investor presentation - ahipreit.com · 5 well positioned for the economic environment daily...

TRANSCRIPT

Investor PresentationTSX: HOT.UN (CAD$) TSX: HOT.U (US$) TSX: HOT.DB.U (Debentures)

March 2018 (Q4 2017 Information)

Forward Looking StatementsThis corporate update is a summary and should be read together with the more detailed information, financial data and statements made available by American Hotel Income Properties REIT LP (the “REIT”). This corporate update contains forward-looking statements which reflect management’s expectations regarding objectives, plans, goals, strategies, future growth, results of operations, performance and business prospects and opportunities of the REIT. The words “plans”, “expects”, “scheduled”, “estimates”, “intends”, “anticipates”, “projects”, “believes” or variations of such words and phrases or statements to the effect that certain actions, events or results “may”, “will”, “could”, “would”, “might”, “occur”, “be achieved” or “continue” and similar expressions identify forward-looking statements. Some of the specific forward- looking statements in this corporate update include, but are not limited to, statements with respect to the ability of the REIT to execute its growth strategies; the expected tax treatment of the REIT and of the REIT’s distribution to Unitholders; the expected growth in the U.S. lodging industry and trends; and other considerations which are outlined in the REIT’s Annual Information Form dated March 27, 2017. Forward-looking statements are necessarily based on a number of estimates and assumptions that, while considered reasonable by management of the REIT as of the date of this corporate update, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The REIT’s estimates, beliefs and assumptions, which may prove to be incorrect, include the various assumptions set forth herein, including, but not limited to the REIT’s future growth potential, results of operations, future prospects and opportunities, industry trends remaining unchanged, no change in legislative or regulatory matters, future levels of indebtedness, the tax laws as currently in effect remaining unchanged, the continual availability of capital and the current economic conditions remaining unchanged. When relying on forward-looking statements to make decisions, the REIT cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not the times at or by which such performance or results will be achieved. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements, including, but not limited to, the factors discussed under the “Risk Factors” in the REIT’s latest Management’s Discussion and Analysis. The forward-looking information contained herein is made as of March 15, 2018 and, except as expressly required by applicable law, the REIT assumes no obligation to publicly update or revise such information.

All figures presented are in U.S. dollars, unless otherwise stated.

3

Company Overview

115 Hotels; 11,708Rooms

33States; 92 Cities

53.9% Debt-to-Gross Book Value

10.0% Yield

American Hotel Income Properties REIT LP (“AHIP”)

▪ Invests in high-quality premium branded hotel properties, primarily in the Upscale to Upper-Upscale chains, including such brands as Residence Inn (by Marriot), Hampton Inn and Suites (by Hilton) and Holiday Inn Express (by IHG).

▪ Hotel properties are located across the U.S. , primarily in secondary markets (such as Cincinnati or Baltimore) that benefit from multiple demand generators, including business parks, sports arenas, medical centres, universities and interstates/airports

▪ In addition, AHIP’s Economy Lodging portfolio provides accommodations for guests in more remote locations and caters to the lodging needs of railway crews along major rail lines.

Properties are purchased with an average 8% cap rate using long-term fixed-rate debt that averages 4.61%.

AHIP provides a $0.051 USD monthly cash distribution to unitholders, equivalent to USD $0.648 per unit on an annualized basis.

▪ All units receive USD cash distributions, regardless of whether the units were purchased using our Canadian dollar listing (TSX: HOT.UN) or USD listing (TSX: HOT.U, OTC:AHOTF)

Equivalent to a 10% yield¹ - one of the highest in the Canadian and US REIT sector

The increasing value of the US dollar relative to the Canadian dollar benefits Canadian unitholders

▪ AHIP generates its revenue and income in USD, and provides its monthly cash distribution to unitholders in USD.

▪ Canadian investors have benefited from a 3.9% increase in the USD relative to the Canadian dollar since January 1, 2018²

Monthly USD cash distributions

4(1) Based on March 15, 2018 HOT.UN trading price of $8.05 CAD(2) 1.2517 USD/CAD rate as of Jan 1, 2018 to 1.3010 USD/CAD on March 15, 2018

American Hotel Income Properties trades in both the Canadian dollar (HOT.UN) and U.S. dollar (HOT.U) on the TSX. Regardless of which ticker unitholders invest through, AHIP provides its monthly cash distributions in U.S. dollars.

