investor presentation november pt bank negara indonesia tbk · legal division compliance division...

TRANSCRIPT

Investor Presentation

November 2010

PT Bank Negara Indonesia (Persero) Tbk(Persero) Tbk

C:\DPS NEW\Pres\PPT\PresPrint.pot

Agendag

O iOverviewof BNI

Going Forward Performance

1

Section 1Section 1

Overview of BNI

C:\DPS NEW\Pres\PPT\PresPrint.pot

Overview of BNI

Key milestones Highlights

BNI established as first wholly owned state bank

BNI first distributed the official currency of Indonesia

Merger with several commercial banks

Primary task of improving Indonesia’s economy with

1946 – 1968

Strong pedigree – initially set up as Central bank

Compelling brand name – 64 years history

emphasis on industrial sectors

First state‐owned bank to go public

Launched BNI Securities in 1995

h d l f

Top product synergies in BNI family

Extensive network – 1,112 branches, four overseas branches and one agencyLaunched life insurance unit in 1996

Asian Financial Crisis

Government recapitalization, owning 99.1% of BNI

Established Syariah banking in 2000

$

four overseas branches and one agency

Large, premium customer base – over10 million customers1969 – 2007

Secondary Offering, US$445m new Tier‐1 capital

Increased public ownership to 23.6%

New management team introduced

I l t d t f tiReinvigorated management team

R b t ROE d ROA i tImplemented transformation program

Government owns 73.3% of BNI

Continue to strengthen BNI through key hires

BNI h bli h d i lf k l d i I d i h h h lf f i

2008 – 2010Robust ROE and ROA improvement trajectory

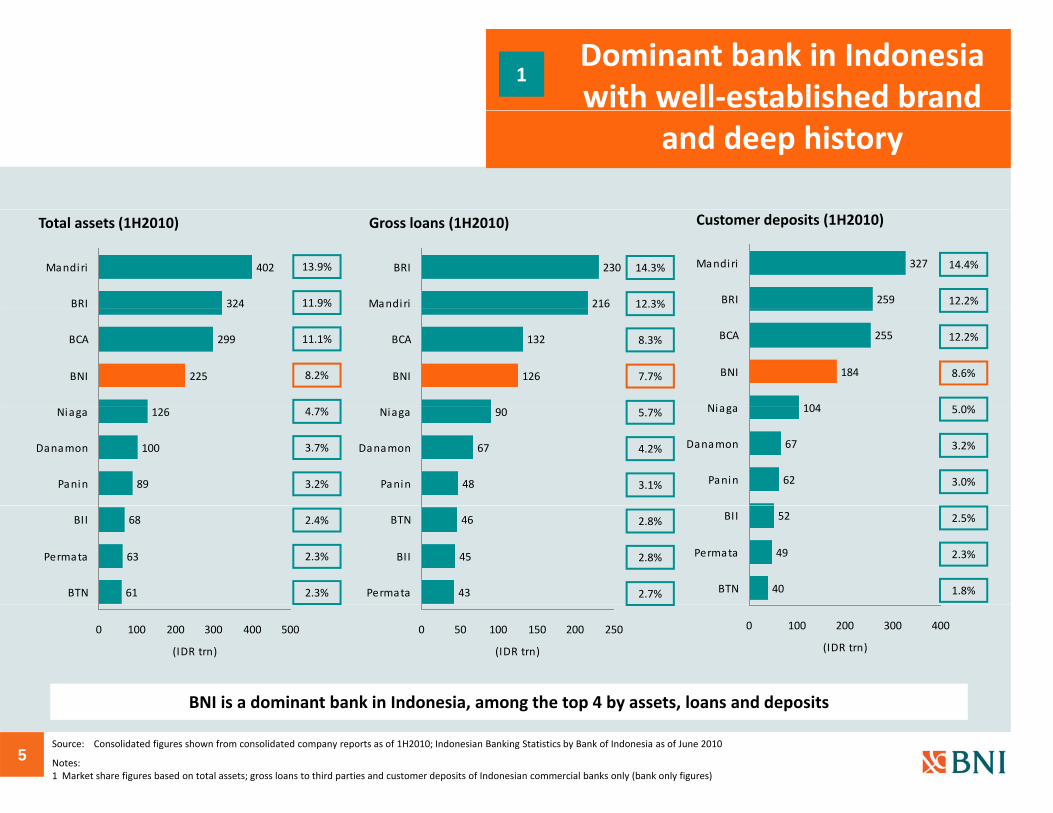

Dominant bank in Indonesia

3

BNI has established itself as a market leader in Indonesia through over half a century of operations

C:\DPS NEW\Pres\PPT\PresPrint.pot

1Dominant bank in Indonesia with well‐established brand

and deep history

BNI has a long track record, rivaled by none, in the Indonesian banking sectorYear of brand establishment

1963

1998

19711946

1956 2008

1957 2002

1959 1968

Strong brand recognized by the industry globally

2010Best Local

2010Best Local

2009No 1

2009No 1

2009 / 2007Top Brand Award –

2005The Banker

2009 / 2008 / 2007Banking Service

2006Indonesia

2010Best Domestic

2010Top 3 Customer Best Local

CashManagement Bank –Large CorporatesAsia Money

Best Local CashManagement Bank –Medium CorporatesAsia Money

No. 1 Arranger for Indonesia Syndicated Loans IFR

No. 1 Bookrunner for Indonesia Syndicated LoansIFR

Top Brand Award –Category: Credit card in Recognition of Outstanding Achievement in Building the Top BrandFrontier Consulting Group and Marketing Magazine

The Banker Award – Bank of the Yearin IndonesiaThe Banker

Banking Service Excellence AwardsInfobank & MRI

Indonesia Corporate Brand Visualization Award Businessweek

Best Domestic FX Provider of Single‐Bank Electronic Trading in IndonesiaAsia Money

Top 3 Customer Satisfaction Among Largest Banks in IndonesiaRoy Morgan

and Marketing Magazine

FXPOLL

BEST DOMESTIC FXPROVIDER OF SINGLE

BANK ELECTRONIC TRADING IN INDONESIA

4

C:\DPS NEW\Pres\PPT\PresPrint.potDominant bank in Indonesia with well‐established brand

1

and deep history

Total assets (1H2010)

13.9%

11.9%

Gross loans (1H2010)

14.3%

12.3%

Customer deposits (1H2010)

14.4%

12.2%216

230

Mandiri

BRI

324

402

BRI

Mandiri

259

327

BRI

Mandiri

11.1%

8.2%

8.3%

7.7%

12.2%

8.6%

5 0%

126

132

BNI

BCA

225

299

BNI

BCA

104

184

255

Niaga

BNI

BCA

4.7%

3.7%

3.2%

5.7%

4.2%

3.1%

5.0%

3.2%

3.0%48

67

90

Panin

Danamon

Niaga

89

100

126

Panin

Danamon

Niaga

62

67

104

Panin

Danamon

Niaga

2.4%

2.3%

2.3%

2.8%

2.8%

2.7%

2.5%

2.3%

1.8%43

45

46

Permata

BII

BTN

61

63

68

BTN

Permata

BII

40

49

52

BTN

Permata

BII

BNI is a dominant bank in Indonesia among the top 4 by assets loans and deposits

0 50 100 150 200 250

(IDR trn)

