STC’s Custodian. Summary investment performance data is also provided to the Board.

Investment returns can differ from the crediting rate attributed to an investment option due to tax and other adjustments.

The principal goals of investment performance monitoring is to:

asses the extent to which the investment objectives are being achieved;

ascertain the existence of any particular weakness in an underlying Investment Manager; and

assess the ability of the underlying Investment Managers to successfully meet the investment objectives.

STC will also asses the Master Investment Manager’s performance in managing underlying Investment Managers, by comparing the investment performance of the underlying Investment Managers against the performance of relevant market indices.

Returns of the investment options will be monitored in relation to relevant investment objectives. The appropriateness of these investment options will be assessed at least

Investment Policy Statement

14

quarterly and kept under regular review to reflect any fundamental changes in the investment environment.

Each underlying Investment Manager’s performance will be monitored regularly with a view to an annual evaluation of rolling 3 and 5 year results. If an underlying Investment Manager fails to meet the objectives set, its role will be reviewed by IC in conjunction with the STC’s Master Investment Manager and/or its Asset Consultant.

Whilst a thorough review of the asset allocation is undertaken annually and are reviewed on a quarterly basis, the asset allocation ranges may also be considered outside of the review process in the event there are significant changes to the economic landscape or the investment market.

8.2. Reporting Framework

STC receives a variety of daily, weekly, monthly, quarterly and annual reports from, amongst others, its Master Investment Managers, the underlying Investment Managers, Custodian, Administrator and Asset Consultant. The STC Asset and Liability team is primarily responsible for receiving and monitoring this information and producing summary reports to be presented to the IC and the Board as required.

9. Review

The Investment Policy Statement and the arrangements contained in the policy will be reviewed annually. The STC Asset and Liability team will initiate the annual review. These review outcomes will be reported to the IC for review and recommendation to the Board for approval.

Investment Policy Statement

15

10. Definitions The following terms have the following meanings:

(a) “SAA” - is where the long-term asset allocation target and ranges have been

determined, within which the Fund operates to achieve its investment objectives. The strategic asset allocation target and ranges remain static; i.e. asset allocations are not expected to change frequently;

(b) “DAA” - is an investment approach that permits asset allocation targets to be changed during the investment period. This would typically be in response to changes in specific market factors and/or conditions that change the STC’s investment views in the short and medium term; and

(c) “STC” – means the SAS Trustee Corporation as defined in the SA Act.

Investment Policy Statement

16

Appendix 1 - Investment strategy & implementation regulatory framework Section 58 of the SA Act requires STC to determine and give effect to an investment strategy for the Schemes. The investment strategy must have regard to the circumstances of the Schemes, including:

(a) the risk involved in making, holding and realising, and the likely return from, the investments having regard to the Schemes’ objectives and their cash flow requirements;

(b) the composition of the investments as a whole, including the extent to which the

investments are diverse or involve exposure to risks from inadequate diversification; (c) the liquidity of the investments having regard to the Schemes’ cash flow requirements; (d) the ability to discharge the existing and prospective liabilities under the Schemes; (e) any other matter which a trustee is required to consider in determining an investment

strategy under the Superannuation Industry (Supervision) Act 1993 (Cth) (SIS Act). Section 14C of the Trustee Act 1925 (NSW) provides that a trustee may also take into account the following matters when exercising a power of investment:

(a) the purposes of the trust and the needs and circumstances of the beneficiaries; (b) the desirability of diversifying trust investments; (c) the nature of, and the risk associated with, existing trust investments and other trust

property; (d) the need to maintain the real value of the capital or income of the trust; (e) the risk of capital or income loss or depreciation; (f) the potential for capital appreciation; (g) the likely income return and the timing of income return; (h) the length of the term of the proposed investment; (i) the probable duration of the trust; (j) the liquidity and marketability of the proposed investment during, and on the

determination of, the term of the proposed investment; (k) the aggregate value of the trust estate; (l) the effect of the proposed investment in relation to the tax liability of the trust; (m) the likelihood of inflation affecting the value of the proposed investment or other trust

property; (n) the costs (including commissions, fees, charges and duties payable) of making the

proposed investment; and (o) the results of the latest review of existing trust investments.

