investor presentationibtplc.com/wp-content/uploads/2016/07/international-biotechnology... ·...

TRANSCRIPT

Investor

PresentationThis document has been issued in the UK by SV Health Managers LLP

(authorised and regulated by the Financial Conduct Authority), and may

only be distributed to persons falling within the definition of authorised

persons, investment professionals or high net worth bodies as defined

in the Financial Services & Markets Act 2000.

2017

2

This document is issued for information purposes only by SV Health Managers LLP who is authorised and regulated by the Financial Conduct

Authority (“FCA”). It does not constitute an offer by SV Health Managers LLP to enter into any contract/agreement nor is it a solicitation to buy,

sell, hold or subscribe for any investment. Nothing in this document should be deemed to constitute the provision of financial, investment or

other professional advice in any way. The contents of this document are based upon sources of information believed to be reliable, however,

save to the extent required by applicable law or regulations, no guarantee, warranty or representation (express of implied) is given as to its

accuracy or completeness and SV Health Managers LLP , its members, officers and employees of the managing member do not accept any

liability or responsibility in respect of the information or any views expressed herein. Holdings are subject to change and should not be

construed as research or investment advice. Similarly, any reference to a specific company does not constitute a recommendation to buy, sell,

hold or subscribe in any company or its securities.

Prospective investors should inform themselves as to any applicable legal requirements, taxation and exchange control regulations in the

countries of their citizenship, residence or domicile which might be relevant. Past performance is not indicative of future results, which may vary.

The value of investments and the income derived from investments can go down as well as up. Future returns are not guaranteed, and a loss of

principal may occur.

All views expressed in this document are current as of the date of this presentation and may be subject to change. No part of this material may,

without SV Health Managers prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any

person that is not an employee, officer, director, or authorised agent of the recipient.

Copyright © 2017, SV Health Managers LLP . All rights reserved.

Disclaimer

3

Agenda

Introduction and management team

Biotech sector

International Biotechnology Trust

4

Introduction

Award winning

closed end

fund

Biotechnology

Sector focused

Yield and capital

growth

Adding value through active

management

Managed by

specialist experts

Diversified

portfolio

Investment and Wealth

Management Awards 2015

Cumulative Return Return Return Return

31 August 2017 1 YR 2YR 3YR

IBT Cum NAV (GBP) (adjusted for dividend) 20.9% 75.7% 199.1%

NASDAQ Biotechnology Index (GBP) 21.7% 57.0% 208.3%

Source: Bloomberg and SV Health Managers LLP

NAV=GBP252M, 31 August 2017

Geography

Market Cap

5

Management Team

Ailsa Craig

Investment Manager

BSc

10 years healthcare investing,

3 years analyst

Previously, at Baring Asset

Management as a research analyst,

and Insight Investment / Rothschild

Asset Management (merged 2003)

within the Global/US investment

team

Dr Carl Harald Janson

Lead Investment Manager

CEFA, PhD, Medical Doctor

13 years healthcare investing,

7 years pharmaceuticals industry

experience

Prior Carnegie Asset Management,

Danske, H&Q, KD, Astra

Five year performance record at

Carnegie Asset Management;

Carnegie Biotechnology Fund +115%,

NBI +1%. Bloomberg rated it as the

top performing fund out of 40 peers

worldwide, for the 6 years and

3 months that Carl Harald Janson was Principal Fund Manager

Kate Bingham

Investment Manager

MBA

25 years healthcare investing

Kate has a first class degree in

Biochemistry from Oxford University

and graduated from Harvard

Business School with an MBA (Baker

Scholar)

