investor campus - biznews.com campus key global indices jse all share - last month south africa...

TRANSCRIPT

1

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Key Global Indices

JSE All Share - Last Month

South Africa Market Review

FTSE 100 - Last Month

UK Market Review

S&P 500 - Last Month

US Market Review

Markets in Asia are trading mostly lower this morning, ahead of the release of

US nonfarm payrolls data later today. In Japan, Screen Holdings and Nippon

Telegraph & Telephone shed 5.5% and 1.3%, respectively. In Hong Kong,

Haitong Securities soared 12.9%, following news that the company was in

discussions with Banco Espirito Santo to acquire its investment-banking division.

In South Korea, Korean Air Lines advanced 0.2%, after the South Korean

government stated that it would launch a feasible study on a likely expansion of

Jeju International Airport. The Nikkei 225 Index is trading 0.1% lower at

17,871.38, while the Kospi Index is trading marginally lower at 1,985.54. The

Hang Seng Index is trading 0.7% in positive territory at 24,007.44.

Nikkei 225 - Last Month

Asia Market Review

US markets ended in negative territory yesterday, as the ECB’s decision to delay

additional stimulus dampened investor sentiment. Energy sector stocks, Range

Resources, Transocean and Diamond Offshore Drilling plummeted 6.1%, 4.6%

and 4.3%, respectively, tracking a decline in oil prices. Ford Motor shed 1.3%, as

the company expanded a recall of about 38,500 vehicles in the US due to

defective airbags. PVH Corporation fell 1.4%, after posting 3Q15 revenue below

market estimates. On the upside, Microsoft climbed 1.6%, after Barnes & Noble

agreed to buy the company’s stake in Nook Media LLC. The S&P 500 Index

dropped 0.1% to settle at 2,071.92, while the DJIA Index fell 0.1% to close at

17,900.10. The NASDAQ Index declined 0.1% to finish at 4,769.44.

UK markets finished lower yesterday, after the ECB Chief, Mario Draghi, stated

that the policymakers would first ascertain if the region’s economy requires

additional stimulus measures at the start of FY15. Meanwhile, the BoE left its key

interest rate unchanged. Oil sector stocks, Tullow Oil, BP, and Royal Dutch Shell

Class ‘B’ retreated 2.9%, 2.3% and 1.3%, respectively. Rio Tinto declined 2.6%,

after it revealed that tough conditions prevailed for the company in the short

term. Peers, Anglo American and BHP Billiton lost 2.8% and 1.2%, respectively.

However, TUI Travel climbed 3.6%, after its annual underlying operating profit

rose 11.0%. easyJet gained 2.9%, after reporting a 3.1% annualised rise in its

passengers for November. The FTSE 100 Index fell 0.6% to close at 6,679.37.

South African markets closed in the red yesterday, after the European Central

Bank (ECB) decided to delay its stimulus package to next month. Major losers,

Eqstra Holdings, Assore and Ascension Properties dropped 6.8%, 4.2% and

4.2%, respectively. Retail sector stocks, Truworths International, Mr Price Group

and Clicks Group declined 2.7%, 1.9% and 1.7%, respectively. Barclays Africa

Group, FirstRand and Nedbank Group fell 2.3%, 1.7% and 1.4%, respectively.

On the upside, Famous Brands gained 2.9%, after the company announced that

it has tied up with Shoprite in the opening of a Debonairs Pizza outlet in Angola.

Gold miners, Sibanye Gold and Harmony Gold Mining gained 1.6% and 1.5%,

respectively. The JSE All Share Index dropped 0.9% to close at 49,392.59.

5 December 2014

48,614

49,446

50,278

51,109

4-Nov 13-Nov 24-Nov 3-Dec

6,389

6,532

6,675

6,818

4-Nov 13-Nov 24-Nov 3-Dec

1,992

2,026

2,061

2,095

4-Nov 13-Nov 24-Nov 3-Dec

16,613

17,097

17,582

18,066

4-Nov 13-Nov 24-Nov 3-Dec

Last Close 1D Chg 1D % Chg YTD% Chg 1M % Chg 1Y % Chg P/E Multiple (x)

JSE All Share 49,392.59 -464.59 -0.9 6.8 -0.8 12.3 17.05

JSE Africa Resource 10 43,380.15 -694.32 -1.6 -15.0 -8.8 -11.9 13.25

JSE Africa Financial 15 15,328.28 -156.35 -1.0 20.3 1.0 26.5 13.06

JSE Africa Industrial 25 61,444.62 -523.80 -0.8 12.8 1.3 20.5 22.28

FTSE 100 6,679.37 -37.26 -0.6 -1.0 3.5 2.6 19.06

German DAX 30 9,851.35 -120.44 -1.2 3.1 7.5 7.8 17.31

France CAC 40 4,323.89 -67.97 -1.5 0.7 4.7 4.2 25.90

S&P 500 2,071.92 -2.41 -0.1 12.1 3.0 15.6 18.36

Dow Jones Industrials 17,900.10 -12.52 -0.1 8.0 3.0 12.7 15.99

Nasdaq Composite 4,769.44 -5.03 -0.1 14.2 3.2 18.1 77.92

Nikkei 225* 17,871.38 -15.83 -0.1 9.8 6.1 16.1 21.87

Shanghai Composite* 2,881.28 -18.18 -0.6 37.0 19.3 28.8 14.09

Hang Seng Index* 24,007.44 174.88 0.7 2.3 -0.1 0.4 10.43

*Time - SAST 6:00:00 AM

2

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Commodities

At 06:00 SAST today, Brent crude oil fell 0.3% to trade at $68.79/bl.