Investment Policy Statement

17

Additionally, section 52(6) of the SIS Act requires trustees of superannuation funds to formulate, review regularly and give effect to an investment strategy for the whole of the fund, and for each investment option offered by the trustee in the fund, having regard to: (a) the risk involved in making, holding and realising, and the likely return from, the

investments covered by the strategy, having regard to the trustee's objectives in relation to the strategy and to the expected cash flow requirements in relation to the fund;

(b) the composition of the investments covered by the strategy, including the extent to

which the investments are diverse or involve the fund in being exposed to risks from inadequate diversification;

(d) the liquidity of the investments covered by the strategy, having regard to the expected

cash flow requirements in relation to the fund; (e) whether reliable valuation information is available in relation to the investments covered

by the strategy; (f) the ability of the fund to discharge its existing and prospective liabilities; (g) the expected tax consequences for the fund in relation to the investments covered by

the strategy; (h) the costs that might be incurred by the fund in relation to the investments covered by

the strategy; and (i) any other relevant matters.

Investment Policy Statement

18

Appendix 2 – Investment Beliefs Defined Benefit

Investment Belief Guiding Principles

Objectives

The Trustee believes: Investment objectives require a the target rate of return to be established by setting it at CPI + X % p.a., measured over rolling X year periods, as amended from time to time.

Evaluating the Trustee’s expectations of meeting the stated return target each year is important to setting the investment objectives.

Investment performance should not be measured relative to other superannuation funds (especially defined contribution funds) because they have different objectives to the STC schemes.

Evaluating the historical rate of return of the fund can provide useful analysis, measured after taking into account appropriate tax adjustments and franking credits on a time weighted basis.

Risk is multi-dimensional, with the main investment risk being the probability of not achieving the target rate of return over the long term. Short term risk (ie the likelihood of losing capital) is also important to achieving STC’s investment objectives

Having regard to other measures of risk, including the likelihood of a negative annual return, is necessary to successfully manage risk. In this respect: The investment strategy should have an expected probability of no more than a 4 years in 20 chance of a negative return. Other measures of risk include the magnitude of negative annual returns, and returns relative to an agreed comparator.

Negative returns in the near term have a disproportionately large impact on the Fund’s ability to achieve full funding as a result of the Fund being in a negative net cash flow position.

As long as the Fund’s long term objectives are expected to be met, the Fund will be biased towards the protection of capital, even if this means giving up potentially higher returns

Governance

The Trustee believes: High quality governance of the investment process is critical to our success.

The Trustee aims to have an appropriate balance of responsibilities and accountabilities between the Board, the Investment Committee, the internal investment team and external agents. The Trustee ensures that resources are directed towards those areas with the greatest expected contribution to the achievement of our investment objectives. The Trustee aims to have open, clear lines of communication with the key decision makers in the NSW Government as a key stakeholder of the Fund.

Investing only in opportunities that the Trustee understands and where there is an appropriate alignment of interests between the Fund and the external agents.

The internal team is appropriately staffed so that it can exert a suitable level of oversight and influence on the external agents used and also as appropriate for the investment strategy adopted by the Fund.

Investment Policy Statement

19

Investment Belief Guiding Principles

Speed of execution is necessary for comparative advantage.

To ensure comparative advantage, the Trustee aims to have the appropriate resources and processes in place to efficiently and timeously implement our investment decisions.

Investment Strategy

The Trustee believes: Asset allocation decisions have the greatest impact on investment outcomes.

Making asset allocation decisions to exploit a diverse range of risk premia on a systematic basis is a key determinant to generate rewards.

Investment markets offer long term rewards for placing capital at risk (“risk premia”). The Trustee understands that the size of risk premia will vary over time, providing opportunities to enhance return and reduce risk by deviating from a neutral position.