5

Well positioned for the economic environment

Daily guestroom rates can change daily, to mitigate any inflationary risk

▪ Unlike other REIT sectors where revenue is derived from long-term leases, hotel REITs provide anatural inflationary hedge due to the daily pricing adjustments of guestroom rates

▪ Revenue management allows our hotel manager to price rooms inventory according to daily changes in demand and room rate trends

Long-term, fixed rate debt structure shields AHIP from short-term changes in interest rates

▪ AHIP has an average term remaining on its mortgages of 7.6 years, and a weighted average loan face interest rate of 4.61%

▪ No significant debt maturities until June 2022

$0

$50

$100

$150

$200

$250

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

DEBT MATURITY LADDER (millions) Mortgages Convertible Debentures

Driving long-term returns and cash flow

Driving RevPAR (Revenue per available room) growth through:

▪ Revenue management (demand management)

▪ Hotel upgrades and renovations (PIP projects)

▪ Enhanced marketing and distribution (through brand partners such as Wyndham Hotel Group)

Investing in our hotels to make them best in class and drive higher market share and demand

▪ $20 million of pre-funded hotel upgrades/renovations (referred to as Property Improvement Plans, or PIPs) scheduled to occur during 2018

▪ Additional $10+ mil of PIP projects to occur in 2019

▪ By the end of 2020, 81% of AHIP’s Premium Branded hotels will have been recently renovated

Have introduced an internal asset management team

▪ Department is charged with overseeing and enhancing the performance of the hotel portfolio to drive strongerreturns for unitholders

▪ Working closely with AHIP’s external hotel manager, the Asset Management team monitors the supply and demand dynamics of specific hotel markets to ensure that each property is consistently well positioned to maximize profitability

▪ Developing long-term strategic plans for each hotel property, including all hotel upgrades and PIP projects

6

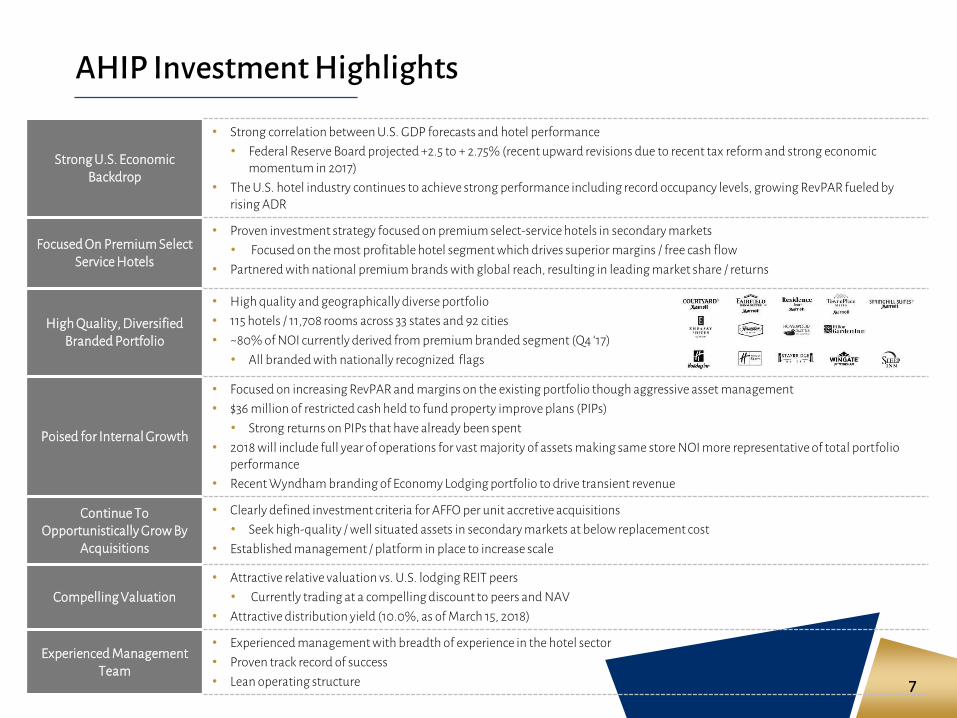

AHIP Investment Highlights

7

Strong U.S. Economic Backdrop

• Strong correlation between U.S. GDP forecasts and hotel performance

• Federal Reserve Board projected +2.5 to + 2.75% (recent upward revisions due to recent tax reform and strong economic momentum in 2017)