Yesterday, Brent crude oil fell 1.0% to settle at $69.01/bl, following news

that Saudi Arabia cut its export prices of crude to the US and Asia.

Yesterday, the Illinois North Central No.2 Yellow corn spot prices rose

2.0% to $3.57/bushel. The US department of Agriculture, in its weekly

sales report, indicated that corn exports from the US totalled 1.17mnt,

compared with trade expectations of between 600.00k and 850.00kt.

At 06:00 SAST today, gold prices declined 0.1% to trade at $1,203.64/oz.

Yesterday, gold declined 0.3% to close at $1,205.27/oz, after the ECB

decided to delay fresh stimulus measures until next year.

Yesterday, copper rose 1.6% to close at $6,535.50/mt. Aluminium closed

1.4% higher at $1,994.50/mt.

Currencies

Yesterday, the South African rand strengthened against the US dollar, after

data released in the US showed that the number of initial jobless claimants

fell less than expected for the previous week. Later today, market

participants will keep a tab on US nonfarm payrolls data along with the gold

and forex reserves report in South Africa for further direction to the South

African rand against the majors.

The yield on benchmark government bonds remained mixed yesterday.

The yield on 2015 bond rose to 6.11% while that for the longer-dated 2026

issue declined to 7.69%.

At 06:00 SAST, the US dollar is trading 0.1% higher against the South

African rand at R11.2040, while the euro is trading 0.1% higher at

R13.8778.

Yesterday, the euro advanced against most of the major currencies, as the

ECB kept its interest rate unchanged and the central bank President, Mario

Draghi, indicated that the ECB is likely to implement further stimulus

measures in the eurozone next month. Separately, the Bank of England

(BoE) kept its policy stance unchanged in its yesterday’s policy meeting.

Later today, eurozone GDP and German factory orders data is expected to

attract investors’ attention.

At 06:00 SAST, the euro remained flat against the US dollar to trade at

$1.2382, while it has gained 0.1% against the British pound to trade at

GBP0.7910.

Crude Oil and Corn Prices Spot

Gold & Platinum Prices Spot

Copper, Aluminium & Iron Ore Prices Spot (Rebased)

USD/ZAR Movement

EUR/ZAR Movement

GBP/ZAR Movement

3.3

3.4

3.5

3.6

4-Nov 13-Nov 24-Nov 3-Dec

68.3

73.4

78.5

83.6

$/b

us

he

l

$/b

bl

Crude - LHS Corn - RHS

1165

1198

1231

1264

4-Nov 13-Nov 24-Nov 3-Dec

1118

1157

1197

1236

$/o

z

$/o

z

Gold - LHS Platinum - RHS

10.8450

11.0248

11.2047

11.3845

4-Nov 13-Nov 24-Nov 3-Dec

13.4464

13.6852

13.9240

14.1628

4-Nov 13-Nov 24-Nov 3-Dec

16.9885

17.3439

17.6994

18.0548

4-Nov 13-Nov 24-Nov 3-Dec

4-Nov 13-Nov 24-Nov 3-Dec

80

90

100

110

Copper Aluminium Iron Ore 62% Fe Content - CFR Qingdao China

3

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Yield Corner

% Closing

Yield

% Change

on Day

Yield % -

1M Ago

South Africa CPI* 5.90 0.00 5.90

South Africa Repo Rate 5.75 0.00 5.75

JSE SA Listed Property Index 5.91 1.03 6.07

R157 (2015) (SA Bond) 6.11 0.11 6.29

R207 (2020) (SA Bond) 7.07 0.28 7.30

R186 (2026) (SA Bond) 7.69 -0.44 7.96

US 10 Year Treasury 2.23 -2.01 2.33

US 30 Year Treasury 2.94 -1.63 3.05

Italian 10 Year Treasury 2.04 2.67 2.44

German 10 Year Treasury 0.77 3.34 0.81

* As on October 2014

South African Government Bond Yields

JSE All Share Index - Major Gainers & Losers

Figures in bracket indicate (Last Close, Absolute Change, % Change)

5.8%

6.5%

7.2%

7.8%

8.5%

9.2%

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

R157 (2015) R186 (2026)

-9.3% -7.4% -5.6% -3.7% -1.9% 0.0%

Eqstra Holdings Ltd (373.00, -27.00, -6.8%)

Ascension Properties Ltd (230.00, -10.00, -4.2%)

Assore Ltd (16298.00, -709.00, -4.2%)

Tongaat Hulett Ltd (15390.00, -575.00, -3.6%)

Blue Label Telecoms Ltd (905.00, -33.00, -3.5%)

Bell Equipment Ltd (1045.00, -35.00, -3.2%)

Illovo Sugar Ltd (2510.00, -80.00, -3.1%)

Resilient Property Income Fund Ltd (8624.00, -252.00, -2.8%)

Anglo American PLC (22468.00, -638.00, -2.8%)

Truworths International Ltd (7690.00, -210.00, -2.7%)

0.0% 1.9% 3.7% 5.6% 7.4% 9.3%

Stefanutti Stocks Holdings Ltd (670.00, 52.00, 8.4%)

PSG Konsult Ltd (720.00, 35.00, 5.1%)

Telkom SA SOC Ltd (7000.00, 253.00, 3.8%)

Quantum Foods Holdings Ltd (325.00, 10.00, 3.2%)

Curro Holdings Ltd (2649.00, 79.00, 3.1%)

Pan African Resources PLC (210.00, 6.00, 2.9%)

Famous Brands Ltd (10600.00, 295.00, 2.9%)

Lewis Group Ltd (8225.00, 208.00, 2.6%)

Santam Ltd (21620.00, 529.00, 2.5%)

Invicta Holdings Ltd (10139.00, 239.00, 2.4%)

