investor presentation july 2006. company overview petroleum exploration and production company...

TRANSCRIPT

INVESTOR PRESENTATION

JULY 2006

COMPANY OVERVIEW

Petroleum Exploration and Production company focused on Latin America

¹ All contracts and Technical Evaluation Agreements (TEAs) 100% owned by Global

² Proved plus Probable (plus Possible) Reserves net to Global independently reported by Ryder Scott Company, LP as at 31 December 2005 – Competent Persons Report

³ Based upon an approximate Brent Price of $58 per barrel – closing price as at 31 December 2005

• Established management team with long-term focus on Latin America – c 15 years

• Listed on AIM March 2002 – year-on-year financial and operational growth

• Profitable with cash flow from production funding capital expenditure and growth

• Emphasis now on high-potential exploration projects – Colombia, Peru and Panama

No. of contracts & TEAs ¹

Acreage P1 + P2(as at Dec 05) ²

P1 + P2 + P3(as at Dec 05) ²

Future Net Revenues for

P1 + P2 ³

Future Net Revenues for P1 + P2 + P3 ³

Royalties payable

11 + 5.2 million 17.5 million BOE 67.5 million BOE $621 million $2.8 billion 5% - 20%

2

FINANCIAL HISTORY

Finding and development cost of $6.88 per proved barrel ($5.97 for 2P bbl) in 2005

Average WTI in 2005: $56 per barrel

Global’s average cash netback per barrel in 2005: $29.15

2002 2003 2004 2005

Turnover $7,619,000 $8,556,000 $10,974,000 $19,045,000

Gross Profit

$1,890,000 $3,239,000

$5,349,000 $9,290,000

G & A

$4,178,000 $2,499,000

$2,241,000 $4,364,000

PBT ($1,901,000)

$797,000

$3,127,000 $5,094,000

Net Income ($2,502,000) $1,034,000

$2,566,000 $4,379,000

Capex

$2,825,000 $4,421,000

$8,700,000 $18,603,000

Total Assets $56,090,000 $56,822,000 $63,727,000 $86,996,000

3

COLOMBIA & PERU

4

Contract Terms in Colombia and Peru:

• Low production-based royalties

• Private treaty negotiations

• No bid process

• No signature bonus

• Contract sanctity

Wood Mackenzie: Latin America Upstream Insights, July 2004: “Peru and Colombia two best contract terms in Latin America”

Harrison Lovegrove, February 2006: “Colombia, the new hot-spot…..2nd best contractual and fiscal framework in Latin America (after Peru)……

but best combination of prospectivity and the fore-mentioned”

Outcome of Recent Elections:

• Colombia (May 2006)

“There is hardly any political risk in Colombia……the landside re-election of Uribe in May 2006 sets the stage for continued stability………….Colombia may well be the most attractive country in Latin America for E&P Investment.” (Source: Carlos Garibaldi of Harrison Lovegrove, LP June 2006)

• Peru (June 2006)

“The Peruvian Presidential elections have resulted in a significant victory for Garcia……this is certainly the result that the business community had been hoping for and should abate any fears about mass nationalisation of the country's natural resources.” (Source: Ambrian June 2006)

BOLIVAR – BUTURAMA

ALCARAVAN –PALO BLANCO / ANTEOJOS

BOCACHICO – TORCAZ

PERU - BRETAÑA FIELDAND BLOCK 95

GLOBALBogotá - Field

OfficeLOS HATOS

PANAMA – GARACHINE (TEA)

LATIN AMERICA PORTFOLIO

VALLE LUNAR (TEA)

LUNA LLENA –PRIMAVERA (EL MIEDO)

CARACOLI

GLOBALLima - Field

Office

RIO VERDE

11 contracts & TEAs = + 5.2 million acres

Global secures high-potential exploration projects through extensive knowledge of both the region and activity by the ‘majors’ over last few decades

Global then conducts extensive geologic analysis prior to contracting

LOS SAUCES

5

SUMMARY TABLE OF ASSETS

Contract / TEA Name ¹ Status P1 + P2 + P3 (as at Dec 05) ²

Unrisked Exploration Potential Resources

(internal estimates)

Acreage

Alcaravan & Los Hatos (Colombia)

Production & Development

4.7 million BOE 25 million BOE 109,000

Block 95 (Peru) Exploration 21.5 million BOE 4,400 million BOE 1,275,000

Bocachico (Colombia) Production & Development

5.4 million BOE 200 million BOE 54,700

Bolivar (Colombia) Production, Development & Exploration

33.5 million BOE 576 million BOE 55,000

Caracoli (Colombia) Exploration - signed Dec 05 250 million BOE 90,000

Garachine (Panama) Exploration - not signed 754 million BOE 1,400,000

Los Sauces (Colombia) Exploration - signed March 06 26 million BOE 61,600

Luna Llena (Colombia) Exploration 0.3 million BOE 100 million BOE 369,000

Rio Verde (Colombia) Production, Development & Exploration

2.1 million BOE 50 million BOE 75,000

Valle Lunar (Colombia) Exploration - TEA 200 million BOE 1,731,000

Total 67.5 million BOE 6.581 billion BOE + 5.2 million

¹ All contracts and TEAs 100% owned by Global

² Proved plus Probable plus Possible Reserves independently reported by Ryder Scott Company, LP as at 31 Dec 2005 – Competent Persons Report