• The U.S. hotel industry continues to achieve strong performance including record occupancy levels, growing RevPAR fueled by rising ADR

Focused On Premium Select Service Hotels

• Proven investment strategy focused on premium select-service hotels in secondary markets

• Focused on the most profitable hotel segment which drives superior margins / free cash flow

• Partnered with national premium brands with global reach, resulting in leading market share / returns

High Quality, Diversified Branded Portfolio

• High quality and geographically diverse portfolio

• 115 hotels / 11,708 rooms across 33 states and 92 cities

• ~80% of NOI currently derived from premium branded segment (Q4 ‘17)

• All branded with nationally recognized flags

Poised for Internal Growth

• Focused on increasing RevPAR and margins on the existing portfolio though aggressive asset management

• $36 million of restricted cash held to fund property improve plans (PIPs)

• Strong returns on PIPs that have already been spent

• 2018 will include full year of operations for vast majority of assets making same store NOI more representative of total portfolio performance

• Recent Wyndham branding of Economy Lodging portfolio to drive transient revenue

Continue ToOpportunistically Grow By

Acquisitions

• Clearly defined investment criteria for AFFO per unit accretive acquisitions

• Seek high-quality / well situated assets in secondary markets at below replacement cost

• Established management / platform in place to increase scale

Compelling Valuation

• Attractive relative valuation vs. U.S. lodging REIT peers

• Currently trading at a compelling discount to peers and NAV

• Attractive distribution yield (10.0%, as of March 15, 2018)

Experienced Management Team

• Experienced management with breadth of experience in the hotel sector

• Proven track record of success

• Lean operating structure

Strong U.S. Economic Backdrop

• U.S. tax reform expected to drive further GDP growth

• Oxford Economics sees a +0.4% increase to GDP from tax reform alone, bringing their forecast 2018 U.S. GDP growth to 2.8%

• Tax reform expected to drive increased demand and U.S. hotels and corresponding gains in guest spending².

• Gains are expected to exceed those for the broader economy as both leisure and corporate travel more directly benefit from increased consumer and corporate spending²

• STR forecasts for 2018¹:

• ADR increase of +2.4%

• Revenue per available room growth of + 2.7%

• Increased supply across most markets will be largely offset by strong occupancy forecasts

• Potential for inflation

• AHIP could have opportunity to raise ADR each night (‘rent’ is determined real time considering supply/demand and economic factors)

8¹ STR Forecasts provided in January 2018² Oxford Economics (parent company of Tourism Economics), data a result of an analysis completed for the American Hotel and Lodging Association

Quality Branded Hotel Portfolio

• AHIP has strategically grown its portfolio since IPO with a focus on increasing the quality and size of the assets that it owns, purchasing hotels in larger markets and geographically diversifying its asset base

9

HOTEL PORTFOLIO EVOLUTION

Portfolio composition (by NOI)

RevPAR $46.38¹ $71.20

ADR $53.87¹ $95.32

Portfolio size 32 hotels / 2,565 rooms 115 hotels / 11,708 rooms

Average # of rooms per hotels 80 115

Average value per hotel $4.9 million $14.4 million

AT TIME OF IPO TODAY (Annual, or as at Dec. 31, 2017)

¹ As disclosed at IPO

Premium Branded

Economy Lodging

Rail Hotels

100% Rail80%

20%

Brand Diversity

10

World-class brand partners with global distribution, effective brand segmentation, guest loyalty programs and premier system standards

• Strong national and regional sales, revenue management and operational teams to drive increased revenue

• External hotel management team with extensive experience to drive margin growth

• Capital reinvestment and asset preservation to increase market share and long-term value creation

67 Premium Branded hotels; 7,684 guestroomsNOI, 80%

NOI, 20%

Premium Branded Hotels

Economy Lodging Hotels

*Net Operating Income (NOI) for Q4 2017

PREMIUM BRANDED HOTELS COMPRISE 80% OF OUR NOI*

46 Economy Lodging hotels; 4,024 guestrooms¹

Favourable contract terms

• Royalty fee carveouts related to AHIP’s existing rail crew contract revenue• Advantageous fee schedule for first several years of the 15-year contract

