investor day 2012: europe, middle east & africa

DESCRIPTION

Investor Day 2012: Europe, Middle East & AfricaTRANSCRIPT

REGION OVERVIEWEMEA

David JohnstonPresident & CEO EMEA

TOUGH MACRO ENVIRONMENT IN EUROPE

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Q3 Q4 2010Q1

Q2 Q3 Q4 2011Q1

Q2 Q3 Q4 2012Q1

Q2

%

GDP Growth

United Kingdom Italy Spain 0

1

2

3

4

5

6

7

8

Q3 Q4 2010 Q2 Q3 Q4 2011 Q2 Q3 Q4 2012 Q2

%

Bond Prices

United Kingdom Italy Spain

-35

-30

-25

-20

-15

-10

-5

0

Q3 Q4 2010 Q2 Q3 Q4 2011 Q2 Q3 Q4 2012 Q2

%

Consumer Confidence

United Kingdom

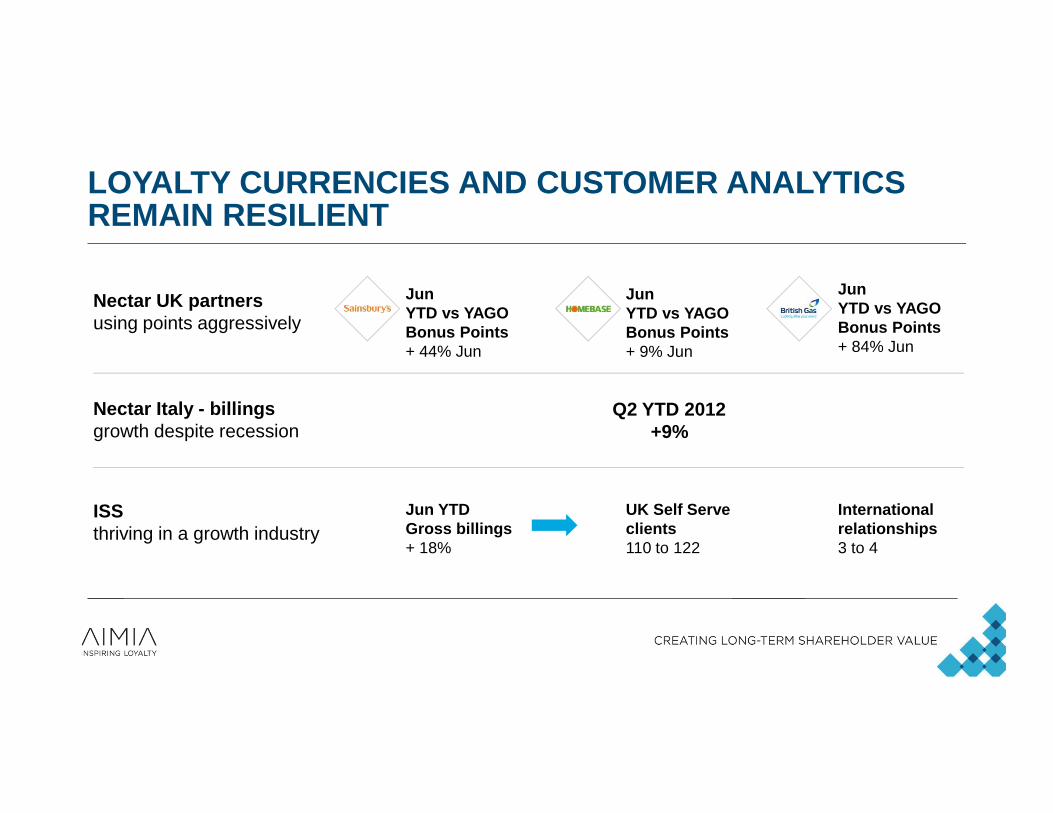

LOYALTY CURRENCIES AND CUSTOMER ANALYTICS REMAIN RESILIENT

Jun YTD vs YAGOBonus Points + 9% Jun

Jun YTD vs YAGOBonus Points+ 44% Jun

Jun YTD vs YAGOBonus Points + 84% Jun

Nectar UK partners using points aggressively

Nectar Italy - billings growth despite recession

ISS thriving in a growth industry

Q2 YTD 2012 +9%

UK Self Serveclients110 to 122

Jun YTDGross billings+ 18%

Internationalrelationships3 to 4

HELPING OUR CLIENTS BUILD STRONGER CUSTOMER RELATIONSHIPS

IMPROVING FINANCIAL PERFORMANCE

3.8%

7.4%

3.9%

5.2%

2010 2011 H1 2011 H1 2012

AEBITDA Margin %

AE Margin %

-19%

120%

55.9%

2010 2011 H1 2012

AEBITDA Growth

AEBITDA YOY% GrowthAEBITDA YoY% Growth

12.3%

5.1%

15.4%

21.5%

19.4%

13.0%

2011 Q12011 Q22011 Q32011 Q42012 Q12012 Q2

Gross Billings

YoY% Growth

2011 Q2 Q3 Q4 2012 Q2Q1 Q1

Adjusted for the impact of the VAT ruling, changes in the breakage rate, Italy launch costs and restructuring costsGB growth, AE% calculated in GBP; AE growth measured in Can$