Deviating from the neutral allocation to reflect current market pricing and risk levels is necessary. Variations from the neutral allocation will occur to avoid capital loss rather than to pursue outsized returns. Diversification amongst risk premia, asset classes, investment managers and individual securities is expected to enhance the reward earned for each unit of risk taken, but will not provide protection against all economic scenarios. The equity risk premium will be the primary driver of returns above the risk-free rate, but other risk premia are to be exploited, especially those which are expected to have low correlations with the equity risk premium.

Successful investing requires consideration of both quantitative and qualitative factors.

Using both quantitative and qualitative analysis when setting investment strategy and managing risk is required.

Improving environmental, sustainability and governance (ESG) of the portfolio assets will improve the long term performance of the funds.

Achieving long term performance requires the investment strategy to consider ESG diligently.

Active Management

The Trustee believes: Active management assists in achieving higher returns (e.g. above that available from investing in a passively managed fund) and as a source of downside protection (e.g. where the manager has the freedom to make active asset allocation decisions).

Active management will only be used in those asset classes or strategies where it is considered likely that it will add value, after allowing for fees and tax and where there is a high degree of conviction in the manager’s skill.

Investment outcomes should be evaluated net of fees, taxes and any other investment charges or implementation effects.

Where the Trustee invests passively, careful consideration is given to the benchmark used, and where appropriate, use benchmarks other than market cap

Investment Policy Statement

20

Investment Belief Guiding Principles

weighted benchmarks.

Liquidity

The Trustee believes: There is an expected return premium for investing in illiquid assets.

Allocation to illiquid assets should be balanced with the Trustee’s ability to meet expected net cash flows in all reasonably likely scenarios.

The Fund’s cash flow position is a necessary consideration when determining how much liquidity risk to take.

The Fund’s negative cash flow position means the Trustee aims to hold at least two years’ of projected benefit payments in liquid assets (i.e. assets that can reasonably be expected to be sold under normal market conditions within 180 days).