4

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

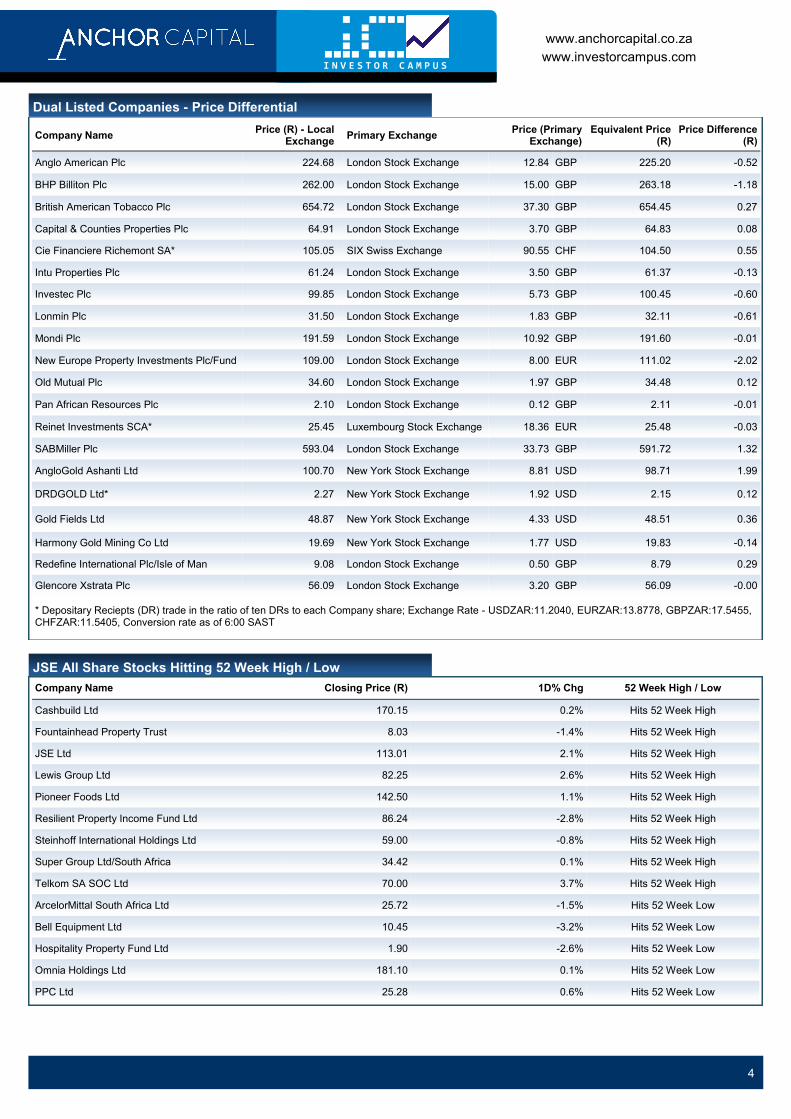

Dual Listed Companies - Price Differential

Company Name Price (R) - Local

Exchange Primary Exchange

Price (Primary Exchange)

Equivalent Price (R)

Price Difference (R)

Anglo American Plc 224.68 London Stock Exchange 12.84 GBP 225.20 -0.52

BHP Billiton Plc 262.00 London Stock Exchange 15.00 GBP 263.18 -1.18

British American Tobacco Plc 654.72 London Stock Exchange 37.30 GBP 654.45 0.27

Capital & Counties Properties Plc 64.91 London Stock Exchange 3.70 GBP 64.83 0.08

Cie Financiere Richemont SA* 105.05 SIX Swiss Exchange 90.55 CHF 104.50 0.55

Intu Properties Plc 61.24 London Stock Exchange 3.50 GBP 61.37 -0.13

Investec Plc 99.85 London Stock Exchange 5.73 GBP 100.45 -0.60

Lonmin Plc 31.50 London Stock Exchange 1.83 GBP 32.11 -0.61

Mondi Plc 191.59 London Stock Exchange 10.92 GBP 191.60 -0.01

New Europe Property Investments Plc/Fund 109.00 London Stock Exchange 8.00 EUR 111.02 -2.02

Old Mutual Plc 34.60 London Stock Exchange 1.97 GBP 34.48 0.12

Pan African Resources Plc 2.10 London Stock Exchange 0.12 GBP 2.11 -0.01

Reinet Investments SCA* 25.45 Luxembourg Stock Exchange 18.36 EUR 25.48 -0.03

SABMiller Plc 593.04 London Stock Exchange 33.73 GBP 591.72 1.32

AngloGold Ashanti Ltd 100.70 New York Stock Exchange 8.81 USD 98.71 1.99

DRDGOLD Ltd* 2.27 New York Stock Exchange 1.92 USD 2.15 0.12

Gold Fields Ltd 48.87 New York Stock Exchange 4.33 USD 48.51 0.36

Harmony Gold Mining Co Ltd 19.69 New York Stock Exchange 1.77 USD 19.83 -0.14

Redefine International Plc/Isle of Man 9.08 London Stock Exchange 0.50 GBP 8.79 0.29

Glencore Xstrata Plc 56.09 London Stock Exchange 3.20 GBP 56.09 -0.00

* Depositary Reciepts (DR) trade in the ratio of ten DRs to each Company share; Exchange Rate - USDZAR:11.2040, EURZAR:13.8778, GBPZAR:17.5455, CHFZAR:11.5405, Conversion rate as of 6:00 SAST