0 100 200 300 400 500

(IDR trn)

0 100 200 300 400

(IDR trn)

5

BNI is a dominant bank in Indonesia, among the top 4 by assets, loans and deposits

Source: Consolidated figures shown from consolidated company reports as of 1H2010; Indonesian Banking Statistics by Bank of Indonesia as of June 2010

Notes: 1 Market share figures based on total assets; gross loans to third parties and customer deposits of Indonesian commercial banks only (bank only figures)

C:\DPS NEW\Pres\PPT\PresPrint.pot

Stable deposit franchise ith l t f f di

5

with low cost of funding

Cost of deposits (1H2010)1 CASA ratio (1H2010) Loans‐to‐deposit ratio (1H2010)

73.3BCA 51.6BCA2.88BCA

57.3

59.2

60.2

Mandiri

Mega

BNI

68.5

66.2

63.6

BNI

Mandiri

Mega

4.32

4.11

3.50

BRI

Mandiri

BNI

44.0

44.8

57.1

Niaga

Permata

BRI

86.5

85.5

76.5

Niaga

BII

Panin

5.08

4.81

4.78

Permata

Panin

Niaga

38 5

41.1

43.4

Danamon

BII

Panin

100 2

88.9

87.3

Danamon

BRI

Permata

5 53

5.35

5.29

Danamon

BTN

BII

BNI’s large and stable deposit base has given the bank robust liquidity and low cost of funding

38.5

0.0 20.0 40.0 60.0 80.0

Danamon

(%)

100.2

0.0 20.0 40.0 60.0 80.0 100.0 120.0

Danamon

(%)

5.53

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00

Danamon

(%)

6Source: Detailed company reports as of 1H2010

Note: Consolidated figures shown unless otherwise noted1 Cost of deposits calculated as interest expense from deposits to customers and other banks (including bonus and revenue‐sharing expenses on Syariah funding products)/average deposits

(where interest expense split unavailable, total interest expense is applied); 1H2010 figures are annualized

BNI s large and stable deposit base has given the bank robust liquidity and low cost of funding

C:\DPS NEW\Pres\PPT\PresPrint.pot

Extensive domestic and i t ti l t k

4

international network

BNI’s multiple touch points for individual and corporate customers

Individual customer

Mobile Call ATMsDomesticBranches

Consumerloan

Small business

Medium business

BNI Emeralde banking

Int’lBranches

10.9 million deposit accounts

1.8 million credit cards

97,400 mortgage customers

banking center (4,072)Branches(1,112)1

centers(12)

centers(51)

centers(20)

Emerald(24)

e‐banking Branches(5)2

Corporate/SME customer highlights

143,024 corporate deposit accounts

943 corporate lending accounts

71,982 SME lending accountsIndonesia (1,112 branches)Indonesia (1,112 branches)

Platform for efficient and effective cross‐selling of products and services

7

g p

Notes:1 As of September 30, 2010; Domestic branches include 167 conventional branches, 887 sub‐branches, 58 Syariah branches and sub‐branches2 Four overseas branches in Hong Kong, London, Singapore and Tokyo and an agency in New York

C:\DPS NEW\Pres\PPT\PresPrint.pot

Extensive domestic and i t ti l t k

4

international network

BNI’s global remittance network Incoming remittances

1,500,000

2,000,000

ps

1

1

Market share 23.7% 24.5% 27.4%

1,781,255 1,796,5931,511,984

0

500,000

1,000,000

No. of sli

4

1

2 1

3 2610

256

3

4 8

1

1

11

41

1

0

2008 2009 3Q2010

Outgoing remittances

2.9% 4.2% 5.3%

Remittance representatives (12) Overseas offices (5) & alliances (1)

Market shareSaudi ArabiaJeddah (1)Riyadh (2)Damman (1)Kuwait

QatarDoha (1)MalaysiaKuala Lumpur (2)S b h (1)

Singapore OfficeSingPostHong Kong OfficeSeven‐ElevenT lk l

London OfficeNew York Agency OfficeStrategic alliance with BONYfor web‐based remittancesBNI R itt Ltd

249,830 234,745100 000

150,000

200,000

250,000

No. of slips

Virtual offices1 (51)

KuwaitKuwait City (1)Uni Arab EmiratsAbu Dhabi (1)Dubai (1)

Sabah (1)TaiwanTaipei (1)

51 Virtual office in 11 countries:Brunei: 2 virtual officesSingapore: 6 virtual offices

TelkomselExcelcomindoTokyo OfficeSMBC via ATMGenkin Kakitome (Post Office)

BNI Remittance Ltd, Hongkong

1,650 Correspondents Banks38 OTR2 Domestic Outlets

T f Vi 164,651

0

50,000

100,000

2008 2009 3Q2010

N

Forming the backbone of BNI’s market leading remittance business

g pMalaysia : 10 virtual officesTaiwan : 2 virtual officesQatar : 6 virtual officesBahrain : 4 virtual officesKuwait : 5 virtual officesOman : 3 virtual officesJordania : 4 virtual officesUAE : 8 virtual officesSaudi Arabia: 1 virtual offices

Transfer ViaWeb base (i‐banking) Smart RemittanceSWIFTATM (SMBC)Post Office AlliancesSMS BankingStand‐alone application Remittance Plus

File TransferSWIFT Net – MaybankTelex

8

Forming the backbone of BNI s market leading remittance business

Source: Company reports

Note: Consolidated figures shown unless otherwise noted1 Local remittance agencies2 Outgoing transfers (marketing officers)