Investment Policy Statement

21

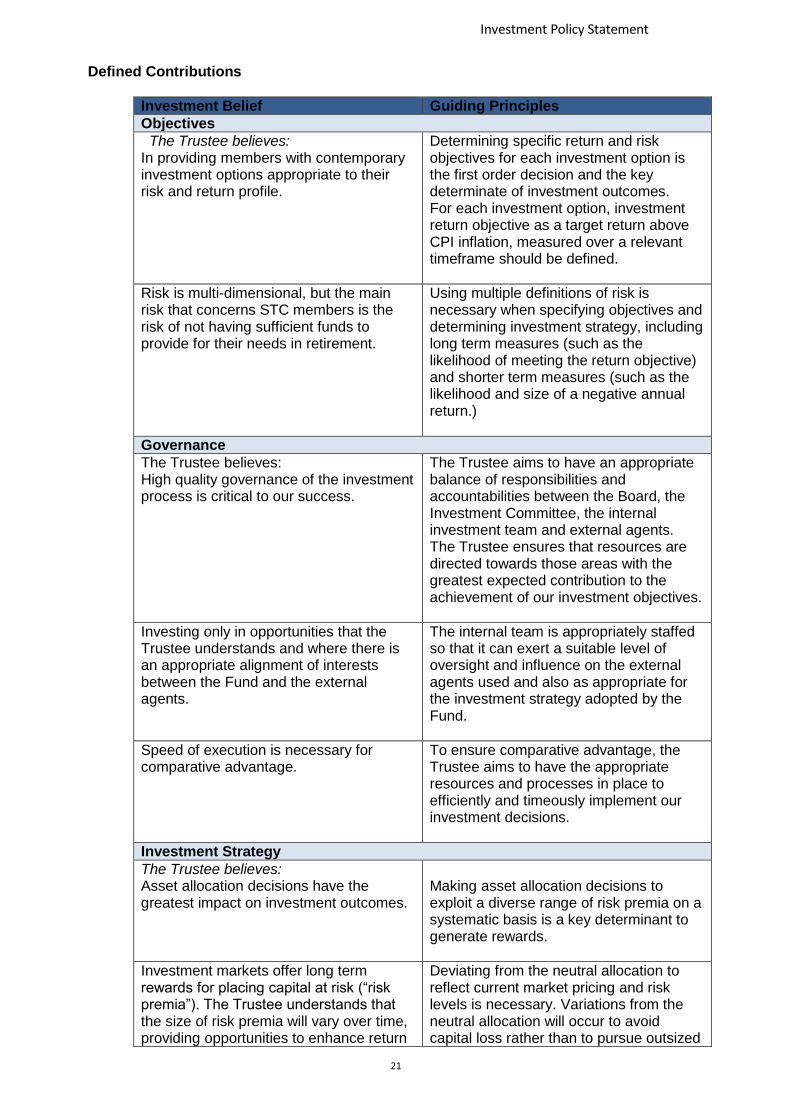

Defined Contributions

Investment Belief Guiding Principles

Objectives

The Trustee believes: In providing members with contemporary investment options appropriate to their risk and return profile.

Determining specific return and risk objectives for each investment option is the first order decision and the key determinate of investment outcomes. For each investment option, investment return objective as a target return above CPI inflation, measured over a relevant timeframe should be defined.

Risk is multi-dimensional, but the main risk that concerns STC members is the risk of not having sufficient funds to provide for their needs in retirement.

Using multiple definitions of risk is necessary when specifying objectives and determining investment strategy, including long term measures (such as the likelihood of meeting the return objective) and shorter term measures (such as the likelihood and size of a negative annual return.)

Governance

The Trustee believes: High quality governance of the investment process is critical to our success.

The Trustee aims to have an appropriate balance of responsibilities and accountabilities between the Board, the Investment Committee, the internal investment team and external agents. The Trustee ensures that resources are directed towards those areas with the greatest expected contribution to the achievement of our investment objectives.

Investing only in opportunities that the Trustee understands and where there is an appropriate alignment of interests between the Fund and the external agents.

The internal team is appropriately staffed so that it can exert a suitable level of oversight and influence on the external agents used and also as appropriate for the investment strategy adopted by the Fund.

Speed of execution is necessary for comparative advantage.

To ensure comparative advantage, the Trustee aims to have the appropriate resources and processes in place to efficiently and timeously implement our investment decisions.

Investment Strategy

The Trustee believes: Asset allocation decisions have the greatest impact on investment outcomes.

Making asset allocation decisions to exploit a diverse range of risk premia on a systematic basis is a key determinant to generate rewards.

Investment markets offer long term rewards for placing capital at risk (“risk premia”). The Trustee understands that the size of risk premia will vary over time, providing opportunities to enhance return

Deviating from the neutral allocation to reflect current market pricing and risk levels is necessary. Variations from the neutral allocation will occur to avoid capital loss rather than to pursue outsized