JSE All Share Stocks Hitting 52 Week High / Low

Company Name Closing Price (R) 1D% Chg 52 Week High / Low

Cashbuild Ltd 170.15 0.2% Hits 52 Week High

Fountainhead Property Trust 8.03 -1.4% Hits 52 Week High

JSE Ltd 113.01 2.1% Hits 52 Week High

Lewis Group Ltd 82.25 2.6% Hits 52 Week High

Pioneer Foods Ltd 142.50 1.1% Hits 52 Week High

Resilient Property Income Fund Ltd 86.24 -2.8% Hits 52 Week High

Steinhoff International Holdings Ltd 59.00 -0.8% Hits 52 Week High

Super Group Ltd/South Africa 34.42 0.1% Hits 52 Week High

Telkom SA SOC Ltd 70.00 3.7% Hits 52 Week High

ArcelorMittal South Africa Ltd 25.72 -1.5% Hits 52 Week Low

Bell Equipment Ltd 10.45 -3.2% Hits 52 Week Low

Hospitality Property Fund Ltd 1.90 -2.6% Hits 52 Week Low

Omnia Holdings Ltd 181.10 0.1% Hits 52 Week Low

PPC Ltd 25.28 0.6% Hits 52 Week Low

5

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Economic Updates

Key Economic Releases Today

Country SAST Economic Indicator Relevance Consensus/

*Actuals Previous/

**Previous Est. Frequency

Japan 1:50 Japan Foreign Reserves (Nov) $1269.10 bn* $1265.90 bn Monthly

Japan 7:00 Leading Economic Index, Prelim (Oct) 104.10 105.60 Monthly

South Africa 8:00 Net Gold & Forex Reserve (Nov) $43.07 bn $43.09 bn Monthly

South Africa 8:00 Gross Gold & Forex Reserve (Nov) $48.66 bn $48.68 bn Monthly

Germany 9:00 Factory Orders n.s.a. (YoY) (Oct) 0.0% -1.0% Monthly

Germany 9:00 Factory Orders s.a. (MoM) (Oct) 0.5% 0.8% Monthly

Spain 10:00 Industrial Production (YoY) (Oct) - 3.6% Monthly

UK 11:30 Consumer Inflation Expectations - 2.8% -

Eurozone 12:00 Gross Domestic Product s.a., Final (QoQ) (Q3) 0.2% 0.0%** Quarterly

Eurozone 12:00 Gross Domestic Product s.a., Final (YoY) (Q3) 0.8% 0.7%** Quarterly

Canada 15:30 Full Time Employment Change (Nov) - 26.50 K Monthly

Canada 15:30 Part Time Employment Change (Nov) - 16.50 K Monthly

Canada 15:30 Participation Rate (Nov) 66.0% 66.0% Monthly

Canada 15:30 Unemployment Rate (Nov) 6.6% 6.5% Monthly

US 15:30 Average Hourly Earnings All Employees (YoY) (Nov) 2.1% 2.0% Monthly

US 15:30 Unemployment Rate (Nov) 5.8% 5.8% Monthly

Canada 15:30 Net Change in Employment (Nov) 0.00 K 43.10 K Monthly

US 15:30 Change in Non-farm Payrolls (Nov) 230.00 K 214.00 K Monthly

US 15:30 Trade Balance (Oct) -$41.20 bn -$43.00 bn Monthly

US 15:45 Fed's Mester Speaks on Financial Stability in Washington - - -

US 17:00 Factory Orders (MoM) (Oct) 0.0% -0.6% Monthly

US 21:45 Fed's Fischer Speaks Via Video to IMF Event in Washington - - -

US 22:00 Consumer Credit Change (Oct) $16.50 bn $15.92 bn Monthly

Note: High Medium Low

Electricity consumption in South Africa dropped 1.0%, on an annual basis, in October, compared with a 0.3% fall reported in September.

On an annual basis, electricity production in South Africa eased 1.0% in October, following a decline of 0.1% posted in September.

The Bank of England (BoE) kept its interest rate steady at 0.50%, in line with market expectations. Also, the BoE asset purchase facility

remained steady at GBP375.00bn, at par with market expectations.

The Halifax house price index in the UK rose 0.4%, on a monthly basis, in November, compared with a drop of 0.4% reported in October.

The ILO unemployment rate in France climbed to 10.4% in 3Q14 from a revised rate of 10.1% posted in 2Q14.

The European Central Bank (ECB) held its interest rate steady at 0.05%, meeting market expectations. The ECB President, Mario Draghi,

at the press conference following the ECB’s policy decision, stated that policymakers would reassess the central bank’s stimu lus measures

early next year and then only decide whether the eurozone economy would be in need of the ECB’s additional stimulus measures.

Furthermore, he hinted that the ECB would act even if it does not find unanimity among policymakers.

The seasonally adjusted initial jobless claims in the US fell to 297.00K in the week ended 29 November 2014, compared with a revised

reading of 314.00K recorded in the prior week.

The seasonally adjusted Ivey Purchasing Managers’ Index (PMI) in Canada rose to 56.90 in November from a reading of 51.20

registered in October.

Takehiro Sato, a Bank of Japan (BoJ) policy board member, stated that the central bank should not commit to achieving a specific inflation

rate within a specific time frame as it cannot directly control prices.

In November, the AIG performance of construction index in Australia eased to 45.40 from a reading of 53.40 reported in October.

6

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

South Africa

Pick n Pay Stores: The retailer indicated that it would donate a day's profit to honour the anniversary of former President Nelson Mandela's

death.

Lonmin Plc: The platinum miner indicated that it has brought black ownership in the company to 26.0% following a series of Black

Economic Empowerment (BEE) transactions.

Famous Brands: The company announced that it has tied up with Shoprite in the opening of a Debonairs Pizza outlet in Benguela, Angola.

