investment summit brussels 2014 marc craquelin, chief...

TRANSCRIPT

Investment Summit Brussels 2014

Marc Craquelin, Chief Investment Officer Financière de l'Echiquier

2

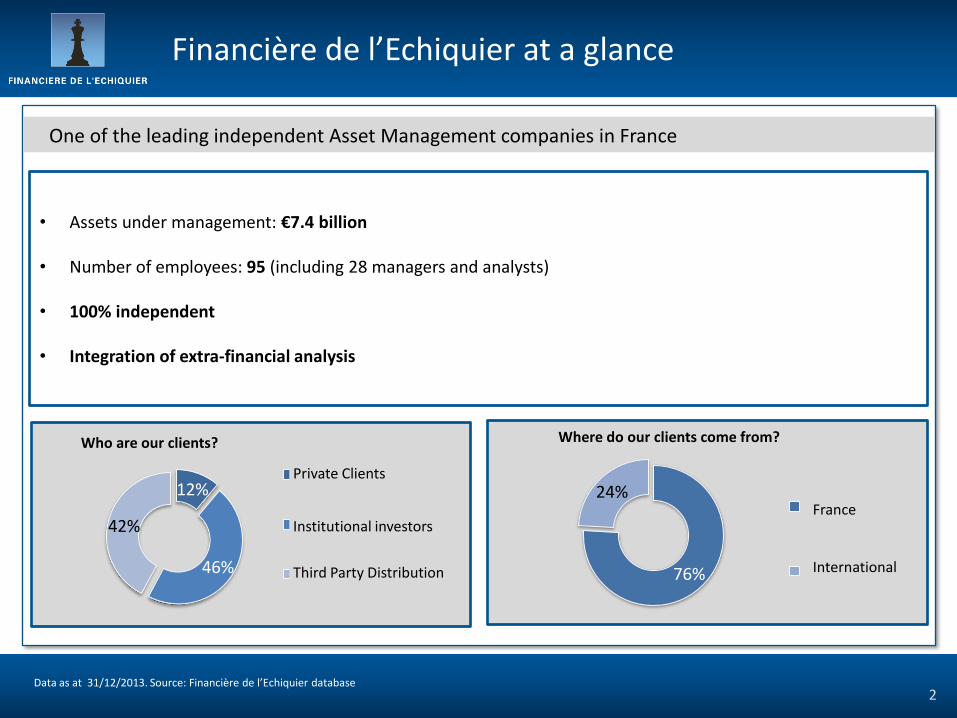

Financière de l’Echiquier at a glance

One of the leading independent Asset Management companies in France

Who are our clients?

12%

46%

42%

Clients privés

Grands comptes etinstitutionnels

Distributeurs 76%

24% France

Hors France

Where do our clients come from?

• Assets under management: €7.4 billion

• Number of employees: 95 (including 28 managers and analysts)

• 100% independent

• Integration of extra-financial analysis

Data as at 31/12/2013. Source: Financière de l’Echiquier database

Private Clients

Institutional investors

Third Party Distribution

France International

Data as at 31/12/2013. Sources: Bloomberg Financière de l’Echiquier database Past performances are not a reliable indicator of future performances and may vary over time. The CAC 40 index is provided as an indication . NR = dividends reinvested 3

2013: performance of core funds

Iboxx Corporate € 3-5 yr

MSCI Eur Small Cap (NR)

Agressor

CAC All Tradable (NR)

Echiquier Major

ARTY

MSCI Europe (NR)

Echiquier Agenor

Echiquier Patrimoine

Echiquier Oblig

Capitalised Eonia

MSCI AC World €(NR)

Composite index (75% Eonia / 25% MSCI Europe NR)

Echiquier Value

+21.8%

+6.4%

+24.3%

+33.4%

+18.6% +19.8%

+39.1%

+6.1%

+0.1%

+2.8%

+8.3%

+5.0%

Echiquier Global

+17.5%

CAC 40 +18.0%

+11.3%

+22.5%

Agressor

Echiquier Value H

Echiquier Agenor

Echiquier Major

Echiquier Oblig ARTY

Echiquier Patrimoine

CAC All Tradable

75% Eonia & 25% MSCI Europe

MSCI Europe Small Cap

MSCI Europe

Daily capitalised EONIA

IBOXX EUR Corp 3-5 Echiquier Japon

Echiquier Amérique

0%

20%

40%

60%

80%

100%

120%

140%

0% 5% 10% 15% 20% 25%

Data in weekly stages as at 28/12/2013. Sources: Morningstar, Financière de l’Echiquier database Performances of the Fund and the benchmark include distributed income (as of the 2013 financial year). However, up to 2012 inclusive, the benchmark’s performance does not include distributed income, except for fixed income products. 4