Investment Policy Statement

22

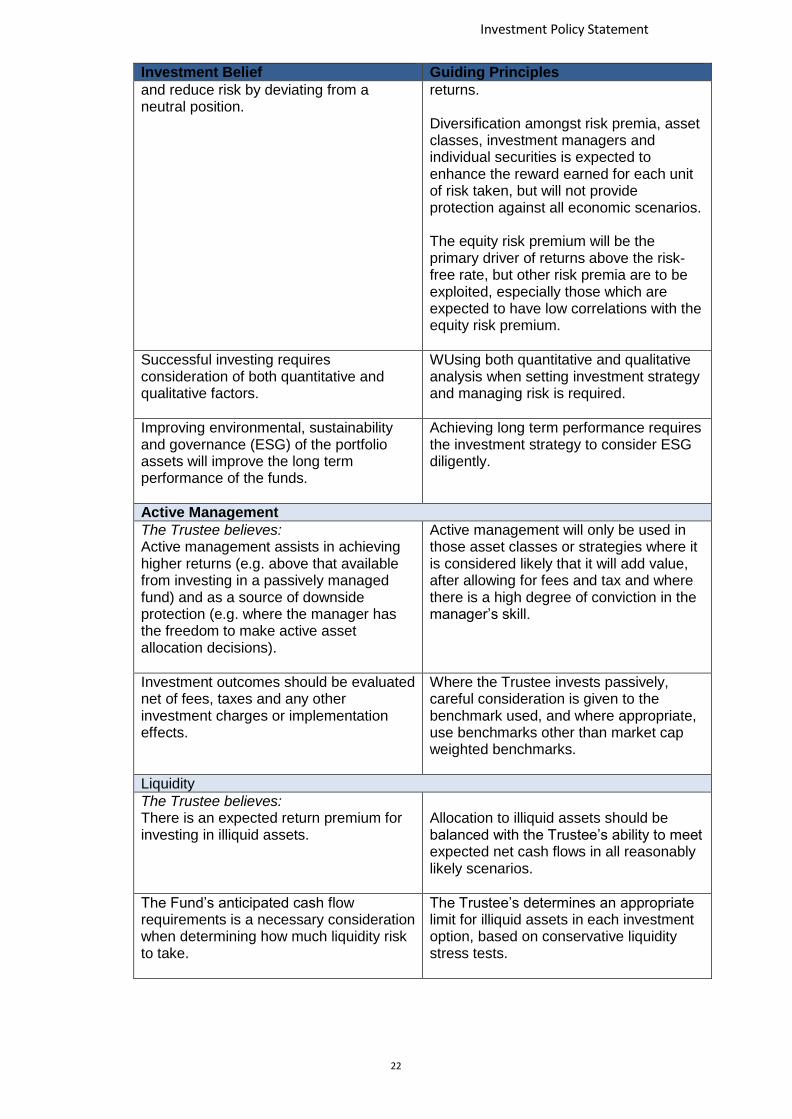

Investment Belief Guiding Principles

and reduce risk by deviating from a neutral position.

returns. Diversification amongst risk premia, asset classes, investment managers and individual securities is expected to enhance the reward earned for each unit of risk taken, but will not provide protection against all economic scenarios. The equity risk premium will be the primary driver of returns above the risk-free rate, but other risk premia are to be exploited, especially those which are expected to have low correlations with the equity risk premium.

Successful investing requires consideration of both quantitative and qualitative factors.

WUsing both quantitative and qualitative analysis when setting investment strategy and managing risk is required.

Improving environmental, sustainability and governance (ESG) of the portfolio assets will improve the long term performance of the funds.

Achieving long term performance requires the investment strategy to consider ESG diligently.

Active Management

The Trustee believes: Active management assists in achieving higher returns (e.g. above that available from investing in a passively managed fund) and as a source of downside protection (e.g. where the manager has the freedom to make active asset allocation decisions).

Active management will only be used in those asset classes or strategies where it is considered likely that it will add value, after allowing for fees and tax and where there is a high degree of conviction in the manager’s skill.

Investment outcomes should be evaluated net of fees, taxes and any other investment charges or implementation effects.

Where the Trustee invests passively, careful consideration is given to the benchmark used, and where appropriate, use benchmarks other than market cap weighted benchmarks.

Liquidity

The Trustee believes: There is an expected return premium for investing in illiquid assets.

Allocation to illiquid assets should be balanced with the Trustee’s ability to meet expected net cash flows in all reasonably likely scenarios.

The Fund’s anticipated cash flow requirements is a necessary consideration when determining how much liquidity risk to take.

The Trustee’s determines an appropriate limit for illiquid assets in each investment option, based on conservative liquidity stress tests.

Investment Policy Statement

23

Appendix 3 – Investment Objectives

Trustee Selection (Defined Benefit) Strategic asset allocation: 54.0% liquid growth; 31.5% alternatives; 14.5% liquid defensive. Investment objective: To maximise the earnings rate subject to a greater than 50% probability of exceeding CPI+4.5% p.a. over rolling 10 year periods. Risk Objective: From 3 to less than 4 negative annual returns estimated over any 20 year period.

