investor presentation results - 1h fy21

TRANSCRIPT

1

Scott Baldwin

Managing Director

Siva Subramani

Chief Financial Officer

16 February 2021

ASX: MNY

Investor PresentationResults - 1H FY21

2

Market leading collections via our

Customer Care teams

Strong proprietary technology

allowing for seamless integration of

third party loan books

About

2

Customer focused,

Consumer & Commercial

finance company

Strong brands across

Australian and New

Zealand

Large addressable market

across Australia & New Zealand

covering new and used assets

for consumers and commercial

purposes

Group now funding over $30m

of asset purchases a month

Ubiquitous customer

journey from introducer

to loan settlement –

driven by proprietary

technology with strong

integration with

introducers software

3

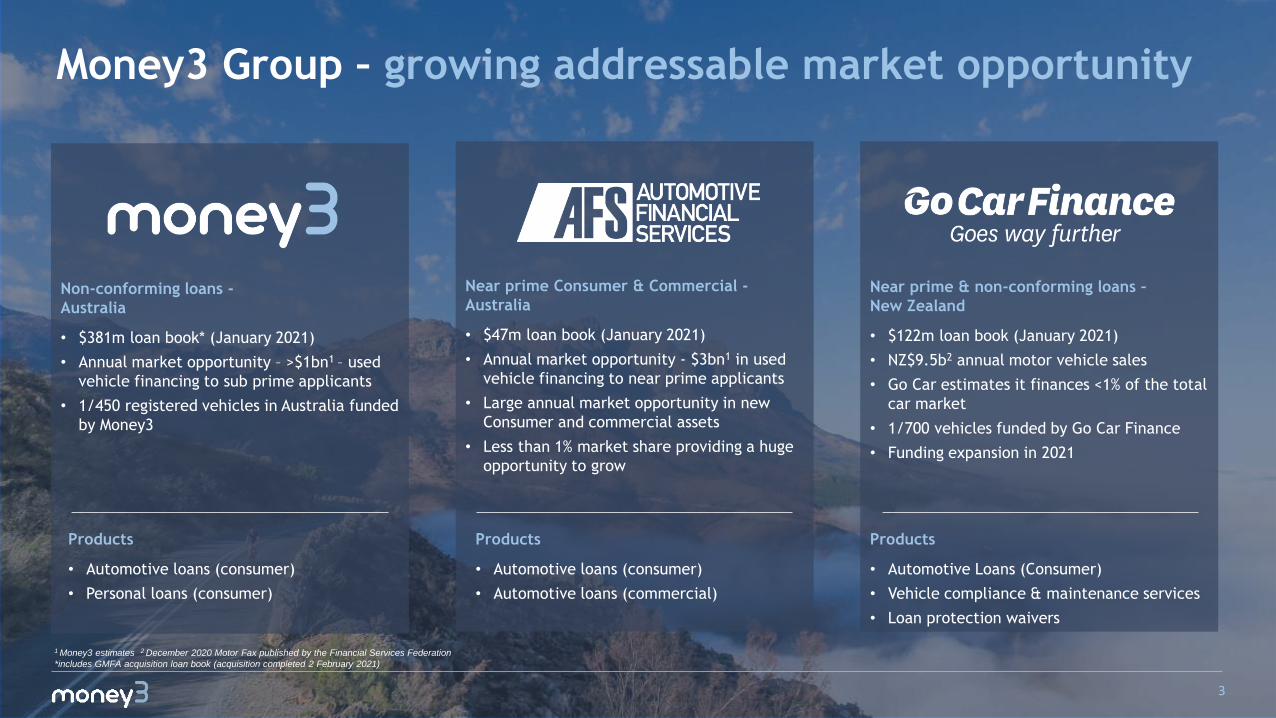

Money3 Group – growing addressable market opportunity

Near prime & non-conforming loans –

New Zealand

• $122m loan book (January 2021)

• NZ$9.5b2 annual motor vehicle sales

• Go Car estimates it finances <1% of the total

car market

• 1/700 vehicles funded by Go Car Finance

• Funding expansion in 2021

Products

• Automotive Loans (Consumer)

• Vehicle compliance & maintenance services

• Loan protection waivers

Products

• Automotive loans (consumer)

• Automotive loans (commercial)

Products

• Automotive loans (consumer)

• Personal loans (consumer)

Near prime Consumer & Commercial -

Australia

• $47m loan book (January 2021)

• Annual market opportunity - $3bn1 in used

vehicle financing to near prime applicants

• Large annual market opportunity in new

Consumer and commercial assets

• Less than 1% market share providing a huge

opportunity to grow

Non-conforming loans -

Australia

• $381m loan book* (January 2021)