6

OUTLINE H2 2006 ACTIVITY

7

TASK NAME H1 Q3 Q4

Drilling / Spudding / Location Preparation – up to 8 wells in 2006*

Rio Verde – Tilodiran 2 ●

Rio Verde – Tilodiran 3 ● ●

Los Sauces – Los Sauces 1 ●

Luna Llena – Primavera 1, 2, 3, 4 and 5 ●

Seismic / Geochemical Programmes – up to 4 / 5 in 2006*

Luna Llena – Primavera field ● ●

Los Sauces ● ●

Caracoli ●

Peru – Block 95 / Bretana field ●

Panama - Garachine ●

Workover & Field Facility Programmes ● ● ●

Improved Recovery Programmes

Bocachico – Torcaz field (CO2) ● ● ●

Bolivar – Buturama field (Methane gas) ● ●

Pre New Contracting Activity ● ● ●

* Subject to weather conditions and other operators

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Gross barrels of oil per day *

base production

+ Primavera 1, 2, 3, 4, 5

+ Tilodiran 3

+ Los Sauces 1

+ Tilodiran 2

OUTLINE NEAR-TERM PRODUCTION PROFILE

* Net barrels of oil per day to GED = c. 85% of gross

8

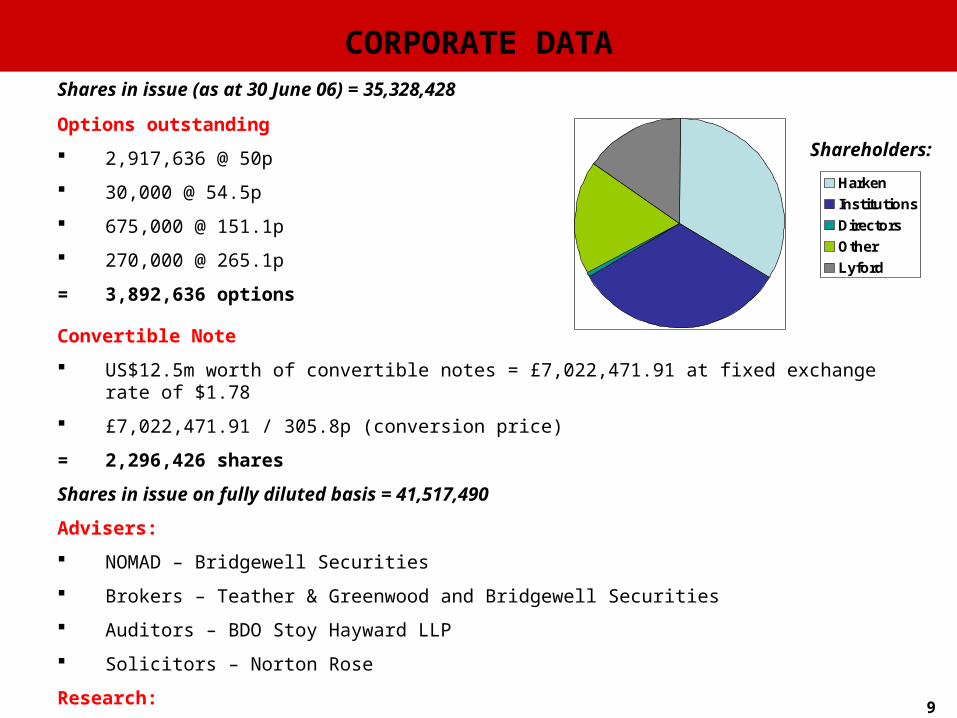

CORPORATE DATAShares in issue (as at 30 June 06) = 35,328,428

Options outstanding

2,917,636 @ 50p

30,000 @ 54.5p

675,000 @ 151.1p

270,000 @ 265.1p

= 3,892,636 options

Convertible Note

US$12.5m worth of convertible notes = £7,022,471.91 at fixed exchange rate of $1.78

£7,022,471.91 / 305.8p (conversion price)

= 2,296,426 shares

Shares in issue on fully diluted basis = 41,517,490

Advisers:

NOMAD – Bridgewell Securities

Brokers – Teather & Greenwood and Bridgewell Securities

Auditors – BDO Stoy Hayward LLP

Solicitors – Norton Rose

Research:

Teather & Greenwood, Bridgewell Securities and Ambrian Partners

Harken

Institutions

Directors

Other

Lyford

Shareholders:

9

APPENDICES

BOARD OF DIRECTORS - COMPANY STRUCTURE

Mikel Faulkner (Executive Chairman) Chief Executive experience with Harken Energy Corporation and an earlier background of service with Arthur

Andersen and the U.S. Navy; B.S., M.B.A.