Previously Kate worked in business

development for Vertex

Pharmaceuticals, a biotechnology

company in Cambridge, MA and at

Monitor Company, a strategy

consulting firm

6

SV Health Investors

One of the world’s leading dedicated life sciences investors

Founded 1993

100% focused

on healthcare

USD 2.4bn raised in seven venture funds

External recognition, through winning the

Dementia Discovery Fund in a highly competitive

process

55 staff worldwide

USD 2.4bn raised in seven SV venture funds

GBP 145m raised by Dementia Discovery Fund

Based in SV’s busy London office, International Biotechnology

Trust is a significant part of SV, which has advised or managed it

since 2001

Global reach

- Boston, San Francisco and London Offices

Over 70 live venture investments in

Healthcare, Biotechnology and Medical Devices

11PhD’s, 7MD’s, 13MBA’s

- Oncology, Molecular biology, Neuroscience,

Neuropharmacology, Physiology, Biochemistry, Chemistry

External recognition, through winning the Dementia Discovery Fund in a highly competitive process

7

Agenda

Introduction and management team

Biotech sector

International Biotechnology Trust

8

Biotech is a high growth sector

Source: Bloomberg

13.08% y/y

NASDAQ Biotech

Index (NBI)

6.33% y/y MSCI

World Equity Index

(MXWO)

NASDAQ biotech index has consistently outperformed the world equity and healthcare indices

8.38% y/y MSCI

World Healthcare

Index (MXWO0HC)

Biotech return 13% yoy over

the last 20 years

2017

9

Demand is growing

and so is innovation

Increasingly elderly population

%

Source: US Census Bureau – Worldwide population

0

10

20

30

40

50

60

70

80

90

100

2008 2040

>65 years <65 years

7%

Disclosed Worldwide Active R&D Projects in Development by Stage

Source: Pharmaceutical Research and Manufacturers of America (PhRMA),

Pharmaprojects, Bank of America Merrill Lynch Global Research

Phase 2

More drugs in development

Phase 3

*N.B. Most large pharmaceutical companies do not

disclose all their phase 1 programs due to “lack of

materiality”.2100

1800

1500

1200

900

600

300

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Phase 1

14%

10

Charts for US "Mega LC" Biotech Include: GILD AMGN CELG BIIB + GENZ DNA IMNX MEDI CHIR before acquisition

Source: EvercoreISI

P/E

Why buy now?

Mega Large Cap (>USD50bn) Biotech – 10 Year Next 12 Months P/E

Now is one of the few opportunities in the last decade to buy mega cap biotech companies at below the market

AMGN

BIIB

CELG

*(GILD)

S&P500

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

6/9

/201

7

6/2

4/2

016

7/1

0/2

015

7/2

5/2

014

8/9

/201

3

8/2

4/2

012

9/9

/201

1

9/2

4/2

010

10/9

/20

09

10/2

4/2

008

11/9

/20

07

US LC Biotech (Mean) w/o GILD US MegaLC Biotech (Mean) S&P500

11

M&A a constant theme

Over the past three years, 13 companies in International Biotechnology Trust’s portfolio have been acquired

(five in 2016/2017)

0

50

100

150

200

250

300

350

400

450

500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Average 320

events/year

Announced M

&A

tra

nsactio

ns

Source: ‘Life Sciences Dealmaking 2015’ Thomson Reuters

Volume of announced life sciences industry-wide M&A events by year

30 – 60%

premium

Premiums for listed U.S and European Biopharma Companies

42%

49% 49%

61%

50%

43%

69%

53%

33%

55%

36%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Avera

ge P

rem

ium

s P

aid

*

Source: HBM Pharma/Biotech M&A Report 2016

*US Deals, no data for European

2015

Big pharma and big biotech have accrued significant cash reserves which they may deploy

12

Drug pricing

11% of Federal healthcare spending is on therapeutic drugs

Source: Avalere Health, Piper Jaffray, Organisation for Economic Co-operation and Development

Hospitals 42%

Physicians 19%

Brand Drugs 9%

Generic drugs 2%

Nursing homes 7%

Home health 6%

Professionals 2%

Durable Medicals Equipment 1% Other 11%

Estimated Distribution of U.S. Federal Spending on Healthcare 2015-2024

Political debate on drug pricing is ebbing away

Republicans appear to be ‘industry friendly’

Major changes are not expected

• Innovation drugs will continue to command premium prices

• Price increases on marketed drugs will be capped

• Generic drug pricing will remain under pressure

13

Agenda

Introduction and management team

Biotech sector

International Biotechnology Trust

14

Performance – 1, 3, 5 years

*

Cumulative Return to 31 August 2017 12m (%) 3yr (%) 5yr (%)