DELIVERING ON OUR STRATEGIC PLAN

Renewals• Sainsbury’s• Homebase• HSBCExpanding coalition partners• British Gas• Original Marines• Unicredit

Mobile• Nectar, Sainsbury’s & BP

mobile apps• Location-based offersAnalytics• Enhanced Self Serve modules• Share of Wallet• Loyalty Self ServeCRM• Campaign Execution Tool• Offer engine

• VAT mitigated

• Improving leverage

• Strengthened commercials

STRENGTHEN CUSTOMER

RELATIONSHIPS

DRIVE INNOVATION

BUILD MARGINS

MOMENTUM FROM STRATEGY THROUGH TO EXECUTION

UK MEA OTHER

COALITIONLOYALTY

LOYALTYANALYTICS

PROPRIETARYLOYALTY

Jan-Pieter LipsMD Nectar

NECTAR

INCREASENECTAR’S

FOOTPRINT

DRIVE VALUE FORPARTNERS

GROWTHE MEMBER

BASE

MONETISEMEMBERSTHROUGH

INNOVATION

GROWTH DRIVERS OF THE NECTAR BUSINESS

LOYALTY PAYS 100% PARTNER RENEWAL IN THE LAST 18 MONTHS

11

SAINSBURY’S RENEWAL IN PARTICULAR SETS NECTAR UP FOR A PROFITABLE AND SUSTAINABLE FUTURE

“We have signed a new long-term contract with

Nectar to ensure we retain this source of

customer insight - a key competitive advantage”

JUSTIN KINGCEO Sainsbury’s

• Nectar at the core of Sainsbury’s marketing

• Joint Business Plan to drive value for both parties

• Contract renewal with improved terms

• Extended 7 year term

12

BRITISH GAS LAUNCH HAS EXCEEDED EXPECTATIONS AND DRIVEN GREAT RESULTS

“Our partnership with Nectar is delivering some great results.

55% of the customers that have joined us as a

result of Nectar fall within our highest value category and nearly two million of

our Nectar-collectors now self-serve, incentivised by points. Brand perceptions

have also benefited.”