The first Debonairs Pizza site will open in January FY15 and will soon be followed by six further Debonairs Pizza restaurants across Angola.

Gordhan welcomes ‘good compromise’ in PPC deal: PPC plans to name its new CEO at the end of the month, says Chairman, Bheki

Sibiya, after the company brokered a deal with activist shareholders aimed at averting a boardroom coup.

SABMiller says it has a head start in Colombia: Sabmiller’s strategy in Colombia was already suited to deal with new competitors,

management told investors last month as the company prepares to contend with a fresh wave of competition in its single largest market.

Rio Tinto not looking at mergers to raise defences against Glencore: Global mining company, Rio Tinto, is not looking to make any

major acquisition to protect itself from a potential Glencore takeover, CE Sam Walsh said at a meeting with investors on Thursday.

Transnet seals loco deal with Chinese manufacturer: Transnet and Chinese locomotives manufacturer, CSR Zhuzhou Electric

Locomotive (CSR), have signed an agreement paving the way for locomotive manufacturing in South Africa.

Uber valued at $40.00bn in $1.20bn equity funding: Uber Technologies Inc. has completed the next stage of its funding, garnering

$1.20bn to boost its international expansion.

Eskom accuses judge of misconduct: Eskom accused a judge, who acted as an arbitrator in a dispute with one of its contractors, of

misconduct in an effort to set aside his award against it.

Bobroff finally concedes his fee agreements are illegal: After years of strong denials, personal injury law firm, Ronald Bobroff and

Partners (RBP), has acknowledged that its common law contingency fee agreement was illegal.

UK and US

Kroger Co.: The retailer, in its 3Q15 results, indicated that its sales increased to $24.99bn from $22.47bn posted in the corresponding

period a year ago. Its diluted EPS excluding adjustment items was reported at $0.69, better than market expectations of $0.61/share. The

company sees FY15 EPS to be between $3.32 and $3.36, versus market consensus of $3.29/share.

Dollar General: In its 3Q15 results, the chain of discount retail stores stated that its net sales climbed to $4.72bn from $4.38bn reported in

the similar period prior year. Its adjusted diluted EPS was registered at $0.79, lower than market expected EPS of $0.80. The company

expects its FY15 total sales to increase approximately 8.0%, compared with FY14 and it plans to open approximately 730 new stores in

2015. Additionally, the company revealed that it still intends to buy Family Dollar.

Ulta Salon Cosmetics and Fragrance: The chain of beauty superstores, in its 3Q15 results, revealed that its net sales rose to $745.72mn

from $618.78mn reported in the same period prior year. Its net diluted EPS was posted at $0.91, better than market anticipations of $0.84/

share. The company expects its 4Q15 diluted EPS to be between $1.21 and $1.26, versus market consensus of $1.27/share.

United Natural Foods: In its 1Q15 results, the distributor of organic foods indicated that its net sales rose to $1.99bn from $1.60bn

registered in the same period prior year. Its diluted net EPS climbed to $0.66 from $0.56 recorded in the similar period earl ier year. In FY15,

the company estimates GAAP diluted EPS in the range of approximately $2.88 to $3.01, compared with GAAP diluted EPS of $2.52

reported in the earlier year.

Sears Holdings: The retailer, in its 3Q15 results, stated that its revenue from merchandise sales and services dropped to $7.21bn from

$8.27bn recorded in the corresponding period previous year. Its diluted loss per share was reported at $5.15, more than market expected

loss of $3.31/share.

Five Below: In its 3Q15 results, the company revealed that its net sales advanced to $137.98mn from $110.75mn recorded in the same

period preceding year. Its diluted EPS was posted at $0.06, in line with market estimates. The company sees 4Q15 GAAP EPS in the range

of $0.59 to $0.62, versus market consensus of $0.63/share and 4Q15 revenue in the range of $262.00mn to $266.00mn, versus market

consensus of $268.83mn. Furthermore, the company announced that its COO, Joel Anderson, has been appointed as its new CEO,

effective 1 February 2015.

Finisar Corporation: The manufacturer of optical communication components, in its 2Q15 results, indicated that its revenue advanced to

$296.98mn from $290.72mn registered in the corresponding period earlier year. Its diluted EPS was recorded at $0.23, worse than market

anticipations of $0.25/share. The company expects 3Q15 EPS to be between $0.23 and $0.27, versus market consensus of $0.28/share.

MetLife: Media reports revealed that US regulators are close to a final decision to label MetLife systemically important.

Reynolds American: The company announced that Andrew D. Gilchrist, its Executive Vice President would be promoted to Executive Vice

President and CFO, effective 1 March 2015 and the current CFO, Thomas R. Adams, plans to retire in March.

Corporate Updates

7

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Best Buy: The company announced that it has entered into a definitive agreement to sell its Five Star business to the Jiayuan Group, a

Chinese based real estate firm.

American Realty Capital Properties: The company announced that it has entered into a settlement agreement with RCS Capital

Corporation to resolve their dispute over the sale of Cole Capital Partners and Cole Capital Advisors to RCS Capital, wherein the company

would get a settlement amount of $60.00mn.

Starz LLC: Media reports revealed that the pay TV channel is considering alternatives to a sale after failing to find buyer.

RADA Electronic Industries: The company announced that a leading MOD has selected its MHR-based tactical radars that would help to

detect and alert from short-range threats for the latter’s national alert system. The deliveries are expected to complete in FY15.