Many benefits to drive stronger performance at AHIP’s Economy Lodging hotels

• Expect to draw more transient guests

• Stronger brand recognition

• Access to Wyndham’s worldwide reservations network

• Ability to offer guests access to Wyndham’s award-winning rewards program

• Ability to drive higher occupancy for rooms otherwise not used by rail crew contract guests

On Nov. 1, 2017, AHIP announced an agreement to rebrand 46 (all) of our Economy Lodging Hotels under Wyndham hotel brands

PREMIUM BRANDED HOTELS BRANDS

ECONOMY LODGING HOTELS BRANDS

¹ Additional two properties owned are not currently open

Why U.S. Secondary Markets? Why Select Service Hotels?

11

0.0 1.0 2.0 3.0 4.0 5.0

Primary Secondary Markets

Economic Outlook

• GDP forecasts are the highest correlation to performance of the U.S. hotel industry

• The U.S. Federal Reserve Board projects 2.5% to2.75%+ GDP growth in 2018; Oxford Economics projects 2.8% growth

• The U.S. hotel industry continues to achieve strong performance including record occupancy levels, growing RevPAR fueled by rising ADR

Area of Opportunity3.4M guestrooms

U.S.

Canada

U.S. Secondary Markets

• Includes cities such as Cincinnati and Baltimore

• 3.4 million guestrooms (vs 1.6 in Primary markets)

• Deep pipeline of high quality assets

• Strategically located within or near large population centres (>2M pop.), transportation corridors and demand generators

Select Service Hotel Advantages

• Strong consumer demand and broad appeal

• Simple, efficient operational model

• Higher margins with lower volatility

Million guestrooms

400,000 guestrooms

1. Source: CBRE Hotels’ Americas Research - Hotel Horizons® March 2017 – May 2017, STR2. Source: STR Inc., Tourism Econometrics

Top 6 Cities

Top 25 Cities

GUESTROOMS BY COUNTRY / MAJOR CITIES

Poised for Internal Growth

Hotel portfolio to benefit from strong U.S. economy and expected impact of U.S. tax reform

• Oxford Economics predicts an o.4% incremental U.S. GDP growth due to tax changes, bringing forecast GDP growth to +2.8% in 2018

• Oil and Gas regions in the U.S. are seeing meaningful improvement from prior years

• AHIP’s Premium Branded Oklahoma hotels have seen a 26.5% increase in RevPAR in Q4 2017 relative to Q4 2016

• Wyndham brand agreement expected to drive incremental transient guest business to our Economy Lodging hotels

• 2017 AFFO per unit impacted by timing differential of capital raised and deployed• Closing of financings and closing of acquisitions

• Overallotment options

• PIP programs: US$36 million of undeployed pre-funded PIP capital is with lenders and not generating incremental returns.

• Cash will be deployed during 2018 and 2019 for scheduled renovations.

• Once deployed over the next 12-24 months, this restricted cash is expected to have a slightly positive impact on FFO per share, assuming an 8% yield (the acquisition all-in Cap rate)

• PIP program in process

• While PIP programs are scheduled to have as minimal impact as possible, some displacement will occur in the short term; however, these renovations are expected to drive better long-term results and market share

12

AFTER

BEFORE

Capital Investment & Renovation History

13

Current Reserve Funds allow AHIP to complete scheduled PIPs over the next 24 months with minimal disruption to AFFO and the payout ratio.

$12,200 $13,200

$25,000

$36,100 $35,800 $35,600

$17,100

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

YE 2015 YE 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 2018E

RESERVE FUND (’000)

$36 million of restricted cash held on deposit for upcoming PIP renovations in 2018 & 2019.

• No need to raise additional capital for upcoming hotel renovations

• Cash on deposit is not return generating until deployed for hotel improvements

The Residence Inn Pittsburgh Cranberry received a comprehensive, high-impact renovation. $3.3 million invested into 96 guestroom improvements and extensive lobby and common area renovations. These investments positioned hotel to be one of the most competitive hotels within the market.