International Biotechnology Trust Share Price Total Return (GBP) 30.5 106.5 217.6

International Biotechnology Trust NAV (adjusted for dividends) (GBP) 20.9 75.7 199.1

Quoted* 31.2 81.6 242.7

NASDAQ Biotechnology Index (GBP) 21.7 57.0 208.3

S&P 500 (GBP) 18.5 69.0 140.4

FTSE All-Share (GBP) 14.4 24.8 63.7

FTSE 100 (GBP) 14.0 22.3 57.0

Source: Bloomberg and SV Health Managers LLP

*excludes fees

International Biotechnology Trust has outperformed vs its benchmark in rising and falling markets

Lead fund manager (Carl Harald Janson) started in September 2013

*See table on page 8 of the annual report for definition of “unquoted” portfolio. This part of the portfolio was 10.8% of NAV at the period end.

The remainder of the portfolio (89.2% of NAV) is the “quoted” portfolio.

15

Results

12 months to 31 August 2017

International Biotechnology Trust returns

• Share price returned 30.5%, NAV/share returned 20.9% versus 21.7% NASDAQ Biotech Index (GBP)

• Discount narrowed from 13.5% to 7.3%, using cum NAV

• Quoted* return of 31.2% & unquoted* return of (25.7)%

Contributors

• Positive contributors: Exelixis GBP 7.1M, Vertex GBP 6.6M, Ariad GBP 6.5M, Incyte GBP 5.9M,

and Tesaro GBP 5.5M

• Negative contributors: Shire GBP (2.0)M, Reshape Medical GBP (1.5)M, EBR Systems GBP (1.3)M,

OncoEthix GBP (1.2M), and Kalvista GBP (1.2)M

Other

• Currency – positive impact of GBP 5.4M

• Turnover 199% annualised

• Gearing at the beginning of the period (31 August 2016) was -6%, end of period (31 August 2017) was -2%,

range over period (-7% to 5%)

*See table on page 8 of the annual report for definition of “unquoted” portfolio. This part of the portfolio was 10.8% of NAV at the period end.

The remainder of the portfolio (89.2% of NAV) is the “quoted” portfolio.

16

Dividend up 17.4% y-o-y*

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

1997 2000 2003 2006 2009 2012 2015

UK Base Rate in last 20 years

Source: Bank of England ‘Statistical Interactive

Database - official Bank Rate history’