TUI Travel: The company, in its FY14 results, announced that its revenue dropped to GBP14.62bn from GBP15.05bn posted in the

preceding year. However, its diluted EPS rose to 16.30p from 4.60p recorded in the previous year. The company also indicated that it is

pleased with the progress in Winter 2014/15 trading and the strong start to Summer 2015 trading in the UK continues. The combination of

its market leadership position, scale, focus on unique holidays distributed increasingly online and its relationship with the customer

throughout their whole holiday experience continues to provide a strong basis for sustainable, profitable growth. The merger with TUI AG

would strengthen and future-proof its combined Group.

DS Smith: In its 1H15 results, the company indicated that its revenue narrowed to GBP1.97bn from GBP2.08bn reported in the same

period a year ago. However, its diluted EPS rose to 10.10p from 7.50p posted in the corresponding period a year ago. The company also

stated that its outlook remains positive as the business continues to grow, despite economic headwinds in many of its markets. The

company expects continued performance in line with its medium term financial targets.

Greene King: The pub retailer and brewer, in its 1H15 results, announced that its revenue increased to GBP614.90mn from GBP595.40mn

posted in the same period preceding year. However, its diluted EPS dropped to 29.30p from 31.40p posted in the corresponding period

previous year.

Betfair Group: The online betting exchange, in its 1H15 results, indicated that its revenue climbed to GBP237.60mn from GBP188.00mn

recorded in the same period preceding year. Its diluted EPS jumped to 53.70p from 25.70p posted in the corresponding period a year ago.

The company also stated that it continues to expect revenue from sustainable markets to grow in line with the market. The company

anticipate revenue from other countries falling, on average, by between 15.0% and 25.0% per annum as a result of market exits and its

strategy of not investing in these regions. The company now expects FY15 EBITDA of between GBP97.00mn and GBP103.00mn.

A.G. Barr Plc: The soft drinks seller, in its trading update, indicated that its revenue for the 18 weeks to 30 November 2014 dropped 0.6%,

on a like for like basis, due to lower promotional activity. However, the company indicated that it is confident of achieving its expectations for

the year, and expects further growth for the following financial year.

Reed Elsevier: The company and Reed Elsevier NV announced that it would implement an additional irrevocable, non-discretionary

programme to repurchase their respective ordinary shares up to the value of GBP100.00mn in total between 1 January 2015 and 25

February 2015, ahead of its results announcement on 26 February 2015.

easyJet Plc: The company indicated that the number of passengers increased 3.1% to 4,386,296 in November 2014 from 4,255,978

posted in November 2013, while load factor rose to 89.5% from 89.0% reported in the previous year. On a rolling 12 months ending

November 2014, the number of passengers climbed 6.6% to 65,204,437 from 61,182,101, while load factor rose to 90.8% to 89.3%.

BTG Plc: The specialist healthcare company indicated that it has agreed to acquire PneumRx Inc. in a deal worth up to $475.00mn. The

company also stated that the acquisition would be funded in part by a cashbox placing with gross proceeds of approximately

GBP150.00mn, representing approximately 5.0% of the company's market capitalisation based on 03 December 2014 closing share price.

Hays Plc: The specialist recruitment company indicated it has acquired 80.0% of Veredus Corporation for an initial consideration of

approximately $44.00mn, on a cash free/debt free basis.

Carillion Plc: The company indicated that it has been awarded support services contracts by Heathrow Airport Limited and by Barts Health

NHS Trust, which together are worth approximately GBP80.00mn.

Financial Times

Unilever to run spreads business as separate unit: Unilever is to run its underperforming margarine and spreads business as a

standalone unit, in a move investors said was a likely precursor to disposal.

Orange Chief says BT poised to decide on bid for EE or O2: BT should decide whether to buy a mobile operator in the UK before

Christmas, says the Chief Executive of Orange, which is in talks to sell EE to the British telecoms group.

Capital Group cuts Aviva stake amid takeover of Friends Life: Capital Group, among the world’s biggest asset managers, has sold

about GBP410.0mn worth of shares in Aviva since a leak two weeks ago forced the insurer to set out preliminary terms of the sector’s

biggest deal in 15 years.

Sky cashes in lead stake in gambling unit: Sky has added GBP600.00mn in cash to its financial firepower by selling an 80.0% stake in

its Sky Bet gambling business, as it plans its response to the shake-up taking place in the UK telecoms sector.

Corporate Updates

8

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Towergate’s bankers invite ownership bids: Towergate’s bankers have invited its bondholders to take control of the heavily-indebted

insurance broker, underscoring the scale of the financial difficulties facing one of Britain’s biggest private companies.

GSK drops plan to sell older drugs: GlaxoSmithKline has ditched plans for a multibillion-pound sale of some of its older medicines,

halting an auction that had attracted interest from several of the world’s largest private equity groups.

Church challenges Shell and BP over climate change: The Church of England has waded in to the debate over climate change by

urging Royal Dutch Shell and BP to cut their carbon emissions and invest more in renewables, the first time it has attempted to use its

position as an investor as a “force for good”.

Bentley creates 300 jobs with Crewe R&D centre: Bentley is to build a research and development centre at its Crewe headquarters,

creating 300 jobs as the luxury carmaker seeks to produce a new generation of models and capitalise on its global success.

Microsoft quits struggling ereader Nook: Microsoft is bailing out of Nook, the struggling ereader business owned by Barnes & Noble, in a

move that clears the way for America’s largest bookstore chain to spin off the lossmaking division.

EU’s Hill considers shelving bank structural reforms: The EU’s new financial services Chief may withdraw a proposal next year to

overhaul the structure of big European banks if it remains mired in a political stalemate.

Qataris and Brookfield raise bid for Canary Wharf owner Songbird: The Qatar Investment Authority and Brookfield Property Partners

have increased their bid for control of Songbird Estates, the majority owner of east London business district Canary Wharf, to GBP2.60bn.