10.1%RevPAR Growth

13.9%Market Share Gain¹

¹ March 2015 vs. March 2014

AFTER

BEFORE

Hampton Inn, Harrisonburg University, VA

The Hampton Inn Harrisonburg was acquired as part of AHIP’s ‘Virginia Portfolio’ acquisition, and had historically achieved average market performance. Analysis showed the property to be under-performing in ADR and RevPAR.

AHIP invested $4.4 million dollars for exterior upgrades and all 159 guestrooms received a fresh, contemporary new look, including one suite that was converted into a boardroom that better positioned the hotel to attract small business meetings and corporate group.

As a direct result of the renovations:

29.3%RevPAR Growth¹

12.3%Market Share Gain¹

Value Creation

14¹ Q1 2016 vs. Q1 2015

Investment Case Study: Virginia Portfolio

15

Four hotels were acquired in Virginia in November 2013 for a purchase price of US$37.1 million and US$7.6 million of PIPs & reserve

VIRGINIA ACQUISITION: PIPS AND PERFORMANCE(Capex in US$000’s)

AVG. REVPAR INDEX PER YEAR: VIRGINIA ACQUISITION (Market share measure in region of hotel. 100 = ‘average’ market share )

• Portfolio consists of 3 Hampton Inns and 1 Fairfield Inn & Suites• 402 guestrooms in total

• First year after acquisition usually involves higher levels of renovations = temporary impact on ANOI (displacement, construction)

• New supply in markets can at times impact RevPAR and ANOI

• AHIP and its hotel manager can use PIPs defensively to drive market share in these situations

4,471

215

2,9452,544

3%

27%

-10%

6%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2015 2016 2017 3-yr AnnualAverage

Capex ANOI per key - Annual growth

133

137

131

100

105

110

115

120

125

130

135

140

2015 2016 2017

HAMPTON INN, HARRISONBURG SOUTH

New supply entered hotel markets in 2017

New supply entered hotel markets in 2017

Investment Case Study: NC & GA Portfolio

16

Four hotels were acquired in North Carolina and Georgia in July 2014 for a purchase price of US$30.5 million and US$1.8 million of PIPs & reserve

$927

$249

$617 $598

-20%

37%

7% 5%

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

100

200

300

400

500

600

700

800

900

1,000

2015 2016 2017 3-yr AnnualAverage

Capex ANOI per key - Annual growth

108

111

113

100

102

104

106

108

110

112

114

116

2015 2016 2017

NC & GA ACQUISITION: PIPS AND PERFORMANCE(Capex in ‘000)

AVG. REVPAR INDEX PER YEAR: NC & GA ACQUISITION (Market share measure in region of hotel. 100 = ‘average’ regional market share)

• Portfolio consists of 2 Fairfield Inn & Suites, 1 Hampton Inn, 1 Springhill Suites• 387 guestrooms in total

• First year after acquisition usually involves higher levels of renovations = temporary impact on ANOI (displacement, construction)

• Following years benefit from the upgrades (increased market share and ANOI)

FAIRFIELD INN & SUITES, KINGSLAND, GA

$252

$1,748

$3,161

$1,7208%

18%

-1%

8%

-5%

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2016 2017 3-yr AnnualAverage