Strategic asset allocation At 01/02/15

Dynamic asset allocation range

Liquid growth 54.0% 38.0% - 70.0%

Australian Equities 27.0%

International Equities 27.0%

Alternatives 31.5% 23.5% - 39.5%

Property 9.0%

Alternatives - Other 12.5%

Infrastructure 10.0%

Liquid defensive 14.5% 10.5% - 29.5%

Australian Fixed Interest 5.0%

International Fixed Interest 2.0%

Cash 7.5%

Total 100.0%

Investment Policy Statement

24

Defined Contributions – Growth Strategic asset allocation: 54.0% liquid growth; 31.0% alternatives; 15.0% liquid defensive. Investment objective: To maximise the earnings rate subject to a greater than 50% probability of exceeding CPI+4.5% p.a. over rolling 10 year periods. Risk Objective: From 3 to less than 4 negative annual returns estimated over any 20 year period.

Strategic asset allocation At 01/02/15

Dynamic asset allocation range

Liquid growth 54.0% 38.0% - 70.0%

Australian Equities 27.0%

International Equities 27.0%

Alternatives 31.0% 23.0% - 39.0%

Property 7.5%

Alternatives - Other 13.0%

Infrastructure 10.5%

Liquid defensive 15.0% 10.5% - 30.0%

Australian Fixed Interest 5.5%

International Fixed Interest 2.0%

Cash 7.5%

Total 100.0%

Investment Policy Statement

25

Defined Contributions – Balanced Strategic asset allocation: 38.0% liquid growth; 25.5% alternatives; 36.5% liquid defensive. Investment objective: To maximise the earnings rate subject to a greater than 60% probability of exceeding CPI+3.0% p.a. over rolling 7 year periods. Risk Objective: From 2 to less than 3 negative annual returns estimated over any 20 year period.

Strategic asset allocation At 01/02/15

Dynamic asset allocation range

Liquid growth 38.0% 28.0% - 48.0%

Australian Equities 19.0%

International Equities 19.0%

Alternatives 25.5% 17.5% - 33.5%

Property 8.5%

Alternatives - Other 8.0%

Infrastructure 9.0%

Liquid defensive 36.5% 26.5% - 46.5%

Australian Fixed Interest 13.5%

International Fixed Interest 4.0%

Cash 19.0%

Total 100.0%

Investment Policy Statement

26

Defined Contributions – Conservative Strategic asset allocation: 20.0% liquid growth; 20.0% alternatives; 60.0% liquid defensive. Investment objective: To maximise the earnings rate subject to a greater than 70% probability of exceeding CPI+2.0% p.a. over rolling 4 year periods. Risk Objective: From 0.5 to less than 1 negative annual returns estimated over any 20 year period.

Strategic asset allocation At 01/02/15

Dynamic asset allocation range

Liquid growth 20.0% 12.5% - 27.5%

Australian Equities 10.0%

International Equities 10.0%

Alternatives 20.0% 12.0% - 28.0%

Property 7.5%

Alternatives - Other 6.5%

Infrastructure 6.0%

Liquid defensive 60.0% 50.0% - 70.0%

Australian Fixed Interest 11.5%

International Fixed Interest 4.0%

Cash 44.5%

Total 100.0%

Investment Policy Statement

27

Defined Contributions – Cash Strategic asset allocation: 100% liquid defensive. Investment objective: To maximise the earnings rate subject to a greater than 80% probability of exceeding CPI+0.25% p.a. over rolling 3 year periods. Risk Objective: From less 0.5 negative annual returns estimated over any 20 year period.