• Annual market opportunity – >$1bn1 – used

vehicle financing to sub prime applicants

• 1/450 registered vehicles in Australia funded

by Money3

1 Money3 estimates 2 December 2020 Motor Fax published by the Financial Services Federation

*includes GMFA acquisition loan book (acquisition completed 2 February 2021)

4

1H FY21 Highlights

• Acquired Automotive Financial Services (AFS) broadening addressable

market and adding $46.7m (end of January 2021) to Group’s loan book;

• Acquired GMF Australia Pty Ltd (GMFA), a subsidiary of General Motors

Financial Corporation Inc, adding $23.3m to the loan book;

• Strong start to 2H FY21 with continued outperformance in

customer collections as a result of a market leading Customer Care team

that leverages strong proprietary tech;

• Oversubscribed capital raise – adding $52m equity to fund acquisitions and

loan book growth;

• Record cash collections in 1H FY21 $165m up 23.6% over pcp;

• Credit Quality of book continues to improve which will lead to an on

going reduction in impairment provisions;

• Secured $250m warehouse facility with Credit Suisse –$10m reduction in

cost of funds when fully deployed;

• Secured $55m warehouse facility with Westpac.

5

Strong loan book growth

Strong book growth via

organic growth

and acquisition at start

2H, providing a solid

foundation for underpin

FY22 results

151

214253

373

434474

550

0

100

200

300

400

500

600

FY16 FY17 FY18 FY19 FY20 Dec-20 Feb-21

Loan Book

($m)

Acquisitions drive strong start to

2H FY21

95.6%

1.8%

2.6%

Loan Book - Feb 2021Auto - Consumer Auto - Commercial Personal

6

Highlights – 1H FY21

Loan bookincreased

11.1% on pcp, 9.3%

increase since

June 30

Cash collected increased

23.6% to $165.0mon pcp

New loan

originations(cash advanced)

9.3%increase on pcpto $151.1m

EBITDAincreased

32.8% to $40.5m on pcp

Revenueincreased

8.3%to $67.9m on pcp

Good credit quality driving a reduction

in bad debts and improving impairment

provisions

Funding and strategic partnerships has

allowed New Zealand to take market

share

Strong positive cashflow impact from

government stimulus allowing customers

to pay out loans earlyNPATincreased

26.8% to $19.9m on pcp

Strong loan origination growth despite

Victorian and Auckland lockdown

7

1H FY21 Financial Results (unaudited)

Group Financial Results(Continuing operations)

Amounts in $m unless otherwise stated

1H

FY21

1H

FY20

Mvt %

Revenue 67.9 62.7 8.3%

Bad debts, net (7.6) (9.7) (21.6%)

Movement in impairment provisions (0.4) (2.8) (85.7%)

Expenses (19.4) (19.7) (1.5%)

EBITDA 40.5 30.5 32.8%

EBITDA margin 59.6% 48.6%

NPAT 19.9 15.7 26.8%

NPAT Margin 29.3% 25.1%

8.3%Increase in

Revenue

32.8%Increase in

EBITDA

26.8%Increase in

Group NPAT

Loan Book$474.0m

31 December 2020

1H FY21 Financial Results

8

Increasing trend in Amount Financed Australia$101.4m cash advanced in

1H FY21

Increase in Group’s

cash advanced on pcp

9.3%$22.5

$24.6$22.9

$10.0

$17.4

$23.2

$26.6

$21.0

$25.2$26.7

$32.6 $31.7

-

500

1,000

1,500

2,000

2,500

$0

$5

$10

$15

$20

$25

$30

$35

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20

Amount Financed - Group

Amount Financed Loan Count

$m Count

Lock downNew Zealand$49.7m cash advanced in

1H FY21Lock down

9

Improving credit quality

Improving credit

quality driving down

impairment provision

requirements and

improving EBITDA

Positive impact on “Strong”

credit quality customers as a

result of Customer Care

initiative and Government

stimulus

49.1%

47.7%

46.2%

53.8%

23.5%

26.0%

31.8%

26.7%

23.4%

22.6%

18.5%

17.2%

1.8%

2.3%

2.6%

2.1%

2.2%

1.4%

0.9%

0.1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

FY18

FY19

FY20

1H FY21

Strong Good Watch List Sub-standatd Credit impaired

Credit quality should

continue to improve with

recent acquisitions

10

Funding – very solid foundation

• $250m warehouse facility with Credit Suisse – providing for a $10.0 million interest expense saving when fully deployed,

• $150m funding facility with FCCD (Fortress Australia) – scheduled to be repaid at the end of FY21,

• $55m warehouse facility with Westpac – supporting the growth of Automotive Financial Services

• $8.5m funding facility with Australian Office of Financial Management

• Over subscribed $52m equity raise to fund further loan book growth and acquisitions

• $70m cash on hand at the end of January 2021

• In advanced negotiation with a New Zealand bank for a $40m debt facilityto support the growth of Go Car Finance

11

AFS acquisition

1 https://afico.com.au/2 AFICO - AFS secures S&P Global Ratings 3 AFICO - Westpac increases senior debt (source: https://afico.com.au/)

Strategic

fit

Acceleration

into near prime

automotive segment

Servicing several

hundred Dealer

Groups1

Strong loan

book quality2

Earnings

accretive

Funding

diversification

from large

Australian bank3

Successful business

model and

experienced

management team

Lot of similarities

with the Go Car

acquisition in

2019

Acquisition completed on 4 January 2021

FY22 Revenue(forecast)

~$14m

FY22 NPAT(forecast)

~$~2.5m

Strong loan book quality

30+ days arrears less

than 1% of book

Purchase consideration

$10.8m

12

1HFY21 - New Zealand Growing from strength to strength

Cash

collections

up 44.2% to

$27.7 on pcp

Loan Book$115.0m

up 39.0% on

June 2020

• Go Car finance acquisition completed in March 2019

• Strong strategic fit with group

• Growing contributions to loan book growth (Loan book doubling

since acquisition) and profitability

• 20.6% contribution to group revenue and growing

• 1/700 registered vehicles in New Zealand financed with

significant opportunity to grow market share

• Margins expected to improve with loan book growth

• Has maintained Group growth during Victorian lockdown period

• Good blueprint for Automotive Financial Services acquisition

Cash

advanced

up 70.1% to

$49.7m on pcp

13

Group - Gross loan book growth

Expanding addressable market & market

share is driving strong growth

momentum, group now advancing over

$1.5m per day in new loan origination

341 391

195

400536

791

0

200

400

600

800

1000

Oct-20 Post cap raise & new debt facilities*

Capital Structure – loan book capacity

Equity^ Debt

(AUDm)

*Includes $40m debt facility offer from a NZ Bank^Includes deferred revenue impairment provision on loan book

Existing debt facilities support loan

book growth to ~$800m#

Return on Equity (RoE) to grow

towards 20% with increasing leverage

as new debt facilities are utilised

253373

434

600

0

200

400

600

800

1,000

FY18 FY19 FY20 FY21 .. 2024

Gross Loan Book(AUDm)

Forecast

$1bn

Aspiration

#assumes fortress is repaid at the end of FY21

14

Forecast NPAT $36m

• FY21 forecast takes into consideration the continuing uncertainty around COVID-19 with the following assumptions;

• No prolonged lockdowns occurring in the reminder of the financial year;

• Stability in unemployment rates;

• Announced Government stimulus packages remaining in place until March 2021; and

• Anticipate paying 9 cents in dividends for FY21.

Target Loan book ~$600m by end of FY21

• Strong loan book growth and significant improvement in the cost of debt will provide the foundation a significant uplift in NPAT and ROE

Continue to pursue strategic acquisitions to add scale in terms of product or distribution channels

FY21 - Outlook

15

Appendix 1 – Corporate Information

CAPITAL STRUCTURE

ASX 300 Company

Shares on issue 207.6 million

Share Price (15th February 2021) $2.87

Market capitalisation $595.8 million

Earnings per share (1H FY21) – Basic 10.64 cents

Dividends per share (interim) 3.00 cents

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Share Price – 12-months

16

114.3

137.3

0

30

60

90

120

150

1H FY20 1H FY21

Australia – Cash Collections$m

19.2

27.7

0

6

12

18

24

30

1H FY20 1H FY21

New Zealand – Cash Collections$m

Appendix 2 – Cash collections

17

The content of this presentation has been prepared by Money3

Corporation Limited (the Company) for general information

purposes only.

Any information included in this presentation on COVID-19’s impact

on future financial performance, including industry sectors, income,

profit and employment types, represent estimates of

management. However due to the unprecedented nature of the

events, these views are inherently uncertain and Money3 takes no

responsibility for the accuracy of such views.

Any recommendations given are general and do not take into

account your personal circumstances and therefore are not to be

taken as a recommendation or advice to you.

You should decide whether to contact your financial adviser so a

full and complete analysis can be made in respect to your personal

situation.

Whilst all care has been taken compiling this presentation neither

the Company nor any of its related parties, employees or directors

give any warranty with respect to the information provided or

accept any liability to any person who relies on it.

Disclaimer

18

Managing Director

Scott Baldwin

Telephone: +61 3 9093 8255

Email: [email protected]

Chief Financial Officer

Siva Subramani

Telephone: +61 3 9093 8246

Email: [email protected]

Investor Relations

Simon Hinsley

Telephone: +61 401 809 653

Email: [email protected]