BTG buys US healthcare group for up to $475.00mn: BTG has reinforced its status as one of Europe’s fast-growing healthcare

companies with a deal worth up to $475.00mn to buy the US maker of a device that helps tackle breathing difficulties.

Stress test fears prompt Co-op Bank to scrap bonus vote: The Co-operative Bank has cancelled an imminent shareholder vote on

bonuses after conceding it will probably fail forthcoming bank stress tests.

Digital challenger bank Atom secures backing of Jim O’Neill: Jim O’Neill, the former Chairman of Goldman Sachs Asset Management,

has joined a number of high-profile investors to back Atom, the UK’s first digital-only bank aiming to challenge high street lenders.

US oil reserves at highest since FY75: US proven oil reserves last year rose to their highest level since FY75, official figures have shown,

in the latest sign of how the shale revolution has transformed the country’s energy supply outlook.

Reckitt Benckiser looks to core of ‘health, hygiene and home’: Next week shareholders in RB — the former Reckitt Benckiser — will

vote on ending the household group’s dependency on its opiate-substitute business.

Mulberry falls into red amid difficult luxury market: Red was the new black at handbag maker Mulberry after a tumultuous period

pushed the British luxury group into a loss in 1H15.

SoftBank buys $250.00mn stake in GrabTaxi: SoftBank has bought a $250.00mn stake in GrabTaxi, a southeast Asian Uber-style taxi-

hailing app, in the latest example of the Japanese telecoms group expanding its reach into faster-growing parts of Asia.

Ryanair passenger numbers jump 22.0% as it revises up profits: Ryanair has offered further proof that trying to please customers is

more profitable than annoying them as it reported that passenger numbers in November jumped 22.0% on last year to 6.35mn.

Rio Tinto: Lost 2.6% to GBP29.34, after management cut FY15 copper production guidance at a London investor day.

Ladbrokes: Rose 1.8% to GBP1.16, helped by a reheat of speculation that it is among the potential buyout targets for Playtech, up 1.3% to

GBP6.46.

Lex:

Global Brands Group: Beckham on board: David Beckham’s advert for Haig Club whisky is all about the power of celebrity. Diageo

knows Mr Beckham sells, which is why they hired him. Mr Beckham knows it, too. On Wednesday, Hong Kong-listed brand management

company, Global Brands Group, signed a deal with the former English footballer and his business partner Simon Fuller to exploit the pulling

power of celebrities. The partners will own half each of a joint venture intended to create new lifestyle brands, backed by high-profile sports

and entertainment stars. The business, as yet, has no other names signed up and no products to sell, although revenues from most of Mr

Beckham’s existing endorsements are part of the deal. Yet, despite Mr Beckham’s zeal for this “first of a kind” joint venture, it is not, in fact,

the first time that GBG has attempted to create celebrity-branded products. In FY10 LF USA (now renamed GBG USA) partnered with Star

Branding to create MESH. Its goal is also to develop brands inspired by names such as Jennifer Lopez and Marc Anthony. GBG does not

disclose earnings from individual brands, but perfumes from Ms Lopez’s stable reportedly garnered revenues of around $80.00mn in the

decade to FY12. GBG’s contribution to — and revenues from — subsequent development is unclear. In FY11 Beyoncé and Tina Knowles’

Beyond Productions joined LF USA. So the deal may not be so revolutionary. Still, the involvement of Mr Beckham and Mr Fuller may give

the venture more drive.

Corporate Updates

9

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Budget airlines: load up: The largest UK-listed budget airlines, Ryanair and easyJet, have made a good business of digging away at the

foundations of the flag carriers. Both eroded the price of short-haul holiday flights, forcing larger airlines to adopt similar discounting. Next

easyJet, followed by Ryanair, took aim at the flag carriers’ business customers. By doing so, both found another rich vein of passengers.

Thursday’s November air traffic data, released by both companies, prompted Ryanair to upgrade its full-year earnings forecast. Share

prices of both reacted positively, with Ryanair up 8.0% and easyJet up 3.0%. One reason for the delight is the suggestion of less

seasonality in their businesses. November falls between holiday travel periods. Yet load factor (passengers as a proportion of available

seats) grew for both — Ryanair’s by seven percentage points. This despite having 13.0% more seats available than last year. Rising load

factors hint that pricing is relatively firm. The real reason to own these two airlines is their stronger return on capital, which is notable given

their lack of net debt. Their returns on invested capital (equity plus net debt) have consistently remained above larger rivals. The question is

whether the two can sustain these relatively high returns in the next couple of years, as their fleets expand further and they continue to take

on the bigger airlines.

Unilever: I can’t believe its not a spin-off: Margarine and other spreads are 7.0% of sales and although Unilever is taking market share, it

is a declining market. So the unit is a drag on growth. On Thursday, Unilever said it would put most of the spreads business into a

standalone unit so that a dedicated team can focus on turning it around. It is not, Unilever insists, the first step towards a full separation.

And the group’s management seems more enthusiastic about other parts of the empire. Over the past six years it has sold EUR2.80bn of

turnover, mainly in foods. Pasta sauces, peanut butter and diet drinks have all been shown the door. In the same period it has bought

EUR3.00bn of turnover, mainly in personal care. True, by spinning off foods Unilever would lose a cash machine that can fund growth

elsewhere, but with net debt (according to Jefferies) of just 1.00 times earnings before interest, tax, depreciation and amortisation, the group

has plenty of flexibility. Today the combined market capitalisation of the two companies is $100.00bn. The internal separation Unilever has

proposed looks like a messy halfway house, and raises questions about how committed the company is to food in general and spreads in

particular. It should dispel those questions, and be decisive.