WILL ORR, Marketing and insight director

CUSTOMERINCREASE

+2m

On-line account

INCREASE

+5

Net Promotor Score

13

ANNOUNCING OUR NEWEST PARTNER …

14

• Most visited retail website in the UK

• 17m unique monthly visitors

• Retail sales and peer to peer

• ‘Elephant’: top-5 partner

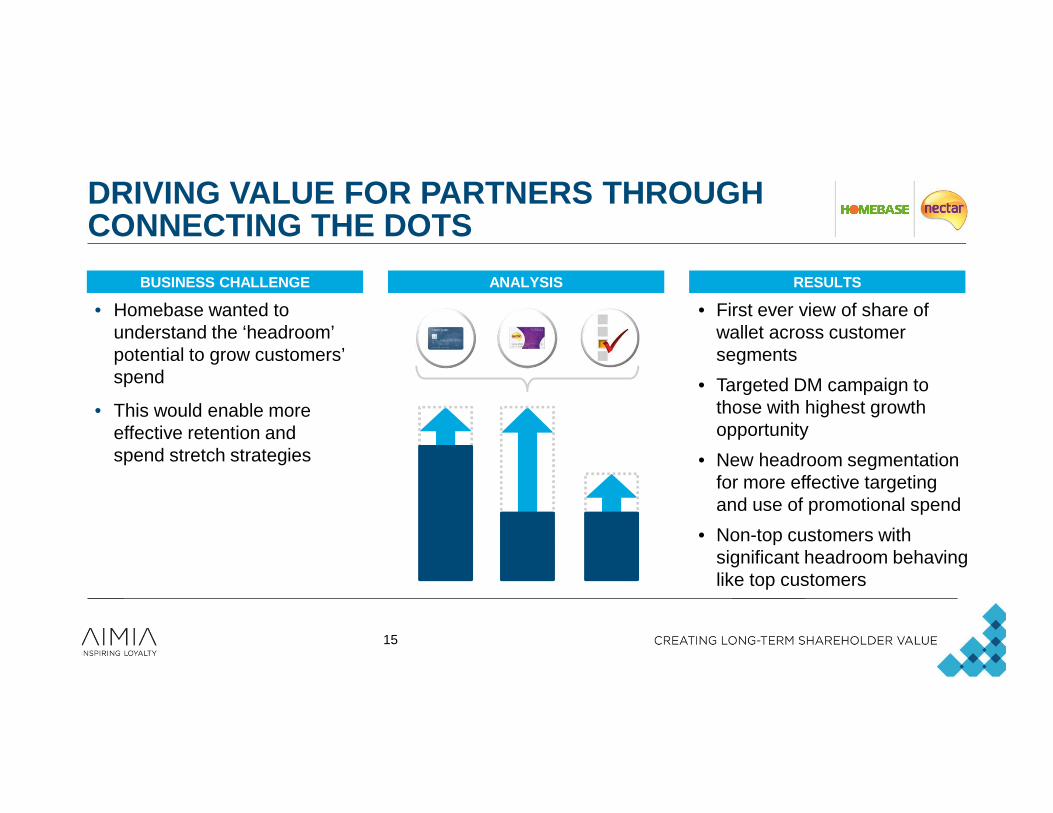

DRIVING VALUE FOR PARTNERS THROUGH CONNECTING THE DOTS

BUSINESS CHALLENGE ANALYSIS RESULTS

• Homebase wanted to understand the ‘headroom’ potential to grow customers’ spend

• This would enable more effective retention and spend stretch strategies

• First ever view of share of wallet across customer segments

• Targeted DM campaign to those with highest growth opportunity

• New headroom segmentation for more effective targeting and use of promotional spend

• Non-top customers with significant headroom behaving like top customers

15

WE’VE HAD A MAJOR FOCUS ON INNOVATION OF MEMBER INTERACTION

16

AND WE’RE TESTING A DEALS PROPOSITION TO FURTHER MONETISE OUR MEMBER BASE

17

WE’RE MOVING WELL BEYOND THE TRADITIONAL ‘TRANSACTION’ MOMENT INTO ‘INTERACTIONS’