Funds’ risk/return profile over five years

Performance

Volatility

Diversified and bond funds

Equity funds

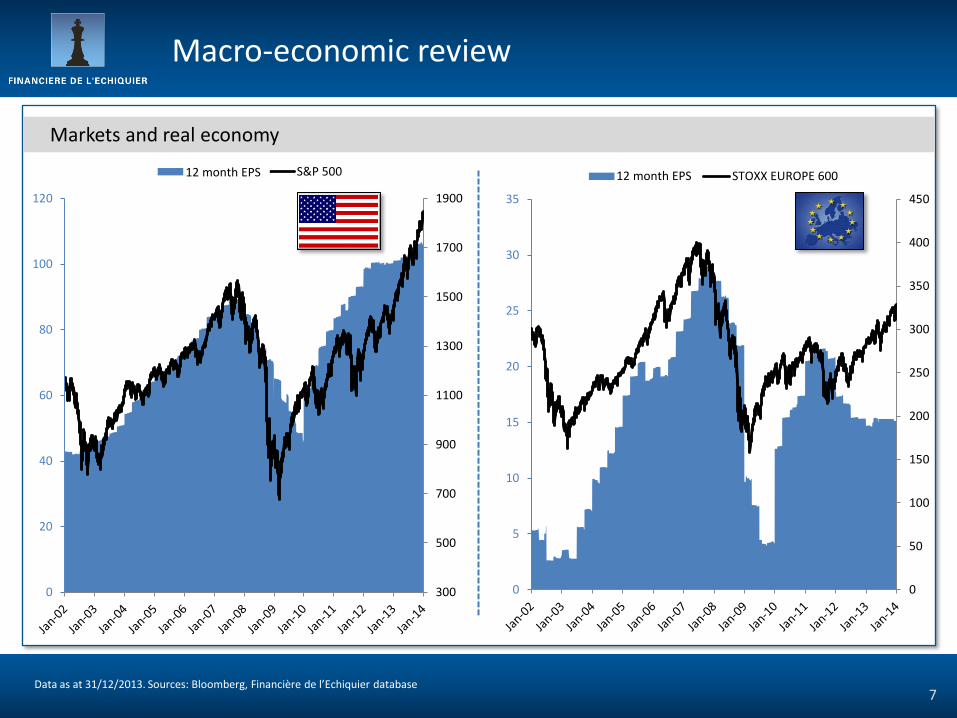

M a c r o - e c o n o m i c r e v i e w

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database Past performances are not a reliable indicator of future performances and may vary over time.

2013: Emerging markets were lagging

Macro-economic review

6

+32.1%

+26.4%

+21.0%

+31.0% +31.5%

+30.3%

-26.8%

-1.0%

-20.3%

-1.9%

MSCI United States +31.8%

MSCI Emerging markets -2.6%

MSCI Europe +25.2%

Performances in USD dividends reinvested

0

50

100

150

200

250

300

350

400

450

0

5

10

15

20

25

30

35

BPA 12 mois STOXX EUROPE 600

7

Macro-economic review

Markets and real economy

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database

300

500

700

900

1100

1300

1500

1700

1900

0

20

40

60

80

100

120

BPA 12 mois S&P 50012 month EPS 12 month EPS

M a c r o - e c o n o m y U n i t e d S t a t e s

30

35

40

45

50

55

60

65

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

PMI manufacturier aux Etats-Unis

58%

60%

62%

64%

66%

68%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Taux de participation des plus de 16 ans aux Etats-Unis

9

Macro-economic figures in the US

Latest data as at 31/12/2013. Sources: US Bureau of Labor Statistics, Bloomberg, Financière de l’Echiquier database

Momentum remains intact

-6,0%

-4,0%

-2,0%

0,0%

2,0%

4,0%

6,0%

Mar-09 Sep-10 Mar-12 Sep-13

Variation annualisée du PIB trimestriel aux Etats-Unis

dec-13

6%

7%

8%

9%

10%

11%

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Taux de chômage aux Etats-Unis

nov-13

Manufacturing PMI in the US Annualised change in quarterly GDP in the US

Unemployment rate in the US Participation rate of over 16 yrs in the US

10

The strength of US companies

Latest data as at 31/12/2013. Sources: Exane Research, Bloomberg, Financière de l’Echiquier database The stocks shown are provided as an example. Neither their presence in the portfolios managed nor their performance are guaranteed .

Keeping things in perspective

Momentum remains intact

5,0%

7,5%

10,0%

12,5%

15,0%

17,5%

20,0%

2003 2005 2007 2009 2011 2013

ROE entreprises américaines ROE entreprises européennes

0

50

100

150

200

250

300

350

400

450Productivité Salaire réel

25

35

45

55

65

-25

-20

-15

-10

-5

0

5

10

15

2000 2002 2004 2006 2008 2010 2012 2014

CAPEX (a/a) ISM Nouvelles commandes

(…)

ISM new orders ROE of European companies ROE of US companies

Productivity Real wages

E m e r g i n g M a r k e t s

12

A less advantageous liquidity environment

Latest data as at 31/12/2013. Sources: Bloomberg, FMI, Datastream, Les Cahiers Verts de l’Economie, Financière de l’Echiquier database

Key macro-economic figures

2013 GDP growth Inflation Gross government

debt (% of GDP) Current balance

(% of GDP) Currency reserves

(% of GDP USD) Central bank interest rates

10-year rate 2013 MSCI

performance (USD)