C:\DPS NEW\Pres\PPT\PresPrint.pot

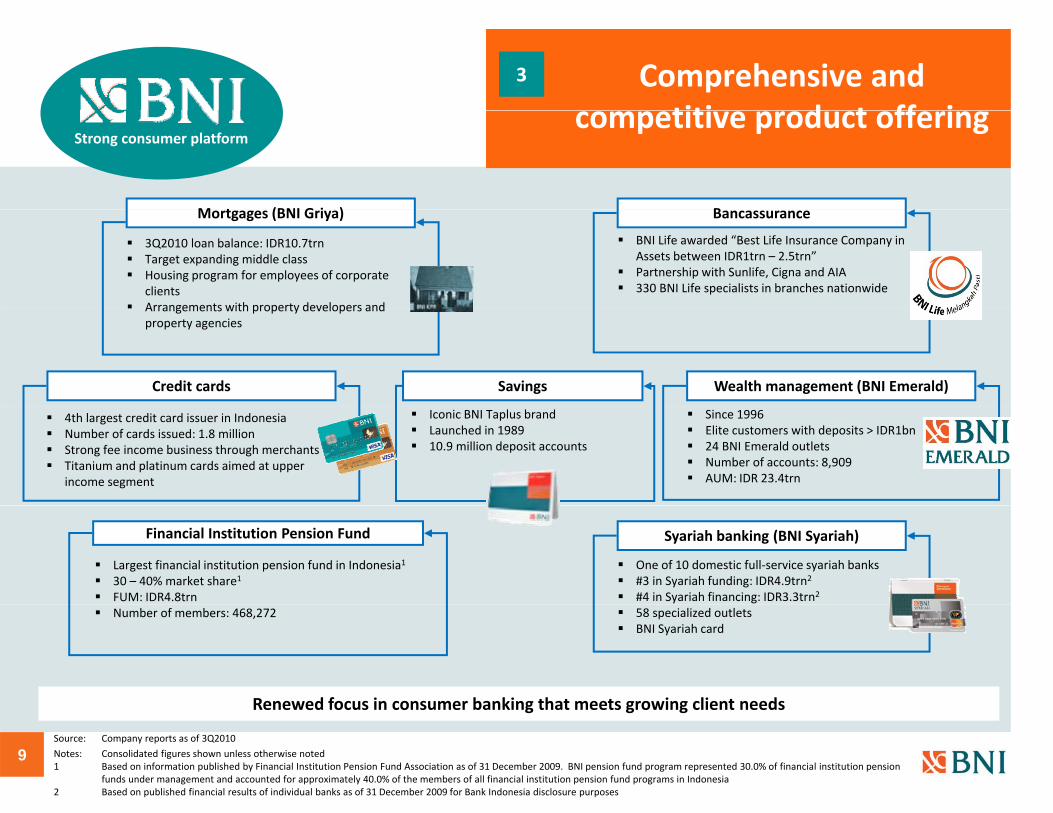

3 Comprehensive and titi d t ff i

M t (BNI G i )

Strong consumer platform

B

competitive product offering

Mortgages (BNI Griya)

3Q2010 loan balance: IDR10.7trnTarget expanding middle classHousing program for employees of corporate clientsArrangements with property developers and

Bancassurance

BNI Life awarded “Best Life Insurance Company in Assets between IDR1trn – 2.5trn”Partnership with Sunlife, Cigna and AIA330 BNI Life specialists in branches nationwide

Credit cards

Arrangements with property developers and property agencies

Wealth management (BNI Emerald)Savings

4th largest credit card issuer in IndonesiaNumber of cards issued: 1.8 millionStrong fee income business through merchantsTitanium and platinum cards aimed at upper income segment

Since 1996Elite customers with deposits > IDR1bn24 BNI Emerald outletsNumber of accounts: 8,909AUM: IDR 23.4trn

Iconic BNI Taplus brandLaunched in 198910.9 million deposit accounts

Financial Institution Pension Fund

Largest financial institution pension fund in Indonesia1

30 – 40% market share1

FUM: IDR4.8trn

Syariah banking (BNI Syariah)

One of 10 domestic full‐service syariah banks#3 in Syariah funding: IDR4.9trn2

#4 in Syariah financing: IDR3.3trn2

Renewed focus in consumer banking that meets growing client needs

Number of members: 468,272 58 specialized outletsBNI Syariah card

9

Renewed focus in consumer banking that meets growing client needs

Source: Company reports as of 3Q2010

Notes: Consolidated figures shown unless otherwise noted1 Based on information published by Financial Institution Pension Fund Association as of 31 December 2009. BNI pension fund program represented 30.0% of financial institution pension

funds under management and accounted for approximately 40.0% of the members of all financial institution pension fund programs in Indonesia2 Based on published financial results of individual banks as of 31 December 2009 for Bank Indonesia disclosure purposes

C:\DPS NEW\Pres\PPT\PresPrint.pot

Comprehensive and titi d t ff i

3

competitive product offering

Trusted partner to Indonesian and multi‐national corporates

Consumer Construction Education

U i it f I d i

Real estateEnergy Communications DiversifiedInfrastructure

University of Indonesia

SalimGroup

Corporate loans Commercial loans Cash management clients

Group

215

100

150

200

250

anagem

ent

f accou

nts)

29,665

46,284

30,000

40,000

50,000

oans (IDRbn)

38,106

50,833

40,000

60,000

loans (IDRbn)

07‐3Q10 CAGR = 17.6%

07‐3Q10 CAGR = 11.0%

9

0

50

100

2007 1H2010

Cash ma

(No. of

0

10,000

20,000

2007 3Q2010

Corporate lo

Leading corporate banking franchise backed by rapidly growing client base

0

20,000

2007 3Q2010

Commercial

10

Leading corporate banking franchise backed by rapidly growing client base

Source: Company reports as of 3Q2010 and 1H2010Notes: Consolidated figures shown unless otherwise noted

C:\DPS NEW\Pres\PPT\PresPrint.pot

Transformation begins with th i ht lthe right people

Change Management Office Internal Audit

S i Pl i

Board of Commissioners

P id t Di tHuman Resources Division

Training & Development Division

Strategic Planning Division

Corporate Secretary

Managing Director – Managing Director – Managing Director –

President Director (Chief Executive Officer/CEO)

Vice President Director (Chief Risk Officer/CRO)

Managing Director –

Consumer Loan Division

Wealth Management Division

Consumer & Retail Banking

Card Business Division

Treasury & FI

International Division

Treasury Division

Network & Services

Network & Services Division

Chief of Network & Services

Corporate Funding & Financial Division

Corporate Banking Division 1

Corporate Banking Division 2

Business Banking

Consumer Funding & Financial Division

Pension Fund Unit

Transactional Banking & Financial Services Division

Middle Business Division

Small Business Division

Managing Director –Compliance

Legal Division

Compliance Division

Managing Director –Operations & IT

Banking Operations Division

IT Division

Chief Financial Officer (CFO)

General Affairs Division

Financial Control Division

Chief Business Risk Officer

Loan Recovery Divisions

Credit Risk Divisions

Managing Director –Entreprise Risk Management

Risk Management Division

BNI h d i ifi h f i b i h i h l i h i h l

Service Committee

DisciplinaryCommittee

Human ResourcesCommittee

Planning & Budgeting Committee

Technology Management Committee

Risk & CapitalCommittee

Subsidiaries Mgmt Unit

Key new hires / appointment made under transformation program since: 2010 2009 2008

11

BNI has undergone significant human resource transformation by putting the right people in the right places

C:\DPS NEW\Pres\PPT\PresPrint.pot

Senior management teamg

Gatot M. SuwondoPresident Director/CEOSince February 2008

Felia SalimVice President Director/CROSince February 2008

Yap Tjay SoenManaging Director/CFOSince February 2008

Krishna R SupartoManaging DirectorBusiness Banking

Ahdi Jumhari LuddinManaging Director Compliance

Suwoko SingoastroManaging DirectorNetwork and Services

Previously: Vice President Director of BNI, MD of Bank Danamon

Previously: Independent Commissioner of BNI, Deputy Chairman ‐ IBRA, Director, Jakarta Stock Exchange

Previously: Commissioner of Bank Mandiri & BNI, Director‐CFO of BII, various executive positions in Astra, Asia Food & Properties, Tuban Petro Chemical, & ANTAM

Since February 2008Previously: President Director of Barclays Securities, Managing Director of Bank Danamon