Source: SV Health Managers LLP

%

– Response to current low yield environment

– In 2016, a dividend of 4% of NAV introduced

– Met out of capital reserves, without affecting investment strategy

– Proposed dividend represents a rise of 17.4% above previous

year

Year ended Aug 16 Proposed for Year ended Aug 17

First Interim

Dividend

Second Interim

Dividend

First Interim

Dividend

Second Interim

Dividend

Amount 11.5p 11.5p 13.5p* (+17.4%) 13.5p*

Declared 13 Dec 16 12 Jul 17 At AGM*

Ex-Div Date 07 Jan 17 04 Aug 17 05 Jan 18*

Payment date 31 Jan 17 31 Aug 17 31 Jan 18* 31 Aug 18*

* Subject to Shareholder Approval at AGM in Dec 17

Source: SV Health Managers LLP

17

Profitable 51%

Revenue 23%

Development Stage 26%

Source: SV Health Managers LLP

Geography

Portfolio breakdown

Stage

US & Canada 85%

Europe & UK 15%

>USD30BN 40%

USD5-30BN 20%

USD1-5 BN 18%

USD500M-1BN 8%

<USD500M 14%

Market cap

31 August 2017, NAV GBP 252M

Therapeutic areas

Oncology 33%

Rare Diseases 14%

Neurology/Psychiatry 12%

Infectious Diseases 11%

Ophthalmology 8%

Inflammation 7%

Metabolic Disorders 5%

Medtech 2%

Other 8%

18

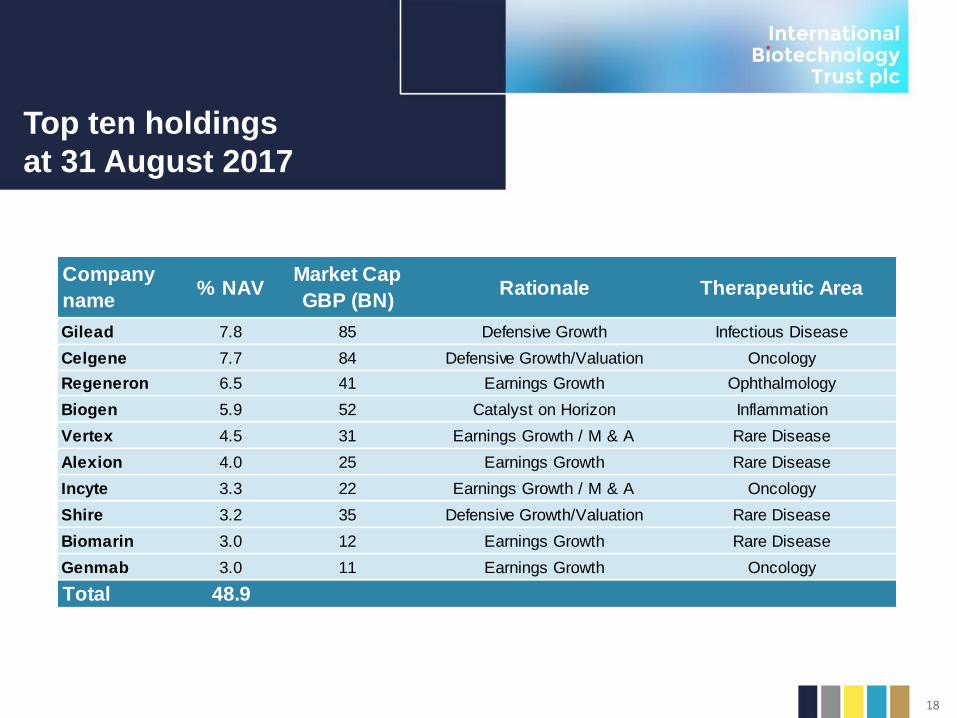

Top ten holdings

at 31 August 2017

Company

name% NAV

Market Cap

GBP (BN) Rationale Therapeutic Area

Gilead 7.8 85 Defensive Growth Infectious Disease

Celgene 7.7 84 Defensive Growth/Valuation Oncology

Regeneron 6.5 41 Earnings Growth Ophthalmology

Biogen 5.9 52 Catalyst on Horizon Inflammation

Vertex 4.5 31 Earnings Growth / M & A Rare Disease

Alexion 4.0 25 Earnings Growth Rare Disease

Incyte 3.3 22 Earnings Growth / M & A Oncology

Shire 3.2 35 Defensive Growth/Valuation Rare Disease

Biomarin 3.0 12 Earnings Growth Rare Disease

Genmab 3.0 11 Earnings Growth Oncology

Total 48.9

19

Buybacks

Source: Bloomberg

NAV/Share

Share price

Discount

Buybacks

Dividend announced

20

Cash/Gearing

Investment process

Investment

Process

Risk Mitigation News Flow

Management

DCF Valuation M&ASell Discipline

Medical/Investment

Conferences

Actively managing investments in shares

with high risk news events

VIX

21

Awards

2015 UK Tech Awards ‘Best Tech Fund Manager’

2015 Investor Chronicle Financial Times ‘Best Specialist Fund’

2016 Most Significant Contribution Kate Bingham

Investment and

Wealth Management

Awards 2015

2017 BIA Lifetime Achievement Award Kate Bingham

2017 Citywire Investment Trust Awards ‘Best Specialist Equities’

22

Summary

Biotech sector has strong fundamentals but is currently undervalued

Top performing trust in sector, outperforming in rising and falling markets

Access to full spectrum of quoted and unquoted biotech companies

Exposure to both growth and yield

Unique approach to risk mitigation

Support and expertise from leading industry players at SV Health Investors