Stephen Voss (Executive Director / Managing Director) Formerly President of Harken International, Ltd. and prior experience with Chevron Oil Company; B.S., M.B.A.

Guillermo Sanchez (Executive Director / Director of International Negotiations) Formerly Sr. V.P. of Harken Energy Corporation with previous experience at Republic Bank and Texaco; B.S.

Lord Freeman (Non-executive Director) Member of House of Lords and Chairman of Thales Holdings UK plc. A consultant to PricewaterhouseCoopers (London) and chairman of their corporate finance advisory board. Formerly a partner and managing director of Lehman Brothers.

Alan Henderson (Non-executive Director) Chairman of Forum Energy Plc and a director of Aberdeen New Dan Investment Trust Plc and Aberdeen New Thai Investment Trust plc. Previously chairman of Ranger Oil UK Ltd and director of Ranger Oil Ltd.

David Quint (Non-executive Director) Chief Executive of RP&C International. Formerly an attorney with Arter & Hadden and then managing director

of the London-based international financing arm of a US oil and gas company.

11

20 full-time employees in London (UK), Texas (USA) and Bogotá (Colombia)

6 professional consultants in Bogotá with prior experience at Exxon, Elf Aquitaine, Chevron and Texaco

New subsidiary office opened in Lima (Peru) in January 2006

RIO VERDE CONTRACT (COLOMBIA)

12

PorvenirPump Station

Rio Verde Contract

Los Hatos #1

Tilodiran #2

Tilodiran #1

Macarenas #1

Macarenas #2

Canacabare

Palo Blanco

Tilodiran #3

Global Productive Field

Global Energy Oil Pipeline

Braspetro Pipeline

Braspetro and Ecopetrol Pipeline

Previously Drilled Well

Planned Wells

Unrisked exploration potential resources = 50m BOE*

Tilodiran 2 well – estimated stabilized oil rate of c 1,100 boepd

Rig mobilisation to Tilodiran 3 well expected late Q3 / Q4 2006 – dependent on weather and other operators

* internal estimate

RIO VERDE - TILODIRAN STRUCTURE

13

RIO VERDE CONTRACTDEPTH MAP GACHETA FORMATIONCURRENT PRODUCING RESERVOIR

DP: msl

TILODIRAN-2

TILODIRAN-3

Tilodirán-1Gachetá Reservoir @ 12387’ (-11745’)

DEPTH GACHETA R

ESERVOIR

-11745’

Fig. 22

Tilodirán-3 prognosisGachetá Reservoir @ 12355’ (-11713’)

ANTICIPATED FORMATION TOPS

Formaciones MD TVDLEON 7940' 7940'Carbonera C5 10425' 10425'Mirador 11500' 11500'Cuervos 11580' 11580'Barco 11620' 11620'Guadalupe 11750' 11750'Gacheta 12080' 12080'Ubaque 12525' 12525'

TILODIRAN-3 (Vertical Well)

well prognosis

Main fault cuts Base of Mirador.

Tilodiran 3:

• same seismic line of Tilodiran 1 location

• c 500m to the east

LOS SAUCES CONTRACT (COLOMBIA)

14

Unrisked exploration potential resources = 26m BOE*

First exploratory well expected to be spudded late Q4 2006 – dependent on weather and other operators

Perenco operates the Tocaria and Morichal fields

* internal estimate

Rio Verde

Los Sauces

La Gloria Pipeline

Los Sauces

LUNA LLENA CONTRACT (COLOMBIA) – PRIMAVERA FIELD

15

Valle Lunar

Primavera Field(formerly El Miedo Field)

Meta River

Barge Transport

Luna Llena

Rio Verde

Los Sauces

Unrisked exploration potential resources = 100m BOE*

Acquisition of new 2D seismic shortly

5 wells to be drilled / spudded in Q4 2006 – weather dependent

Negotiations to contract a rig very advanced

Shallow wells = c 3,000 feet / $1.1m apiece

* internal estimate

BLOCK 95 CONTRACT (PERU) – BRETANA FIELD

16

Bretana DiscoveryBretana Discovery

AA

BB

CC

EE

FF

BLOCK 95 CONTRACT (PERU) – BRETANA FIELD

4 Major Exploration Plays

17

• Unrisked exploration potential resources = 4,400 million BOE*

• Significant, existing seismic profiling a number of leads and prospects

• Oil tests and / or shows in a number of wells within the contract

• Lead / prospect maximum closures of 5,000 to 24,000 acres

* internal estimate

INVESTOR PRESENTATION

JULY 2006