Capex ANOI per key - Annual Growth

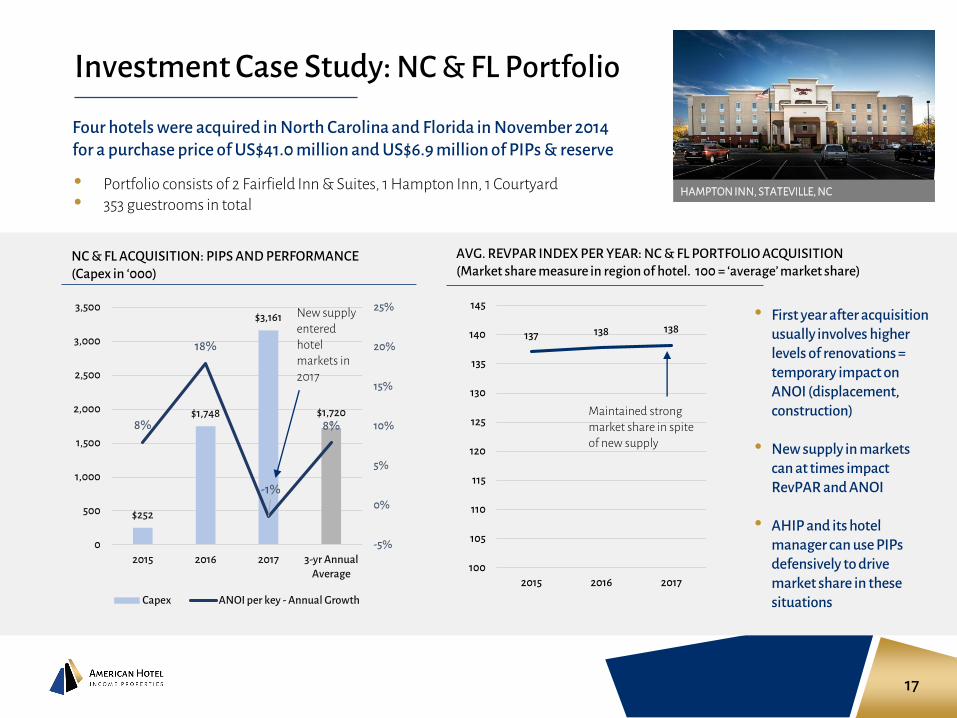

Investment Case Study: NC & FL Portfolio

17

Four hotels were acquired in North Carolina and Florida in November 2014 for a purchase price of US$41.0 million and US$6.9 million of PIPs & reserve

NC & FL ACQUISITION: PIPS AND PERFORMANCE(Capex in ‘000)

AVG. REVPAR INDEX PER YEAR: NC & FL PORTFOLIO ACQUISITION (Market share measure in region of hotel. 100 = ‘average’ market share)

• Portfolio consists of 2 Fairfield Inn & Suites, 1 Hampton Inn, 1 Courtyard• 353 guestrooms in total

• First year after acquisition usually involves higher levels of renovations = temporary impact on ANOI (displacement, construction)

• New supply in markets can at times impact RevPAR and ANOI

• AHIP and its hotel manager can use PIPs defensively to drive market share in these situations

137 138 138

100

105

110

115

120

125

130

135

140

145

2015 2016 2017

HAMPTON INN, STATEVILLE, NC

Maintained strong market share in spite of new supply

New supply entered hotel markets in 2017

Selective and Opportunistic Acquisition Strategy

18

AHIP seeks to acquire properties that meet the following criteria:

• Accretive to AFFO per unit

• Stabilized in-place income

• All-in trailing capitalization rate >8% (all in, fully-loaded, including PIP costs)

• Acquisition cost below replacement cost

• Strong demand generators

• Limited new supply

• Complement existing premium branded, select-service hotels

• Targeted geographic diversification within secondary U.S. markets

Experienced Management Team

19

Rob O’NeillChief Executive Officer

Ian McAuleyPresident

Azim LalaniChief Financial Officer

Anne YuVice President, Finance

▪ Hotel industry veteran ▪ Co-Founder of Coast Hotels and O’Neill Hotels & Resorts▪ Founder of CHIP REIT, which was subsequently sold to B.C. Investment Management Corp. for C$1.2 billion

▪ Co-Recipient of the Canadian Hotel Industry Entrepreneur of the Year Award from the Canadian Hotel Investment Conference

▪ President and CEO of Continuum Health Care Holdings Ltd. which was sold▪ Co-Founder, President and Chief Operating Officer of Superior Lodging Corp., Recipient of Hotelier Magazine’s Pinnacle

Awards – Company of the Year▪ Co-Founder and partner in InnVentures Hospitality Corp., a Vancouver-based boutique hotel management and

consulting firm

▪ More than 20 years of experience in financial reporting, corporate finance, operations, business valuation, taxation and risk management

▪ Senior Vice President of Operations for two TSX-listed commercial REITs▪ Vice President of Real Estate and Risk Management at SilverBirch Hotels & Resorts▪ Audit Manager at KPMG

▪ More than 15 years experience in financial reporting, internal controls, corporate finance and Canadian and US tax. ▪ Manager at Pricewaterhouse Coopers▪ Controller and Manager of Financial Reporting of Sterling Shoes Inc. ▪ Controller of Ventyx Software Solutions Inc. (formerly MDSI Mobile Data Solutions Inc.)