Since February 2008Previously: Director, Banking Supervisory, Bank Indonesia

Since February 2008Previously: EVP Network &Operation, GM of NetworkDistribution Division

Honggo Widjojo KangmastoManaging DirectorNetwork and ServicesSince May 2010

Darmadi SutantoManaging DirectorConsumer BankingSince May 2010Previously: Director of

il ki S

SutantoManaging DirectorEnterprise Risk ManagementSince May 2010Previously: GM Risk

i i i G

Adi SetiantoManaging DirectorTreasury and Financial InstitutionsSince May 2010

i l G i i l

Sutirta BudimanChief Business Risk OfficerSince September 2010Previously: Commissioner of BNI Securities, CFO of

k i iPreviously: MD Permata Bank, MD Indofood, EVP Bank Mandiri

Retail Banking RBS Management Division, GM Training Division

Previously: GM InstitutionalFunding, GM Bancassurance

Aneka Kimia Raya

12

BNI has been further enhancing its management through key hires with strong industry experience

C:\DPS NEW\Pres\PPT\PresPrint.pot

Board of Commissioners

Peter B. Stok Tirta HidayatPeter B. StokPresident Commissioner(Independent) Since May 2009Previously: Commissioner BankPermata, President DirectorB k Ni P id t

Tirta HidayatVice President CommissionerSince May 2010Previously: Lecturer fromUniversity of Indonesia,Economic Deputy at Vice President office

Achil Ridwan DjayadiningratC i i

Fero PoerbonegoroC i i

Bank Niaga, PresidentDirector Bank Dagang Negara

Bagus RumbogoC i iCommissioner

(Independent)Since February 2008Previously: Managing Director of BNI(Compliance and Human Resource)

Commissioner(Independent)Since February 2008Previously Managing Director of BNI (Treasury & Private Banking)Managing Director of Bank BCA

CommissionerSince May 2010Currently: Advisor to the Ministry of State‐Owned Enterprises

BS KusmuljonoCommissioner(Independent)

Ekoputro AdijayantoCommissionerSince May 2010

This transformation will only be made possible by our effective and experienced professionals

Since May 2010Previously : Commissioner BRI,President Director of PT PNM

Currently: Advisor for Ministry of State‐Owned EnterprisesPreviously SVP Bank Mandiri

13

This transformation will only be made possible by our effective and experienced professionals

Section 2Section 2

Strategy & Next Steps

C:\DPS NEW\Pres\PPT\PresPrint.pot

BNI transformation

Start Small Think Big

Energise, mobilise and start implementing transformation

processFix the basics

Compete with domestic leaders

Differentiate ourselves from the pack and strive to be the

best in classprocess best in class

2008

Improve asset qualityAggressively seek low cost of fundingImplement customer centric operating model

Increase asset qualitySharpening focus of BNI portfolio on corporate and consumerDiversify fee‐based incomeda

y

b i l i i f i i d h d li d f l f

First 6 months 6‐18 months 18‐36 months 36‐60 months

Implement customer centric operating modelImprove cross‐sellingStrengthen capital position

Diversify fee based incomeAggressive CASA growthIncrease efficiency of operations

BNI Tod

15

BNI began implementing its transformation program in 2008 and has delivered a strong set of results so far

C:\DPS NEW\Pres\PPT\PresPrint.pot

Well positioned fort h f thnext phase of growth

1 Dominant bank in Indonesia with well‐established brand and deep history

S l i i d i li2

3 Comprehensive and competitive

Strongly positioned to capitalize on Indonesia’s growth

Top business bank3 p pproduct offering

4 Extensive domestic and international t k

Top business bank

5

network

Stable deposit franchise with low cost of funding

6

g

Significant improvement in credit risk management

Top 3 consumer bank

16

C:\DPS NEW\Pres\PPT\PresPrint.pot

To bet b i b ktop business bank

Business Banking Client PortfolioBusiness Banking Client Portfolio

Diamond Clients

Foundation Clients

orpo

rates

ing

s e alers

uction

Client focused model

8 target industries

Developing deep industry knowledge

1

Base Corporate

Ruby Clients

Portfolio Clientsm‐Sized

panies

Co

& Gas and

Min

ommun

ication

Chem

icals

Agriculture

ood & Beverage

ers & W

holesa

Electricity

ering & Con

str

Understanding who most valuable clients are

Through maintaining strong relationships with li t

2

Base Commercial

Small Businesses

Med

iuCo

mp

Oil & Co Fo

Retail

Engine

e clients

Providing customized sales and service treatment to add value

Relationship‐based pricing and solutions

Business Banking Relationship Managers

Business Banking Products and Services Suite

Relationship based pricing and solutions

Providing first‐class product support

Increasing product specialization

3

We are moving from a product‐centric model to a customer‐based model h d ff l d k h

Business Banking Products and Services SuiteCredit &Funding

TransactionalBanking

TradeFinance

TreasuryProducts

Fostering collaboration across products

17

to enhance our product offering to our clients and market share

C:\DPS NEW\Pres\PPT\PresPrint.pot

To bet 3 b ktop 3 consumer bank

Key Target Customer Segments

i h h

Dominant Value Propositions

Consumer & Retail Banking Products and

Services

High Net Worth

Affluent Families

l

Lifetime Banking Partner

L di th i Di t

Deposits

LendingYoung Elites

Students

Leading the way in Direct Banking

“Wealth management supermarket” for mass

Remittance

Middle Income Families

Wealthy Singles

supermarket for mass affluent

Leader in Wealth Planning & Management

Cards

Wealth ManagementGolden Oldies

g ea t a age e t

BNI will be positioned to become the Lifetime Banking Partner for our retail customers by understanding their needs

18

p g y g

C:\DPS NEW\Pres\PPT\PresPrint.pot

Rights issue to lead t h tnext chapter

1 Strategic transformation underway1 Strategic transformation underway

Ri h i ill f h h b2 Rights issue will further enhance our asset base

3 Rights issue will finance our business growth

19

Section 3Section 3

Performance

C:\DPS NEW\Pres\PPT\PresPrint.pot

Exceptional turnaroundt d tproven to date

2007 3Q2010

1. Asset qualityGross NPL: IDR7.6tnNPL ratio: 8.53%1

Coverage: 71.9%1 +

Q

Gross NPL: IDR5.5tnNPL ratio: 4.38%1

Coverage: 118.3%1

2. Low cost fundCost of deposits: 4.73% LDR: 60.6% +Cost of deposits: 3.53%

LDR: 68.6%

3. Productivity, Efficiency and Profitability

NIM: 5.4%2

CIR: 65.8%ROAA: 0.51%3 / ROAE: 5.6%3 +

NIM: 6.1%2

CIR: 51.5%ROAA: 1.74%3 / ROAE: 19.5%3

4. Strengthen BNI Incorporated

ATMs: 2,476Number of customers: 9.6mNon‐interest income: IDR4.1tn

+ATMs: 4,072Number of customers: 10.9mNon‐interest income: IDR3.4tn

BNI h fi d h b i d i d b k i f k l d hi

5. Strengthen CapitalTier‐1 capital: 11.2%CAR: 15.9%

Tier‐1 capital: 10.2%CAR: 12.4%

21

BNI has fixed the basics and is ready to embark on its strategy for market leadership

Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 Based on Bank Indonesia classification2 Calculated based on net interest and Syariah income for the relevant year/period as a percentage of average total interest earning assets excluding commitments and contingencies. Annualized for 3Q2010 3 Return on average assets calculated as net income / average assets; Return on average equity calculated as net income to shareholders / equity attributed to bank shareholders. Annualized for 3Q20104 Cost of deposits calculated as interest expense on deposits from customers and other banks/average deposits from customers and other banks. Annualized for 3Q2010

C:\DPS NEW\Pres\PPT\PresPrint.pot

Balance sheet

(IDR bn, FYE 31 December) 2007 2008 2009 3Q2009 3Q2010 YoY (%)

Total assets 183,342 201,741 227,497 203,060 224,811 10.7%

Placement with other Banks & BI 32,382 31,993 38,153 28,283 31,460 11.2%

Marketable securities 52,901 44,529 50,237 43,447 50,261 15.7%

Loans (gross) 88,651 111,994 120,843 122,116 126,074 3.2%

Customer deposits 146 189 163 164 188 469 163 654 183 772 12 3%Customer deposits 146,189 163,164 188,469 163,654 183,772 12.3%

Deposits from other Banks 3,804 4,100 3,819 3,495 3,155 (9.7%)

Marketable securities issued 1,269 1,269 1,261 1,267 1,277 0.7%

Borrowings 6,309 8,617 5,570 7,737 5,185 (33.0%)

Shareholders’ equity 17,220 15,431 19,144 18,406 21,318 15.8%

22Source: Company reports

Note: Consolidated figures shown unless otherwise noted

C:\DPS NEW\Pres\PPT\PresPrint.pot

Loan compositionp

Loan breakdown by segment (%) Loans by currency (%)

6.6% 5.6% 3.9% 3.8%2.0% 2.8% 2.7% 2.6%100%

Gross loans (IDR trn)

(10.4%)

34.7%

07‐09 CAGR (%)

88.7 112.0 120.8 126.1 11.8%13.3%20.1%26.3%

50%

75%

100%

y g ( ) y y ( )

14.9% 15.4%15.3% 16.6%

80%18.5%

( )88.2%86.7%79.9%73.7%

0%

25%

50%

2007 2008 2009 3Q2010

43.0% 42.8% 44.4% 40.3%

40%

60%18.6%

Average yield on IDR loans – 1H2010 (%)

IDR Foreign

28 7%30 0%

33.5% 33.4% 33.7% 36.7%20%17.2% 12.3% 11.8%

13.5% 14.1%

28.7%

10.0%

20.0%

30.0%

0%

2007 2008 2009 3Q2010

Corporate SME Consumer Internationa l Syariah

0.0%

Corporate Medium Small Consumer Credit Card

23Source: Company reports

Note: Consolidated figures shown unless otherwise noted

C:\DPS NEW\Pres\PPT\PresPrint.pot

Loan diversification

Loan breakdown by economic sector Consumer loan composition

27 6%90%

100%

88.7Gross loans (IDR trn)

112.0 120.8 126.1

11.3%10.4%

8.1%5.1%

3.1% 1.8% 2.4%1.1%1.6%2.6%

1.7%1.1%1.6%1.5%2.0%

90%

100%

13.2Gross loans (IDR trn)

17.2 18.4 20.9

3.2%

4.2%6.3% 7.0% 6.9%

27.6% 30.3% 29.3% 29.6%

4 8%3.0% 3.2%

4.9%

60%

70%

80%

26.8%26.5%

22.8%

13.3%

11.3%

60%

70%

80%

20.0%18 8%

4.5%4.6% 6.4% 7.1%

5.3%5.0% 4.7% 7.1%

4.3%6.0% 5.7%4.8%

40%

50%

60%24.7%

40%

50%

60%

28.5% 26.0% 23.4% 22.9%

18.8%20.2% 18.9%

10%

20%

30%

36.0%40.9%

44.7%51.0%

10%

20%

30%

Manufacturing Hospita l i ty Agricul ture

Constructions Electrici ty Gas & Water Mining

0%

10%

2007 2008 2009 3Q 20100%

10%

2007 2008 2009 3Q2010

Mortgages Auto Credit cards

24Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 Others include Business services, Social services as well as Others not classified2 Consumer loans includes outstanding credit card receivables

Constructions Electrici ty, Gas & Water Mining

Transportation & Comm OthersMulti ‐purpose Unsecured Cash col latera l

C:\DPS NEW\Pres\PPT\PresPrint.pot

Marketable securities

Securities by type1 Currency breakdown

17 6%13.4%

20 2%

100%

y yp y

Total (IDR trn)

3.0% 1.9%5.3%9 5%

2.5% 3.2%100%

17.319.510.216.2

17.6%25.9%

20.2%

80%15.7%

17 3%

2.0%

9.8%

16.7% 16.3%

2.6%

6.8%

9.5%

70%

80%

90%

82.4%74 1%

86.6%79.8%40%

60%21.3%

17.3%22.6%

50%

60%

74.1%

20%

74.3%

52.5%60.5%

56.1%

20%

30%

40%

0%

2007 2008 2009 3Q2010

IDR Foreign

0%

10%

2007 2008 2009 3Q2010

25Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 Others include Medium term notes and Other debt securities

Certi fi cate of BI Bonds Mutua l funds Credit l inked notes Others

C:\DPS NEW\Pres\PPT\PresPrint.pot

Customer depositsp

Customer deposits by type Deposits by currency

15.0% 15.7% 18.4% 19.4%

60%

80%

100%

100%

62.3%CASA 57.9% 55.1% 56.5%

146.2Customerdeposits (IDRtrn) 163.2 188.5 183.8

85.0% 84.3% 81.6% 80.6%

0%

20%

40%

2007 2008 2009 3Q2010

37.7%42.1% 44.9% 43.5%80%

32.9%32.1%

31 2% 31.4%40%

60%

Dep

osits (ID

Rbn)

Cost of deposits 1

IDR Foreign

8.00

29.4% 25.8% 23.9% 25.1%

31.2%

20%

40%

3.854.73 4.33

3.53

2 00

4.00

6.00st of deposit (%

)

23.9%

0%

2007 2008 2009 3Q2010

Current Savings Time

0.00

2.00

2007 2008 2009 3Q2010

Cos

26Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 Cost of deposits calculated as the sum of interest expense on deposits to customers and banks; Mudharabah profit‐sharing and Wadiah bonus/Average deposits to customers and other

banks. Annualized for 3Q2010

C:\DPS NEW\Pres\PPT\PresPrint.pot

Liquidity managementq y g

Optimal liquidity1Room for loan expansion

60.668.6

64.168.6

60.0

80.0

sit ratio (%

) 29.9 30.6 28.8 27.3

20

30

40

sets (%)

0.0

20.0

40.0

2007 2008 2009 3Q2010

Loan

to dep

os

0

10

20

2007 2008 2009 3Q2010

Liquid ass

106.6120.0R (%

)

Healthy IDR liquidity Flush with FX liquidity

68 275.080 0%

)

88.0

46.2 42.040.0

80.0

n de

nominated

LDR

52.6

65.0 68.2

20.0

40.0

60.0

80.0

enom

inated

LDR (%

0.0

2007 2008 2009 3Q2010Foreign

0.0

2007 2008 2009 3Q2010

IDR de

27Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 Liquid assets calculated as sum of cash, government bonds and net placement to other banks and Bank of Indonesia / total assets

C:\DPS NEW\Pres\PPT\PresPrint.pot

Stable deposit franchise ith l t f f di

5

with low cost of funding

Customer deposits by type Deposit breakdown by customers

62 3%CASA 57 9% 55 1% 56 5%

100%

62.3%CASA 57.9% 55.1% 56.5%

146.2Customer deposits (IDRtrn) 163.2 188.5 183.8

19.6%19 8%

2.7%2.2%

1 9%

200,000

163,164

188,469183,772

37.7%42.1% 44.9% 43.5%80%

30.2% 28.7%

23.5%

21.9%

19.8%1.9%

1.2%150,000

bn)

146,189

32.9%32.1%

31.2% 31.4%40%

60%

Deposits (IDRbn)

25.0%

26.5%100,000

Deposits (IDRb

29.4%25.8% 23.9% 25.1%

20% 50.3%49.7%

48.1% 48.9%50,000

Deposit franchise strengthened by cash management business

0%

2007 2008 2009 3Q2010

Current Savings Time Individua l / Reta i l Insti tutiona l Government Syariah

0

2007 2008 2009 3Q2010

28

Deposit franchise strengthened by cash management business

Source: Company reports

Note: Consolidated figures shown unless otherwise noted

C:\DPS NEW\Pres\PPT\PresPrint.pot

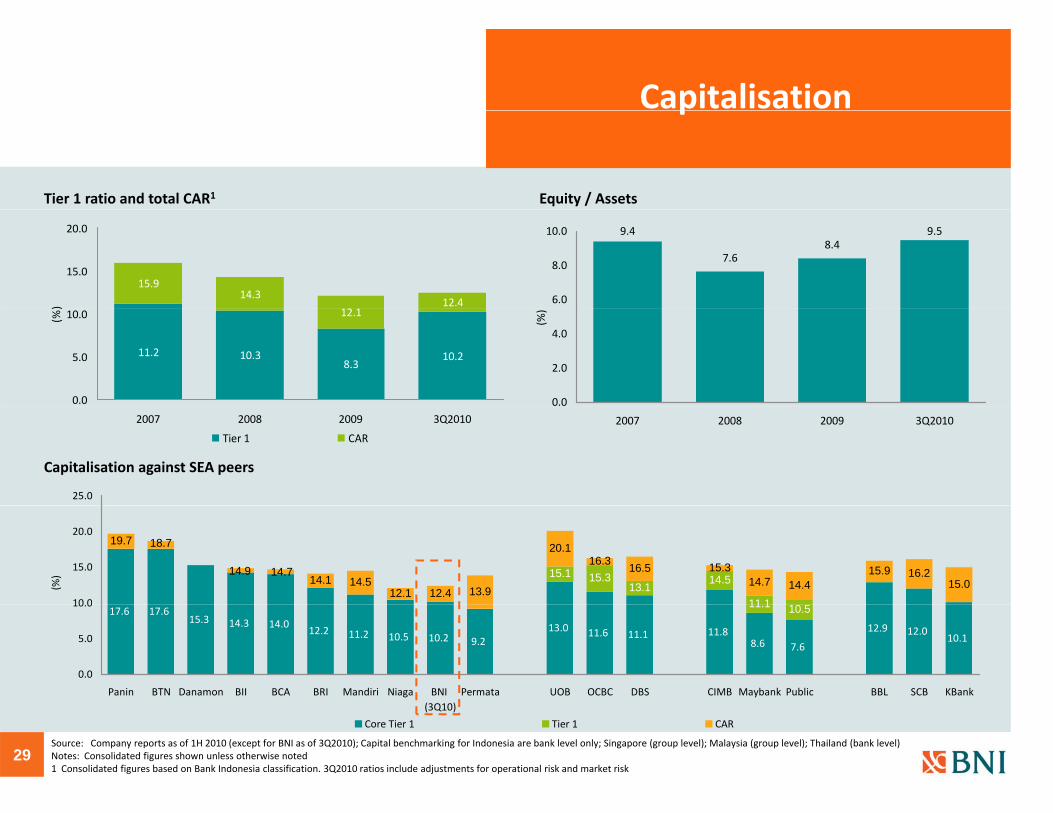

Capitalisationp

Tier 1 ratio and total CAR1 Equity / Assets

12.414.3

15.915.0

20.0

)

9.4

7.68.4

9.5

6.0

8.0

10.0

11.2 10.38.3

10.2

12.1

0.0

5.0

10.0(%)

0.0

2.0

4.0

(%)

25.0

2007 2008 2009 3Q2010

Capitalisation against SEA peers

Tier 1 CAR

2007 2008 2009 3Q2010

13.1 15.3 15.1 14.5

11 1

15.0 16.2 15.9

14.4 14.7 15.3 16.5 16.3

20.1

13.9 12.4 12.1 14.5 14.1

14.7 14.9

18.7 19.7

10 0

15.0

20.0

(%)

17.6 17.615.3 14.3 14.0

12.2 11.2 10.5 10.2 9.213.0 11.6 11.1 11.8

8.6 7.6

12.9 12.010.1

10.5 11.1

0.0

5.0

10.0

Panin BTN Danamon BII BCA BRI Mandiri Niaga BNI ( )

Permata UOB OCBC DBS CIMB Maybank Public BBL SCB KBank

29

(3Q10)

Core Tier 1 Tier 1 CAR

Source: Company reports as of 1H 2010 (except for BNI as of 3Q2010); Capital benchmarking for Indonesia are bank level only; Singapore (group level); Malaysia (group level); Thailand (bank level)Notes: Consolidated figures shown unless otherwise noted1 Consolidated figures based on Bank Indonesia classification. 3Q2010 ratios include adjustments for operational risk and market risk

C:\DPS NEW\Pres\PPT\PresPrint.pot

Strong asset quality and d t i i liprudent provision policy

Gross NPL balance Net charge‐off ratio

3.57%

4.34%

3.48%

3.00%

4.00%

5.00%7,565

5,596 5,762 5,5206,000

8,000

bn)

1.92%

0 00%

1.00%

2.00%

0

2,000

4,000

(IDR

0.00%

2007 2008 2009 3Q2010

NPL ratio2 NPL coverage ratio2

2007 2008 2009 3Q2010

140%8.53%9.00%

71.9%

101.0%

120.1% 118.3%

60%

80%

100%

120%

140%

5.00% 4.77%4.38%

6.00%

0%

20%

40%

2007 2008 2009 3Q2010

0.00%

3.00%

2007 2008 2009 3Q2010

30Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 Charge‐off ratio calculated as provision expense / average gross loans. Annualised for 3Q20102 Based on Bank Indonesia classification. BNI is in the process of transitioning to a new accounting standard PSAK 55 which would impair all loans that have been individually assessed, this would increase impaired loans from IDR 5.5tn to IDR 6.9tn as of 30 September 2010, the implied impaired loan ratio would be 5.51% and implied loan coverage ratio would be 94.0%

C:\DPS NEW\Pres\PPT\PresPrint.pot

Income statement

(IDRbn, FYE 31 December) 2007 2008 2009 3Q2009 3Q2010 YoY (%)

Net interest income 7,467 9,912 11,133 8,310 9,005 8.4%

Non interest income 4,130 3,549 4,295 3,146 3,404 8.2%

Operating income 11,597 13,461 15,428 11,456 12,409 8.3%

Operating expenses (7,626) (7,228) (7,991) (5,708) (6,391) 12.0%

Pre‐Provision Operating Profit 3 971 6 233 7 437 5 748 6 018 4 7%Pre Provision Operating Profit 3,971 6,233 7,437 5,748 6,018 4.7%

Net provisions (2,704) (4,359) (4,051) (3,483) (1,776) (49.0%)

Profit before tax 1,481 1,932 3,444 2,343 4,249 81.4%

Net Income to shareholders 898 1,222 2,484 1,855 2,954 59.3%

31Source: Company reports

Note: Consolidated figures shown unless otherwise noted

C:\DPS NEW\Pres\PPT\PresPrint.pot

Net interest income

Interest income composition Interest expense compositionInterest

3.2%2.2%

1 8%1.0%2.1% 7.7%

4.3% 3.4%5.4% 3.3% 1.6% 3.4%100%

7.4 6.7 8.3 5.4Interestexpense(IDRbn)

0.5%12 3%

0.3% 0.2%100%

14.5 16.1 18.9 14.4Interest income(IDRbn)

NIM (%) 5.4 6.5 6.1 6.1

1.8%

75%

2.6%3.3%

6.2%

5.5%6.3%

4.9%4.5%

3.0%1.9%24.6%

21.7%16.8% 12.3%

75%

91.5%87.2%

91.8% 90.1%

50%

75 6%

1.2%

2.0%12.3%

50%

25%56.8%65.6%

71.9% 75.6%

25%

Depos i ts Syariah Borrowing Marketable Securi ties

0%

2007 2008 2009 3Q2010

Loans Syariah Marketable Securi ties Placement Govt Others

0%

2007 2008 2009 3Q2010

32Source: Company reports

Note: Consolidated figures shown unless otherwise noted

p y g

C:\DPS NEW\Pres\PPT\PresPrint.pot

Non‐interest income

Non‐interest income breakdown1 Recurring fee income breakdown

21 2%13.8% 13.5% 13.3%

90%

100%

351

4,500

35.6%Non interest income ratio

26.4% 27.8% 27.4%

4,1304,295

23 1%15.5%

7.8%3.9%

5.3% 6.0%

2.2%

1.5% 1.6% 1.8%

4.7%

3.8% 5.1% 4.7%6.6%

6.0% 5.2% 4.6%21.2%

3.6%

60%

70%

80%

680 1,027

266

630

262

322

351

91184

365

3,000

3,549

3,404

17.0%

13.5%15.3% 15.8%

5.1%

8.6%

8.8%15.2%

7.9%23.1%

40%

50%

60%

1,223

424

674

764

995

1 500

(IDR bn

)

31.4%26.0% 29.9% 30.9%

10%

20%

30%

1,5971,976

2,231

1,461

1,500

Monthly account services Credit card

Investment and financial services FX trading

ATM Bill payments

0%

2007 2008 2009 1H 2010

Fee and commissions Gains on marketable securities

Insurance premium Foreign exchange gains

0

2007 2008 2009 3Q2010

33

Bank guarantee Trade finance

OthersOthers

Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 In 2008, there was a decrease in the value of marketable securities of IDR143bn

C:\DPS NEW\Pres\PPT\PresPrint.pot

Operating expensesp g p

Breakdown of operating expenses Cost income ratio

3.9% 4 9%

3.8% 3.6% 4.2% 4.3%

3.5% 4.7% 5.4% 4.4%

90%

100%

7,626Operatingexpenses(IDR bn)

7,228 7,991 6,391

80.0%

31.3%

9.1%9.8%

12.8%16.1%

4.9% 5.3% 6.7%

70%

80%

90%

65.8%

53.7%51.8% 51.5%

60.0%

31.3%31.5%

28.9%27.2%

40%

50%

60%

40.0%

48.4% 45.6% 43.3% 41.3%20%

30%

20.0%

0%

10%

2007 2008 2009 3Q2010

Personnel Expense Genera l & Adminis trative

Underwri ting Insurance Promotion Expense

0.0%

2007 2008 2009 3Q2010

34Source: Company reports

Note: Consolidated figures shown unless otherwise noted

Underwri ting Insurance Promotion Expense

Depos i t Premium Others

C:\DPS NEW\Pres\PPT\PresPrint.pot

Profitabilityy

Return on average assets1 Return on average equity1

1.74%

2.00%19.5%20.0%

1.74%

1.50%14.4%15.0%

1.16%

1.00%

7.5%

10.0%

0.51%

0.64%

0.50%

5.6%

5.0%

0.00%

2007 2008 2009 3Q2010

0.0%

2007 2008 2009 3Q2010

35Source: Company reportsNotes: Consolidated figures shown unless otherwise noted1 Return on average assets calculated as net income / average assets; Return on average equity calculated as net income to shareholders / equity attributed to bank shareholders.