Turkey 3.8% 8.0% 36.0% -7.4% 13.6% 6.5% 10.2% -28.1%

South Africa 2.0% 5.7% 43.0% -6.1% 11.9% 5.0% 7.9% -8.9%

India 3.8% 9.0% 67.2% -4.4% 15.3% 7.8% 8.8% -5.3%

Indonesia 5.3% 9.5% 26.2% -3.4% 11.5% 7.5% 8.5% -25.0%

Brazil 2.5% 5.9% 68.3% -3.4% 17.1% 10.0% 10.7% -18.7%

Mexico 1.2% 3.3% 44.0% -1.3% 13.3% 3.5% 6.4% -2.0%

Thailand 3.1% 2.0% 47.1% 0.1% 39.7% 2.3% 3.9% -16.9%

China 7.6% 3.0% 22.9% 2.5% 41.0% 6.0% 4.6% +0.4%

Russia 1.5% 6.2% 14.1% 2.9% 22.7% 5.5% 7.9% -2.6%

Malaysia 4.7% 2.0% 57.0% 3.5% 42.2% 3.0% 4.1% +4.2%

Korea 2.8% 1.8% 35.7% 4.6% 28.9% 2.5% 3.6% +3.1%

13

Political reforms headed in the right direction

Source: Financière de l’Echiquier database

Improving social environment Changing demographic

policy Protecting

the environment Reforming

rural policy

Modernising institutions

Reforming fiscal policy

Improving the legal system

Using financial markets Reducing privileges of SOE

Modernising the financial system

Deregulating prices in competitive sectors

Cleaning up market awarding methods

China: the main challenge

M a c r o - e c o n o m y E u r o p e

250

300

350

400

450

500

550

600

65

75

85

95

105

115

125

135

145

Dec-12 Jun-13 Dec-13

Itraxx Main Europe Itraxx CrossOver

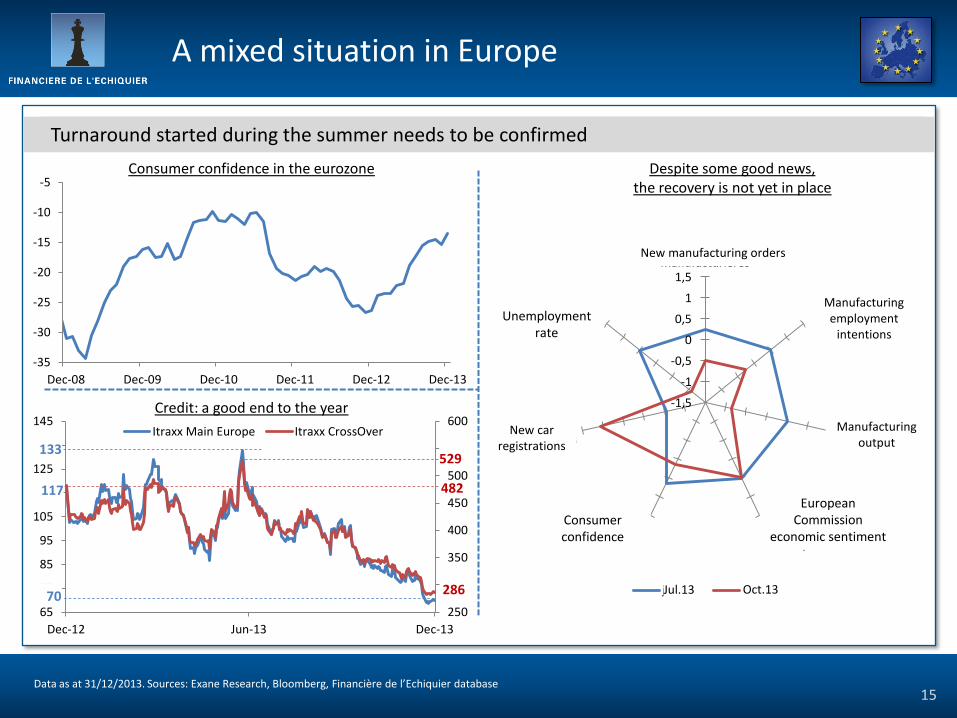

15

Turnaround started during the summer needs to be confirmed

Data as at 31/12/2013. Sources: Exane Research, Bloomberg, Financière de l’Echiquier database

A mixed situation in Europe

Credit: a good end to the year

Consumer confidence in the eurozone Despite some good news, the recovery is not yet in place

133 529

117 482

70 286

-35

-30

-25

-20

-15

-10

-5

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

-1,5

-1

-0,5

0

0,5

1

1,5

Nouvelles commandesmanufacturières

Intentionsd'embauches

manufacturières

Productionmanufacturière

Sentimentéconomique de la

CommissionEuropéenne

Confiance desconsommateurs

Nouvellesimmatriculations

Taux de chômage

juil.-13 oct.-13

Manufacturing employment

intentions

New manufacturing orders

Manufacturing output

European Commission

economic sentiment

Unemployment rate

New car registrations

Consumer confidence

Jul.13 Oct.13

16 Data as at 31/12/2013. Sources: BofA Merrill Lynch, Bloomberg, Financière de l’Echiquier database

A changed understanding of Europe vs emerging markets

Change in flows towards developed countries to the detriment of emerging countries

-50 $bn

0 $bn

50 $bn

100 $bn

150 $bn

200 $bn

250 $bn

300 $bn

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13

Cumul des souscriptions sur les fondsactions des pays émergents

Cumul des souscriptions sur les fondsactions des pays développés

-20 $bn

-10 $bn

0 $bn

10 $bn

20 $bn

30 $bn

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13

Cumul des souscriptions sur les obligations émergentes

Cumul des souscriptions sur les obligations High Yield (paysdéveloppés)

-10 $bn

0 $bn

10 $bn

20 $bn

30 $bn

40 $bn

50 $bn

60 $bn

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13

Flux cumulés sur les fonds actions Europe

0 $bn

1 $bn

2 $bn

3 $bn

4 $bn

5 $bn

6 $bn

7 $bn

2000 2002 2004 2006 2008 2010 2012 2014

Cumul des souscriptions ETF Europe(iShare MSCI EMU ETF)

Total subscriptions into emerging markets equity funds

Total subscriptions into developed markets equity funds

Total inflows into equity funds in Europe Total subscriptions for Europe ETFs (iShare MSCI EMU ETF)

Total subscriptions into emerging bond markets

Total subscriptions into high-yield bonds (developed markets)

5,00

7,00

9,00

11,00

13,00

15,00

17,00

19,00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

PER (forward 12 mois) MSCI Europe

PER (forward 12 mois) MSCI USA

PER (forward 12 mois) MSCI Emerging

17

Long-term valuation references

Data as at 31/12/2013. Sources: Exane Research, Financière de l’Echiquier database

Less room for disappointment

Extent of variation over 10 years

10.3

13.4

15.6

10.4

18.2

14.2

12.1

10.6

7.4

16.9

14.3

6.3

Median

Median

Median

MSCI Europe 12-month forward PER

MSCI USA 12-month forward PER

MSCI Emerging 12-month forward PER

18

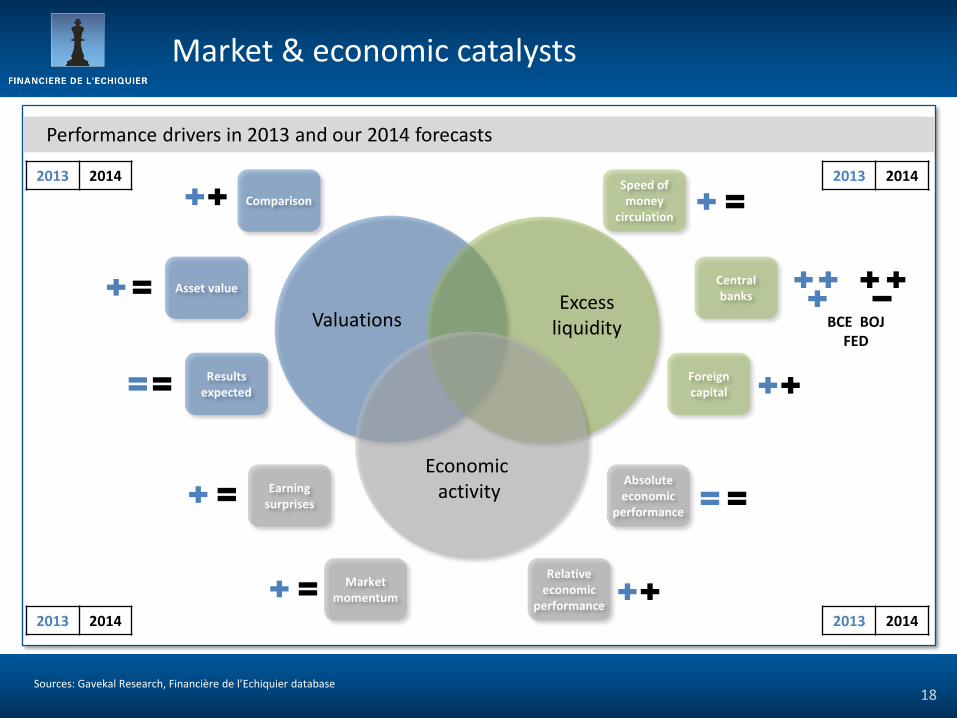

Performance drivers in 2013 and our 2014 forecasts

Sources: Gavekal Research, Financière de l’Echiquier database

Market & economic catalysts

Excess liquidity Valuations

Economic activity

Asset value Central banks

Comparison Speed of money

circulation

Foreign capital

Results expected

Earning surprises

Market momentum

Relative economic

performance

Absolute economic

performance

2013 2014

BCE BOJ FED

2013 2014 2013 2014

2013 2014

19 Source: Financière de l’Echiquier database The stocks shown are provided as an example. Neither their presence in the portfolio managed, nor their performance are guaranteed.

Our investment themes for 2014

Our stock picks

The lagging cycle in Europe The "contrarian" view on Europe

Emerging markets victims Long-term vision still intact

Oil & Gas services Paper

Growth/Value

F i x e d I n c o m e M a r k e t s

21

“Bond-picking”

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database Past performances are not a reliable indicator of future performances and may vary over time. The funds are primarily invested in bonds. They present a risk of capital loss. The stocks shown are provided as an example. Neither their presence in the portfolio managed, nor their performance are guaranteed.

Strong choices paid off…

10-year government bonds

-11.7%

-6.4%

-4.4%

-1.8%

+0.4%

+8.9%

+14.6%

Echiquier "High Yield"

2013 performance

BBB-

BBB+

AA+

AAA

AAA

AA-

5-year corporate bonds

Echiquier Oblig

Iboxx Corporate 3-5 years (BBB)

+6.4%

+2.8%

2013 Performance

+0.5%

+11.1%

+8.4%

B-

BBB

AA

22

Stop the preconceived ideas on corporate credit: the “best” risk/return profile

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database

… with no increase in volatility

Lehman Brothers

Greek crisis

100 day historical volatility

Euro crisis

Announcement of "tapering"

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

4,50%

5,00%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Euro MTS 3-5 ans

Iboxx Corporate 3-5 ansIboxx Corporate 3-5 yrs

Euro MTS 3-5 yrs

23

Our guidelines for 2014

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database The stocks shown are provided as an example. Neither their presence in the portfolios managed, nor their performance are guaranteed.

Our convictions

ECB still active Beware of duration

200 + 200 ≠ 100 + 300

Courbe des taux allemands

Always new ideas

- Subordinated debt (LT2) - Maturity 10 years - Yield on purchase: 7.1%

- Corporate bond - Maturity 6 ½ years - Yield on purchase: 4.9% B

BB-

- Corporate bond - Maturity 6 years - Yield on purchase: 4.1% B

0

200

400

600

800

1000

1200

2005 2006 2007 2008 2009 2010 2011 2012 2013

Itraxx CrossOver

Moyenne mobile 1an glissant

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

0 ans 5 ans 10 ans 15 ans 20 ans

Courbe des taux allemands (forward 2 ans)

1-year yoy moving average

German interest rates curve (2-year forward) German interest rates curve

5 yrs 10 yrs 15 yrs 20 yrs

24

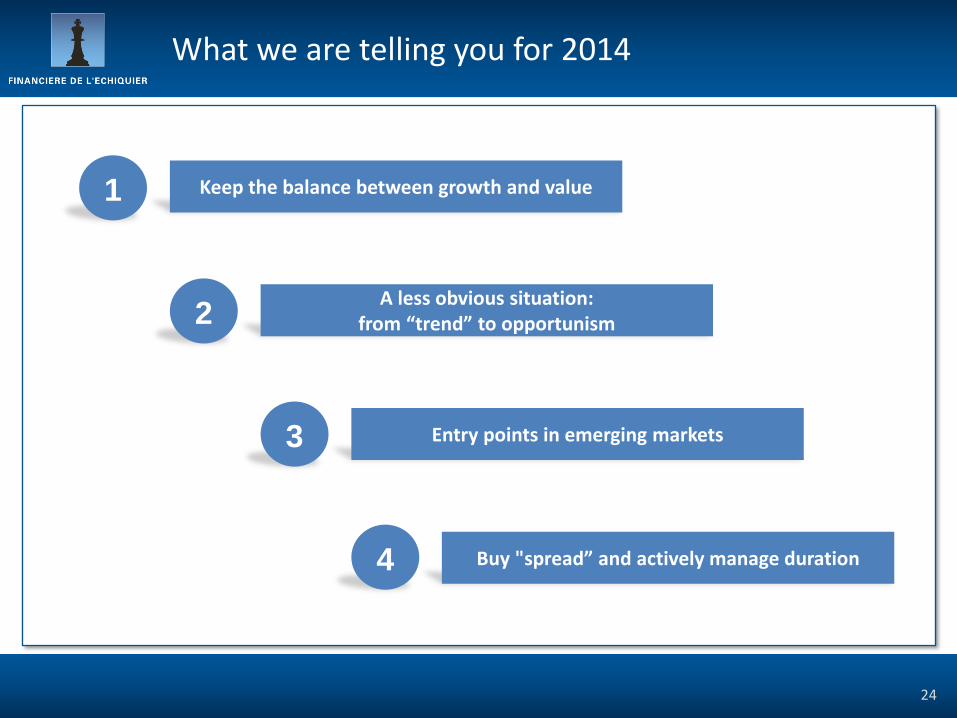

Keep the balance between growth and value 1

A less obvious situation: from “trend” to opportunism 2

Entry points in emerging markets 3

Buy "spread” and actively manage duration 4

What we are telling you for 2014

A G R E S S O R A R T Y

Data as at 31/12/2013. Sources: Bloomberg, Morningstar, Financière de l’Echiquier database The fund is mostly invested in equities. It presents the risk of capital loss. 26

AGRESSOR Fund overview

“Carte blanche” to the portfolio manager since 1991

Contrarian and opportunist

No constraints in style or size

Constant attention paid to the “value of things”

Demanding purchase prices and ability to reduce equity exposure to 60%

Looking for charismatic managers

Projects carried by the best managers with the support of key shareholders

Past performances do not predict future performances and are not constant over time. The performance of the fund and the benchmark indicator take account of distributed income items (as of 2013). In contrast, until 2012, the benchmark indicator performance does not take account of distributed income items.

EV/sales 2014 1.5

P/E 2014 16.6

Yield (%) 2.1

Average capitalisation (€m) 13 320.5

Shares in the portfolio 46

Total assets (€m) 1 446

0

50

100

150

3-years

+26.6% +19.3%

5-years

+48.4%

+21.8%

2013

+140.5%

+22.5%

Benchmark Agressor

Agressor

Agressor has gained 1,571.2% since its creation in 1991 compared with 197.7% for its benchmark index

Data as of 31/01/2014. Source : Database Financière de l’Echiquier

27

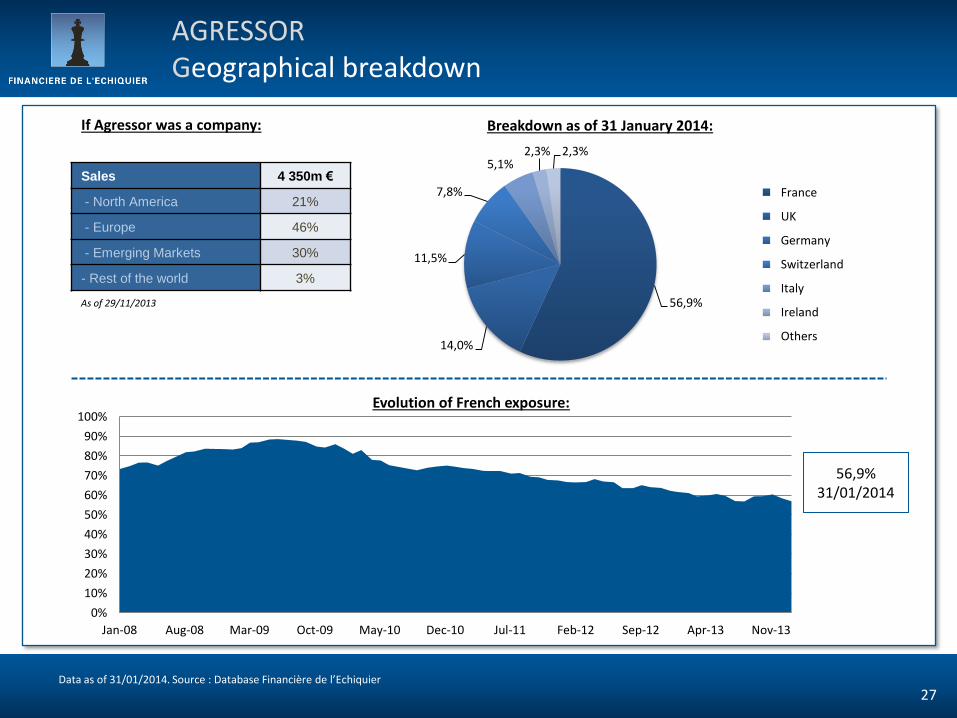

AGRESSOR Geographical breakdown

56,9% 31/01/2014

Breakdown as of 31 January 2014:

Evolution of French exposure:

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-08 Aug-08 Mar-09 Oct-09 May-10 Dec-10 Jul-11 Feb-12 Sep-12 Apr-13 Nov-13

56,9%

14,0%

11,5%

7,8%

5,1% 2,3% 2,3%

France

Royaume-Uni

Allemagne

Suisse

Italie

Irlande

Autres

France

UK

Germany

Switzerland

Italy

Ireland

Others

Sales 4 350m €

- North America 21%

- Europe 46%

- Emerging Markets 30%

- Rest of the world 3%

As of 29/11/2013

If Agressor was a company:

The value of things A return to normal

A strongly undervalued quality group An entry point to South-East Asia SAIPEM emerging from a difficult phase

28

AGRESSOR Our choices for 2014

Emerging consumers

MICHELIN is the global leader in tyres.

The group is set to benefit from the recovery in the replacement tyre cycle in Europe and the US, combined with a take-off in the Chinese market.

Specialty tyres (35% of group EBIT), in which the group shares a duopoly with BRIDGESTONE, are worth more than €10bn alone.

MICHELIN has one of the lowest valuations in the market at 8.5x 2014e PER .

SAIPEM is the global co-leader in offshore

oil installations.

The group suffered a very difficult year in 2013 with hefty losses on certain contracts, causing the departure of the management team.

The priority for the new team: to restore strong discipline in new orders and to pay down the group’s debt.

At 1.1x capital employed, the market sees no value creation potential for the group which has proven its quality and its unique expertise in the past.

DKSH is a Swiss group specialised in the

distribution of mass market products in South-East Asia.

The group is the local intermediary for major names in the sector: NESTLE, BEIERSDORF, LINDT and BAYER are among its clients.

Growth potential of more than 10% a year

and ability to improve margins on the back of increasingly sophisticated services.

At 12.4x 2014e EBIT, we can make the most of the outlook for this group which is 100% exposed to consumer spending in emerging markets.

Source: Financière de l’Echiquier database The stocks shown are provided as an example. Neither their presence in the portfolios managed, nor their performance is guaranteed .

29

Keep the balance between growth and value 1

A fund that remains “contrarian” 2

Re-investing on the emerging market theme 3

AGRESSOR Key takeaways

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database The fund is mostly invested in equities and bonds. It presents the risk of capital loss. 30

ARTY Fund overview

An “all-weather” solution for growing your savings

Companies: search for best risk/return profile

Dividends on equities Coupons on bonds

Mobility against volatile markets

Capacity to invest from 0-50% in equities

Past performances do not predict future performances and are not constant over time. Performances by the fund and the benchmark indicator take account of distributed income items (as of 2013). In contrast, until 2012, the performance of the benchmark indicator in the equities segment does not take account of distributed income items.

4.2% Average yield 3.6% Yield to maturity 31.4% EV/sales 2014 1.8

P/E 2014 13.3

Average capitalisation (€m) 43 236

Shares in the portfolio 35

Duration 2.0

No. of bond lines 81

Total assets (€m) 427.3

Exposure to equities

0

5

10

15

20

25

30

35

40

45

50

3-year 5-year

+8.3% +5.0%

2013

+49.9%

+17.5% +14.5%

+6.6%

ARTY

Benchmark ARTY

ARTY has gained 38.9% since it was created in 2008 compared with 8.2% for its benchmark index

-1%

Main ratios

- 35 positions

- Average capitalisation: €43.2bn

- Yield: 4.2%

- P/Book (2013): 2.1

- PER (2014): 13.3 Growth Value

Mar

ket

cap

ital

isat

ion

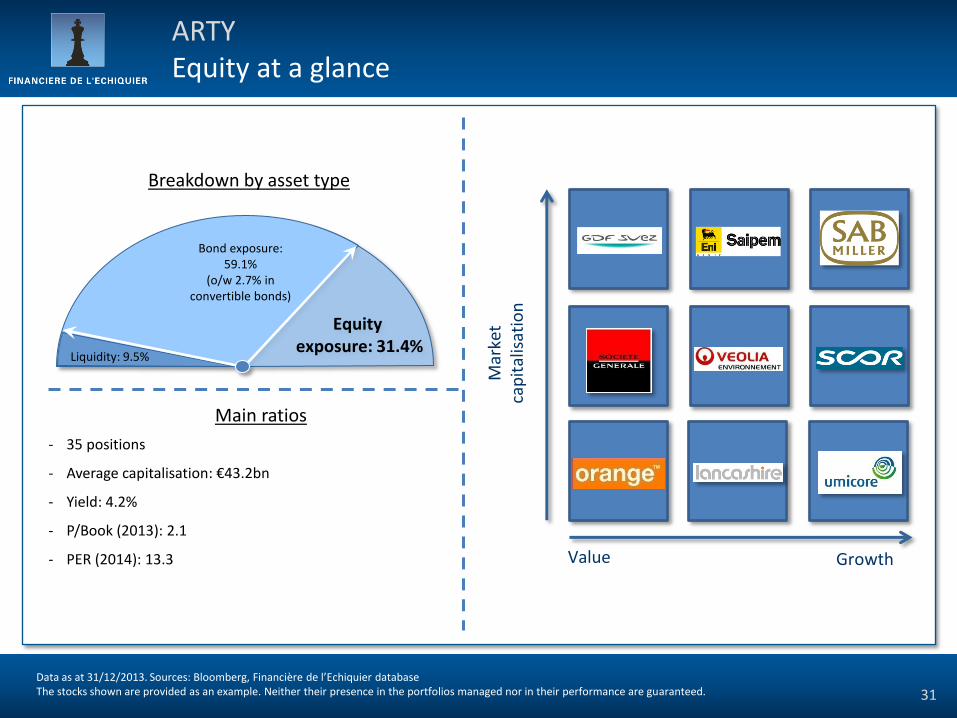

ORANGE

SOC GEN

SCOR

SABMILLER

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database The stocks shown are provided as an example. Neither their presence in the portfolios managed nor in their performance are guaranteed. 31