Executive team has over 95 years of collective real estate investing experience

Financial HighlightsAs at Q4 2017

20

89.2%83.4%

90.9%

40.0%

60.0%

80.0%

100.0%

120.0%

Q1 2015 Q2 2015 Q3 2015 Q4 2015 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017

Seasonality and AFFO Payout Ratio

28.6%30.2% 29.6%

20.0%

25.0%

30.0%

35.0%

Q1 2015 Q2 2015 Q3 2015 Q4 2015 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 2017

Seasonality and EBITDA Margin

Seasonal impacts on performance

21

Hotels REITs are more seasonal that other real estate investment trusts/sectors

AHIP is best reviewed and evaluated on an annual basis to account for seasonal changes

• Revenue and EBITDA margin is typically much higher in Q2 and Q3 than in Q1 and Q4, therefore AFFO payout ratio also sees fluctuations (due to stable monthly distributions and seasonally affected AFFO)

Track Record of Growth (USD$)

22

$220,031

$65,759

$48,052

$93,143

$143,767

$173,515

$303,710

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

2013 2014 2015 2016 2017

REVENUE GROWTH ($'000)

$11,183

$24,427

$41,175

$52,355

$89,761

$-

$15,000

$30,000

$45,000

$60,000

$75,000

$90,000

$105,000

2013 2014 2015 2016 2017

EBITDA GROWTH ($'000)

Financial Highlights (USD$)

23

Q4 2017Three months ended

December 31, 2017

Q4 2016Three months ended

December 31, 2016

201712 months ended

December 31, 2017

201612 months ended

December 31, 2016

Number of Guestrooms 11,708 8,156 11,708 8156

Revenue (‘000) $82,222 $44,346 $303,710 $173,515

EBITDA (‘000) $20,435 $12,072 $89,761 $52,355

EBITDA Margin 24.9% 27.2% 29.6% 30.2%

FFO per diluted unit $0.17 $0.19 $0.82 $0.92

AFFO per diluted unit $0.14 $0.17 $0.70 $0.80

AFFO Payout Ratio 115.1% 103.5% 90.9% 83.4%

Debt/Gross Book Value 53.9% 44.0%

WA Loan Interest Rate 4.61% 4.59%

WA Loan Term 7.59 years 7.70 years

Appendices

24

• Geographic diversity – map of properties

• Portfolio Growth – by Guestrooms

• 2018 PIP schedule

Geographic Diversity based on Demand

Consistent with AHIP’s investment strategy, all properties are strategically located within or near:

▪ Larger population centers

▪ Transportation corridors

▪ Demand generators

115 hotels in 92 cities totaling 11,708 guestrooms

25

Economy Lodging HotelsPremium Branded Hotels

11,708Guestrooms (As at Q4 2017)

8.5%CAGR since Q1 2013

44%Growth since Q4 2016

Portfolio Growth – Total Guestrooms

26

2,50

5

2,56

4

2,64

1

3,11

3

3,51

6

3,57

1

3,95

8 5,11

9

5,22

8

5,86

0

6,79

7

6,91

5

7,0

48

7,0

95

7,11

9 8,15

6 9,38

3

11,5

70

11,5

70

11,7

08

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

GUESTROOM GROWTH

Upcoming PIP projects

27

Scheduled Renovation Dates

Hotel Name and Guestrooms Q1 2018 Q2 2018 Q3 2018 Q4 2018

Embassy Suites Cincinnati (227 guestrooms) X X

Embassy Suites DFW South (305 guestrooms) X X

Hilton Garden Inn White Marsh (155 guestrooms) X

Staybridge Suites Tampa East/Brandon (100 guestrooms) X

Residence Inn Baltimore White Marsh (131 guestrooms) X

Embassy Suites Columbus (284 guestrooms) X X

Fairfield Inn & Suites Jacksonville (89 guestrooms) X

Residence Inn Chattanooga (109 guestrooms) X

Homewood Suites Dover Rockaway (108 guestrooms) X

Homewood Suites Allentown (108 guestrooms) X

Homewood Suites Bethlehem (113 guestrooms) X

The following hotel properties are scheduled to undergo PIP projects estimated to be more than US$500,000 in 2018:

28

ahipreit.com

(604) 630-3134

800-925 West Georgia Street Vancouver, BC V6C 3L2 Canada

Questions? Please contact us at: