investor presentation september 2012 - … · number of business correspondents (bcs) ... mutual...

TRANSCRIPT

Investor Presentation

SEPTEMBER 2012

South Indian Bank… At A Glance

2

• Number of years in banking business83 Years

• Number of branches730

• Number of ATM’s743

• Business as on Sept 2012` 67110Cr

• Business Growth (Y – to – Y)19%

• Last 5 years business CAGR26%

• Net Profit for the Half Year ending Sept 2012` 220.18Cr

• Net Interest Margin (Sept 12)3.09 %

• Capital Adequacy Ratio (Basel II –Sept 12)14.43%

• Net Non-Performing Assets (Sept 12)0.86%

3

History & Background

Future Strategy

Overview

Key Strength

Business Performance

CONTENTS

4

HISTORY &

BACKGROUND

First private sector bank to open a NRI branch in Nov,1992

& an IFB branch in March 1993.

One of the oldest Banks in South India.

First among private sector Banks in Kerala to become aSCB in 1946.

Listed in NSE, BSE & CSE- IPO in 1998. FPO In 2006.

Successful QIP in Sept 2007 & 2012

Incorporated on January 25, 1929. Head Office:

Thrissur, Kerala.

The THIRD largest branch network among Private Sector

banks, in India, with all its branches under Core banking

System.

First bank among the Private sector banks in Kerala to

open an "Overseas Branch”, June ’93.

History & Pioneering Initiatives

5

6

Shareholding Pattern – as on Sept-2012

Diversified shareholding & tradition of good corporate governance practices

7

32.46%

7.20%

11.19%

45.27%

3.89%

Individuals

Corporates

FI's and Banks

FII's

Others

Vision & Mission

8

CORPORATE VISION

MISSION

To emerge as the most preferred bank in the country in terms ofbrand, values, principles with core competence in fostering customeraspirations, to build high quality assets leveraging on the strong and vibranttechnology platform in pursuit of excellence and customer delight and tobecome a major contributor to the stable economic growth of the nation.

To provide a secure, agile, dynamic and conducive banking environment tocustomers with commitment to values and unshaken confidence, deploying thebest technology, standards, processes and procedures where customerconvenience is of significant importance and to increase the stakeholders’value.

9

OVERVIEW

Healthy Fundamentals

Adequately Capitalised;

•14.43% CRAR & 12.32% Tier 1 ratio

Asset Quality;

•1.74% GNPAs & 0.86% NNPAs

•51.21% NPA Coverage ratio

•15.52% ROE, 1.06% ROAA

Strong Growth

• One of the fastest growing banks in

India.

• 26% CAGR in business in last 5 years

•Constant growth in Business &

Profitability

Most advanced technology in all

spheres of banking operations &

delivery channels.

Key Competitive Advantage

• Fast expanding branch network

• High Asset Quality with well diversified

Loan portfolio

• 8.87 % market share in Kerala’s NRI

deposit base.

•Strong boost to Income from high

yielding gold loans forming 22.11% of the

loan book.

Significant Turnaround

•Benchmarked HR Practices & Introduced

Performance Linked Incentive

schemes, ESOS, Annual Performance

contest- Awards.

•Forward looking Human Capital

Management Strategy

•Highly skilled human capital- 50% of

human capital under age 30 with

professional qualification

SIB SIB

SIBSIB

Key Strengh

10

Spread of Branches

11

Average Branch & ATM network

growth @ 20% (for last & current FY)

Vast and Rapidly Growing Branch Network

12

17%

48%

20%

15%

Rural

Semi- Urban

Urban

Metro

Branch Network Category wise as on Sept 2012

13

STATESNo: of

BranchesSTATES

No: of Branches

STATESNo: of

Branches

Kerala 401 Chhattisgarh 3 Himachal Pradesh 1

Tamil Nadu 130 Orissa 2 Meghalaya 1

Karnataka 40 Madhya Pradesh 2 Nagaland 1

Andhra Pradesh 46 Rajasthan 2

Maharashtra 25 Pondicherry 2

Delhi 24 Assam 2

West Bengal 10 Jharkhand 2

Uttar Pradesh 9 Bihar 1

Gujarat 9 Uttaranchal 1

Punjab 4 Chandigarh 1

Haryana 4 Jammu & Kashmir 1

Goa 5 Tripura 1 Total 730

State wise distribution of Branches Category wise as on Sept 2012

14

Num

ber

of

Bra

nches a

dded

Network Expansion (Number of branches added)

0

10

20

30

40

50

60

70

FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13(proposed)

25 25

30

50

61 59

50

15

Nu

mb

er

of

Bra

nch

es

Branch Network

475500 530

580

641

700750

0

100

200

300

400

500

600

700

800

FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 (proposed)

16

Nu

mb

er

of

AT

Ms a

dd

ed

Network Expansion (Number of ATMs added)

0

20

40

60

80

100

120

140

160

180

FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 (proposed)

50 55

93

116

174

137

17

Nu

mb

er

of

AT

Ms

ATM Network

225280

373

489

663

800

0

100

200

300

400

500

600

700

800

900

FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 (proposed)

Project SIBERTECH- 100% Core Banking Solution (CBS) using FINACLE from Infosys.

Centralized Data Centre with most advanced technological platform in a new state of the art “Green” complied building at Kochi, Kerala.

Emphasis on IT security & Risk Management - Disaster-recovery site at Bangalore for CBS & Regular IS Audits.

Member of INFINET & 743 On-line ATMs through NFS tie-up with other banks

A host of hi-tech products- International debit & credit cards, high speed & secure Internet & Mobile Banking for retail & corporate clients.

Online Value added services - Stock trading, ticket booking, mobile recharges, shopping, Utility payments, offerings.

SIB FINS Card -A smartcard based FI initiative in association with M/s Coromandel InfoTech India Ltd., Chennai, as the technology service provider.

Successfully implemented RTGS & NEFT in all branches.

Successfully launched Smart card at Christ University, Bangalore which works as Access card, Identity card, ATM card and card for payment of fees in Christ College for around 10000 students.

Best-in-class IT products & solutions in all banking operations like Treasury, Risk Management, AML, Credit Processing, HR, Audit & KYC.

18

EFFICIENT SERVICE LEVERAGING ON TECHNOLOGY

RANGE OF PRODUCTS

19

Loan Products Deposit products Other Products

Retail Business Loans

Housing Loans/

Mortgages

Auto Loans

Personal Loans

Education Loans

Employee Group Loans

SME Loans

•Savings Bank Accounts

•Current Accounts

•Fixed/ Recurring

Deposits

• Depository Account

• Mutual Funds sales

• Life Insurance sales

• General Insurance sales

• Group Insurance sales

• E-payment

• Cash Management Services

• Online Foreign Inward Remittance

• m-Commerce

• New Pension Scheme

•Gold Coins/ingots

Commercial Banking

•Working Capital Loans

•Term Loans

•Letters of Credit

•Banks Guarantees

• Bill Finance

•Wholesale Deposits

Retail Banking

Wholesale Banking

20

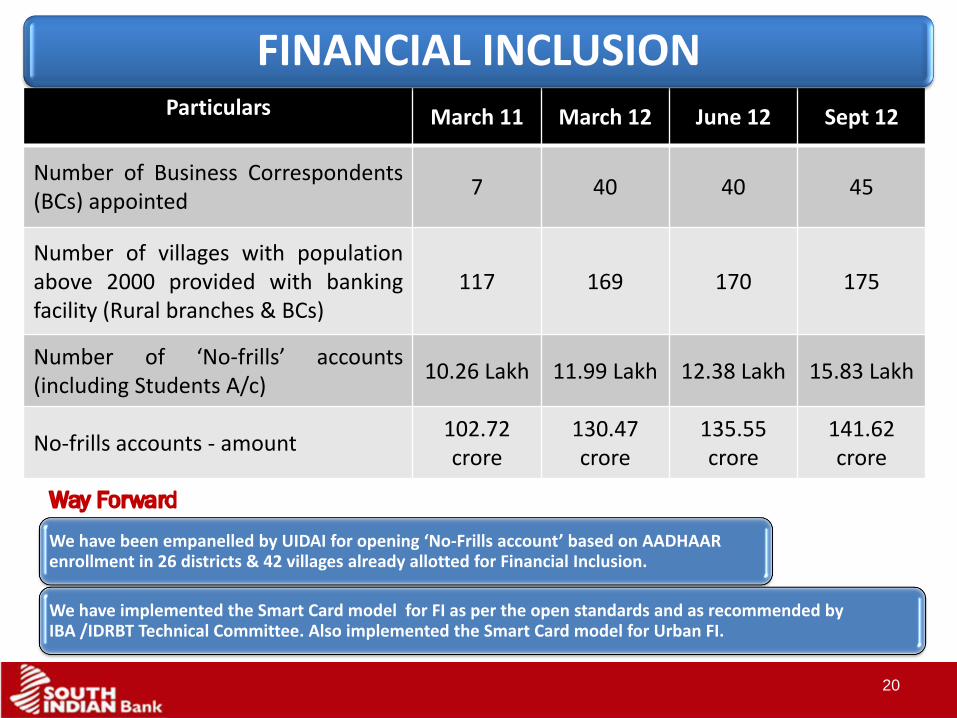

Particulars March 11 March 12 June 12 Sept 12

Number of Business Correspondents(BCs) appointed

7 40 40 45

Number of villages with populationabove 2000 provided with bankingfacility (Rural branches & BCs)

117 169 170 175

Number of ‘No-frills’ accounts(including Students A/c)

10.26 Lakh 11.99 Lakh 12.38 Lakh 15.83 Lakh

No-frills accounts - amount102.72 crore

130.47 crore

135.55 crore

141.62crore

We have been empanelled by UIDAI for opening ‘No-Frills account’ based on AADHAAR enrollment in 26 districts & 42 villages already allotted for Financial Inclusion.

We have implemented the Smart Card model for FI as per the open standards and as recommended by IBA /IDRBT Technical Committee. Also implemented the Smart Card model for Urban FI.

FINANCIAL INCLUSION

Life Insurance with LIC

General Insurance with Bajaj Allianz

Mutual funds –All the leading AMCs in India

Sri Lanka's Hatton National Bank (HNB)

• Improve the remittance flow to India and Sri Lanka

More than 30 exchange houses & banks in middle east

• Facilitating fast remittances for more than 2lakh NRI customers, mostly from Gulf countries

Providing managerial support to overseas exchange house - HADI exchange house

21

Strategic Tie Ups

RECOGNITIONS

Best Bank in Asset Quality (Pvt Sect or Bank) Award - Dun & Bradstreet 2011

Best Bank in Priority Sector Lending (Pvt Sect or Bank) Award - Dun & Bradstreet 2011

Technology Excellence Award 2011-12 from IDRBT

Technology Excellence Award in 2010 from IRDBT

India’s Best Bank 2010 Award – “Business world – Price Water House CoopersBest Banks Survey 2010”

Best Asian Banking Website - Asian Banking & Finance Magazine, Singapore.

Best Old Pvt Sector Bank - Financial Express India's Best Banks 2008-2009.

Best Pvt Sector bank in the Service quality segment Outlook Money - CFore Survey.

Best Website Award from Kerala Management Association

22

23

BUSINESS

PERFORMANCE

Business Performance

24

Net Profit

220.18

177.44

Business

67110

56386

Advance

28620

23348

Deposit

38490

33038

Net NPA

0.86%

0.25%

Gross NPA

1.74%

0.99%

(` in Crores)

Financial Highlights – As on Sept 2012

Sept 2012

Sept 2011

24% 19% 23% 17%

Profitability (Half Year)

25

Net Profit 24%

135177

220229

309

407

0

100

200

300

400

500

SEPT-2010 SEPT-2011 SEPT-2012

Net Profit Operating Profit

(` in Crores)

ROA coming mainly from Core Income

26

*Annualized

Improved Quality of Earnings

0.92

0.98 0.97

1.02

1.071.05 1.05 1.06

0.80

0.85

0.90

0.95

1.00

1.05

1.10

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

ROA*

ROAA*

27

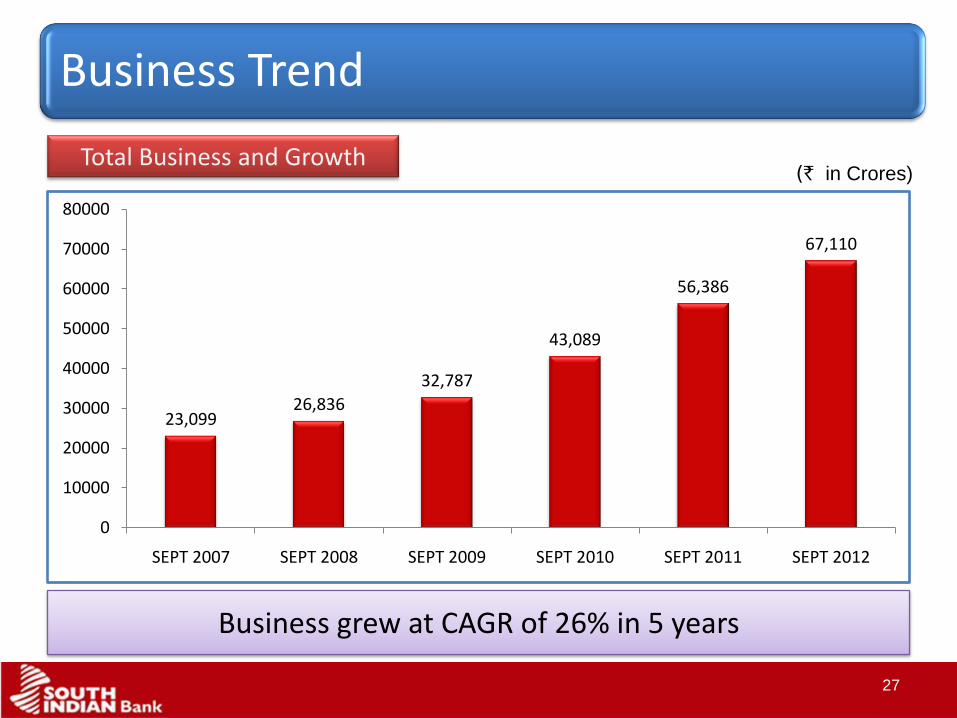

Total Business and Growth

Business grew at CAGR of 26% in 5 years

(` in Crores)

23,09926,836

32,787

43,089

56,386

67,110

0

10000

20000

30000

40000

50000

60000

70000

80000

SEPT 2007 SEPT 2008 SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

Business Trend

28

Credit Deposit Ratio

69.21%

71.94%

70.67%

74.36%

66.00%

67.00%

68.00%

69.00%

70.00%

71.00%

72.00%

73.00%

74.00%

75.00%

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

29

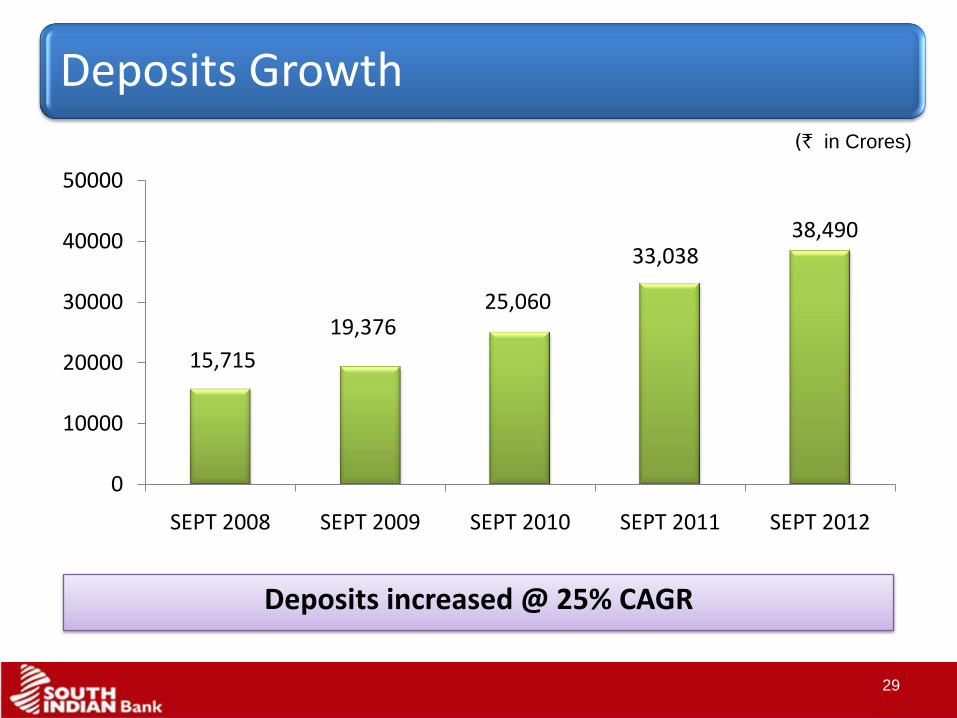

Deposits increased @ 25% CAGR

(` in Crores)

Deposits Growth

15,715

19,37625,060

33,03838,490

0

10000

20000

30000

40000

50000

SEPT 2008 SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

30

Low Cost deposits form 19.96% of total deposits.

Annual Trend in Low cost depositsComposition of Deposits

(` in Crores)(` in Crores)

Deposits – Composition and Trend

SB Deposit

632116% CD

Deposit13624%

Term Deposit3080780%

3791

4888

57646321

8451091 1274 1362

0

1000

2000

3000

4000

5000

6000

7000

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

SB Deposit CD Deposit

Advances increased by 27% (CAGR)

31

(` in Crores)

Advances Growth

11121

13411

18029

23348

28620

0

5000

10000

15000

20000

25000

30000

35000

SEPT 2008 SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

Adavance

32

Advances – Composition (Sept 2012)

Sector Upto 5 Crores Above 5 Crores Total % to total

Agriculture 1165.48 415.98 1581.46 5.54%

MSME 2032.56 353.39 2385.94 8.34%

Large Scale Industries 407.66 4978.13 5385.79 18.82%

Housing 1137.83 429.25 1567.08 5.48%

Commercial Real Estate 40.40 72.55 112.95 0.39%

NBFC 60.87 1986.75 2047.62 7.15%

Food Credit 0.00 524.49 524.49 1.83%

Infrastructure 0.00 4808.18 4808.18 16.80%

Gold Loan (Non Priority) 5354.44 0.00 5354.44 18.71%

FSLD 832.75 0.00 832.75 2.91%

LC Bills 0.00 2650.07 2650.07 9.26%

Miscellaneous 1246.24 123.17 1369.42 4.78%

Total 12278.23 16341.96 28620.19 100%

33

Trend in Cost of Deposits Trend in Yield on Advances

Trend in Cost & Yield (Annualized)

7.20%6.34%

7.66%

8.30%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

Cost of Deposit

11.68%

10.61%

12.11% 12.76%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

34

Trend in Cost of Deposits(cumulative)

Trend in Yield on Advances(cumulative)

Trend in Cost & Yield (Quarterly)

7.60%7.66% 7.77% 7.94%

8.41%

8.30%

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12

11.75%

12.11%12.30%

12.50%

13.01%

12.76%

11.00%

11.20%

11.40%

11.60%

11.80%

12.00%

12.20%

12.40%

12.60%

12.80%

13.00%

13.20%

Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12

35

SLR & Non SLR Securities Composition of Investment Bookas on 30- Sept 2012

` in Crores

Category Amount Percentage

Held to Maturity 8913.83 90.76%

Held for Trading 9.61 0.10%

Available for Sale 897.45 9.14%

Total 9820.89 100%

Investment Portfolio

39474593

6146

7621

8699

7591045

381

9531122

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

SEPT 2008 SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

SLR Securities Non-SLR Securities

(` in Crores)

36

Sep-11 Dec-11 Mar-12 Jun-12 Sep-12

Total

Investment

Portfolio

3.69 4.07 4.08 4.08 4.43

Total HM

Investment

Portfolio

4.61 4.55 4.51 4.57 4.68

Total HFT

and AFS

together

Investment

Portfolio

0.39 0.64 0.90 1.39 1.67

Duration of Investments

5.95%6.29%

6.73%7.27%

3.20%

4.00%

4.80%

5.60%

6.40%

7.20%

8.00%

8.80%

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

Investment Portfolio

Yield on Investments

(In Years)

37

The bank has CRAR in excess of the required minimum of 9% stipulated by RBI.

CRAR – Basel 2

Adequately Capitalized

17.55

15.86

13.4814.43

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

Yearly

38

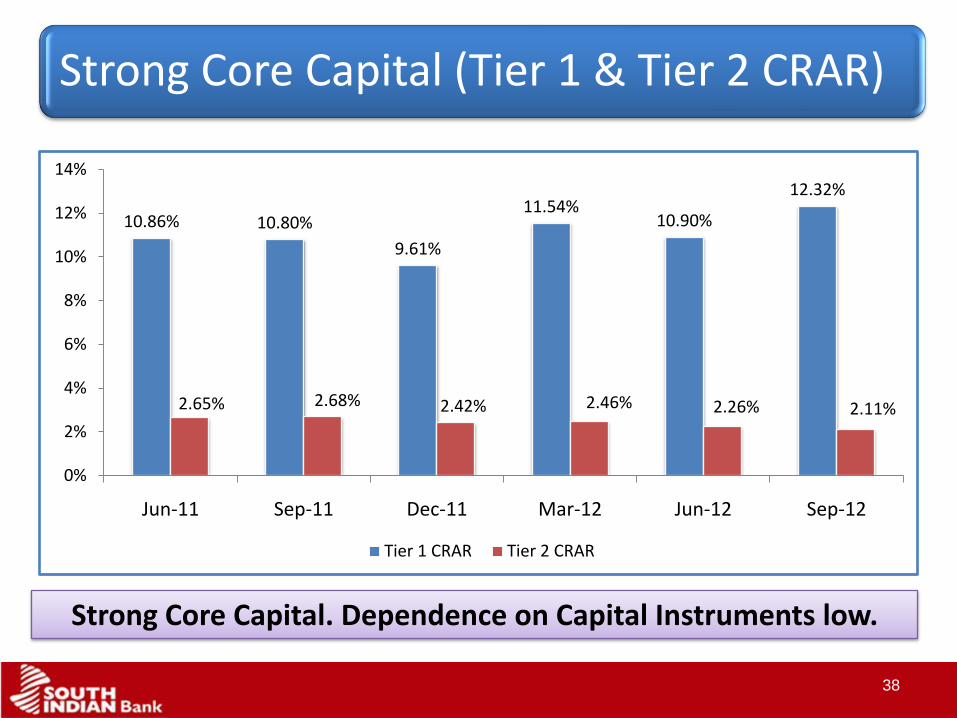

Strong Core Capital. Dependence on Capital Instruments low.

Strong Core Capital (Tier 1 & Tier 2 CRAR)

10.86% 10.80%

9.61%

11.54%10.90%

12.32%

2.65% 2.68% 2.42% 2.46% 2.26% 2.11%

0%

2%

4%

6%

8%

10%

12%

14%

Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12

Tier 1 CRAR Tier 2 CRAR

39

RWA Tier 1 Capital Tier 2 Capital Total Capital

Jun 10 11270 1476 326 1802

Sep 10 11861 1551 330 1881

Dec 10 13174 1622 340 1962

Mar 11 14647 1650 401 2051

Jun 11 15152 1645 401 2046

Sep 11 15173 1643 408 2051

Dec 11 17069 1640 414 2054

Mar 12 16987 1960 417 2377

June 12 17955 1957 406 2363

Sep 12 19423 2393 410 2803

(` in crores)

Strong Core Capital (Trend)

40

Gross Annual income grew in 5 years at CAGR 28.25%

Total Income Trend in Expenses

Trend in Income & Expenses

(` in crores)

549684

815

977

1437

1882

0

200

400

600

800

1000

1200

1400

1600

1800

2000

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

Int Exp Staff Exp Other Exp

668846

10561206

1751

2289

0

500

1000

1500

2000

2500

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

Int on Adv Int on Inv Oth Int Non-Int Income

41

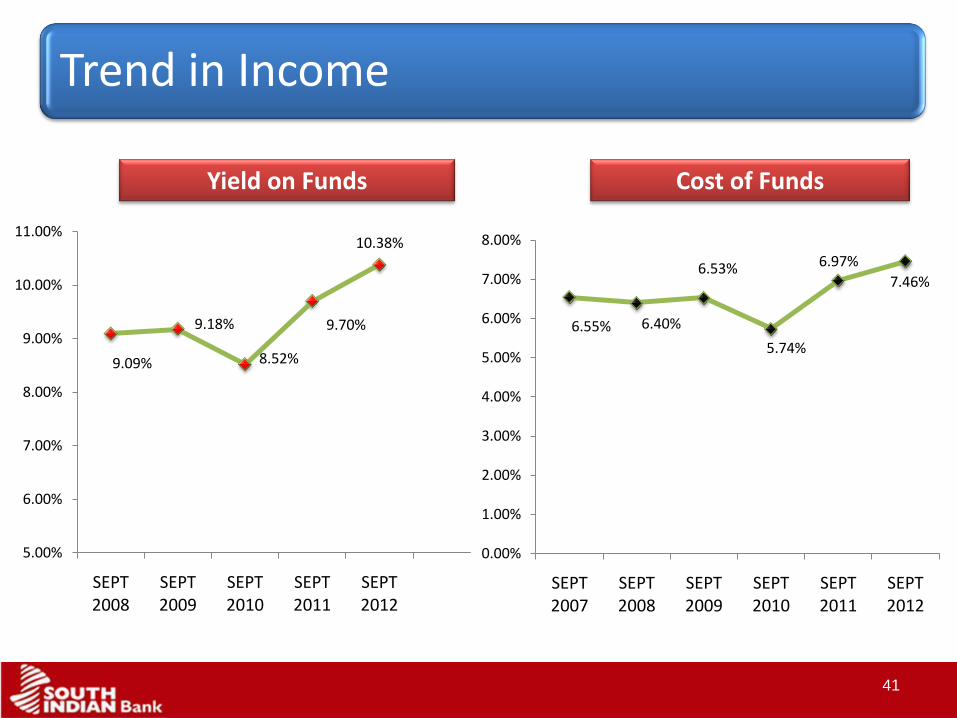

Yield on Funds Cost of Funds

Trend in Income

9.09%

9.18%

8.52%

9.70%

10.38%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

6.55% 6.40%

6.53%

5.74%

6.97%

7.46%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

42

Particulars Half year ended Sept

2011

Half year ended Sept

2012

Commission, Exchange & Brokerage 15.94 21.11

Profit on sale of investment (Net) 26.24 30.80

Profit on sale of Land, Building & Other assets (Net) 0.02 -0.06

Profit on Exchange Transactions (Net) 11.72 11.62

Miscellaneous Income

1. Processing Fees 6.84 8.25

2. Technology Related 17.96 23.79

3. Bullion 0.58 2.27

4. Transaction Related 23.14 33.32

5. Interest on IT refund - 15.14

6. Others 2.26 1.57

Total 104.70 147.81

(` in crores)

Composition of Other Income

43

Net profit grew at CAGR of 25% (Y-Y) in last 5 years.Net Interest margin (NIM) remains at moderate range.

Growth in Net Profit

Profitability

Net Interest Margin

(` in Crores)

2.64%

3.00% 3.00%

3.09%

2.40%

2.50%

2.60%

2.70%

2.80%

2.90%

3.00%

3.10%

3.20%

SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

90101

135

177

220

0

50

100

150

200

250

SEPT 2008 SEPT 2009 SEPT 2010 SEPT 2011 SEPT 2012

44

Return on Average Asset

Efficiency

Return on Equity Return on Asset

44

11.85%

14.43% 14.49%

16.67%17.53%

15.52%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

0.94%

1.06%

1.00%

1.03%

1.05%1.06%

0.88%

0.90%

0.92%

0.94%

0.96%

0.98%

1.00%

1.02%

1.04%

1.06%

1.08%

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

45

Efficiency

Cost / Income Ratio Earning Per Share (Annualized)

45

1.46

2.001.80

2.39

3.13

3.80

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

52.57%

44.92%

50.72%

49.20%

45.56% 45.16%

40%

42%

44%

46%

48%

50%

52%

54%

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

46

(` in Lakh)

Profit Per Employee

(` in Lakh)