RESEARCH

PRE-PURCHASE

PURCHASE

POST-PURCHASE

AWARENESS

Interactions

18

NECTARS MOMENTUM IS CLEARLY VISIBLE IN OUR METRICS

15.5m

18.5m

16.1%

20.7%

2.2m

4m

75%

83%

19

INCREASENECTAR’S

FOOTPRINT

DRIVE VALUE FORPARTNERS

GROWTHE MEMBER

BASE

MONETISEMEMBERSTHROUGH

INNOVATION

GROWTH DRIVERS OF THE NECTAR BUSINESS

20

21

ISSNEW BUSINESS with Sainsbury’s

Peter GleasonPresident ISS

SHOPPER MARKETING IS A KEY STRATEGY FOR DRIVING SALES

• Shopper marketing is about understanding how target consumers behave as shoppers throughout the total purchase journey

• ISS services currently provide the core of shopper marketing understanding and execution• The growth of shopper marketing as a whole continues at a fast pace

ISS IS WELL POSITIONED TO CAPITALISE ON SHOPPER MARKETING GROWTH

OUR INSIGHT OFFERING AND TARGETED MEDIA CHANNELS ARE GROWING STRONGLY

Targeted media channels utilise customer data colle cted via loyalty cards to deliver relevant, timely offers to shoppers on a one to one basis

EXAMPLES INCLUDE:-

The targeted nature of these comms enables the evaluation of campaign ROI – we know who was issued with offers and we can accurately track redemption rates

Used intelligently, targeted comms facilitate the building of highly valued relationships between retailer and customer

COUPON AT TILL DIRECT MAIL MOBILE

Our insight tools and capabilities utilise customer data collected via loyalty cards to deeply understa nd customer purchasing behaviour

EXAMPLES INCLUDE:-

The speed and flexibility of our primary insight tool, Self Serve, is widely recognised in the market place. This is complemented by a growth in our offering of insight advisory and consultancy services

SELF SERVE INSIGHTS CONSULTANCY

NON-TARGETED MEDIA INCLUDES OVER 20 CHANNELS

Non targeted channelsare more of a mass communication vehicle and customer data is not currently used in deployment

Traditional channels include:

IN STORE

AROUND THE STORE

AT HOME

THE NEXT GENERATION OF ISS IS UPON US

• We are creating a new business in the UK with Sainsbury’s that will accelerate the overall growth of ISS

• This new business is a natural development for our relationship with Sainsbury’s

• The partnership opens up lots of exciting new opportunities including

– New store targeted media channels

– A streamlined buy in process for CPGs

– Closer alignment with Sainsbury's strategic plan

• Long term revenue and profit growth is significantly enhanced by this new partnership