Strategic asset allocation At 01/02/15

Liquid growth 0.0%

Alternatives 0.0%

Liquid defensive 100.0%

Australian Fixed Interest 0.0%

International Fixed Interest 0.0%

Cash 100.0%

Total 100.0%

Investment Policy Statement

28

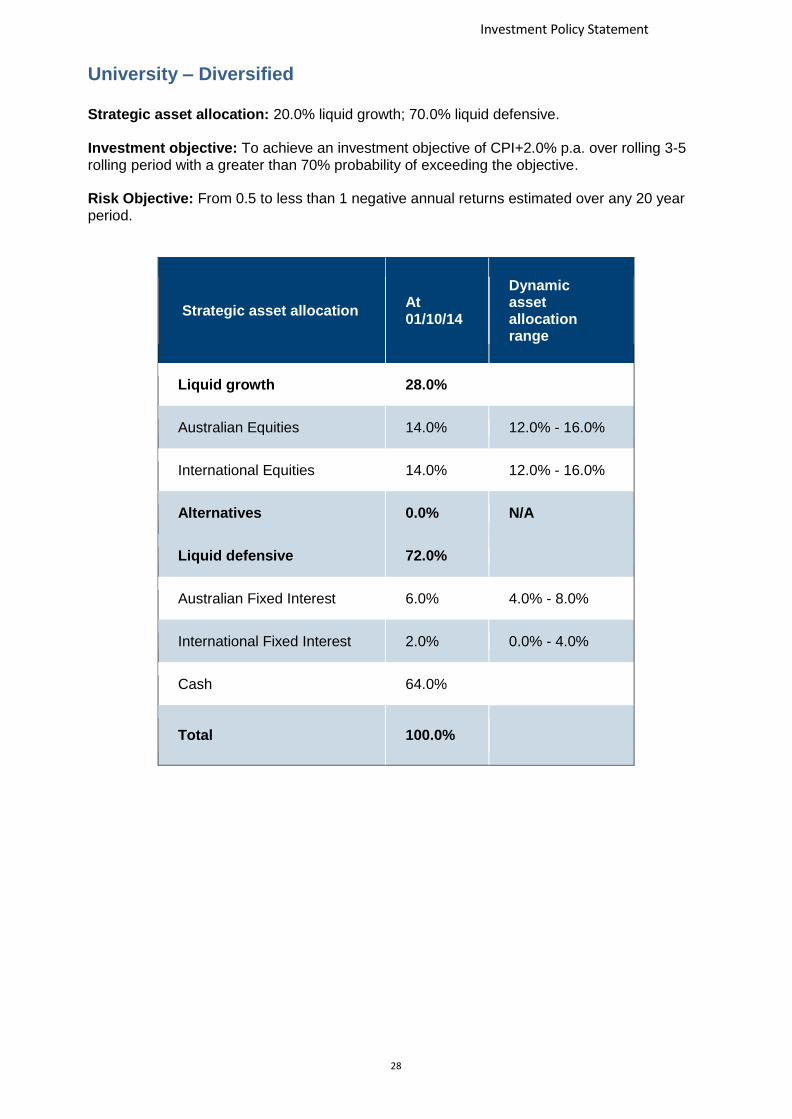

University – Diversified Strategic asset allocation: 20.0% liquid growth; 70.0% liquid defensive. Investment objective: To achieve an investment objective of CPI+2.0% p.a. over rolling 3-5 rolling period with a greater than 70% probability of exceeding the objective. Risk Objective: From 0.5 to less than 1 negative annual returns estimated over any 20 year period.

Strategic asset allocation At 01/10/14

Dynamic asset allocation range

Liquid growth 28.0%

Australian Equities 14.0% 12.0% - 16.0%

International Equities 14.0% 12.0% - 16.0%

Alternatives 0.0% N/A

Liquid defensive 72.0%

Australian Fixed Interest 6.0% 4.0% - 8.0%

International Fixed Interest 2.0% 0.0% - 4.0%

Cash 64.0%

Total 100.0%

Investment Policy Statement

29

University – Cash Strategic asset allocation: 100% liquid defensive. Investment objective: To achieve an investment objective of CPI+0.25% p.a. over rolling 3 year period with a greater than 80% probability of exceeding the objective. Risk Objective: From less 0.5 negative annual returns estimated over any 20 year period.

Strategic asset allocation At 01/10/14

Liquid growth 0.0%

Alternatives 0.0%

Liquid defensive 100.0%

Australian Fixed Interest 0.0%

International Fixed Interest 0.0%

Cash 100.0%

Total 100.0%