Corporate Updates

10

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

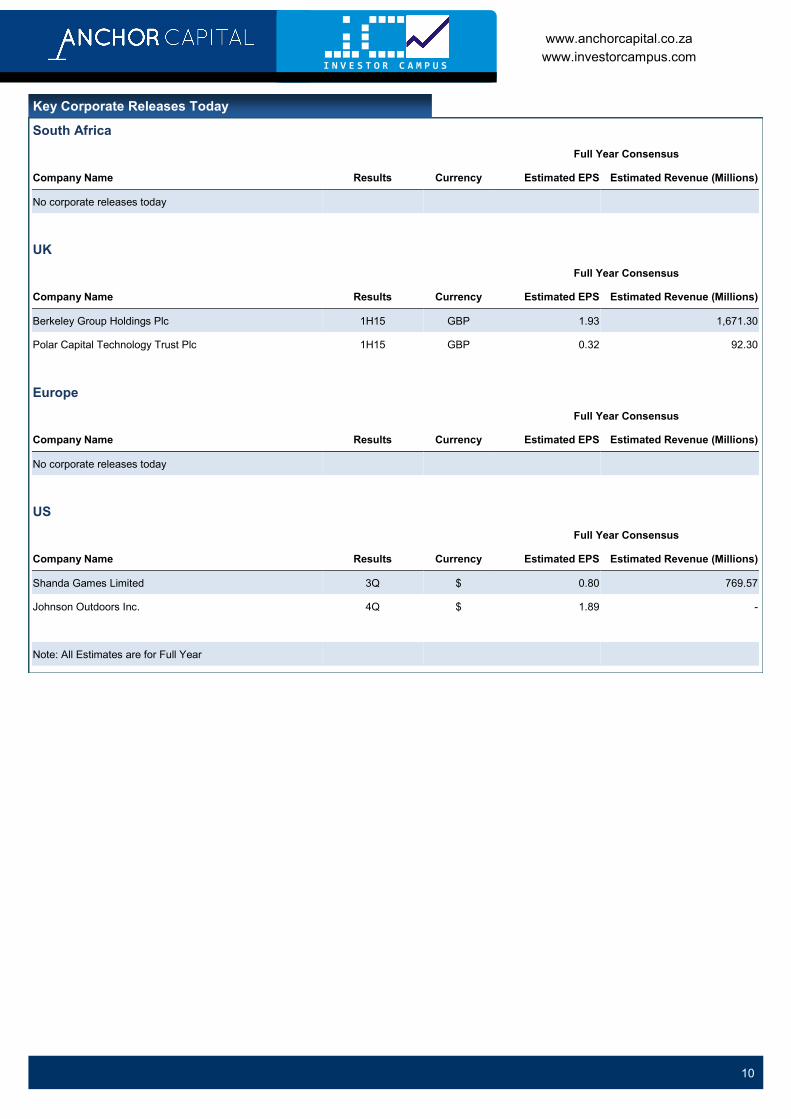

Key Corporate Releases Today

South Africa

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

No corporate releases today

UK

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

Berkeley Group Holdings Plc 1H15 GBP 1.93 1,671.30

Polar Capital Technology Trust Plc 1H15 GBP 0.32 92.30

Europe

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

No corporate releases today

US

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

Shanda Games Limited 3Q $ 0.80 769.57

Johnson Outdoors Inc. 4Q $ 1.89 -

Note: All Estimates are for Full Year

11

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

South Africa Ex-Dividend Calendar

Date Company Name Dividend Type Last Day to Trade Amount

- Afrimat Limited Interim 5-Dec-14 R0.13

- Ascendis Health Limited Final 5-Dec-14 R0.15

- Combined Motor Holdings Limited Interim 5-Dec-14 R0.33

- Country Bird Holdings Limited Return Prem. 5-Dec-14 R5.00

- Holdsport Limited Special Cash 5-Dec-14 R0.99

- Holdsport Limited Interim 5-Dec-14 R0.85

- Hosken Consolidated Investments Limited Spinoff 5-Dec-14 1.2003:1

- Hosken Consolidated Investments Limited Interim 5-Dec-14 R0.35

- Ingenuity Property Investments Limited Regular Cash 5-Dec-14 R0.03

- Insimbi Refractory and Alloy Supplies Limited Interim 5-Dec-14 R0.02

- Investec Australia Property Fund (IAP) Interim 5-Dec-14 R0.38

- Investec Limited (INL) Interim 5-Dec-14 R1.46

- Investec Plc (INP) Interim 5-Dec-14 GBP0.09

- Investec Property Fund Limited (IPF) Interim 5-Dec-14 R0.55

- Mr Price Group Limited Interim 5-Dec-14 R2.12

- Pick n Pay Stores Limited (PWK) Interim 5-Dec-14 R0.09

- Pick n Pay Stores Limited (PIK) Interim 5-Dec-14 R0.20

- Tsogo Sun Holdings Limited Interim 5-Dec-14 R0.29

12 Anchor Capital (Pty) Ltd (Reg no: 2009/002925/07). An authorised Financial Services Provider; FSP no: 39834

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Disclaimer

This report and its contents are confidential, privileged and only for the information of the intended recipient. Anchor Capital (Pty) Ltd and Ripple Effect 4

(Pty) Ltd make no representations or warranties in respect of this report or its content and will not be liable for any loss or damage of any nature arising

from this report, the content thereof, your reliance thereon its unauthorised use or any electronic viruses associated therewith. This report is proprietary

to Anchor Capital (Pty) Ltd and Ripple Effect 4 (Pty) and you may not copy or distribute the report without the prior written consent of the authors.

The business of money: Global asset management and

stockbroking

The business of knowledge: Financial education, information

and valuation services