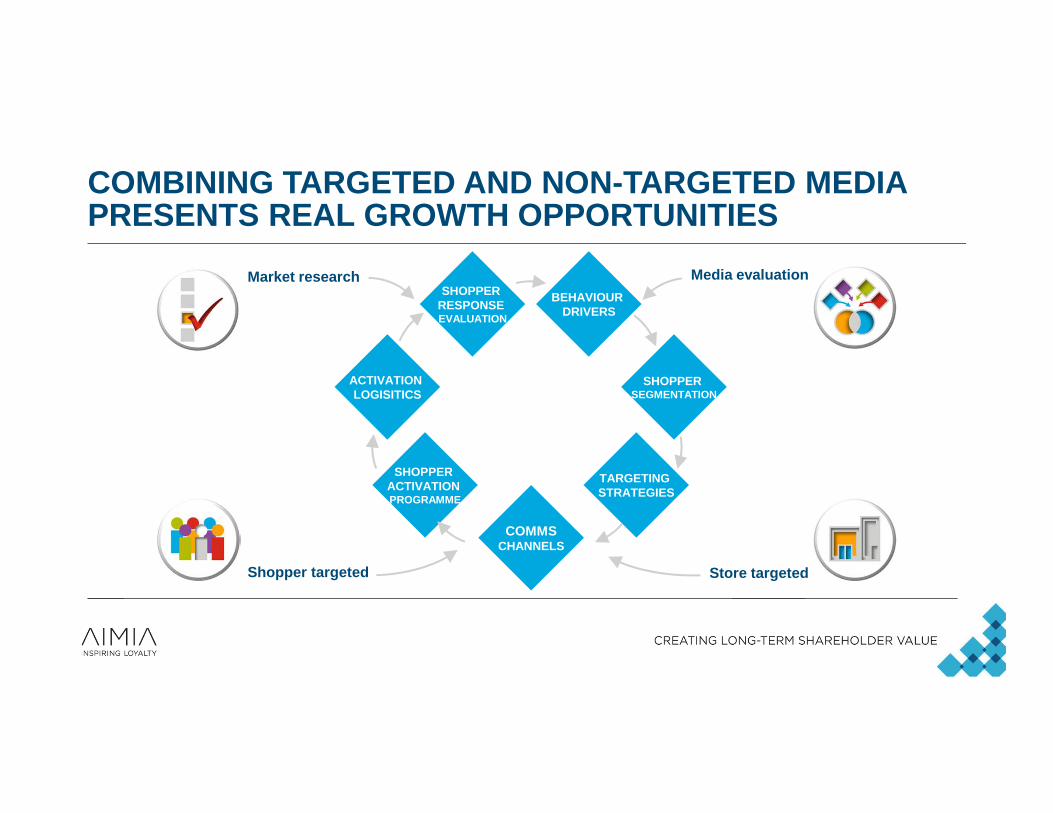

COMBINING TARGETED AND NON-TARGETED MEDIA PRESENTS REAL GROWTH OPPORTUNITIES

Shopper targeted Store targeted

BEHAVIOUR DRIVERS

SHOPPER SEGMENTATION

TARGETING STRATEGIES

COMMSCHANNELS

SHOPPER ACTIVATION PROGRAMME

ACTIVATION LOGISITICS

SHOPPER RESPONSE EVALUATION

Media evaluationMarket research

AIMIA, SAINSBURY’S, CPGs AND SHOPPERS ALL BENEFIT AS A RESULT OF THIS NEW PARTNERSHIP

Stronger relationship with Sainsbury’s and supply of wider range

of services whilstretaining IP

Stronger relationship& communications

with customers; capitalise on market growth opportunity

Unique opportunity

to drive ROI via integrated campaigns

Faster, more relevant environment

WE HAVE GROWN OUR INTERNATIONAL PRESENCE AND CONTINUE TO BUILD OUR GLOBAL BUSINESS

• ‘Store of the future’

• Category planning

• Coles Express

• Offer Engine

• Strategic consulting

• Fully launched

• Over 185 Sobeys users

• 12 CPG suppliers already signed up

• Customer Self Serve

• Embedded Self Serve into Category Management

• Review of commercialisation opportunities

REGION OVERVIEWEMEA

David JohnstonPresident & CEO EMEA

20 Sept 2012

NECTAR ITALIA DELIVERING RESULTS IN A TOUGH ENVIRONMENT

ITALY JUN 2012

GDP growth (0.7)%

Bond Yield 5.8 %

Unemployment 10.8 %

DELIVERY FOR PARTNERS

• Highest spontaneous awareness in market

• Newly acquired customers driving 1-3% Y1 sales growth

DELIVERY FOR MEMBERS

• Engagement – 12 cards swiped every second

• Customer Satisfaction 8.2/10

• Over €50m of rewards distributed to members

MIDDLE EAST SUCCESSFUL PROGRAMME RELAUNCH

AIR MILESMIDDLE EAST 2012 Q2

Change YoY

Points issuance(millions) 13.7%

Gross Billings +AED 24m

PROPRIETARY FOCUSED ON LOYALTY - EUROPE

PROPRIETARY FOCUSED ON LOYALTY - MIDDLE EAST

Saudi Arabia’s largest

Leisure & Hospitality

Loyalty Program

Qatar’s largest

Telecom Loyalty

Program

MOMENTUM FROM STRATEGY THROUGH TO EXECUTION

UK MEA OTHER

COALITIONLOYALTY

LOYALTYANALYTICS

PROPRIETARYLOYALTY

THANK YOU