Annualised for 3Q2010

C:\DPS NEW\Pres\PPT\PresPrint.pot

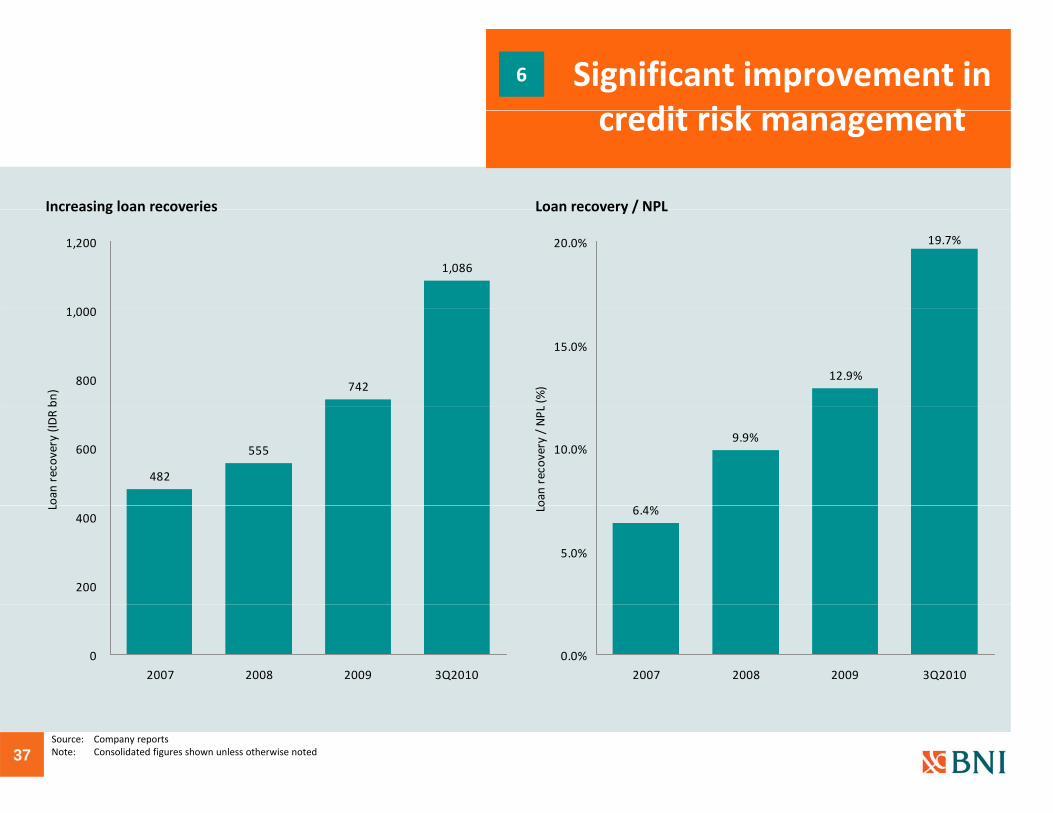

Significant improvement in dit i k t

6

credit risk management

NPL ratio1 Gross NPL1

8.53%

8.00%

10.00%

(%)

NPL ratio

7,565

5,596 5,762 5,5206,000

8,000

DR bn

)

Gross NPL

5.00% 4.77% 4.38%

0 00%

2.00%

4.00%

6.00%

NPL ratio (

0

2,000

4,000

Gross NPL (ID

0.00%

2007 2008 2009 3Q2010

Adequate provisioningGross charge‐off ratio

0

2007 2008 2009 3Q2010

140%

3.25%

4.41%

3.44% 3.56%

3.00%

4.00%

5.00%

rge‐off ratio (%

)

71.9%

101.0%

120.1% 118.3%

60%

80%

100%

120%

140%

rage

ratio (%)

0.00%

1.00%

2.00%

2007 2008 2009 3Q2010

Gross char

0%

20%

40%

60%

2007 2008 2009 3Q2010

NPL cover

36Source: Company reportsNote: Consolidated figures shown unless otherwise noted1 3Q2010 based on Bank Indonesia classification2 Gross provisions (before loan recoveries) / average gross loans. Annualised for 3Q2010

C:\DPS NEW\Pres\PPT\PresPrint.pot

Significant improvement in dit i k t

6

credit risk management

Increasing loan recoveries Loan recovery / NPL

19.7%20.0%

1,086

1 000

1,200

Increasing loan recoveries Loan recovery / NPL

12.9%

15.0%

L (%)742800

1,000

bn)

9.9%10.0%

oan recovery / NPL

482

555600

Loan

recovery (ID

R

6.4%

5.0%Lo

200

400

L

0.0%

2007 2008 2009 3Q2010

0

2007 2008 2009 3Q2010

37Source: Company reportsNote: Consolidated figures shown unless otherwise noted

ApendixApendix

Indonesia Macro Indocators

C:\DPS NEW\Pres\PPT\PresPrint.potStrongly positioned to capitalise on Indonesia’s

2p

growth

Largest Southeast Asia economy Strong private consumption

I d i

Singapore14%

Philippines12%

1,7822,000

n)

36% 57% 58% 55% 74% 50% 62% 2009 Private consumption (% of GDP)

Government consumption9%

Investment30%

Indonesia40%

Thailand20%

Malaysia14%

743

317145 119 96 74

500

1,000

1,500

Nom

inal priv

ate

consum

ption (US$b

Net exports3%

Private consumption

58%

Low banking penetration

2009 Southeast Asia GDP US$1,340bn 2009 Indonesia GDP US$551bn

218 4,683 210 249 546 56 129Credit o/s (US$bn)

74

0

China India Indonesia Thailand Philippines Malaysia Singapore

Credit o/s per capita (US$)

45,004 3,526 7,564 3,923 473 622 565

50%26%

18%24% 8%10%

14%9%

80.0%

120.0%

160.0%

dit / GDP (%

)

125% 106% 98% 96% 51% 36% 29%

Indonesia is the largest Southeast Asia economy with a growing financial sector

61%87%

48% 70%38% 19%

26%

31%3%2%8% 7%3%5%

0.0%

40.0%

Singapore China Malaysia Thailand India Philippines Indonesia

2008

Total cred

Corporate Mortgage retail Non‐mortgage retail

39Source: EIU as of September 2010; Global Insight as of September 2010; Street Research; Low banking penetration data for December 2008; Bank Indonesia

Indonesia is the largest Southeast Asia economy with a growing financial sector The banking sector remains underpenetrated with headroom for growth

C:\DPS NEW\Pres\PPT\PresPrint.pot

2Strongly positioned to capitalise on Indonesia’s p

growth

Credit growth1 Strong expected GDP growth

13.7%

7.2% 7.2%

14.1% 13.3% 12.7%

7.7%

10.4%

6 9%

9.8%7.9%

12.5%

14.2%

8 0%

12.0%

16.0%

35.5%31.0%

18 5%

30.0%

40.0%

2005

‐10E

6.8%6.9%

0.0%

4.0%

8.0%

India China Indonesia Philippines Malaysia Singapore Thailand

18.5% 17.3%15.1%

12.5% 10.6%

0.0%

10.0%

20.0%

Indonesia India China Philippines Singapore Thailand Malaysia

Loan

CAGR 2

2012E 2013E

Positive demographics

1,334.7 1,166.0 240.3 98.0 67.0 27.9 5.0 2009

Population (m)

Indonesia India China Philippines Singapore Thailand Malaysia

Large attractive market densely populated

IndonesiaPopulation: 240 millionMalaysia

56%46% 49% 42%

54%46%

64%

8% 5% 6% 5% 9% 5% 9%

40%

60%

80%

100%

SingaporePopulation: 5 million

Population: 240 millionyPopulation: 28 million

SumateraPopulation: 51 million

KalimantanPopulation: 14 million

SulawesiPopulation: 17 million

Maluku and Papua

DKI JakartaPopulation: 10 million

35%49% 46% 53%

37%49%

28%

0%

20%

China India Indonesia Philippines Thailand Malaysia Singapore

<30 31‐64 65+

Bali and Nusa TenggaraPopulation: 13 million

Java (excluding DKI Jakarta)Population: 127 million

Population: 6 million

40

Growth in Indonesia over the coming years is expected to be strong, supported by positive demographics

Source: EIU as of September 2010, Indonesia Center Bureau of Statistics (BPS)

Note:1 Loan CAGR based on private sector credit growth