ARTY Equity at a glance

VEOLIA

Equity exposure: 31.4%

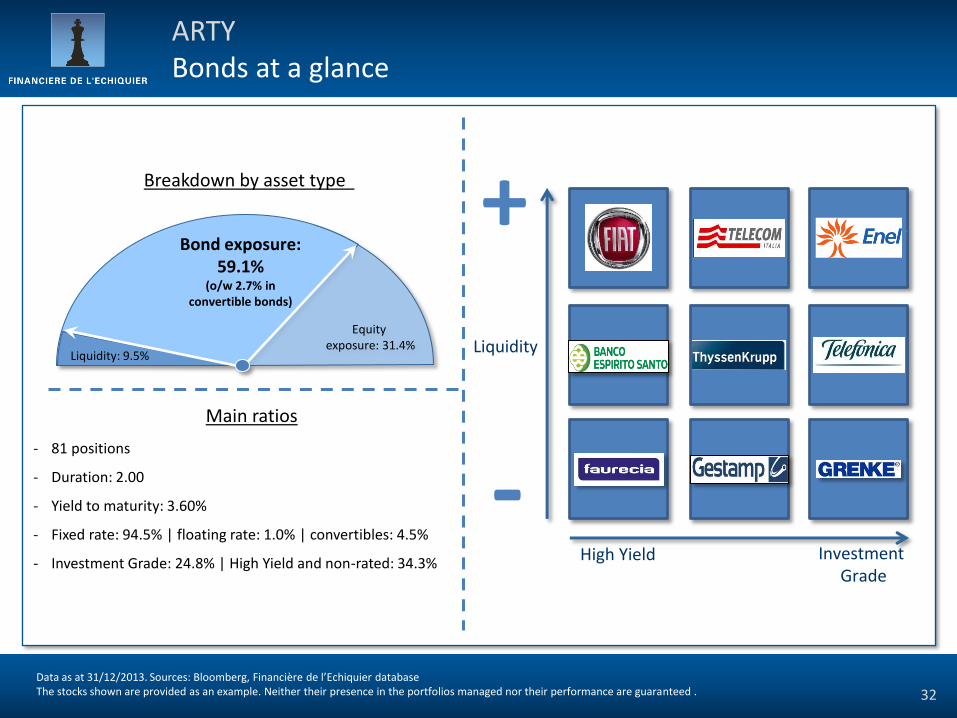

Bond exposure: 59.1%

(o/w 2.7% in convertible bonds)

Liquidity: 9.5%

Breakdown by asset type

-1%

Breakdown by asset type

BES

Investment Grade

High Yield

Liquidity

Main ratios

- 81 positions

- Duration: 2.00

- Yield to maturity: 3.60%

- Fixed rate: 94.5% | floating rate: 1.0% | convertibles: 4.5%

- Investment Grade: 24.8% | High Yield and non-rated: 34.3%

CONTINENTAL 7,50% 2017

CEGEDIM 7,00% 2015

GRENKE 4,00% 2015

Saint-Gobain 7,25% 2013

APRR 5,00% 2017

DEUTSCHE TEL 5,75% 2015

+

-

Equity exposure: 31.4%

Bond exposure: 59.1%

(o/w 2.7% in convertible bonds)

Liquidity: 9.5%

Data as at 31/12/2013. Sources: Bloomberg, Financière de l’Echiquier database The stocks shown are provided as an example. Neither their presence in the portfolios managed nor their performance are guaranteed . 32

ARTY Bonds at a glance

33

ARTY Key takeaways

Mobility in asset allocation 1

Rebalancing Value vs. Growth 2

Buy "spread“ and actively manage duration 3

34

2014 The year of stock-picking!

This document is destined for professional investors and has no contractual value. It cannot be distributed to third parties without the prior agreement of Financière de l’Echiquier. The information is provided from the best sources we possess. This information and the document do not represent an investment recommendation. Past performances are not a reliable indicator of future performances and may vary over time. Past performances must not therefore be the central element in the subscriber’s investment decision: other elements presented in the funds’ prospectus should be taken into consideration. The performances of the funds and the benchmark indicators take account of distributed income items (as of 2013). In contrast, until 2012, the performance of the benchmark indicator does not take account of distributed income items. This is not the case for Echiquier Patrimoine whose benchmark index is the Capitalised Eonia. For further information on the funds presented, please refer to their prospectuses available on simple request from the investment company on +33.(0)1.47.23.90.90 or by contacting your usual representative. Echiquier Value, Echiquier Global Emergents, Echiquier Global Convertibles and Echiquier Entrepreneurs are authorised for marketing in France. Agressor, Echiquier Major, Echiquier Agenor, Echiquier Global, Echiquier Patrimoine and ARTY are authorised for marketing in France, Germany, Belgium, Spain, Italy, The Netherlands and Switzerland. They are also available under the framework of life insurance contracts under Luxemburg law under Freedom to Provide Services (FPS). Acropole Convertibles Monde and Acropole Convertibles Europe are authorised for marketing in France, Austria, Germany and Spain. We thank you for your confidence in us. Fund risk profile:

- The funds present the risk of capital loss. - The funds are primarily invested in equities and bonds. If the stocks to which they are

exposed lose value, the funds’ NAV could fall. - Bonds and convertible bonds, like any other debt security, carry default risk and offer

no guarantee on the payment of coupons. - The management method is discretionary. There is a risk that the funds are not

invested at all times in the best performing stocks. - In the small and midcap markets, the volume of shares listed on the stockmarket is

reduced and market movements are therefore greater on the downside and faster than for large caps. The funds’ NAV can therefore decline more rapidly and to a greater extent.

For Echiquier Global, Echiquier Global Emergents and Acropole Convertibles Monde: A risk associated with investing in emerging markets exists resulting in particular from the way these markets function and are supervised, which can deviate from the standards prevailing on major international stock exchanges, or from political and regulatory factors. We invite you to consult the funds’ prospectuses for all further information on these risks. All of the costs attributable to the funds are available in the prospectuses. Current costs are updated annually and are available in the funds’ KIIDs.

35