Productivity

Average Business Per Employee Profit Per Employee

46

534 574636

773

9431038

0

200

400

600

800

1,000

1,200

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

3.394.05 4.23

5.26

6.43

7.22

0

1

2

3

4

5

6

7

8

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

47

Productivity

Average Business Per Branch Operating Profit Per Branch

47

43.2449.60

55.63

65.58

81.2586.96

0

10

20

30

40

50

60

70

80

90

100

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

49.20

62.9269.94

75.44

96.60

111.85

0

20

40

60

80

100

120

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

(` in Lakh)(` in crore)

48

Asset Quality as on September 2012

Gross NPA & Net NPA(%) Provision Coverage

48

3.41%

1.86%1.61%

1.27%0.99%

1.74%

0.71%

0.40% 0.43% 0.38% 0.25%

0.86%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

Gross NPA Net NPA

75.03%70.55%

58.38%

71.20%74.70%

51.21%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

SEPT 2007

SEPT 2008

SEPT 2009

SEPT 2010

SEPT 2011

SEPT 2012

49

(` in Crore)

Break-up of Provision

49

Particulars Year ended

31/03/2011

Year ended

31/03/2012

Half Year

ended

30/09/2011

Half Year

ended

30/09/202

For NPA advance 27.74 21.04 2.54 63.86

For Depreciation on

Investments9.37 14.07 14.86 0

For NPA investment 0.26 -0.69 0 0

For standard assets 21.60 39.75 21.17 7.28

For income tax 152.94 170.69 87.37 105.41

For Restructured advances -0.05 4.01 4.94 10.54

General Provision 20 0 0 0

Other impaired assets 0.84 2.79 1.16 -0.33

Others (ADWDRS) 0 -1.80 0 0

Total Provisions and

Contingencies 232.70 249.86 132.04 186.76

50

Performance Highlights Jun-11 Sep-11 Dec-11Year ended

Mar-12June-12 Sep-12

CRAR Basel 2 (%) 13.51% 13.48% 12.03% 14.00% 13.16% 14.43%

Return on Average

Assets (Annualised) 1.02% 1.05% 1.06% 1.12% 1.22% 1.06%

NIM (%) 2.80% 3.00% 3.05% 3.10% 3.15% 3.09%

Gross NPA's 236 230 234 267 295 496

Net NPA 63 58 58 76 95 242

Gross NPA (%) 1.07% 0.99% 0.94% 0.97% 1.08% 1.74%

Net NPA (%) 0.29% 0.25% 0.24% 0.28% 0.35% 0.86%

Provision Coverage 73.15% 74.70% 75.18% 71.36% 67.71% 51.21%

CASA 6790 7038 7280 7179 7835 7684

CASA % 21.47% 21.30% 21.51% 19.67% 21.09% 19.96%

Deposits 31622 33038 33834 36501 37153 38490

Advances 22151 23348 25050 27635 27349 28620

Yield on advances 11.75% 12.11% 12.30% 12.50% 13.01% 12.76%

(` in Crore)

Performance Highlights

50

51

FUTURE STRATEGY

Key Focus

Aims to increase total business mix to ` 1.25 lakh Crore by March 2015.

Enhancing income from Technology products, Treasury, Forex and gold coins

Ramping up low cost as well as retail liabilities.

Enhancing productivity per branch/per employee

52

IMPORTANT NOTICE

53

No representation or warranty, express or implied is made as to, and no reliance should be placed on, thefairness, accuracy, completeness or correctness of such information or opinions contained herein. The informationcontained in this presentation is only current as of its date. Certain statements made in this presentation may not bebased on historical information or facts and may be “forward looking statements”, including those relating to theCompany’s general business plans and strategy, its future financial condition and growth prospects, and futuredevelopments in its industry and its competitive and regulatory environment. Actual results may differ materiallyfrom these forward-looking statements due to a number of factors, including future changes or developments in theCompany’s business, its competitive environment and political, economic, legal and social conditions in India. Thiscommunication is for general information purpose only, without regard to specific objectives, financial situations andneeds of any particular person. This presentation does not constitute an offer or invitation to purchase or subscribefor any shares in the Company and neither any part of it shall form the basis of or be relied upon in connection withany contract or commitment Important Notice whatsoever. The Company may alter, modify or otherwise change inany manner the content of this presentation, without obligation to notify any person of such revision or changes. Thispresentation can not be copied and/or disseminated in any manner.

53

54